Protein Ingredients Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 29.77 Billion |

| Market Size (2031) | USD 38.21 Billion |

| Growth Rate (2026 - 2031) | 5.12% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | North America |

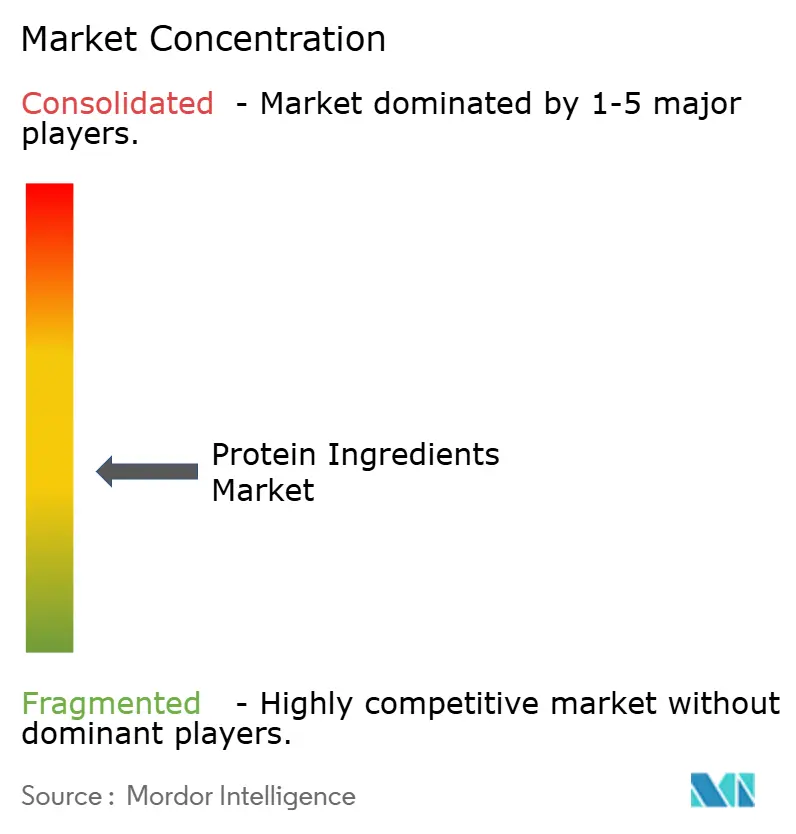

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Protein Ingredients Market Analysis by Mordor Intelligence

The protein ingredients market size was valued at USD 28.32 billion in 2025 and estimated to grow from USD 29.77 billion in 2026 to reach USD 38.21 billion by 2031, at a CAGR of 5.12% during the forecast period (2026-2031). The market growth is driven by increasing demand for diverse and sustainable protein sources, expansion in precision-fermentation capabilities, and robust demand from functional food, beverage, and supplement segments. Plant proteins dominate the market due to expanded regulatory approvals for new crops, while microbial protein production is increasing due to its efficient production methods. North America continues to be the largest revenue generator, with the Middle East showing potential for significant growth through investments in food security initiatives. In technological developments, protein isolates and hydrolysates are gaining market share in premium segments by addressing solubility and taste challenges in ready-to-drink products. The market shows moderate competition, with established agribusiness companies expanding their traditional soy and dairy offerings through biotechnology partnerships, while new entrants develop innovative protein solutions.

Key Report Takeaways

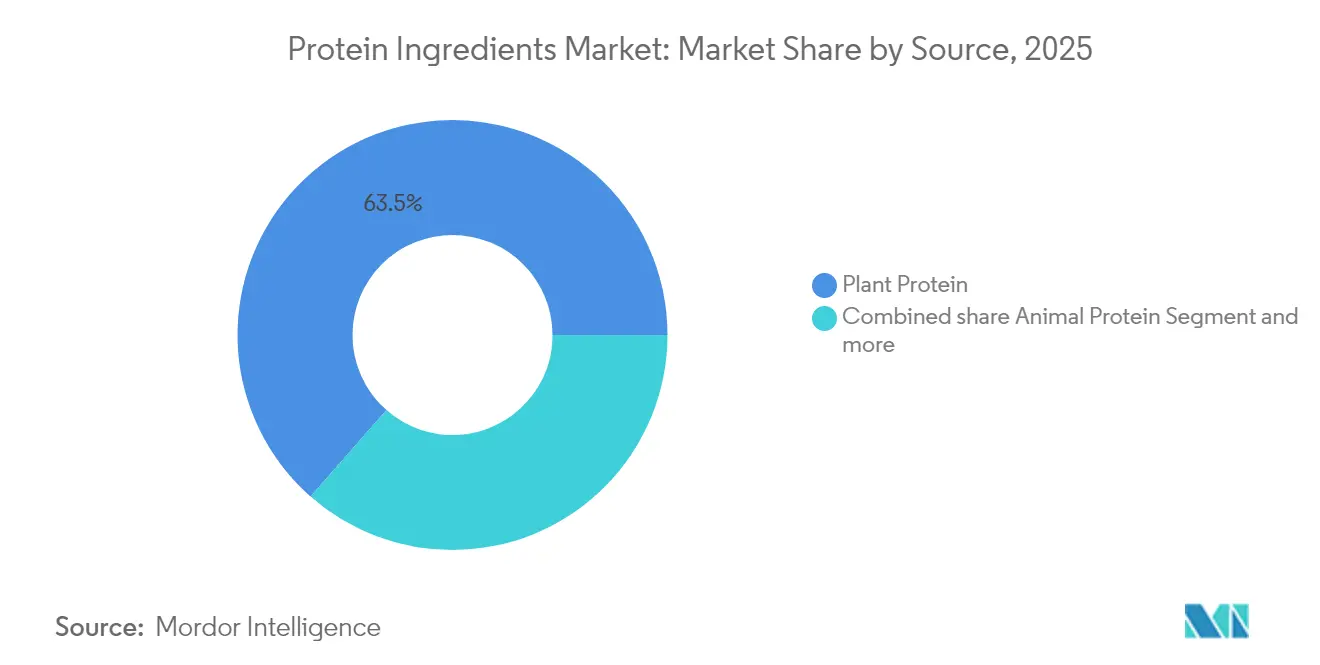

- By source, plant proteins accounted for 63.52% of protein ingredients market share in 2025, while microbial proteins are projected to expand at a 6.29% CAGR to 2031.

- By form, concentrates led with 44.62% revenue share in 2025; isolates are forecast to advance at an 8.18% CAGR through 2031.

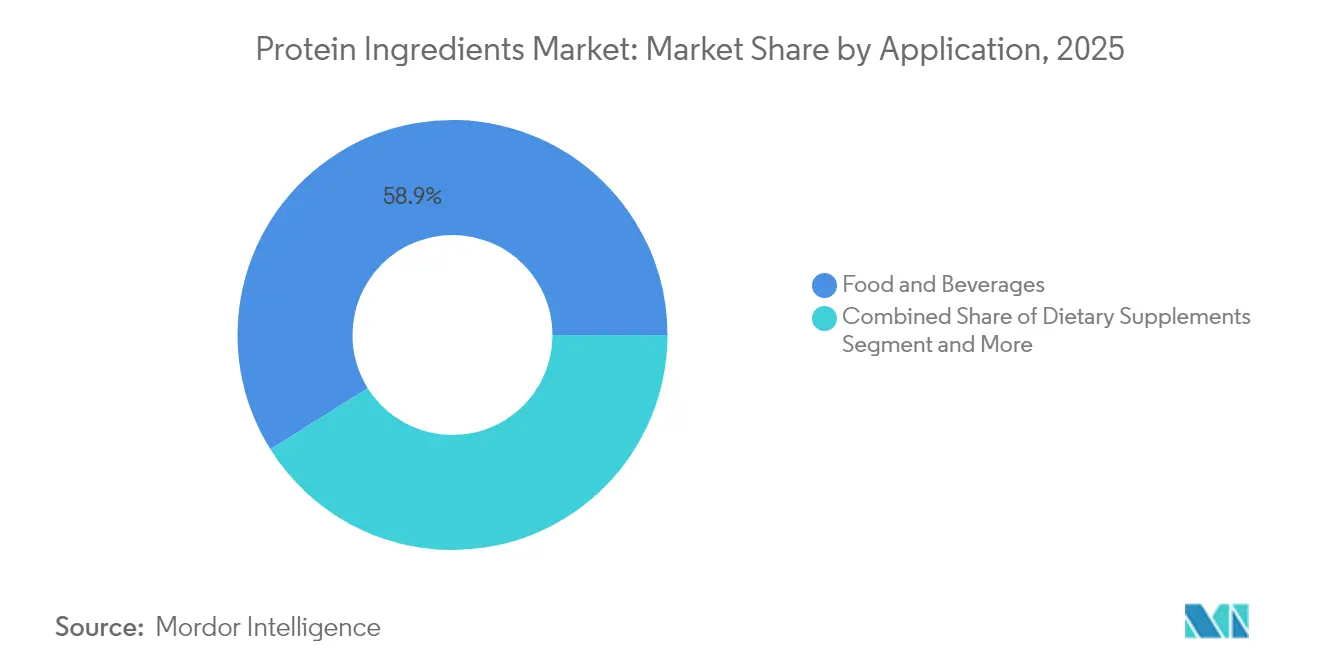

- By application, food and beverage commanded 58.92% of the protein ingredients market size in 2025; dietary supplements and sports nutrition are tracking the fastest growth at 6.12% CAGR to 2031.

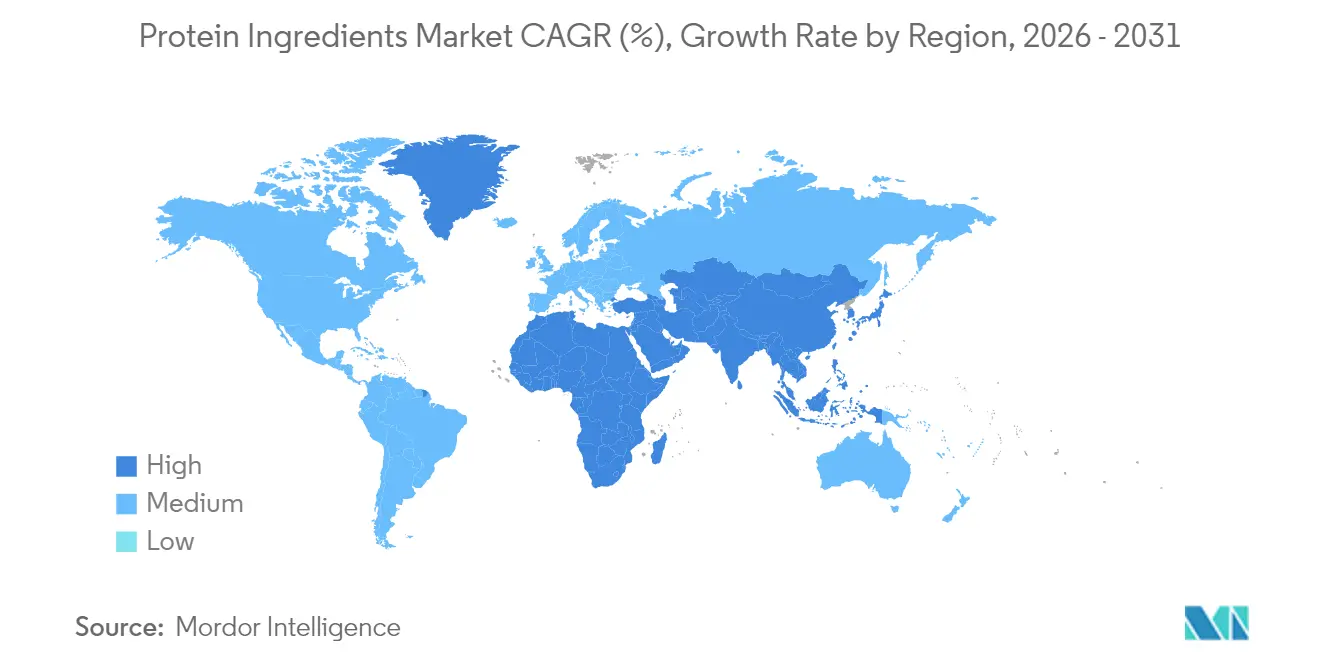

- By geography, North America captured 29.10% of protein ingredients market share in 2025, whereas the Middle East and Africa region is set to grow at 6.41% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Protein Ingredients Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing consumer preference for ready-to-drink protein beverages | +1.2% | Global, with North America and Europe leading adoption | Medium term (2-4 years) |

| Growing production of plant-based meat | +0.9% | North America, Europe, Asia-Pacific core markets | Long term (≥ 4 years) |

| Rising demand for nutritional, fortified and functional foods | +0.8% | Global, with emerging markets showing accelerated growth | Medium term (2-4 years) |

| Increasing demand for sports nutrition | +0.7% | North America, Europe, with spillover to Asia-Pacific | Short term (≤ 2 years) |

| Aging population and rising adoption of preventive healthcare | +0.6% | Global, concentrated in developed economies | Long term (≥ 4 years) |

| Increased application in animal feed and pet food | +0.5% | Global, with Asia-Pacific and North America leading | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Consumer Preference for Ready-to-Drink Protein Beverages

The global market shows an increase in ready-to-drink (RTD) beverage launches with protein content, driving suppliers to develop isolates with improved solubility and heat stability for acidic, shelf-stable products. Precision-fermentation technology allows manufacturers to produce casein and whey alternatives that match dairy functionality without cold-chain requirements. This development has shifted procurement focus from commodity costs to bio-identical performance capabilities. The growth in beverages requires protein manufacturers to create refined, specialized hydrolyzed forms that offer better dispersibility with minimal flavor impact. For instance, companies such as Future Cow are investing in precision fermentation to produce bioidentical milk proteins through yeast fermentation, providing dairy functionality without traditional supply limitations. These technological advancements have made processing compatibility and functional performance key factors in ingredient selection.

Growing Production of Plant-based Meat

Advances in plant-based meat production are fundamentally transforming protein extraction and texturization processes across the global food manufacturing industry. Advanced seed-breeding techniques have yielded peas with 75% protein content, significantly reducing processing requirements and energy consumption throughout the entire manufacturing chain. Major agricultural companies are strategically adapting their business models by investing heavily in alternative protein production facilities, research and development, and innovative technologies. Cargill's February 2024 expansion of its partnership with ENOUGH aims to increase mycoprotein production to over 1 million tons by 2033, highlighting the substantial shift in production capabilities and market demand. The rapid growth of plant-based meat has also influenced regulatory frameworks and compliance requirements, as evidenced by the FDA's revised guidelines for protein quality assessment, which extend beyond the traditional PDCAAS (Protein Digestibility-Corrected Amino Acid Score) method to evaluate complex new protein combinations, formulations, and nutritional profiles in alternative meat products.[1]Source: United Soybean Board, "Protein Content Claims Explained: FDA Recommendations & Labeling Guidelines", soyconnection.com

Rising Demand for Nutritional, Fortified and Functional Foods

The functional foods segment is experiencing a comprehensive transformation in its approach to protein ingredients, with manufacturers increasingly focusing on components that deliver sophisticated, targeted health benefits extending well beyond conventional nutritional value. This evolution has led to the emergence of specialized market categories and premium pricing structures. Protein ingredients are advancing into advanced bioactive applications, where scientifically engineered collagen peptides for precise glycemic control, technologically advanced precision-fermented lactoferrin, and highly refined osteopontin are being strategically integrated into premium infant formula products and comprehensive healthy-aging solutions. The European Union's progressive novel-food clearances for insect-derived protein powders demonstrate the growing regulatory acceptance and market validation of alternative protein sources that efficiently deliver both high-quality protein content and essential functional micronutrients. These significant market developments have contributed to a substantial increase in average selling prices across various product categories, effectively maintaining robust profit margins even during periods of downward pressure on commodity protein prices in the global market.

Increasing Demand for Sports Nutrition

The sports nutrition segment drives innovation in protein ingredients, with manufacturers focusing on improving absorption rates and bioavailability. Technical specifications differentiate premium products from standard offerings in the market. Current sports nutrition formulations incorporate rapid-absorption hydrolysates, specific amino-acid ratios, and natural processing aids to enhance performance. Growing demand in the Asian market has increased the need for protein-electrolyte beverages and acidified milk products, which require proteins with low viscosity and stability across temperature and pH ranges. Manufacturers with global food-safety certifications gain competitive advantages, particularly among consumers who value supply chain transparency. The trend toward clean-label protein ingredients continues, as demonstrated by Kemin obtaining Global Food Safety Initiative (GFSI) certification in June 2024 for their Proteus functional proteins, addressing consumer demands for transparency and quality standards.

Restraints Impact Analysis of Protein Ingredients Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory environment | -0.8% | Global, with Europe and United States having most complex frameworks | Long term (≥ 4 years) |

| Growing allergen concerns | -0.6% | Global, with developed markets showing highest sensitivity | Medium term (2-4 years) |

| Solubility challenges in plant-based protein beverages | -0.4% | Global, with North America and Europe leading RTD adoption | Short term (≤ 2 years) |

| Flavor and texture limitations | -0.3% | Global, with Asia-Pacific showing highest sensitivity to taste | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory Environment

The regulatory approval process for novel protein ingredients presents significant market entry barriers, as approval timelines frequently extend beyond standard product development cycles, benefiting established companies. The European Food Safety Authority's (EFSA) 2025 guidelines require comprehensive documentation for toxicity testing, allergenicity assessments, and detailed production strain analysis, including genetic stability data and metabolic characterization, increasing barriers and giving advantages to companies with in-house regulatory expertise.[2]Source: European Food Safety Authority, “EFSA Guidance on Novel Food Applications 2025,” efsa.europa.eu For insect protein manufacturers, the regulatory landscape is particularly complex, requiring simultaneous compliance with both novel food regulations and animal feed approval processes across multiple jurisdictions. including the EU's Novel Food Regulation, the FDA's GRAS notification system, and various Asia-Pacific regulatory frameworks. This complex regulatory environment drives market consolidation, favoring companies that possess established regulatory expertise and sufficient financial resources to manage extensive documentation requirements and multi-year approval processes.

Growing Allergen Concerns

The emergence of novel protein sources has increased the complexity of allergen management due to new allergenic profiles that current testing methods may not effectively detect. This creates liability concerns and slows market adoption. The risk of cross-reactivity between insect proteins and crustacean allergens, along with post-translational modifications in fermented proteins, requires new detection protocols and clear labeling practices. The European Commission's requirement for explicit allergen statements on insect-derived foods may limit market adoption until consumers become more familiar with these products. Plant protein allergen concerns are expanding beyond traditional sources like soy and wheat to include emerging proteins from legumes and novel crops, requiring more sophisticated allergen management systems throughout the supply chain. Companies that can demonstrate comprehensive allergen control capabilities gain competitive advantages as the industry invests in advanced detection technologies to address these complex allergen profiles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Protein Ingredients Market Segment Analysis

By Source:

Plant Proteins Lead Sustainable TransformationPlant proteins dominated with 63.52% of protein ingredients market revenue in 2025, supported by European Union approval for high-yield aquatic crops like duckweed in February 2025, which achieves 43% protein content.This significant market share reflects increasing consumer demand for plant-based alternatives and substantial investments in production infrastructure. The plant-based protein ingredients market is expected to grow steadily through 2031, driven by new large-scale fractionation facilities in North America and Europe, enhanced processing technologies, and expanding applications across food and beverage sectors. Microbial proteins, while an emerging segment, are growing at a 6.29% CAGR, benefiting from CO₂-fed fermentation systems that minimize land and water usage while improving sustainability metrics. These innovative production methods are attracting significant research and development investment from major food manufacturers.

The industry is evolving toward sophisticated hybrid protein formulations that combine plant, microbial, and select animal-source proteins to optimize nutrition, functionality, and cost. These blends address specific market needs across various applications, from sports nutrition to meat alternatives. While dairy-derived whey and casein proteins remain important in applications requiring complete amino-acid profiles and established supply chains, their market share is decreasing as alternative proteins gain regulatory approval and demonstrate improved functionality. Insect proteins represent a small but significant segment, with mealworm approvals in pet food applications creating potential pathways for future human food applications. The segment is experiencing increased investment in production facilities and research into extraction methods.

By Form:

Isolates Drive Premium ApplicationsConcentrates maintained a dominant market share of 44.62% in 2025, attributed to their cost-effectiveness, versatility, and broad applicability across food products, including baked goods, snacks, and processed foods. The lower production costs and simpler processing requirements make concentrates particularly attractive for mass-market applications. Isolates are projected to grow at an 8.18% CAGR, driven by beverage and clinical-nutrition manufacturers requiring proteins with ≥90% purity for clean label claims, enhanced functionality, and superior nutritional performance. The launch of NUTRALYS Fava S900M by Roquette in May 2024, achieving 90% protein content in fava bean isolates, demonstrates the technological advancements in extraction and purification processes supporting isolate adoption in premium applications.

Hydrolyzed and textured protein variants serve distinct market segments: hydrolysates provide rapid absorption and improved digestibility for sports nutrition products, medical foods, and infant formulas, while textured proteins create the complex fibrous structures and meat-like texture needed for plant-based burgers, nuggets, sausages, and other meat alternatives. The implementation of continuous-flow enzymatic processes and energy-efficient membrane systems increases production yields across all protein forms while reducing water consumption, helping companies meet both profitability targets and environmental sustainability goals in their manufacturing operations. These technological improvements have also led to enhanced protein quality, reduced processing time, and improved cost efficiency across the production chain.

By Application:

Food & Beverage Dominance with Supplement GrowthFood and beverage applications account for 58.92% of the protein ingredients market share in 2025, driven by extensive protein fortification across bakery products, dairy items, snack foods, and ready-to-drink beverages. Product development focuses on advanced clean-label stabilization techniques to maintain product texture, mouthfeel, flavor profiles, and shelf stability with increased protein content. The supplements and sports nutrition segments are growing at a 6.12% CAGR, driven by increased consumer adoption of active lifestyles, widespread e-commerce accessibility through platforms like Amazon and specialized retailers, and scientifically validated product claims supported by clinical studies.

The animal feed and pet food segments are experiencing rapid transformation with insect-based proteins (black soldier fly larvae, mealworms) and single-cell protein alternatives (yeast, algae, bacteria) replacing traditional fishmeal sources, reducing supply chain uncertainties and environmental impacts such as overfishing and marine ecosystem disruption. The personal care segment is incorporating specialized collagen and elastin peptides in topical formulations, including anti-aging serums, moisturizing creams, and regenerative lotions, creating market opportunities for manufacturers who can comply with both food and cosmetic Good Manufacturing Practice standards while ensuring product efficacy and safety.

Geography Analysis

North America Protein Ingredients Market

North America accounts for 29.10% of 2025 revenue, influencing global specifications through its advanced dairy processing and biotechnology infrastructure. The region's sophisticated processing facilities, research institutions, and established supply networks create an ecosystem that sets industry standards. The United States and Canada are expanding capacity through significant investments in plant protein extraction facilities and precision fermentation technologies, while efficient regulatory frameworks facilitate new product introductions across multiple protein categories.

Europe Protein Ingredients Market

Europe maintains growth through favorable novel food policies and consumer adoption of sustainable diets. The region's comprehensive regulatory framework and streamlined approval process has accelerated the commercialization of alternative proteins. Insect farming operations, algae cultivation facilities, and mycelium-based protein production centers are scaling up operations, with mainstream retailers incorporating these ingredients into an expanding range of private-label products.

MEA Protein Ingredients Market

The Middle East and Africa region demonstrates the highest growth at 6.41% CAGR, supported by government-backed diversification initiatives. Saudi Arabia's USD 70 million investment in single-cell protein technology encompasses research facilities, production infrastructure, and workforce development programs. The UAE's agricultural land-lease programs in Africa include technology transfer agreements, logistics partnerships, and market access provisions. These initiatives reduce import reliance and establish export-oriented protein ingredient production centers with integrated value chains.

Competitive Landscape

The protein ingredients market exhibits a concentration ratio of 4 out of 10, indicating moderate fragmentation. Major agribusiness companies strengthen their positions through product development. In January 2025, Axiom Foods introduced Oryzatein 2.0, a rice protein designed for infant food formulations, featuring non-GMO, hexane-free properties with smooth texture and enhanced digestibility.

Companies such as Archer Daniels Midland Company, Cargill Incorporated, Roquette Frères, FrieslandCampina Ingredients, and Kerry Group plc operate in specialized market segments. These organizations differentiate themselves through reduced carbon emissions and clean-label products. They utilize venture capital funding for proprietary technology development and form partnerships with established manufacturers to access markets efficiently.

The market experiences frequent mergers and acquisitions, driven by companies seeking to expand their product portfolios and geographical presence. Industry certifications, exemplified by Kemin's Global Food Safety Initiative approval, strengthen credibility with brand owners and enable integration into multinational supply chains. These certifications also help companies meet stringent regulatory requirements and demonstrate their commitment to quality and safety standards.

Protein Ingredients Industry Leaders

-

Archer Daniels Midland Company

-

Cargill Incorporated

-

Kerry Group plc

-

Roquette Frères

-

FrieslandCampina Ingredients

- *Disclaimer: Major Players sorted in no particular order

Protein Ingredients Market Companies Covered in this Report

- Archer Daniels Midland Company

- Cargill Incorporated

- Kerry Group plc

- Roquette Freres

- Fonterra Co-operative Group Ltd.

- FrieslandCampina Ingredients

- Glanbia plc

- DuPont de Nemours, Inc. (IFF Nourish)

- BASF SE

- Ingredion Incorporated

- Darling Ingredients Inc.

- CP Kelco

- Axiom Foods Inc.

- Burcon NutraScience Corp.

- Tate and Lyle PLC

- MycoTechnology Inc.

- Calysta Inc.

- NOW Foods

- AMCO Protein

- Kewpie Corporation

Recent Industry Developments in Protein Ingredients Market

- May 2025: Arla Foods Ingredients expanded its distribution partnership with Brenntag Group to include the three largest food and nutrition markets in Southeast Asia. Through this partnership, Brenntag distributes Arla's protein ingredient portfolio in Vietnam, Thailand, and Indonesia.

- May 2025: Bunge Limited invested EUR 484 million in a soy protein concentrate facility in Morristown, Indiana. The facility produces soy protein concentrates and includes quality testing laboratories. This investment aligns with Bunge's strategy to expand its plant-based protein portfolio.

- May 2025: Darling Ingredients Inc. and Tessenderlo Group signed a non-binding term sheet to merge their collagen and gelatin segments into a new company, Nextida. The merger aims to capitalize on the growing demand for collagen-based health and wellness products.

- January 2025: Cargill, Incorporated has made strides in 3D printing and mycoprotein technologies, successfully tackling the taste and texture hurdles that have long challenged the alternative protein industry. These advancements play a pivotal role in developing products that not only match the flavor and texture of traditional meat but also align in price.

Global Protein Ingredients Market Report Scope

The global protein ingredients market is segmented by source, which is classified as the animal source, and plant source. The animal source is sub-segmented into dairy protein, egg protein, gelatin, and others and similarly, plant source is classified as soy protein, wheat protein, and vegetable protein. By application, the market is classified as animal feed, food & beverage, infant formulations, cosmetics & personal care, and pharmaceuticals. Also, the study provides an analysis of the protein ingredients market in the emerging and established markets across the world, including North America, Europe, Asia-Pacific, South America, and Middle East & Africa.

Segmentation Overview

| Animal Protein | Dairy Ingredients | Whey Protein Concentrates |

| Whey Protein Hydrolysates | ||

| Whey Protein Isolates | ||

| Casein and Caseinates | ||

| Egg Protein | ||

| Gelatin and Collagen | ||

| Other Animal Proteins | ||

| Plant Proteins | Soy | |

| Pea | ||

| Wheat | ||

| Rice | ||

| Potato | ||

| Hemp | ||

| Others | ||

| Microbial Proteins | Mycoprotein | |

| Algea Protein | ||

| Insect Protein |

| Concentrates |

| Isolates |

| Textured/Hydrolyzed |

| Food and Beverage | Bakery and Confectionery |

| Meat Analogs and Extenders | |

| Dairy Alternatives | |

| Savoury Snacks and Bars | |

| Beverages | |

| Infant and Early-Life Nutrition | |

| Dietary Supplements and Sports Nutrition | |

| Animal Feed | |

| Personal Care and Cosmetics | |

| Pharmaceuticals and Clinical Nutrition |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle East and Africa |

| By Source | Animal Protein | Dairy Ingredients | Whey Protein Concentrates |

| Whey Protein Hydrolysates | |||

| Whey Protein Isolates | |||

| Casein and Caseinates | |||

| Egg Protein | |||

| Gelatin and Collagen | |||

| Other Animal Proteins | |||

| Plant Proteins | Soy | ||

| Pea | |||

| Wheat | |||

| Rice | |||

| Potato | |||

| Hemp | |||

| Others | |||

| Microbial Proteins | Mycoprotein | ||

| Algea Protein | |||

| Insect Protein | |||

| By Form | Concentrates | ||

| Isolates | |||

| Textured/Hydrolyzed | |||

| By Application | Food and Beverage | Bakery and Confectionery | |

| Meat Analogs and Extenders | |||

| Dairy Alternatives | |||

| Savoury Snacks and Bars | |||

| Beverages | |||

| Infant and Early-Life Nutrition | |||

| Dietary Supplements and Sports Nutrition | |||

| Animal Feed | |||

| Personal Care and Cosmetics | |||

| Pharmaceuticals and Clinical Nutrition | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Rest of North America | |||

| Europe | Germany | ||

| France | |||

| United Kingdom | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Saudi Arabia | ||

| United Arab Emirates | |||

| South Africa | |||

| Rest of Middle East and Africa | |||

Key Questions Answered in the Report

What is the current size of the protein ingredients market?

The protein ingredients market size stands at USD 29.77 billion in 2026 and is projected to reach USD 38.21 billion by 2031.

Which protein source holds the largest market share?

Plant proteins command the largest share at 63.52% of 2025 revenue, reflecting consumer demand for sustainable options.

Which region is growing the fastest?

The Middle East and Africa region leads with a 6.41% CAGR forecast, driven by food-security investments in alternative protein facilities.

Why are isolates growing faster than concentrates?

Isolates offer ≥90% purity and superior solubility, attributes sought in premium beverages and clinical-nutrition products, supporting their 8.18% CAGR.

Page last updated on: