Candidate Relationship Management Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

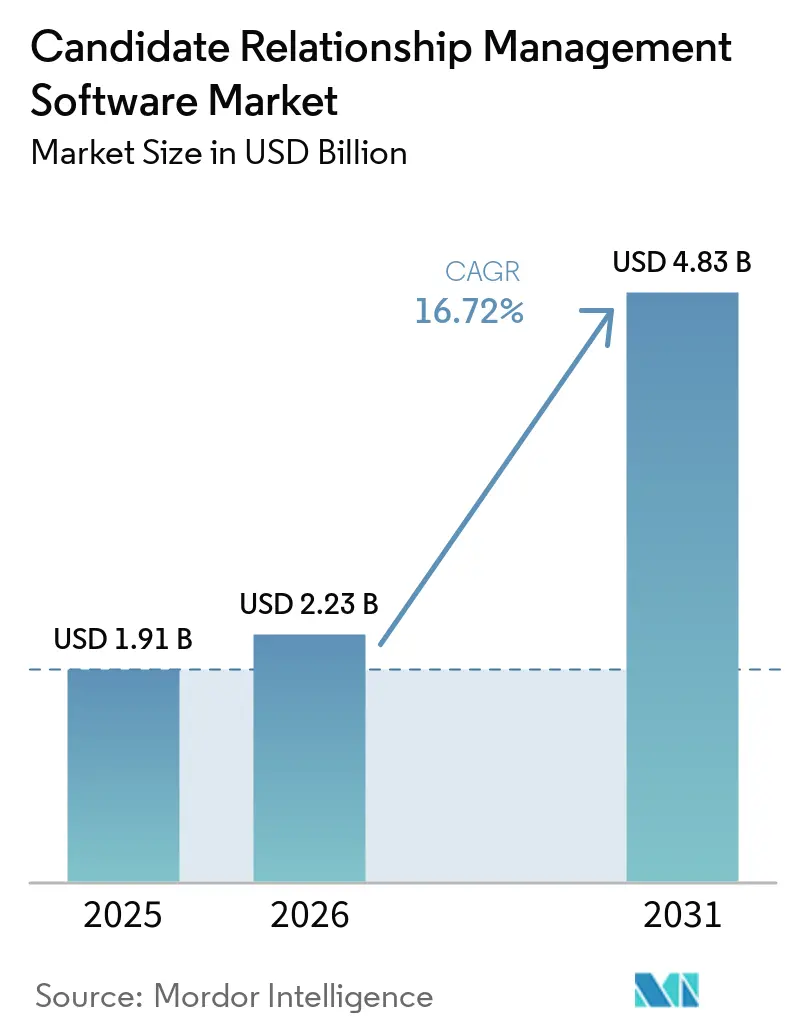

| Market Size (2026) | USD 2.23 Billion |

| Market Size (2031) | USD 4.83 Billion |

| Growth Rate (2026 - 2031) | 16.72% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Candidate Relationship Management Software Market Analysis by Mordor Intelligence

The candidate relationship management software market size is projected to be USD 1.91 billion in 2025, USD 2.23 billion in 2026, and reach USD 4.83 billion by 2031, growing at a CAGR of 16.72% from 2026 to 2031. The candidate relationship management software market is expanding because hiring teams are moving away from reactive applicant tracking and toward ongoing talent pipeline management that keeps candidates warm before roles open. Persistent shortages in technology, clinical healthcare, and advanced manufacturing continue to make transactional hiring costly for large employers, which increases the value of platforms built for continuous engagement. Agentic AI is also changing the operating model, because sourcing, matching, outreach, scheduling, and re-engagement are now increasingly handled through automated workflows instead of manual recruiter effort. Enterprise AI spending, workforce digitalization, and hybrid hiring are widening the addressable use cases for the candidate relationship management software market across regions and employer types. The report covers deployment model, organization size, buyer type, end-user industry, and geography, with forecasts provided in value terms in USD.

Key Report Takeaways

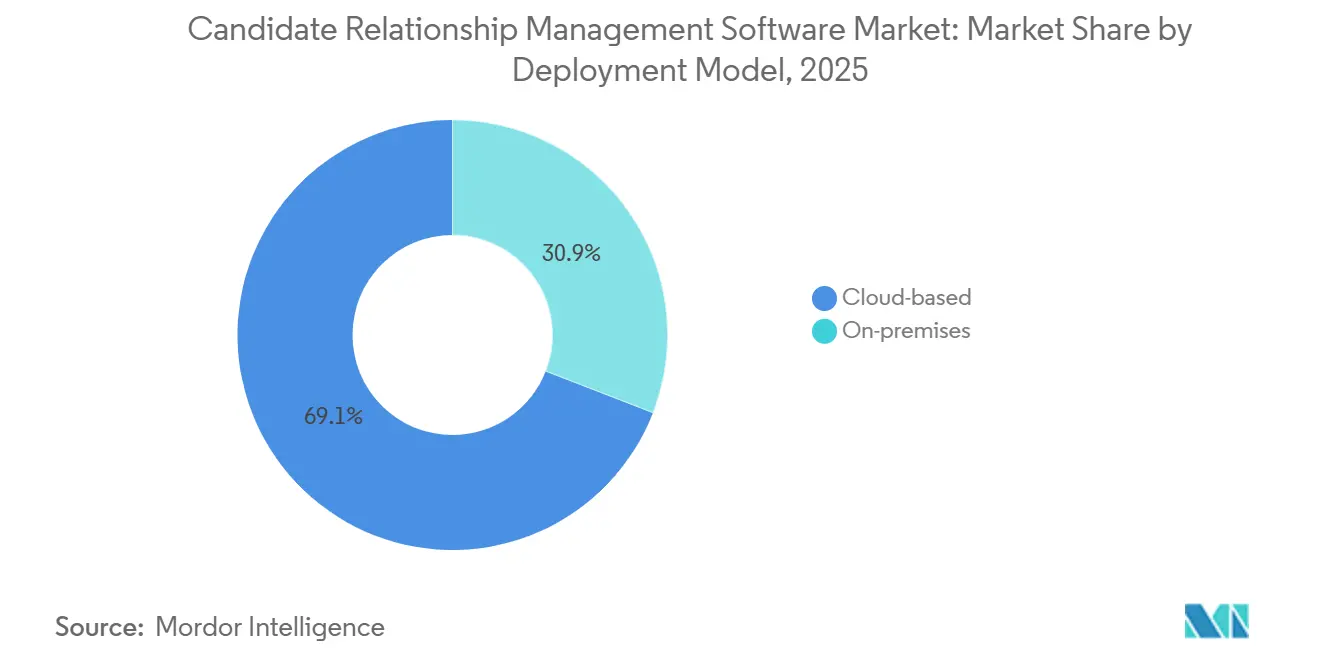

- By deployment model, cloud-based platforms accounted for 69.12% of revenue in 2025. Further, the segment recorded the highest projected CAGR at 17.19% through 2031.

- By organization size, large enterprises accounted for 62.86% of the candidate relationship management software market in 2025, while SMEs recorded the highest projected CAGR of 18.34% through 2031.

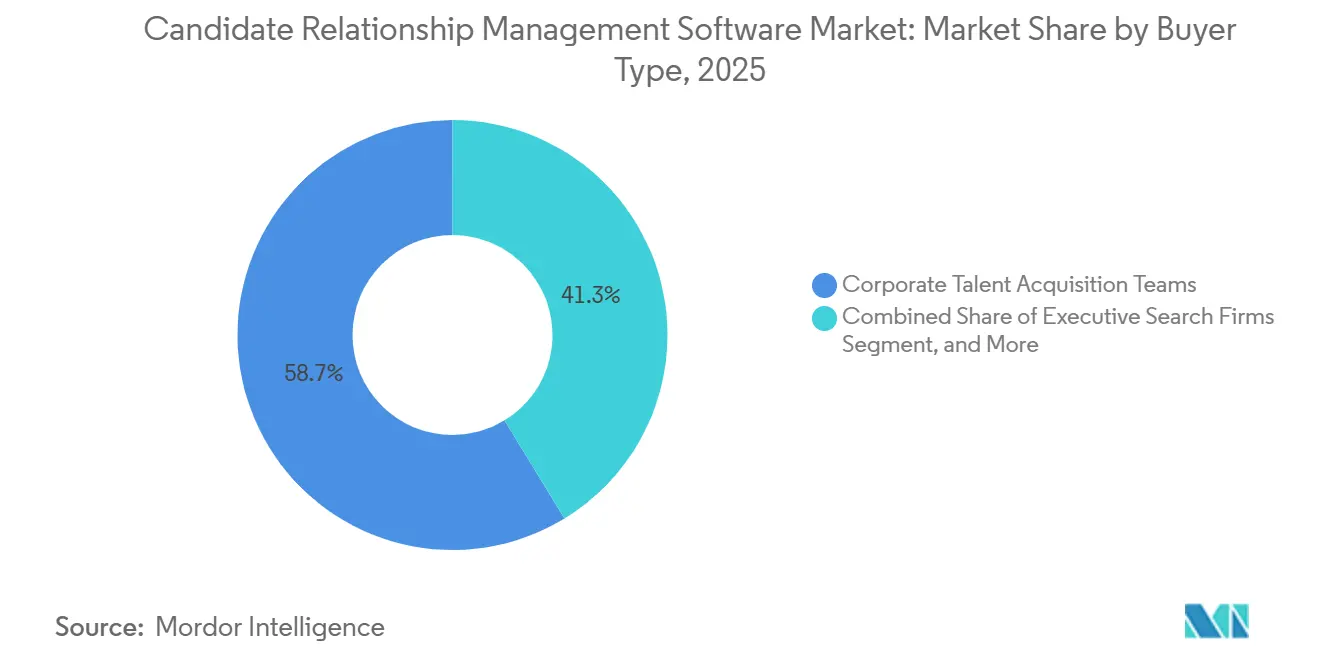

- By buyer type, corporate talent acquisition teams represented 58.72% of buyer-side spending in 2025. Staffing and recruitment agencies recorded the highest projected CAGR at 17.41% through 2031.

- By end-user industry, information technology and telecommunications accounted for 31.73% of spending in 2025, while healthcare and life sciences are projected to expand at an 18.94% CAGR through 2031.

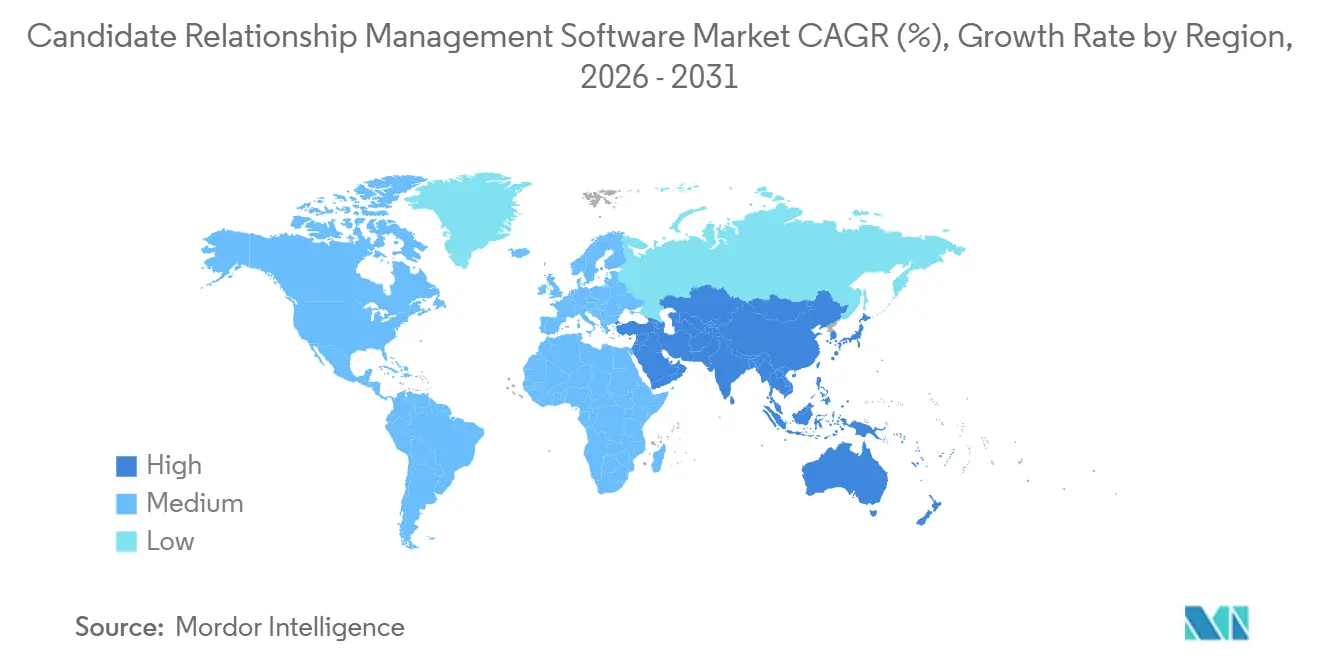

- By geography, North America held 38.91% of revenue in 2025, while Asia-Pacific is projected to grow at a 17.83% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Candidate Relationship Management Software Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Expansion of Agentic AI Across Recruiting Workflows | +4.2% | Global, with early concentration in North America and Western Europe | Short term (≤ 2 years) |

| Need For Proactive Talent Pipelines in Hard-To-Fill Roles | +3.5% | North America, Western Europe, and Asia-Pacific core, including India, Australia, and Singapore | Short term (≤ 2 years) |

| Rising High-Volume Hiring Automation Demand | +2.9% | Global, with highest intensity in North America, India, and Southeast Asia | Medium term (2-4 years) |

| Shift Toward Skills-Based Hiring and Talent Rediscovery | +2.3% | North America and EU, with spillover to Asia-Pacific core | Medium term (2-4 years) |

| Growing Demand For First-Party Talent Community Building | +1.8% | North America and EU | Long term (≥ 4 years) |

| Rising Need For Candidate Fraud and Identity Verification | +1.1% | Global, with early adoption in North America and Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expansion of Agentic AI Across Recruiting Workflows

Agentic AI is becoming the clearest turning point in the candidate relationship management software market because it moves the product from task support to workflow execution. In the candidate relationship management software market, these systems are now being used to source, match, engage, schedule, and re-engage talent with much less recruiter intervention between steps. SmartRecruiters reported early customer results from Winston Screen that showed a 75% reduction in time-to-decision, and AI-recommended candidates were 100% more likely to move to interview stages.[1]SmartRecruiters, “SmartRecruiters Unveils Agentic AI Hiring Capabilities,” SmartRecruiters, smartrecruiters.com This changes how buyers measure platform value, because the economics shift from headcount-led hiring capacity to software-led pipeline expansion. Phenom reinforced this direction in March 2026 when it introduced an orchestration layer that lets enterprises configure and govern multiple AI agents with defined roles and guardrails

Need For Proactive Talent Pipelines In Hard-To-Fill Roles

The candidate relationship management software market is also benefiting from shortages in cybersecurity, clinical nursing, and advanced manufacturing that make last-minute sourcing less reliable. Employers are building longer-term talent communities because hard-to-fill roles often need sustained contact with passive candidates before a job opens. The iCIMS Workforce Report for March 2026 found that 91% of frontline hiring managers saw role fulfillment as urgent, while applications fell 14% month over month in February 2026.[2]iCIMS, “Workforce Report,” iCIMS, icims.com In the candidate relationship management software market, that gap raises demand for tools that nurture silver medalists, alumni, and previously engaged contacts instead of restarting every search from zero. Talent rediscovery features strengthen this use case further because semantic skills matching can surface old applicants against new requirements with more relevance than a keyword-only search.

Rising High-Volume Hiring Automation Demand

High-volume recruitment is a major growth engine for the candidate relationship management software market because speed and candidate drop-off matter more than recruiter judgment alone in these workflows. Retail, logistics, hospitality, and frontline healthcare need large numbers of hires, and they need those hires processed through channels that candidates already use on mobile devices. iCIMS launched Frontline AI in March 2026 with a 24/7 conversational hiring flow over SMS and WhatsApp for frontline roles. Customers using comparable iCIMS AI-assisted workflows reported up to a 75% reduction in time-to-fill, a 90% reduction in manual hiring tasks, and up to 10x more hires per recruiter. The candidate relationship management software market gains from this pattern because post-application engagement, especially interview scheduling and follow-up, is now as important as top-of-funnel sourcing when employers are trying to protect throughput.

Shift Toward Skills-Based Hiring And Talent Rediscovery

Skills-based hiring is reshaping the candidate relationship management software market because platforms now need to maintain a live record of candidate capabilities rather than a static record of job titles. In the candidate relationship management software market, vendors are responding by building dynamic skill layers that can be refreshed from public profiles, internal records, and application history. Beamery has positioned this model around native skills intelligence and CRM capability across Workday and SAP SuccessFactors environments. Cornerstone Workforce AI has also highlighted how customer-specific skill architectures can be aligned with changing labor demand, bringing CRM workflows closer to workforce planning. This trend is gaining extra force in Europe because the EU AI Act requires stronger data governance and bias controls for AI systems used in recruitment.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Integration Complexity Across ATS, HCM, and Communication Tools | -3.2% | Global, most acute in North America and Europe where multi-system HCM stacks are prevalent | Medium term (2-4 years) |

| AI Governance and Candidate Transparency Obligations | -2.3% | Europe and the United Kingdom primarily, with spillover to North America | Short term (≤ 2 years) |

| Candidate Distrust of Black-Box Screening Workflow | -1.5% | Global, with highest sensitivity in Europe and Australia | Medium term (2-4 years) |

| AI-Generated Application Noise and Deepfake Risk | -1.1% | Global, with highest impact in North America and Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Integration Complexity Across ATS, HCM, And Communication Tools

Integration complexity remains a major restraint on the candidate relationship management software market because modern recruiting stacks often combine multiple HR, payroll, communication, and workflow systems. The challenge grows when employers try to connect agentic workflows to environments that were designed for slower batch synchronization rather than live action across tools. This is especially difficult in large enterprises that run mixed HCM environments and expect clean data movement across recruiting, onboarding, and workforce systems. Vendors that can offer certified native connectors are gaining an advantage because buyers now treat integration effort as a core cost of ownership rather than a technical afterthought. The candidate relationship management software market, therefore, faces a practical adoption limit in organizations where implementation effort, data mapping, and long-term maintenance remain harder to solve than the product use case itself.

AI Governance And Candidate Transparency Obligations

The candidate relationship management software market is also under pressure from governance requirements that are becoming part of product design, legal review, and procurement. Under Regulation EU 2024/1689, AI-based recruitment and candidate-selection systems fall under the high-risk category, which increases expectations around risk management, data governance, transparency, human oversight, and conformity assessment. Article 50 transparency obligations enter into force on August 2, 2026, which means employers and vendors must be clearer about when AI materially influences hiring decisions. This favors larger vendors that can absorb compliance costs and document their controls faster than smaller entrants. Phenom’s completion of a conformity assessment in March 2026 shows how governance readiness is becoming a commercial differentiator rather than only a legal requirement.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud-Based Infrastructure Defines Platform Architecture

Cloud-based deployment held 69.12% of the candidate relationship management software market share in 2025, which confirms that SaaS delivery has become the default operating model for enterprise talent technology. The candidate relationship management software market has moved firmly toward cloud architecture because vendors can update features continuously, connect more easily to job boards and HCM platforms, and roll out AI enhancements without long customer upgrade cycles. Avature released more than 300 platform features across 2025 and another 91 updates in Q1 2026, which shows the release pace that cloud environments can sustain. Data residency options also strengthen adoption because organizations can pursue compliance needs without giving up access to newer automation features.

On-premises deployments still matter in defense, government intelligence, and parts of financial services where network isolation and internal control remain non-negotiable. In the candidate relationship management software industry, that remaining installed base is pushing vendors toward hybrid designs that preserve AI functionality while keeping sensitive candidate data inside controlled environments. This matters because the candidate relationship management software market continues to serve buyers with very different security postures, even as cloud delivery remains dominant. The result is not a reversal of cloud leadership, but a narrower on-premises role centered on sensitive environments that cannot externalize candidate records.

By Organization Size: Large Enterprises Anchor Spend As SMEs Accelerate

Large enterprises accounted for 62.86% of the candidate relationship management software market in 2025, reflecting the scale of their hiring operations and the complexity of their recruiting environments. The candidate relationship management software market has strong large-enterprise demand because global employers need configurable workflows, permissions, multilingual interfaces, analytics, and deep integration across systems. Workday stated that customers using its unified talent acquisition suite increased recruiter capacity by up to 54% and reduced hiring manager review time by up to 35%.[3]Workday, “Workday Named A Leader In Talent Acquisition Suites,” Workday Newsroom, workday.com These outcomes matter most in large organizations where small productivity gains translate into meaningful hiring volume improvements.

SMEs are emerging as the faster-growing part of the candidate relationship management software market, projected to grow CAGR at 18.34% by 2031, because SaaS delivery and broader AI availability are lowering entry barriers. Smaller employers can now adopt modular platforms without committing to the same implementation depth required by large global companies. The candidate relationship management software industry is also seeing SME demand rise in regulated supply chains, where buyers increasingly expect credible controls around AI use and data handling. Cornerstone’s use of ISO/IEC 42001 within its AI management approach reflects the growing importance of governance language even in mid-market procurement

By Buyer Type: Corporate Talent Acquisition Teams Set The Spending Agenda

Corporate talent acquisition teams accounted for 58.72% of buyer-side spending in 2025, underscoring that in-house recruiting remains the center of software purchasing in this category. The candidate relationship management software market is benefiting from this shift, as companies are building their own talent communities to reduce agency dependency and improve response, conversion, and acceptance rates over time. In-house TA teams also increasingly manage candidate experience as a brand issue, which gives continuous engagement tools a more strategic role than a traditional workflow tracker. This helps explain why CRM functionality is now treated as core infrastructure in many enterprise recruiting environments.

Staffing and recruitment agencies remain the second-largest buyer segment, projected to grow at a 17.41% CAGR by 2031, and their needs keep a portion of the candidate relationship management software market oriented toward placement speed, recruiter productivity, and margin protection. Bullhorn’s launch of Amplify in May 2025 reflected this model by automating sourcing, screening, and candidate submission without requiring additional recruiter headcount.[4]Bullhorn, “Bullhorn Launches Amplify,” Bullhorn, bullhorn.com RPO providers also remain structurally attractive buyers because one platform investment can be used across multiple clients and hiring programs. Executive search firms are smaller users of the candidate relationship management software market, and they usually value long-term relationship tracking and communication history more than high-volume pipeline automation.

By End-User Industry: Technology Leads While Public Sector Demand Builds

Information technology and telecommunications accounted for 31.73% of spending in 2025, which made it the largest end-user group in the candidate relationship management software market. This leadership reflects the sector’s persistent need for scarce technical talent, high attrition in key roles, and long-standing reliance on passive candidate engagement. The candidate relationship management software market has been especially relevant for technology employers because their hiring patterns are global, skills-led, and highly dependent on maintaining warm talent pools between openings. SmartRecruiters’ April 2026 release of agentic CRM functions, including talent pool activation and compliance-aware outreach across email, SMS, and WhatsApp, aligned closely with those technology hiring needs.

Healthcare and Life Sciences is the fastest-growing end-user vertical, expanding at a CAGR of 18.94% from 2026 to 2031, as providers and life sciences organizations digitize complex hiring processes traditionally burdened by regulatory requirements, credential verification, and specialized talent shortages. In developed markets, an aging workforce and the post-pandemic realization of healthcare hiring's structural inefficiencies compared to private-sector employers in terms of speed and candidate experience are prompting a shift in procurement budgets toward digital talent acquisition infrastructure. Other sectors, including Banking, Financial Services, and Insurance (BFSI), manufacturing, and government and education, are also experiencing notable growth. BFSI emphasizes both talent quality and regulatory compliance, manufacturing faces a critical shortage of skilled trades, and the government is focused on modernizing outdated hiring workflows, all of which support the case for CRM investments. Additionally, sectors such as retail, e-commerce, professional services, and hospitality benefit from CRM automation during high-volume, often seasonal hiring periods. This automation delivers measurable returns on investment, particularly in reducing time-to-fill and cost-per-hire metrics.

Geography Analysis

North America held 38.91% of the candidate relationship management software market share in 2025, which kept it as the largest regional contributor. The region benefits from deep enterprise HR technology adoption, higher recruiting technology budgets, and a strong base of CRM-oriented vendors in the United States. The candidate relationship management software market is also supported by a mature buyer base in North America, where employers increasingly expect AI features to sit inside broader hiring workflows rather than operate as stand-alone tools. Canada adds demand through financial services and technology hiring, while Mexico supports growth through manufacturing expansion and cross-border talent sourcing needs. Regulatory attention around AI in hiring is also reinforcing interest in platforms that can document decisions, support transparency, and maintain stronger governance controls.

Asia-Pacific is projected to expand at a 17.83% CAGR through 2031, which makes it the fastest-growing regional segment in the candidate relationship management software market size. Growth in the region is being supported by workforce digitalization, large enterprise hiring programs, and candidate behavior that is already comfortable with mobile-first communication. India remains central to this momentum because the scale of its technology and business services workforce creates demand for high-volume talent pool segmentation and automated nurture at enterprise scale. Australia and Singapore also continue to function as early-adopter markets where advanced use cases are tested before wider deployment across the region.

Europe remains a meaningful part of the candidate relationship management software market, with Germany, the United Kingdom, and France as the largest national contributors. Germany shows a split adoption pattern, where a large group of employers already use candidate management systems, while another sizable group still has no immediate implementation plans. The United Kingdom stands out for relationship-led recruiting in financial and professional services, where talent competition remains intense and local supply is limited. Across Europe, the EU AI Act is directly shaping vendor selection because buyers increasingly want conformity evidence and candidate notification mechanisms before transparency obligations apply in August 2026.[5]European Union, “Regulation (EU) 2024/1689,” EUR-Lex, eur-lex.europa.eu The Middle East, Africa, and South America remain earlier-stage regions in the candidate relationship management software market, but multinational hiring activity and economic diversification programs are gradually formalizing demand for structured talent pipeline management.

Competitive Landscape

The candidate relationship management software market remains moderately fragmented, with competition split between large HCM platform vendors and specialist providers built around recruiting workflows. SAP SE, through SmartRecruiters, Oracle, Workday, and Microsoft, compete by embedding CRM capabilities into broader enterprise software environments. At the same time, Phenom, Beamery, iCIMS, Avature, and Bullhorn compete by offering stronger workflow configurability, AI depth, and specialization for different buyer needs. The candidate relationship management software market is therefore moving along two parallel tracks, one based on suite consolidation and the other based on product depth in defined recruiting use cases. This structure keeps switching pressure high because buyers weigh integration simplicity against functional breadth and compliance readiness.

Workday’s unification of Workday Recruiting, HiredScore AI for Recruiting, and Paradox conversational AI illustrates how the candidate relationship management software market is consolidating around shared data layers and broader suite outcomes. Oracle reinforced the same direction in April 2026 with 8 embedded Fusion Agentic Applications for HR, using native HCM data as the base for AI-led hiring workflows. Phenom took a different but equally important route by turning EU AI Act conformity into a market signal for European enterprise procurement. SmartRecruiters also raised the bar by adding agentic CRM, agentic interviewing, fraud detection, and native SAP SuccessFactors integration in one release cycle.

Open space remains in public-sector recruitment, SME-friendly agentic tooling, and messaging-led engagement models that go beyond email-first workflows. Several newer vendors are gaining attention by offering autonomous sourcing and rediscovery tools at price points that are easier for smaller TA teams to adopt. Another competitive issue is portfolio clarity, because listing both Jobvite and Employ as separate entities can overstate concentration where parent-subsidiary overlap already exists. In practice, the candidate relationship management software market still rewards vendors that can combine product breadth, integration quality, AI governance, and vertical fit without forcing buyers into long implementation cycles.

Candidate Relationship Management Software Industry Leaders

Microsoft Corporation

Bullhorn, Inc.

Avature Limited

Phenom People, Inc.

Radancy, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Oracle introduced Fusion Agentic Applications for HR at the Oracle AI World Tour in New York. The launch embedded 8 specialized AI agents into Oracle Fusion Cloud HCM, including a Hiring Workspace for Store Managers to reduce retail recruiting administration burden and an AI Agent Studio enabling organizations to build custom agentic workflows using reusable agents without traditional coding.

- April 2026: SmartRecruiters, an SAP company, unveiled agentic CRM, agentic interviewing capabilities, applicant fraud detection, and a native SAP SuccessFactors integration. Early customers using the Winston Screen agentic tool reported a 75% reduction in time-to-decision, with AI-recommended candidates 100% more likely to advance to interview stages.

- March 2026: Phenom unveiled a new AI architecture at IAMPHENOM 2026, including the industry's first EU AI Act conformity assessment for a talent AI platform, an Orchestration Engine for governing unlimited AI agents, a Compliance Agent with guardrail and routing policy creation, and a Candidate Fraud Detection system incorporating cognitive assessments, an AI interviewer, and biometric identity verification.

- June 2025: SmartRecruiters launched its next-generation AI-powered hiring platform, declaring the traditional ATS era obsolete and positioning SmartOS and the Winston AI companion as the foundation for agentic talent acquisition. The platform introduced modular, outcome-aligned pricing and agentic workflows for enterprise customers across corporate, high-volume, and hybrid hiring models.

Global Candidate Relationship Management Software Market Report Scope

Candidate Relationship Management (CRM) Software is a recruitment solution designed to enable organizations to develop, maintain, and manage long-term relationships with potential job candidates. Unlike traditional Applicant Tracking Systems (ATS), it prioritizes proactive engagement with talent pipelines over merely processing applications.

The Candidate Relationship Management Software Report is Segmented by Deployment Model (Cloud-based, and On-premises), Organization Size (Large Enterprises, and SMEs), Buyer Type (Corporate Talent Acquisition Teams, Staffing and Recruitment Agencies, Executive Search Firms, and Recruitment Process Outsourcing Providers), End-User Industry (Information Technology and Telecommunications, Healthcare and Life Sciences, Banking, Financial Services, and Insurance, Manufacturing, Retail and E-commerce, Professional Services, Government and Education, Hospitality and Travel, Media and Entertainment, and Other End-user Industries) and Geography (North America, South America, Europe, Asia-Pacific, the Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Cloud-based |

| On-premises |

| Large Enterprises |

| Small Medium Enterprises (SMEs) |

| Corporate Talent Acquisition Teams |

| Staffing and Recruitment Agencies |

| Executive Search Firms |

| Recruitment Process Outsourcing Providers |

| Information Technology and Telecommunications |

| Healthcare and Life Sciences |

| Banking, Financial Services, and Insurance |

| Manufacturing |

| Retail and E-commerce |

| Professional Services |

| Government and Education |

| Hospitality and Travel |

| Media and Entertainment |

| Other End-user Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Netherlands | |

| Nordics | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Singapore | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Israel | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Kenya | |

| Rest of Africa |

| By Deployment Model | Cloud-based | |

| On-premises | ||

| By Organization Size | Large Enterprises | |

| Small Medium Enterprises (SMEs) | ||

| By Buyer Type | Corporate Talent Acquisition Teams | |

| Staffing and Recruitment Agencies | ||

| Executive Search Firms | ||

| Recruitment Process Outsourcing Providers | ||

| By End-user Industry | Information Technology and Telecommunications | |

| Healthcare and Life Sciences | ||

| Banking, Financial Services, and Insurance | ||

| Manufacturing | ||

| Retail and E-commerce | ||

| Professional Services | ||

| Government and Education | ||

| Hospitality and Travel | ||

| Media and Entertainment | ||

| Other End-user Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Netherlands | ||

| Nordics | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current and forecast value of the candidate relationship management software space?

The candidate relationship management software market stood at USD 1.91 billion in 2025, reached USD 2.23 billion in 2026, and is forecast to reach USD 4.83 billion by 2031 at a 16.72% CAGR.

What is driving demand for candidate relationship management software platforms?

Demand is being driven by skill shortages, continuous talent pipelining, agentic AI adoption, and higher automation needs in high-volume hiring environments.

Which deployment model leads adoption in candidate relationship management software?

Cloud-based deployment led with 69.12% of revenue in 2025 because it supports faster updates, easier integrations, and quicker rollout of AI functions.

Which end-user group spends the most on these platforms?

Information technology and telecommunications held the largest end-user share at 31.73% in 2025, reflecting strong demand for scarce technical talent and ongoing passive candidate engagement.

Which region is growing the fastest for candidate relationship management software?

Asia-Pacific is the fastest-growing region, with a projected 17.83% CAGR through 2031, supported by workforce digitalization and large enterprise hiring volumes.

Why are governance and compliance becoming more important in recruiting software?

The EU AI Act treats AI-based recruitment systems as high-risk, which is pushing vendors and buyers to focus more on transparency, conformity, auditability, and human oversight.

Page last updated on: