Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

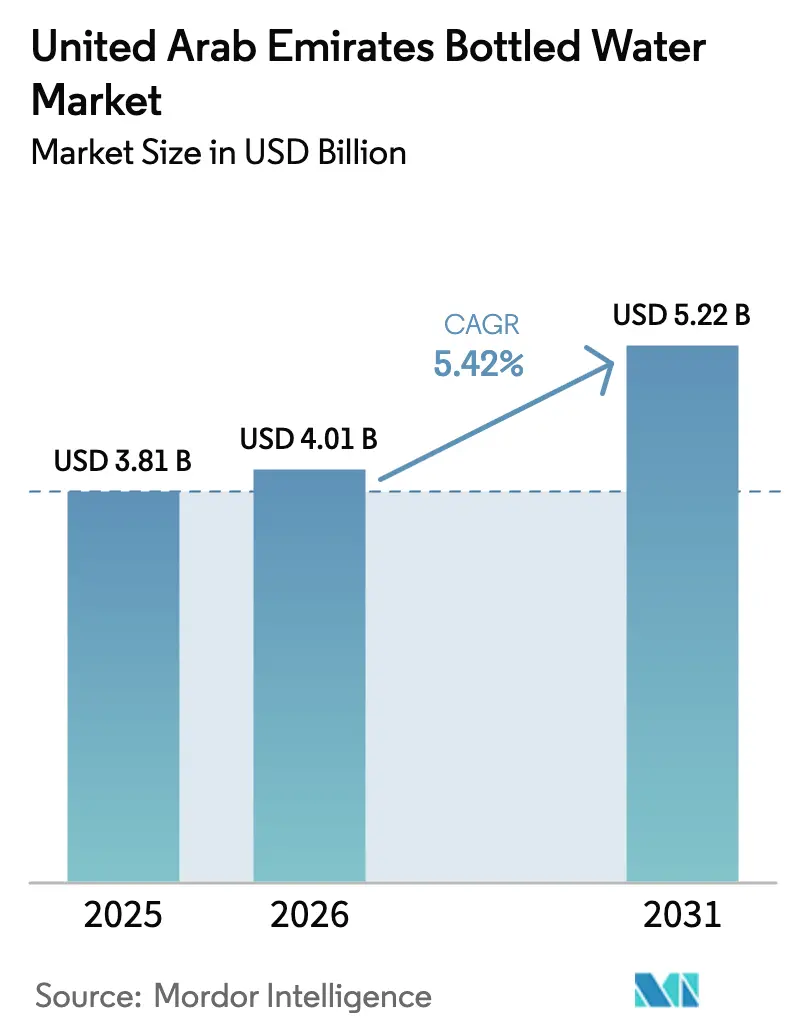

| Base Year Market Size (2025) | USD 3.81 Billion |

| Market Size (2026) | USD 4.01 Billion |

| Market Size (2031) | USD 5.22 Billion |

| Growth Rate (2026 - 2031) | 5.42% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Arab Emirates Bottled Water Market Analysis by Mordor Intelligence

The United Arab Emirates bottled water market was valued at USD 3.81 billion in 2025 and estimated to grow from USD 4.01 billion in 2026 to reach USD 5.22 billion by 2031, at a CAGR of 5.42% during the forecast period (2026-2031). The market’s momentum is largely driven by the country’s status as the world’s highest per capita consumer of bottled water. This trend is shaped by the country’s harsh climate, its sizeable expatriate population, and the steady influx of tourists. As one of the Middle East’s top travel destinations, the United Arab Emirates continues to see rising demand for bottled water, with many consumers opting for it over tap water due to greater confidence in its quality and safety. Additionally, the market is witnessing increasing interest in functional, fortified, and flavored water options, highlighting a shift toward more specialized hydration choices. Together, these dynamics reinforce the market’s long-term growth outlook and signal strong potential for continued product innovation and expansion.

Key Report Takeaways

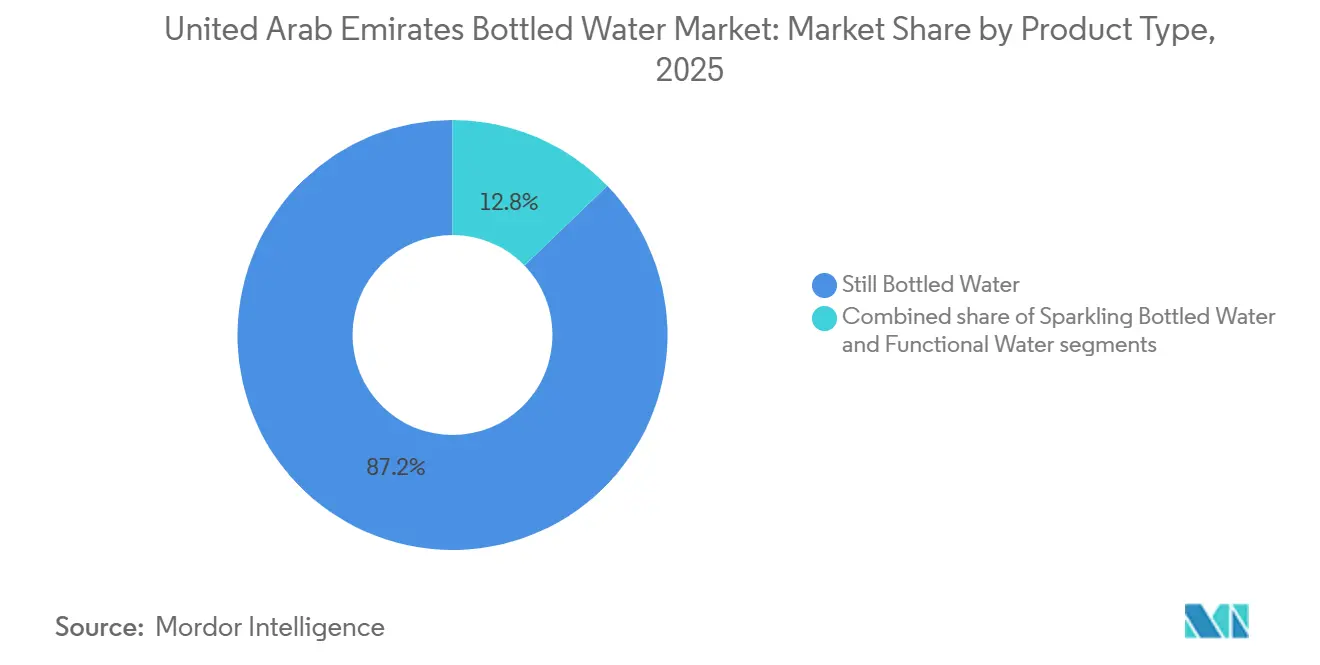

- By product type, still water led with 87.21% of United Arab Emirates bottled water market share in 2025. Functional and flavored water is forecast to expand at a 6.01% CAGR through 2031.

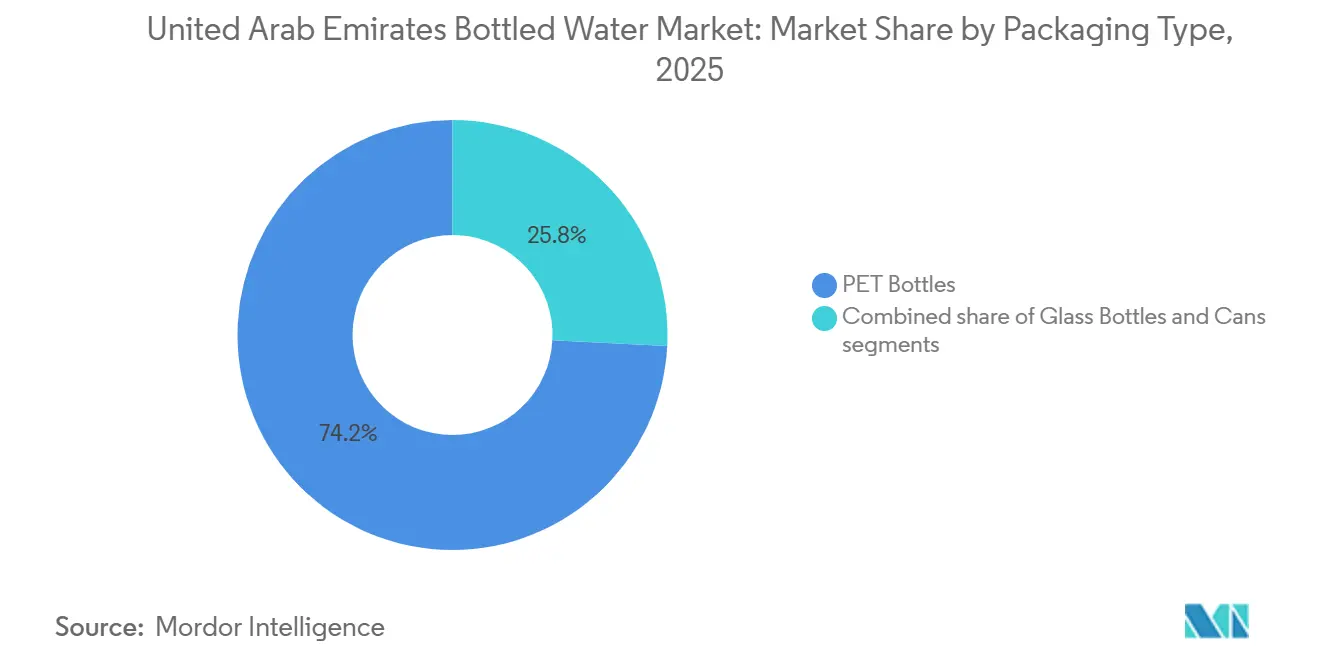

- By packaging format, PET bottles held 74.18% share of the United Arab Emirates bottled water market size in 2025. Aluminum cans are projected to grow at a 6.33% CAGR between 2026 and 2031.

- By category, the mass segment accounted for 73.14% of United Arab Emirates bottled water market size in 2025. The premium segment is advancing at a 6.68% CAGR to 2031.

- By distribution channel, off-trade accounted for 65.28% of United Arab Emirates bottled water market size in 2025, while on-trade is growing at a 5.84% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United Arab Emirates Bottled Water Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing preference for functional and enhanced water among fitness-focused consumers | +1.2% | Dubai, Abu Dhabi urban cores with high expatriate fitness culture | Medium term (2–4 years) |

| Expansion of the tourism and hospitality industry boosting bottled water demand | +1.5% | Dubai, Abu Dhabi, Ras Al Khaimah tourism zones | Short term (≤ 2 years) |

| Growth in the number of foodservice outlets supporting higher consumption | +0.9% | Dubai, Abu Dhabi, Sharjah | Medium term (2–4 years) |

| Regulatory frameworks and stringent quality standards contributing to market growth | +0.6% | Dubai (Municipality jurisdictions) | Long term (≥ 4 years) |

| Rising shift toward sustainable and environmentally friendly packaging solutions | +0.8% | Dubai, Abu Dhabi leading sustainability mandates | Medium term (2–4 years) |

| Harsh climatic conditions across the GCC driving higher bottled water consumption | +1.3% | Dubai, Abu Dhabi | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing preference for functional and enhanced water among fitness-focused consumers

Health-conscious consumers in the United Arab Emirates are increasingly embracing functional water products as the wellness market evolves beyond basic hydration. This shift is reinforced by the rapid expansion of fitness centers in Dubai and Abu Dhabi, which have become important distribution hubs for enhanced water offerings. Coupled with rising awareness of preventive health practices and strong disposable income levels, this mindset is encouraging consumers to spend more on beverages that deliver added functional benefits. According to the Gym Nation report from 2025, 92% of respondents in United Arab Emirates and the Kingdom of Saudi Arabia aspire to improve their health, further driving the category's growth beyond traditional sports drinks into daily consumption patterns, particularly among expatriate communities seeking wellness-oriented products[1]Source: Gym Nation, “UAE & KSA Health and Fitness Report 2025,” gymnation.com. Additionally, the functional water segment benefits from clear regulatory oversight through Emirates Quality Mark standards, which ensures consumer confidence in product claims and nutritional content.

Expansion of the tourism and hospitality industry boosting bottled water demand

Tourism expansion creates sustained demand for bottled water across the United Arab Emirates' hospitality infrastructure, with hotel guests consuming significantly higher volumes than residents. The country welcomed 18.72 million overnight visitors in Dubai during January-December 2024, representing a 9% increase compared to 2023, according to the Department of Economy and Tourism[2]Source: Department of Economy and Tourism, “Tourism Performance Report December 2024,” dubaidet.gov.ae. This expansion strengthens the United Arab Emirates' standing as a leading global luxury travel destination and boosts demand for convenient, on-the-go hydration solutions. At the same time, the hospitality sector’s growing focus on sustainability is creating opportunities for domestic bottled water brands to gain ground over imported products by lowering carbon footprints while preserving service quality. Together, these dynamics point to a strong and sustained growth outlook for the region’s bottled water market.

Growth in the number of foodservice outlets supporting higher consumption

The rapid expansion of restaurants and cafés in the United Arab Emirates is fueling steady demand for bottled water across multiple price tiers and consumption occasions. Within the hospitality, restaurant, and catering (HORECA) sector, strong emphasis is placed on quality and luxury, making premium bottled water a standard offering in upscale hotels, fine-dining restaurants, and corporate environments. In these settings, premium water is not just a beverage but a marker of refinement, enhancing the dining experience and reinforcing the establishment’s commitment to excellence. It also serves as a key element of menu differentiation, helping venues meet the expectations of discerning, high-spending guests who associate premium water with superior service and elevated hospitality standards. This trend is further supported by the expanding hospitality sector, as evidenced by the increase in Dubai's 5-star hotels from 134 in 2020 to 168 in 2024, according to the Dubai Statistics Center[3]Source: Dubai Statistics Center, “Hotel Establishment Data 2024”, dsc.gov.ae. The visibility of bottled water in these establishments reinforces its perceived value in consumers' homes and amplifies overall market demand.

Regulatory frameworks and stringent quality standards contributing to market growth

Regulatory frameworks create a robust foundation through mandatory Emirates Quality Mark certification and stringent monitoring systems. The United Arab Emirates Department of Energy's Water Quality Regulations 2025 establish comprehensive standards for bottled water producers, while the Ministry of Industry and Advanced Technology's approval of recycled PET in water bottles opens new supply chain opportunities[4]Source: Department of Energy, “Water Quality Regulation 2025,” doe.gov.ae. The United Arab Emirates Water Security Strategy 2036 also supports market growth by outlining clear objectives such as a 21% reduction in water demand, improved water productivity to USD 110 per cubic meter, and expanded national water storage capacity. Uniform regulatory frameworks across the emirates, along with adherence to international quality standards, further enable industry expansion by attracting new investments, boosting production capabilities, and opening pathways for export-oriented growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising environmental issues linked to plastic usage and waste generation | -0.7% | UAE (Dubai, Abu Dhabi leading waste-management reforms) | Medium term (2–4 years) |

| Intensifying competition from home water-purification systems | -0.5% | UAE (urban Dubai, Abu Dhabi, Sharjah residential segments) | Medium term (2–4 years) |

| Growing consumer inclination toward sustainable alternatives | -0.4% | UAE (expatriate and national environmentally conscious segments) | Long term (≥ 4 years) |

| Premium pricing of functional water limiting broader adoption | -0.3% | UAE (price-sensitive mass-market consumers) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising environmental issues linked to plastic usage and waste generation

Rising environmental concerns related to plastic usage and waste generation are emerging as significant restraints in the United Arab Emirates bottled water market. With high per-capita consumption of bottled water, the volume of single-use plastic waste has become a major sustainability challenge. Landfills and coastal areas increasingly face pollution pressures, prompting both public and governmental scrutiny of plastic-dependent industries. Growing awareness of microplastics, carbon emissions from plastic production, and improper waste disposal is influencing consumer behavior, with more individuals seeking eco-friendly alternatives. Regulatory bodies in the United Arab Emirates are also tightening guidelines on plastic usage, recycling, and extended producer responsibility, increasing compliance costs for manufacturers. Additionally, global sustainability benchmarks are pushing businesses to shift toward biodegradable packaging or reusable solutions. These environmental pressures collectively hinder market expansion and require producers to innovate to remain competitive.

Intensifying competition from home water-purification systems

Intensifying competition from home water-purification systems is becoming a notable restraint on the United Arab Emirates bottled water market. As advanced filtration, reverse-osmosis, and UV purification technologies become more accessible and affordable, many households are opting for in-home systems as a long-term, cost-effective alternative to bottled water. These systems offer the convenience of continuous purified water, reducing reliance on single-use bottles while appealing to environmentally conscious consumers. Growing concerns about plastic waste and the desire for sustainable living further accelerate the shift toward home purification solutions. Additionally, manufacturers of purification devices are expanding their presence in the country through aggressive marketing and service-based models, increasing their competitive pressure. As adoption rises, bottled water brands face declining household consumption and must innovate or diversify to sustain market relevance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Functional Variants Gain Traction Amid Still Water Dominance

Still bottled water held a dominant 87.21% share of the market in 2025, underscoring its role as the primary hydration choice for the majority of consumers. This dominance is strongly supported by mass-market PET bottle formats, which remain the most accessible and widely used packaging type. These formats cater effectively to residential households, daily commuters, and institutional buyers such as offices, schools, and hospitals. The segment’s strength also stems from its affordability and convenience, making it suitable for both bulk purchasing and on-the-go consumption. Consumer trust in the purity and safety of still bottled water further reinforces its leadership position.

Functional and flavored water represents the fastest-growing category, expanding at a CAGR of 6.01% through 2031. This growth is being propelled by fitness-oriented expatriates and local consumers seeking enhanced hydration solutions. Increasing interest in electrolyte-infused, vitamin-fortified, and performance-focused water options is reshaping consumption patterns within the country. These products align with rising health consciousness and the growing adoption of active lifestyles. The segment also benefits from premium positioning, appealing to consumers seeking added value beyond basic hydration. As demand accelerates, functional and flavored water is emerging as a key driver of diversification and innovation within the United Arab Emirates bottled water market.

By Category: Premium Segment Expands on Sustainability and Provenance

Mass-market bottled water products held a commanding 73.14% share of the market in 2025, reflecting the influence of price-conscious purchasing behaviors across a broad consumer base. This segment’s strength is rooted in competitive pricing models, wide distribution coverage, and a consumer preference for practical hydration over premium attributes. Local producers have effectively secured this space by delivering reliable quality at affordable price points. Easy access through supermarkets, convenience outlets, and traditional retail channels further strengthens the segment’s dominance. As a result, mass-market bottled water continues to serve as the backbone of overall market demand.

The premium bottled water category is gaining strong momentum, registering a projected CAGR of 6.68% through 2031, fueled by imported brand positioning, functional product innovations, and sustainability credentials that validate higher pricing. Market insights show a rising readiness among consumers to spend more for elevated quality perceptions and eco-friendly attributes. This pattern corresponds with the United Arab Emirates' solid economic footing, highlighted by its GDP per capita of USD 50,033.1 as of April 2025, according to the World Bank, which supports the growth of premium choices targeting affluent buyers and the hospitality industry. Premium brands have carved out differentiation through distinctive mineral profiles and upscale packaging aesthetics.

By Packaging Format: PET Leadership Challenged by Sustainable Alternatives

PET bottles remained the leading packaging format with a 74.18% market share in 2025, supported by their cost-effectiveness, strong supply chain integration, and high consumer acceptance. Although PET benefits from mature production and recycling systems, rising environmental concerns continue to challenge its long-term viability. The Ministry of Industry and Advanced Technology’s approval of recycled PET has opened avenues for more sustainable packaging solutions without compromising affordability. Producers are increasingly investing in advanced processing technologies to enhance material efficiency and lower manufacturing expenses. Furthermore, innovations in PET barrier properties have broadened its suitability across a wider range of beverage categories.

Aluminum cans represent the fastest-growing packaging type, expanding at a 6.33% CAGR through 2031, bolstered by their premium image and strong sustainability appeal. This momentum is particularly visible in on-trade environments, where packaging aesthetics significantly influence consumer choices. For example, Nestlé S.A.'s Perrier brand has introduced sparkling water in aluminum cans, positioning it as a refined alternative. Glass bottles continue to maintain relevance within premium and imported product segments, especially in upscale hospitality and retail settings. Aluminum’s lightweight profile helps reduce transport-related costs and emissions, further strengthening its value proposition. Its infinite recyclability has also drawn increasing interest from beverage companies aiming to elevate their environmental performance.

By Distribution Channel: On-Trade Gains as Foodservice Expands

Off-trade channels lead the market with a 65.28% share in 2025, supported by strong consumer preferences for retail-based purchases and bulk buying. Supermarkets and hypermarkets remain the primary distribution formats, offering competitive pricing and broad product assortments, while convenience stores cater to quick, on-the-go needs. The dominance of this channel is reinforced by the steady growth of retail outlets and the rising penetration of online retail platforms. Strategic store placement and streamlined inventory management systems contribute to consistent product availability. In addition, off-trade retailers capitalize on loyalty programs and seasonal promotions to sustain their competitive advantage and retain customers.

On-trade channels are projected to expand at a 5.84% CAGR through 2031, driven by the rapid development of the hospitality sector and the increasing number of food service establishments across the United Arab Emirates. This outlook is strengthened by positive tourism forecasts and the continued evolution of the restaurant industry. Online retail platforms are also gaining traction due to their convenience, efficient delivery options, and suitability for bulk orders, reflecting shifting consumer habits toward e-commerce and home delivery. The growing influence of food delivery applications has further bolstered the on-trade channel’s presence. Additionally, advancements in digital payment solutions and mobile ordering technologies have enhanced overall customer engagement and streamlined service experiences within on-trade environments.

Geography Analysis

The United Arab Emirates bottled water market is strongly shaped by the country’s harsh climatic conditions and limited freshwater resources, which drive exceptionally high per capita consumption across all emirates. Regions such as Dubai and Abu Dhabi contribute the largest share of demand due to their dense populations, strong expatriate base, and thriving commercial sectors. These emirates host most of the country’s hospitality, retail, and tourism infrastructure, creating continuous demand for both mass-market and premium bottled water. High urbanization also supports an extensive distribution network, enabling efficient last-mile delivery and availability across supermarkets, convenience stores, and food service outlets.

Northern emirates such as Sharjah, Ajman, and Ras Al Khaimah play a significant role, driven by a growing residential population and rising retail expansion. These emirates exhibit strong demand for affordable, mass-market bottled water formats, particularly large-volume PET bottles preferred by households and labor accommodations. Local manufacturers operating within these regions benefit from proximity to industrial zones, lower production costs, and easy access to distribution corridors linking retail outlets across the country. Sharjah’s increasing investment in industrial and commercial infrastructure further supports steady consumption.

Tourism-driven emirates such as Dubai, Abu Dhabi, and Ras Al Khaimah also continuously influence the premium bottled water segment. High-end hotels, luxury resorts, and fine-dining establishments create consistent demand for imported and premium water brands, including sparkling, functional, and glass-bottled products. The rapid expansion of tourism campaigns, international events, and hospitality investments further fuels consumption among visitors and expatriates. Additionally, the country's role as a regional logistics hub enables seamless importation of global brands and supports the diversification of product offerings across emirates.

Regulatory Landscape

Bottled drinking water and natural mineral water sold in the United Arab Emirates are subject to mandatory conformity and quality controls anchored by the Ministry of Industry and Advanced Technology (MoIAT). Products must comply with the Emirates Conformity Assessment Scheme (ECAS) and obtain the Emirates Quality Mark (EQM), typically supported by ISO 17025 laboratory testing, documented QMS/FSMS systems, and potential factory audits, which raises the compliance bar for both domestic producers and importers.

Market access also depends on federal and local requirements related to recycled plastic use and labeling. Cabinet Resolution No. 26 of 2013 governs control of bottled drinking water, while Federal Law No. 105 of 2022 addresses circulation of bottled drinking water in recycled plastic bottles, aligning packaging choices with food-contact safety requirements. Labels commonly require local authority acceptance (for example, Dubai Municipality processes for imports) and must carry core information in Arabic and English. In April 2025, MoIAT issued an update to national conformity mark designs with defined transition timelines, driving packaging artwork and inventory changeovers across regulated categories, including bottled water.

Competitive Landscape

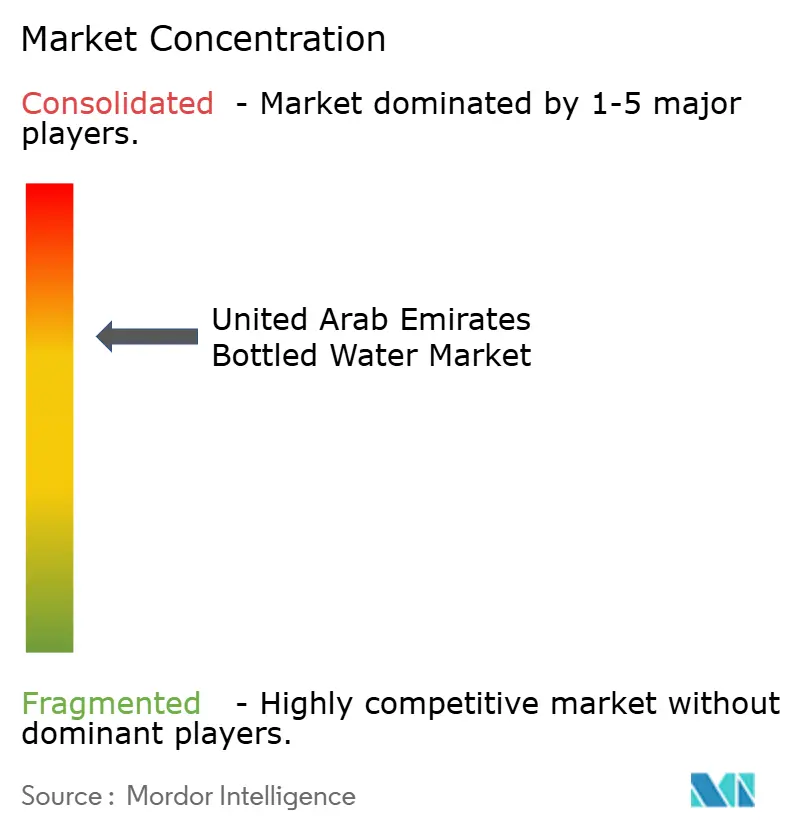

The United Arab Emirates bottled water market is consolidated, with leading players in the United Arab Emirates bottled water market maintaining competitive edges through vast distribution networks, robust brand equity, and stringent compliance with regulatory standards. Prominent companies such as Danone S.A., Reignwood Group, Nestlé S.A., and Ma Hawa continue to dominate the premium segment by prioritizing product differentiation, premium packaging, and targeted market expansion. Their competitive strength is further supported by long-standing relationships with retailers, hospitality partners, and institutional buyers, enabling them to maintain consistent visibility and market penetration.

Across the industry, companies are actively engaged in growth-oriented strategies aimed at expanding their geographic footprint, reinforcing brand identity, and improving product availability across both off-trade and on-trade channels. Investments in new product development such as functional, mineral-rich, or environmentally sustainable variants have become central to strengthening market relevance. Firms are also increasing their focus on supply chain optimization, digital integration, and marketing initiatives to elevate consumer engagement and sustain long-term competitiveness in a rapidly evolving marketplace.

A notable example of these strategic efforts emerged in October 2024, when FIJI Water, owned by The Wonderful Company LLC, entered into a partnership with Dubai-based Al Maya Group to accelerate its expansion in the country. This collaboration reflects a mutually beneficial approach: FIJI Water gains access to Al Maya Group’s vast supermarket network, well-established FMCG distribution channels, and multi-country franchise operations, while Al Maya strengthens its premium product offering. Backed by support from the Fijian government embassy, the partnership underscores how international brands are leveraging strong regional distributors to deepen market penetration and capture the growing demand for premium bottled water in the country.

United Arab Emirates Bottled Water Industry Leaders

The Wonderful Company LLC

Reignwood Group

Sophia Water

Nestlé S.A

Danone S.A.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Sustainability-compliant packaging and circular service models are creating clearer opportunities in a category still dominated by PET bottles (74.18% share in 2025). MoIAT oversight of recycled PET for food-contact applications, alongside the continued emphasis on EQM compliance, supports incentives for certified suppliers of rPET, packaging converters, and bottlers that can demonstrate validated quality systems. It also supports premium differentiation routes through glass and cans in hospitality and on-trade settings.

Local operator capacity additions and portfolio broadening point to active investment across mainstream retail and home and office delivery (HOS). Agthia Group expanded its UAE water footprint through the acquisition of Riviere Mineral Water Desalination and Filling Factory LLC in March 2025, adding bottling facilities in Abu Dhabi and Dubai and strengthening distribution into everyday consumption occasions. On the manufacturing side, Mai Dubai commissioned a high-speed PET line in December 2025 (up to 100,000 bottles per hour), which supports demand for equipment suppliers, utilities optimization, and local sourcing programs tied to high-throughput bottling. In parallel, BE WTRs circular bottling concept indicates service-led routes to capture hotel and event demand, alongside product innovation across functional, fortified, and flavored water.

Recent Industry Developments

- May 2026: BE WTR launched a home delivery app in Dubai as part of its phased UAE expansion. The initiative strengthens direct-to-consumer access for premium water and supports recurring demand beyond hotel-only consumption, while improving service visibility versus traditional home and office delivery operators.

- June 2025: Bisleri International partnered with UAE-based Apparel Group to manufacture, market, and distribute Bisleri beverage products in the UAE. The tie-up draws on Apparel Group's local retail and distribution footprint, lowering route-to-market barriers for the incoming brand and increasing competitive pressure in mass and convenience-led channels.

- November 2024: Agthia Group partnered with Capital Catering to provide bottled water services for Etihad Airways and the Abu Dhabi National Exhibitions Company. The agreement reinforces Agthias position in institutional and event-driven demand, supporting volume stability through large, contracted consumption occasions.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers packaged drinking water sold in the UAE through retail, food-service, e-commerce, and bulk home or office delivery, valued in revenue terms. It includes bottled water that is sealed for consumption and sold as still or sparkling options across common pack formats.

Scope exclusions: Excludes water filtration and dispenser systems, unbranded tanker refills, soda-maker syrups, and post-mix fountain water.

Segmentation Overview

- By Product Type

- Still Bottled Water

- Sparkling Bottled Water

- Functional/Flavored Bottled Water

- By Packaging Format

- PET Bottles

- Glass Bottles

- Cans

- By Category

- Mass

- Premium

- By Distribution Channel

- On-Trade

- Off-Trade

- Supermarket/Hypermarket

- Convenience/Grocery Stores

- Online Retail Stores

- Others Distribution Channel

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by building the demand and supply context for bottled water in the UAE, and then matching it to practical indicators we can observe year over year. Public sources such as UAE Federal Competitiveness and Statistics Centre releases, Dubai Statistics Center updates, and UAE customs and trade statistics are used to understand population, visitor flows, and import dependence for packaged beverages.

We also refer to sources such as municipality or food safety authority updates on bottled water standards, published sustainability and packaging rules, and peer-reviewed papers on water consumption behavior in hot climates. Company annual reports, press releases, and retailer announcements help confirm pack formats, channel emphasis, and pricing moves. Where needed, paid subscriptions that compile company financials, news and financials, import and export shipment-level records, and patent databases are used to speed up cross-checks. The sources listed above are illustrative only, and many other public documents were reviewed to collect, validate, and clarify data points.

Primary Interviews and Surveys

Primary work is used to pressure-test the desk assumptions on volume movement, channel mix, and realistic price ladders across pack sizes, especially where public data is not consistent. We speak with brand owners, distributors, large-format retailers, food-service buyers, and packaging and logistics stakeholders, and the coverage is kept balanced across the main emirates so the view does not become Dubai-only.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 21% | |

| Mid tier: 45% | Functional/Unit leaders: 32% | |

| Smaller Players: 22% | Managers: 47% |

Market-Sizing & Forecasting

The core sizing logic uses a top-down build where beverage consumption signals and trade and production indicators are reconstructed into a bottled-water value pool for the UAE, then filtered using channel and pack patterns. To keep the totals grounded, we also run selective bottom-up checks using sampled brand price points by pack size, observed shelf assortment, and distributor or retailer throughput ranges, and we adjust totals when the two views do not line up.

Key inputs used in the model include per-capita bottled water consumption direction, population and visitor inflows, on-trade versus off-trade share movement, the split between small packs and large packs (including bulk delivery packs), and price progression by pack size and material. We also track signals that affect value growth, such as premiumization into glass or functional claims, and changes in freight and resin-linked packaging costs that can move realized pricing.

For forecasting, scenario analysis is used around tourism and population growth, channel shifts to e-commerce and delivery, and expected pricing behavior under inflation and packaging regulation. When a bottom-up check has gaps, we fill them with conservative ranges based on comparable pack sizes and channel norms from interviews, and then keep the final result tied back to the same demand pool logic.

Data Validation & Update Cycle

Outputs are validated through several passes that look for mismatches between the model and independent signals, such as import patterns, major retail price moves, and reported capacity or expansion activity. When an outlier shows up, the driver is traced to a specific assumption, for example channel share, pack mix, or pricing, and it is corrected only after it is rechecked against a second source or a follow-up expert touchpoint.

Before sign-off, the numbers are reviewed by another analyst to confirm math integrity, consistent currency treatment, and that the assumptions are explained in plain terms. Reports refresh on an annual cycle, and interim updates are triggered when major events occur, such as regulation changes, sharp cost shocks, or large capacity additions. Right before delivery, we do a fresh review so clients receive the most current view available.

Mordor Intelligence's UAE Bottled Water Market Estimate Compared With Other Published Estimates

Published market sizes for bottled water in the UAE often do not match because groups use different product boundaries, price levels, and channel inclusion, and then they apply different growth assumptions over the same years. Even when the end label sounds the same, the included items can shift the final number by a lot.

Unbranded tanker refills and post-mix fountain water sit outside Mordor Intelligence's scope, and this usually pulls value lower versus sources that treat all packaged and served drinking water as one bucket. Differences also come from whether bulk home and office delivery is valued at manufacturer selling price or at retail-equivalent price, and whether imported premium water is converted using the same average exchange rate timing. Some estimates also lean aggressive on premiumization and tourism recovery, while others keep a steadier price curve tied to observed shelf prices and trade signals.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 4.01 B (2026) | |

| Industry Publisher A | USD 1.61 B (2025) | Uses a narrower value capture that appears closer to packaged retail sales only, with limited clarity on bulk home or office delivery valuation and on-trade inclusion, which can understate the total compared with a full channel view. |

| Consultancy B | USD 1.75 B (2024) | Base year and scope notes are high level, and the estimate likely reflects a different price basis and segment coverage, which can compress the current value if premium imports, food-service, or delivery formats are not fully counted. |

The spread in the table is mainly explained by what gets counted as bottled water revenue and how channels are valued, rather than a simple math disagreement. By tying the market to clear consumption signals, channel splits, and pack-level price checks, the final number stays traceable and can be repeated when new trade or pricing data becomes available.

Key Questions Answered in the Report

How large is the UAE bottled water market in 2026?

The UAE bottled water market size is USD 4.01 billion in 2026 and is forecast to reach USD 5.22 billion by 2031.

Which packaging format is growing fastest?

Aluminum cans are projected to post the highest growth at a 6.33% CAGR between 2026 and 2031.

Why is functional bottled water gaining traction?

Rising gym usage, wellness tourism, and new Nutri-Mark labeling encourage consumers to trade up to electrolyte- and vitamin-enriched variants.

How does regulation impact new entrants?

Mandatory Emirates Quality Mark certification and potential fines up to AED 500,000 elevate compliance costs, favoring companies with ISO-certified facilities.

What role does tourism play in demand?

High hotel occupancy and ambitious visitor targets ensure that on-premise channels remain a structural growth driver for bottled water sales.

Page last updated on: