Childcare Management Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 267.15 Million |

| Market Size (2031) | USD 405.42 Million |

| Growth Rate (2025 - 2030) | 8.70% CAGR |

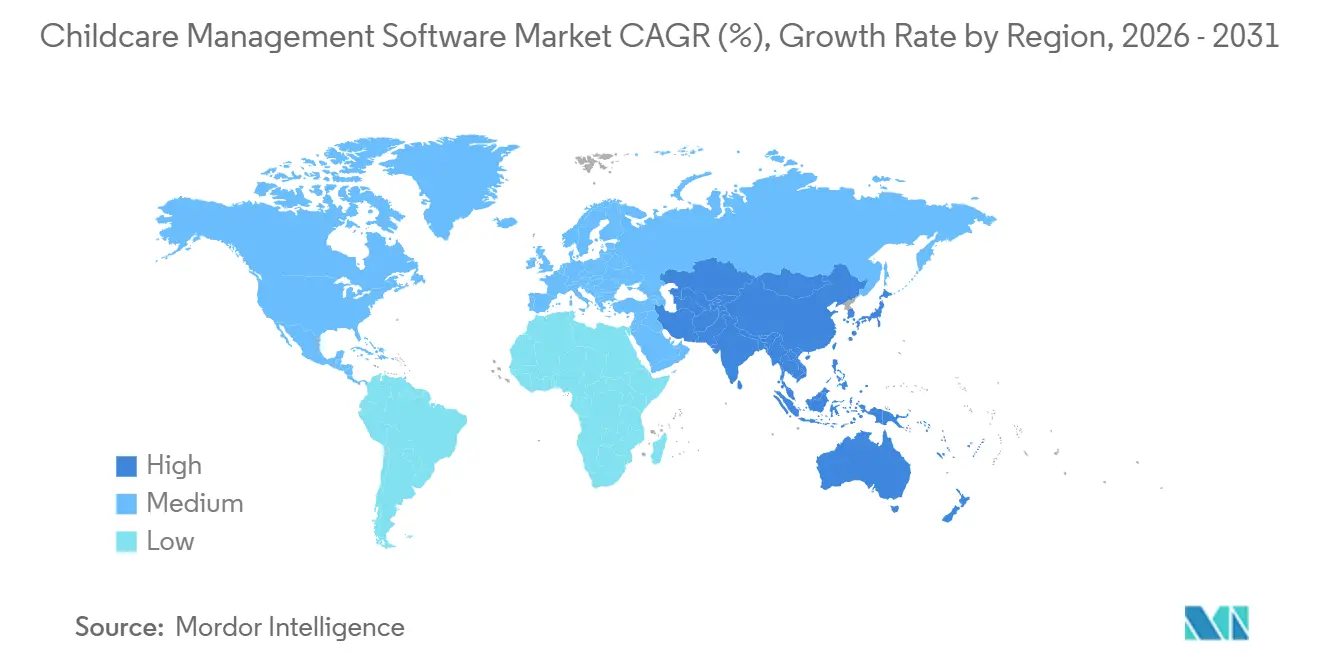

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

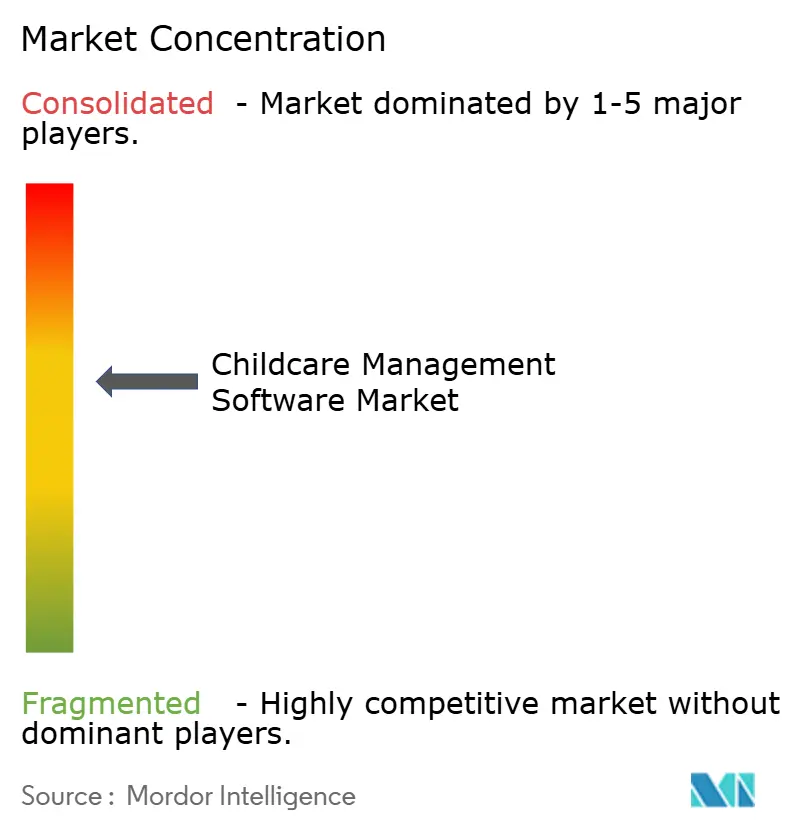

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Childcare Management Software Market Analysis by Mordor Intelligence

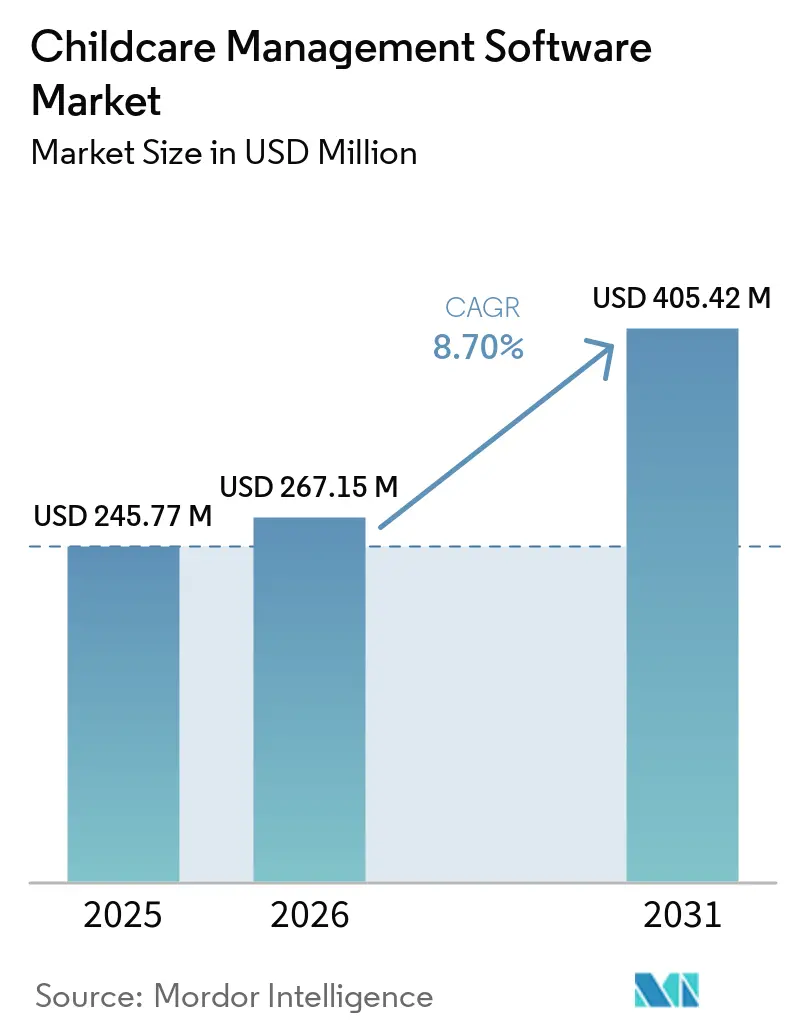

The childcare management software market size is expected to be USD 245.77 million in 2025, USD 267.15 million in 2026, and reach USD 405.42 million by 2031, growing at a CAGR of 8.70% from 2026 to 2031. Steady migration from paper files to cloud platforms is reshaping daily operations, as centers automate attendance, billing, and parent engagement. United States and state-level rules that return subsidy calculations to real-time attendance reporting are accelerating software purchases, while similar mandates in Australia and India reinforce the global scope of digital compliance. Large multi-site chains are standardizing technology stacks to capture data synergies and reduce vendor overlap, and smaller operators adopt subscription models that avoid capital outlays. Embedded payment rails inside applications are opening complementary revenue pools, prompting vendors to bundle tuition financing, staff earned-wage access, and card processing into a single interface.

Key Report Takeaways

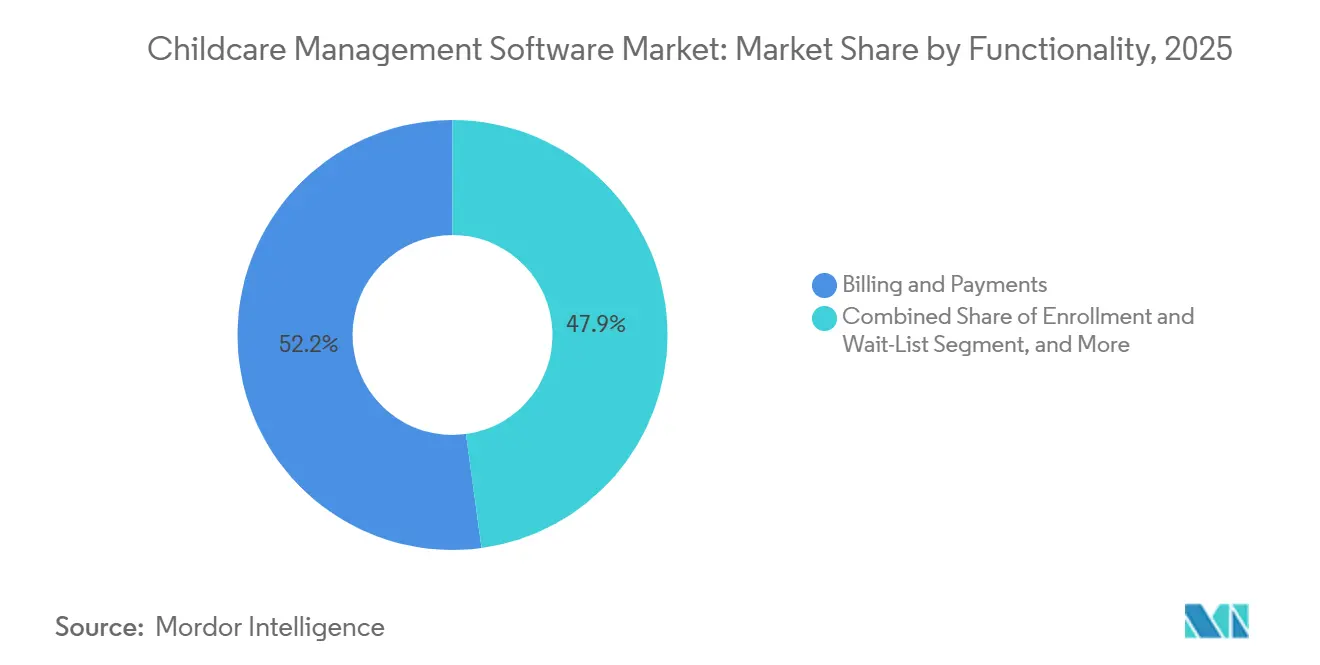

- By functionality, billing and payments led with 52.15% of the childcare management software market share in 2025, whereas embedded fintech modules are forecast to advance at an annual 7.85% CAGR through 2031.

- By deployment, cloud solutions captured 36.45% of the childcare management software market size in 2025, while the same model is projected to expand at an 8.87% CAGR to 2031.

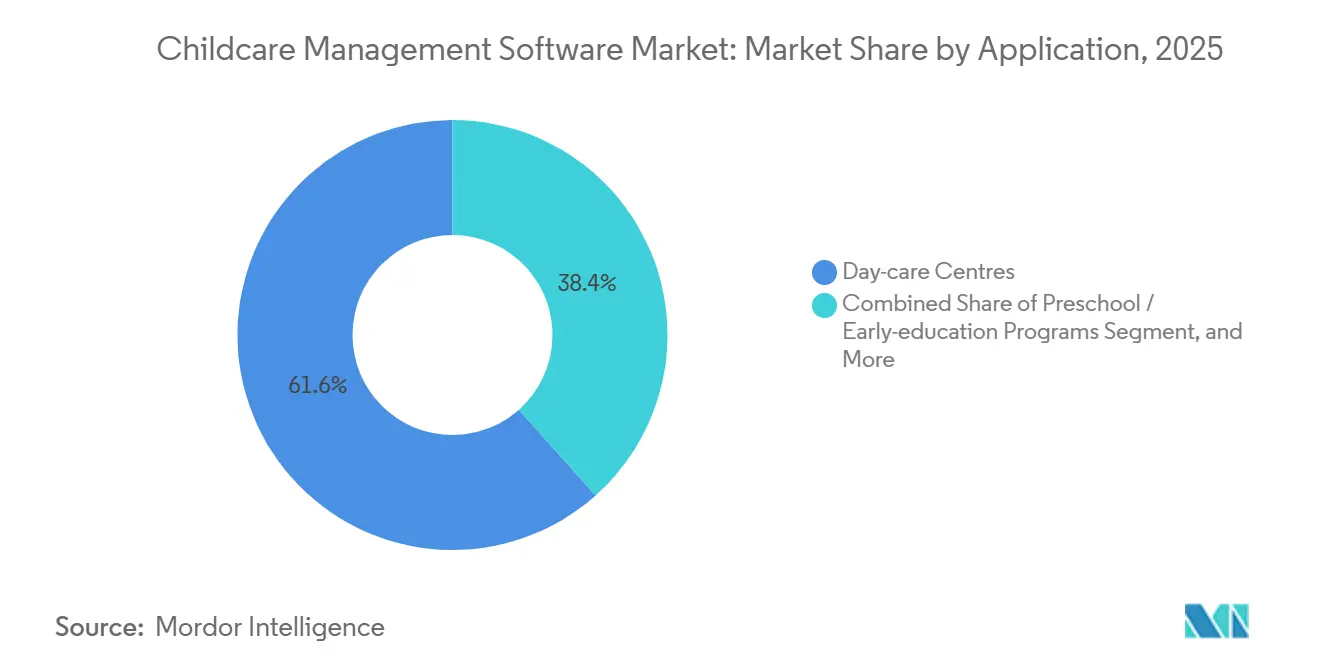

- By application, day-care centers held 66.67% revenue share of the childcare management software market in 2025, whereas home-based providers are set to grow at 7.27% CAGR through 2031.

- By end-user, multi-location operators commanded 58.75% of the childcare management software market size in 2025, and employer-sponsored programs represent the fastest trajectory at an 8.2% CAGR to 2031.

- By geography, North America accounted for 40.44% of the childcare management software market in 2025, Asia-Pacific is expected to record a leading 9.08% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Childcare Management Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Digitization and Automation Needs in Childcare Centres | +2.1% | North America, Europe, Asia‑Pacific | Medium term (2–4 years) |

| Growing Dual‑Income Households Elevating Administrative Efficiency Demands | +1.8% | Urban regions worldwide | Long term (≥ 4 years) |

| Government Mandates for Digital Attendance and Subsidy Compliance | +2.3% | United States, Australia, India | Short term (≤ 2 years) |

| Cloud Affordability Unlocking SME Adoption | +1.5% | Global | Medium term (2–4 years) |

| Embedded Fintech Revenue Streams Within Platforms | +0.7% | North America, Europe, Asia‑Pacific | Long term (≥ 4 years) |

| Private‑Equity Roll‑Ups Standardizing Software Stacks Across Centres | +0.3% | North America, Europe | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising Digitization and Automation Needs in Childcare Centres

Federal and state regulations now specify electronic record keeping, pushing centers to retire clipboards in favor of cloud dashboards that track check-ins, ratio compliance, and curriculum milestones. Updated United States privacy guidance extends oversight to biometric identifiers, which in turn obliges platforms to encrypt facial or fingerprint data and document parental consent.[1]Federal Trade Commission, “COPPA Rule Amendments: Final Rule,” ftc.gov Minnesota’s 2026 electronic attendance rule strengthens this momentum, adding thousands of small providers to the digital fold. Automated billing, enrollment, and meal counting reduce paperwork, freeing staff for instructional duties. India’s nationwide Poshan Tracker illustrates the scale effect: a single platform synchronizes data from 1.4 million centers and 89.5 million children, proving that cloud tools can handle extreme transaction volumes while supporting multilingual interfaces.

Growing Dual-Income Households Elevating Administrative Efficiency Demands

Dual-income families allocate higher budgets to quality childcare and expect smartphone convenience. United States labor statistics show both parents employed in 66% of married-couple households, a configuration that values late-pickup options and contactless tuition payment. Australia reports similar patterns as the Cheaper Child Care reforms widen subsidy access, raising enrollment demand and enlarging waitlists. Mobile apps that push real-time photos and meal notes satisfy parent expectations for transparency, while automated reminders cut missed invoices. Corporate-backed centers add further momentum, with surveys indicating that more than 80% of employees rank childcare support among top workplace benefits, nudging employers toward software that integrates payroll deductions and badge access.

Government Mandates for Digital Attendance and Subsidy Compliance

Public authorities now tie reimbursement to time-stamped attendance rather than roster enrollment. The United States Department of Health and Human Services reinstated attendance-based calculations in January 2026, compelling operators to capture daily data feeds for subsidy portals. Similar electronic requirements apply to Australia’s Child Care Subsidy, which disbursed AUD 20.9 billion (USD 13.8 billion) in 2024-2025 and conditions payment on timely digital submissions. Mandatory audit trails elevate minimum product features: geofenced check-in, photo ID verification, and immutable logs. The predictable cash-flow benefit encourages even hesitant centers to onboard technology swiftly.

Cloud Affordability Unlocking SME Adoption

Subscription pricing removes hardware outlays, and automatic updates ease the need for onsite IT. Many centers operate on slim margins, so the option to cancel monthly contracts reduces perceived risk. Cloud dashboards consolidate multi-site analytics, allowing owners to track occupancy, aging receivables, and staff certifications from a single screen. As connectivity improves in secondary cities, mobile-first interfaces sidestep the desktop entirely, aligning with caregiver shift patterns and after-hours parent queries.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data‑Privacy and Cyber‑Security Compliance Costs | −1.2% | United States, Europe | Short term (≤ 2 years) |

| High Switching Costs and Staff Tech‑Adoption Barriers | −0.9% | Global | Medium term (2–4 years) |

| Fragmented State‑Level Regulations Complicating Localization | −0.5% | United States, Europe | Long term (≥ 4 years) |

| Freemium App Saturation Driving Down Average Revenue Per User | −0.4% | North America, Europe | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Data-Privacy and Cyber-Security Compliance Costs

Child-centric data is acutely sensitive, attracting tight oversight under rules such as COPPA in the United States and GDPR in Europe. Recent amendments broaden biometric scopes and impose annual audit obligations, increasing outlays for encryption, penetration tests, and breach insurance.[2]United States Department of Education, “FERPA Guidance for Early Childhood Programs,” ed.gov Smaller operators often lack compliance officers, so they either pay premium tiers for turnkey protection or delay adoption, slowing overall platform penetration.

High Switching Costs and Staff Tech-Adoption Barriers

Paper attendance books remain familiar and inexpensive, making the leap to cloud dashboards a perceived risk. Staff turnover above 30% forces repeated training cycles, draining limited professional-development budgets. Data migration presents further headaches when historic invoices or immunization records live in incompatible formats. Vendors that bundle white-glove onboarding and multilingual tutorials soften these frictions but elevate customer-acquisition costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Functionality: Embedded Fintech Reshapes Revenue Models

Billing and payments represented 52.15% of the childcare management software market share in 2025, confirming the centrality of tuition collection to platform value. Many centers now channel recurring invoices through automated clearing house debits, card vaults, or digital wallets, ensuring prompt settlement and fewer paper checks. In parallel, embedded lending modules offer tuition-installment plans that improve affordability for households and stabilize monthly cash flow for operators. Communication suites layer secure photo feeds, developmental milestone logs, and push alerts, enhancing parental loyalty and raising net promoter scores. Curriculum planners align activities with government learning frameworks, while analytics dashboards deliver occupancy forecasts and subsidy reconciliation, demonstrating the breadth of features bundled into modern suites. Together, these modules transform the childcare management software market size into a composite of subscription, transaction, and value-added service revenues.

Continued expansion in embedded payments is projected to lift average revenue per user, even as basic seat licenses face price pressure. Vendors that certify against rising privacy rules and integrate seamlessly with state subsidy APIs hold an execution advantage. Smaller providers gravitate toward modular purchasing, adding payroll advances or point-of-sale meal charges only after mastering core billing. This graduated path sustains upsell pipelines and cushions revenue volatility.

By Deployment: Cloud Dominates as SMEs Prioritize Flexibility

In 2025, cloud installations captured 36.45% of the childcare management software market, and their share continues to rise due to the growing preference for flexible and scalable solutions. Subscription platforms eliminate the necessity for on-premise servers, reducing infrastructure costs and simplifying IT management for childcare centers. Additionally, automatic patches ensure compliance with evolving privacy standards without requiring manual oversight, which is particularly beneficial for centers with limited technical expertise. Rural centers, in particular, value tablet access that syncs offline data once connectivity is restored, minimizing disruptions during field trips, power outages, or other connectivity challenges.

On the other hand, on-premise deployments remain the preferred choice in public-sector or franchise settings, where data sovereignty and extensive custom coding are critical requirements. However, these deployments face challenges such as lengthy procurement cycles, high upfront costs, and ongoing maintenance contracts, which slow their broader adoption across the market. To address these concerns, hybrid models have emerged as a viable alternative. These models allow attendance kiosks to operate locally while simultaneously replicating data to the cloud, offering a balanced solution for centers that are cautious about fully transitioning to cloud-based systems. This approach provides the benefits of both on-premise and cloud solutions, catering to the specific needs of childcare centers with varying levels of technological readiness.

By Application: Home-Based Providers Embrace Digital Tools

In 2025, day-care centers accounted for 66.67% of the revenue in the childcare management software market. This dominance was driven by their significant volume and higher per-child administrative spending, which underscores their reliance on advanced software solutions to streamline operations. However, home-based providers, which typically operate out of one or two rooms, are emerging as the fastest-growing segment within the market. These smaller operators depend heavily on mobile apps that automate various tasks, such as populating daily sheets, sending payment links, and compiling regulatory logs, all with minimal manual effort. This reliance on automation allows them to efficiently manage their operations despite limited resources.

After-school programs, on the other hand, derive value from scheduling grids that help coordinate bus routes and extracurricular activities, ensuring smooth daily operations. Meanwhile, nursery chains prioritize centralized dashboards that enable them to track license renewals across multiple regions, ensuring compliance with regulatory requirements. This diverse range of operational needs across different childcare providers highlights the importance of adaptable software solutions. As a result, configurable templates and role-based permissions have become standard features in nearly all childcare management software, catering to the unique demands of each segment.

By End-User: Employer-Sponsored Programs Gain Traction

In 2025, multi-location operators captured 58.75% of the childcare management software market. These scale players benefit significantly by distributing implementation costs across hundreds of classrooms, making their operations more cost-efficient. Additionally, their chain-wide rollouts generate extensive and richer datasets, which play a crucial role in improving benchmarks related to occupancy rates, payroll ratios, and fee elasticity. This ability to leverage data at scale provides them with a competitive advantage in the market. Sites sponsored by employers, particularly those managed by third-party specialists located on corporate campuses, are projected to experience the highest CAGR during the forecast period.

These sites are increasingly preferred by human resources teams due to their ability to integrate advanced features such as single sign-on, payroll deduction, and workforce analytics dashboards. These functionalities streamline administrative processes and provide valuable insights into workforce management, making them highly attractive to corporate clients. In contrast, stand-alone centers often gravitate toward freemium tiers of childcare management software. These tiers typically cover basic functionalities like attendance tracking and invoicing but lack advanced analytics capabilities. This trend underscores the fact that a single product tier rarely satisfies the diverse requirements of all client types, as different operational scales and priorities demand tailored solutions.

Geography Analysis

North America remained the largest region with 40.44% share of the childcare management software market in 2025, buoyed by federal subsidy reforms and high credit-card penetration that eases embedded payment adoption. The Midwest and Northeast lead biometric check-in adoption as state licensors tighten auditing.

Asia-Pacific posts the strongest growth outlook at 9.08% CAGR. India’s Poshan Tracker validates how national platforms can turbocharge digital maturity even in dispersed rural settings. Australia’s expanded subsidy outlays, coupled with target ratios for qualified early-educators, are prompting centers to invest in cloud tools that automate staffing compliance and subsidy reconciliation. Japan, South Korea, and Singapore combine elevated digital literacy with aging demographics, fostering corporate daycare chains that demand enterprise-grade software.

Europe exhibits steady, rule-driven uptake. The United Kingdom’s 30-hour entitlement extension expands the addressable base, while GDPR keeps security certifications front and center. Germany and France channel public funds through region-specific portals, incentivizing vendors to localize tax codes and subsidy claim files.

Competitive Landscape

No single vendor dominates the childcare management software market, with none surpassing the 20% revenue mark. Procare Solutions caters to enterprise chains, offering deep integrations with human-capital systems and role-based access.[3]Procare Solutions, “2025 Childcare Payment Trends Report,” procaresoftware.com Brightwheel appeals to small and mid-sized centers with its mobile-first interface and a tiered freemium model. SofterWare’s ChildWatch is tailored for camps and faith-based operators, and European supplier Famly stands out with its GDPR compliance and multilingual support. These vendors address diverse customer needs, creating a moderately fragmented market landscape.

The industry's monetization strategy is evolving, shifting from seat licenses to transaction revenue. Tuition processing and optional financing are becoming key drivers of gross margin growth. This shift reflects a broader trend in the software market, where recurring revenue streams are prioritized. Amendments to COPPA have further raised compliance standards, favoring vendors with in-house legal and security teams. These teams enable faster certifications, creating a competitive advantage and establishing a barrier to entry for smaller players.

Private-equity interest in childcare center chains is reshaping the market dynamics. Consolidated operators increasingly prefer standardized software solutions, which streamline operations and ensure consistency across locations. These operators often negotiate multi-year master agreements with vendors, locking in preferred partnerships and securing stable recurring revenue. This trend underscores the growing importance of long-term vendor relationships in driving market stability and growth.

Childcare Management Software Industry Leaders

Procare Solutions LLC

Lillio Inc

Brightwheel

KinderSystems LLC

QK Technologies Pty Ltd (QikKids)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: LEIFRAS Corporation acquired four childcare facilities in Japan, expanding regional coverage and driving demand for unified attendance and billing dashboards.

- January 2026: United States Department of Health and Human Services reinstated attendance-based billing for Child Care and Development Fund subsidies, accelerating real-time attendance software rollouts.

- June 2026: Minnesota’s mandate for electronic attendance records took effect, propelling software adoption among small subsidized providers.

- April 2025: Federal Trade Commission finalized COPPA amendments broadening biometric definitions and mandating written retention schedules, influencing product roadmaps toward advanced security features.

Global Childcare Management Software Market Report Scope

The Childcare Management Software Market comprises entities that develop digital platforms designed to automate and optimize administrative, operational, and communication processes for childcare centers, preschools, and early learning programs. These platforms typically offer functionalities such as enrollment management, attendance tracking, billing and invoicing, staff scheduling, parent communication, and compliance reporting.

The Childcare Management Software Market Report is Segmented by Functionality (Parent Engagement, Enrollment, Curriculum Management, Staff and HR, Billing, Compliance, and Analytics), Deployment (Cloud, On-Premise), Application (Day-Care, Preschool, After-School, Home-Based, Nursery Chains), End-User (Stand-Alone, Multi-Location, Government and Non-Profit, Employer-Sponsored, Other), and Geography (North America, Europe, Asia-Pacific, South America, Middle East, Africa). Market Forecasts are in Value (USD).

| Parent Engagement and Communication |

| Enrollment and Wait-List |

| Curriculum / Learning Management |

| Staff and HR / Scheduling |

| Billing and Payments |

| Compliance, Reporting and Analytics |

| Cloud |

| On-Premise |

| Day-Care Centres |

| Preschool / Early-Education Programs |

| After-School Programs |

| Home-Based Providers |

| Nursery Chains and Franchises |

| Stand-Alone Centres |

| Multi-Location Operators |

| Government / Non-Profit Providers |

| Employer-Sponsored Child-Care Programs |

| Other End-Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Functionality | Parent Engagement and Communication | |

| Enrollment and Wait-List | ||

| Curriculum / Learning Management | ||

| Staff and HR / Scheduling | ||

| Billing and Payments | ||

| Compliance, Reporting and Analytics | ||

| By Deployment | Cloud | |

| On-Premise | ||

| By Application | Day-Care Centres | |

| Preschool / Early-Education Programs | ||

| After-School Programs | ||

| Home-Based Providers | ||

| Nursery Chains and Franchises | ||

| By End-User | Stand-Alone Centres | |

| Multi-Location Operators | ||

| Government / Non-Profit Providers | ||

| Employer-Sponsored Child-Care Programs | ||

| Other End-Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected value of the childcare management software market by 2031?

The childcare management software market is expected to reach USD 405.42 million by 2031, growing at an 8.70% CAGR during 2026-2031.

Which region will lead growth in childcare management platforms?

Asia-Pacific is projected to record the fastest regional growth at a 9.08% CAGR through 2031, driven by India's national digitization initiatives and expanded childcare subsidies in Australia.

Which functionality currently generates the most revenue for vendors?

Billing and payments modules accounted for 52.15% of total revenue in 2025, highlighting the importance of automated tuition collection for childcare centers.

Why are cloud deployments gaining traction among small centers?

Cloud-based platforms captured 36.45% market share in 2025 due to month-to-month subscriptions, elimination of hardware costs, automatic updates, and suitability for budget-constrained centers.

What drives employer interest in on-site or subsidized childcare?

Surveys indicate over 80% of employees view childcare as a key workplace benefit, and pilot programs show employer-sponsored childcare improves retention and reduces absenteeism.

How do new privacy regulations influence software selection?

Stricter requirements under COPPA and GDPR, including expanded biometric-data definitions and tighter retention rules, are driving demand for platforms offering encryption, consent management, and annual security audits.

Page last updated on: