United States Alternative Protein Ingredients Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

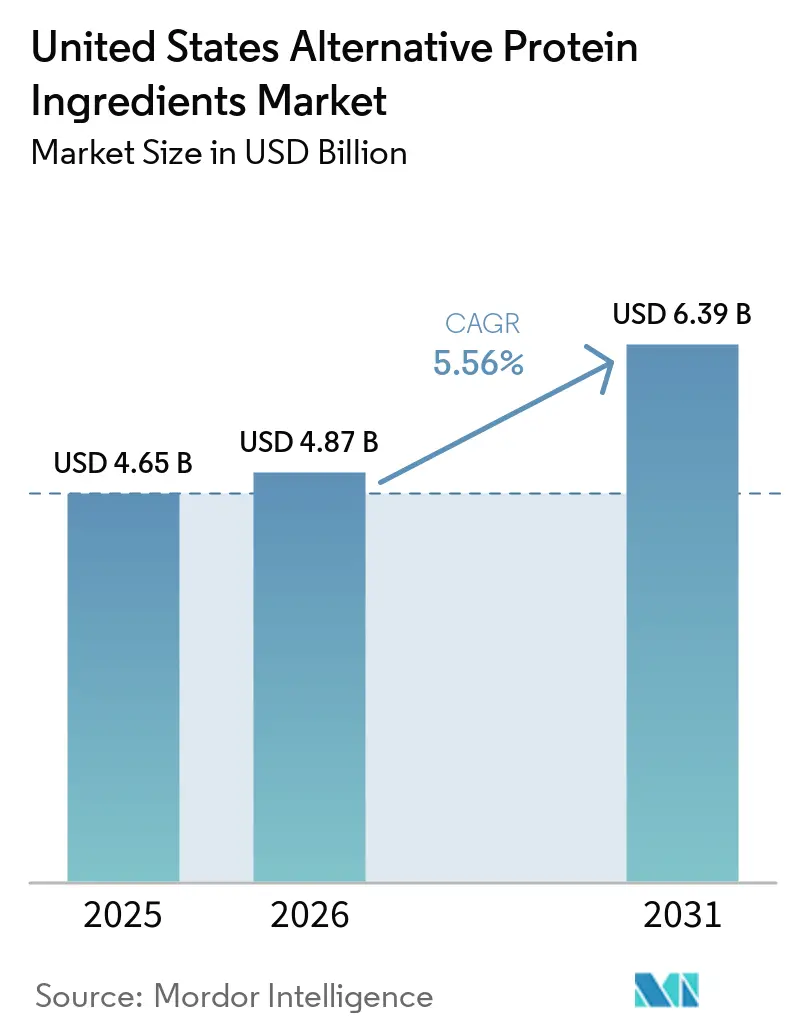

| Base Year Market Size (2025) | USD 4.65 Billion |

| Market Size (2026) | USD 4.87 Billion |

| Market Size (2031) | USD 6.39 Billion |

| Growth Rate (2026 - 2031) | 5.56% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Alternative Protein Ingredients Market Analysis by Mordor Intelligence

The US alternative protein ingredients market size was valued at USD 4.7 billion in 2025 and estimated to grow from USD 4.9 billion in 2026 to reach USD 6.4 billion by 2031, at a CAGR of 5.6% during the forecast period 2026-2031. The US alternative protein ingredients market is moving at a measured pace because buyers are giving more weight to ingredients that already work well in processing, scale more reliably, and fit current product formulas with less risk. Demand is being supported by stronger interest in high-protein foods, broader use of plant-forward menu formats, and steady product work in beverages, dairy alternatives, and sports nutrition. The US alternative protein ingredients market is also benefiting from lower early-stage barriers in some fermentation applications, even though the path to large food-grade volumes still depends on further gains in purification, drying, and plant utilization. Competition is centered on a few large ingredient suppliers with broad soy and pea infrastructure, while newer firms are focused on specialty proteins where formulation value is higher and direct price competition is lower. Regional demand patterns are widening beyond the coastal base, which gives the US alternative protein ingredients market a broader consumption base while keeping the Midwest important for processing capacity and delivered-cost advantage.

Key Report Takeaways

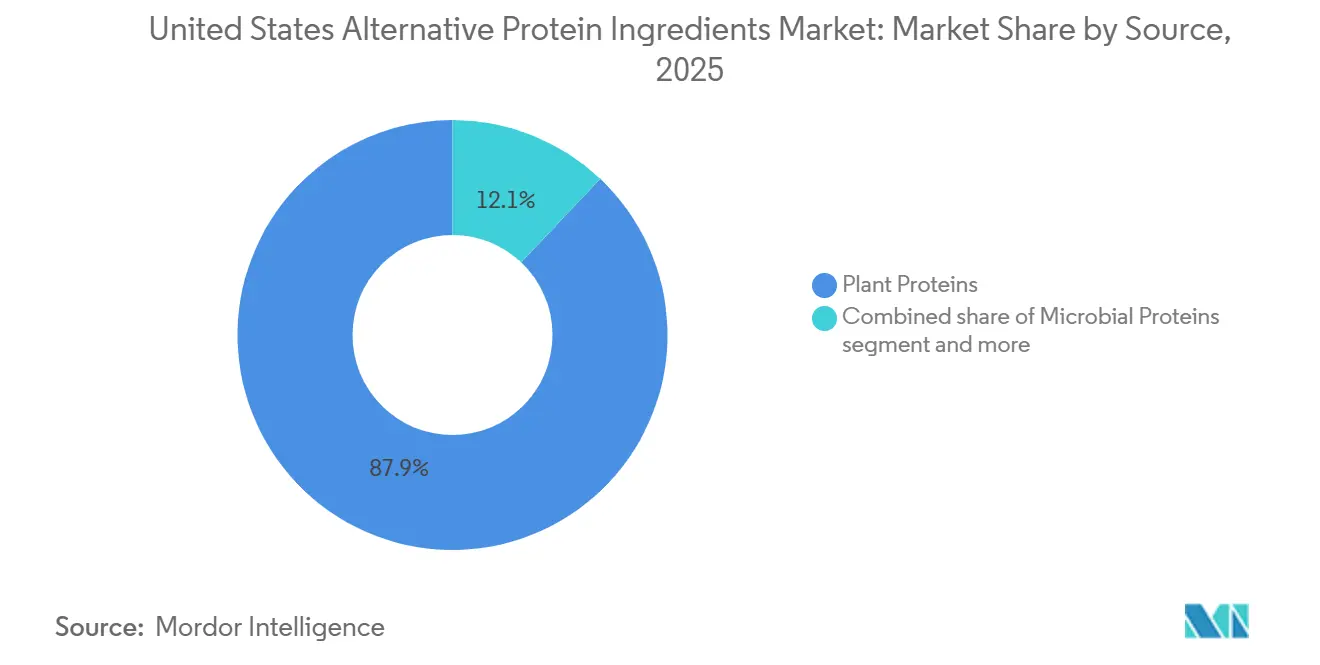

- By source, plant proteins held 87.94% of the source segment in 2025, while microbial proteins recorded the fastest projected growth at 10.96% through 2031.

- By form, protein isolates accounted for 44.62% of the form segment in 2025, while textured proteins and TVP are forecast to grow at 8.01% through 2031.

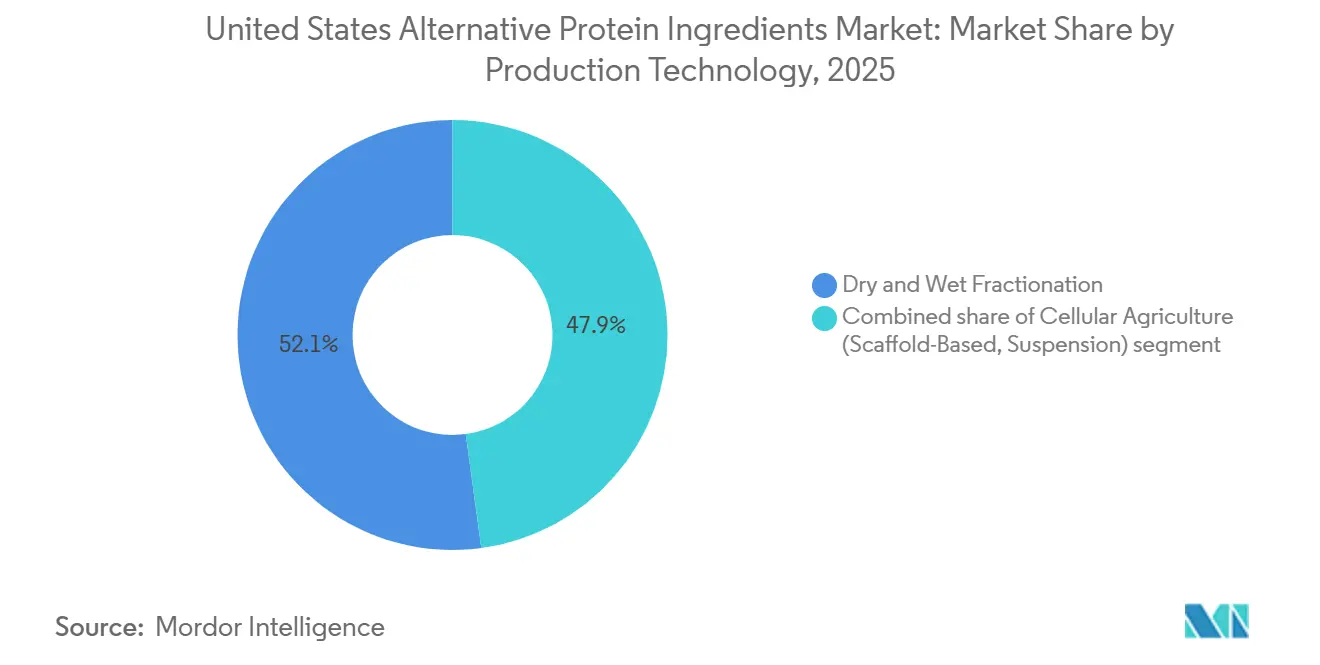

- By production technology, dry and wet fractionation represented 52.13% of the segment in 2025, while cellular agriculture is projected to expand at 7.51% through 2031.

- By application, food and beverage captured 51.13% of the segment in 2025, while the dietary supplements and sports nutrition segment is expected to grow at 7.83% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Alternative Protein Ingredients Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for High-Protein Functional Foods | +1.4% | Global, led by the United States retail and sports nutrition channels | Short term (≤ 2 years) |

| Retail and Foodservice Reformulation Toward Plant-Forward Menus | +1.1% | The United States (West, Midwest, and South retail corridors) | Short term (≤ 2 years) |

| Precision Fermentation Cost Curves Improving Commercial Viability | +0.9% | The United States, with a West Coast research and development concentration and a Midwest fermentation infrastructure | Medium term (2–4 years) |

| Clean-Label and Allergen-Reduction Positioning | +0.7% | The United States (Northeast and West coastal markets, with spill-over to the Midwest) | Short to medium term (1–3 years) |

| Insect and Fermentation Side-Streams from the United States Agri-Processing | +0.6% | Midwest corn and soybean processing belt, with early gains in Illinois and Iowa | Long term (≥ 4 years) |

| Growing Vegan, Vegetarian, and Flexitarian Populations | +0.9% | The United States (West, Midwest, and South retail corridors) | Medium to Long Term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for high-protein functional foods

High-protein positioning has evolved from a niche sports nutrition claim into a mainstream purchasing criterion across a broad range of food and beverage categories. According to ADM's 2025 Alternative Protein Landscape Report, 66% of global consumers actively aim to increase their protein intake, while 86% prefer obtaining protein from a wider variety of sources, reinforcing demand for alternative protein ingredients across diverse applications. As protein shifts from a premium differentiator to a baseline product expectation, competition increasingly centers on identifying protein sources that deliver superior functionality while maintaining cost efficiency. This dynamic strengthens the position of established plant proteins, particularly soy and pea isolates, which combine high protein content with desirable functional properties such as emulsification, gelation, and extrusion performance. At the same time, the rapid expansion of functional foods is accelerating demand for specialty proteins, including precision-fermented egg proteins, animal-free dairy proteins, and mycoprotein isolates, particularly in premium applications such as Greek-style yogurt alternatives and ready-to-drink beverages where protein concentration, solubility, and neutral flavor profiles are critical product differentiators. Consequently, ingredient manufacturers with portfolios spanning both high-volume commodity protein concentrates and high-value specialty protein isolates are better positioned to address evolving customer requirements across mass-market and premium food segments.

Retail and foodservice reformulation toward plant-forward menus

The growing adoption of alternative proteins by large foodservice operators and consumer packaged goods (CPG) manufacturers is emerging as a significant demand driver for alternative protein ingredients. According to the Plant Based Foods Association, the United States plant-based retail market reached USD 7.9 billion in 2025, with ready-to-drink (RTD) beverages and baked goods recording strong growth of 12.1% and 8.6%, respectively, despite continued volume declines in the traditional plant-based meat segment[1]Source: Plant Based Foods Association, “2026 State Of The Industry,” Plant Based Foods Association, plantbasedfoods.org. This divergence indicates that demand is increasingly shifting toward protein fortification across mainstream food categories rather than relying solely on meat analog applications. At the same time, hybrid meat products combining animal and plant proteins are gaining traction across quick-service restaurants (QSRs) and institutional foodservice channels. ADM's research shows that 64% of plant-forward consumers are interested in hybrid protein products, while commercial buyers continue to favor formulations with a higher meat-to-plant ratio. This trend expands demand for textured soy protein concentrates and pea-based extrusion ingredients, which are well-suited for hybrid formulations. As a result, institutional procurement and foodservice contracts are expected to provide a more stable source of ingredient demand than retail plant-based product launches, where volumes remain susceptible to shifting consumer preferences and shelf-space rationalization.

Precision fermentation cost curves improving commercial viability

Precision fermentation is following a rapid cost-reduction trajectory, making it an increasingly viable platform for producing alternative protein ingredients. According to the Good Food Institute, production costs for leading commercial precision-fermentation proteins have declined from approximately USD 1,000 per kilogram in 2015 to below USD 50 per kilogram in 2025, with further reductions expected as production scales beyond 100,000-liter fermentation facilities. The Good Food Institute Europe also reported that nearly 24% of the 67 precision-fermented molecules assessed already exhibit favorable cost dynamics compared to conventionally produced counterparts, with continued improvements anticipated through advances in strain engineering and substrate optimization[2]Source: Good Food Institute, “Fermentation Capacity And Cost Materials,” Good Food Institute, gfi.org. However, the primary economic challenge has shifted from fermentation to downstream processing. Synthesis Capital's 2026 analysis estimates that centrifugation, filtration, and drying account for 50–85% of total manufacturing costs, indicating that future cost competitiveness will depend more on innovations in purification technologies, membrane separation, and spray-drying efficiency than on increasing bioreactor scale alone. Although North American food-grade fermentation capacity continues to expand, it remains insufficient to significantly displace conventional protein production in the near term, positioning precision fermentation as a medium- to long-term growth driver for the alternative protein ingredients market rather than an immediate source of large-scale supply.

Clean-label and allergen-reduction positioning

The growing consumer preference for clean-label products is reshaping sourcing strategies within the alternative protein ingredients market by increasing demand for minimally processed, transparent, and allergen-friendly protein sources. Non-GMO and organic soy protein ingredients continue to command premium pricing, encouraging manufacturers to secure certified feedstock through long-term supply agreements to ensure supply stability. At the same time, proteins derived from pea, rice, hemp, and fava beans are gaining traction as they simultaneously address clean-label, soy-free, and gluten-free product requirements, enabling food manufacturers to satisfy multiple consumer preferences with a single ingredient platform. Product innovation is further supporting this trend. For instance, Roquette's May 2024 launch of NUTRALYS Fava S900M, a 90% protein-content fava bean isolate with a neutral taste and light color, was developed to meet the growing demand for allergen-friendly, clean-label protein ingredients with strong sustainability credentials. Furthermore, the FDA's proposed review of mandatory GRAS notifications, expected in October 2025, is anticipated to strengthen regulatory requirements for novel protein ingredients, increasing the importance of robust safety documentation and potentially favoring established suppliers with well-developed regulatory portfolios.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Scale-Up and Food-Grade Processing Capacity | -1.1% | Global, concentrated in the United States, fermentation and high-moisture extrusion infrastructure | Medium term (2–4 years) |

| Taste, Texture, and Consumer Acceptance Gaps Versus Animal Protein | -0.7% | The United States broadly, with the strongest resistance in the South and Midwest, legacy meat markets | Short to medium term (1–3 years) |

| Regulatory, Labeling, GRAS, and State-Level Compliance Complexity | -0.5% | National, with early gains in California, New York, and Texas, regulatory clusters | Medium term (2–4 years) |

| Regulatory Restrictions Impact Insect Protein Adoption | -0.4% | National, with state-level feedstock restrictions adding layers of complexity | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High cost of scale-up and food-grade processing capacity

The high capital investment required to establish food-grade alternative protein production facilities remains a significant restraint on market expansion. Commercial-scale precision fermentation plants with 100,000–200,000-liter bioreactor capacity typically require capital investments ranging from USD 150–300 million and are designed for operating lifespans of 15–20 years. Such substantial financial commitments create high barriers to entry, limiting participation primarily to large agribusiness companies and well-funded biotechnology firms. Consequently, scaling production is constrained not by technological readiness but by the availability of long-term capital. This challenge has become more pronounced as investment activity weakened in 2025, with total funding for alternative protein companies declining and fermentation-focused investments falling by 43% to USD 357 million. Reduced investment is expected to slow the expansion of commercial production capacity, delaying economies of scale and limiting the industry's ability to compete with conventional protein sources on cost. As demand for precision-fermented proteins continues to grow, production capacity may struggle to keep pace over the medium term, increasing the risk of supply constraints and limiting wider adoption across food and beverage applications.

Taste, texture, and consumer acceptance gaps versus animal protein

Despite years of investment in formulation, most alternative protein ingredient applications still struggle to achieve sensory parity with animal protein, with the gap most evident in high-volume product categories. Beany off-notes in soy protein and earthy flavors in pea concentrate continue to require masking solutions, flavors, enzymes, or blending. These interventions add cost and complexity, creating a structural drag, particularly for low-margin commodity applications in institutional foodservice. ADM's 2026 research is expected to highlight that consumers in hybrid product trials prefer a higher meat-to-plant ratio, suggesting that tolerance for plant-protein sensory deviation narrows as product price points fall below the premium grocery tier. More granular data indicate that while 72% of Millennials and 68% of Gen Z expressed openness to fermentation-derived proteins in ADM's 2025 survey, only 12% of US adults used plant-based proteins more than half the time as animal protein replacements, according to 2025 market data. This reflects a persistent behavioral gap between stated openness and actual substitution. For the ingredient industry, this creates an ongoing need to invest in flavor technology and high-moisture extrusion to improve fibrous texture, delaying the timeline for cost-competitive mass-market adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Microbial Proteins Disrupt a Plant-Dominated Supply Base

Plant proteins are expected to account for 87.94% of the source segment in 2025, supported by soy protein's decades-long processing infrastructure and pea protein's allergen-friendly profile, which has driven its rise as the dominant non-GMO alternative since 2020. Within plant proteins, soy leads by volume, supported by ADM's integrated Decatur, Illinois, complex and Cargill's Midwest origination infrastructure. Meanwhile, pea, hemp, and rice proteins are gaining specification preference among formulators seeking soy-free and gluten-free declarations. Wheat protein serves a distinct niche in bakery and meat-extension applications, where high-gluten cohesion is a functional requirement.

Microbial proteins are projected to grow at a CAGR of 10.96% through 2031, making them the fastest-growing source segment. The segment spans three sub-categories: mycoprotein, led by Quorn and Nature's Fynd in US retail channels; algae protein, anchored in nutraceuticals and sports nutrition; and insect proteins, primarily serving animal feed and pet food. The Protein Brewery's commercial availability of Fermotein mycoprotein in the US, with 2026 capacity sold out according to the company, illustrates how quickly commercially validated microbial sources are absorbing available near-term supply. Ingredient buyers must consider that the two fastest-growing sub-categories within microbial proteins serve fundamentally different application requirements. Precision-fermented fungal proteins perform well in texturized meat-analog formats, while algae-derived concentrates primarily target high-value nutritional and functional food applications. As a result, competitive dynamics within this source segment are likely to bifurcate rather than converge as it scales.

By Form: Textured Proteins Gain on Isolates as Hybrid Formats Proliferate

Protein isolates are expected to account for 44.62% of the form segment in 2025, supported by their widespread use in beverages, sports nutrition, and clinical products that require high protein density and minimal impact on finished-product texture. Protein concentrates, hydrolysates, and peptides comprise the remaining conventional forms. Hydrolysates are gaining traction in sports recovery and infant nutrition formulations, where rapid amino acid absorption offers a functional point of differentiation.

Textured proteins and TVP are forecast to register the fastest growth among all form segments, with an 8.01% CAGR through 2031. High-moisture extrusion technology continues to improve whole-muscle-like fibrous structures in soy and pea formats, creating foodservice contract opportunities that were previously inaccessible to plant proteins. ADM’s expected May 2026 launch of Arcon IH, Arcon SB, and Arcon 412 soy protein concentrates, each engineered to deliver specific textures in ham, sausage, and chicken nugget applications, highlights how functional differentiation, rather than commodity volume, is shaping competitive positioning in this form category. Roquette is expected to reinforce this trend with its June 2025 addition of NUTRALYS T WHEAT 600L and NUTRALYS T PEA 700XC to its textured protein range, targeting manufacturers seeking non-soy, gluten-containing, or pea-based texturants as supply chain alternatives. For formulators, the practical implication is that the cost-per-texture-unit gap between plant-based and animal-protein texturants is narrowing faster than the protein content gap, making textured formats the segment most likely to achieve broad mainstream foodservice adoption over the forecast period.

By Production Technology: Cellular Agriculture Leads Growth from a Narrow Base

Dry and wet fractionation is expected to account for 52.13% of the production technology segment in 2025, reflecting the capital already deployed in large-scale soy crushing, pea wet milling, and wheat gluten extraction facilities concentrated in the US Midwest processing corridor. In the United States, installed textured plant protein extrusion capacity is expected to reach utilization rates of 70–80% in 2026, indicating that new greenfield investment, rather than utilization gains, will be required to expand supply materially. Extrusion and texturization and precision fermentation represent the middle tier. Among specialty ingredient developers, precision fermentation is expected to attract the most research and development and capital attention, despite a 43% decline in dedicated fermentation funding in 2025.

Cellular agriculture, which includes scaffold-based and suspension culture platforms, is projected to record the fastest growth across all technology segments, at a CAGR of 7.51% through 2031. However, it will grow from a narrow commercial base that continues to advance through sequential pre-market safety and facility review processes before meaningful commercial volumes can enter the ingredient supply chain. This technology mix also has a less-discussed implication: US ingredient buyers sourcing from multiple production technologies now face divergent supply chain risk profiles. These range from fractionation capacity constraints to single-supplier strain dependencies in mycoprotein and precision fermentation, making portfolio diversification across technologies a practical procurement requirement rather than an aspirational goal.

By Application: Dietary Supplements Outpace Food and Beverage in Growth Rate

Food and Beverage is expected to account for 51.13% of the application segment in 2025, with meat alternatives, dairy alternatives, and bakery collectively forming the volume core of ingredient demand. Within the Food and Beverage sub-segments, dairy alternatives (plant-based milks, yogurts, and cheese) and meat, poultry, and seafood alternatives require the highest functional performance specifications and, consequently, use the most premium-priced protein forms. Snacks represent an emerging application for textured proteins and pea crisps, while beverages are incorporating high-solubility isolates and precision-fermented proteins into RTD formats. According to the Plant Based Foods Association (PBFA), these formats are expected to grow by 12.1% in US plant-based retail during 2025[3]Source: Plant Based Foods Association, “2026 State Of The Industry,” Plant Based Foods Association, plantbasedfoods.org. Animal Feed and Pet Food, as well as Personal Care and Cosmetics, are becoming increasingly important secondary applications. Pet food represents North America's largest near-term market for insect protein, while Geltor's PrimaColl biodesigned collagen polypeptide, cleared by the FDA for both food and beauty applications, demonstrates how a precision-fermented protein can bridge personal care and nutrition within a single regulatory dossier.

Dietary Supplements and Sports Nutrition are expected to grow at a CAGR of 7.83% through 2031, outpacing the overall market and the Food and Beverage segment. Growth is driven by active-lifestyle consumers’ demand for high-purity, non-GMO protein powders and functional stacks that command significant per-kilogram premiums. The EVERY Company's commercial-scale egg white protein, now distributed through partnerships with Walmart and sold at metric-ton volumes, shows how precision-fermented proteins are achieving mainstream distribution in nutritional formats well ahead of their adoption in cost-sensitive food applications.

Geography Analysis

The West is expected to remain the strongest early-adoption cluster in the United States alternative protein ingredients market, with 67.3% household penetration for plant-based foods in 2025 and an 81.4% repeat purchase rate, the highest among United States regions, according to the Plant Based Foods Association (PBFA). California continues to play a critical role, as its natural grocery density and product development ecosystem help new formats move more quickly from trial to repeat purchase. The region is also expected to account for 31% of the United States spending on tofu, tempeh, and seitan in 2025, highlighting the depth of demand for established non-meat protein formats, according to the PBFA. Growth in repeat purchases of plant-based seafood alternatives further indicates that Western demand is expanding across multiple protein formats. This trend reinforces the West’s role not only as a demand center but also as a proving ground for higher-value and newer ingredient systems before they scale nationally.

The Midwest is the key production base in the United States alternative protein ingredients market and provides the clearest signal that demand is expanding beyond the original coastal centers. The draft noted that extrusion capacity is concentrated in states such as Illinois, Iowa, Minnesota, and Nebraska, linking regional strength directly to raw material access and established processing corridors. The Midwest is expected to be the only United States region to record plant-based food sales growth in 2025, at 2.4% year over year, while household penetration is expected to rise by 2.7% during the same period, according to the PBFA. Nebraska and North Dakota are also expected to post plant-based dairy household penetration growth of 11.7% and 10.2%, respectively, suggesting that product adoption is reaching more mainstream retail territories, according to the PBFA. This combination of demand growth and processing proximity gives Midwest-based suppliers a practical cost advantage in serving domestic food and beverage buyers.

The South is expected to account for 36% of the total United States plant-based food spending in 2025, making it the largest regional spending base in the country, according to the PBFA. The draft also showed 23.8 million dairy alternative purchasers in the South, far above the 5.2 million plant-based meat shoppers in the region, indicating that dairy-format demand is the main volume engine there, according to the PBFA. The Northeast is smaller in absolute scale, but it remains important for premium applications, where repeat purchases and specialty functionality carry greater value. Plant-based cheese repeat purchase rates are expected to rise by 7.6% in 2025, while plant-based seafood alternatives are expected to post 31.1% dollar growth, supporting stronger demand for specialized protein systems in the region, according to the PBFA.

Competitive Landscape

The US alternative protein ingredients market is moderately consolidated at the commodity layer, where ADM, Cargill, and Roquette stand out by combining protein processing scale with broad customer access. ADM benefits from its large Midwest infrastructure and broad protein portfolio, while Cargill maintains a strong position through its ingredient network and agricultural sourcing reach. Roquette holds a distinct position as it has advanced further into non-GMO and alternative plant sources, such as pea and fava, helping it serve brands seeking allergen and label differentiation. As a result, the leading tier comprises companies that can simultaneously provide supply reliability, technical service, and broad commercial scale.

The specialty layer of the US alternative protein ingredients market is more diverse, with companies such as Perfect Day, The EVERY Company, and Geltor focusing on narrower protein propositions. These companies compete through proprietary biology, product fit, and the ability to support higher-value formulations that large commodity systems do not always address, rather than through sheer capacity. The competitive gap between commodity concentrates and premium fermentation-derived proteins also creates opportunities for suppliers that can offer clean-label, non-soy, and non-GMO formats at better economics than the most specialized ingredients. In this context, competition depends not only on scale but also on where each supplier positions itself on the cost-functionality curve. The market remains active as buyers seek more options, though most still require ingredients that can move quickly from pilot work to reliable commercial supply.

Recent strategic moves indicate how leading players are positioning themselves to balance functionality and scale. ADM is expected to launch eight new soy and pea protein solutions in May 2026, including ProFam 883 and ProFam 894 soy protein isolates for dairy alternatives and beverages, along with allergen-free pea flour for baked goods and batters. Roquette is expected to expand its textured protein line in June 2025 with NUTRALYS T WHEAT 600L and NUTRALYS T PEA 700XC, supporting manufacturers seeking non-soy or alternative texturizing systems. Geltor’s PrimaColl also demonstrates how specialty firms are using a single regulatory pathway to support both nutrition and beauty applications, broadening the commercial return on one protein platform. These developments suggest that companies able to combine functional precision with dependable scale, rather than relying on novelty alone, will shape the next stage of the US alternative protein ingredients market.

United States Alternative Protein Ingredients Industry Leaders

Archer Daniels Midland Company

Cargill, Incorporated

Roquette Frères

Ingredion Incorporated

Kerry Group plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: ADM launched 8 new soy and pea protein solutions in North America and Europe, including the ProFam 883 and ProFam 894 soy protein isolates for dairy alternatives and beverages, and allergen-free pea flour for baked goods and batters. The move signals ADM's strategic push from commodity TVP toward high-functionality isolates, directly competing in segments previously dominated by specialty ingredient houses.

- June 2025: Roquette expanded its NUTRALYS portfolio with two new textured proteins: NUTRALYS T WHEAT 600L (its first textured wheat protein) and NUTRALYS T PEA 700XC. Both target manufacturers are seeking non-soy texturants for plant-based meat alternatives and sustainable nutrition applications.

- November 2024: Ingredion and Lantmännen entered a strategic long-term partnership for pea protein development. Lantmännen is committed to investing more than EUR 100 million in a state-of-the-art pea protein isolate factory in Sweden, with construction expected to be completed in 2027.

United States Alternative Protein Ingredients Market Report Scope

Alternative protein ingredients refer to any non-traditional, macro-nutrient-rich food components sourced from plants, fungi, microorganisms, insects, or animal tissue cultures. The United States alternative protein ingredients market is segmented by source, form, production technology, and application. By Source, the market is segmented into plant proteins and microbial proteins. The plant proteins segment is further sub-segmented into soy protein, wheat, pea, rice, hemp, and others. Similarly, the Microbial proteins segment is further sub-segmented into mycoprotein, algae protein, and insect proteins. The insect proteins segment is further sub-segmented into cricket, black soldier fly larvae (bsfl), and others. By form, the market is segmented into protein isolates, protein concentrates, textured proteins and TVP, and hydrolysates and peptides. By production technology, the market is segmented into dry and wet fractionation, extrusion and texturization, precision fermentation, and cellular agriculture (scaffold-based, suspension). By application, the market is segmented into food and beverage, dietary supplements and sports nutrition, animal feed and pet food, and personal care and cosmetics. The food and beverage segment is further sub-segmented into bakery, beverages, dairy and dairy alternative products, meat/poultry/seafood and meat alternative products, snacks, and others. The Market Forecasts are Provided in Terms of Value (USD).

| Plant Proteins | Soy Protein | |

| Wheat | ||

| Pea | ||

| Rice | ||

| Hemp | ||

| Others | ||

| Microbial Proteins | Mycoprotein | |

| Algae Protein | ||

| Insect Proteins | Cricket | |

| Black Soldier Fly Larvae (BSFL) | ||

| Others | ||

| Protein Isolates |

| Protein Concentrates |

| Textured Proteins and TVP |

| Hydrolysates and Peptides |

| Dry and Wet Fractionation |

| Extrusion and Texturization |

| Precision Fermentation |

| Cellular Agriculture (Scaffold-Based, Suspension) |

| Food and Beverage | Bakery |

| Beverages | |

| Dairy and Dairy Alternative Products | |

| Meat/Poultry/Seafood and Meat Alternative Products | |

| Snacks | |

| Others | |

| Dietary Supplements and Sports Nutrition | |

| Animal Feed and Pet Food | |

| Personal Care and Cosmetics |

| Source | Plant Proteins | Soy Protein | |

| Wheat | |||

| Pea | |||

| Rice | |||

| Hemp | |||

| Others | |||

| Microbial Proteins | Mycoprotein | ||

| Algae Protein | |||

| Insect Proteins | Cricket | ||

| Black Soldier Fly Larvae (BSFL) | |||

| Others | |||

| Form | Protein Isolates | ||

| Protein Concentrates | |||

| Textured Proteins and TVP | |||

| Hydrolysates and Peptides | |||

| Production Technology | Dry and Wet Fractionation | ||

| Extrusion and Texturization | |||

| Precision Fermentation | |||

| Cellular Agriculture (Scaffold-Based, Suspension) | |||

| Application | Food and Beverage | Bakery | |

| Beverages | |||

| Dairy and Dairy Alternative Products | |||

| Meat/Poultry/Seafood and Meat Alternative Products | |||

| Snacks | |||

| Others | |||

| Dietary Supplements and Sports Nutrition | |||

| Animal Feed and Pet Food | |||

| Personal Care and Cosmetics | |||

Key Questions Answered in the Report

What is the 2026 value of the US alternative protein ingredients space?

The US alternative protein ingredients market was estimated at USD 4.9 billion in 2026 and is projected to reach USD 6.39 billion by 2031 at a 5.56% CAGR.

Which source category leads current demand?

Plant proteins lead the source mix with 87.94% share in 2025 because soy and pea already have the strongest commercial infrastructure and the widest application base.

Which application is growing the fastest through 2031?

Dietary supplements and sports nutrition are the fastest-growing applications, with a projected 7.83% CAGR through 2031, supported by demand for high-purity and premium protein formats.

Why are textured proteins gaining traction faster than some other forms?

Textured proteins and TVP are projected to grow at 8.01% through 2031 because improved extrusion performance is helping manufacturers deliver more meat-like structure in foodservice and retail products.

Page last updated on: