Soy Lecithin Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 0.73 Billion |

| Market Size (2031) | USD 1.03 Billion |

| Growth Rate (2026 - 2031) | 7.20% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Soy Lecithin Market Analysis by Mordor Intelligence

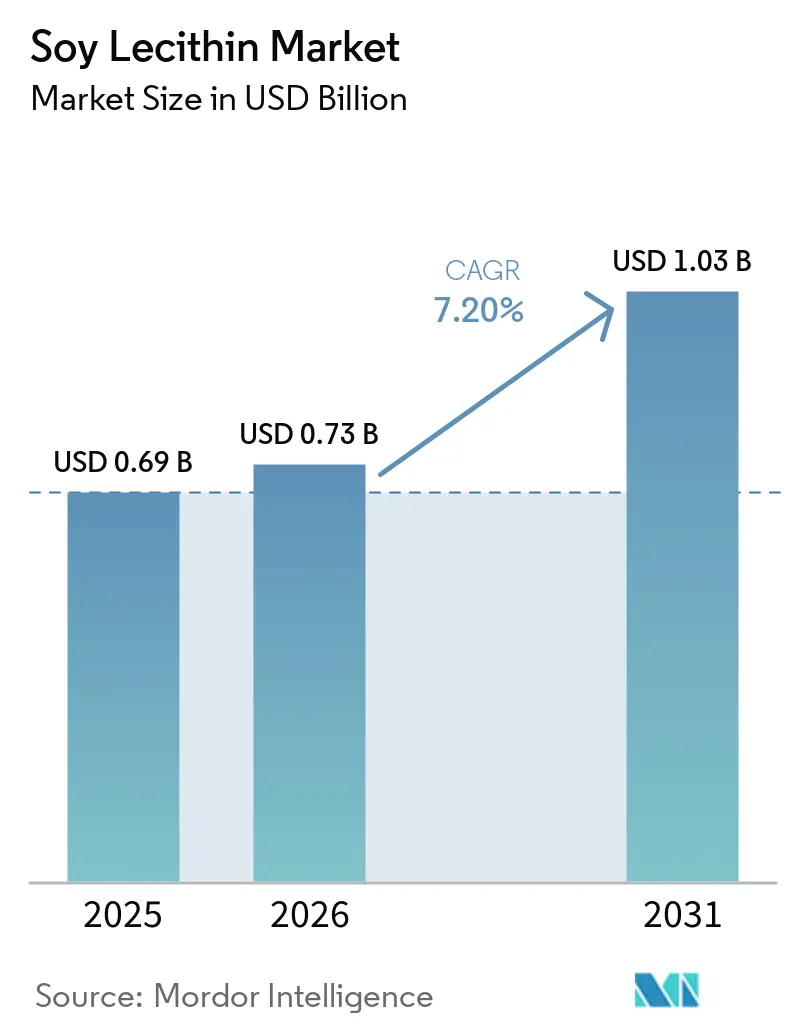

In 2025, the soy lecithin market was valued at USD 0.69 billion. It is projected to grow to USD 0.73 billion in 2026 and reach USD 1.03 billion by 2031, with a CAGR of 7.2% during the forecast period (2026-2031). The market is closely linked to soybean oil refining, as lecithin is a co-product of crushing and degumming. This connection ties production costs to oilseed margins and crop availability, rather than lecithin demand alone, ensuring cost competitiveness but increasing sensitivity to changes in soybean processing and farm economics. Demand is rising as food manufacturers replace synthetic emulsifiers with label-friendly ingredients. Soy lecithin also has broad regulatory approval in the U.S. and Europe. Additionally, the market benefits from growth in premium nutrition, personal care, and organic products, where buyers prefer plant-based emulsifiers, simpler ingredient lists, and detailed origin documentation. Competition focuses on portfolio depth and premium grades, with larger processors leveraging scale and smaller players emphasizing purity, certification, and specialized functionality.

Key Report Takeaways

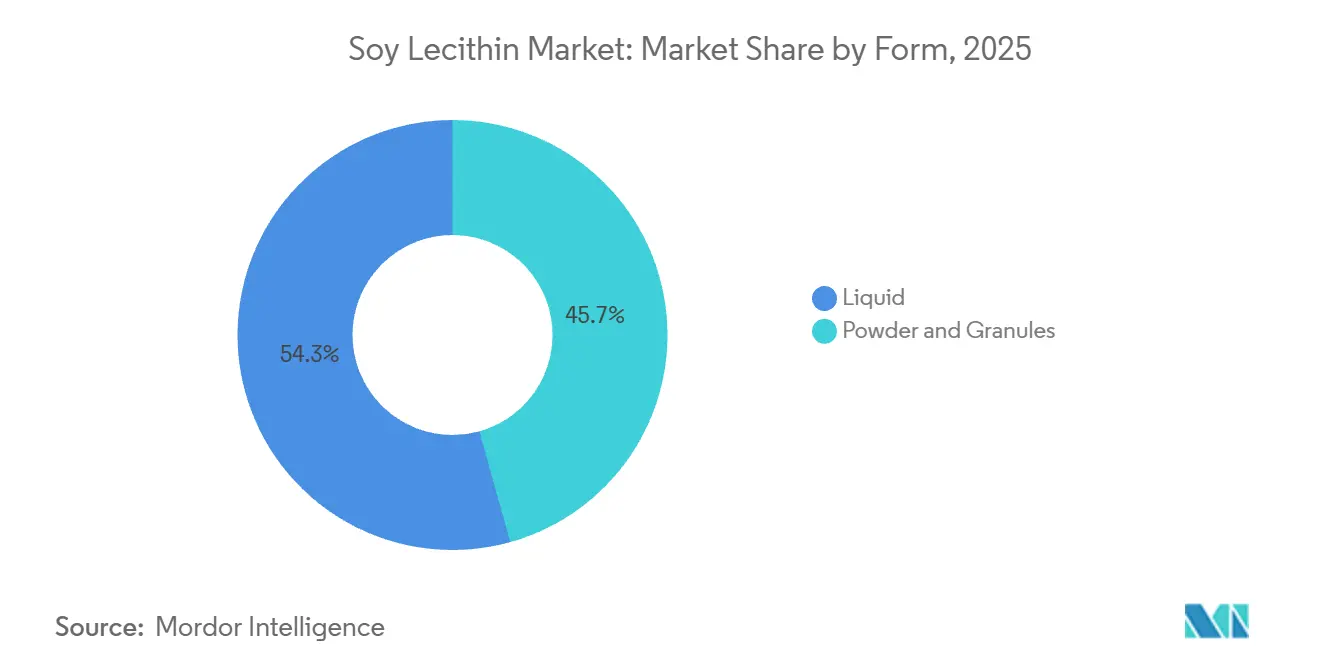

- By form, liquid held 54.33% of the soy lecithin market share in 2025, while powder and granules is projected to expand at an 7.98% CAGR through 2031.

- By nature, conventional accounted for 86.72% of the market in 2025, while organic is forecast to grow at an 8.76% CAGR through 2031.

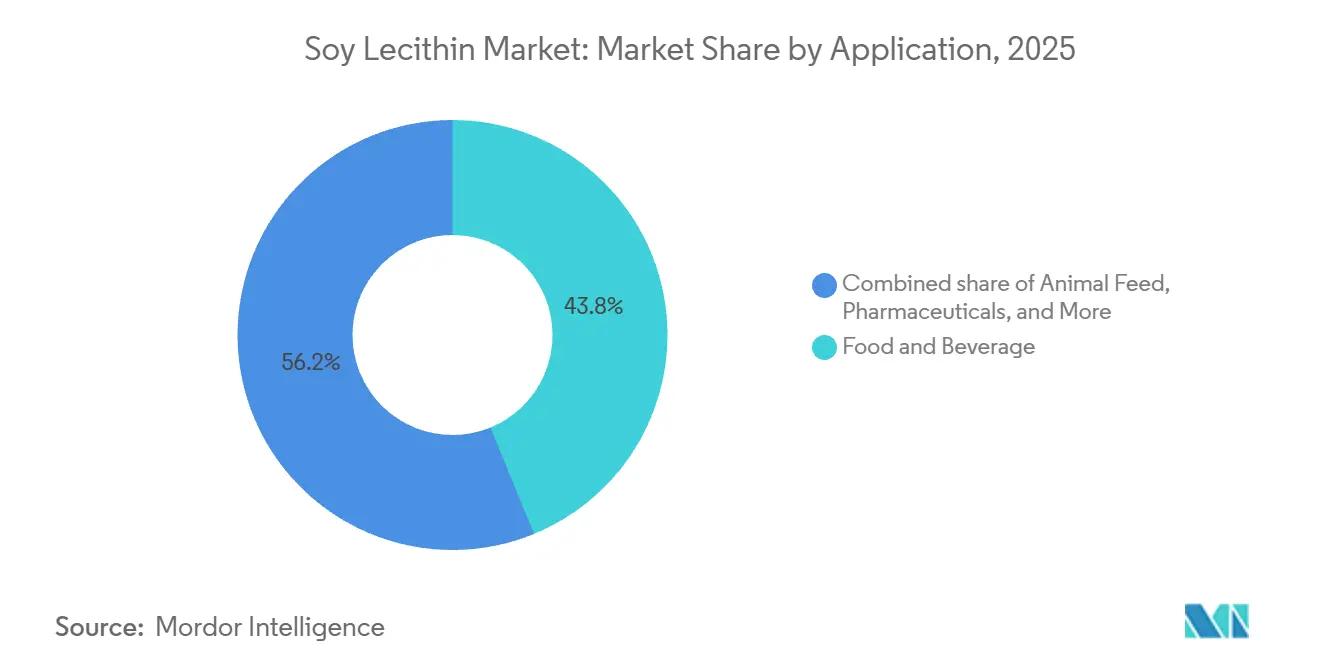

- By application, food and beverage captured 43.81% of the market in 2025, while cosmetics and personal care are set to advance at a 9.5% CAGR through 2031.

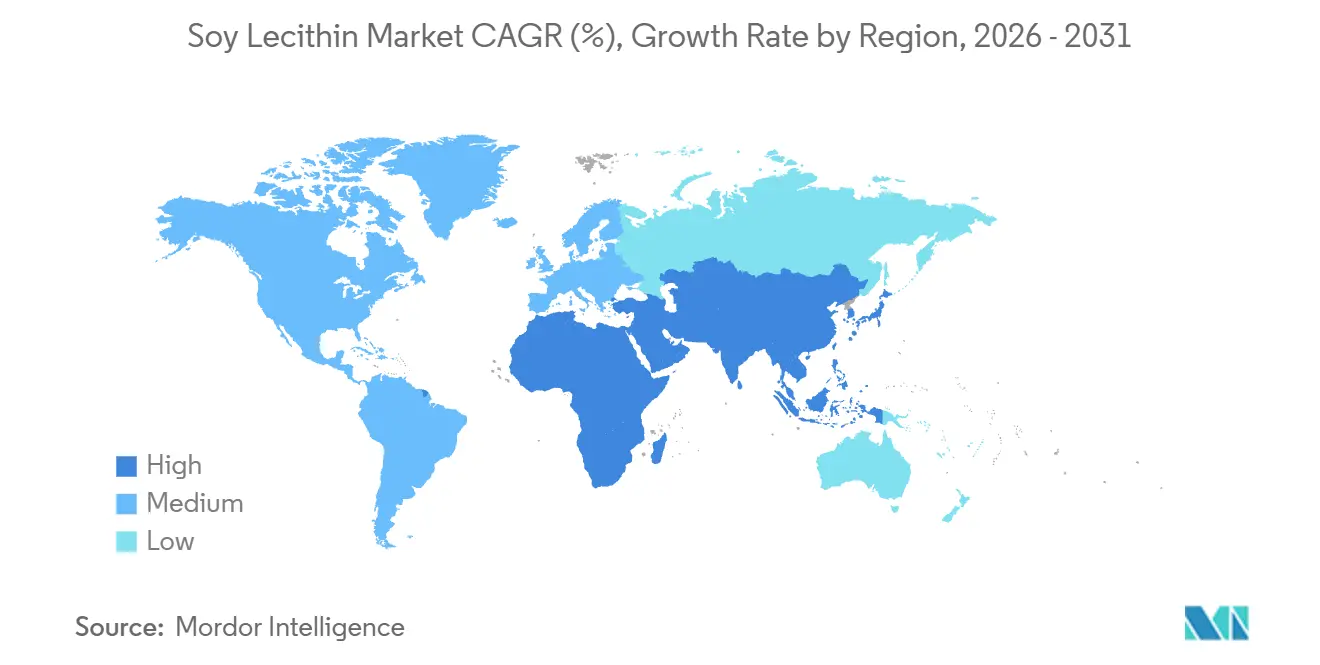

- By geography, North America led with 33.37% revenue share in 2025, while Asia-Pacific recorded the highest projected CAGR at 9.89% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Soy Lecithin Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Natural Emulsifiers | +2.1% | Global | Short term (≤ 2 years) |

| Shift Toward Clean-Label Products | +1.5% | North America and Europe | Medium term (2-4 years) |

| Growth in Processed Food Applications | +1.2% | Asia-Pacific core, spillover to Middle East and Africa | Medium term (2-4 years) |

| Expanding Use in Bakery and Confectionery Products | +0.8% | Global | Short term (≤ 2 years) |

| Increasing Use in Nutraceuticals and Dietary Supplements | +0.6% | North America, Europe, and Asia-Pacific | Long term (≥ 4 years) |

| Advances in Liquid and De-Oiled Lecithin Applications | +0.5% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Natural Emulsifiers

As manufacturers pivot away from synthetic emulsifiers, facing heightened consumer scrutiny, soy lecithin emerges as a favored choice in the reformulation of processed foods. Its stronghold is bolstered by its GRAS status in the U.S. (under 21 CFR 184.1670) and its designation as E322 in the European Union. These approvals ease regulatory challenges for formulators operating in multiple regions[1]Source: European Commission, “Regulation (EC) No 1333/2008 on Food Additives”, eur-lex.europa.eu. Moreover, soy lecithin's versatility allows it to manage emulsification, wetting, release, and dough conditioning within a single formulation. This capability enables food producers to streamline recipes without compromising performance. Such versatility is crucial in sectors like bakery, confectionery, spreads, and dairy, where a single ingredient change can influence texture, machinability, and shelf stability. Consequently, the soy lecithin market is not only capturing market share from synthetic additives in new product launches but is also being integrated into a broader portfolio refinement of established product lines.

Shift Toward Clean-Label Products

As the clean-label trend gains momentum, soy lecithin is finding its way from premium shelves to mainstream food retail. In Europe, the established framework under Regulation (EC) No. 1333/2008, coupled with ongoing additive reviews, has heightened the appeal of ingredients fitting accepted food use categories. This backdrop bolsters the steady incorporation of lecithin in reformulation efforts. Food brands and private label suppliers are gravitating towards naturally derived materials, familiar to consumers and recognized by major regulatory systems, giving the soy lecithin market a significant boost. Organic production rules further cement this trend. De-oiled lecithin, when sourced under U.S. and EU organic standards, can bolster certified processing. Consequently, the soy lecithin market is now intricately linked to label transparency, procurement discipline, and retailer ingredient policies, extending beyond mere emulsifier demand.

Growth in Processed Food Applications

The soy lecithin market is supported by processed food manufacturing, particularly in Asia-Pacific and the Middle East and Africa, where packaged food production is growing from a smaller base. The USDA's June 2026 outlook increased the U.S. soybean crush estimate for the 2025/26 marketing year to 2.65 billion bushels, boosting lecithin availability and ensuring a steady supply for food ingredient channels. In China, soybean prices rose from RMB 3,900/MT (USD 557/MT) in January 2025 to RMB 4,400/MT (USD 628/MT) by the 2025/26 harvest[2]Source: U.S. Department of Agriculture, “Oilseeds and Products Annual, China, People’s Republic of”, apps.fas.usda.gov. Despite higher prices, favorable crushing economics sustained the production of soybean derivatives. The soy lecithin market benefits as industrial food buyers prioritize performance, availability, and cost, leading to stable demand compared to categories influenced by retail perception. This stability supports a broad application base in bakery, confectionery, dairy, beverage powders, and feed-related food systems.

Increasing Use in Nutraceuticals and Dietary Supplements

The soy lecithin market is shifting towards higher-value applications as phosphatidylcholine-rich grades gain popularity in dietary supplements and nutraceuticals. Demand is highest for de-oiled powders and granules that disperse easily, flow smoothly through capsule and tablet production lines, and support applications like cognitive health, liver support, and cardiovascular supplements. Supplement manufacturers require both functionality and consistent manufacturing, favoring established suppliers with validated process controls that meet 21 CFR Part 111 standards. These regulations raise entry barriers for smaller suppliers lacking documented systems, batch consistency, or application support. As a result, the market is moving towards specialized grades, where value lies in purity, precise dosing, and end-use documentation rather than commodity volume.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fluctuations in Soybean Raw Material Supply | -1.0% | Global | Short term (≤ 2 years) |

| Price Volatility of Soybeans | -0.8% | North America, South America, and Asia-Pacific | Short term (≤ 2 years) |

| Allergen Concerns Related to Soy | -0.5% | North America and Europe | Medium term (2-4 years) |

| Competition From Alternative Emulsifiers | -0.6% | Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fluctuations in Soybean Raw Material Supply

The soy lecithin market faces a key limitation as its supply depends on soybean crushing decisions driven by oil and meal economics, not lecithin demand. USDA data for the 2025/26 marketing year indicates U.S. soybean ending stocks at 340 million bushels. Additionally, the 2026/27 season-average farm price is forecast at USD 11.40 per bushel, a USD 1.00 increase from the previous year, signaling tighter processor economics if selling conditions weaken[3]Source: U.S. Department of Agriculture, “Soybeans and Oil Crops, Market Outlook”, ers.usda.gov. As a result, the soy lecithin market remains vulnerable to changes in soybean planting, yield, trade flows, and crush margins, even when downstream lecithin demand is stable. This disconnect between market demand and supply response means processors do not increase crushing solely due to higher emulsifier demand. Consequently, the market may experience tighter supply and higher prices even with steady, diversified demand growth across end uses.

Allergen Concerns Related to Soy

Allergen disclosure rules are creating challenges for the soy lecithin market, as these rules do not apply to all competing lecithin sources. In the U.S. and the EU (under Annex II of Regulation No. 1169/2011), soy is classified as a major allergen, requiring manufacturers to clearly label soy-derived ingredients. This makes the soy lecithin market more vulnerable, particularly in premium food and personal care products, where brands often choose sunflower or rapeseed lecithin to avoid allergen-related concerns, despite higher costs. The impact is most significant in products emphasizing purity, family safety, or simple labeling over cost. In Europe, stricter allergen management is increasing the focus on precautionary labeling and ingredient control, keeping allergen handling a constant challenge for the soy lecithin market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Liquid Leads on Industrial Scale While Dry Formats Expand into Precision Applications

In 2025, liquid lecithin held a 54.3% share of the soy lecithin market, maintaining its position as the leading form. Its dominance stems from its established use in chocolate, margarine, release agents, and bakery fat systems, where it ensures viscosity control, wetting, and uniform dispersion during continuous manufacturing. The soy lecithin market relies heavily on these high-volume food lines, driving consistent demand for large processors and repeat purchases. Liquid grades also have the simplest processing among major lecithin formats, providing a cost advantage in industrial applications. This balance of cost and functionality makes liquid lecithin the preferred choice for applications needing natural emulsification within tight budgets.

Powder and granules are the fastest-growing segment, with an 8.0% CAGR projected for this segment of the soy lecithin market through 2031. This growth reflects shifting demand as the industry increasingly serves supplements, functional foods, and instant beverages requiring free-flowing, precisely dosed ingredients. De-oiled powder, with higher phospholipid concentration and better dispersibility in water-based systems, is ideal for capsules, sachets, and dry blends. Granules are gaining popularity in sports nutrition, nutrition bars, and ready-to-consume products, where ingredient visibility is important to consumers. Additionally, value-chain suppliers now offer more certified non-GMO, Kosher, Halal, and organic-compatible de-oiled grades, simplifying sourcing for formulators in export markets.

By Nature: Conventional Holds the Volume Base While Organic Advances Through Certified Demand

In 2025, conventional soy lecithin led the market with an 86.7% share. This dominance is due to widespread conventional soybean cultivation, cost-efficient non-segregated supply chains, and the suitability of conventional grades for bulk food and feed applications. Buyers in the soy lecithin market prioritize process performance and cost over identity preservation or organic certification, particularly in large industrial uses. Here, lecithin functions mainly as a processing aid without adding significant branded value. Additionally, global soybean production patterns support this trend, as mainstream cultivation volumes far exceed certified organic supplies.

Organic lecithin is projected to grow at an 8.8% CAGR through 2031, making it the fastest-growing segment in the soy lecithin market. This growth is driven by stricter retailer standards, increased demand for origin transparency, and higher procurement expectations in premium food, personal care, and nutrition sectors. The organic segment faces higher barriers, as sourcing requires segregation, certification, and detailed documentation from soybean origin to the final product. These requirements favor larger or well-organized suppliers capable of managing traceability at scale. Moreover, suppliers now offer more certified organic and non-GMO de-oiled soy lecithin than before, enabling faster adoption among buyers who previously relied on limited sourcing options or exemptions.

By Application: Food and Beverage Anchors Volume While Personal Care Builds the Premium Layer

In 2025, the food and beverage sector led the soy lecithin market, comprising 43.8% of its size. Bakery and confectionery drive demand, using lecithin for fat dispersion, machinability, texture control, and shelf-life stability in high-volume products. Dairy systems, beverage mixes, and processed foods also rely on lecithin to maintain oil-water balance and improve product consistency. Additionally, animal feed benefits from lecithin's role in fat digestibility and pellet cohesion, strengthening the soy lecithin market's volume while being less affected by retail ingredient perceptions. The pharmaceutical sector is expanding its use of lecithin in lipid-based delivery systems, where phospholipid functionality outweighs commodity pricing.

Growing at a 9.5% CAGR through 2031, the cosmetics and personal care sector is the fastest-growing segment in the soy lecithin market. In products like creams, lotions, and haircare, soy lecithin acts as an emulsifier, skin-conditioning agent, and carrier for active ingredients, adding value beyond stabilization. The market is benefiting from increasing demand for plant-based, vegan, and transparent labeling in premium personal care. Its compatibility with botanical oils and extracts also makes lecithin ideal for formulations emphasizing naturally derived ingredients. This trend creates a premium niche for the soy lecithin market, where supplier selection focuses on purity, traceability, and application support over bulk availability.

Geography Analysis

In 2025, North America held a 33.4% share of the soy lecithin market, leading the region due to its strong soybean crushing infrastructure, extensive food processing, and major suppliers like ADM, Cargill, and Bunge. USDA’s June 2026 outlook projected U.S. soybean crush for the 2025/26 marketing year at 2.65 billion bushels, ensuring ample co-products for food-grade lecithin. The region’s certification systems for organic and non-GMO supply chains support both premium domestic and export demands, balancing high-volume conventional sales with certified product development.

Europe remains crucial in the soy lecithin market, driven by strict standards on ingredient origin, labeling, and clean-label preferences. The region demands premium non-GMO and organic grades, especially in bakery, confectionery, and processed foods, where transparency and retailer policies are key. EU regulations on food additives, allergens, and organic production ensure disciplined procurement, shaping product mixes and sourcing. South America, while a major global supplier due to its soybean processing scale, has limited value-added certified volumes compared to conventional output.

Asia-Pacific is the fastest-growing region, with a 9.9% CAGR projected through 2031. Growth is fueled by rising processed food production in China and India, increasing animal feed complexity, and higher demand for nutraceuticals and personal care products. China’s role as a leading soybean importer and processor drives regional demand, though trade tensions and supplier disruptions in early 2025 caused some uncertainties. India is gaining importance with expanding crushing capacity and traceability-focused soybean programs, supporting domestic lecithin production. In the Middle East and Africa, demand is led by processed food imports, confectionery manufacturing, and a growing nutraceutical sector.

Competitive Landscape

ADM, Cargill, and Bunge lead the soy lecithin market, benefiting from integrated oilseed-crushing networks and broad customer bases. They leverage feedstock access, refining and logistics scale, and the ability to supply liquid and de-oiled grades across multiple sectors. Beyond these leaders, the market remains fragmented, with specialized suppliers serving niches like pharmaceutical-grade, identity-preserved, and certified-organic products. This division between large-scale commodity supply and specialized differentiation shapes market competition.

In March 2026, Bunge expanded its portfolio by acquiring IFF’s soy protein concentrate, lecithin, and crush business, including the Solec brand. This move strengthened its offerings in liquid, powdered, and fractionated lecithins from soy, sunflower, and rapeseed, enhancing its reach in confectionery, bakery, and nutrition sectors. Earlier, in January 2025, Cargill launched a new soy lecithin production line at its Ponta Grossa facility in Brazil, modernizing equipment and boosting supplies for food-grade and technical-grade applications. These actions highlight how top suppliers are diversifying their offerings in form, origin, and application while protecting commodity volumes.

Specialists like Lipoid GmbH, LASENOR EMUL S.L., and American Lecithin Company focus on purity, application support, and certifications rather than scale. They maintain margins as buyers in pharmaceuticals, supplements, and premium foods prioritize tailored functionality and traceable sourcing over cost. Certified-organic supply offers opportunities for premium pricing, especially in cosmetics and nutraceuticals requiring batch-level documentation. Technological advancements, such as hydrolyzed and hydroxylated lecithins, improve emulsification at lower usage rates for demanding applications. While scale drives mainstream business, technical specialization dominates the premium segment.

Soy Lecithin Industry Leaders

Archer Daniels Midland Company

Cargill, Incorporated

Bunge Global SA

Wilmar International Limited

Lipoid GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Bunge Global SA completed the acquisition of International Flavors & Fragrances' (IFF) soy protein concentrate, lecithin, and soy crush businesses, including the Solec™ brand. This transaction expanded Bunge's lecithin portfolio to include liquid, powdered, and fractionated lecithins from soy, sunflower, and rapeseed, enhancing supply chain breadth for confectionery, bakery, and food supplement manufacturers globally.

- January 2026: ADM and Bayer extended their partnership by three years to scale sustainable soybean cultivation in India, targeting 100,000 farmers across 200,000 hectares under ProTerra-certified sustainable farming practices. The initiative progressively expands India's domestic supply base for traceability-verified soy lecithin, directly relevant to the country's growing pharmaceutical excipient and nutraceutical markets.

- January 2025: Cargill launched a new soy lecithin production line at its Ponta Grossa industrial facility in Brazil, as part of a BRL 35 million equipment modernisation programme. The facility processes more than 750,000 metric tons of soybeans annually; the new lecithin line supplies food-grade and technical-grade lecithin to animal feed and industrial customers in Asia and Europe.

Global Soy Lecithin Market Report Scope

| Liquid |

| Powder and Granules |

| Conventional |

| Organic |

| Food and Beverage | Bakery and Confectionery |

| Dairy Products | |

| Beverages | |

| Other Food and Beverage | |

| Animal Feed | |

| Dietary Supplements | |

| Pharmaceuticals | |

| Cosmetics and Personal Care | |

| Other Applications |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Form | Liquid | |

| Powder and Granules | ||

| By Nature | Conventional | |

| Organic | ||

| By Application | Food and Beverage | Bakery and Confectionery |

| Dairy Products | ||

| Beverages | ||

| Other Food and Beverage | ||

| Animal Feed | ||

| Dietary Supplements | ||

| Pharmaceuticals | ||

| Cosmetics and Personal Care | ||

| Other Applications | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the 2031 value outlook for soy lecithin?

The soy lecithin market is forecast to reach USD 1.03 billion by 2031, rising from USD 0.73 billion in 2026 at a 7.2% CAGR.

Which region leads global demand for soy lecithin?

North America held the largest regional share in 2025 at 33.37%, supported by strong soybean crushing and food processing infrastructure.

Which region is growing the fastest through 2031?

Asia-Pacific is projected to record the highest CAGR at 9.89% through 2031, driven by processed foods, feed demand, and expanding nutraceutical and personal care use.

Why are dry lecithin formats gaining traction?

Powder and granules are growing faster, at 7.98% CAGR, because they work well in supplements, instant beverage mixes, sachets, and other precision-dosed applications.

Page last updated on: