Procurement Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 10.74 Billion |

| Market Size (2031) | USD 17.11 Billion |

| Growth Rate (2026 - 2031) | 9.76% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Procurement Software Market Analysis by Mordor Intelligence

The procurement software market size is projected to expand from USD 9.81 billion in 2025 and USD 10.74 billion in 2026 to USD 17.11 billion by 2031, registering a CAGR of 9.76% between 2026 to 2031. Demand pivots around autonomous workflows that combine cloud-native architectures, generative-AI copilots, and tokenized cross-border payment rails, each lowering cost-to-serve while accelerating decision cycles. Cloud deployment dominates because elastic SaaS platforms slash data-center overhead, give real-time spend visibility, and update features for every tenant in near-real time. End-user uptake broadens as healthcare group purchasing organizations link sourcing decisions to value-based reimbursement, while SMEs gain entry through freemium tiers and embedded finance that convert capital expense into operating expense. Regionally, North American maturity anchors current revenue, yet Asia Pacific outpaces on growth as public e-procurement mandates and leapfrog cloud adoption converge.

Key Report Takeaways

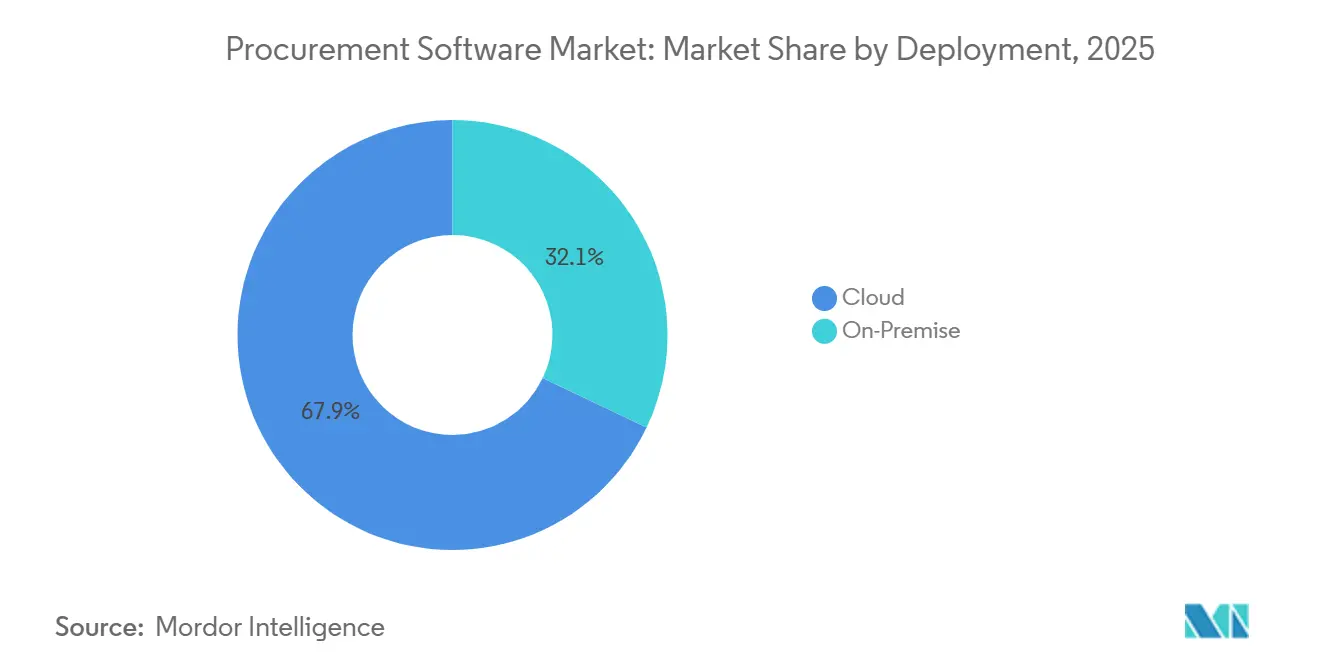

- By deployment, cloud captured 67.92% of the procurement software market share in 2025 and remains the fastest-growing model, with a 9.81% CAGR through 2031.

- By end-user industry, manufacturing led with a 21.63% revenue share in 2025, while healthcare recorded the highest projected CAGR of 9.79% through 2031.

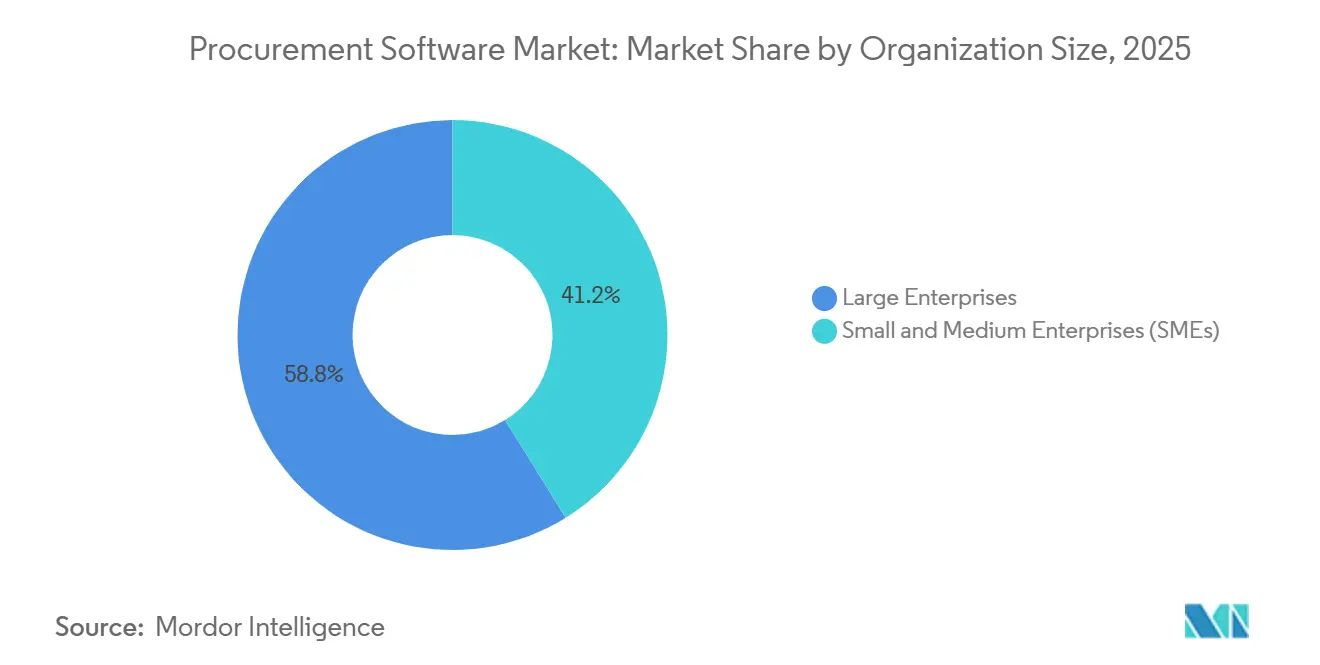

- By organization size, large enterprises accounted for 58.82% of 2025 spending, whereas SMEs are set to expand at a 9.77% CAGR during 2026-2031.

- By application module, procure-to-pay held 62.81% share in 2025, and contract lifecycle management is advancing at 9.01% CAGR through 2031.

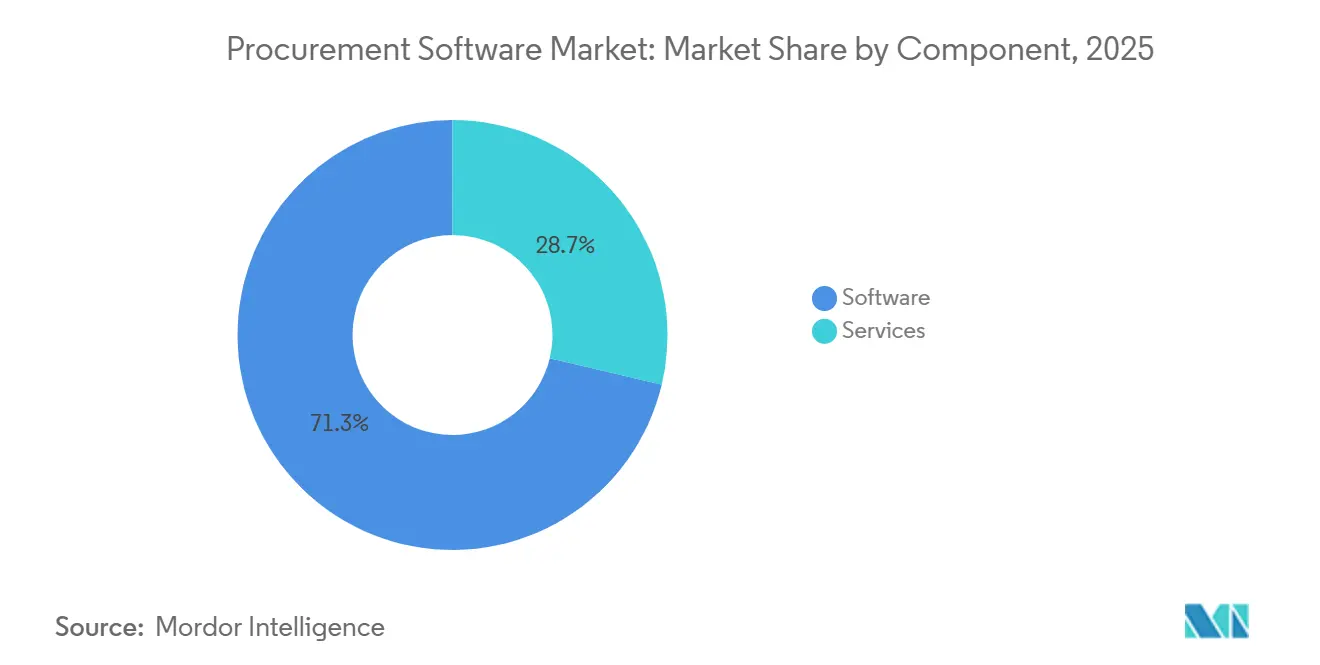

- By component, software licenses represented 71.28% of 2025 revenue, although services post the strongest outlook with a 9.83% CAGR to 2031.

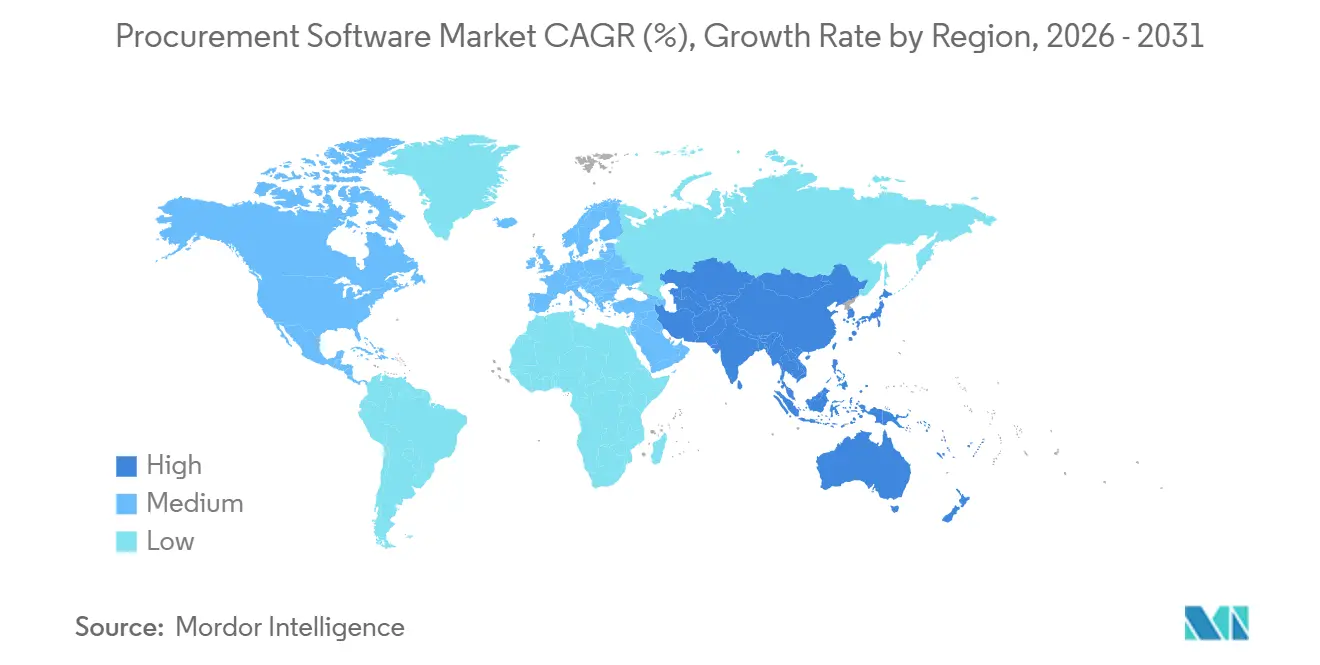

- By geography, North America contributed 33.64% of 2025 revenue, yet Asia Pacific exhibits the quickest trajectory with a 9.87% CAGR over the forecast window.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Procurement Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Automating End-to-End Procurement Workflows | +2.5% | Global, strongest in North America and Western Europe | Medium term (2-4 years) |

| Seamless ERP and e-Procurement Integration | +2.0% | Global, concentrated where SAP, Oracle, and Microsoft Dynamics prevail | Short term (≤ 2 years) |

| Migration to Cloud-Native Platforms | +1.8% | North America and Europe core, rapid uptake in Asia Pacific | Medium term (2-4 years) |

| Generative AI Copilots Accelerating Sourcing | +1.5% | Early adopters in North America and Europe, expanding to Asia Pacific | Long term (≥ 4 years) |

| Tokenized B2B Payment Rails | +0.8% | Global pilots in Asia Pacific and Middle East | Long term (≥ 4 years) |

| Green Public Procurement and Carbon APIs | +0.7% | Europe first, spreading to North America and Asia Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Automating End-to-End Procurement Workflows

Organizations collapse requisition, approval, supplier discovery, contracting, and invoicing into a single platform that removes manual handoffs and prunes cycle time by up to half. Robotic process automation now drafts the bulk of purchase orders, reallocating human effort toward supplier relationship management. The resulting operating-expense reduction approaches 20% in industries exposed to volatile input prices, giving early adopters headroom to negotiate volume discounts that shield margins during commodity swings. Real-time dashboards redirect budgets within hours when disruptions hit, a capability that proved decisive during the 2025 semiconductor shortage. Firms that achieve this level of automation also report materially faster supplier onboarding, strengthening resiliency against single-source risk.

Seamless ERP and e-Procurement Integration

Bidirectional data flow between core ERP systems and procurement suites eliminates duplicate master records, curbing invoice discrepancies and shortening monthly close cycles. Pre-built adapters from leading vendors now synchronize contract terms, chart-of-accounts codes, and tax data without custom code, shrinking integration risk for multisuite enterprises. Middleware further federates data for conglomerates running multiple ERP instances, enabling unified spend analytics that surface maverick spend and unlock volume-discount leverage. Firms completing clean integrations often cite double-digit productivity gains across procurement staff because requisitioners transact from within the familiar ERP interface. This integration stickiness, in turn, raises switching costs and underpins vendor renewal rates.

Migration to Cloud-Native Platforms

Elastic compute allows enterprises to scale during quarter-end budget flushes without idle infrastructure during lull periods, cutting IT overhead by more than one-third versus on-premise estates. Vendors manage patches, disaster recovery, and compliance certifications such as SOC 2 and ISO 27001, lifting a heavy administrative burden from buyers. Multi-tenant architectures deliver simultaneous AI-model updates, ensuring that every tenant benefits from continual learning that sharpens fraud detection and spend classification. Edge-cloud hybrids emerge in regulated sectors to meet residency mandates, processing transactions locally while syncing sanitized analytics to central clouds. Asia Pacific leapfrogs legacy stacks entirely, with public-sector e-procurement mandates giving local firms the impetus to adopt cloud from day one.

Generative AI Copilots Accelerating Autonomous Sourcing

Conversational assistants draft RFPs, parse supplier proposals, and recommend award scenarios built on total-cost models that weigh delivery risk, quality scores, and carbon intensity. Buyers can ask natural-language questions-“Which suppliers missed lead times last quarter?”-and receive instant visualizations without SQL.[1]“Microsoft Copilot Studio,” Microsoft, microsoft.com Early adopters automate low-value purchases altogether, escalate only exceptions above materiality thresholds, and report a nearly one-third compression of the sourcing cycle. Contract compliance improves when AI flags non-standard clauses prior to execution, avoiding downstream disputes. Uptake spreads fastest where data hygiene is strong, underscoring the interdependence between cleansing legacy spend data and realizing AI value.

Restraint Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy-System Integration Complexity | -1.2% | Global, acute where ERP instances are heavily customized | Short term (≤ 2 years) |

| Data-Security and Regulatory Compliance | -1.0% | Europe, North America, spreading globally | Medium term (2-4 years) |

| Algorithmic Bias in AI Spend Analytics | -0.5% | North America and Europe | Medium term (2-4 years) |

| Disruptive FinTech Entrants and Price Pressure | -0.6% | Global, prominent on cross-border payment corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Legacy-System Integration Complexity

Enterprises with aging, highly customized ERP codebases require months of mapping, testing, and remediation before procurement suites can go live. Custom extensions in legacy SAP or Oracle environments create brittle dependencies that break during upgrades, inflating budgets and delaying ROI. Data-quality problems such as duplicate supplier records further hamper synchronization, often forcing businesses to postpone platform rollouts until parallel ERP modernization concludes. Vendors now offer pre-certified connectors that shift part of the integration risk onto themselves, yet highly tailored deployments still overrun initial schedules. These hurdles make integration complexity the single most cited reason for stalled digital-procurement programs.

Data-Security and Regulatory Compliance Concerns

Procurement platforms process personally identifiable information and sensitive supplier pricing, exposing buyers to stringent breach-notification and privacy-law regimes. The European Union’s NIS2 Directive compels critical-infrastructure operators to perform supply-chain cyber-risk assessments, while GDPR Article 28 mandates explicit processor controls.[2]“NIS2 Directive,” European Commission, europa.eu U.S. state privacy statutes further fragment compliance obligations, raising operating costs for vendors lacking robust governance frameworks. Enterprises in banking and defense demand private-cloud or on-premise instances to satisfy residency mandates, slowing SaaS adoption and complicating feature-parity roadmaps. Absent proven zero-trust architectures and third-party penetration tests, many mid-market platforms are excluded from regulated-industry tenders.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment: Cloud Dominance Reinforced by AI Workloads

Cloud deployment captured 67.92% of the procurement software market share in 2025, reflecting enterprise preference for elastic capacity that absorbs traffic spikes without capital expense. The segment’s 9.81% CAGR underscores how multi-tenant SaaS platforms spread AI model-training costs across thousands of customers, making autonomous invoice matching and predictive risk scoring financially viable for mid-size firms. On-premise installations persist in defense and banking, where data-sovereignty rules limit external hosting, but hybrid architectures increasingly bridge local transaction processing with centralized analytics. Edge computing also gains favor among retailers operating in connectivity-challenged regions, lowering latency and ensuring continuous transaction flow during network outages.

The procurement software market benefits when cloud vendors roll updates in hours rather than quarters, enabling rapid response to regulatory changes such as electronic-invoice mandates or carbon-reporting rules. Conversely, on-premise buyers face six-to-twelve-month upgrade cycles that delay access to new functionality and inflate total cost of ownership. Even regulated entities are piloting shielded SaaS models that encrypt sensitive fields yet retain multi-tenant economics, signaling a gradual erosion of the long-standing on-premise stronghold. Taken together, these trends reinforce cloud’s leadership position for the foreseeable horizon.

By End-User Industry: Healthcare Outpaces Manufacturing

Manufacturing led 2025 revenue with 21.63% share, underpinned by complex bill-of-materials management and just-in-time inventory strategies that reward tight supplier coordination. Yet healthcare is the fastest riser, tracking a 9.79% CAGR as hospitals tie procurement savings to value-based reimbursement metrics, making every percentage point of supply cost a bottom-line imperative. Procedure-level integration with electronic health records allows clinicians to benchmark implant utilization and negotiate evidence-based pricing, cutting orthopedic spend by double digits. Group-purchasing organizations amplify buying power and help hospitals adjudicate supplier performance on infection-control or readmission measures.

Elsewhere, retail and e-commerce platforms automate tariff calculations and customs documentation to mitigate border friction, while BFSI institutions deploy software to meet third-party risk obligations under global capital rules. Government agencies adopt e-procurement to meet transparency and accessibility mandates, and IT-telecom firms use spend analytics to tame SaaS subscription sprawl.[3]“eForms Regulation,” European Commission Single Market, ec.europa.eu The ability to configure sector-specific workflows-such as subcontractor compliance checklists for construction-positions vertical SaaS vendors to seize whitespace overlooked by horizontal suites. Consequently, the procurement software market broadens not only by enterprise size but also by depth of industry fit.

By Organization Size: SMEs Close the Adoption Gap

Large enterprises retained 58.82% spending share in 2025, benefiting from the resources to integrate procurement platforms across dozens of legal entities and reconcile data from heterogeneous ERP estates. Nonetheless, SMEs exhibit a 9.77% CAGR because freemium tiers and usage-based pricing swap hefty upfront licenses for manageable operating fees. Embedded finance enables suppliers to receive early payment while buyers stretch terms, effectively bundling working-capital solutions into the procurement workflow and making software adoption accretive to cash flow.

The procurement software market gains resilience when SME onboarding accelerates: a 50-employee manufacturer can now deploy source-to-pay in weeks, not months, using preconfigured templates that include tax and compliance rules. Meanwhile, large multinationals leverage master-data governance and consolidated analytics to unlock cross-entity volume discounts worth several percentage points of addressable spend. Both tiers increasingly demand outcome-based services, aligning vendor compensation with measured savings or compliance metrics.

By Application Module: Contract Management Gains Momentum

Procure-to-pay held 62.81% of 2025 application revenue because automated three-way matching and dynamic-discount programs shaved eight to twelve days off days payable outstanding, directly improving working-capital ratios. Contract lifecycle management, however, posts the fastest 9.01% CAGR as AI clause extraction, obligation tracking, and e-signature tie-ins shrink execution cycles from weeks to days and reduce post-award leakage. E-sourcing modules further compress supplier pricing through reverse auctions, while spend-analysis engines classify nearly every transaction against standardized taxonomies, surfacing category-level saving opportunities.

Supplier relationship management adds qualitative metrics such as on-time delivery, quality defects, and ESG compliance to scorecards that feed future award decisions. Catalog management rounds out the suite by synchronizing punchout links to supplier sites, ensuring requisitioners always see live availability and negotiated pricing, thereby curbing maverick spend. As enterprises mature, they migrate from standalone modules to integrated suites that share master data and analytics, reinforcing network effects within the procurement software market.

By Component: Services Gain Share Through Outcome-Based Pricing

Software licenses accounted for 71.28% of 2025 revenue, reflecting entrenched perpetual-license models among large enterprises seeking budget predictability. Services, though, expand at a 9.83% CAGR as buyers outsource implementation, data migration, and even transactional procurement tasks under managed-service contracts that guarantee cost-saving outcomes. System integrators bundle fixed-price go-lives with change-management and training programs, cutting deployment timelines nearly in half for standardized rollouts.

Managed procurement operations based in cost-effective delivery centers, lower run-rate expenses by up to one-third and free internal staff for strategic sourcing activity. Subscription models that bundle license, hosting, and support into a single annual charge now account for the majority of new bookings, shifting upgrade risk from buyer to vendor. This shift stabilizes vendor revenue streams and accelerates innovation cycles, providing a virtuous loop that sustains growth in the procurement software market.

Geography Analysis

North America generated 33.64% of 2025 revenue, thanks to mature ERP ecosystems, supplier-diversity mandates under Executive Order 14091, and early adoption of generative-AI-enabled procurement copilots. Federal transparency requirements that demand machine-readable contract data drive platform penetration across civilian agencies, while Canadian entities migrate to comply with digital-accessibility rules. Mexico’s export-focused manufacturers embed software to automate United States-Mexico-Canada Agreement origin certifications, underscoring how trade pacts can catalyze digital procurement.

Asia Pacific advances at a 9.87% CAGR, the fastest worldwide, propelled by government portals such as India’s GeM and China’s centralized public-procurement reforms that oblige electronic sourcing above specified thresholds. Japan allocates substantial funds to API-ready government systems, and Australia applies modern slavery legislation that forces businesses to audit supply chains for forced-labor risk, bringing procurement platforms to the front line of ESG compliance. Companies leapfrog legacy infrastructure entirely, opting for cloud-native suites that offer localized language packs, tax rules, and payment integrations from day one.

Europe balances North American maturity with Asia Pacific’s growth velocity. The European Union’s forthcoming eForms mandates standardize contract notices, cutting cross-border tender costs and favoring platforms with built-in schema support. Green-deal initiatives require lifecycle carbon accounting, compelling software to ingest emissions data and present cradle-to-gate footprints during bid evaluation. Germany’s supply-chain due-diligence act extends human-rights audits to first-tier suppliers, and similar legislation is debated across the bloc, reinforcing compliance-driven adoption. South America and Middle East markets remain nascent but gather momentum as Brazil and Saudi Arabia roll out national e-procurement portals, while much of Africa still contends with connectivity gaps that delay widescale deployment.

Competitive Landscape

The sector is moderately concentrated; the five largest providers-SAP, Coupa, Oracle, Jaggaer, and Ivalua-capture a high share of global revenue, while more than two hundred regional or vertical specialists divide the remainder. Incumbents leverage deep ERP integrations and multi-module breadth to entrench existing customers, yet they face declining price leverage as FinTech entrants embed procure-to-pay directly into banking rails at materially lower transaction fees. Vertical specialization intensifies; for example, healthcare-focused suites integrate clinical utilization data, whereas construction platforms automate subcontractor safety compliance.

Generative-AI copilots and autonomous agents represent the current innovation frontier, and vendors race to patent graph-based supplier-risk models or natural-language query engines that democratize analytics. Blockchain-native challengers pilot tokenized B2B payment rails, settling cross-border invoices in under forty-eight hours at spreads well below SWIFT, forcing traditional suites to consider distributed-ledger add-ons or partnership routes. Security and compliance become hygiene factors rather than differentiators as ISO 27001 and SOC 2 Type II attestations appear in nearly every enterprise request for proposal.

Strategic moves over the past eighteen months illustrate defensive and offensive plays, SAP embedded its Joule AI copilot into Ariba, Oracle acquired Determine to tighten Fusion lock-in, Coupa earmarked significant investment for autonomous procurement agents, Workday added supply-chain finance to capture payment spread economics, and Jaggaer partnered with a global bank to test blockchain settlement. While incumbent market share remains stable for now, the procurement software market could tip if next-generation platforms prove that lower cost of ownership and faster innovation outweigh legacy integration inertia.

Procurement Software Industry Leaders

SAP SE

Coupa Software Inc.

Oracle Corporation

Jaggaer, LLC

Ivalua Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: SAP launched Joule AI copilot within Ariba, enabling natural-language RFP generation and award recommendations.

- January 2026: Coupa committed USD 150 million to autonomous procurement agents that execute low-value purchases without human touch.

- December 2025: Oracle acquired Determine for USD 1.2 billion, folding contract management into the Fusion ERP suite.

- November 2025: Workday introduced embedded supply-chain finance, offering suppliers 48-hour payment while buyers extend terms to 90 days.

Global Procurement Software Market Report Scope

Procurement software is a program that includes features such as executing the online ordering process, generating purchase orders, matching invoices to the materials received, and electronically paying all bills. It helps in increasing productivity, reduces external costs, spending controls, and process efficiencies, and generates electronic requests for proposal (e-RFP), electronic requests for information (e-RFI), and electronic requests for quotation (e-RFQ). Procurement software, along with e-procurement, helps in reducing the complete procurement life cycle.

The Procurement Software Market Report is Segmented by Deployment (Cloud and On-Premise), End-User Industry (Retail, Manufacturing, Transportation and Logistics, Healthcare, BFSI, IT and Telecom, Government and Public Sector, and Other End-User Industries), Organization Size (Large Enterprises and SMEs), Application Module (e-Sourcing, Contract Management, Spend Analysis, Procure-to-Pay, SRM, and Catalog Management), Component (Software and Services), and Geography. The Market Forecasts are Provided in Value (USD).

| Cloud |

| On-Premise |

| Retail |

| Manufacturing |

| Transportation and Logistics |

| Healthcare |

| BFSI |

| IT and Telecom |

| Government and Public Sector |

| Other End-User Industries |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| e-Sourcing |

| Contract Management |

| Spend Analysis and Analytics |

| Procure-to-Pay |

| Supplier Relationship Management |

| Catalog Management |

| Software |

| Services |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Deployment | Cloud | |

| On-Premise | ||

| By End-User Industry | Retail | |

| Manufacturing | ||

| Transportation and Logistics | ||

| Healthcare | ||

| BFSI | ||

| IT and Telecom | ||

| Government and Public Sector | ||

| Other End-User Industries | ||

| By Organization Size | Large Enterprises | |

| Small and Medium Enterprises (SMEs) | ||

| By Application Module | e-Sourcing | |

| Contract Management | ||

| Spend Analysis and Analytics | ||

| Procure-to-Pay | ||

| Supplier Relationship Management | ||

| Catalog Management | ||

| By Component | Software | |

| Services | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected global procurement software market size by 2031?

The category is expected to reach USD 17.11 billion by 2031.

Which deployment approach is expanding fastest and what drives that growth?

Cloud-based suites grow at a 9.81% CAGR because elastic SaaS cuts ownership costs and delivers real-time AI updates.

How quickly are small and medium enterprises adopting platforms?

SME spending is advancing at a 9.77% CAGR as freemium tiers and embedded finance remove high upfront fees.

What benefits do generative-AI copilots bring to sourcing teams?

Copilots auto-draft RFPs, flag risky clauses, and reduce sourcing cycle time by roughly one-third.

Which geographic region shows the highest growth momentum through 2031?

Asia Pacific leads with a 9.87% CAGR, propelled by government e-procurement mandates and leapfrog cloud adoption.

Page last updated on: