Plant-based Protein Supplements Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

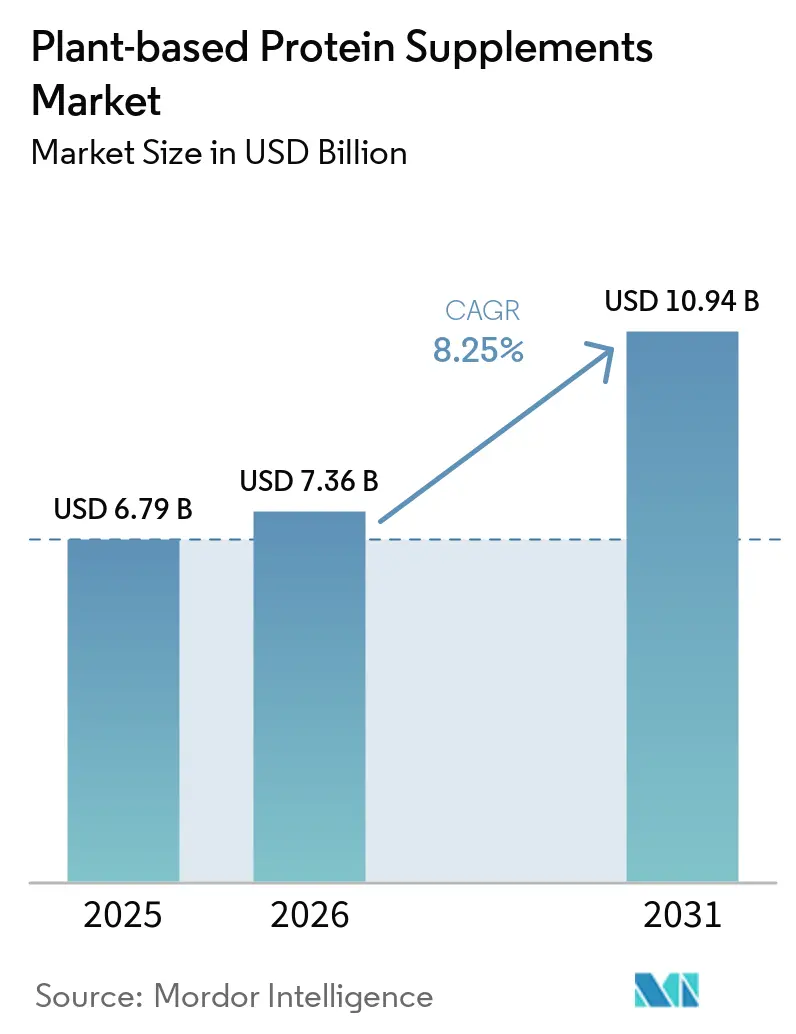

| Market Size (2026) | USD 7.36 Billion |

| Market Size (2031) | USD 10.94 Billion |

| Growth Rate (2026 - 2031) | 8.25% CAGR |

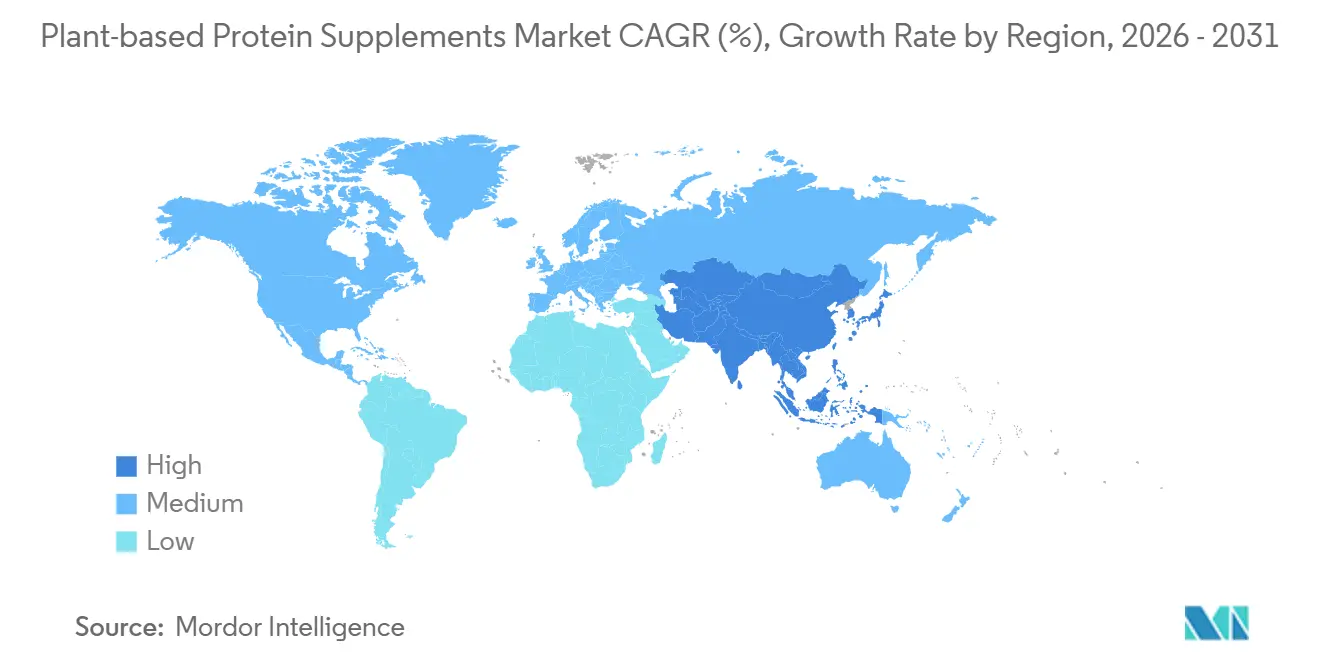

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Plant-based Protein Supplements Market Analysis by Mordor Intelligence

The plant-based protein supplements market size was valued at USD 6.79 billion in 2025 and estimated to grow from USD 7.36 billion in 2026 to reach USD 10.94 billion by 2031, at a CAGR of 8.25% during the forecast period (2026-2031). The plant-based protein supplements market is moving into a broader daily nutrition role as more consumers shift away from dairy-based supplements for lifestyle, digestive, and ingredient-transparency reasons, and that change is giving plant formats a wider audience than the category had a few years ago. ADM reported that 46% of global consumers identified as flexitarians in 2025, indicating that a large consumer base is already open to plant-forward choices without fully abandoning animal protein[1]Source: ADM, “2025 Alternative Protein Landscape Report,” ADM, adm.com. Veganuary added another strong demand funnel, with 25.8 million participants in early 2025. The plant-based protein supplements market is also benefiting from its expansion beyond gym-focused use, as higher protein intake is increasingly linked with healthy aging, lower frailty risk, and better long-term health support, bringing older adults and medically guided users into the category. Powders still set the volume base, pharmacies continue to build trust at the point of purchase, and online channels are opening faster routes for newer brands to scale, which means competition is widening without giving any single company a decisive advantage. The result is a plant-based protein supplements market that remains fragmented, with large nutrition groups, direct-to-consumer brands, and focused clean-label specialists all competing around taste improvement, blended protein quality, and access to repeat buyers.

Key Report Takeaways

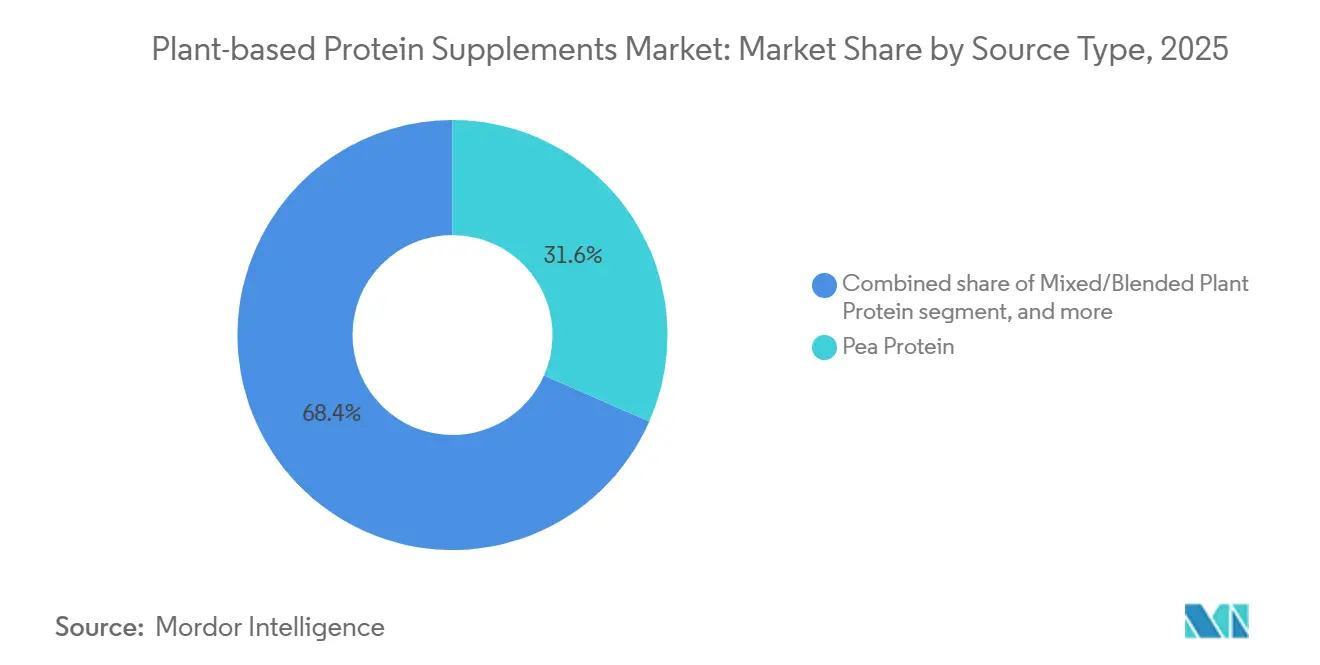

- By source, pea protein held 31.55% of the plant-based protein supplements market share in 2025, while mixed and blended proteins are expected to grow at a CAGR of 8.67% through 2031.

- By product type, powders led with 44.26% revenue share in 2025, while RTD beverages are expected to grow fastest at a 9.15% CAGR through 2031.

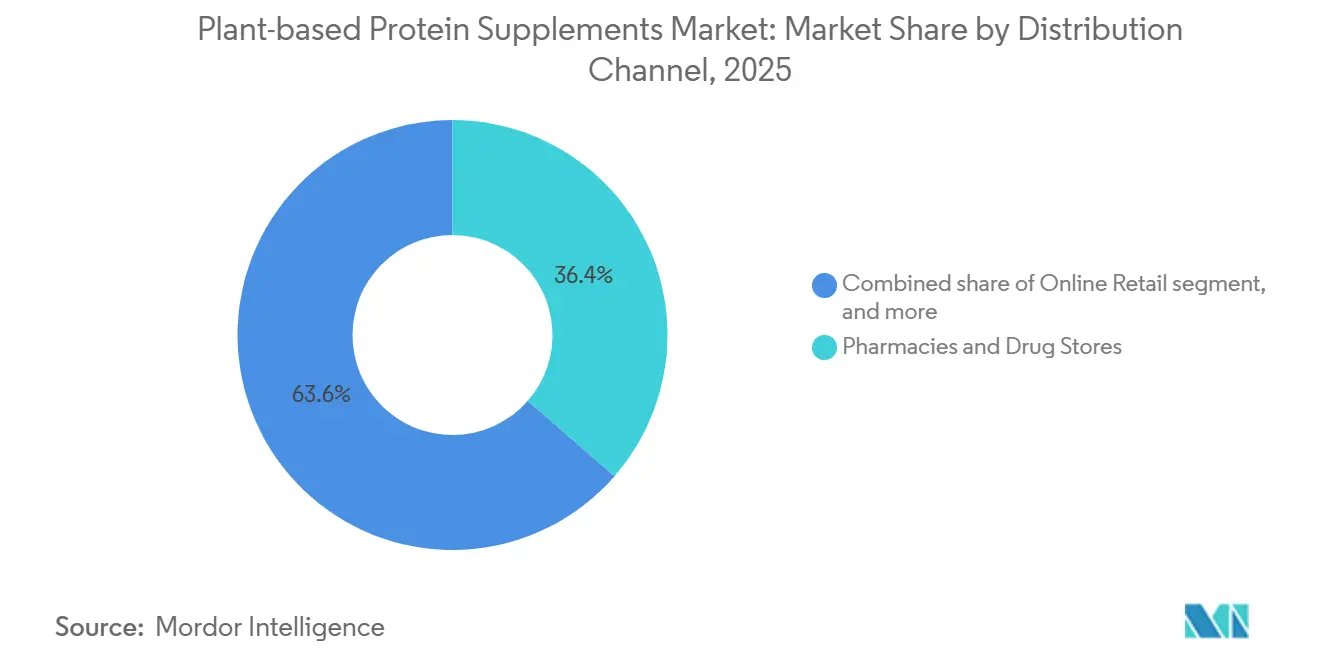

- By distribution channel, pharmacies and drug stores led the plant-based protein supplements market with a 36.42% share in 2025, while online retail is anticipated to register the fastest CAGR of 10.86% during 2026-2031.

- By geography, North America accounted for the largest share of the plant-based protein supplements market, at 41.53% in 2025, while Asia-Pacific is projected to grow at the fastest CAGR of 9.53% during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Plant-based Protein Supplements Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Shift Toward Vegan And Flexitarian Lifestyles | +1.8% | Global, with highest intensity in North America and Western Europe | Medium term (2-4 years) |

| Growing Lactose Intolerance And Dairy-Free Nutrition Demand | +1.4% | Global, particularly APAC, South America, and MEA | Long term (≥ 4 years) |

| Sports Nutrition And Active Aging Protein Intake Expansion | +1.2% | North America, Europe, urban APAC | Medium term (2-4 years) |

| Convenience-Led Shift Toward RTD And On-The-Go Formats | +0.9% | North America and APAC core, spill-over to Europe | Short term (≤ 2 years) |

| Increasing Preference For Clean-Label Protein Supplements | +0.8% | North America and Western Europe | Medium term (2-4 years) |

| Rising Demand For Weight Management And Satiety Products | +0.7% | Global, with early gains in urban North American centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising shift toward vegan and flexitarian lifestyles

The plant-based protein supplements market is drawing strength from a broader consumer base than just strict vegans, as flexitarian eating has become a practical middle ground for many households rather than a niche identity. ADM found that 46% of global consumers identified as flexitarians in 2025, a large enough share to push plant protein into everyday nutrition rather than limiting it to specialty shelves. Veganuary’s 25.8 million participants in early 2025 also matter because they create a recurring annual cycle of product trial, and even partial retention from that trial base supports regular category growth. This pattern matters commercially because it adds new buyers to the category rather than shifting spend among consumers who were already committed to plant-based products. It also means brands that position plant protein as convenient, familiar, and easy to use in daily routines are likely to reach a larger audience than brands that market only to a narrow vegan consumer base.

Growing lactose intolerance and dairy-free nutrition demand

The plant-based protein supplements market is also benefiting from a long-standing nutritional need, as dairy avoidance is not only a preference issue for many consumers but also tied to digestive tolerance. The U.S. National Institutes of Health states that lactose malabsorption affects 65% of the global adult population, and prevalence rises above 80% in East Asian populations, which makes dairy-free protein support relevant across a very large consumer base[2]Source: National Institutes of Health, “Lactose Intolerance,” MedlinePlus Genetics, nih.gov . This creates durable demand for plant-based supplements that can serve people who want to avoid digestive discomfort without giving up protein intake. It also increases interest in soy-free, nut-free, and allergen-aware formulas, because consumers who avoid dairy often look more closely at ingredient tolerance across the rest of the label. As a result, blended protein products that offer a broader amino acid profile while remaining friendly to common sensitivities are gaining greater market share in the plant-based protein supplements market.

Sports nutrition and active aging protein intake expansion

The plant-based protein supplements market is no longer tied solely to performance users, as protein supplementation is now part of healthy aging and broader wellness routines. Research published in npj Aging in 2026 found that protein intake above the recommended daily allowance was associated with lower risks of falls, frailty progression, and all-cause mortality in older adults, which widens the category’s addressable audience far beyond gym users. The European Society for Clinical Nutrition and Metabolism recommended a protein intake of 1.0 to 1.5 g/kg/day for older adults, depending on health status, providing formal clinical support for higher protein consumption in later life. The Chinese Nutrition Society also updated its guidance for older adults to 1.0 to 1.2 g/kg/day and identified plant protein as supportive of heart health, which strengthens the case for adoption in aging populations across Asia. These shifts help move plant protein from an optional sports add-on into a more regular nutrition tool for recovery, maintenance, and age-related health support.

Increasing preference for clean-label protein supplements

The plant-based protein supplements market is also being shaped by stronger consumer scrutiny around sourcing, ingredient simplicity, and documented product quality. Clean-label expectations now extend beyond the ingredient list, as buyers increasingly want proof that products have been sourced, processed, and labeled transparently. That makes certification, allergen control, and clear protein quality documentation more important in purchase decisions, especially in pharmacy and specialty retail settings where credibility matters. It also creates a wider gap between brands that can support quality claims with documented formulation work and brands that rely mostly on marketing language. In practice, this is pushing the plant-based protein supplements market toward fewer weak formulations and more products built around traceable ingredients, balanced amino acid blends, and labels that can withstand closer consumer review.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Amino-Acid Completeness And Taste-Masking Trade-Offs | -0.8% | Global | Short term (≤ 2 years) |

| Price Premium Versus Conventional Protein Supplements | -0.7% | Emerging markets including South America, MEA, and APAC | Medium term (2-4 years) |

| Allergen Concerns Linked To Soy And Nut-Based Proteins | -0.5% | Global, particularly North America and Europe | Long term (≥ 4 years) |

| Regulatory Complexity Around Protein And Health Claims | -0.4% | Europe and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Amino-acid completeness and taste-masking trade-offs

The plant-based protein supplements market still faces a formulation challenge because single-source plant proteins do not fully match the amino acid balance that many consumers expect from whey. Pea protein is low in methionine and cysteine, while rice protein is low in lysine, so brands often use multi-source blends to close nutritional gaps and offer a more complete profile. That solution works, but it raises development demands because successful blending requires ingredient quality control, careful formulation, and consistent flavor performance. Taste is another barrier, especially in pea-based products, where beany notes and gritty texture can reduce repeat purchase if the product is not well formulated. These nutrition and sensory trade-offs do not stop growth in the plant-based protein supplements market, but they do slow category expansion for brands that lack the scale or technical capability to improve flavor, texture, and protein balance simultaneously.

Price premium versus conventional protein supplements

The plant-based protein supplements market also faces pricing pressure, as plant-based formulas often remain more expensive than conventional whey products in many retail settings. The gap comes from added processing, flavor masking, sourcing controls, and certification work, all of which can raise the final shelf price. Developed markets are absorbing that premium more easily, especially where clean-label and dairy-free demand is already established, but the issue remains more visible in price-sensitive parts of Asia-Pacific, South America, the Middle East, and Africa. That limits the consumer base in those regions to more affluent urban buyers and slows broader household adoption. It also increases strain on mid-tier brands, as they face margin pressure from both lower-cost private-label competitors and larger companies that can spread production costs over a larger sales base.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Blended Formats Challenging Pea Protein’s Incumbency

Pea protein held 31.55% of the plant-based protein supplements market share in 2025, maintaining its leading position after years of brand-building, supply chain investments, and product familiarity. Its strength comes from an allergen-friendly, non-GMO profile that appeals to consumers seeking an alternative to soy, as well as its leucine content, which supports its relevance in muscle-focused products. Soy protein still has deep roots in the category, but its growth is less straightforward in developed markets, where buyers increasingly question GMO origins and scrutinize label positioning. Rice protein has maintained a steady place in clinical and pediatric nutrition because of its mild taste and hypoallergenic profile, while hemp, quinoa, pumpkin seed, and related sources remain smaller but visible in premium sustainability-led offerings. This leaves the plant-based protein supplements market with a clear split between scale suppliers that can support broader distribution and smaller suppliers that mainly serve specialized, clean-label, or premium niches.

Mixed and blended proteins are projected to grow at an 8.67% CAGR through 2031, making them the fastest-rising source segment in the plant-based protein supplements market outlook. Their momentum reflects a simple product logic: buyers and formulators alike recognize that multi-source blends usually perform better than single-source formulas in terms of amino acid balance. ADM reinforced this direction in May 2026 when it launched 8 new protein ingredient solutions across North America and Europe, including enhanced pea and soy isolates and multi-source blends aimed at specialty nutrition, beverages, and sports supplements. Certification frameworks such as USDA Organic and Non-GMO Project standards also support premium positioning for blends sold through pharmacy and specialty channels where trust matters. In the plant-based protein supplements industry, that gives an edge to brands that can document protein quality clearly and combine nutritional completeness with a label that looks simple and credible to the buyer.

By Product Type: RTD Beverages Redefining Category Convenience

Powders led product demand with 44.26% share in 2025, and that position reflects their strong value per gram of protein, broad flavor range, and long-standing fit with gym, sports, and routine supplement use. Powder also gives consumers more control over serving size and mixing, which helps explain why it remains the base format for repeat users who already have a protein habit. Protein bars still hold a useful place in on-the-go eating because they offer portability and a more structured snack occasion. Other formats, including capsules and food-linked applications, remain smaller and are more relevant where ease of use matters more than product variety. This mix keeps powders at the center of the plant-based protein supplements market, even as format innovation continues to pull new consumers into ready-to-use options.

RTD beverages are forecast to expand at a 9.15% CAGR through 2031, which makes them the fastest-growing product format in the plant-based protein supplements market. Their appeal extends beyond performance nutrition because they eliminate the preparation step, reduce friction in daily use, and fit more naturally into office, travel, and recovery routines. That convenience also matters for older adults and medically guided users, who may be less willing to measure powder or blend shakes regularly. Large companies are increasingly treating ready-to-drink products as a bridge between specialized sports nutrition and mainstream grocery consumption, and that is helping plant protein move into more everyday purchase occasions. Over time, RTD innovation is likely to shape the next phase of the plant-based protein supplements industry by bringing protein into simpler, more frequent, and more accessible use cases.

By Distribution Channel: Online Commerce Reshaping Brand Hierarchies

Pharmacies and drug stores accounted for 36.42% of the market in 2025, making them the largest distribution channel for plant-based protein supplements. Their lead reflects the trust advantage that health-focused retail still carries, because consumers often associate pharmacy shelves with stronger product credibility and more careful selection. That matters in supplements, where many buyers still want reassurance about quality, safety, and intended use before switching to a different product type. Supermarkets and hypermarkets play different roles, serving as the primary point of trial for newer users who encounter plant protein during routine shopping trips rather than through a health-specific search. Other channels, including specialty health stores, gyms, and network-based selling, remain important for premium and performance-oriented products, but they do not match the reach of pharmacy-led retail.

Online retail is projected to grow at a 10.86% CAGR through 2031, which makes it the fastest-expanding route to market in the plant-based protein supplements market. iHerb reported USD 2.9 billion in net sales for fiscal 2025, up 19% year over year, while fulfilling more than 44 million orders for 15 million active global customers, which shows how large dedicated digital health retail has become[3]Source: iHerb, “iHerb Achieves Record USD 2.9 Billion Net Sales in Fiscal 2025,” iHerb Press Release, iherb.com. Online channels give challenger brands more room to explain formulations, reach niche dietary groups, and build repeat purchase through targeted communication that would be harder to execute on a crowded physical shelf. They also allow rapid feedback on flavors, claims, and ingredient positioning, which helps brands adjust faster than traditional retail cycles usually allow. For that reason, the plant-based protein supplements market is likely to keep rewarding companies that use digital channels not only for sales, but also for education, retention, and product refinement.

Geography Analysis

North America held a 41.53% share of the plant-based protein supplements market in 2025, making it the leading regional contributor. The region benefits from a mature supplement culture, broad participation in sports nutrition, and strong consumer familiarity with protein as a daily wellness product rather than a specialized fitness purchase. The United States remains the anchor market because global incumbents, specialist challengers, and digital-first brands all compete at meaningful scale there. Nestlé’s Annual Review 2025 stated that Orgain recorded 33% sales growth in its RTD protein shake range during 2025, which shows that even a competitive category in North America still has room for strong brand expansion. Canada and Mexico are smaller in the regional mix, but both offer room for growth as innovation spreads beyond the U.S. core and digital retail improves access for consumers outside major urban centers.

Europe presents a different operating environment for the plant-based protein supplements market, as demand is shaped by national food habits, strong interest in local and minimally processed ingredients, and tighter rules on health claims. Germany stands out as the region’s most developed sub-market, supported by strong gym participation and consumer willingness to pay for certified clean-label products. The United Kingdom has shown strong product development momentum in plant-based and non-animal protein ingredient launches, while France has seen plant protein sales move further into mainstream grocery channels instead of staying confined to specialty health retail. This means Europe is not a uniform opportunity, and successful brands usually need country-specific positioning, cleaner labels, and careful message control to scale across the region.

Asia-Pacific is forecast to grow at a 9.53% CAGR through 2031, which makes it the fastest-growing regional part of the plant-based protein supplements market size outlook. The region combines several supportive factors at once, including high lactose intolerance rates, rising urban incomes, broader exposure to protein supplementation, and a digital commerce model that can reach consumers without depending heavily on cold-chain infrastructure. The U.S. National Institutes of Health notes that lactose malabsorption exceeds 80% in East Asian populations, which gives dairy-free protein products a strong underlying demand base in several important Asia-Pacific markets. India adds a particularly strong long-term case because of its vegetarian food traditions and domestic pulse-processing base, while Southeast Asia and China are expanding demand through urban middle-class adoption. South America and the Middle East and Africa remain smaller in scale, but Brazil’s soy infrastructure, rising fitness culture, and improving awareness of plant-based nutrition suggest that these regions will continue to add incremental growth to the wider plant-based protein supplements market.

Competitive Landscape

The plant-based protein supplements market remains moderately fragmented, with competition spread across multinational nutrition groups, established supplement companies, digital-first specialists, and a long tail of smaller challenger brands. This structure prevents any single company from taking a dominant position and keeps competition focused on formulation quality, brand trust, and route-to-market strength rather than pure scale alone. Nestlé has shown how large players can still gain share in selected niches, as its Annual Review 2025 noted that Orgain’s RTD protein shake range grew 33% in sales during 2025. At the same time, online health retail is giving newer brands a viable path to scale, and iHerb’s fiscal 2025 performance showed that dedicated digital supplement distribution now has enough reach to influence category structure. The result is a plant-based protein supplements market where leadership depends on maintaining credibility across both product science and consumer access.

A clear area of competition in the plant-based protein supplements market is the shift toward blended proteins that can improve amino acid balance without compromising a clean-label position. ADM’s May 2026 launch of 8 new ingredient solutions for specialty nutrition, beverages, and sports supplements shows that upstream ingredient innovation is still pushing the category forward and giving downstream brands more tools to upgrade product performance. Nestlé Health Science also widened the medical nutrition edge of the category in March 2026 with Compleat Paediatric Oral Blends across seven European markets, using pea and rice proteins in an on-the-go format for children with special medical nutrition needs. These moves show that leading companies are not only competing in mainstream sports nutrition, they are also pushing plant protein deeper into specialty and clinically guided use cases.

White-space opportunities remain strongest in elderly-focused protein support, allergen-aware soy-free blends, and convenient RTD products built for price-sensitive Asia-Pacific consumers. Challenger brands are still relevant because they often move faster on sourcing transparency, organic certification, and multi-source formulation than larger companies with broader portfolios. Incumbents still have advantages in manufacturing scale, retail access, and the ability to spread innovation across powder, bar, RTD, and hybrid formats. That balance means the plant-based protein supplements market is unlikely to tip quickly toward consolidation, even as larger companies continue to strengthen their position through line extensions and targeted innovation. The companies that are likely to perform best will be those that can narrow taste gaps, defend price points, and translate protein quality science into products that feel simple and trustworthy to everyday buyers.

Plant-based Protein Supplements Industry Leaders

Nestlé S.A.

Glanbia plc

Danone S.A.

Herbalife Ltd.

Amway Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Danone's Silk Canada launched the 18g Protein plant-based beverage, the first-to-market high-protein complete-protein plant milk in Canada, available at major grocery retailers nationwide. The product targets mainstream consumers seeking convenient daily protein supplementation beyond dairy.

- March 2026: Nestlé Health Science launched Compleat Paediatric Oral Blends across seven European markets, a first-of-its-kind pediatric nutrition supplement in an on-the-go pouch format formulated with pea and rice proteins alongside 50+ fruits and vegetables. The launch opens the plant protein channel into medically supervised pediatric nutrition.

- February 2026: Sunwarrior introduced the Organic Protein Warrior Blend Performance, delivering 21g of organic plant protein from a blend of pea, mung bean, fava bean, and chia seeds. The multi-source approach targets amino acid completeness for athletes and wellness seekers seeking clean organic certification.

- July 2025: Herbalife launched MultiBurn, its most advanced weight-management supplement, formulated as a plant-based, clean-label product designed to support metabolism, appetite control, and energy. The launch deepened Herbalife's presence in the fast-growing plant-based weight management segment.

Global Plant-based Protein Supplements Market Report Scope

Plant-based protein supplements are nutritional products derived from plant sources that provide protein to support fitness, wellness, and dietary requirements. The plant-based protein supplements market is segmented by source, product type, distribution channel, and geography. By source, the market includes soy protein, pea protein, rice protein, mixed/blended plant protein, and other plant protein sources. Based on product type, the market is categorized into powders, ready-to-drink beverages, protein bars, and other supplement formats. By distribution channel, the market covers supermarkets/hypermarkets, pharmacies and drug stores, online retail, and other distribution channels. By geography, the report covers North America, Europe, Asia-Pacific, South America, and the Middle East and Africa, with market size and forecasts provided for each region. For each segment, market sizing and forecasts have been done on the basis of value (USD) and volume (Tons).

| Soy Protein |

| Pea Protein |

| Rice Protein |

| Mixed/Blended Plant Protein |

| Other Plant Protein |

| Powder |

| Ready-to-drink Beverages |

| Protein Bars |

| Others |

| Supermarkets/Hypermarkets |

| Pharmacies and Drug Stores |

| Online Retail |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Rest of Middle East and Africa |

| By Source | Soy Protein | |

| Pea Protein | ||

| Rice Protein | ||

| Mixed/Blended Plant Protein | ||

| Other Plant Protein | ||

| By Product Type | Powder | |

| Ready-to-drink Beverages | ||

| Protein Bars | ||

| Others | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Pharmacies and Drug Stores | ||

| Online Retail | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current outlook for plant-based protein supplements through 2031?

The plant-based protein supplements market is projected to grow from USD 7.36 billion in 2026 to USD 10.94 billion by 2031 at an 8.25% CAGR, supported by wider daily-use adoption, dairy-free demand, and healthy aging applications.

Which product format leads sales today?

Powders led the category in 2025 with 44.26% share because they offer strong value per gram of protein, flexible usage, and deep roots in sports nutrition.

Which format is growing the fastest?

RTD beverages are forecast to grow at a 9.15% CAGR through 2031 because they fit better into convenience-driven routines and reduce preparation effort for mainstream users.

Why is pea protein still the leading source?

Pea protein held 31.55% share in 2025 because it combines broad familiarity, an allergen-friendly profile, and solid muscle-support positioning, even as blended proteins gain momentum.

Page last updated on: