Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

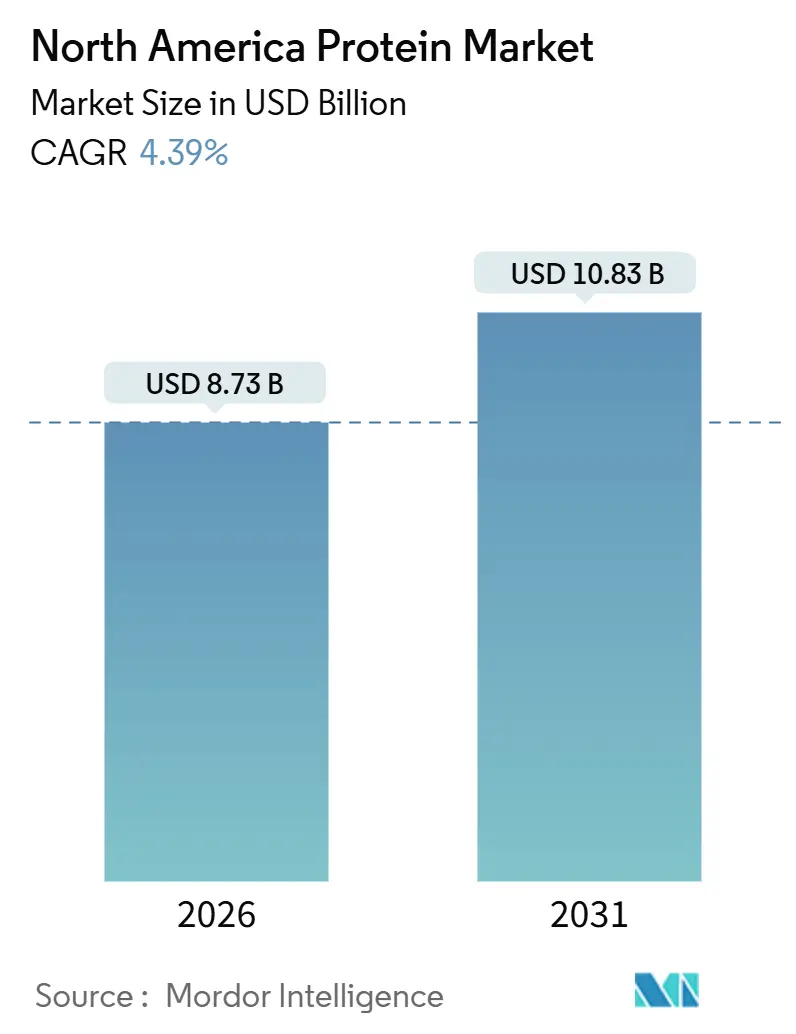

| Market Size (2026) | USD 8.73 Billion |

| Market Size (2031) | USD 10.83 Billion |

| Growth Rate (2026 - 2031) | 4.39% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Protein Market Analysis by Mordor Intelligence

The North America protein market size is valued to be USD 8.73 billion in 2026 and is projected to climb to USD 10.83 billion by 2031, translating into a 4.39% CAGR for the forecast period. Steady growth is now tied less to sheer tonnage and more to premiumization strategies that pair high DIAAS scores with clean-label claims coveted by retailers and food-service buyers. The 2025 Dietary Guidelines Advisory Committee’s shift toward amino-acid digestibility elevates the value of ingredients that demonstrate superior ileal absorption, opening pricing headroom for suppliers that can validate functionality through clinical work. Subsidies embedded in the 2025 Farm Bill have lowered domestic pea and hemp feedstock costs, thereby narrowing the historical price gap with Asian isolates and encouraging localized sourcing for United States and Canadian processors. Precision-fermented proteins are gaining regulatory traction after Health Canada approved β-lactoglobulin from yeast and Fy Protein, which has emboldened venture capital to target fermentation capacity across Ontario and Québec. At the same time, anti-dumping measures on high-protein pea imports are rerouting demand toward regional crush facilities, boosting Midwest and Prairie processing margins while tightening off-shore formulation options.

Key Report Takeaways

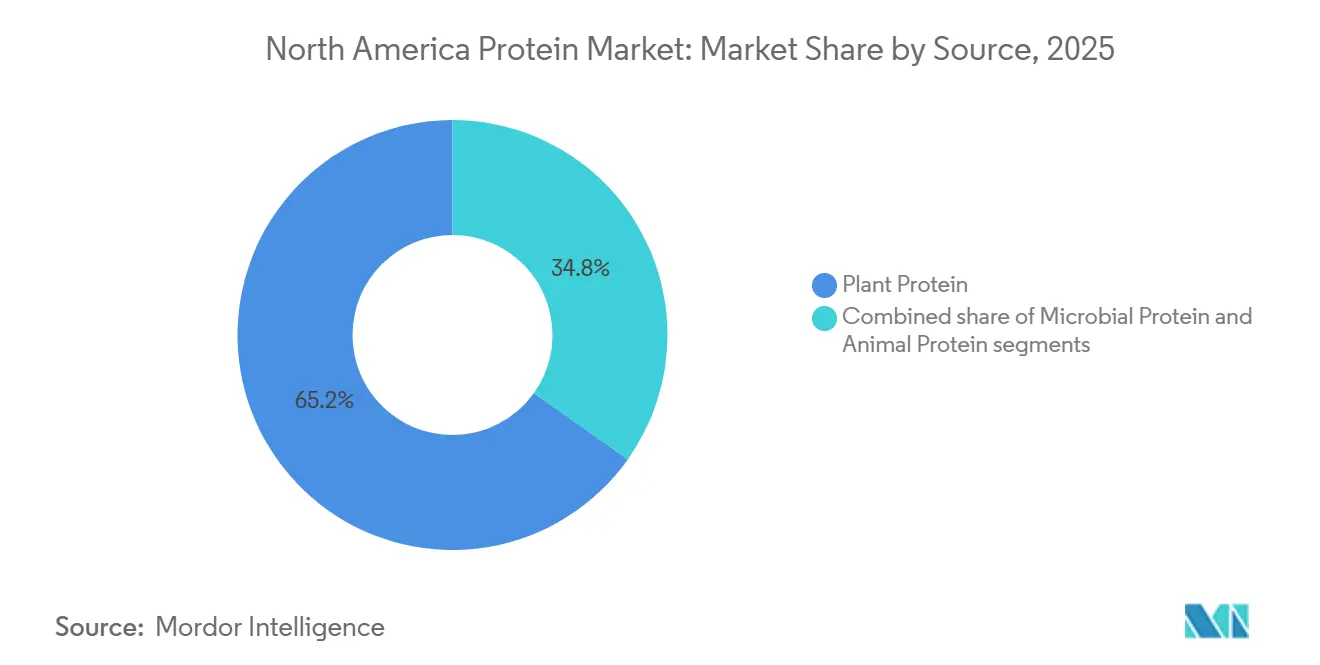

- By source, plant-based proteins led with 65.17% revenue share in 2025, while microbial proteins are forecast to expand at a 6.35% CAGR through 2031.

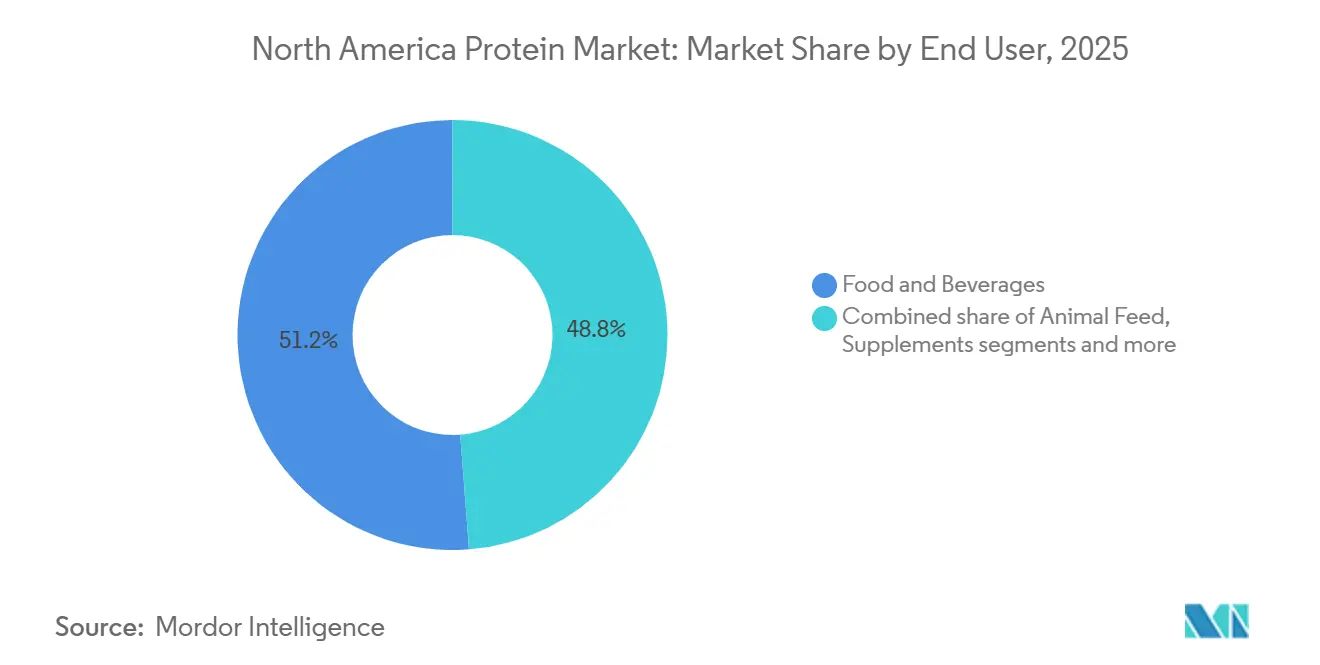

- By end user, food and beverages absorbed 51.23% of ingredient volumes in 2025, whereas personal care and cosmetics applications are advancing at a 6.16% CAGR through 2031.

- By country, the United States captured 81.49% of the North American protein market share in 2025, while Mexico is projected to post the highest 6.54% CAGR over the same horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Protein Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand for plant-based and vegan alternatives grows due to dietary shifts toward flexitarian lifestyles | +1.2% | United States, Canada, urban Mexico | Medium term (2–4 years) |

| Sports and performance-nutrition boom | +0.9% | United States, Canada | Short term (≤ 2 years) |

| Protein fortification of mainstream food and beverage products | +0.7% | North America-wide | Medium term (2–4 years) |

| Clean-label trends favor natural, non-GMO proteins amid awareness of GMOs' potential harms | +0.6% | United States, Canada | Long term (≥ 4 years) |

| US Farm Bill 2025 incentives for domestic pea and hemp processing | +0.5% | United States (Midwest, Northern Plains) | Medium term (2–4 years) |

| Sustainability preferences for eco-friendly proteins like insect or algae support ethical sourcing | +0.4% | United States, Canada | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Demand for plant-based and vegan alternatives grows due to dietary shifts toward flexitarian lifestyles

Shifting dietary preferences toward flexitarian lifestyles are driving the demand for plant-based and vegan alternatives, as consumers increasingly integrate animal and plant proteins for health and ethical considerations. This shift supports clean-label trends favoring natural, non-GMO options, with companies like Archer Daniels Midland Company (ADM) enhancing pea and soy isolates for food applications to address these needs. Rising health consciousness further propels this demand, as plant proteins provide digestible alternatives to animal sources, aiding muscle repair and immunity. Innovations in taste and texture, such as Roquette Frères' advancements in pea protein, are overcoming previous barriers to consumer acceptance. Data from The Good Food Institute and the Plant Based Foods Association indicate that 6 in 10 or 59% of United States households purchased plant-based foods in 2024, showcasing adoption beyond strictly vegan consumers [1]Source: The Good Food Institute, "U.S. Retail Market Insights for the Plant-Based Industry," gfi.org. Additionally, sustainability preferences for eco-friendly sourcing, increased demand for sports nutrition, and regulatory approvals for novel ingredients are shaping the market. Manufacturers like Ingredion Incorporated are meeting these requirements by supplying allergen-free plant proteins that cater to aging populations and the expanding e-commerce market. These factors collectively drive growth in non-overlapping segments like food and beverages, independent of broader economic conditions.

Sports and performance-nutrition boom

The increasing focus on fitness and gym culture, along with the expansion of sports nutrition, including personalized protein blends, is driving the demand for high-quality proteins that support muscle recovery and performance enhancement. This trend reflects growing health consciousness, with consumers prioritizing muscle repair and immunity. Athletes are increasingly opting for whey and plant-based protein options, while manufacturers such as Glanbia PLC are addressing market needs through innovations in taste, texture, and digestibility, including specialized whey protein isolates for performance formulations. According to the Bureau of Labor Statistics, 21.5% of adults in the United States participated in sports, exercise, and recreational activities daily in 2024, up from 20.1% in 2022, highlighting increased engagement beyond casual fitness [2]Source: Bureau of Labor Statistics, "American Time Use Survey - 2024 Results," bls.gov . Furthermore, clean-label trends, such as non-GMO proteins, support for healthy aging through sarcopenia prevention, the rising demand for plant-based alternatives in flexitarian diets, sustainability considerations, e-commerce accessibility, and regulatory approvals for novel protein blends, are shaping the market. These factors enable diverse applications, such as nutritional supplements, without creating economic dependencies.

Protein fortification of mainstream food and beverage products

Protein fortification is gaining momentum across mainstream categories, with bakery, snack, and beverage manufacturers projected to fortify an additional 8% of product SKUs with protein isolates or concentrates between 2024 and 2025. This growth is fueled by consumer willingness to pay 15-20% premiums for products positioned for satiety and muscle health, reflecting increasing health consciousness related to muscle repair and weight management. The trend is supported by innovations in taste and texture, such as functional whey and plant protein concentrates supplied by Fonterra Co-operative Group for bakery applications, and aligns with the rising fitness culture and demand for sports nutrition products that enhance fortified everyday foods. Furthermore, it is linked to clean-label preferences for natural, non-GMO options, the shift toward plant-based and flexitarian diets, support for healthy aging to combat sarcopenia, sustainability considerations, e-commerce growth, and regulatory approvals for novel fortificants. A 2024 survey by the International Food Information Council (IFIC) revealed that 71% of Americans are actively trying to consume more protein, up from 59% in 2022 [3]Source: International Food Information Council (IFIC), "2024 IFIC Food & Health Survey," ific.org. This growing demand is driving diverse food and beverage applications, reducing reliance on overlapping product categories within the market.

Clean-label trends favor natural, non-GMO proteins amid awareness of GMOs' potential harms

Clean-label trends are driving the demand for natural, non-GMO proteins, fueled by increasing awareness of potential health risks associated with GMOs and a growing focus on health-conscious choices. Consumers are prioritizing minimally processed protein sources for muscle repair, weight management, and immunity enhancement, avoiding synthetic additives to support overall wellness. Product innovations are addressing these needs by improving taste and texture, with companies like Cargill Incorporated offering non-GMO pea and soy protein isolates for clean-label formulations in food applications. This trend aligns with the expanding fitness culture and the growth of sports nutrition, where performance blends emphasize purity. Additionally, the rising demand for plant-based vegan alternatives reflects the shift toward flexitarian diets, while protein fortification in bakery, snacks, and beverages caters to satiety needs and supports healthy aging by addressing sarcopenia with digestible options. Sustainability preferences are also influencing the adoption of eco-friendly protein sources, such as algae and insect proteins. E-commerce growth has enabled greater access to transparent labeling, and regulatory approvals for novel clean ingredients are further supporting market expansion. These factors collectively drive growth across non-overlapping segments, including food and beverages and supplements, as consumers increasingly seek verifiable natural protein options to mitigate health risks associated with GMOs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production costs for plant-based and alternative proteins limit affordability compared to animal sources | -0.8% | North America-wide, acute in specialty proteins | Short term (≤ 2 years) |

| Allergenicity concerns with certain proteins (e.g., soy, dairy) restrict usage | -0.3% | United States, Canada, select urban Mexico | Medium term (2–4 years) |

| Supply chain disruptions from raw material volatility affect availability of specialty ingredients | -0.4% | United States (Midwest), Canada (Prairies), Mexico | Short term (≤ 2 years) |

| Stringent regulations on labeling, claims, and novel foods delay product launches | -0.5% | United States (FDA), Canada (Health Canada) | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High production costs for plant-based and alternative proteins limit affordability compared to animal sources

High production costs for plant-based and alternative proteins limit their affordability compared to animal-based proteins, with supply chain disruptions caused by raw material price volatility further hindering the scaling of specialty ingredients required for diverse applications. These challenges are compounded by processing difficulties in achieving desirable taste and texture, leading to elevated expenses for manufacturers such as PURIS, which faces high costs in producing pea protein concentrates despite innovations aimed at improving functionality. This directly impacts product development efforts that could enhance consumer acceptance in mainstream categories. Additionally, consumer misconceptions regarding the quality and digestibility of plant-based proteins slow adoption, even as demand grows for clean-label, natural, and non-GMO options. While flexitarian diets and vegan alternatives are gaining traction, these trends intersect with other market drivers, such as increasing health consciousness, the need for muscle repair, the rise of fitness culture, the expansion of sports nutrition, protein fortification in bakery and snack products, support for healthy aging, sustainability preferences for eco-friendly sourcing, the growth of e-commerce, and regulatory approvals for novel proteins. Collectively, these factors constrain growth in non-overlapping segments such as food and beverages and supplements, in a market still dominated by cost-competitive animal proteins.

Allergenicity concerns with certain proteins (e.g., soy, dairy) restrict usage

Allergenicity concerns surrounding soy and dairy proteins continue to limit their usage, as food manufacturers increasingly prioritize clean-label, hypoallergenic formulations to meet consumer demand. The rising awareness of lactose intolerance, milk protein allergies, and soy sensitivities has driven brands to reformulate products or reduce reliance on these traditional protein sources, creating formulation challenges in bakery, beverage, and nutrition applications where these proteins have historically been dominant. Ingredient suppliers, such as Archer Daniels Midland Company (soy protein isolates) and Arla Foods Ingredients (whey and milk proteins), are facing growing substitution pressures from emerging alternatives like pea, fava bean, and rice proteins. Regulatory labeling requirements further add to reformulation costs and complexity, extending product development cycles and delaying commercialization. These developments underscore the connection between allergen risk mitigation and sourcing diversification strategies, as manufacturers strive to balance protein functionality with allergen avoidance. Collectively, these factors constrain the growth of soy and dairy proteins, despite the strong overall demand for protein products.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Microbial Platforms Gain Regulatory Traction

Plant proteins represented 65.17% of the market value in 2025, with microbial proteins projected to grow at a compound annual growth rate (CAGR) of 6.35% through 2031, marking the fastest growth among source categories. Pea protein isolates dominate plant-based protein volumes, primarily utilized in meat analogues and dairy alternatives due to their neutral flavor profiles and high solubility. Ingredion's October 2024 launch of dispersibility-enhanced pea protein addresses persistent formulation challenges in ready-to-drink beverages. Soy protein concentrates and isolates maintain cost advantages, supported by USDA data indicating 2024 soybean production reached 4.37 billion bushels, a 5% year-over-year increase. However, these proteins face challenges from allergen concerns and non-GMO certification requirements, which increase procurement costs by 10–15%. Hemp protein isolates achieved their first commercial sales in April 2024 through the Burcon-HPS partnership, leveraging USDA hemp production programs that provide federal crop insurance and technical assistance to growers.

Animal-derived proteins, including casein, whey, collagen, gelatin, and egg proteins, are utilized in premium applications where their functional performance justifies higher costs. Whey protein isolates command a 15–20% price premium over concentrates due to lactose removal and higher protein purity (≥90%), attributes leveraged by sports nutrition brands to differentiate their products. Arla Foods Ingredients' February 2025 acquisition of Volac's Whey Nutrition business consolidates supply in a segment where three suppliers control approximately 40% of North American whey isolate capacity, raising concerns about pricing power and customer dependency. Moreover, microbial proteins, including algae-derived flours and mycoprotein fermentation platforms, offer sustainable, high-quality alternatives to conventional proteins. Suppliers such as AlgaVia (by Corbion) and Marlow Foods are advancing these segments as brands and manufacturers shift toward novel, sustainable proteins that align with evolving consumer and regulatory expectations.

By End User: Personal Care Emerges as High-Margin Outlet

The food and beverages segment accounted for 51.23% of ingredient volumes in 2025, with personal care and cosmetics applications projected to grow at an annual rate of 6.16% through 2031, marking the fastest growth among end-user segments. Within food and beverages, dairy and dairy alternatives represent the largest sub-segment, driven by reformulations of Greek yogurt and the fortification of plant-based milk, requiring 8 to 12 grams of protein per serving to match the nutritional profile of bovine milk. Meat, poultry, seafood, and their alternatives utilize textured vegetable proteins and isolates to replicate fibrous structures similar to whole-muscle cuts. Bakery and snack manufacturers increased protein inclusion rates between 2024 and 2025 to meet consumer demand for satiety-enhancing products that support premium pricing. Ready-to-drink protein shakes and fortified coffee in the beverages category face technical challenges related to heat stability and pH sensitivity, limiting protein source options to highly soluble isolates.

Supplements, including sports and dietary supplements, baby food and infant formula, and elderly and medical nutrition, rely on specific protein types to meet regulatory and functional requirements. Sports supplements prioritize whey isolates and hydrolysates for rapid absorption, while infant formula regulations favor dairy-based proteins due to their established safety profiles. Personal care and cosmetics applications, growing at a 6.16% CAGR, utilize collagen peptides, keratin hydrolysates, and silk proteins for bioavailability and structural reinforcement in hair care, skin care, and color cosmetics. Meanwhile, animal feed remains a significant outlet for lower-grade protein meals and co-products, though its growth is slower as livestock producers optimize feed conversion ratios and adopt synthetic amino acids.

Geography Analysis

The United States is projected to account for 81.49% of North America's protein market revenue in 2025. This leadership is driven by vertically integrated supply chains that span Midwest crop production, crushing, fractionation, and extrusion processes, ensuring efficient just-in-time delivery to food manufacturers. The growing focus on health consciousness, particularly for muscle repair and fitness, further supports this dominance. Streamlined operations, such as Archer Daniels Midland's August 2025 soy protein network rationalization, consolidate high-efficiency plants to meet the demand for clean-label, non-GMO proteins, aligning with the shift toward flexitarian diets. Additionally, FDA enforcement of Current Good Manufacturing Practices (CGMP) under 21 CFR Part 110 enhances sanitation, allergen control, and traceability, giving domestic suppliers a competitive edge over offshore competitors and fostering product innovations in sports nutrition and bakery/snack fortification.

Mexico is anticipated to grow at a compound annual growth rate (CAGR) of 6.54% through 2031, making it the fastest-growing national segment in the region. This growth is driven by increased consumption of fortified bakery products, ready-to-drink beverages, and processed meats, which utilize protein isolates for improved nutrition and texture. Manufacturers like Bunge North America are addressing allergen-friendly applications by supplying pea protein hydrolysates, balancing high production costs with clean-label demands and e-commerce accessibility. The expansion of sports nutrition and products supporting healthy aging further contributes to this growth.

Canada plays a strategically significant role in the protein market, supported by federal initiatives for plant-protein processing and expedited approvals for novel food products. The country's contribution aligns with clean-label, non-GMO trends and sustainability efforts, including the development of eco-friendly algae proteins by suppliers such as Merit Functional Foods. These innovations address allergenicity concerns and processing challenges related to taste in supplements, catering to flexitarian demands and fitness-focused blends. Robust agricultural practices mitigate climate-related yield impacts, while e-commerce growth further strengthens Canada's position as a premium source of protein products. This complements the United States' efficiency and Mexico's consumption-driven growth in a market increasingly focused on traceability and health-oriented products.

Competitive Landscape

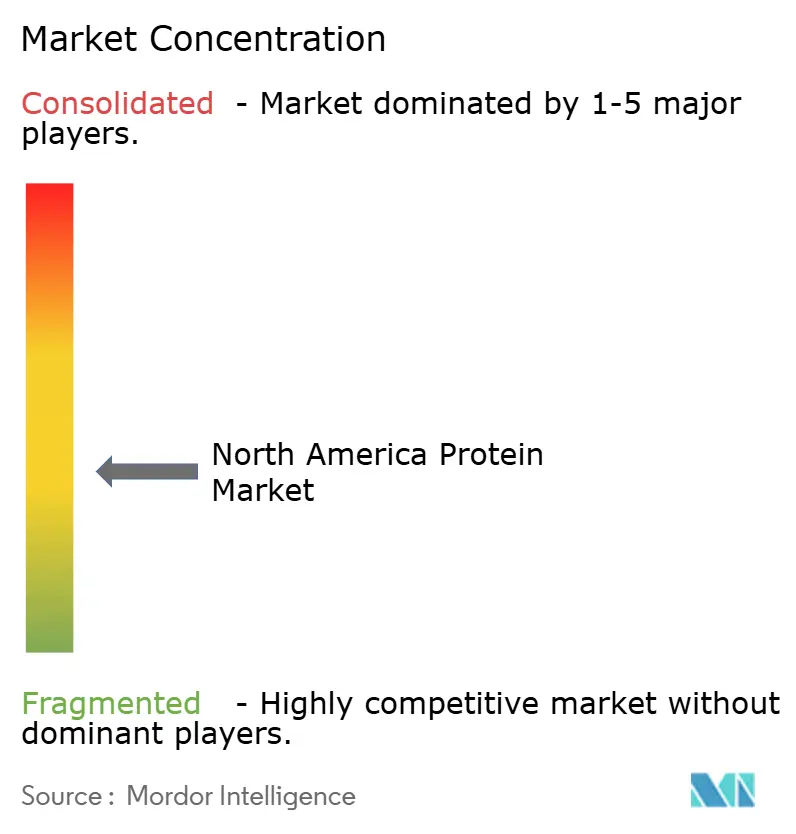

The competitive landscape reflects moderate fragmentation, with established multinational processors and emerging specialized players competing for market share. Prominent ingredient manufacturers, including Archer Daniels Midland and Cargill, utilize extensive production capabilities and diverse product portfolios spanning soy, wheat, and pea proteins to cater to various food and beverage segments. These established companies benefit from integrated supply chains and long-term customer relationships, enabling them to remain competitive even as consumer demand shifts toward alternative protein sources.

Nutrition-focused companies such as Glanbia and Kerry Group bring significant expertise in applications, particularly in sports nutrition and functional food formulations. Their ability to tailor whey, milk, and plant-based protein isolates to meet specific end-use requirements highlights the importance of performance-driven ingredients. This capability positions them as preferred partners for brands seeking high-quality products and technical support in product development.

Specialized entrants focusing on algae, insect, and fermentation-derived proteins are transforming the competitive landscape by addressing sustainability and emerging nutrition trends. Companies like Arbiom, with its fermentation-based protein ingredients, and Allmicroalgae, which produces algal protein solutions, are gaining traction among formulators seeking innovative and eco-conscious alternatives. The coexistence of traditional industry leaders and niche innovators demonstrates how the market balances scale, functionality, and evolving consumer preferences.

North America Protein Industry Leaders

-

Archer Daniels Midland Company

-

Bunge Limited

-

Kerry Group PLC

-

Cargill Incorporated

-

Roquette Frères

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Burcon NutraScience Corp. completed its first commercial sale of Puratein C, a canola protein isolate. Derived from non-GMO canola seeds cultivated in North America, Puratein C contained all nine essential amino acids and achieved a protein digestibility-corrected amino acid score (PDCAAS) of 1.0. Its potential applications included baked goods, dairy alternatives, ready-to-drink beverages, meat substitutes, and sauces.

- March 2025: Arla Foods Ingredients entered into a contract manufacturing agreement with Valley Queen to enhance its production capacity and address the increasing demand for protein-enriched dairy products in the United States. Based in South Dakota, Valley Queen manufactures ingredients from the Nutrilac ProteinBoost range. This patented microparticulate whey protein concentrate was designed to boost protein content in food and beverages while maintaining their texture and taste.

- March 2025: Vivici, a Dutch ingredients startup, introduced ViviteinTM BLG to the United States market. As the flagship ingredient within its ViviteinTM protein platform, ViviteinTM BLG became available, enabling B2B customers to develop innovative and distinctive products for consumers in the United States.

North America Protein Market Report Scope

Animal, Microbial, Plant are covered as segments by Source. Animal Feed, Food and Beverages, Personal Care and Cosmetics, Supplements are covered as segments by End User. Canada, Mexico, United States are covered as segments by Country.

By Source

| Animal | Casein and Caseinates |

| Collagen | |

| Egg Protein | |

| Gelatin | |

| Insect Protein | |

| Milk Protein | |

| Whey Protein | |

| Other Animal Protein | |

| Microbial | Algae Protein |

| Mycoprotein | |

| Plant | Hemp Protein |

| Pea Protein | |

| Potato Protein | |

| Rice Protein | |

| Soy Protein | |

| Wheat Protein | |

| Other Plant Protein |

By End User

| Animal Feed | |

| Food and Beverages | Bakery |

| Beverages | |

| Breakfast Cereals | |

| Condiments/Sauces | |

| Confectionery | |

| Dairy and Dairy Alternatives | |

| Meat/Poultry/Seafood and Alternatives | |

| RTE/RTC Foods | |

| Snacks | |

| Personal Care and Cosmetics | |

| Supplements | Baby Food and Infant Formula |

| Elderly and Medical Nutrition | |

| Sport and Dietary Supplements |

By Country

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Source | Animal | Casein and Caseinates |

| Collagen | ||

| Egg Protein | ||

| Gelatin | ||

| Insect Protein | ||

| Milk Protein | ||

| Whey Protein | ||

| Other Animal Protein | ||

| Microbial | Algae Protein | |

| Mycoprotein | ||

| Plant | Hemp Protein | |

| Pea Protein | ||

| Potato Protein | ||

| Rice Protein | ||

| Soy Protein | ||

| Wheat Protein | ||

| Other Plant Protein | ||

| By End User | Animal Feed | |

| Food and Beverages | Bakery | |

| Beverages | ||

| Breakfast Cereals | ||

| Condiments/Sauces | ||

| Confectionery | ||

| Dairy and Dairy Alternatives | ||

| Meat/Poultry/Seafood and Alternatives | ||

| RTE/RTC Foods | ||

| Snacks | ||

| Personal Care and Cosmetics | ||

| Supplements | Baby Food and Infant Formula | |

| Elderly and Medical Nutrition | ||

| Sport and Dietary Supplements | ||

| By Country | United States | |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

Market Definition

- End User - The Protein Ingredients Market operates on a B2B basis. Food, Beverages, Supplements, Animal Feed, and Personal Care & Cosmetic manufacturers are considered to be end-consumers in the market studied. The scope excludes manufacturers buying liquid/dry whey to be used for application as a binding agent or thickener or other non-protein applications.

- Penetration Rate - Penetration Rate is defined as the percentage of Protein-Fortified End User Market Volume in the Overall End User Market Volume.

- Average Protein Content - Average protein content is the average protein content present per 100 g of product manufactured by all end-user companies considered under the scope of this report.

- End User Market Volume - End-user market volume is the consolidated volume of all types and forms of end-user products in the country or region.

| Keyword | Definition |

|---|---|

| Alpha-lactalbumin (α-Lactalbumin) | It is a protein that regulates the production of lactose in the milk of almost all mammalian species. |

| Amino acid | It is an organic compound that contains both amino and carboxylic acid functional groups, which are required for the synthesis of body protein and other important nitrogen-containing compounds, such as creatine, peptide hormones, and some neurotransmitters. |

| Blanching | It is the process of briefly heating vegetables with steam or boiling water. |

| BRC | British Retail Consortium |

| Bread improver | It is a flour-based blend of several components with specific functional properties designed to modify dough characteristics and give quality attributes to bread. |

| BSF | Black Soldier Fly |

| Caseinate | It is a substance produced by adding an alkali to acid casein, a derivative of casein. |

| Celiac disease | Celiac disease is an immune reaction to eating gluten, a protein found in wheat, barley, and rye. |

| Colostrum | It is a milky fluid that’s released by mammals that have recently given birth before breast milk production begins. |

| Concentrate | It is the least processed form of protein and has a protein content ranging from 40-90% by weight. |

| Dry protein basis | It refers to the percentage of "pure protein" present in a supplement after the water in it is completely removed through heat. |

| Dry whey | It is the product resulting from drying fresh whey which has been pasteurized and to which nothing has been added as a preservative. |

| Egg protein | It is a mixture of individual proteins, including ovalbumin, ovomucoid, ovoglobulin, conalbumin, vitellin, and vitellenin. |

| Emulsifier | It is a food additive that facilitates the blending of foods that are immiscible with one another, such as oil and water. |

| Enrichment | It is the process of addition of micronutrients that are lost during the processing of the product. |

| ERS | Economic Research Service of the USDA |

| Extrusion | It is the process of forcing soft mixed ingredients through an opening in a perforated plate or die designed to produce the required shape. The extruded food is then cut to a specific size by blades. |

| Fava | Also known as Faba, it is another word for yellow split beans. |

| FDA | Food and Drug Administration |

| Flaking | It is a process in which typically a cereal grain (like corn, wheat, or rice) is broken down into grits, cooked with flavors and syrups, and then pressed into flakes between cooled rollers. |

| Foaming agent | It is a food ingredient that makes it possible to form or maintain a uniform dispersion of a gaseous phase in a liquid or solid food. |

| Foodservice | It refers to the part of the food industry which includes businesses, institutions, and companies which prepare meals outside the home. It includes restaurants, school and hospital cafeterias, catering operations, and many other formats. |

| Fortification | It is the deliberate addition of micronutrients that are not found in them naturally or which are lost during processing, to improve a food product's nutritional value. |

| FSANZ | Food Standards Australia New Zealand |

| FSIS | Food Safety and Inspection Service |

| FSSAI | Food Safety and Standards Authority of India |

| Gelling agent | It is an ingredient that functions as a stabilizer and thickener to provide thickening without stiffness through the formation of gel. |

| GHG | Greenhouse Gas |

| Gluten | It is a family of proteins found in grains, including wheat, rye, spelt, and barley. |

| Hemp | It is a botanical class of Cannabis sativa cultivars grown specifically for industrial or medicinal use. |

| Hydrolysate | It is a form of protein manufactured by exposing the protein to enzymes that can partially break the bonds between the protein's amino acids and break down large, complicated proteins into smaller pieces. Its processing makes it easier and quicker to digest. |

| Hypoallergenic | It refers to a substance that causes fewer allergic reactions. |

| Isolate | It is the purest and most processed form of protein which has undergone separation to obtain a pure protein fraction. It typically contains ≥ 90% of protein by weight. |

| Keratin | It is a protein that helps form hair, nails, and the outer layer of skin. |

| Lactalbumin | It is the albumin contained in milk and obtained from whey. |

| Lactoferrin | It is an iron‑binding glycoprotein that is present in the milk of most mammals. |

| Lupin | It is the yellow legume seeds of the genus Lupinus. |

| Millenial | Also known as Generation Y or Gen Y, it refers to the people born from 1981 to 1996. |

| Monogastric | It refers to an animal with a single-compartmented stomach. Examples of monogastric include humans, poultry, pigs, horses, rabbits, dogs, and cats. Most monogastric are generally unable to digest much cellulose food materials such as grasses. |

| MPC | Milk protein concentrate |

| MPI | Milk protein isolate |

| MSPI | Methylated soy protein isolate |

| Mycoprotein | Mycoprotein is a form of single-cell protein, also known as fungal protein, derived from fungi for human consumption. |

| Nutricosmetics | It is a category of products and ingredients that act as nutritional supplements to care for skin, nails, and hair natural beauty. |

| Osteoporosis | It is a medical condition in which the bones become brittle and fragile from loss of tissue, typically as a result of hormonal changes, or deficiency of calcium or vitamin D. |

| PDCAAS | Protein digestibility-corrected amino acid score (PDCAAS) is a method of evaluating the quality of a protein based on both the amino acid requirements of humans and their ability to digest it. |

| Per-capita consumption of animal protein | It is the average amount of animal protein (such as milk, whey, gelatin, collagen, and egg proteins) that is readily available for consumption by each person in an actual population. |

| Per-capita consumption of plant protein | It is the average amount of plant protein (such as soy, wheat, pea, oat, and hemp proteins) that is readily available for consumption by each person in an actual population. |

| Quorn | It is a microbial protein manufactured using mycoprotein as an ingredient, in which the fungus culture is dried and mixed with egg albumen or potato protein, which acts as a binder, and then is adjusted in texture and pressed into various forms. |

| Ready-to-Cook (RTC) | It refers to food products that include all of the ingredients, where some preparation or cooking is required through a process that is given on the package. |

| Ready-to-Eat (RTE) | It refers to a food product prepared or cooked in advance, with no further cooking or preparation required before being eaten. |

| RTD | Ready-to-Drink |

| RTS | Ready-to-Serve |

| Saturated fat | It is a type of fat in which the fatty acid chains have all single bonds. It is generally considered unhealthy. |

| Sausage | It is a meat product made of finely chopped and seasoned meat, which may be fresh, smoked, or pickled and which is then usually stuffed into a casing. |

| Seitan | It is a plant-based meat substitute made out of wheat gluten. |

| Softgel | It is a gelatin-based capsule with a liquid fill. |

| SPC | Soy protein concentrate |

| SPI | Soy protein isolate |

| Spirulina | It is a biomass of cyanobacteria that can be consumed by humans and animals. |

| Stabilizer | It is an ingredient added to food products to help maintain or enhance their original texture, and physical and chemical characteristics. |

| Supplementation | It is the consumption or provision of concentrated sources of nutrients or other substances that are intended to supplement nutrients in the diet and is intended to correct nutritional deficiencies. |

| Texturant | It is a specific type of food ingredient that is used to control and alter the mouthfeel and texture of food and beverage products. |

| Thickener | It is an ingredient that is used to increase the viscosity of a liquid or dough and make it thicker, without substantially changing its other properties. |

| Trans fat | Also called trans-unsaturated fatty acids or trans fatty acids, it is a type of unsaturated fat that naturally occurs in small amounts in meat. |

| TSP | Textured soy protein |

| TVP | Textured vegetable protein |

| WPC | Whey protein concentrate |

| WPI | Whey protein isolate |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms