Benefit Administration Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

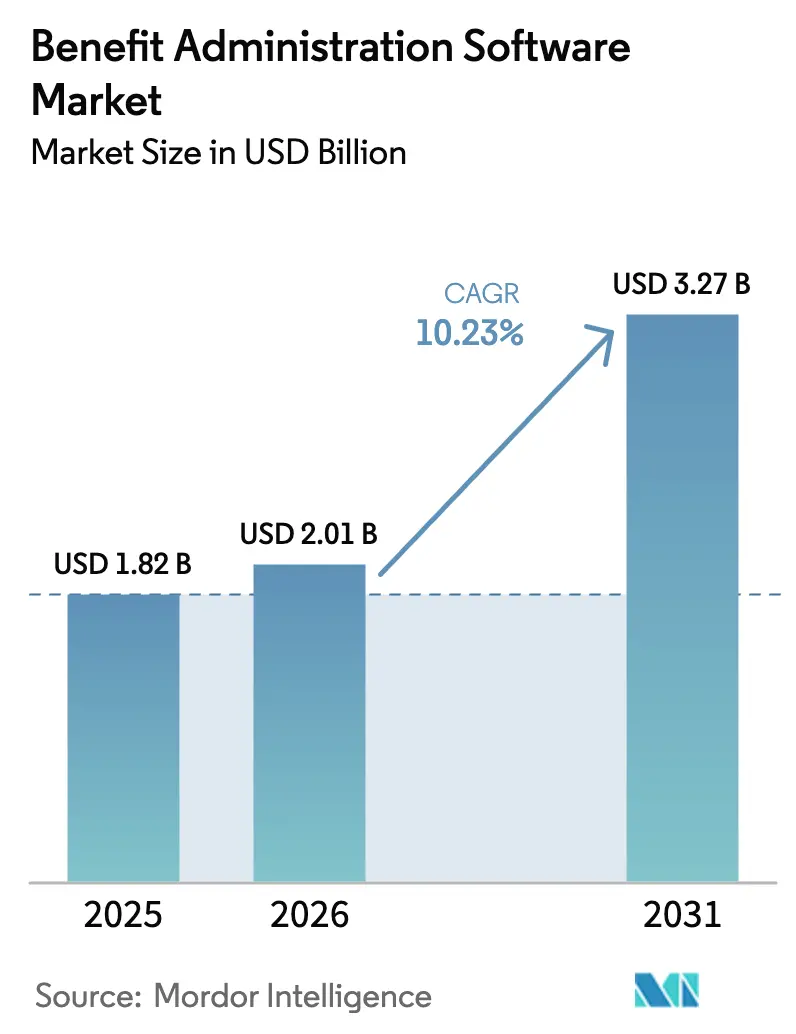

| Market Size (2026) | USD 2.01 Billion |

| Market Size (2031) | USD 3.27 Billion |

| Growth Rate (2026 - 2031) | 10.23% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Benefit Administration Software Market Analysis by Mordor Intelligence

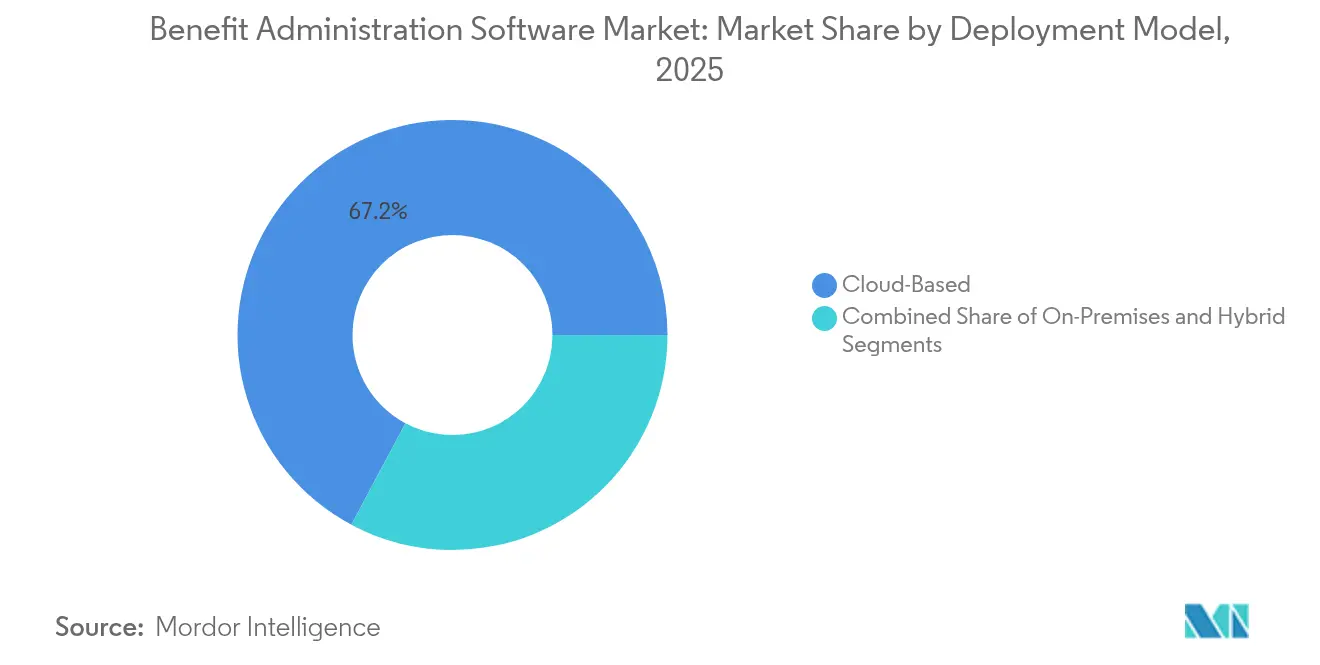

The Benefit Administration Software Market size in 2026 is estimated at USD 2.01 billion, growing from 2025 value of USD 1.82 billion with 2031 projections showing USD 3.27 billion, growing at 10.23% CAGR over 2026-2031. Expansion is tied to cloud-first strategies, tightening data-privacy regulations, and fast-moving artificial intelligence adoption that lifts user experience and compliance accuracy. Cloud-based deployment holds a 67.6% revenue share in 2024, while hybrid architectures expand at a 13.2% CAGR on the strength of flexible data-sovereignty controls. Large enterprises command 62.3% of total spending, yet small and medium enterprises (SMEs) are growing 13.6% a year thanks to pay-per-use pricing from vendors such as Gusto and Rippling. North America leads with 39.2% share, but Asia-Pacific is advancing 13.1% annually as multinationals localize benefits programs and domestic firms accelerate digitalization. Competitive pressure remains moderate as traditional HCM vendors face challenger platforms and API aggregators that simplify connectivity.

Key Report Takeaways

- By deployment model, cloud solutions held 67.20% of the benefit administration software market share in 2025, while hybrid deployments are forecast to expand at a 12.79% CAGR through 2031.

- By organization size, large enterprises led with a 61.70% share of the benefit administration software market size in 2025, whereas the SME segment is projected to grow 13.09% per year.

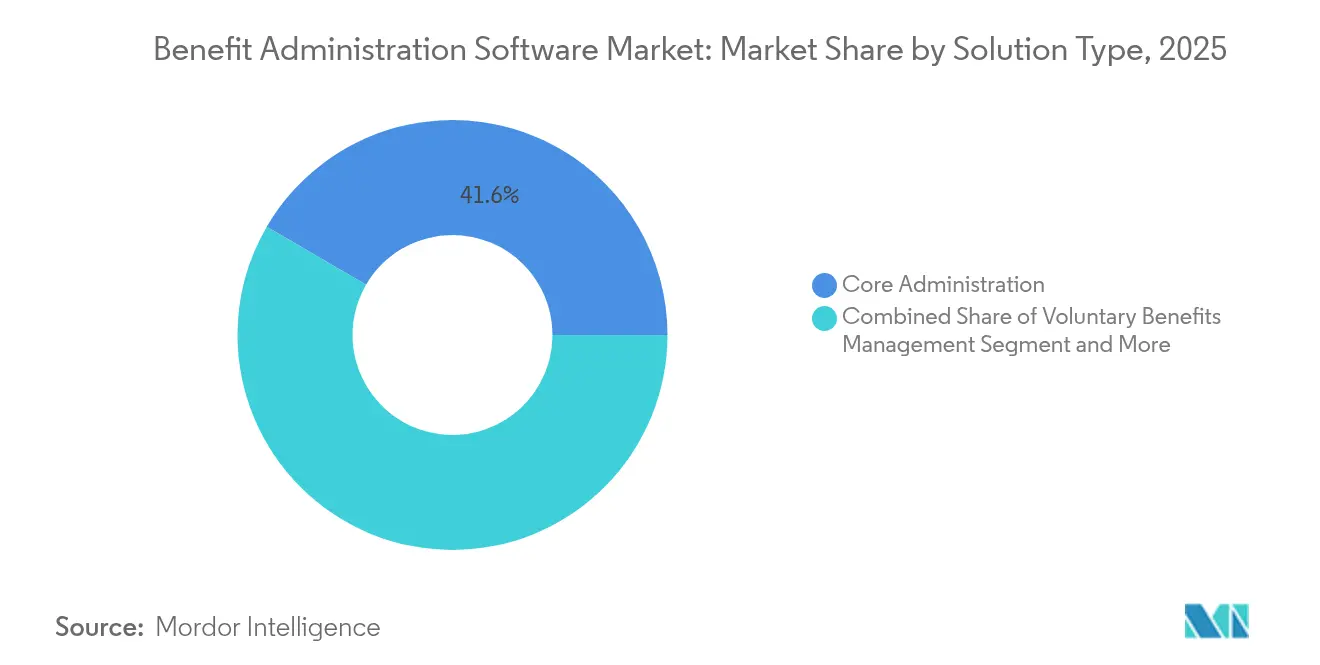

- By solution type, core administration captured 41.60% revenue share in 2025; worksite benefits administration is set to rise at a 12.62% CAGR to 2031.

- By end-user industry, IT and telecommunications represented 28.40% of spending in 2025, while BFSI is expected to expand 12.48% annually.

- By delivery channel, self-service portals held 49.60% revenue share in 2025; mobile apps are projected to advance at a 12.86% CAGR through 2031.

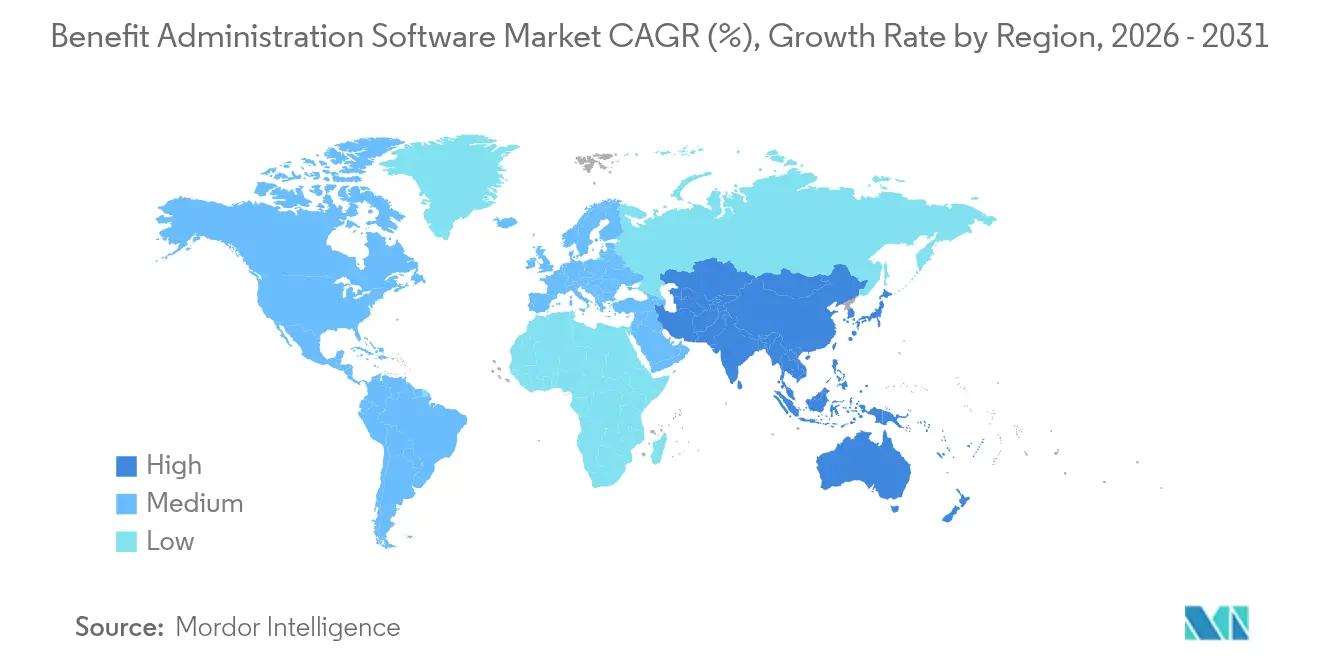

- By geography, North America accounted for 38.80% of the benefit administration software market in 2025, yet Asia-Pacific posts the fastest growth at 12.72% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Benefit Administration Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud migration of HR Tech stacks | +2.1% | Global, with early gains in North America and Europe | Medium term (2-4 years) |

| Pay-per-use pricing attracting SMEs | +1.8% | Global, particularly strong in Asia-Pacific and Latin America | Short term (≤ 2 years) |

| Growing regulatory complexity (ACA, IR35, etc.) | +2.3% | North America and Europe primarily, expanding to APAC | Long term (≥ 4 years) |

| Intensifying war-for-talent in post-pandemic era | +1.5% | Global, with concentration in developed markets | Medium term (2-4 years) |

| Adoption of AI-driven decision support in benefits | +1.9% | North America and Europe leading, APAC following | Long term (≥ 4 years) |

| Embedded-benefits APIs inside HCM super-apps | +1.2% | Global, with tech-forward markets leading adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cloud migration of HR tech stacks

Organizations moving benefit systems to cloud infrastructure gain measurable performance, security, and scalability improvements. Alight Solutions completed a full AWS transition in February 2025, posting USD 75 million annualized savings, a 40% server reduction, and 43% faster enrollment response times while raising security controls by 85%. [1]Alight Solutions, “Alight completes cloud migration transformation, delivering enhanced performance and significant cost savings,” alight.com These outcomes validate how cloud architecture removes legacy capacity limits, enables real-time global data synchronization, and shortens release cycles that keep compliance rules current. The benefit administration software market, therefore, aligns migration roadmaps with enterprise-wide cloud strategies, positioning cloud platforms as the operating backbone for multinational benefits programs.

Pay-per-use pricing attracting SMEs

Flexible subscription tiers are lowering adoption barriers for firms with 50-500 employees. Gusto offers plans beginning at USD 59 per month plus USD 8 per employee, and Rippling starts at USD 8 per user, models that bypass traditional license fees. [2]Gusto, “Product Pricing,” gusto.com These economics open enterprise-grade functionality—carrier feeds, automated filings, and self-service portals—to resource-constrained businesses. The SME segment’s 13.6% CAGR outpaces the benefit administration software market average, reflecting the pricing lever’s potency. Vendors reinforce traction with rapid no-code configuration and guided onboarding that reduce implementation lead times.

Growing regulatory complexity

Mandates such as the Affordable Care Act require eligibility tracking, affordability tests, and IRS Form 1095 filings, exposing employers to penalties of up to USD 4,320 per worker for non-compliance. European GDPR obligations intensify data-handling requirements, prompting automated workflows that encrypt, audit, and report personal information. SyncStream’s Clear ACA platform screens data, flags risk, and has served more than 40,000 employers, cutting manual review labor by 60%. Regulatory uncertainty, therefore, channels budget toward software that codifies multi-jurisdictional rules and maintains audit trails at scale.

Intensifying war-for-talent

Tight labor markets push employers to enrich voluntary benefits portfolios without inflating fixed costs. Decision-support engines help employees personalize packages, boosting perceived value. Higher engagement directly links to retention, a critical metric as attrition expenses climb. Vendors emphasize consumer-grade portals, AI chat guidance, and real-time cost comparisons that simplify complex choices, thereby sharpening employers’ competitive stance for scarce skill sets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration hurdles with legacy HRIS | -1.4% | Global, particularly acute in large enterprises | Medium term (2-4 years) |

| Rising data-privacy compliance costs | -1.1% | Europe (GDPR), North America (state laws), expanding globally | Long term (≥ 4 years) |

| Shortage of domain-skilled implementation partners | -0.8% | Global, more pronounced in emerging markets | Short term (≤ 2 years) |

| Vendor lock-in risks in multi-country roll-outs | -0.6% | Multinational corporations globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Integration hurdles with legacy HRIS systems

Roughly 70% of deployments encounter data-mapping or interface challenges that extend launch timelines by up to 60%. [3]SHRM, “How to Meet Challenges When Deploying New HR Technology,” shrm.org Complexities arise when payroll, time-tracking, and EHR systems use divergent schemas, forcing middleware layers that raise cost. Healthcare providers illustrate the issue as benefit platforms must mesh with clinical records and union payroll structures. High custom-code maintenance burdens strain IT teams, delaying ROI and prompting some buyers to postpone transitions.

Rising data-privacy compliance costs

GDPR readiness expenses average USD 1.3 million for mid-size enterprises, covering encryption, consent orchestration, ongoing audits, and breach-response plans. US state laws, such as CCPA, introduce additional variance. Smaller businesses feel the burden most, as requirements scale irrespective of workforce size. Continuous monitoring, staff training, and legal reviews add 15-20% to total ownership cost, deterring some organizations from full-featured rollouts until vendors embed turnkey compliance toolkits.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud Infrastructure Dominance Drives Hybrid Innovation

Cloud offerings contributed 67.20% of 2025 revenue, reinforcing the benefit administration software market’s shift toward managed environments that remove patching and hardware upkeep. Hybrid architectures, however, are climbing at 12.79% CAGR as organizations balance cloud flexibility with on-premises data-sovereignty mandates. This dual-stack approach underpins the benefit administration software market size expansion among regulated firms.

Hybrid solutions keep sensitive personnel files within private data centers while routing analytics, mobile access, and carrier exchanges through cloud microservices. Healthcare systems often host HIPAA-protected data locally but deploy cloud enrollment portals that integrate pre-built carrier APIs. This method improves uptime, supports multi-site access, and avoids wholesale infrastructure write-offs. Vendors now package edge-gateway appliances, accelerating integrations and easing traffic orchestration. Consequently, hybrid innovation sustains adoption among risk-averse buyers while preserving cloud economics.

By Organization Size: SME Acceleration Reshapes Market Dynamics

Large enterprises held 61.70% of the benefit administration software market share in 2025, anchored by multi-location complexity and deeper IT budgets. The SME cohort, though, is tracking a 13.09% CAGR, adding vitality to overall benefit administration software market growth.

SMEs accept cloud defaults and rapid-setup templates that cut project times from months to weeks. Low entry pricing aligns spend with headcount, a pivotal design principle for firms scaling hiring plans. Vendors offer guided implementation wizards and out-of-box compliance libraries that replace enterprise-grade consulting. As a result, the benefit administration software market size linked to SMEs grows faster than any other buyer group, prompting providers to prioritize simplified UX, chat support, and marketplace app stores tailored to limited HR staff.

By Solution Type: Core Administration Leadership Meets Worksite Benefits Growth

Core administration platforms generated 41.60% of 2025 revenue, reaffirming their role as the transactional backbone of the benefit administration software market. Worksite benefits management is outpacing at a 12.62% CAGR, driven by employer interest in voluntary products that elevate retention without increasing fixed payroll costs.

Worksite engines manage supplemental health, pet insurance, student-loan repayment, and lifestyle perks delivered via payroll deduction. AI compares plan value, nudging employees toward optimal mixes, while mobile alerts raise enrollment completion rates. As employers broaden offerings, data silos risk fragmentation. Leading vendors thus embed configurable rules engines and consolidated dashboards that span core and voluntary lines, securing a unified employee view and satisfying carrier reporting standards.

By End-user Industry: IT Sector Leadership Drives BFSI Innovation

The technology and telecommunications vertical accounted for 28.40% of the 2025 demand, setting usability expectations for the benefit administration software market. BFSI institutions, under heavy regulatory oversight, will grow 12.48% annually as they modernize legacy stacks and compete for digitally savvy talent.

Finserv firms require rigorous audit trails, segregation-of-duties logic, and dynamic plan design to align with regional banking laws. They are early adopters of secure cloud enclaves and encrypted API gateways. Vendors respond with configurable approval workflows, multi-currency payroll feeds, and automated statutory reporting. Lessons learned in IT—from consumer-grade UI to AI chatbots—transfer into BFSI rollouts, accelerating time-to-value while meeting strict supervisory guidelines.

By Delivery Channel: Self-Service Portals Lead Mobile App Revolution

Self-service portals commanded 49.60% of transactions in 2025, functioning as the default interaction point across the benefit administration software market. Mobile applications, however, are climbing 12.86% CAGR, as 70% of employees prefer smartphone access for planning tasks.

Modern apps surface plan comparisons, digital ID cards, and wellness nudges inside a unified interface. Benefitfocus earns a 4.6-star rating from 23,000 users, demonstrating demand for intuitive design. Push notifications cut call-center load, while biometric log-in secures sessions. Service bureau and outsourced models persist, particularly for employers lacking HR capacity. Those providers integrate branded portals and mobile containers to preserve white-glove service while meeting user expectations for on-demand visibility.

Geography Analysis

North America contributed 38.80% of 2025 revenue, reflecting intricate ACA reporting, ERISA requirements, and mature voluntary benefits ecosystems. Employers invest in advanced rule engines and AI assistants that constantly parse evolving federal and state statutes. Vendor R&D hubs in the United States nurture rapid feature iteration, cementing regional leadership.

Asia-Pacific is the fastest riser at 12.72% CAGR to 2031, aided by accelerated cloud adoption and rising middle-class expectations for employer-sponsored coverage. Multinationals opening regional headquarters require single-tenant platforms that localize languages, currencies, and statutory contributions. Domestic enterprises, particularly in India and Southeast Asia, leapfrog on-premises software, opting straight for mobile-first solutions that align with high smartphone penetration. Government digitization roadmaps and increasing financial wellness awareness further stoke demand.

Europe posts steady contributions, shaped by GDPR and country-specific labor codes. The benefit administration software market size attached to the region favors vendors with proven encryption, retention, and audit frameworks. South America, along with the Middle East and Africa, remains an emerging pocket where multinational rollouts seed early adoption. Expansion accelerates when governments tighten reporting mandates or incentivize digital HR upgrades, positioning these regions as medium-term growth corridors.

Competitive Landscape

The market balances established HCM conglomerates with agile cloud natives. ADP, Workday, SAP, and Alight secure large-enterprise contracts through global payroll breadth and bundled services. Their combined share places the market in a moderate-concentration band. Challenger vendors—Rippling, Gusto, Benefitfocus, Employee Navigator—win mid-market accounts by blending consumer-grade design with aggressive pricing.

Differentiation pivots on AI assistants, developer ecosystems, and integration simplicity. Workday’s AI Agent Partner Network lets Accenture, AWS, and Microsoft embed intelligent agents that manage payroll queries or suggest personalized benefits, fortifying stickiness among Fortune 100 adopters. Alight’s Microsoft Teams integration brings contextual benefits and support into daily collaboration flows, elevating engagement metrics. API aggregators such as Finch reduce connectivity friction, enabling niche vendors to surface employee data without deep IT intervention.

Consolidation remains active. Alight purchased Hodges-Mace in February 2025, adding a SmartBen user base of 1.2 million lives. Employee Navigator acquired Ease to gain 22 integrations and reinforce brokerage channels, while large vendors continuously scout niche AI or compliance start-ups to plug capability gaps. Competitive intensity, therefore, centers on ecosystem reach and time-to-value rather than baseline functionality, steering the benefit administration software market toward platform convergence.

Benefit Administration Software Industry Leaders

Automatic Data Processing, Inc. (ADP)

Workday Inc.

SAP SE

Oracle Corporation

Ultimate Kronos Group (UKG)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Workday introduced its AI Agent Partner Network and Agent Gateway with Accenture, AWS, and Microsoft participation.

- March 2025: Workday’s Spring release delivered 350 new features plus AI-driven talent and finance tools.

- February 2025: Alight Solutions released Alight Worklife with Microsoft Teams integration and AI analytics.

- February 2025: Alight Solutions acquired Hodges-Mace, adding 1.2 million lives and deepening voluntary benefits expertise.

- February 2025: Alight Solutions finished its AWS migration, saving USD 75 million annually and cutting server count by 40% while improving enrollment response times by 43%.

- January 2025: Rippling published 2025 compliance guides spotlighting automated monitoring modules.

- December 2024: bswift launched a next-generation mobile app focused on benefits engagement.

- October 2024: OutSail analyzed Employee Navigator’s acquisition of Ease, citing 22 new integrations and a two-tier support model.

Global Benefit Administration Software Market Report Scope

The benefit administration software market encompasses technology solutions designed to streamline the management of employee benefits, such as health insurance, retirement plans, and paid time off. These platforms automate enrollment, compliance, and communication processes, improving efficiency for HR teams and enhancing employee experience. The market caters to organizations of all sizes, supporting integration with payroll systems and regulatory compliance requirements.

The Benefit Administration Software Market is segmented by deployment type (cloud-based, on-premises), organization size (small and medium enterprises (SMEs), large enterprises), solution type (core administration solutions, voluntary benefits management, worksite benefits administration, other solution type), end-user industry (healthcare, IT and telecom, retail, education, manufacturing, other end-use industries), and Geography (North America, Europe, Asia Pacific, Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Cloud-Based |

| On-Premises |

| Hybrid |

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

| Core Administration |

| Voluntary Benefits Management |

| Worksite Benefits Administration |

| Retirement Plan Administration |

| Other Solutions |

| Healthcare |

| IT and Telecom |

| Retail and E-Commerce |

| Manufacturing |

| Education |

| BFSI |

| Government/Public Sector |

| Other End-user Industries |

| Self-Service Portal |

| Mobile App |

| Service Bureau/Outsourced |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Singapore | ||

| Malaysia | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Deployment Model | Cloud-Based | ||

| On-Premises | |||

| Hybrid | |||

| By Organization Size | Small and Medium Enterprises (SMEs) | ||

| Large Enterprises | |||

| By Solution Type | Core Administration | ||

| Voluntary Benefits Management | |||

| Worksite Benefits Administration | |||

| Retirement Plan Administration | |||

| Other Solutions | |||

| By End-user Industry | Healthcare | ||

| IT and Telecom | |||

| Retail and E-Commerce | |||

| Manufacturing | |||

| Education | |||

| BFSI | |||

| Government/Public Sector | |||

| Other End-user Industries | |||

| By Delivery Channel | Self-Service Portal | ||

| Mobile App | |||

| Service Bureau/Outsourced | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Singapore | |||

| Malaysia | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected size of the benefit administration software market by 2031?

The benefit administration software market is expected to reach USD 3.27 billion by 2031, growing at a 10.23% CAGR.

Which deployment model is expanding fastest?

Hybrid deployment is the quickest-growing model, posting a 12.79% CAGR as firms blend cloud flexibility with on-premises control.

How are SMEs influencing market growth?

SMEs are advancing 13.09% annually as pay-per-use pricing and rapid cloud onboarding lower adoption barriers.

Which region offers the highest growth potential?

Asia-Pacific is forecast to expand 12.72% per year through 2031, propelled by rapid digitalization and evolving employee expectations.

What role does artificial intelligence play in modern benefit software?

AI powers decision support, personalized plan recommendations, and predictive analytics that boost enrollment rates by up to 30%.

Why are data-privacy regulations a constraint for buyers?

Compliance frameworks such as GDPR drive average readiness costs of USD 1.3 million for mid-sized firms, raising total ownership expenses.

Page last updated on: