Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

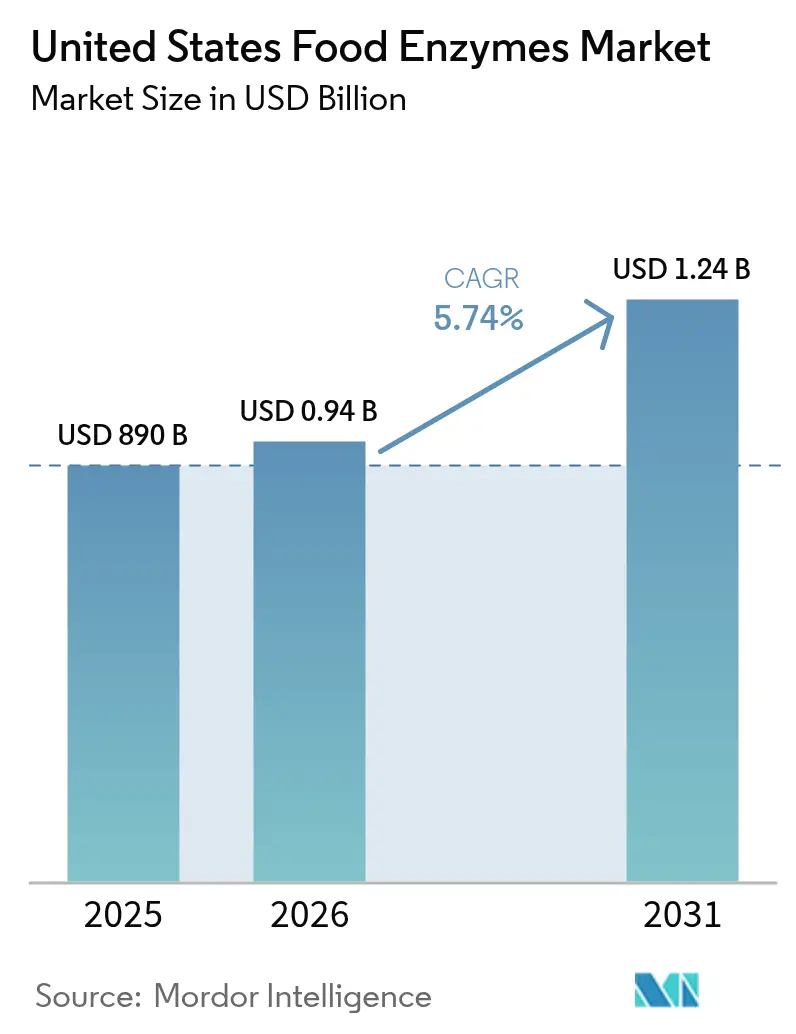

| Base Year Market Size (2025) | USD 890 Billion |

| Market Size (2026) | USD 0.94 Billion |

| Market Size (2031) | USD 1.24 Billion |

| Growth Rate (2026 - 2031) | 5.74% CAGR |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United States Food Enzymes Market Analysis by Mordor Intelligence

The United States food enzymes market size is expected to grow from USD 890 million in 2025 to USD 941.09 million in 2026 and is forecast to reach USD 1.24 billion by 2031 at 5.74% CAGR over 2026-2031. This growth trajectory reflects the sector's maturation beyond basic processing aids toward sophisticated biotechnological solutions that address emerging consumer demands and regulatory pressures. Robust demand for clean-label processing aids, steady modernization of bakery and dairy plants, and stricter sustainability mandates continue to reposition enzymes from cost-saving additives to strategic bioprocessing tools. Manufacturers deploy carbohydrases, proteases, and emerging lipase systems to shorten production cycles, reduce energy use, and achieve label simplification without sacrificing taste or safety. On the demand side, specialty nutrition, plant-based alternatives, and functional food launches present fresh revenue streams, while renewed focus on supply-chain resilience is accelerating domestic enzyme capacity investments.

Key Report Takeaways

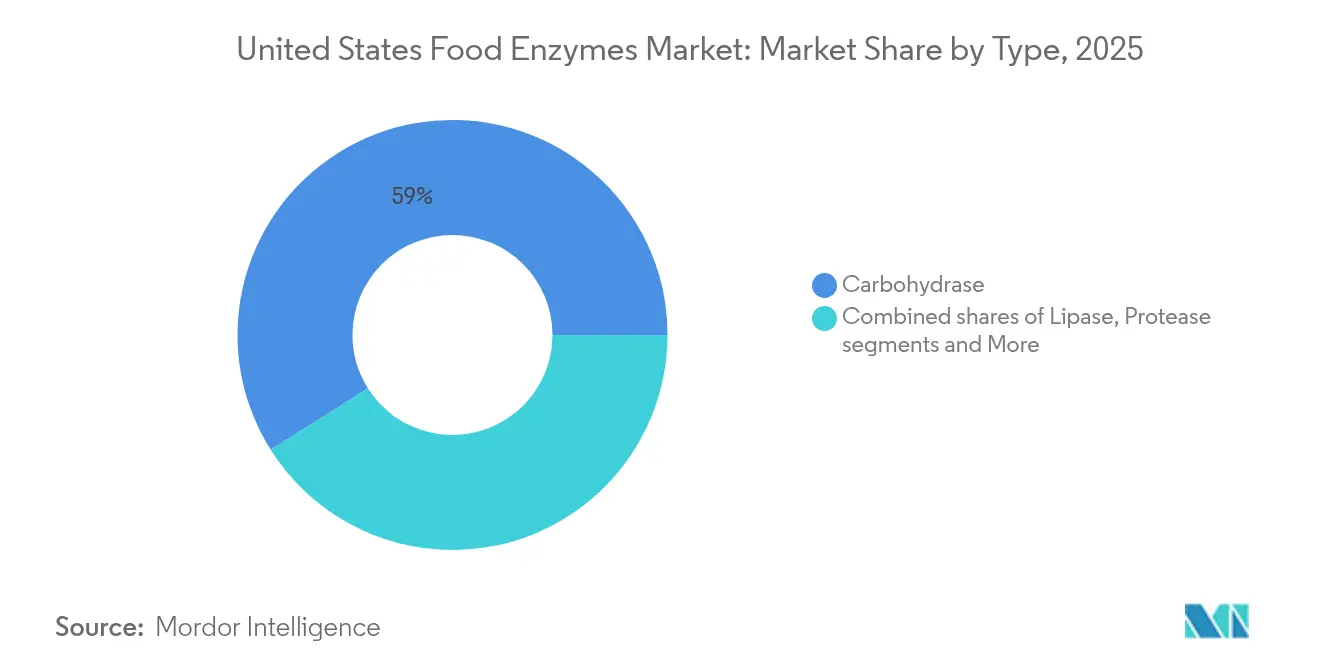

- By type, carbohydrase commanded 58.96% of the food enzymes market size in 2025; the lipase segment is advancing at a 6.42% CAGR through 2031.

- By form, powder formats accounted for 64.55% of the food enzymes market size in 2025 and are expanding at a 6.51% CAGR to 2031.

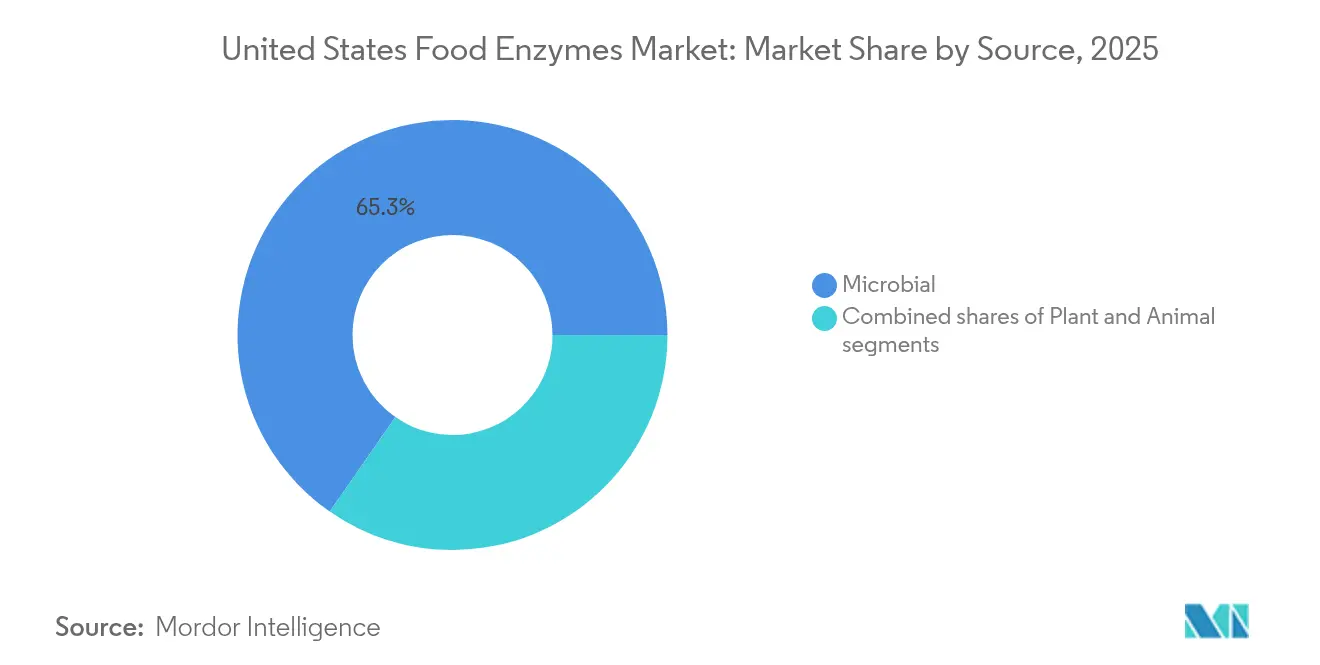

- By source, microbial systems led with 65.33% revenue share in 2025, while plant-derived alternatives are set to grow at a 6.67% CAGR.

- By application, bakery and confectionery commanded 29.74% of the food enzymes market size in 2025; the dairy and desserts segment is advancing at a 6.95% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Food Enzymes Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Expansion of functional and fortified food segment | +1.2% | National, concentrated in health-conscious metropolitan areas | Medium term (2-4 years) |

| Strong growth in the United States baking industry | +0.9% | National, with strength in Midwest grain belt regions | Short term (≤ 2 years) |

| Rising trend of plant-based and vegan food products | +1.4% | National, led by West Coast and Northeast markets | Medium term (2-4 years) |

| Growing demand for processed and packaged food products | +0.8% | National, driven by convenience-focused demographics | Short term (≤ 2 years) |

| Boom in craft beer and artisanal food sector | +0.6% | Regional, concentrated in urban craft brewing hubs | Long term (≥ 4 years) |

| Advancement in microbial and genetically modified enzymes | +1.0% | National, with regulatory advantages in biotechnology clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of functional and fortified food segment

Consumer demand for health-optimized food products has created substantial opportunities for specialized enzyme applications that enhance nutrient bioavailability and create novel functional properties. The FDA's approval of alpha-galactosidase from genetically modified Saccharomyces cerevisiae for guar gum processing demonstrates regulatory acceptance of advanced enzyme technologies in functional food production according to the European Food Safety Authority[1].European Food Safety Authority, "Safety evaluation of the food enzyme α‐galactosidase", www.efsa.europa.euFurther, Amplifye's launch of the P24 protease enzyme, which increases amino acid absorption by approximately 30% and targets improved blood glucose control, exemplifies how enzyme innovation is addressing specific health outcomes rather than general processing efficiency. This shift toward therapeutic-adjacent applications positions enzymes as active ingredients rather than passive processing aids, justifying premium pricing and creating differentiated market positions.

Strong growth in the United States baking industry

The United States baking sector's resilience during economic uncertainty has created sustained demand for enzyme solutions that optimize production efficiency and product quality. Enzyme applications in baking have evolved beyond traditional amylase use toward specialized solutions for clean-label formulations and extended shelf life, addressing consumer preferences for recognizable ingredients without sacrificing product performance. The industry's focus on automation creates opportunities for enzyme systems that reduce variability and enable consistent quality across different production environments. Rising input costs and labor shortages have made enzyme-enabled process optimization essential for maintaining profitability, particularly for mid-tier operators competing against both artisanal producers and large-scale manufacturers.

Rising trend of plant-based and vegan food products

Plant-based food production requires sophisticated enzyme solutions to overcome inherent challenges in texture, flavor, and nutritional profile that distinguish these products from animal-derived alternatives. The development of specialized enzymes for plant protein processing, such as those targeting oligosaccharide reduction in soy-based products, addresses digestibility issues that have historically limited consumer acceptance according to FDA (Food and Drug Administration)[2]Food and Drug Administration, "GRN 1120, Alpha-Galactosidase Enzyme", www.fda.gov. Alpha-galactosidase applications in plant-based dairy alternatives demonstrate how enzyme technology enables manufacturers to create products with improved sensory characteristics and reduced anti-nutritional factors. The segment's growth trajectory benefits from regulatory advantages, as plant-based enzymes often qualify for clean-label positioning and align with sustainability messaging that resonates with target demographics.

Advancement in microbial and genetically modified enzymes

Directed-evolution platforms and computational protein design reduce enzyme development timelines from years to months, enabling manufacturers to respond rapidly to changing customer preferences. These technological advancements accelerate product development cycles and increase the market's ability to meet evolving consumer demands. Genetically optimized enzyme variants operate across wider pH and temperature ranges, allowing food processors to achieve energy savings through lower-temperature processing. This optimization enhances production efficiency and reduces operational costs across the food processing industry. The United States food enzymes market benefits from the FDA's established GRAS (Generally Recognized as Safe) process for microbial enzymes, providing a regulatory advantage compared to other global markets according to FDA (Food and Drug Administration). This streamlined regulatory framework encourages innovation and market entry for new enzyme products, further stimulating market growth.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Regulatory compliance and labeling requirements impact market growth | -0.7% | National, with state-level variations in labeling requirements | Short term (≤ 2 years) |

| Impact of environmental and processing factors on enzyme performance | -0.5% | National, particularly affecting temperature-sensitive applications | Medium term (2-4 years) |

| Varying enzyme performance on different substrate materials | -0.6% | National, affecting different application areas | Short term (≤ 2 years) |

| Legal challenges and patent disputes shape enzyme technology market | -0.5% | National, affecting all enzymes segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory compliance and labeling requirements impact market growth

The complex regulatory landscape for enzyme approvals creates significant barriers to market entry and product innovation, particularly for novel enzyme applications that lack established safety profiles. The FDA's GRAS notification process, while providing a pathway for enzyme approval, requires extensive documentation and safety studies that can cost millions of dollars and take years to complete according to FDA (Food and Drug Administration). State-level variations in labeling requirements add complexity for manufacturers operating across multiple jurisdictions, requiring different formulations or labeling approaches for the same product. The increasing consumer demand for transparency has elevated scrutiny of enzyme sources and production methods, creating pressure for more detailed disclosure that may reveal proprietary information. Regulatory uncertainty around genetically modified enzyme sources continues to create market segmentation, with some applications requiring non-GMO alternatives that may have inferior performance characteristics or higher costs.

Impact of environmental and processing factors on enzyme performance

Enzyme stability and activity remain highly dependent on processing conditions, creating operational constraints that limit application flexibility and require specialized handling protocols. Research on carbohydrases from Aspergillus niger demonstrates that optimal temperatures vary significantly across enzyme types, with α-galactosidase performing best at 57.6°C while cellulase requires only 46.5°C for optimal activity according to ScienceDirect.These temperature sensitivities create challenges for manufacturers using multiple enzyme systems in single processes, requiring compromise conditions that may reduce overall efficiency. pH variations, metal ion presence, and substrate interactions can significantly impact enzyme performance, necessitating careful process control and potentially expensive buffering systems. Long-term enzyme stability during storage and transportation remains a concern, particularly for liquid formulations that may require cold chain management, adding to operational costs and complexity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Carbohydrase Dominance Faces Lipase Innovation

Carbohydrase enzymes hold 58.96% market share in 2025, dominating food processing applications from baking to brewing. The segment's dominance stems from the ubiquity of carbohydrate substrates in food processing and the mature technology platforms that enable cost-effective production at scale. Amylases lead this segment, particularly in baking where they improve dough properties and shelf life. Pectinases support juice and wine production, while cellulases serve brewing and plant-based food processing. Specialized carbohydrases handle oligosaccharide modification in functional foods.

Lipase enzymes project 6.42% CAGR through 2031, driven by dairy processing, flavor development, and plant-based foods. Protease enzymes maintain positions in meat and dairy processing but face growth limitations. The development of extremophilic enzymes represents an emerging opportunity, with research demonstrating superior performance under harsh processing conditions that conventional enzymes cannot tolerate according to PMC (PubMed Central). Other enzyme categories, including transglutaminase and glucose oxidase, address specialized applications in processed foods and baking, respectively, maintaining stable but limited market positions.

By Form: Powder Stability Drives Market Preference

Powder formulations dominate with 64.55% market share in 2025 and project 6.51% CAGR through 2031, driven by superior stability and handling convenience. The powder form's advantages include enhanced storage capabilities, efficient transportation, and precise dosing accuracy, reducing operational complexity in food processing. Their longer shelf life and temperature stability make them ideal for complex supply chains, while compatibility with automated systems improves processing efficiency.

Liquid enzyme formulations are facing challenges in stability and handling requirements. While liquid forms excel in applications requiring immediate activity and liquid processing integration, they require cold storage and have shorter shelf lives. These formulations maintain relevance in specialized processing, particularly where precise pH control is needed, despite powder forms' overall advantages.

By Source: Microbial Leadership Challenged by Plant-Based Growth

Microbial enzyme sources dominate with 65.33% market share in 2025, benefiting from established fermentation technologies, consistent quality control, and regulatory acceptance that enables large-scale commercial production. The microbial platform's advantages include predictable production yields, genetic modification capabilities that enable enzyme optimization, and established safety profiles that facilitate regulatory approval processes. Genetically modified microbial systems offer particular advantages in producing enzymes with enhanced stability, specificity, or activity levels that cannot be achieved through natural sources.

Plant-derived enzymes show the strongest growth potential at 6.67% CAGR through 2031, driven by clean-label positioning and consumer preference for natural ingredients that align with transparency and sustainability trends. The plant source category benefits from consumer perception advantages and regulatory simplicity that can accelerate product development and market acceptance. Plant enzymes often qualify for organic and non-GMO certifications that command premium pricing in certain market segments, particularly those targeting health-conscious consumers.

By Application: Bakery Stability Contrasts with Dairy Innovation

The bakery and confectionery segment maintains the largest market share at 29.74% in 2025, supported by the sector's fundamental reliance on enzyme technology for dough conditioning, shelf life extension, and product quality optimization. Traditional amylase applications continue to drive volume, while specialized enzymes for clean-label formulations and gluten-free products create premium positioning opportunities. The segment benefits from established application protocols and proven ROI that facilitate adoption across different bakery operation scales. Recent innovations in enzyme combinations for artisanal bread production and automated baking systems demonstrate the segment's continued evolution beyond commodity applications.

Dairy and desserts applications demonstrate the highest growth trajectory at 6.95% CAGR through 2031, driven by innovation in plant-based alternatives and functional dairy products that require sophisticated enzyme solutions. Lactase applications in lactose-free products continue to expand as manufacturers target broader consumer demographics, while specialized enzymes for protein modification enable texture improvements in reduced-fat and high-protein dairy formulations. The segment's growth reflects the dairy industry's transformation toward value-added products that command premium pricing and require differentiated processing capabilities.

Geography Analysis

The United States food enzymes market demonstrates concentrated growth patterns that reflect regional food processing infrastructure, regulatory environments, and consumer preferences that vary significantly across different geographic areas. The Midwest region benefits from proximity to agricultural raw materials and established food processing clusters that create natural advantages for enzyme applications in grain-based products and livestock processing. California's leadership in plant-based food innovation and stringent environmental regulations drive demand for enzyme solutions that enable clean-label formulations and sustainable processing practices. The Northeast corridor's concentration of specialty food manufacturers and health-conscious consumers creates premium market opportunities for functional enzyme applications. Texas and the Southeast benefit from large-scale food processing operations and growing Hispanic populations that drive demand for traditional and ethnic food products requiring specialized enzyme applications.

Regional variations in regulatory interpretation and enforcement create different competitive dynamics across state markets, with some jurisdictions demonstrating greater openness to novel enzyme applications while others maintain conservative approval processes. The concentration of biotechnology expertise in certain regions, particularly California's Bay Area and the Boston-Cambridge corridor, influences innovation patterns and creates clusters of enzyme development activity. Food safety regulations and inspection protocols vary across states, creating different operational requirements for enzyme suppliers and food manufacturers.

Climate variations across the country affect raw material quality and processing requirements, creating regional differences in enzyme application needs and performance optimization strategies. The West Coast's focus on organic and sustainable food production creates market opportunities for plant-derived and non-GMO enzyme solutions, while traditional agricultural regions may prioritize cost-effectiveness and proven performance over sustainability positioning.

Competitive Landscape

The United States food enzymes market exhibits oligopolistic characteristics, reflecting the dominance of established biotechnology companies that leverage patent portfolios, specialized manufacturing capabilities, and extensive regulatory expertise to maintain competitive barriers. Major players include International Flavors & Fragrances Inc., Kerry Group plc., DSM-Firmenich, and Associated British Foods plc.

The recent completion of the Novozymes-Chr. Hansen merger creating Novonesis exemplifies the industry's consolidation trend, with the combined entity targeting EUR 200 million in annual revenue synergies through enhanced R&D capabilities and global manufacturing optimization. Furthermore, strategic partnerships between enzyme suppliers and equipment manufacturers, such as the Thyssenkrupp Uhde-Novonesis collaboration on enzymatic esterification technology, demonstrate how competitive advantage increasingly depends on integrated solutions rather than standalone enzyme products.

Competitive dynamics reflect a bifurcated market structure where global leaders compete on innovation and scale while regional specialists focus on application expertise and customer service in niche segments. The industry's high R&D intensity creates ongoing pressure for patent development and protection, with companies investing heavily in computational protein design and directed evolution technologies to maintain technological leadership.

United States Food Enzymes Industry Leaders

-

International Flavors & Fragrances, Inc.

-

Puratos Group

-

DSM-Firmenich AG

-

Kerry Group plc

-

Associated British Foods plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Novonesis acquired dsm-firmenich's share of the Feed Enzyme Alliance, expanding its enzyme portfolio and strengthening its position in specialized enzyme applications. This acquisition demonstrates the ongoing consolidation in enzyme markets and Novonesis's strategy to leverage its combined capabilities across multiple application areas.

- February 2025: Thyssenkrupp Uhde and Novonesis launched innovative enzymatic esterification technology that reduces energy consumption by 60% and greenhouse gas emissions while improving product quality in ester production. The technology represents a significant advancement in sustainable chemical processing with applications extending to food ingredient production.

- July 2024: Lallemand made a strategic investment in Turkish enzyme company Livzym, indicating expansion into emerging enzyme production markets and potential supply chain diversification strategies.

- January 2024: The combination of Novozymes and Chr. Hansen was successfully completed, creating Novonesis as a leading global biosolutions partner with projected organic revenue growth of 6-8% through 2025 and expected annual revenue synergies of EUR 200 million.

United States Food Enzymes Market Report Scope

The US food enzymes market is segmented by type that includes carbohydrases, proteases, lipases and other types. Based on application, the market is segmented into bakery, confectionery, dairy and frozen desserts, meat, poultry, and seafood products, beverages, and other applications.

By Type

| Carbohydrase | Amylases |

| Pectinases | |

| Cellulases | |

| Other | |

| Protease | |

| Lipase | |

| Other Enzymes |

By Form

| Powder |

| Liquid |

By Source

| Plant |

| Microbial |

| Animal |

By Application

| Bakery and Confectionery |

| Dairy and Desserts |

| Beverages |

| Meat and Meat Products |

| Soups, Sauces, and Dressings |

| Other Applications |

| By Type | Carbohydrase | Amylases |

| Pectinases | ||

| Cellulases | ||

| Other | ||

| Protease | ||

| Lipase | ||

| Other Enzymes | ||

| By Form | Powder | |

| Liquid | ||

| By Source | Plant | |

| Microbial | ||

| Animal | ||

| By Application | Bakery and Confectionery | |

| Dairy and Desserts | ||

| Beverages | ||

| Meat and Meat Products | ||

| Soups, Sauces, and Dressings | ||

| Other Applications |

Key Questions Answered in the Report

What is the current size of the United States food enzymes market?

The food enzymes market is valued at USD 941.09 million in 2026 and is projected to reach USD 1.24 billion by 2031.

What compound annual growth rate is forecast for the food enzymes market through 2031?

The market is expected to expand at a 5.74% CAGR during the 2026-2031 period.

Which enzyme type holds the largest revenue share in the United States?

Carbohydrases lead with 58.96% of the food enzymes market share in 2025.

Which application segment is growing the fastest in the food enzymes market?

Dairy and desserts are advancing at a 6.95% CAGR, the highest among application segments.

Page last updated on: