Pension Administration Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

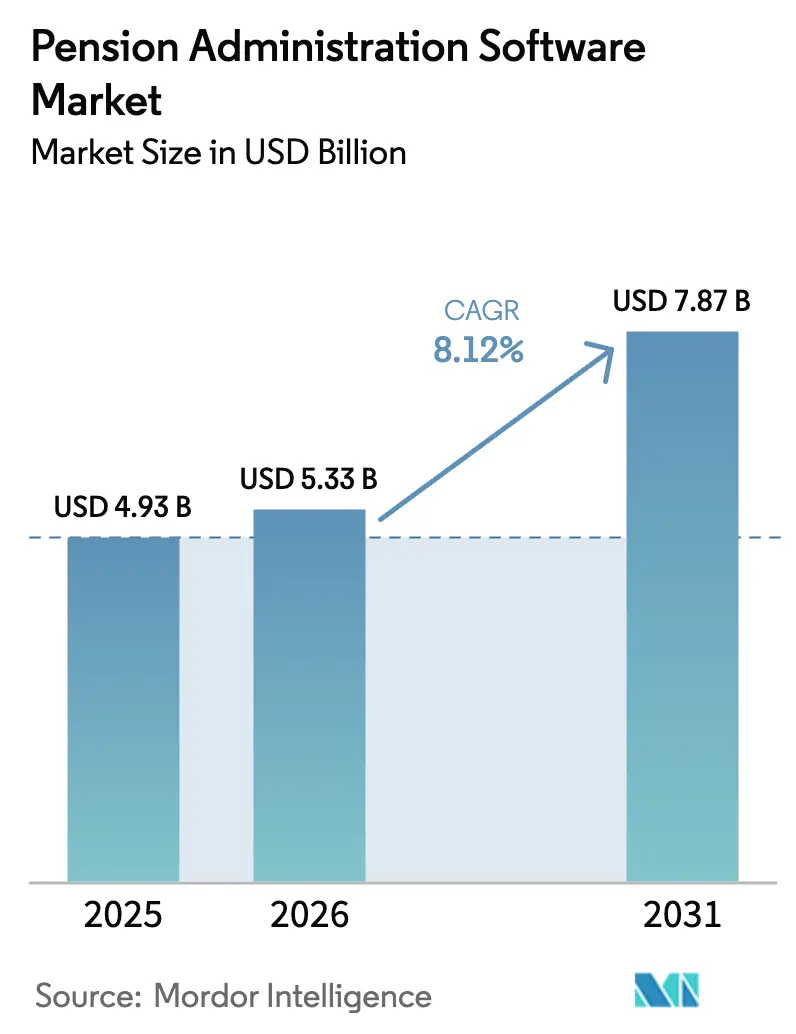

| Market Size (2026) | USD 5.33 Billion |

| Market Size (2031) | USD 7.87 Billion |

| Growth Rate (2026 - 2031) | 8.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pension Administration Software Market Analysis by Mordor Intelligence

The pension administration software market size is expected to grow from USD 4.93 billion in 2025 to USD 5.33 billion in 2026 and is forecast to reach USD 7.87 billion by 2031 at 8.12% CAGR over 2026-2031. Growth is propelled by accelerated digitization, regulatory pressure for real-time reporting, and the urgent replacement of aging legacy systems. Organizations are shifting workloads to the cloud to avoid hardware refresh cycles and shrink IT overhead, while public-sector modernization mandates inject sizable budgets into system upgrades. At the same time, cybersecurity incidents and integration costs temper the pace of adoption, creating a dynamic landscape in which vendors differentiate through AI-enabled analytics, automated compliance, and intuitive self-service portals.

Key Report Takeaways

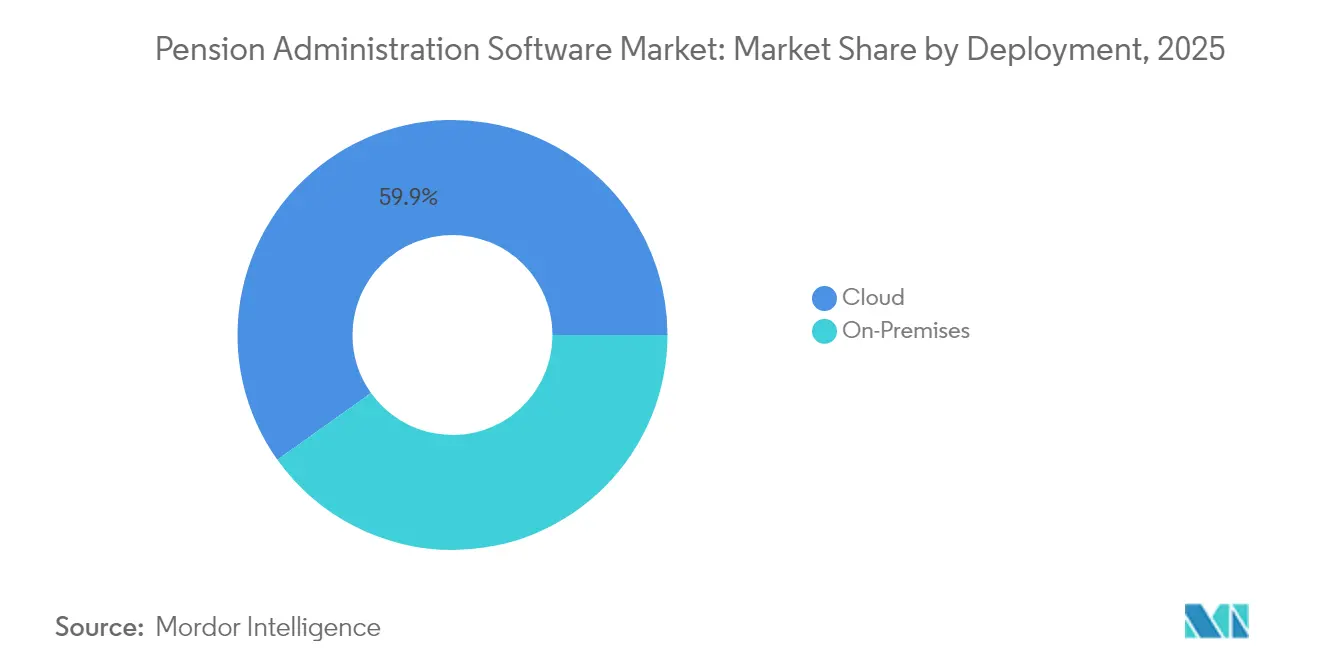

- By deployment, cloud models held 59.85% of the pension administration software market share in 2025, and this segment is expanding at a 12.35% CAGR to 2031.

- By enterprise size, government entities led with 42.35% revenue share in 2025, while SMEs posted the quickest rise at an 10.62% CAGR through 2031.

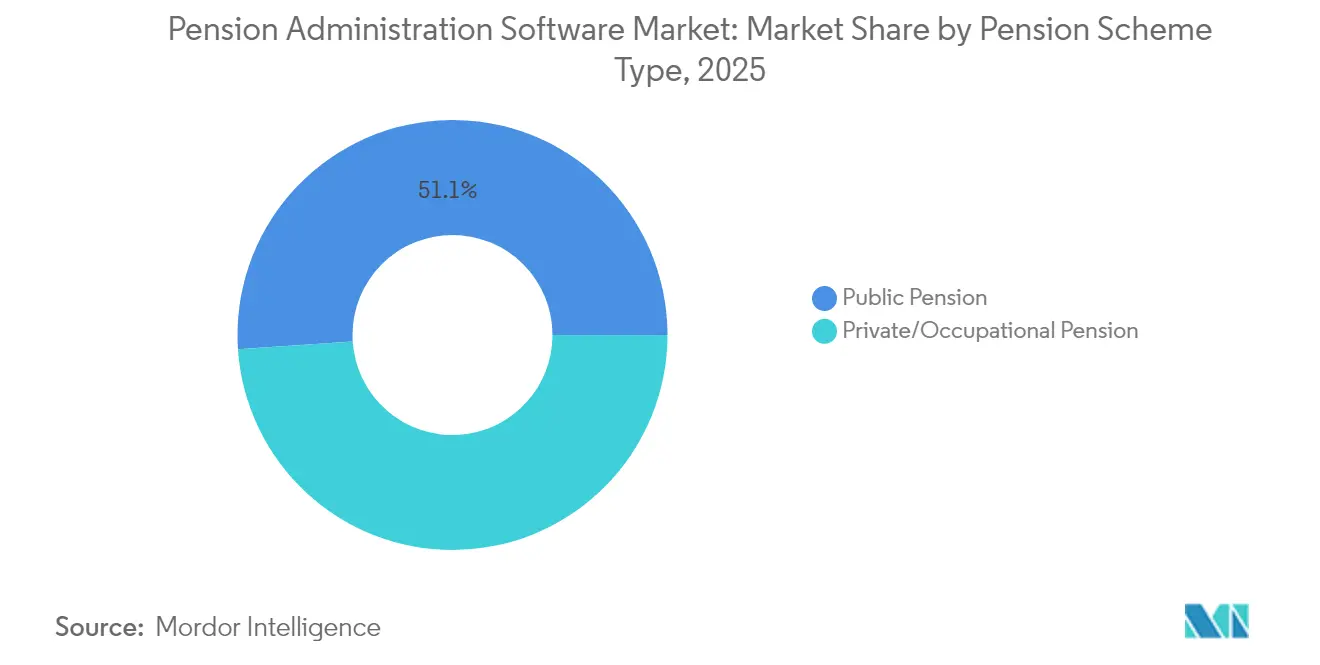

- By pension scheme type, public plans accounted for 51.05% of the pension administration software market size in 2025; private and occupational schemes are on track for a 9.98% CAGR to 2031.

- By functionality, contribution and payroll processing remained the largest category at 26.55% in 2025, whereas self-service portals are advancing at a 12.05% CAGR to 2031.

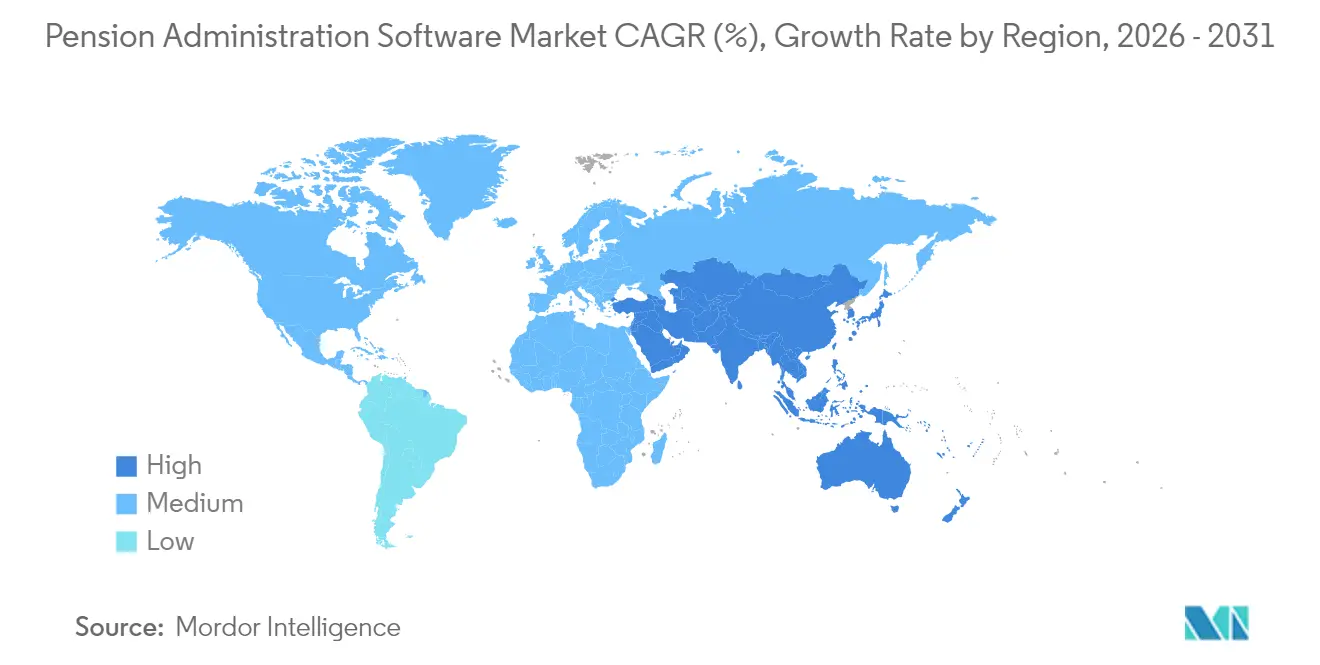

- By geography, North America dominated with 33.85% market share in 2025, and Asia-Pacific is growing the fastest at 13.35% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Pension Administration Software Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-native deployments slash IT overhead | +2.1% | North America and EU first movers; global diffusion | Medium term (2-4 years) |

| Regulatory shift toward real-time reporting | +1.8% | Led by US ERISA and EU GDPR | Short term (≤ 2 years) |

| Public-sector modernization mandates | +1.5% | North America and APAC core; spill-over to EU | Medium term (2-4 years) |

| Ageing workforce boosts pension complexity | +1.2% | Developed economies worldwide | Long term (≥ 4 years) |

| AI-based risk analytics gain traction | +0.9% | North America and EU early adopters; APAC catching up | Medium term (2-4 years) |

| Tokenised pension asset pilots | +0.4% | US, UK, Singapore | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cloud-native Deployments Slash IT Overhead

Moving pension workloads to cloud environments is producing 30–40% reductions in total cost of ownership, helped by vendors such as Oracle, whose 2024 filings show cloud services rising to 37% of revenue after USD 8.9 billion of R&D spending. SAP’s Q1 2024 results mirror this pattern with 24% cloud revenue growth, backed by an EUR 14.2 billion (USD 16.49 billion) backlog. Despite these gains, agencies migrating from on-premises systems—Wiltshire Pension Fund is a notable example—encounter temporary cost spikes linked to data reconciliation and staff retraining.

Regulatory Shift Toward Real-time Reporting

The January 2025 U.S. Department of Justice rule restricting access to sensitive personal data intensifies compliance demands for pension systems that handle cross-border information, with enforcement commencing in April 2025. The Department of Labor’s Field Assistance Bulletin 2025-02 lays out additional annual funding notice stipulations under the SECURE 2.0 Act.[2]U.S. Department of Labor, “Field Assistance Bulletin 2025-02,” dol.gov European guidelines are tightening concurrently, as EIOPA reviews sustainability risk disclosures that require ESG data capture.

Public-sector Modernization Mandates

Governments are reallocating significant budgets to overhaul aging platforms. The U.S. Technology Modernization Fund granted USD 18.3 million to the Office of Personnel Management in December 2024 to migrate systems supporting 2.8 million annuitants.[1]U.S. General Services Administration, “Technology Modernization Fund Announces Investments,” gsa.gov California Teachers’ Retirement System is investing USD 523.1 million to finish its Pension Solution Project by late 2025. In Asia, China’s 2025 Government Work Report underscores expanded digital infrastructure spending to prepare for demographic shifts.

Ageing Workforce Boosts Pension Complexity

Rising life expectancy increases the intricacy of benefit calculations, pushing administrators toward configurable software that can manage multiple plan designs. The Virginia Retirement System disbursed USD 6.47 billion in 2024 while serving more than 832,000 members across varied schemes. Emerging markets follow suit, with Somalia introducing a defined-benefit plan for civil servants in 2024 that employs career-average formulas. Multiple Latin American reforms, led by Mexico’s lower retirement age and Panama’s proposed hikes, create further software complexity.

Restraints Impact Analysis of Pension Administration Software Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising migration and integration costs | -1.4% | Most acute in North America and EU | Short term (≤ 2 years) |

| Cyber-security and data-sovereignty concerns | -0.8% | Global; amplified in cross-border operations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Migration and Integration Costs

CEM Benchmarking calculates that pension administration expenses jumped 15.6% year-on-year in 2024, nearly triple the peer average, lifting total cost per member to USD 51. Smaller plans face an added burden: SECURE 2.0’s automatic-enrollment mandate, effective January 2025, introduces compliance work that pushes many SMEs toward external solutions. Each year’s IRS cost-of-living adjustments compel continuous software updates, inflating operating budgets.

Cyber-security And Data-sovereignty Concerns

The December 2024 breach at Carruth Compliance Consulting exposed personally identifiable information for more than 40,000 education workers and generated multiple lawsuits. Public retirement associations warn that inadequate vendor vetting and minimal employee training combine to heighten breach risk. At a policy level, new U.S. data-sovereignty rules restrict foreign access to sensitive records, which may narrow hosting options for global plans seeking unified platforms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Pension Administration Software Market Segment Analysis

By Deployment:

Cloud Dominance Accelerates Infrastructure TransformationCloud models claimed 59.85% of the pension administration software market share in 2025, outstripping on-premises alternatives and projecting a 12.35% CAGR through 2031. This momentum stems from lower ownership costs and elastic scaling that better match fluctuating member volumes. The pension administration software market size attached to cloud platforms is on course to multiply as agencies fund multi-year conversions. Migration, however, exposes complexity in data validation and retraining, often leading to interim cost spikes. Hybrid environments are now bridging the gap, enabling sensitive data to stay behind a firewall while analytics leverage cloud horsepower.

On-premises deployments persist in jurisdictions with stringent data localization mandates or entrenched infrastructure investments. Yet as leading vendors secure ISO 27001 certifications and sovereign-cloud offerings expand, the value proposition of pure on-premises stacks erodes. Investment disbursements such as the USD 18.3 million Technology Modernization Fund grant underline how public budgets are migrating to cloud-first architectures.

By Enterprise Size:

Government Leadership Drives SME AccelerationPublic entities dominated the pension administration software market with a 42.35% share in 2025, reflecting the scale of government benefit obligations and the rigor of statutory reporting. Even so, SMEs register the fastest expansion at 10.62% CAGR to 2031 as subscription pricing lowers entry barriers. Mandatory automatic enrollment under SECURE 2.0 intensifies compliance pressures on small plans that lack in-house expertise, steering them into turnkey cloud services.

Large employers continue steady adoption, focusing on deep analytics and multi-plan coordination. The pension administration software market size allocated to SMEs remains comparatively small, but its growth trajectory signals democratization of capabilities once reserved for billion-dollar plans.

By Pension Scheme Type:

Private Sector Innovation Challenges Public DominancePublic schemes controlled 51.05% of global revenue in 2025, yet private and occupational schemes are set for a 9.98% CAGR to 2031 as employers seek agile tools that integrate actuarial insight with HR platforms. Private providers such as Smart Pension leverage technology to consolidate assets quickly, evidenced by ten master-trust acquisitions that lifted its assets to GBP 6 billion (USD 7.4 billion) in 2024.

Public plans wield budget stability and clear oversight but face lengthier procurement cycles. Meanwhile, the pension administration software market share held by private schemes expands as employers chase faster member services and automated contribution management.

By Functionality:

Self-Service Portals Lead Digital Member Experience RevolutionContribution and payroll processing accounted for 26.55% of 2025 revenue, yet self-service portals deliver the fastest rise at 12.05% CAGR; they streamline transactions and meet member expectations for on-demand access. Secure portals enable retirees to update information, view statements, and initiate withdrawals without administrator intervention, cutting call volumes and latency.

Risk and actuarial analytics gain ground as longevity and investment volatility challenge funding strategies. Administrators demand unified dashboards that overlay AI-driven models on contribution data, reinforcing the pension administration software market's ambition to cover every step from enrolment to payout within a single stack.

Geography Analysis

North America Pension Administration Software Market

North America held 33.85% of 2025 revenue, buoyed by large-scale modernization such as the USD 523.1 million CalSTRS Pension Solution Project and the USD 18.3 million OPM upgrade, both aimed at eliminating 1990s-era platforms. SECURE 2.0 adds fresh compliance layers that improve commercial prospects for domestic vendors skilled in U.S. regulation. Canada and Mexico inject additional opportunities through phased reforms and age-eligibility changes.

Europe Pension Administration Software Market

Europe maintains solid momentum as GDPR and evolving ESG rules pressure pension trustees to improve data governance and sustainability disclosures. EIOPA consultations on prudential treatment of climate risk and the growing prevalence of net-zero targets across 29% of European funds reinforce software demand for granular asset tagging and emissions tracking. The pension administration software market size for EU jurisdictions grows steadily, with vendors tailoring multilingual interfaces and data-protection controls.

APAC and MEA Pension Administration Software Market

Asia-Pacific outpaces all regions with a 13.35% CAGR through 2031. China’s plan to channel long-term pension capital into domestic markets requires robust risk and portfolio analytics, while Japan accelerates digital government commitments that include modern pension records. India, Singapore, and Australia diversify demand with blockchain pilots and advanced mobile services, positioning the pension administration software market as a critical layer in national aging strategies. Regions in the Middle East and Africa enter earlier stages of reform, signalling future lift once legislative frameworks solidify.

Competitive Landscape

Competition is moderately fragmented. Oracle and SAP command entrenched client bases, leveraging extensive R&D and global delivery teams; Oracle devoted USD 8.9 billion to research in 2024 and now earns 37% of revenue from cloud services. Specialized vendors such as Sagitec Solutions focus on public-sector tenders, securing a spot on the GovTech 100 list as proof of niche expertise.

Smart Pension underscores consolidation trends, completing its tenth master trust acquisition in March 2025, thereby topping GBP 6 billion (USD 8.17 billion) in assets and using proprietary platforms to streamline onboarding. Alight Solutions, after divesting non-core segments for USD 1.0 billion, doubles down on its Worklife platform to deepen benefits administration and wellness features.

Product differentiation increasingly rests on AI-enabled fraud detection, configurable APIs, and sovereign-cloud deployment options. Vendors cultivate partnerships with analytics firms and cybersecurity specialists to address data-sovereignty hurdles highlighted by the 2024 Carruth breach. Talent scarcity presents a systemic risk: a 2025 Financial Services Skills Commission survey flags data analysis and AI as the most acute gaps hindering implementation speed.

Pension Administration Software Industry Leaders

Heywood Limited

Milliman, Inc.

SAP SE

Oracle Corporation

Capita plc.

- *Disclaimer: Major Players sorted in no particular order

Pension Administration Software Market Companies Covered in this Report

- Oracle Corporation

- SAP SE

- Capita plc

- Equiniti Group plc

- Civica Group

- Heywood Limited

- Sagitec Solutions

- Milliman Inc.

- Buck Global LLC

- Smart Pension Ltd.

- Alight Solutions

- LandP Systems Ltd.

- Aon plc

- Mercer LLC

- PensionSoft Ltd.

- Aquila Heywood

- Vitech Systems Group

- Itek Systems Management

- PensionFusion

- FIS Global

Recent Industry Developments in Pension Administration Software Market

- March 2025: Smart Pension completed its tenth master trust acquisition, transferring GBP 545 million (USD 673 million) and raising AUM to GBP 6 billion (USD 7.4 billion).

- February 2025: Alight Solutions sold its Professional Services and Payroll & HCM Outsourcing units for USD 1.0 billion plus contingent payments to focus on its Worklife platform.

- January 2025: The U.S. Department of Justice issued a final rule restricting access to sensitive personal data by countries of concern, with enforcement from Apr 2025.

- December 2024: The Technology Modernization Fund awarded USD 18.3 million to the Office of Personnel Management to modernize retirement systems.

Pension Administration Software Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the pension administration software market as packaged platforms and cloud services that calculate benefits, collect and reconcile contributions, keep participant records, and execute compliant disbursements for public and private pension schemes worldwide. The definition captures license, subscription, and maintenance revenue tied directly to these functions, and we, therefore, anchor every data point on that boundary.

Scope exclusion: Solutions aimed only at personal finance or wealth management for individuals are outside scope.

Segments Covered in This Report

- By Deployment

- Cloud

- On-Premises

- By Enterprise Size

- SMEs

- Large Enterprises

- Government Entities

- By Pension Scheme Type

- Public Pension

- Private/Occupational Pension

- By Functionality

- Contribution and Payroll Processing

- Benefit Calculation and Disbursement

- Compliance and Reporting

- Risk and Actuarial Analytics

- Self-Service Portals

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East

- Israel

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Mordor analysts interviewed software vendors, state plan trustees, actuaries, and payroll integrators across North America, Europe, and Asia-Pacific. These conversations clarified average selling prices, cloud migration pace, and regional compliance costs that desk work alone could not surface.

Desk Research

We relied first on open, high-quality datasets such as OECD Pension Statistics, the US Bureau of Labor Statistics, EIOPA dashboards, Canada's OSFI filings, and SEC rulemakings. Annual reports, 10-Ks, and investor decks gave cost curves and adoption milestones, while news archives from Dow Jones Factiva and company intelligence from D&B Hoovers helped us, the analyst team, cross-verify vendor revenue splits. Many other public records and trade releases were also reviewed; the listed sources are illustrative, not exhaustive.

Market-Sizing & Forecasting

We built a top-down model beginning with global pension participant counts and average administration spend, which are then split by deployment mode and buyer type. Totals are checked through selective bottom-up lenses such as vendor revenue roll-ups and sampled ASP x user volumes. Key variables like cloud uptake, digitization mandates, average participants per plan, inflation-adjusted ASPs, and plan churn feed a multivariate regression that projects demand to 2030. Any data gap is bridged with regional benchmarks before final calibration.

Data Validation & Update Cycle

Every draft passes triple analyst review; material events like major mergers or new regulation trigger a mid-cycle refresh. Models are revisited annually so clients receive the latest baseline.

How Mordor Intelligence's Pension Administration Software Market Size Compares to Other Published Estimates

Published estimates often diverge because each firm picks its own scope, pricing levers, currency bases, and refresh cadence.

By fixing scope first and re-checking inputs through primary calls, Mordor delivers a balanced, transparent number that decision-makers can trace back to clear variables.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.93 B (2025) | Mordor Intelligence | - |

| USD 3.60 B (2023) | Global Consultancy A | Excludes cloud subscriptions and Asia-Pacific buyers |

| USD 4.50 B (2022) | Industry Association B | Bundles legacy benefits modules with pension tools |

| USD 5.00 B (2024) | Research Boutique C | Adds implementation service revenue to software totals |

These comparisons show that when scope alignment, variable selection, and timely reviews are applied consistently, Mordor Intelligence provides the most dependable starting point for strategy and investment planning.

Key Questions Answered in the Report

What is driving the current demand for pension administration software?

Regulatory pressure for real-time reporting, cloud-native cost savings, and government mandates to modernize legacy systems are the leading demand catalysts.

How fast is the pension administration software market expected to grow?

The market is projected to rise from USD 5.33 billion in 2026 to USD 7.87 billion by 2031, delivering an 8.12% CAGR.

Which deployment model is gaining the most traction?

Cloud-based deployments already represent 59.85% of 2025 revenue and are advancing at a 12.35% CAGR as administrators shift away from on-premises hardware.

Why are self-service portals becoming so important?

Portals give members instant access to statements and benefit calculations, reducing call-center loads and expanding at a 12.05% CAGR—faster than any other functional category.

Which region offers the highest growth potential?

Asia-Pacific leads with a 13.35% CAGR to 2031, fueled by large-scale pension digitization programs in China, Japan, and India.

What are the main obstacles to adoption?

High migration costs for legacy data and rising cyber-security risks, highlighted by recent breaches, remain the top restraints for new system rollouts.

Page last updated on: