Real Estate Investment Software Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

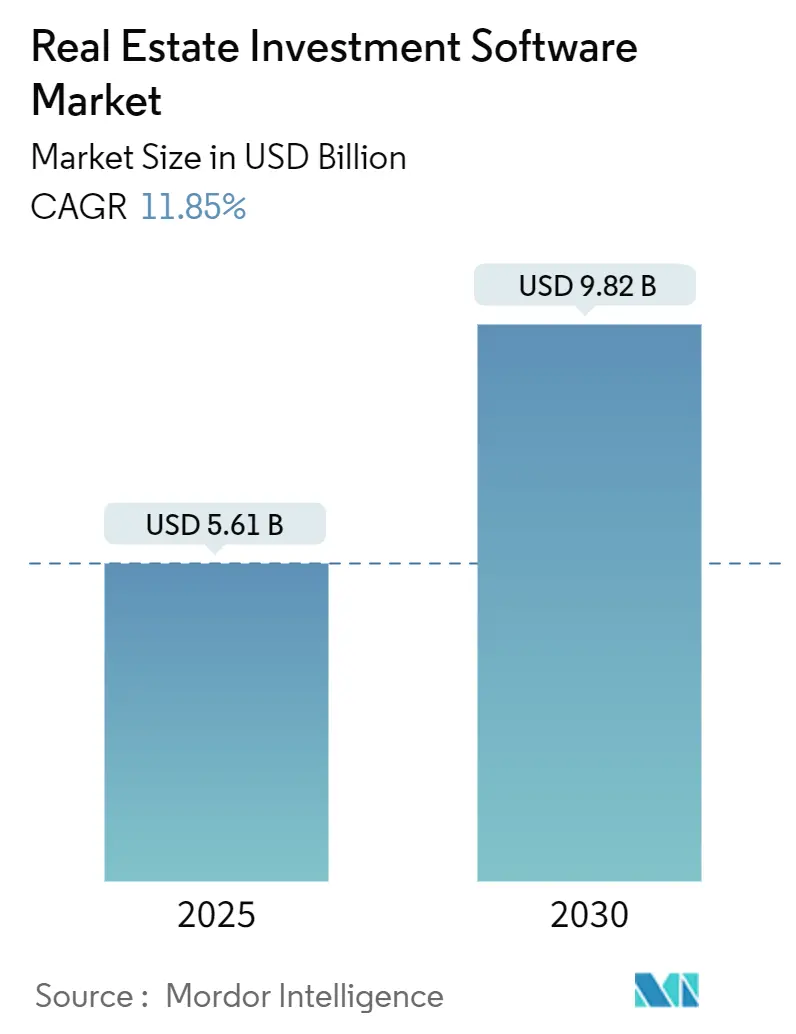

| Market Size (2025) | USD 5.61 Billion |

| Market Size (2030) | USD 9.82 Billion |

| Growth Rate (2025 - 2030) | 11.85% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Real Estate Investment Software Market Analysis by Mordor Intelligence

The real estate investment software market size is USD 5.60 billion in 2025 and is projected to reach USD 9.80 billion by 2030, reflecting an 11.84% CAGR. Cloud-native architectures, compulsory anti-money laundering filings, and artificial intelligence-driven underwriting are accelerating the replacement of spreadsheet workflows. Institutional allocators are increasing their exposure to alternative assets, while small and medium-sized enterprises gain affordable access through subscription pricing. Mandatory disclosure frameworks such as the Financial Crimes Enforcement Network rule and the European Corporate Sustainability Reporting Directive require purpose-built compliance engines, pushing vendors that automate reporting to the forefront. Competition centers on data network effects and API-first platforms that eliminate costly custom integrations, positioning technology leaders to capture incremental wallet share.

Key Report Takeaways

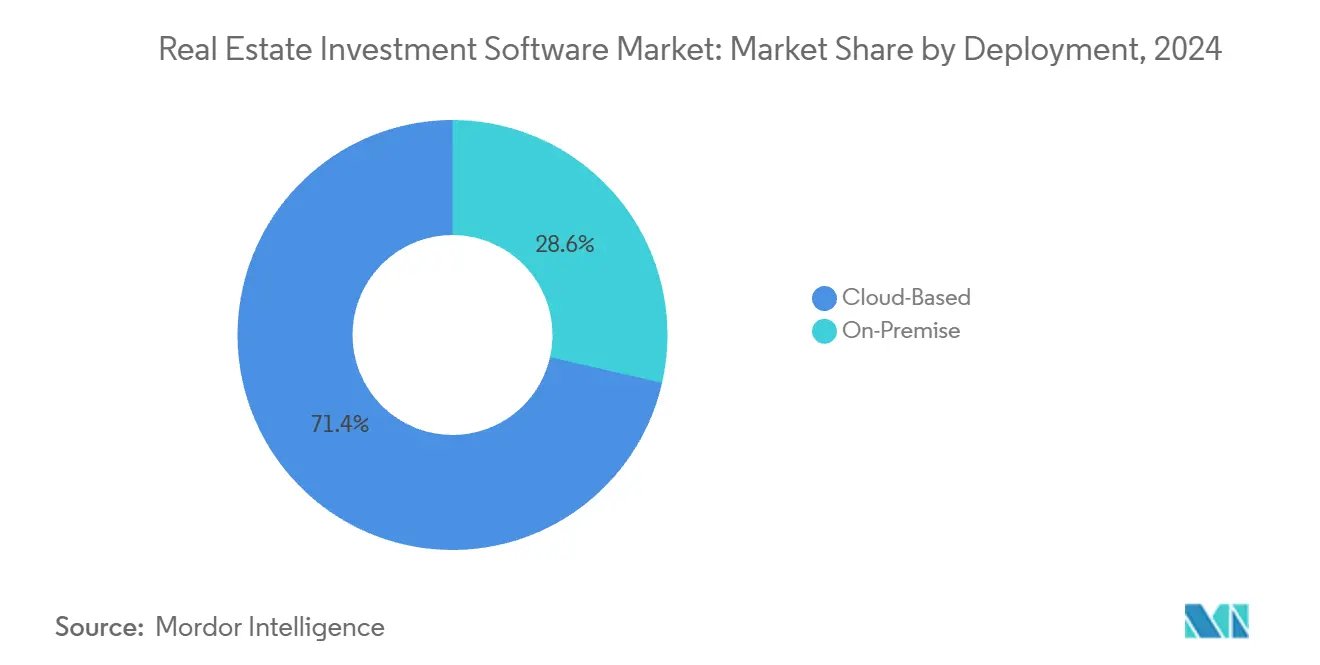

- By deployment, cloud models captured 71.43% real estate investment software market share in 2024 and are advancing at a 13.51% CAGR through 2030.

- By application, asset management software is forecast to expand at a 13.26% CAGR to 2030, while investment management retained a 28.12% share in 2024.

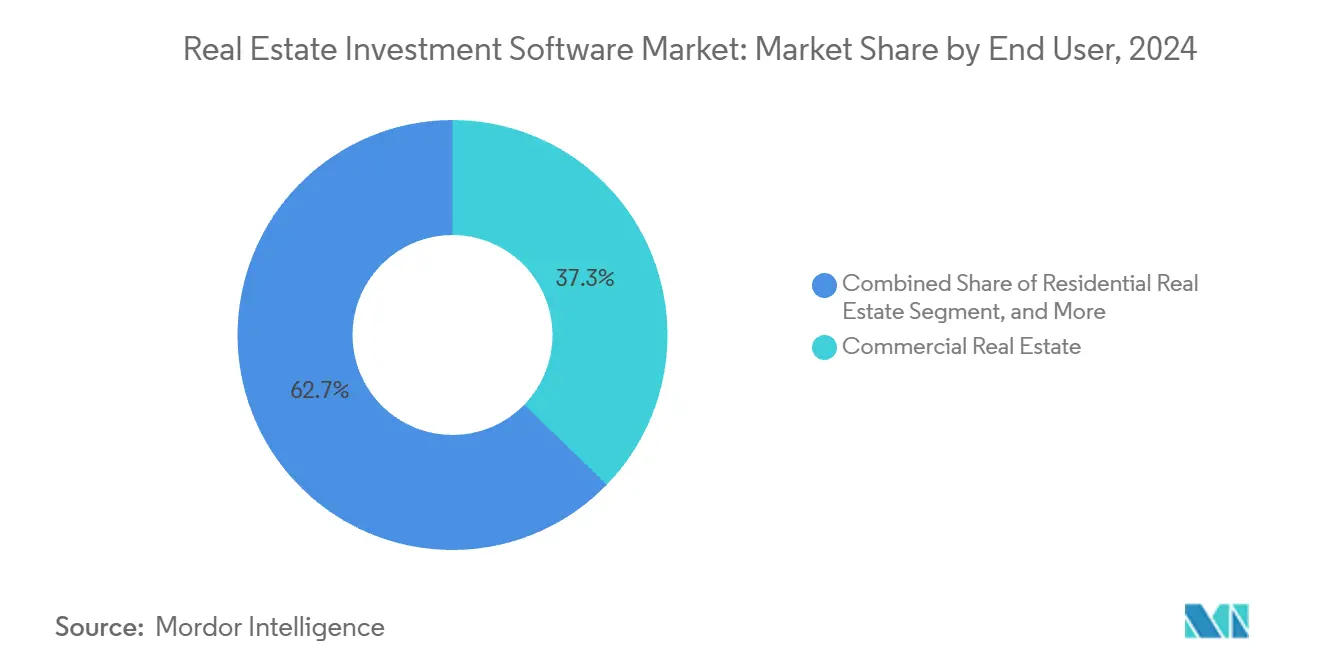

- By end user, commercial real estate led with 37.26% revenue share in 2024; industrial real estate is projected to grow at a 12.51% CAGR to 2030.

- By organization size, large enterprises accounted for 60.37% of 2024 revenue, while small and medium enterprises are expected to expand at a 12.32% CAGR through 2030.

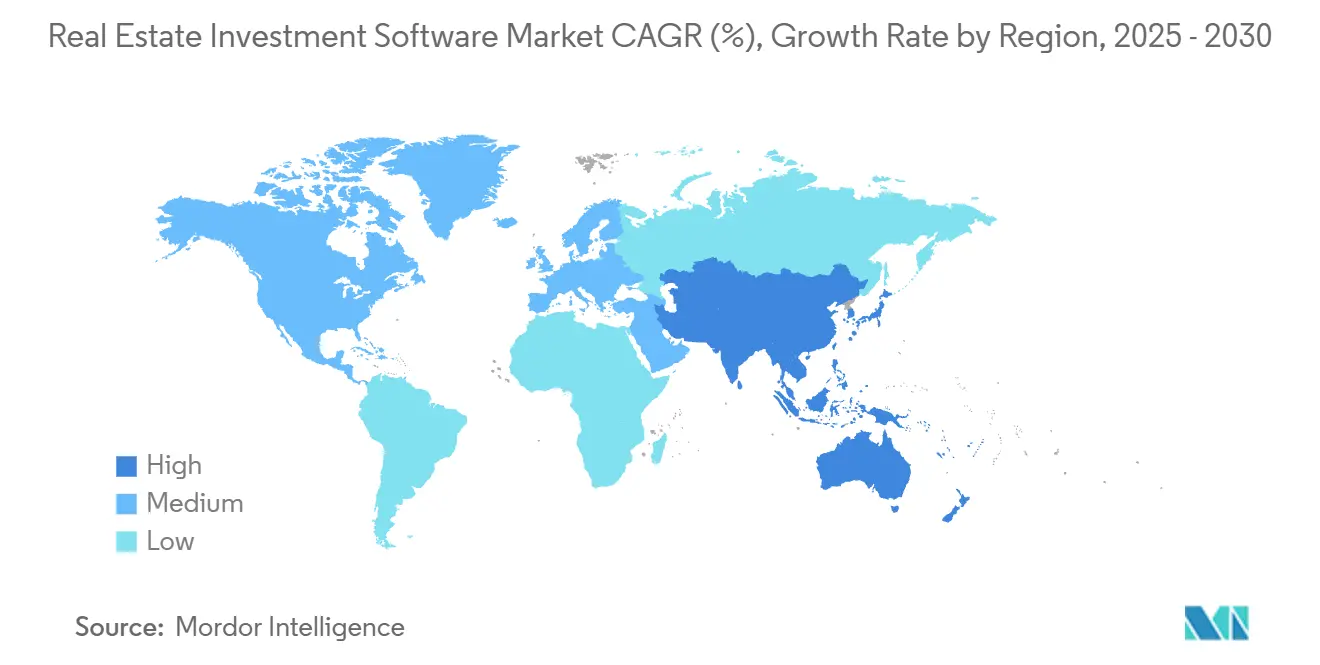

- By geography, North America accounted for 44.81% of the 2024 revenue, whereas the Asia Pacific is forecast to register a 13.16% CAGR through 2030.

Global Real Estate Investment Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Adoption of Cloud Solutions Among Real Estate Asset Managers | +2.80% | Global, early concentration in North America and Western Europe | Short term (≤ 2 years) |

| Growing Institutional Allocation to Alternative Assets | +2.10% | Global, strongest in North America, Asia Pacific, Middle East sovereign wealth hubs | Medium term (2-4 years) |

| Integration of AI-Driven Underwriting and Valuation Tools | +2.50% | North America and Europe lead; Asia Pacific accelerating | Medium term (2-4 years) |

| Increasing Regulatory Reporting Complexity in Global Real Estate | +1.90% | North America, Europe, Asia Pacific | Short term (≤ 2 years) |

| Rise of Tokenization and Fractional Ownership Platforms | +0.90% | Europe, United States, United Arab Emirates | Long term (≥ 4 years) |

| ESG Compliance Pressure on Real Estate Portfolios | +1.80% | Europe, North America, Asia Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of Cloud Solutions Among Real Estate Asset Managers

Multi-tenant software as a service eliminates server maintenance, disaster-recovery hardware, and lengthy upgrade cycles, prompting firms to migrate from on-premise systems. A Deloitte study reported that 81% of commercial real estate executives prioritized cloud migration in 2024. Subscription plans priced at USD 50-USD 150 per user per month replaced six-figure perpetual licenses, opening the real estate investment software market to small syndicators. Security perceptions improved as vendors earned SOC 2 Type II credentials and implemented two-factor authentication, which often surpasses legacy safeguards. Cloud platforms also deliver quarterly updates that automatically embed new FinCEN data schemas, minimizing compliance risk. These economics and operational benefits explain the 13.51% CAGR forecast for cloud deployments.

Integration of AI-Driven Underwriting and Valuation Tools

Artificial intelligence now parses lease abstracts with 95% accuracy, accelerates net operating income forecasts, and shortens bid cycles from weeks to days. Dealpath found that every surveyed institutional firm had adopted or committed to AI underwriting in 2024. JLL’s purchase of Skyline AI embedded satellite imagery and foot-traffic analytics into valuation workflows, indicating sustained investment in predictive modeling. Appraisal regulators now require bias audits and model back-testing, rewarding platforms with robust governance frameworks. Although algorithmic mispricing events, such as Zillow’s 2021 loss, underscore risk, human-in-the-loop validation is mitigating errors and reinforcing adoption.

ESG Compliance Pressure on Real Estate Portfolios

The Corporate Sustainability Reporting Directive requires European issuers to disclose Scope 1, 2, and 3 emissions starting from 2025, making carbon accounting a mandatory component. The EU Taxonomy elevates energy-performance thresholds, steering capital toward certified green buildings. In the United States, anticipated Securities and Exchange Commission climate rules are expected to standardize greenhouse-gas disclosure templates. GRESB participation surpassed 2,100 property funds in 2024, with scores influencing capital allocation among pension plans. Vendors that automate data ingestion from utility meters and generate ESRS-compliant reports can capture premium pricing and secure multi-year contracts.

Increasing Regulatory Reporting Complexity in Global Real Estate

FinCEN’s rule, effective December 2025, mandates electronic filing for residential transfers exceeding USD 50,000, compelling platforms to embed Know-Your-Customer and beneficial ownership modules. India’s Real Estate Regulatory Authority requires quarterly escrow updates and digital audit trails, thereby accelerating software adoption among developers. Singapore’s Monetary Authority imposes enhanced due diligence checks that manual workflows cannot satisfy at scale. These converging rules increase compliance burdens, making configurable workflow engines indispensable across the real estate investment software market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Switching Costs From Legacy Excel Workflows | -1.40% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Data Fragmentation Across Property Management Systems | -1.10% | Global, severe in heterogeneous system landscapes | Medium term (2-4 years) |

| Limited IT Budgets in Small and Medium Real Estate Firms | -0.70% | Global, highest in emerging markets | Short term (≤ 2 years) |

| Cybersecurity Concerns Over Investor Data | -0.60% | Global, stringent jurisdictions with data-residency laws | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Switching Costs From Legacy Excel Workflows

Decades of macros and Visual Basic scripts encode institutional knowledge that is difficult to migrate. Stantem reported that 75% of firms still manually reconcile Excel models with property-management outputs, extending implementation timelines to 12 months or more. Resistance also stems from analysts who fear losing visibility into underlying calculations. Vendors respond with Excel export options and APIs, but these concessions dilute the automation benefits.

Data Fragmentation Across Property Management Systems

Operational data reside in diverse property-management databases lacking standardized APIs. Only 30% of vendors achieved RESO Web API certification by 2024, forcing costly custom integrations and periodic data lags.[1]Real Estate Standards Organization, “RESO Web API,” RESO.ORG Heterogeneous portfolios utilizing multiple systems necessitate weekly CSV uploads or manual entry, which hinders acquisition underwriting and capital redeployment. Although industry consortia advocate for standardization, legacy codebases continue to hinder the development of unified data architectures.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment: Cloud Migration Accelerates as SaaS Economics Favor Scalability

Cloud solutions held 71.43% real estate investment software market share in 2024 and are rising at a 13.51% CAGR, outpacing on-premise alternatives. The real estate investment software market size for cloud deployments equates to USD 4.00 billion in 2025, reflecting subscription models that lower entry barriers for small firms. Vendors deliver quarterly regulatory updates without manual patches, while built-in disaster recovery reduces IT overhead by USD 200,000 annually for mid-sized managers. On-premise remains relevant for sovereign wealth funds that require national data residency under GDPR or China’s PIPL. Hybrid private-cloud offerings now bridge the gap between compliance and scalability, yet the automatic feature releases of multi-tenant SaaS continue to pull market share toward the cloud.

On-premise installations retain a foothold in jurisdictions with strict localization mandates or conservative risk postures. European pension funds sometimes insist on private instances inside national borders, and certain Middle Eastern sovereign investors favor in-country data centers for strategic reasons. Even these clients increasingly adopt containerized deployments that mimic SaaS elasticity. As API ecosystems deepen, cloud vendors can integrate specialty underwriting models, ESG dashboards, and payment gateways faster than on-premise competitors, reinforcing the long-term cloud trajectory within the real estate investment software market.

By Application: Asset Management Software Gains as Institutional Buyers Demand Real-Time KPIs

Investment management modules accounted for 28.12% of 2024 revenue, while asset management software is projected to compound at 13.26% through 2030. The segment’s real estate investment software market size reached USD 1.58 billion in 2025, supported by dashboards that consolidate key performance indicators across multi-region portfolios. Fundraising workflows, waterfall calculations, and investor portals remain core to investment management, but convergence is unfolding as vendors embed asset-level analytics within the fundraising stack. EFront’s end-to-end platform, overseeing USD 567 billion in assets, illustrates buyer preference for unified data flows.

Property accounting has become commoditized, bundled as a standard feature rather than a standalone buy decision. Leasing management, boosted by AI chatbots that reduce vacancy and automate renewals, is experiencing renewed momentum; VTS’s partnership with Salesforce extends tenant engagement into customer-relationship systems. Niche modules covering construction, facilities, and energy management utilize IoT sensors to drive preventive maintenance and reduce carbon emissions. Cross-module interoperability differentiates leading platforms, allowing asset managers to toggle between portfolio-wide financial ratios and site-level occupancy metrics without needing to export data to Excel.

By End User: Industrial Real Estate Software Adoption Surges Amid Logistics Expansion

Commercial real estate generated 37.26% of 2024 demand due to the complexity of office and retail portfolios. Yet, industrial real estate, benefiting from e-commerce logistics, is forecast to grow at a rate of 12.51% annually. Its share of the real estate investment software market size is on track to hit USD 2.00 billion by 2030. Operators deploy warehouse management systems that stream IoT sensor data on throughput, which is then fed directly into investment dashboards. Strong net operating income growth in logistics assets, highlighted by Goldman Sachs, attracts capital and spurs software purchases.

Residential segments, especially single-family rental funds, face the FinCEN reporting requirement that demands automated beneficial-ownership reporting, cementing the need for compliance modules.[2]Financial Crimes Enforcement Network, “FinCEN Issues Final Rule to Establish Reporting Requirements for Certain Transfers of Real Estate,” FINCEN.GOV Senior housing, student housing, and data center owners require specialized asset-class features such as resident care metrics or server uptime analytics. Vendors are therefore launching vertical editions that bundle templates, reporting fields, and peer benchmarks specific to each property type.

By Organization Size: SMEs Embrace SaaS as Subscription Models Lower Entry Barriers

Large enterprises captured 60.37% of 2024 revenue by funding multi-module implementations that cost up to USD 2 million and span two years. Yet small and medium enterprises are expanding at 12.32% through 2030 as vendors price subscriptions at USD 50-USD 150 per user per month, reducing capex to near zero. Freemium tiers enable small syndicators to manage a limited number of assets before upgrading to AI-driven underwriting or investor portals.

Implementation timelines for SMEs now average six weeks, compared with months for legacy systems. EliseAI’s conversational platform, active across 70% of the top U.S. rental operators, exemplifies scalability from startups to large portfolios. Budget constraints persist, but land-and-expand sales models convert basic tenants to premium tiers as assets scale. As a result, SMEs represent the fastest-growing cohort in the real estate investment software market.

Geography Analysis

North America generated 44.81% of the 2024 revenue, driven by the depth of institutional capital and complex compliance mandates. The FinCEN electronic reporting rule compels automated know-your-customer workflows, while the Securities and Exchange Commission climate proposal signals standardized greenhouse-gas reporting. Canada’s pension plans, managing CAD 2 trillion (USD 1.5 trillion), deploy multi-asset dashboards to monitor cross-border holdings. Mexico’s nearshoring boom lifts demand for industrial warehouse management and lease modules. Enterprise adoption remains concentrated among Yardi, RealPage, and MRI, but private-equity consolidation is tightening competition.

Asia Pacific is projected to record a 13.16% CAGR through 2030. China is digitizing state-owned portfolios through super-apps like Beike, which integrate brokerage, financing, and valuation features. India’s RERA enforcement mandates escrow transparency and quarterly progress updates, prompting the integration of cloud dashboards into developer workflows. Japan’s Society 5.0 integrates property data with smart-city platforms, while Australia’s pension funds, overseeing AUD 3.5 trillion (USD 2.3 trillion), require ESG analytics across infrastructure and real estate.[3]Australian Prudential Regulation Authority, “Superannuation Statistics,” APRA.GOV.AU Growing emphasis on green building standards in South Korea and aging demographics in Japan further diversify demand.

Europe’s outlook hinges on the Corporate Sustainability Reporting Directive requiring audited sustainability statements from 2025. The EU Taxonomy sets energy performance thresholds, embedding carbon calculators into deal underwriting. Germany, the United Kingdom, France, Italy, and Spain dominate spending; Allianz and Deutsche Bank’s real estate arms are early adopters of ESG modules. Blockchain land registries in the United Arab Emirates and Saudi Arabia foster interest in tokenization platforms. Africa remains small but viable: mobile-first landlord apps penetrate Kenya and Nigeria’s affordable housing segments, hinting at future growth pathways across the real estate investment software market.

Competitive Landscape

The real estate investment software market hosts a moderate concentration of entrenched vendors complemented by a long tail of innovators. Yardi, RealPage, MRI Software, and Altus Group have grown through product breadth and decades-long client relationships. Thoma Bravo’s 2024 take-private of RealPage enabled larger research budgets and faster AI rollouts. Altus Group’s USD 249.5 million purchase of Reonomy added ownership intelligence to its valuation suite. These acquisitions illustrate the race to assemble end-to-end platforms that eliminate clients’ need for point solutions.

Smaller specialists gain traction by focusing on unmet niches. EliseAI automates leasing conversations, slashing response times and vacancy loss for both large and small operators. VTS enhances the tenant experience by integrating its systems with Salesforce, thereby bridging occupancy analytics and customer relationships. Competitive advantage is tilting toward vendors that leverage data network effects. Platforms aggregating transaction histories, rent rolls, and energy consumption across thousands of assets produce benchmarks that smaller rivals cannot replicate.

API openness and regulatory compliance increasingly define buyer criteria. Only 30% of property-management systems met RESO Web API standards by 2024, keeping integration costs high for laggards. Vendors that natively automate FinCEN filings or CSRD disclosures shield users from legal risk and cut reporting labor. Private-equity funding accelerates consolidation, but continued innovation around AI valuation, IoT data ingestion, and tokenization ensures that challenger firms will keep emerging, preserving a dynamic competitive field.

Real Estate Investment Software Industry Leaders

Altus Group Limited

Yardi Systems Inc.

MRI Software LLC

RealPage Inc.

Juniper Square Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Real estate and construction have emerged as pivotal players in the post-COVID-19 economic recovery, as underscored by the Integrated Industry-Level Production Account from the U.S. Bureau of Economic Analysis and the Bureau of Labor Statistics.

- January 2025: Trane Technologies completed the acquisition of BrainBox AI, strengthening its smart-building energy-optimization suite.

- January 2025: The White House announced investments of over USD 8.9 trillion, both domestic and foreign, highlighting major commitments to real estate, infrastructure, and smart building technologies.

- October 2024: Altus Group acquired Reonomy for USD 249.5 million, integrating property-ownership intelligence into valuation analytics.

Global Real Estate Investment Software Market Report Scope

| Cloud-Based |

| On-Premise |

| Property Accounting |

| Asset Management |

| Leasing Management |

| Investment Management |

| Others |

| Commercial Real Estate |

| Residential Real Estate |

| Industrial Real Estate |

| Special Purpose/REITs |

| Large Enterprises |

| Small and Medium Enterprises |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Kenya | |

| Rest of Africa |

| By Deployment | Cloud-Based | |

| On-Premise | ||

| By Application | Property Accounting | |

| Asset Management | ||

| Leasing Management | ||

| Investment Management | ||

| Others | ||

| By End-User | Commercial Real Estate | |

| Residential Real Estate | ||

| Industrial Real Estate | ||

| Special Purpose/REITs | ||

| By Organization Size | Large Enterprises | |

| Small and Medium Enterprises | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the real estate investment software market in 2025?

The real estate investment software market size is USD 5.60 billion in 2025 with an 11.84% CAGR forecast to 2030.

Which deployment model is growing fastest?

Cloud solutions are advancing at a 13.51% CAGR, reflecting cost advantages and automatic regulatory updates.

Why is Asia Pacific a high-growth region?

China’s portfolio digitization, India’s RERA enforcement, and Japan’s smart-city initiatives drive a 13.16% CAGR through 2030.

What is the main restraint on software adoption?

High switching costs from legacy Excel models delay migration and reduce near-term uptake.

Which application segment is expanding most quickly?

Asset management software is projected to grow at a 13.26% CAGR as investors demand real-time performance dashboards.

How are vendors differentiating?

Leading platforms integrate AI underwriting, ESG reporting, and open APIs that reduce custom integration costs.

Page last updated on: