Vertical Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

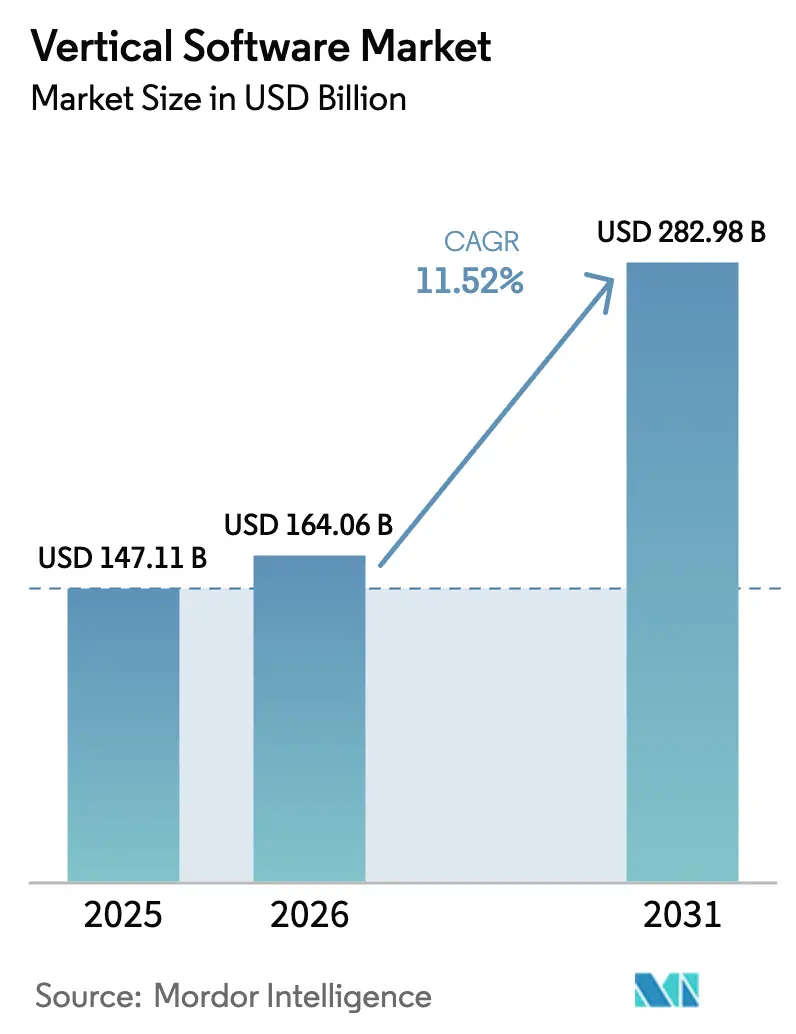

| Market Size (2026) | USD 164.06 Billion |

| Market Size (2031) | USD 282.98 Billion |

| Growth Rate (2026 - 2031) | 11.52% CAGR |

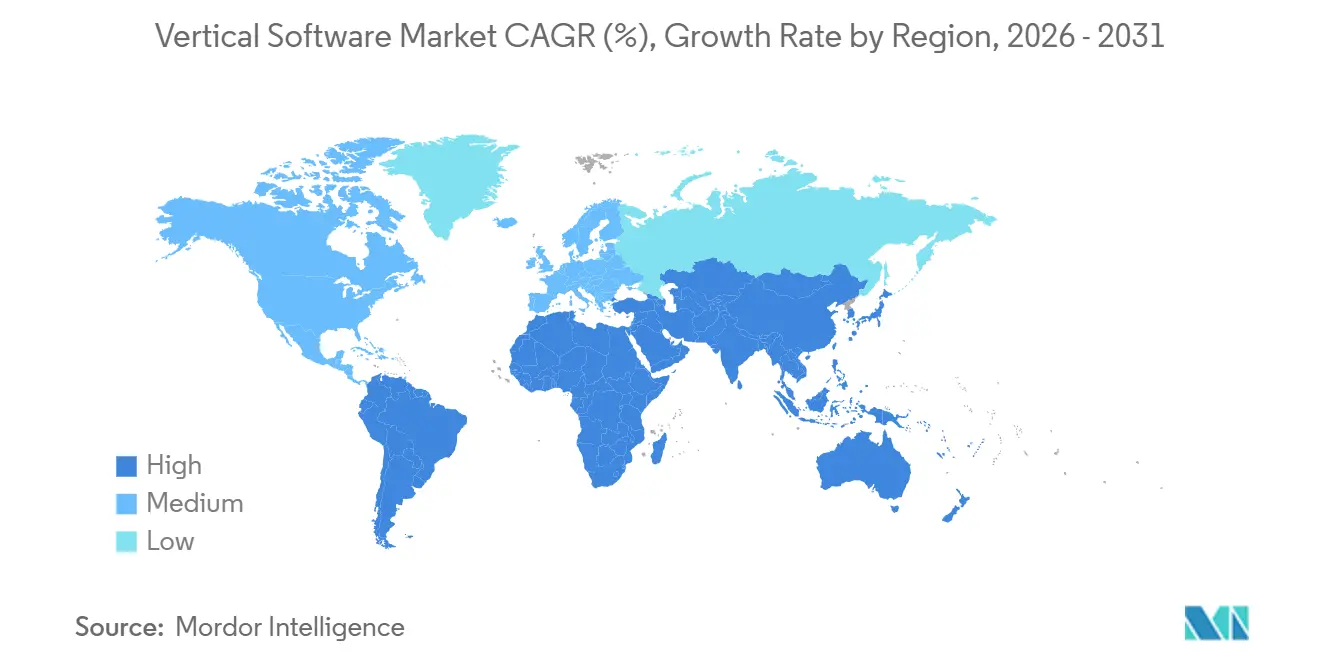

| Fastest Growing Market | Middle East and Africa |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vertical Software Market Analysis by Mordor Intelligence

The vertical software market size was valued at USD 147.11 billion in 2025 and estimated to grow from USD 164.06 billion in 2026 to reach USD 282.98 billion by 2031, at a CAGR of 11.52% during the forecast period (2026-2031). Abandonment of one-size-fits-all suites in favor of workflow-rich industry clouds is accelerating adoption, while embedded analytics and low-code configuration shrink time-to-value for buyers. Subscription economics and auto-scaling capacity have pushed cloud deployment to the forefront, and composable microservice design now lets enterprises integrate best-of-breed modules with minimal disruption. Mid-market firms benefit most, as vertical SaaS removes the capital and talent barriers that once favored large incumbents, and AI-native toolkits unlock precision use cases in manufacturing, healthcare, and agriculture. Regionally, mature North American spending still dominates revenue, yet mobile-first rollouts across the Middle East and Africa are expanding the addressable base more quickly, reshaping vendor go-to-market priorities.

Key Report Takeaways

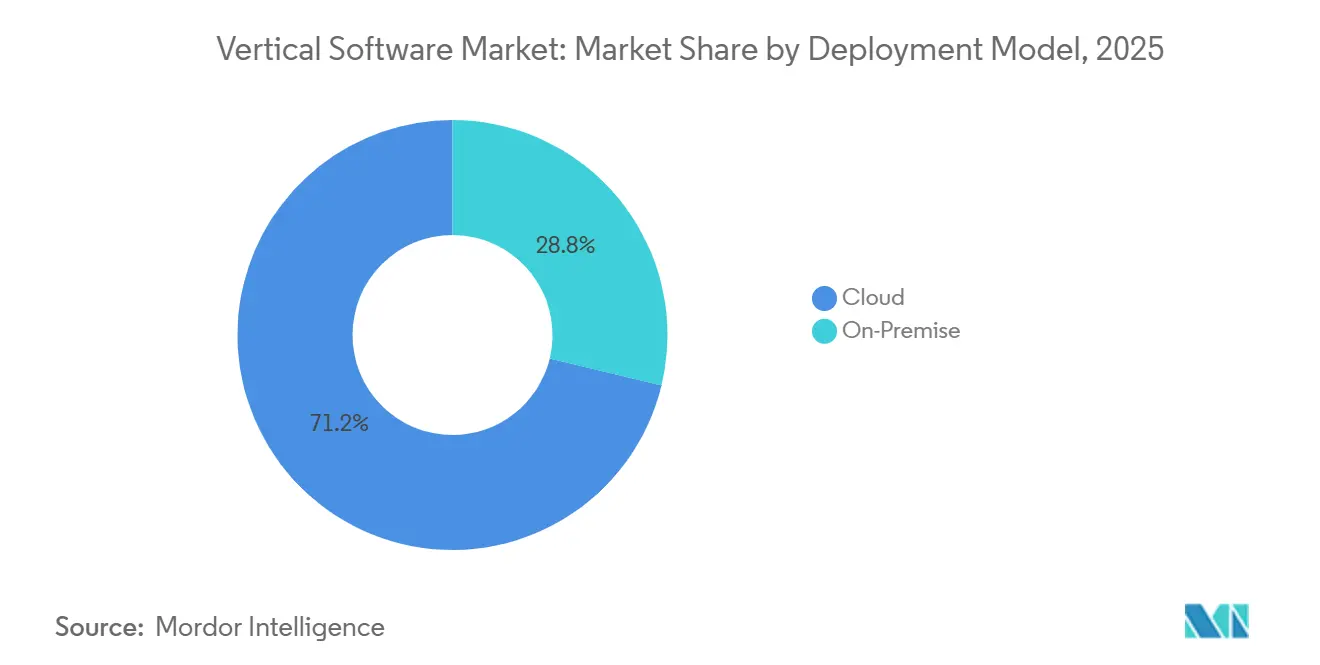

- By deployment model, cloud captured 71.22% of the vertical software market share in 2025 and posted the highest projected CAGR at 11.96% through 2031.

- By organization size, small and medium enterprises accounted for 57.63% of the vertical software market share in 2025 and are projected to expand at an 11.93% CAGR over 2026-2031.

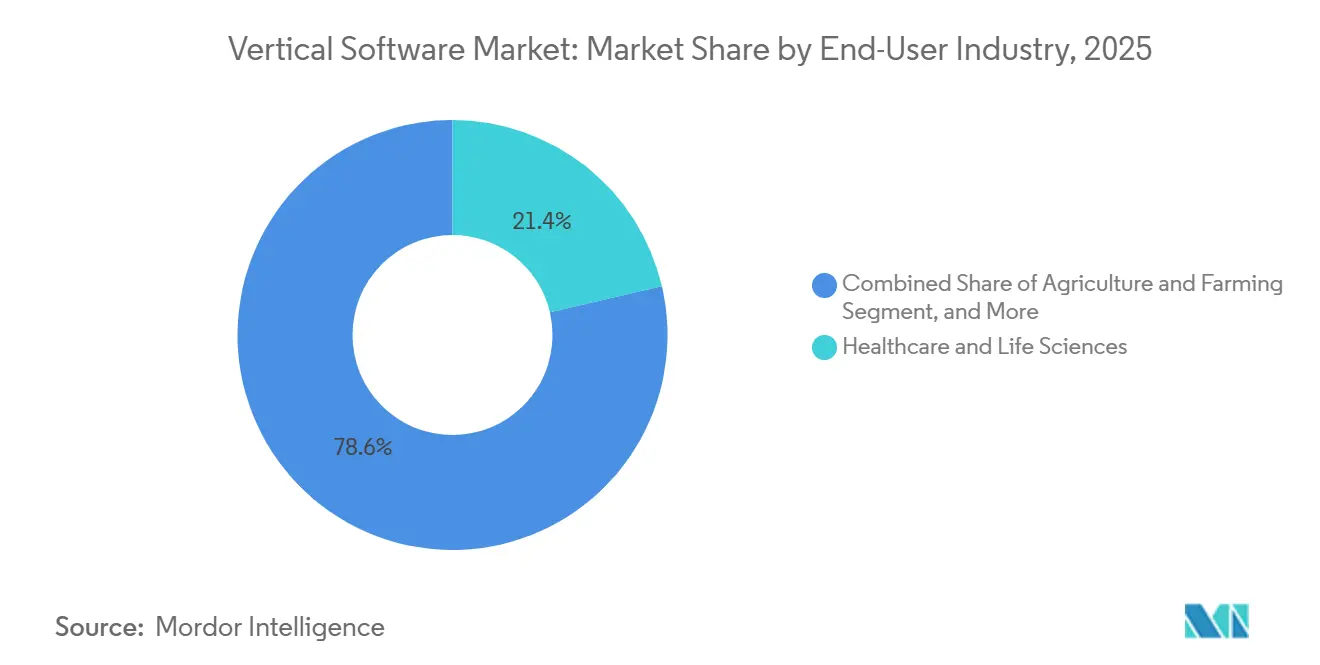

- By end-user industry, healthcare and life sciences led with 21.36% revenue share in 2025, while agriculture is forecast to record the fastest growth at a 13.12% CAGR to 2031.

- By application, customer relationship management accounted for 24.72% of revenue share in 2025, whereas supply chain management applications are expected to grow at a 12.33% CAGR through 2031.

- By geography, North America accounted for 42.38% of the vertical software market share in 2025, while the Middle East and Africa are projected to advance at a 12.56% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Vertical Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Emergence of Industry-Specific Cloud Platforms Accelerating Adoption in the United States and Europe | +3.2% | North America and Europe | Medium term (2-4 years) |

| Regulatory Compliance Pressures in BFSI and Healthcare Boosting Specialized Solutions | +2.8% | Global, with concentration in North America and Europe | Short term (≤ 2 years) |

| AI and ML Toolkits Driving Mid-Sized Manufacturing Modernization in Asia-Pacific | +2.1% | Asia-Pacific core, spill-over to Middle East and Africa | Medium term (2-4 years) |

| Digitalization of Ag-Food Supply Chains Fueling AgTech SaaS in South America | +1.9% | South America, with early gains in Brazil and Argentina | Long term (≥ 4 years) |

| Government-Funded Smart-Hospital Programs Propelling Health-Tech Software | +1.3% | Europe and Asia-Pacific | Medium term (2-4 years) |

| Industry-Led Data-Mesh Architectures Creating Niche Analytics Opportunities | +0.9% | Global, led by North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Emergence of Industry-Specific Cloud Platforms Accelerating Adoption

Hyperscalers and independent software vendors now ship pre-configured industry clouds that wrap core workflows, reference compliance controls, and curated partner services, slashing deployment cycles from months to weeks.[1]Microsoft Corp., “Industry Cloud Solutions,” microsoft.com Buyers in Europe favor localized versions that align with the General Data Protection Regulation and the upcoming Data Act, reinforcing demand for sovereign hosting options. Banking adopters point to open-banking rules under the revised Payment Services Directive that require real-time API orchestration and consent logging, which are unavailable in legacy cores. Health systems migrating electronic records to Microsoft Cloud for Healthcare or Oracle’s Health platform gain native ISO 27001 and ISO 27701 certifications, thereby shortening security reviews. As more vendors add composable microservices, customers can swap modules without a full re-implementation, widening the addressable pool of mid-market clients.

Regulatory Compliance Pressures in BFSI and Healthcare Boosting Specialized Solutions

A tightening web of rules, HIPAA in the United States, GDPR in Europe, and the Payment Card Industry Data Security Standard worldwide, demands granular audit trails, role-based access, and automated breach reporting that horizontal suites rarely provide out of the box. Banks facing Basel III and IFRS 9 must run near-real-time risk and expected-loss models, prompting adoption of purpose-built treasury and credit platforms. Hospitals shifting to value-based reimbursement depend on software that integrates clinical, claims, and social determinants of health data to meet the quality measures required by Medicare programs.[2]Centers for Medicare and Medicaid Services, “Interoperability and Patient Access Final Rule,” cms.gov Life-sciences firms automate adverse-event reporting and trial submissions through vertical platforms already aligned with International Council for Harmonisation guidelines, reducing filing time and regulatory queries. Procurement teams increasingly insert HL7 FHIR certification as a prerequisite, filtering out vendors without proven interoperability credentials.

AI and ML Toolkits Driving Mid-Sized Manufacturing Modernization

94% of Asia-Pacific manufacturers invested in generative-AI pilots in 2025, embedding computer-vision inspection and predictive-maintenance models into shop-floor execution systems.[3]Rockwell Automation Inc., “State of Smart Manufacturing Report 2025,” rockwellautomation.com Japan’s Connected Industries subsidies offset up to 50% of deployment costs, accelerating take-up among tier-two suppliers that previously lacked data-science talent. China’s provincial grants under the Digital China initiative prioritize domestic vendors that bundle AI with industrial-internet security, raising local content requirements. Modern vertical platforms ship with drag-and-drop model orchestration and pre-trained weights, allowing plant engineers to tune algorithms without writing code. Compliance with IEC 62443 cybersecurity standards is now table-stakes in tenders, ensuring that AI gains do not weaken operational-technology defenses.

Digitalization of Ag-Food Supply Chains Fueling AgTech SaaS

South American growers deploy platforms that blend satellite imagery, soil-sensor telemetry, and commodity-price feeds to optimize input use and harvest timing, trimming post-harvest losses by up to 30% in Brazilian pilots. Argentina’s blockchain traceability program links farm data to export documents, lowering certification costs and boosting market access for organic produce. The International Finance Corporation counts more than 1,200 active AgTech startups in Latin America that together raised USD 2.3 billion from 2023 to 2025, intensifying competition and solution diversity. Carbon-credit registries integrated into farm-management suites give smallholders a new revenue stream while aligning with corporate net-zero pledges. Interoperability toolkits, such as the Agricultural Data Application Programming Toolkit, standardize data exchange, fostering ecosystem consolidation and reducing vendor lock-in risks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy Data Silos Slowing Vertical Cloud Migration in the Public Sector | -1.8% | Global, with acute challenges in Europe and North America | Medium term (2-4 years) |

| Shortage of Domain-Savvy Talent Limiting Customization Speed | -1.5% | Global | Long term (≥ 4 years) |

| Rising Cyber-Liability Insurance Costs Inflating Total Cost of Ownership | -1.2% | North America and Europe | Short term (≤ 2 years) |

| Multi-Jurisdiction Regulations Hindering Cross-Border Rollouts in Europe and Asia-Pacific | -1.0% | Europe and Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Legacy Data Silos Slowing Vertical Cloud Migration in the Public Sector

Governments still run mission-critical workloads on mainframes coded in obsolete languages, with data stored in proprietary formats that resist extraction, delaying cloud readiness. Procurement statutes often require on-premise hosting or hybrid topologies that preserve sunk infrastructure, diminishing the economic appeal of SaaS conversions. Even when agencies budget for modernization, FedRAMP or the European NIS2 Directive impose security authorizations that add 12- to 18-month lead times to every deployment. The European Commission earmarked EUR 7.5 billion for public-sector IT over 2021-2027, yet progress remains uneven as member states juggle competing priorities and limited specialist capacity. Until automated migration utilities mature, these legacy knots will continue to dampen public-sector momentum.

Shortage of Domain-Savvy Talent Limiting Customization Speed

Vertical implementations demand experts who pair sector knowledge with platform skills, a talent profile that universities rarely cultivate. Global shortages could leave 85 million tech roles unfilled by 2030, with acute gaps in healthcare informatics, financial modeling, and industrial automation. Vendors report year-long waits to hire clinical workflow consultants or credit risk solution architects, stretching project timelines and ballooning billable hours. Governments push reskilling initiatives, yet most programs emphasize generic coding over domain-specific configuration, leaving the core mismatch unresolved. Without coordinated industry-academia pipelines, talent scarcity will continue to slow customization and constrain vertical software scale-out.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud Dominance Reinforced By Composability Gains

Cloud solutions held a commanding 71.22% of the vertical software market share in 2025, and the segment is forecast to post an 11.96% CAGR through 2031. The lead reflects a decisive buyer preference for subscription pricing, auto-scaling resources, and microservice architectures that speed feature releases and security patches. As industry clouds bundle reference-compliance controls, procurement teams achieve shorter audit cycles and faster sign-offs, deepening adoption across banking, healthcare, and construction. On-prem deployments linger in defense and critical infrastructure environments, where air-gapped networks remain mandatory, but growth is marginal as modernization funds shift to hybrid or full-cloud estates.

Hybrid topologies that keep sensitive data local while moving analytics to the cloud offer a transition path for regulated organizations, yet they add complexity in identity federation and data synchronization. Standards such as ISO 22301 for business continuity and ISO 27017 for cloud security now appear in nearly every request for proposal, setting baseline expectations for uptime and encryption. Hyperscalers respond with sovereign cloud regions that satisfy residency rules without sacrificing elasticity, widening the addressable pool of cloud subscriptions within the vertical software market.

By Organization Size: SMEs Leverage Vertical SaaS To Bypass Legacy Constraints

Small and medium enterprises accounted for 57.63% of 2025 revenue and are projected to expand at an 11.93% CAGR between 2026 and 2031. Mobile-first platforms that ship with preset workflows, automated updates, and built-in regulatory reporting let smaller businesses sidestep the heavy IT lift once required for enterprise resource planning. Clinics, contract manufacturers, and specialty retailers often migrate straight from spreadsheets to cloud suites, realizing productivity gains within weeks. The European Union’s Digital Europe Programme channels grants and training to SME digitalization, accelerating purchase decisions.

Large enterprises, which accounted for 42.37% of 2025 sales, face multi-year migration roadmaps and embedded legacy integrations that slow rollouts, though pilot projects within individual business units are becoming common. These firms increasingly choose composable architectures, so regional teams can plug in localized tax, payroll, or privacy modules without waiting for global template releases. Vendor roadmaps that promise backward-compatible APIs and no-code configuration appeal to both cohorts, yet the relative agility of SMEs keeps their adoption curve steeper, reinforcing their leadership in vertical software market share growth.

By End-User Industry: Healthcare Leads Share, Agriculture Posts Fastest Growth

Healthcare and life sciences accounted for 21.36% of 2025 revenue, supported by electronic health record modernization, telehealth adoption, and tighter value-based reimbursement metrics. Providers favor platforms certified to HL7 FHIR for interoperability, enabling seamless data exchange with payers and research networks. BFSI follows, driven by open-banking mandates that call for real-time risk engines and consent orchestration. These sectors demand rigorous audit trails, positioning purpose-built suites ahead of horizontal alternatives.

Agriculture registers the fastest growth at a 13.12% CAGR, as precision-farming applications blend satellite imagery, IoT soil telemetry, and carbon-credit registries to raise yields and open new revenue streams. Government incentives in Brazil and Argentina subsidize adoption, while venture capital funds support more than 1,200 AgTech startups in Latin America. Education, government, and media verticals are also scaling, propelled by hybrid instruction models, citizen-service digitization, and streaming-centric monetization. Collectively, these varied use cases diversify demand and expand the vertical software market across industries.

By Application: CRM Dominates, SCM Surges On Resilience Imperatives

Customer relationship management accounted for 24.72% of 2025 revenue as enterprises pursue omnichannel engagement and unified customer profiles. Modules for automated outreach, service chatbots, and predictive upsell analytics now ship pre-tuned for banking, healthcare, and hospitality, cutting customization effort. Embedded consent tracking aligns with tightening data-privacy rules, making CRM an indispensable anchor in many digital-transformation roadmaps.

Supply chain management is projected to advance at a 12.33% CAGR through 2031, reflecting corporate urgency to harden logistics against tariff shifts and near-shoring. Modern suites integrate demand sensing, inventory orchestration, and emissions tracking, aligning operational resilience with sustainability disclosures. Vertical ERP offerings continue to bundle finance, HR, and production ledgers, but growth is steadier as many enterprises already hold baseline functionality. Human resource management applications evolve into skills-based planning engines, preparing firms for looming talent shortages highlighted by the International Labour Organization. Together, these dynamics confirm that workflow depth, regulatory readiness, and data-driven insights remain decisive factors guiding application-level spending in the vertical software industry.

Geography Analysis

North America accounted for 42.38% of global revenue in 2025, driven by sophisticated healthcare, BFSI, and technology spending. United States providers accelerate software purchases to comply with interoperability mandates, while Canada’s natural resources exporters adopt ESG reporting suites. Mexico’s manufacturers are deploying vertical platforms to comply with USMCA origin rules, reflecting supply-chain tightening. Although the region expanded 10.1% during 2020-2025, its share is gradually sliding as emerging markets scale faster. South America is forecast to advance at 11.8% through 2031. Brazil’s open-banking rollout and Argentina’s precision-farming incentives stimulate vertical SaaS uptake in finance and agriculture. Regional trade blocs promote interoperability, encouraging cross-border platform adoption in mining, energy, and logistics.

Europe accounted for 28.4% of 2025 revenue, with GDPR, the forthcoming Data Act, and the European Health Data Space driving compliance-driven spend. Germany’s Industrie 4.0 and France’s Industrie du Futur subsidies boost manufacturing software adoption, while the United Kingdom’s post-Brexit regulatory divergence creates dual compliance requirements, bolstering demand for specialized tools. Asia-Pacific is projected to grow at 12.1% through 2031. China’s Digital China initiative, Japan’s Society 5.0 roadmap, and India’s Production-Linked Incentive program all channel subsidies toward smart manufacturing, e-commerce, and digital healthcare. South Korea’s New Deal amplifies AI and 5G deployments, and ASEAN governments coordinate cross-border privacy rules, easing SaaS expansion. These investments collectively enlarge the addressable vertical software market size in the world’s most populous region.

The Middle East and Africa will post the fastest regional CAGR of 12.56%. Gulf Cooperation Council states invest in e-government, tourism, and digital health solutions aligned with national diversification agendas, while Kenya, Nigeria, and South Africa expand fintech ecosystems that leapfrog reliance on card networks. Continental free-trade protocols and pan-African digital-identity schemes further lower adoption barriers, positioning the region as a key frontier for the vertical software market.

Competitive Landscape

The vertical software market is moderately concentrated, with the ten largest vendors accounting for roughly 35% of 2025 revenue, leaving meaningful space for niche specialists to thrive. Scale leaders anchor their positions through certified compliance, deep workflow coverage, and multi-year customer contracts that limit churn. Market entry barriers remain low for cloud-native startups, yet sustained expansion still hinges on domain expertise and go-to-market focus. Overall, rivalry is intense, but pricing power varies widely by industry and by the regulatory criticality of each application. Most segments, therefore, resemble a patchwork of dominant brands and long tails of smaller providers.

Pure-play leaders such as Veeva Systems in life sciences, Guidewire Software in property-casualty insurance, and Procore Technologies in construction maintain defensible moats by embedding industry regulations and best-practice workflows directly into their code bases. Horizontal giants are countering this depth play; Microsoft, Salesforce, Oracle, and SAP now field dedicated industry clouds, pre-configured data models, and specialized sales teams to capture share in regulated sectors. Their success varies because buyers still weigh the breadth of the ecosystem against the domain immersion offered by smaller rivals. Partners such as global systems integrators and hyperscalers often tip the scales in competitive outcomes by bundling migration services or offering preferential infrastructure pricing. Joint ventures and white-label agreements, therefore, multiply as vendors look to close capability gaps without lengthy in-house development.

Private-equity roll-ups led by Constellation Software continue to aggregate dozens of subscale vertical vendors, gaining economies of scope while preserving brand autonomy to protect customer loyalty. Venture capital backs AI-native challengers that blend workflow automation with embedded payments and data marketplaces, reshaping under-digitized niches like field services and specialty retail. Generative AI, blockchain provenance, and low-code orchestration are emerging as the new battlegrounds, shifting competition away from feature checklists toward algorithmic accuracy and data-network effects. These forces collectively ensure that innovation cycles remain brisk, acquisition pipelines stay active, and competitive dynamics evolve rapidly across the vertical software market.

Vertical Software Industry Leaders

Constellation Software Inc.

Verisk Analytics, Inc.

athenahealth, Inc.

Bio-Logic Science Instruments SA

VetBadger LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Veeva Systems acquired Crossix Solutions for USD 430 million to strengthen real-time marketing-effectiveness analytics.

- December 2025: Shopify launched Commerce Components, enabling enterprises to embed Shopify checkout and inventory into existing stacks.

- November 2025: Procore Technologies partnered with Autodesk to synchronize BIM and field operations for contractors.

- October 2025: ServiceTitan raised USD 250 million in Series F funding to expand internationally and add AI-powered scheduling.

Global Vertical Software Market Report Scope

The Vertical Software Market Report is Segmented by Deployment Model (Cloud, and On-Premise), Organization Size (Small and Medium Enterprises, and Large Enterprises), End-User Industry (BFSI, Healthcare and Life Sciences, Education, Government and Legal, Media, Entertainment and Hospitality, Clothing and Apparel, Agriculture and Farming, Other End-User Industries), Application (Customer Relationship Management, Enterprise Resource Planning, Supply Chain Management, Human Resource Management), and Geography (North America, South America, Europe, Asia Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Cloud |

| On-Premise |

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

| BFSI |

| Healthcare and Life Sciences |

| Education |

| Government and Legal |

| Media, Entertainment and Hospitality |

| Clothing and Apparel |

| Agriculture and Farming |

| Other End-User Industries |

| Customer Relationship Management |

| Enterprise Resource Planning |

| Supply Chain Management |

| Human Resource Management |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Deployment Model | Cloud | ||

| On-Premise | |||

| By Organization Size | Small and Medium Enterprises (SMEs) | ||

| Large Enterprises | |||

| By End-User Industry | BFSI | ||

| Healthcare and Life Sciences | |||

| Education | |||

| Government and Legal | |||

| Media, Entertainment and Hospitality | |||

| Clothing and Apparel | |||

| Agriculture and Farming | |||

| Other End-User Industries | |||

| By Application | Customer Relationship Management | ||

| Enterprise Resource Planning | |||

| Supply Chain Management | |||

| Human Resource Management | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How quickly is the vertical software market expected to grow through 2031?

The vertical software market size is forecast to rise from USD 164.06 billion in 2026 to USD 282.98 billion by 2031, registering an 11.52% CAGR.

Which deployment model leads current spending?

Cloud solutions held 71.22% of 2025 revenue and continue to outpace on-premise alternatives.

What segment is expanding the fastest by end-user industry?

Agriculture is the fastest-growing end-user segment, advancing at a 13.12% CAGR on the back of precision-farming software.

Which region offers the highest growth potential?

Middle East and Africa is projected to post the fastest regional CAGR at 12.56% through 2031.

Who are the notable pure-play leaders in vertical software?

Companies such as Veeva Systems, Guidewire Software, and Procore Technologies hold strong positions in life sciences, insurance, and construction respectively.

Why are supply-chain management applications gaining momentum?

Firms are digitizing procurement, inventory, and logistics to manage tariff shifts and near-shoring, driving SCM applications to a 12.33% CAGR.

Page last updated on: