Grant Management Software Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 2.56 Billion |

| Market Size (2030) | USD 4.23 Billion |

| Growth Rate (2025 - 2030) | 10.57% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Grant Management Software Market Analysis by Mordor Intelligence

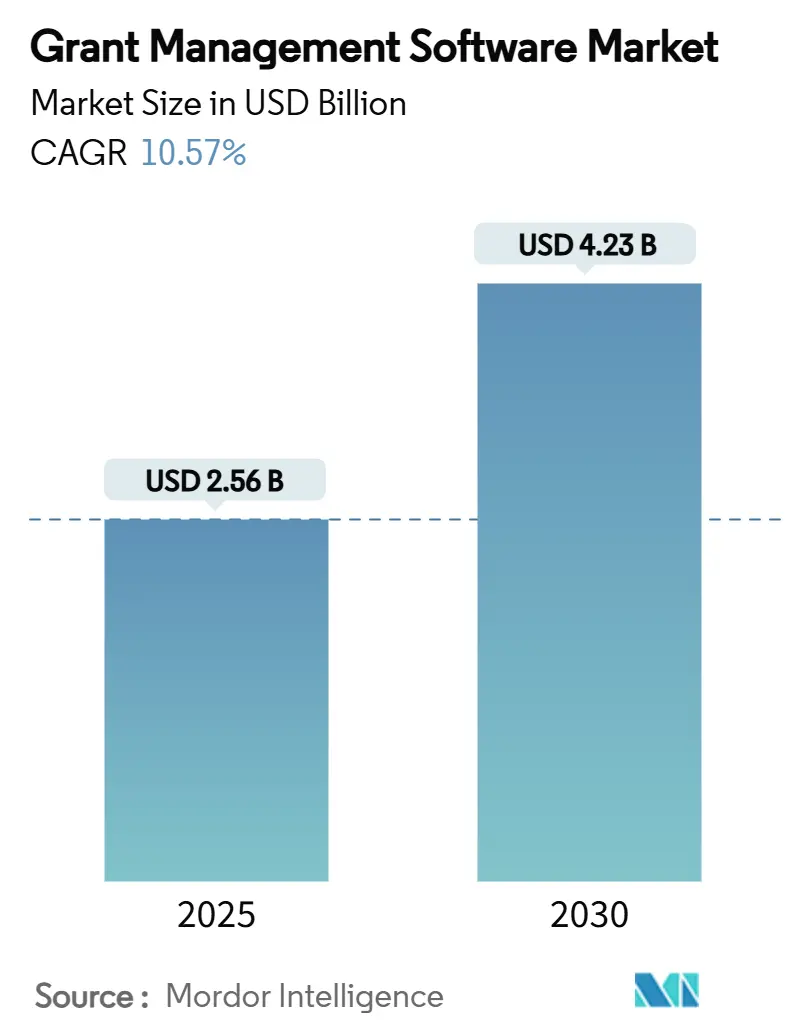

The grant management software market size stands at USD 2.56 billion in 2025 and is forecast to reach USD 4.23 billion by 2030 at a CAGR of 10.57% during 2025-2030. Demand accelerates as government agencies, nonprofits, universities, and healthcare systems modernize award administration to comply with stricter transparency rules, handle larger funding pools created by new federal legislation, and retire legacy platforms that still absorb 80% of U.S. federal IT budgets. Digital-first mandates, growing comfort with cloud procurement, and the rapid infusion of artificial intelligence for fraud detection further expand the grant management software market. The sector also benefits from outcome-based reporting rules that reward grantees able to demonstrate measurable impact in real time. Together, these forces create a favourable environment for both established vendors and cloud-native entrants that offer purpose-built functionality, application programming interfaces, and pre-configured regulatory templates.

Key Report Takeaways

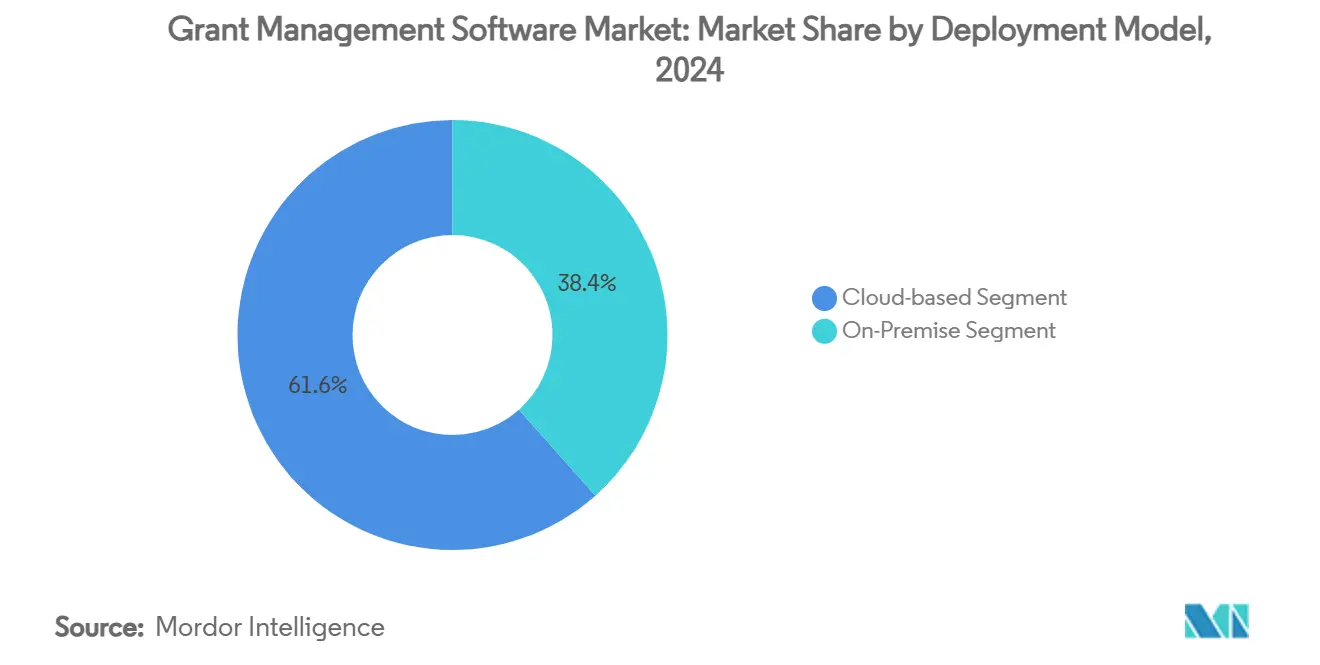

- By Deployment Model, the cloud-based solutions segment captured 61.57% of the grant management software market share in 2024.

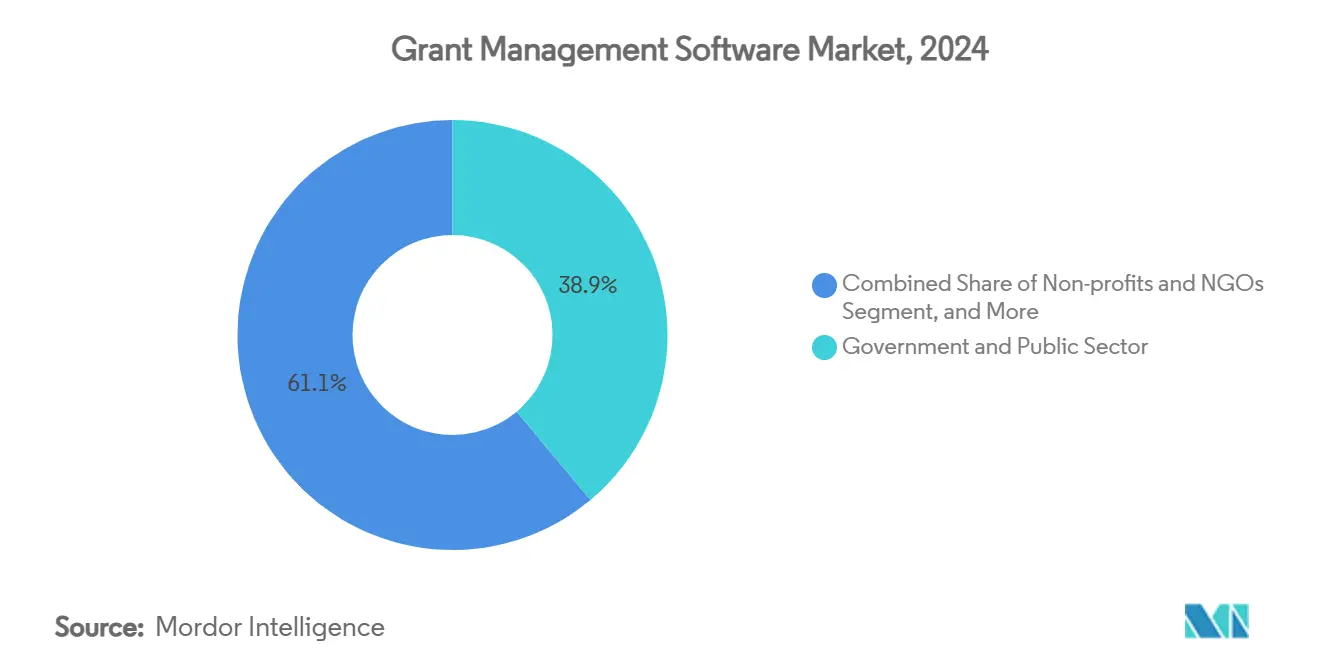

- By End-User, the government and public sector segment is projected to grow at 12.23% CAGR between 2025-2030

- By Component, the software platforms accounted for 69.25% of the overall grant management software market size in 2024.

- By Geography, North America held 45.12% market share of the grant management software in 2024.

Global Grant Management Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid shift to purpose-built SaaS grant platforms | +2.8% | Global, with North America and Europe leading adoption | Medium term (2-4 years) |

| Mandates for outcome-based reporting by donors & governments | +2.1% | Global, particularly strong in North America and EU | Short term (≤ 2 years) |

| Expansion of U.S. federal funding programs post-IIJA & IRA | +1.9% | North America, with spillover effects to allied nations | Medium term (2-4 years) |

| Digital transformation of philanthropic foundations worldwide | +1.7% | Global, with APAC showing accelerated adoption | Long term (≥ 4 years) |

| Integration of predictive AI for fraud-detection & risk-scoring | +1.4% | North America and EU core, expanding to APAC | Long term (≥ 4 years) |

| Emergence of interoperable open-grant-data standards | +1.1% | Global, with UK and US leading standardization efforts | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Shift to Purpose-Built SaaS Grant Platforms

Organizations are abandoning generic customer-relationship platforms in favor of specialist solutions that embed federal Uniform Grant Guidance, automate subaward monitoring, and deliver click-ready compliance reports. The U.S. Office of Management and Budget reinforces this pivot by encouraging commercial off-the-shelf procurement for grants exceeding USD 600 billion annually[1]Data Foundation, “Managing Grants in a Time of Transformation,” DataFoundation.org. Purpose-built SaaS offerings shorten deployment cycles, reduce customization costs, and permit real-time updates as rules evolve. Agencies benefit from pre-mapped data schemas that feed directly into government-wide repositories, while nonprofits gain templates that streamline application forms and post-award reporting. Vendors that master low-code configurability, single sign-on, and FedRAMP authorization now capture outsized demand, strengthening the grant management software market.

Mandates for Outcome-Based Reporting by Donors & Governments

Regulators increasingly require proof that public money translates into quantifiable community benefits. The U.S. DATA Act standardizes financial data across federal grant programs, forcing recipients to submit machine-readable spending and performance metrics[2]Grants.gov, “DATA Act (2014),” Grants.gov. Europe’s Horizon Europe framework follows a similar path, obliging beneficiaries to monitor key performance indicators throughout the project life cycle. Platforms that automatically tag expenditures to outcomes, visualize progress dashboards, and push real-time alerts help grantees avoid clawbacks. Consequently, the grant management software market gains from organizations under pressure to link dollars to results quickly and accurately.

Expansion of U.S. Federal Funding Programs Post-IIJA & IRA

The Infrastructure Investment and Jobs Act deploys USD 1.2 trillion, including USD 65 billion for broadband projects, sparking an influx of complex, multijurisdictional grants that demand advanced digital oversight[3]Government Finance Officers Association, “Infrastructure Investment and Jobs Act Resources,” GFOA.org. Transportation agencies must certify sub-recipient eligibility, document environmental reviews, and align project milestones to reimbursement schedules. Purpose-built platforms provide configurable workflows that route approvals, flag non-compliant expenses, and integrate geospatial data for field validation. As states and municipalities rush to meet application windows, scalable SaaS vendors expand market penetration, reinforcing momentum in the grant management software market.

Digital Transformation of Philanthropic Foundations Worldwide

Large private foundations seek to cut administrative overhead and direct more funds to programs. Many now prioritize cloud platforms that deliver automated due diligence checks, stakeholder portals, and impact analytics. Asia-Pacific foundations, buoyed by strong wealth creation, increasingly adopt AI-enabled tools that score grant proposals against strategic objectives, accelerating funding cycles. Enhanced collaboration features attract cross-border coalitions, adding depth to the grant management software market, particularly in APAC.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented regulatory requirements across jurisdictions | -1.8% | Global, particularly challenging for cross-border operations | Medium term (2-4 years) |

| High switching costs from legacy in-house systems | -1.5% | North America and Europe, where legacy systems are prevalent | Short term (≤ 2 years) |

| Data-sovereignty concerns hindering cross-border SaaS adoption | -1.2% | EU and APAC regions with strict data protection laws | Long term (≥ 4 years) |

| Shortage of grant-tech implementation talent | -0.9% | Global, with acute shortages in specialized technical roles | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented Regulatory Requirements Across Jurisdictions

Differences between U.S. Uniform Guidance, EU Financial Regulation 2024/2509, and domestic rules in emerging markets compel multinational nonprofits to maintain parallel compliance workflows. Each funding body imposes distinct audit trails, cost-classification codes, and data-retention periods, increasing administrative complexity. Platforms must therefore support configurable taxonomies and country-specific data-residency options, adding to development cycles and pricing pressures. This mosaic of rules tempers the wider adoption pace of the grant management software market.

High Switching Costs from Legacy In-House Systems

Federal agencies still earmark 80% of IT budgets for maintaining outdated grant platforms, delaying migration to modern SaaS solutions. Converting years of historical award data and training thousands of staff imposes sizable upfront costs. The U.S. Department of Justice’s JustGrants transition generated 56,000 help-desk tickets in its first year, underscoring the operational risk tied to wholesale system replacements. For many mid-sized nonprofits, the capital outlay and perceived disruption outweigh near-term efficiency gains, slowing overall market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud Dominance Accelerates Digital Shift

Cloud offerings captured 61.57% revenue in 2024 and are projected to grow at 13.71% CAGR through 2030, far outpacing on-premise alternatives. Flexible subscription billing reduces capital expenditure while FedRAMP or ISO 27001 certificates reassure risk-averse agencies. This dynamic underscores why the grant management software market size linked to cloud deployments is expected to surge throughout the forecast horizon. Many federal offices now insert “cloud-first” clauses into grant platform solicitations, prompting vendors to enhance multiregional availability and zero-downtime upgrade paths.

On-premise solutions remain relevant for defense research programs and public-health agencies that handle export-controlled or patient data. These institutions increasingly adopt hybrid strategies, keeping sensitive records on-site while outsourcing applicant portals, document storage, and analytics to commercial clouds. As regulatory confidence in sovereign cloud expands, even conservative bodies signal phased migration plans, reinforcing steady cloud uptake in the broader grant management software market.

By Component: Services Surge on Implementation Complexity

Software platforms contributed 69.25% of 2024 revenue, yet services are slated to expand at 15.85% CAGR through 2030 as organizations request migration roadmaps, API integrations, and role-based training modules. Many grants offices operate lean teams that require external specialists to map legacy data, harmonize cost codes, and align security profiles. The need for wraparound consulting elevates the services line within the grant management software market.

Post-deployment managed services ranging from quarterly compliance audits to AI-driven anomaly detection gain traction as funders tie disbursements to continuous performance feedback. Vendors that package platform licenses with white-glove support increase customer lifetime value and deepen competitive moats inside the grant management software market.

By End-User: Healthcare Emerges as Growth Leader

Government and public-sector bodies held the lion’s share, 38.92% of 2024 spending, yet NIH, FDA, and global health agencies now advocate advanced digital tooling for program monitoring.[4]National Institutes of Health, “Digital Health Technology Derived Biomarkers,” NIH.govHealthcare and life-sciences organizations therefore post the fastest 12.23% CAGR, reflecting rising clinical trial grants, pandemic-preparedness funds, and precision-medicine initiatives. Specific sub-sectors, such as academic medical centers, increasingly rely on outcome dashboards that satisfy Institutional Review Board obligations and donor transparency. This trajectory elevates the healthcare slice of the grant management software market size.

Universities and research institutes follow closely, adopting configurable workflow engines that integrate with electronic research administration suites. Meanwhile, nonprofits with global footprints invest in multilingual applicant portals to attract diversified funding streams, indirectly boosting the grant management software industry’s total accessible revenue.

Geography Analysis

North America generated 45.12% of total 2024 revenue, anchored by federal disbursements exceeding USD 700 billion annually and a mature technology procurement ecosystem. Uniform Grant Guidance compels detailed reporting, while the DATA Act enforces machine-readable formats, positioning the region as the world’s largest adopter of advanced digital grant tools. Cloud vendors with FedRAMP Moderate or High authorization gain a distinct edge. State and local governments further catalyze the grant management software market by leveraging Infrastructure Investment and Jobs Act allocations to deploy enterprise systems that handle complex pass-through funding.

Asia-Pacific is the fastest-growing territory at a forecast 13.57% CAGR. Japan’s Digital Agency awarded JPY 274.9 million (USD 1.8 million) to JDSC for expanding nationwide e-grant processing by 2025, setting a template for municipal replication. Singapore’s Monetary Authority rolled out the Global-Asia Digital Bond Grant Scheme, offering subsidies up to SGD 450,000 (USD 335,000) to foster blockchain-based issuance, indirectly stimulating adjacent grant-tech investments. Regional think tanks emphasize that transparent online public services accelerate citizen trust, suggesting sustained tailwinds for the grant management software market in APAC.

Europe maintains solid momentum amid rigorous Horizon Europe rules and the new Financial Regulation 2024/2509, both of which mandate granular milestone reporting and project auditability. Agencies favor platforms that offer optional EU-only data residency to satisfy GDPR. Domestic vendors in Germany and France win deals by bundling vertical templates for cultural heritage and climate-science grants, balancing competitive pressure from U.S. suppliers. Although data-sovereignty hurdles temper public-cloud uptake, a robust appetite for automated compliance modules keeps the region integral to the global grant management software market.

Competitive Landscape

Competition remains moderate with a mix of diversified enterprise suites and best-of-breed specialists. Blackbaud reported USD 1.2 billion revenue in 2024 with 98% recurring subscriptions, leveraging a multitenant platform that hosts over USD 100 billion in annual grant and donation flows. Its collaboration with Microsoft delivers AI co-pilots that scan invoices and recommend budget reallocations, giving the incumbent a feature breadth advantage. Salesforce markets the Nonprofit Cloud for grantmakers, relying on a global partner network to customize program templates, further densifying the grant management software market.

Fluxx, AmpliFund, and Foundant compete on depth of grant-specific workflows. The August 2024 merger of SmartSimple Software and Foundant pooled engineering talent and expanded a combined global client base, signalling ongoing consolidation. These firms invest heavily in configurable dashboards and advanced permissions that ease consortium-level reporting. Instrumentl, meanwhile, raised USD 55 million in April 2025 to refine AI-powered funding-fit algorithms, touting customer gains of USD 1.1 million in additional awards per year. Platform specialization continues to carve niches focused on higher education, community foundations, or sovereign wealth funds.

Product roadmaps converge on low-code form builders, machine-learning-enabled risk scoring, and open-API ecosystems that link accounting, procurement, and learning-management systems. Vendors offering pre-packaged integrations, FedRAMP authorizations, and EU Cloud Code of Conduct compliance are well positioned to capture procurement cycles dominated by security reviews. As consolidation advances, competition will likely hinge on total cost of ownership, ecosystem breadth, and proven AI demonstrators that automate manual compliance chores, shaping future dynamics in the grant management software market.

Grant Management Software Industry Leaders

Blackbaud, Inc.

Salesforce, Inc.

Fluxx Labs Inc.

AmpliFund

Submittable Holdings, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Instrumentl closed a USD 55 million funding round to accelerate AI-driven grant discovery and workflow automation.

- February 2025: Blackbaud reported FY 2024 revenue of USD 1.2 billion, achieving 4.5% year-on-year growth with 98% recurring billing.

- January 2025: Singapore’s Monetary Authority launched the Global-Asia Digital Bond Grant Scheme offering subsidies up to SGD 450,000 (USD 335,000) for distributed-ledger bond issuance.

- December 2024: UT Health San Antonio selected the Huron Research Suite for grants management, targeting go-live in late 2025.

- October 2024: Blackbaud posted Q3 2024 revenue of USD 286.7 million, with social-sector solutions contributing 89% of total.

Global Grant Management Software Market Report Scope

| Cloud-based |

| On-Premise |

| Software Platform | |

| Services | Implementation and Integration |

| Training and Support |

| Government and Public Sector |

| Non-profits and NGOs |

| Educational and Research Institutions |

| Healthcare and Life-Sciences |

| Corporate Enterprises |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Rest of Africa |

| By Deployment Model | Cloud-based | |

| On-Premise | ||

| By Component | Software Platform | |

| Services | Implementation and Integration | |

| Training and Support | ||

| By End-User | Government and Public Sector | |

| Non-profits and NGOs | ||

| Educational and Research Institutions | ||

| Healthcare and Life-Sciences | ||

| Corporate Enterprises | ||

| By Region | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the grant management software market in 2025?

The grant management software market size is USD 2.56 billion in 2025 and is projected to reach USD 4.23 billion by 2030 at a 10.57% CAGR.

Which deployment model is growing fastest?

Cloud-based deployment leads growth with a projected 13.71% CAGR through 2030 and already represents 61.57% of 2024 revenue.

Which end-user segment offers the highest growth potential?

Healthcare and life-sciences organizations are expected to post the fastest 12.23% CAGR as agencies such as NIH finance digital-health programs.

Why is North America the largest regional market?

North America commands 45.12% share due to stringent Uniform Grant Guidance rules and federal disbursements surpassing USD 700 billion annually.

What are the biggest restraints to faster adoption?

Fragmented regulations, high switching costs from legacy systems, strict data-sovereignty rules, and limited implementation talent collectively slow uptake.

Page last updated on: