Protein Alternatives Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 19.73 Billion |

| Market Size (2031) | USD 25.13 Billion |

| Growth Rate (2026 - 2031) | 4.98% CAGR |

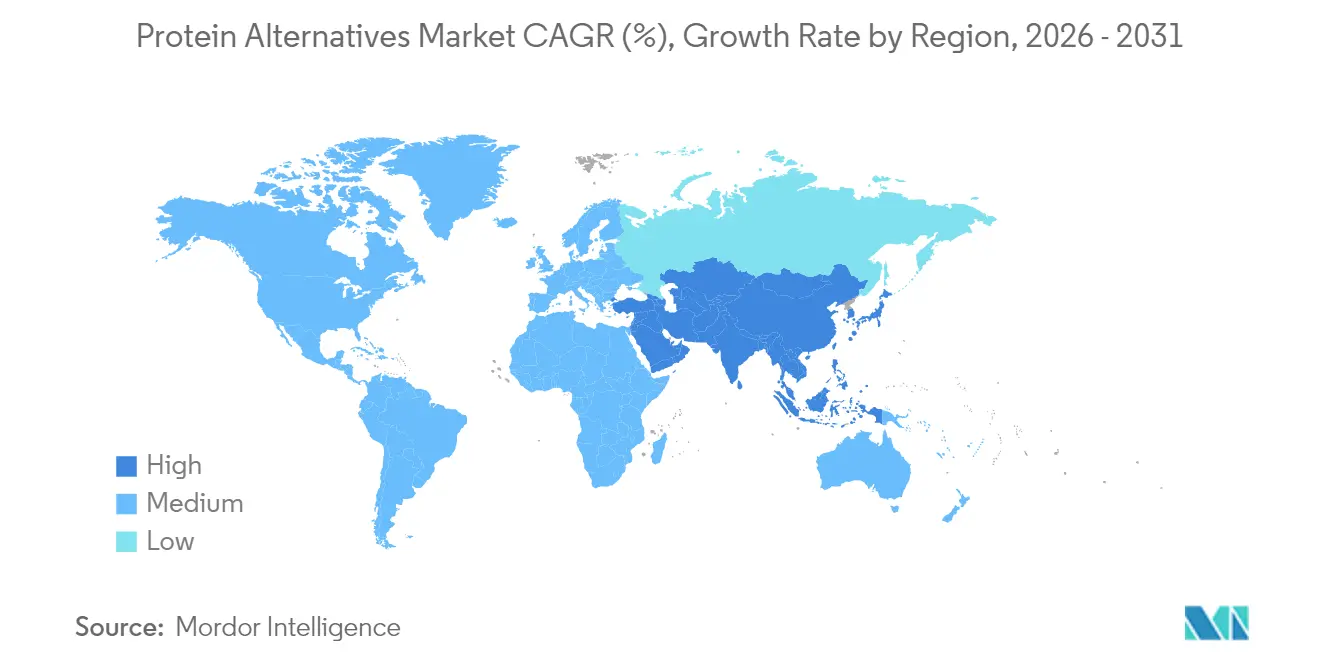

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Protein Alternatives Market Analysis by Mordor Intelligence

The alternative protein market size is expected to grow from USD 18.79 billion in 2025 to USD 19.73 billion in 2026 and is forecast to reach USD 25.13 billion by 2031 at 4.98% CAGR over 2026-2031. The market growth is driven by advances in precision fermentation technology, increasing consumer demand for sustainable food options, and regulatory changes that expedite novel food approvals. Manufacturers are transitioning from pilot to commercial production, reducing per-kilogram costs through larger bioreactor capacity and lower operating costs from renewable energy usage. Consumer packaged-goods companies are increasing their launches of products that replicate the taste and texture of conventional meat and dairy, while restaurant chains are expanding their plant-based menu offerings to reach more mainstream consumers.

Key Report Takeaways

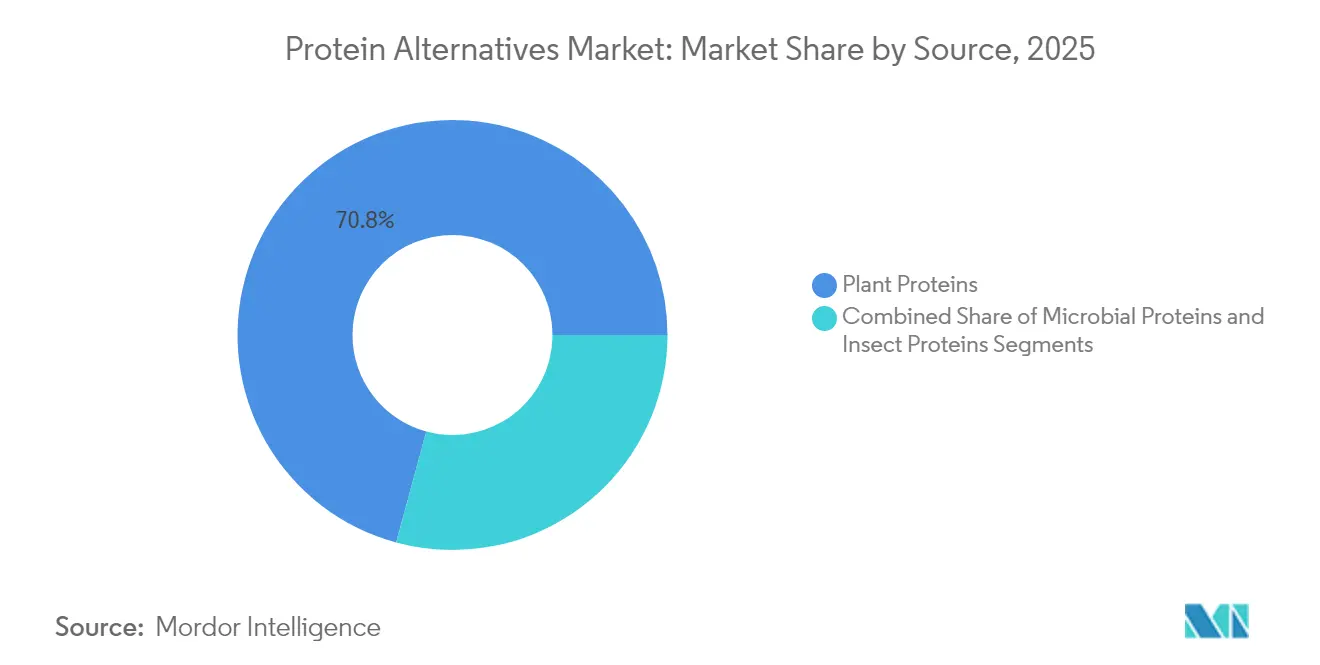

- By source, plant proteins led with 70.78% of 2025 revenue; microbial proteins are poised for the fastest 2026-2031 expansion at 7.45% CAGR.

- By form, protein isolates captured 43.65% 2025 share, whereas textured proteins and TVP are set to grow at 6.1% CAGR through 2031.

- By production technology, dry + wet fractionation held 56.15% of 2025 value; cellular agriculture registers the highest 7.75% CAGR outlook.

- By application, food & beverage accounted for 53.34% of 2025 spending; dietary supplements and sports nutrition stand out with a 7.05% CAGR forecast.

- By geography, Asia-Pacific dominated with 33.55% 2025 share, while the Middle East and Africa is projected to advance at 6.18% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Protein Alternatives Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in precision-fermented protein production | +1.2% | Global, with concentration in North America and EU | Medium term (2-4 years) |

| Growing adoption of plant-based options by quick-service restaurants | +0.8% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Increasing prevalence of lactose intolerance and allergies | +0.6% | Global, particularly Asia-Pacific and Europe | Long term (≥ 4 years) |

| Growing demand for sustainable food sources | +1.1% | Global, strongest in EU and North America | Medium term (2-4 years) |

| Technological advancements in food processing | +0.9% | Global, with innovation hubs in North America, EU, and Asia | Medium term (2-4 years) |

| Growing vegan, vegetarian, and flexitarian populations | +0.7% | Global, led by Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growth in Precision-Fermented Protein Production

Precision fermentation technology enables the production of animal-identical proteins through engineered microorganisms, transforming alternative protein manufacturing. Perfect Day's partnership with Unilever for Breyers lactose-free products validates the commercial potential of this technology. The process significantly reduces water usage and greenhouse gas emissions compared to traditional dairy production methods. The FDA's GRAS pathway provides faster market access compared to EU novel food regulations, creating regulatory advantages for companies. Onego Bio's production of bioidentical egg proteins through precision fermentation offers solutions to avian flu-related supply chain disruptions while providing clean-label alternatives to conventional egg whites. The increasing number of patents in precision fermentation indicates ongoing innovation and strategic positioning among biotechnology companies.

Growing Adoption of Plant-Based Options by Quick-Service Restaurants

Quick-service restaurants are strategically expanding their plant-based menu offerings, introducing meat alternatives such as burger patties, chicken substitutes, and non-dairy cheeses. This expansion has significantly increased consumer exposure and adoption rates. Despite McDonald's decision to discontinue its McPlant burger in the United States, specialized vegan restaurant chains are experiencing substantial growth, while manufacturers have made notable improvements in product taste profiles and competitive pricing. The quick-service segment remains a crucial testing ground for mainstream market acceptance, as products that successfully meet the rigorous operational efficiency standards and consumer price expectations in restaurants demonstrate strong potential for retail market expansion.

Increasing Prevalence of Lactose Intolerance and Allergies

The widespread prevalence of lactose malabsorption among adults continues to drive significant demand for dairy-free protein alternatives. Precision-fermented casein and whey proteins have emerged as viable substitutes, offering identical nutritional profiles and functional properties to conventional dairy products while being completely lactose-free. This technological advancement enables manufacturers to develop innovative products across multiple categories, including premium cheese alternatives, plant-based yogurts, and specialized performance nutrition powders. Furthermore, manufacturers implement rigorous allergen monitoring protocols throughout their production processes and invest in developing specialized variants that exclude the most prevalent allergenic compounds, ensuring broader consumer accessibility.

Growing Demand for Sustainable Food Sources

Environmental sustainability is driving alternative protein adoption as consumers recognize the high carbon footprint and resource requirements of traditional agriculture. Life cycle assessments show that alternative proteins reduce greenhouse gas emissions by up to 97% compared to conventional animal agriculture, though the energy requirements for processing these alternatives remain a consideration.[1]National Academy of Sciences "Perspective on the Environmental Impact of Plant-Based Protein Concentrates and Isolates," pnas.org. The European Union's Green Deal and Farm to Fork strategy provide regulatory frameworks supporting sustainable protein development. Government investments reached USD 523 million globally in 2023, according to the Good Food Institute, indicating policy support for the sector. While consumers demonstrate willingness to pay higher prices for sustainable products, achieving cost parity remains crucial for widespread market adoption. Sustainability considerations increasingly influence business-to-business procurement decisions, particularly in food service and retail private label segments [2]Good Food Institute"Public Investment in Alternative proteins to Feed a Growing World," gfi.org.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Protein legume supply-chain volatility due to El Niño-driven yield swings in Canada and Australia | -0.4% | Global, concentrated impact in North America and Australia | Short term (≤ 2 years) |

| Regulatory restrictions impact insect protein adoption | -0.3% | Europe and North America primarily | Medium term (2-4 years) |

| Taste and Texture Challenges | -0.5% | Global, Strong Impact in North America and Europe | Short term (≤ 2 years) |

| Limited consumer awareness in emerging markets | -0.3% | Asia-Pacific, Latin America, Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Protein Legume Supply-Chain Volatility Due to El Niño-Driven Yield Swings

Severe weather conditions have significantly impacted pulse crop production in Canada and Australia, causing substantial reductions in pea and fava bean availability for processing. These supply constraints have triggered widespread price increases throughout the contract manufacturing chain, particularly affecting the production costs of plant-protein isolates. In response, food manufacturers are implementing strategic measures, including geographical diversification of ingredient sourcing and increased investments in alternative protein production methods such as microbial fermentation and cellular agriculture, to minimize their exposure to climate-related supply disruptions.

Regulatory Restrictions Impact Insect Protein Adoption

Regulatory frameworks for insect proteins remain fragmented and restrictive, particularly in Western markets where consumer acceptance is already challenging. The UK's transition away from EU regulations resulted in stricter requirements, with only four insect species maintaining valid applications by 2024, while other edible insects must be removed from the market pending authorization [3]Food Standards Agency, “Transitional Arrangements for Novel Foods,” food.gov.uk. Allergenicity concerns, particularly cross-reactivity with crustaceans, impact regulatory assessments and labeling requirements. This creates additional compliance challenges for manufacturers, as they must implement strict protocols for allergen testing, documentation, and consumer safety warnings.[4]EFSA, “Safety Assessment of UV-Treated Mealworm Powder,” efsa.europa.eu.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Plant Proteins Hold Scale While Microbial Proteins Accelerate

Plant proteins captured the lion’s share of 70.78% in 2025 as soy, pea, and rice maintained strong purchasing contracts with global manufacturers. The alternative protein market size for plant-based sources will expand steadily yet cede relative share to faster-growing microbial inputs that deliver 7.45% CAGR on the back of precision-fermentation cost curves. Diversification into hemp and chickpea proteins supports allergen-free claims and regional crop strategies, while microbial mycoproteins gain retail listings in Europe.

Soy protein isolate remains the functional workhorse for meat analogs, but companies blend it with pea to improve amino-acid completeness and taste. Mycoprotein suppliers leverage controlled fermentation to bypass agricultural risk, securing year-round capacity. Regulatory nods for algae-based proteins later this decade would further broaden the ingredient toolbox and reduce pressure on pulse supplies.

By Form: Isolates Maintain Lead While Textured Proteins Gain Traction

Protein isolates account for 43.65% of market spend in 2025, primarily used in ready-to-drink beverages and powder formats due to their clear solubility and neutral flavor profile. Textured vegetable protein shows a 6.1% CAGR, driven by high-moisture extrusion technology that creates fibrous structures resembling muscle tissue for meat alternatives like burgers and chicken strips.

Manufacturing companies are investing in advanced extrusion equipment and cooling-die systems to improve texture and moisture retention. While protein isolates maintain strong market share in sports nutrition products, manufacturers are adopting precision-fermented isolates that replicate dairy functionality without lactose content. Hydrolysates maintain a specialized position in clinical and infant nutrition applications where rapid absorption is essential.

By Application: Food & Beverage Leads, Supplements Post Rapid Growth

Food and beverage applications dominated the market with 53.34% of revenue in 2025, as manufacturers expanded their product portfolios with innovative plant-based alternatives. The introduction of meat-free burgers, sausages, dairy-free cheese, and milk alternatives in mainstream retail channels reflects growing consumer demand for sustainable protein options. The dietary supplements and sports nutrition segment is experiencing robust growth at a 7.05% CAGR, with transparent protein beverages and powder blends gaining popularity among fitness enthusiasts who traditionally relied on whey protein products.

Hybrid meat alternatives, which strategically combine plant-based ingredients with cultivated components, are gaining traction in premium food service establishments. These innovative products demonstrate superior technical performance, particularly in moisture retention and reduced cooking loss, offering improved texture and taste profiles that more closely resemble conventional meat products.

By Production Technology: Fractionation Dominant, Cellular Agriculture Rises Fast

Dry and wet fractionation techniques processed 56.15% of protein volumes in 2025, utilizing established infrastructure optimized for soybean and wheat processing. Cellular agriculture demonstrated the highest growth rate at 7.75% CAGR, driven by the installation of large-scale bioreactors producing cultivated chicken and beef prototypes.

Production facilities are shifting to continuous-process systems that reduce batch times and minimize contamination risks. While the cellular agriculture segment currently represents a small portion of the alternative protein market, it receives support through government funding and co-manufacturing facilities that reduce capital requirements for emerging companies. Improvements in serum-free media efficiency are anticipated to drive future cost reductions in the sector.

Geography Analysis

Asia-Pacific holds 33.55% of the 2025 alternative protein market value, driven by urbanization, rising incomes, and government support for food technology manufacturing zones. China's five-year plan includes "future foods" initiatives and provides funding for fermentation pilot facilities. Chinese dairy companies are developing animal-free casein to reduce import dependency. India's alternative protein ecosystem centers around Bengaluru, where contract manufacturers produce plant-protein concentrates for domestic and international markets.

North America's market growth stems from the FDA's efficient GRAS (Generally Recognized as Safe) assessment process, allowing precision-fermented dairy and egg proteins to enter the market quickly. The region maintains strong venture capital investment, while multinational companies participate in co-manufacturing agreements to expand production facilities. Generation Z shows higher acceptance of meat alternatives, while older consumers prioritize cost and familiar products.

Europe integrates alternative proteins into its Green Deal framework, supporting cellular-agriculture development and implementing sustainability reporting requirements that favor low-carbon ingredients. While novel-food approvals take longer than in the United States, approved products benefit from consistent labeling across the EU. The Middle East and Africa region, particularly the UAE and Saudi Arabia, achieves the highest regional growth rate at 6.18%, driven by food security initiatives and sovereign fund investments in fermentation technologies.

Competitive Landscape

Agricultural companies like Cargill, ADM, and Ingredion utilize their existing sourcing and logistics networks to supply pea isolates, canola concentrates, and functional starches to alternative protein manufacturers. These companies leverage their scale advantages while developing in-house extrusion capabilities. Companies such as Beyond Meat and Perfect Day focus on innovation, developing advanced burger formulations and lactose-free dairy proteins that meet heart-health standards.

Strategic partnerships shape the market: Cargill has established a multi-year supply agreement with ENOUGH for mycoprotein meat alternatives, while Believer Meats has partnered with GEA to construct the world's largest cultivated-meat facility. The industry shows increasing maturity through rising patent activity, particularly in enzyme pathways and bioreactor design technologies.

Strategic partnerships shape the market: Cargill has established a multi-year supply agreement with ENOUGH for mycoprotein meat alternatives, while Believer Meats has partnered with GEA to construct the world's largest cultivated-meat facility. The industry shows increasing maturity through rising patent activity, particularly in enzyme pathways and bioreactor design technologies.

Protein Alternatives Industry Leaders

-

ADM

-

Cargill Inc.

-

International Flavors & Fragrances Inc.

-

Kerry Group plc

-

Ingredion Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Griffith Foods introduced its first alternative proteins portfolio, featuring plant-based meat substitutes, legume-based proteins, and innovative protein formulations. The portfolio includes ready-to-market food concepts designed to meet growing consumer demand for sustainable protein alternatives.

- April 2024: InnovaFeed, a producer of insect ingredients for high-quality animal feed, pet food, and plant nutrition, inaugurated its North American Insect Innovation Center (NAIIC) in Decatur, Illinois. This pilot plant is the first step of the company’s planned industrial expansion in North America. The company aims to scale up the production and commercialization of insect protein in the US.

- January 2024: Danish pet food and treat startup Globe Buddy introduced a super-premium dog food, Globe Buddy Brown, incorporating insect-derived protein. The insect protein used in Globe Buddy Brown is claimed to be sourced from black soldier fly larvae supplied by the Danish insect protein producer Enorm.

Global Protein Alternatives Market Report Scope

Protein alternatives are protein-rich ingredients sourced from plants, insects, fungi, or through tissue culture to replace conventional animal-based sources.

The global protein alternatives market is segmented by the source and includes plant protein, mycoprotein, algal protein, and insect protein. The plant protein section is further classified into soy protein, wheat protein, pea protein, and other plant proteins. Based on the application, the market is segmented into food and beverage, dietary supplements, animal feed, pet food, personal care, and cosmetics. The food and beverage segment is sub-segmented into the bakery, confectionery, plant-based dairy products, beverages, and other food and beverages. The report further analyses the global market scenario, including a detailed analysis of North America, Europe, Asia-Pacific, South America, the Middle East, and Africa. For each segment, the market sizing and forecasts were made on the basis of value (USD).

| Plant Proteins | Soy Protein |

| Wheat | |

| Pea | |

| Rice | |

| Hemp | |

| Others | |

| Microbial Proteins | Mycoprotein |

| Algea Protein | |

| Insect Proteins | Cricket |

| Black Soldier Fly Larvae (BSFL) | |

| Others |

| Protein Isolates |

| Protein Concentrates |

| Textured Proteins and TVP |

| Hydrolysates and Peptides |

| Dry and Wet Fractionation |

| Extrusion and Texturization |

| Precision Fermentation |

| Cellular Agriculture (Scaffold-Based, Suspension) |

| Food and Beverage | Plant-Based Meat Analogues |

| Dairy and Dairy Alternative Alternatives | |

| Bakery and Confectionery | |

| Beverages | |

| Other Packaged Foods | |

| Dietary Supplements and Sports Nutrition | |

| Animal Feed and Pet Food | |

| Personal Care and Cosmetics |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Source | Plant Proteins | Soy Protein |

| Wheat | ||

| Pea | ||

| Rice | ||

| Hemp | ||

| Others | ||

| Microbial Proteins | Mycoprotein | |

| Algea Protein | ||

| Insect Proteins | Cricket | |

| Black Soldier Fly Larvae (BSFL) | ||

| Others | ||

| By Form | Protein Isolates | |

| Protein Concentrates | ||

| Textured Proteins and TVP | ||

| Hydrolysates and Peptides | ||

| By Production Technology | Dry and Wet Fractionation | |

| Extrusion and Texturization | ||

| Precision Fermentation | ||

| Cellular Agriculture (Scaffold-Based, Suspension) | ||

| By Application | Food and Beverage | Plant-Based Meat Analogues |

| Dairy and Dairy Alternative Alternatives | ||

| Bakery and Confectionery | ||

| Beverages | ||

| Other Packaged Foods | ||

| Dietary Supplements and Sports Nutrition | ||

| Animal Feed and Pet Food | ||

| Personal Care and Cosmetics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the alternative protein market?

The alternative protein market size reached USD 19.73 billion in 2026 and is on track to hit USD 25.13 billion by 2031 at a 4.98% CAGR.

Which source segment is growing fastest?

Microbial proteins, including precision-fermented whey and mycoproteins, are projected to grow at 7.45% CAGR from 2026-2031, outpacing plant and insect sources.

Which region exhibits the highest growth potential?

The Middle East and Africa shows the fastest expansion at 6.18% CAGR to 2031, supported by food-security investments and sovereign-fund backing of fermentation facilities.

How fragmented is the competitive landscape?

The market is moderately fragmented; the top five suppliers control below 50% of sales, giving both incumbents and start-ups room to acquire share through cost and technology advantages.

What are the main restraints facing the sector?

Supply-chain volatility for pulse crops and prolonged regulatory reviews for insect proteins weigh on near-term growth, though technology shifts and diversified sourcing offer mitigating paths.

Page last updated on: