Soy Sauce Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 61.96 Billion |

| Market Size (2031) | USD 78.25 Billion |

| Growth Rate (2026 - 2031) | 4.78% CAGR |

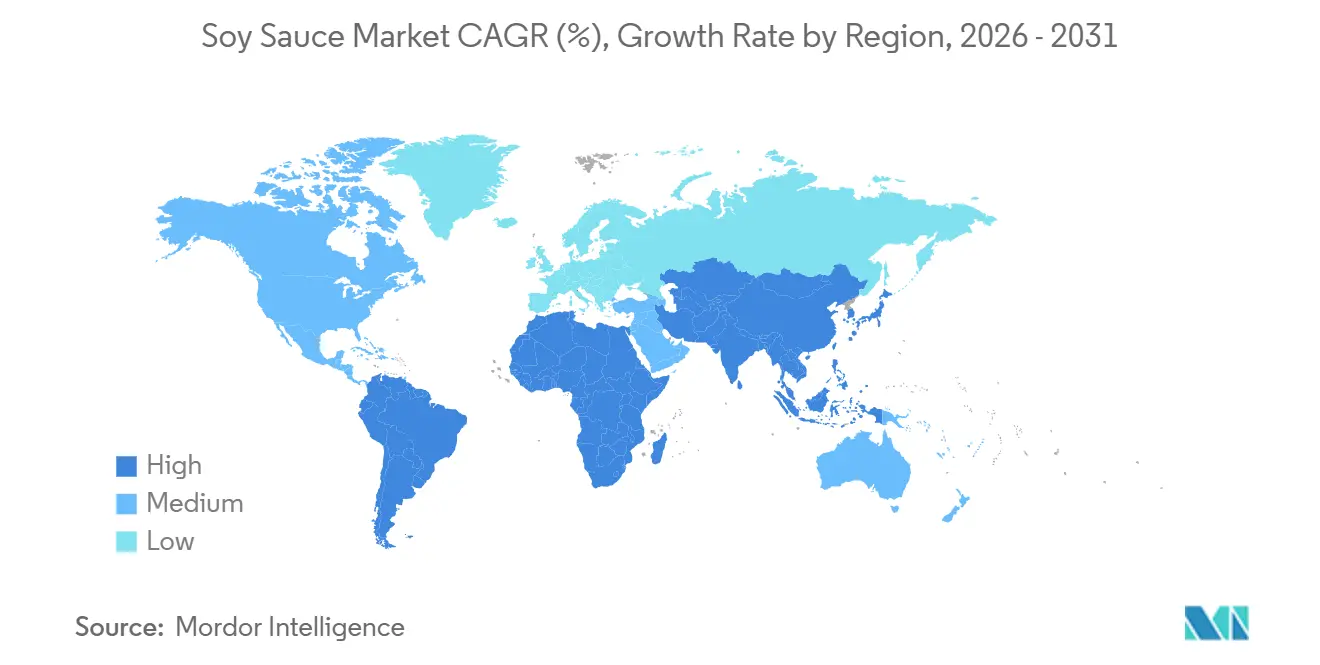

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

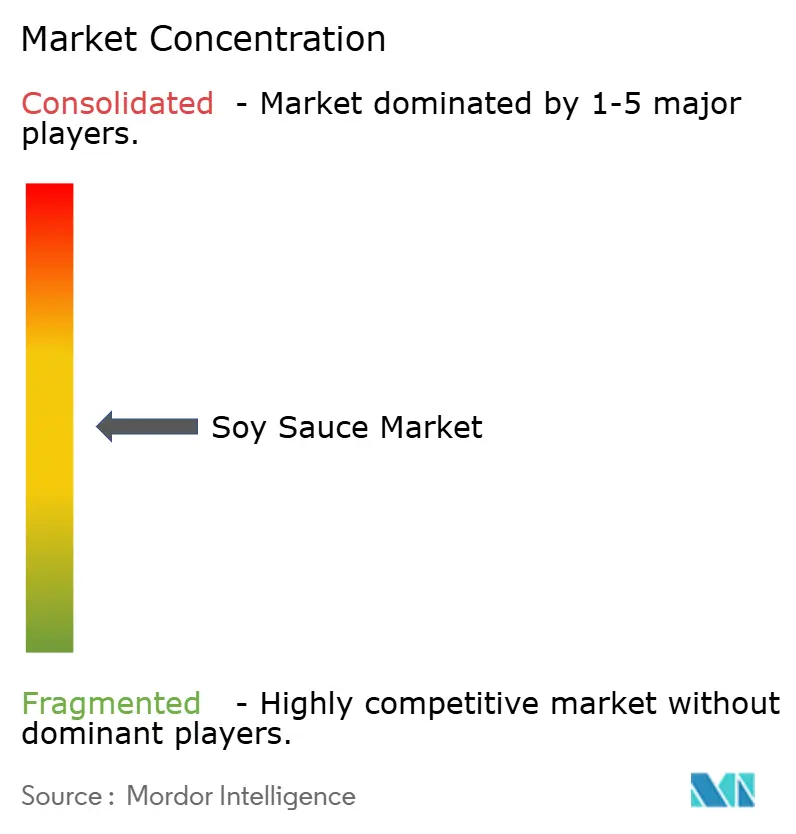

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Soy Sauce Market Analysis by Mordor Intelligence

The soy sauce market size was valued at USD 59.13 billion in 2025 and is estimated to grow from USD 61.96 billion in 2026 to reach USD 78.25 billion by 2031, at a CAGR of 4.78% during 2026-2031. The market is expanding due to growing interest in plant-based diets, the increasing use of umami flavors in cuisines beyond Asia, and the rising demand for ready-to-cook meal kits that often include soy sauce as a key ingredient. These trends are driving higher demand in both the retail and food-processing industries. Consumers are increasingly choosing premium brewed soy sauce over chemically processed alternatives. This shift is influenced by stricter regulations on harmful 3-MCPD contaminants and a growing preference for clean-label, naturally fermented products. In North America, the market is growing faster than the global average, as soy sauce is widely used by meal-kit providers and plant-based meat manufacturers to enhance the savory flavor of their offerings. The market remains moderately consolidated, with established brands and new players competing to meet evolving consumer preferences and capitalize on growth opportunities.

Key Report Takeaways

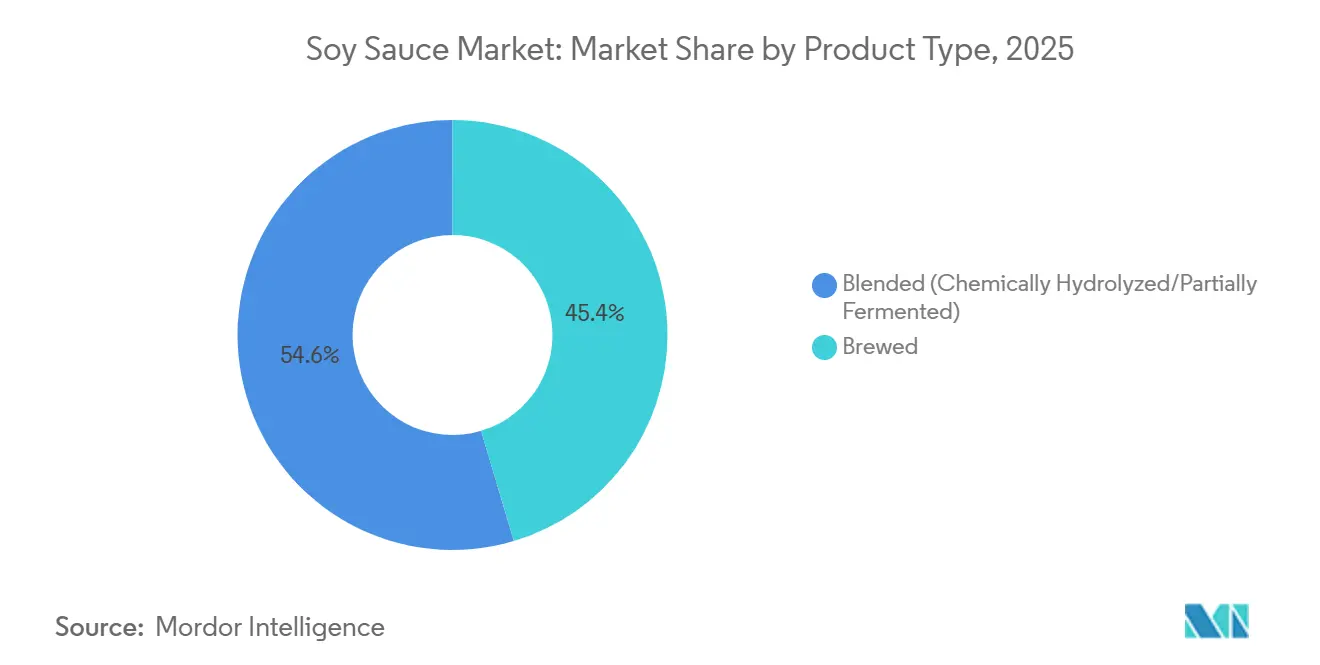

- By product type, blended soy sauce accounted for 54.62% of 2025 revenue, while brewed variants are projected to expand at a 5.47% CAGR through 2031.

- By format, liquid soy sauce accounted for 87.51% of 2025 demand; powdered soy sauce is forecast to grow at a 5.13% CAGR over 2026-2031.

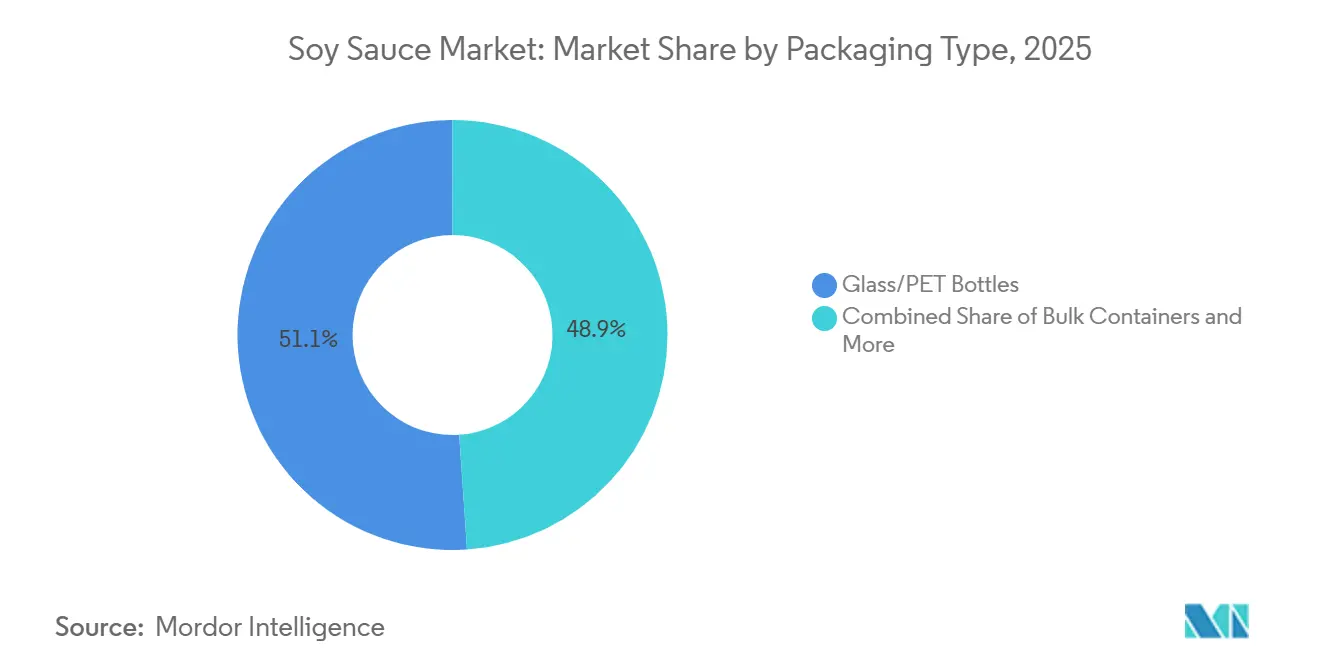

- By packaging type, glass and PET bottles accounted for 51.07% of 2025 sales, whereas pouches and sachets are advancing at a 5.36% CAGR through 2031.

- By end use, retail accounted for 43.18% of 2025 volume, yet food processing is set to grow at a 6.25% CAGR during 2026-2031.

- By geography, Asia-Pacific retained 58.11% of the soy sauce market share in 2025; North America is registering the fastest regional CAGR of 6.41% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Soy Sauce Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher consumption of instant noodles and ready-to-cook Asian meal kits | +0.9% | Global, concentrated in Asia-Pacific, North America, Europe | Medium term (2-4 years) |

| Increasing consumer preference for umami-rich flavors | +1.1% | North America, Europe, urban South America, Middle East | Short term (≤ 2 years) |

| Use of soy sauce in food manufacturing as a natural flavor enhancer | +0.8% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Growth of plant-based and vegan diets | +0.7% | North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Product innovation in mushroom, garlic, and chili variants | +0.6% | North America, Japan, South Korea | Short term (≤ 2 years) |

| Growing preference for low-sodium recipes | +0.5% | North America, Europe, Japan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Higher consumption of instant noodles and ready-to-cook Asian meal kits

The growing popularity of instant noodles and ready-to-cook Asian meal kits is driving global demand for soy sauce. Many instant noodle manufacturers and meal-kit providers include soy sauce sachets in their products, making it more accessible to households and expanding its use beyond traditional Asian cuisine enthusiasts. For instance, data from the World Instant Noodles Association shows that China consumed approximately 43,802 million servings of instant noodles in 2024, underscoring the massive consumer base that supports soy sauce demand in convenience foods[1]Source: World Instant Noodles Association, "Demand Rankings", instantnoodles.org. Premium noodle brands are increasingly focusing on naturally brewed, artisanal soy sauce to enhance the quality and flavor of their offerings. This trend reflects a shift toward higher-quality ingredients that appeal to health-conscious and flavor-focused consumers. Furthermore, the rising interest in Asian-inspired meals, combined with the growing demand for convenient packaged foods in regions such as North America and Europe, continues to drive global soy sauce consumption.

Growth of plant-based and vegan diets is reinforcing the role of soy sauce as a flavor enhancer

The increasing popularity of plant-based and vegan diets is driving higher demand for soy sauce as a natural flavor enhancer. As of February 2026, the World Animal Foundation estimates that there were around 88 million vegans globally, highlighting the growing number of consumers seeking plant-based food options[2]Source: World Animal Foundation, "How Many Vegans Are in the World in 2026? Latest Vegan Stats", worldanimalfoundation.org. Since plant-based recipes often lack the rich, savory taste (umami) found in meat and dairy, soy sauce has become a key ingredient to improve the flavor of vegan dishes, meat substitutes, ready-to-eat meals, and sauces. This trend is especially noticeable in North America and Europe, where food manufacturers are working to improve the taste of processed plant-based products to meet consumer expectations. Additionally, more people are seeking naturally brewed, clean-label products, boosting demand for premium soy sauce varieties. These factors are collectively contributing to the steady growth of the soy sauce market worldwide.

Product innovation in flavored variants such as mushroom, garlic, and chili soy sauce

Flavored soy sauce options, such as mushroom, garlic, and chili-infused varieties, are driving new growth opportunities in the global soy sauce market. Companies like Lee Kum Kee Co. Ltd. are introducing these specialty flavors to meet changing consumer tastes and the growing demand for convenient cooking solutions. These versatile condiments are becoming increasingly popular among consumers who want to prepare meals quickly while enjoying a variety of unique flavors. This trend is especially noticeable in Western markets, where people are exploring diverse culinary experiences. Retailers are also encouraging customers to try these products by offering variety packs and premium flavored options, which help boost sales and increase the value of purchases. Furthermore, the rise of online shopping platforms and personalized product suggestions is making it easier for consumers to discover niche and high-quality soy sauce options.

Growing preference for low-sodium soy sauce

Consumers are increasingly seeking low-sodium food options, driving demand for reduced-sodium soy sauce worldwide. People are becoming more aware of the health risks linked to high sodium intake, such as hypertension, and are opting for healthier alternatives in their diets. A study published by Academic OUP in October 2025 revealed that the risk of hypertension rises by 13% when serum sodium levels reach 140–142 mmol/L and by 29% when levels exceed 143 mmol/L. This has made sodium reduction a key focus for many consumers[3]Source: Academic OUP, "Risk of Hypertension and Heart Failure Linked to High-Normal Serum Sodium and Tonicity in General Healthcare Electronic Medical Records", academic.oup.com. To meet this demand, leading companies such as Kikkoman Corporation and Lee Kum Kee Co. Ltd. have launched reduced-sodium soy sauces. These products cater to health-conscious consumers while maintaining the traditional taste of soy sauce. Additionally, advancements in flavor-enhancing technologies and the use of salt substitutes are enabling manufacturers to offer healthier options without compromising on flavor. This trend is expected to further drive the growth of the reduced-sodium soy sauce segment in the coming years.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High sodium content in conventional formulations | -0.6% | North America, Europe, Japan | Medium term (2-4 years) |

| Allergen concerns tied to soy and gluten | -0.4% | North America, Europe, Australia | Short term (≤ 2 years) |

| Stringent food-safety and quality regulations | -0.5% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Availability of alternative flavor enhancers | -0.3% | Asia-Pacific core, spillover to West | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High sodium content in conventional soy sauce

The high sodium content in traditional soy sauce is a significant challenge for the global soy sauce market, especially as more consumers prioritize healthier eating habits. Concerns about health issues like hypertension and cardiovascular disease, which are linked to high sodium intake, are prompting people to either reduce their soy sauce intake or switch to alternatives such as coconut aminos or vinegar-based dressings. To address this, manufacturers are focusing on creating reduced-sodium soy sauce options. However, reducing sodium levels often impacts the product's flavor, stability, and shelf life, making it difficult to maintain the same quality as regular soy sauce. Additionally, developing these low-sodium variants requires advanced technologies and ingredient adjustments, which increase production costs and complexity. As a result, the market is seeing a clear distinction between standard soy sauce products and premium low-sodium alternatives, with the latter catering to a growing segment of health-conscious consumers.

Risk of allergen concerns related to soy and gluten content

Concerns about allergens, particularly soy and gluten, are hindering the growth of the global soy sauce market. Soy is one of the most common food allergens, and traditional soy sauce production often includes wheat, which contains gluten. As a result, manufacturers must clearly label their products to inform consumers about potential allergens and comply with strict food safety regulations. These issues limit soy sauce's appeal to consumers with soy or gluten sensitivities and reduce its use in foodservice channels that prioritize allergen-free options. Additionally, governments worldwide are introducing stricter rules for allergen testing and labeling, which increases compliance costs for producers. Smaller manufacturers, especially those without specialized facilities for allergen-free production, face significant hurdles. These include higher operational costs and the need for additional investments, which can slow down market expansion and hinder the development of new products. The growing demand for allergen-free alternatives further pressures traditional soy sauce producers to innovate and adapt to changing consumer preferences.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Brewed Variants Gain on Quality Migration

Blended soy sauce, which includes chemically hydrolyzed and partially fermented types, holds the largest share of the global soy sauce market, accounting for 54.62% of total revenue. This type of soy sauce is widely preferred because it is affordable, offers a consistent taste, and has a shorter production time compared to traditionally brewed soy sauce. It is especially popular among foodservice providers and processed food manufacturers due to its cost-effectiveness and suitability for large-scale use. Additionally, its strong demand in emerging markets and among budget-conscious consumers continues to drive its worldwide growth.

Brewed soy sauce is expected to grow at the fastest rate during the forecast period, with a projected CAGR of 5.47% between 2026 and 2031. This growth is largely driven by rising consumer interest in naturally fermented, high-quality condiments with authentic flavors. Many consumers are now prioritizing clean-label products made using traditional brewing methods that avoid heavy chemical processing. The growing popularity of Asian cuisine globally, along with rising demand for artisanal and organic food products, is further boosting the adoption of brewed soy sauce in both domestic and international markets.

By Format: Powdered Soy Sauce Gains in Food Manufacturing

Liquid soy sauce was the most popular product in the global soy sauce market in 2025, accounting for 87.51% of the market share. Its widespread use is due to its convenience and ability to enhance the flavor of various dishes. It is commonly used as a seasoning, marinade, or dipping sauce, especially in Asian cuisines and ready-to-eat meals. The product’s easy availability in retail stores and foodservice outlets has further strengthened its position as the market leader. Its versatility makes it a staple in both home kitchens and commercial food production.

Powdered soy sauce is expected to grow steadily during the forecast period, with a projected CAGR of 5.13% through 2031. This growth is driven by the increasing demand for food ingredients that are easy to use and have a longer shelf life. Powdered soy sauce is widely used in packaged snacks, instant noodles, seasoning mixes, and processed foods due to its durability and ease of transportation. It also provides a consistent flavor, making it a preferred choice for food manufacturers. As the demand for convenience foods continues to rise and innovation in dry seasoning products advances, the powdered soy sauce segment is likely to experience sustained growth in the coming years.

By Packaging Type: Pouches and Sachets Capture Convenience Demand

In 2025, glass and PET bottles held the largest share of the global soy sauce packaging market, contributing 51.07% of total sales. This is mainly because these packaging types are durable, easy to handle, and widely preferred by consumers for retail and foodservice use. Glass bottles are particularly popular for premium and traditionally brewed soy sauce, as they help preserve the product's flavor and quality. PET bottles, on the other hand, are lightweight, cost-effective, and convenient for transportation. The availability of these bottled products in supermarkets, convenience stores, and online platforms has further strengthened their market dominance.

Pouches and sachets are expected to grow at the fastest rate during the forecast period, with a projected CAGR of 5.36% from 2026 to 2031. The rising demand for convenient, portable, and single-use packaging is driving its popularity among households and consumers who prefer on-the-go options. These packaging formats are also gaining traction among foodservice providers and takeaway businesses due to their lower costs and reduced storage needs. Furthermore, advancements in flexible, eco-friendly packaging materials are expected to support the growing adoption of pouches and sachets worldwide.

By End Use: Food Processing Outpaces Retail and Foodservice

In 2025, retail channels accounted for the largest share of the global soy sauce market, contributing 43.18% of the total market revenue. This dominance is mainly due to the high consumer demand for soy sauce through supermarkets, hypermarkets, convenience stores, and online platforms. More people are cooking Asian dishes at home and experimenting with new recipes, boosting retail sales. Additionally, the availability of various soy sauce options, promotional campaigns, private-label products, and the growing use of e-commerce have further strengthened the retail segment's position in the market.

On the other hand, the industrial segment is projected to grow the fastest during the forecast period, with a CAGR of 6.25% through 2031. Food manufacturers are increasingly using soy sauce as a key ingredient in processed foods, ready-to-eat meals, instant noodles, snacks, and frozen products. The growth of the food processing industry and the rising need for bulk and standardized ingredient supplies are driving this demand. Furthermore, the growing popularity of Asian-inspired packaged foods and convenience products is expected to create significant growth opportunities for industrial soy sauce use in the coming years.

Geography Analysis

Asia-Pacific was the largest contributor to the global soy sauce market in 2025, accounting for 58.11% of total sales. This dominance stems from the frequent use of soy sauce in daily meals across countries such as China, Japan, and South Korea, where it is a key ingredient in traditional dishes. In Japan, consumers are increasingly seeking premium soy sauce made using traditional brewing and aging methods. Meanwhile, China drives significant demand through its large-scale consumption of mass-market soy sauce products. Additionally, rising incomes and urbanization in Southeast Asia are expanding the consumer base and supporting market growth in the region.

North America is expected to grow the fastest during the forecast period, with a CAGR of 6.41% from 2026 to 2031. The growing popularity of Asian cuisines and the increasing shift toward plant-based diets are major factors driving this growth. Soy sauce is also becoming a common ingredient in home cooking and meal-kit solutions, appealing to a broader audience. Changing food preferences among diverse populations are further helping the market expand beyond traditional Asian households. Investments in local production facilities and supply chain improvements are expected to enhance product availability and drive future growth in the region.

Europe is experiencing steady growth, driven by rising demand for clean-label, naturally brewed, and premium soy sauce products. Countries like the UK, Germany, and France are leading this trend as consumers show more interest in authentic international flavors and healthier condiment options. In South America and the Middle East & Africa, the market is gradually expanding due to the increasing popularity of Asian food products and condiments. Efforts to localize production, expand retail distribution, and invest in regional manufacturing are expected to create long-term growth opportunities in these emerging markets.

Competitive Landscape

The soy sauce market is moderately consolidated, with a few key players including Foshan Haitian Flavoring & Food, Kikkoman Corporation, Lee Kum Kee Co. Ltd., Yamasa Corporation, and Pearl River Bridge. These companies hold strong positions due to their wide distribution networks, diverse product offerings, and well-established brand reputations in both local and international markets. To ensure long-term growth, they are focusing on increasing production capacity, improving supply chain efficiency, and adopting advanced automation technologies. Their ability to serve both premium and budget-friendly market segments gives them a global competitive edge.

Many companies in the soy sauce market are expanding internationally and adopting vertical integration strategies to secure raw materials and streamline operations. By establishing manufacturing facilities and production hubs across different regions, they aim to reduce logistics costs, improve product availability, and strengthen their presence in fast-growing markets. Additionally, some players are diversifying into related categories, such as food ingredients and seasonings, to create synergies and broaden their revenue streams. These strategies are helping major manufacturers adapt to changing consumer preferences and enhance profitability across regions.

Smaller and artisanal soy sauce brands are gaining attention by offering premium products made with traditional brewing methods, organic ingredients, and unique flavors. The growth of e-commerce and specialty food stores has allowed these brands to reach a wider audience looking for authentic and high-quality condiments. However, strict food safety regulations and quality standards often favor larger companies with better resources for research and compliance. Despite this, emerging brands are finding opportunities through contract manufacturing and third-party fermentation services, which are reducing entry barriers and gradually reshaping the competitive landscape.

Soy Sauce Industry Leaders

-

Foshan Haitian Flavouring & Food Co., Ltd.

-

Kikkoman Corporation

-

Lee Kum Kee Company Limited

-

Yamasa Corporation

-

Guangdong Pearl River Bridge Food Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Kikkoman Corporation launched special soy sauce bottles with designs inspired by anime and Japanese culture. These limited-edition bottles feature manga-style artwork, cherry blossoms, and traditional Japanese themes to attract younger consumers and fans of Japanese culture.

- September 2025: HEYDOH introduced a premium soy sauce range made from single-origin ingredients, aiming to position soy sauce as a high-quality pantry item like artisanal olive oil. The range uses top-quality black soybeans and traditional brewing methods, and offers variants designed for cooking and finishing.

- February 2025: SoyOry launched a specialty soy sauce with green chile and cedar notes. Marketed as a finishing sauce, it appeals to consumers seeking unique, bold flavors and artisanal condiments, contributing to the fusion and premiumization trends in soy sauces.

- January 2025: Kikkoman Foods Inc. launched nine soy sauce products, including traditionally brewed soy sauce and an Umami Joy Sauce alternative, which received vegan certification. This move targets health-conscious and plant-based consumers, reinforcing Kikkoman’s presence in North America’s growing vegan market segment.

Global Soy Sauce Market Report Scope

Soy sauce is a liquid seasoning made through fermentation, using soybeans, wheat, salt, and water. It is commonly used to add flavor to various dishes and cooking preparations. The global soy sauce market is segmented into product type, format, packaging type, end use, and geography. Based on product type, the market is classified into brewed and blended. Based on format, the market is classified into liquid and powdered. Based on end use, the market is classified into food processing/industrial, foodservice/HoReCa, and retail. Based on geography, the market is classified into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The market forecasts are provided in terms of USD (value).

| Brewed |

| Blended (Chemically Hydrolyzed/Partially Fermented) |

| Liquid |

| Powdered |

| Glass/PET Bottles |

| Bulk Containers |

| Pouches/Sachets |

| Food Processing/Industrial | |

| Foodservice/HoReCa | |

| Retail | Supermarkets/Hypermarkets |

| Convenience/Grocery Stores | |

| Online Retail Stores | |

| Other Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Brewed | |

| Blended (Chemically Hydrolyzed/Partially Fermented) | ||

| By Format | Liquid | |

| Powdered | ||

| By Packaging Type | Glass/PET Bottles | |

| Bulk Containers | ||

| Pouches/Sachets | ||

| By End Use | Food Processing/Industrial | |

| Foodservice/HoReCa | ||

| Retail | Supermarkets/Hypermarkets | |

| Convenience/Grocery Stores | ||

| Online Retail Stores | ||

| Other Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the global soy sauce market?

The market is valued at USD 61.96 billion in 2026, reflecting steady growth from 2025 levels.

How fast is the soy sauce market expected to grow?

It is projected to expand at a 4.78% CAGR between 2026 and 2031.

Which region is forecast to post the highest growth rate?

North America is anticipated to record the fastest regional CAGR of 6.41% from 2026 to 2031, fueled by the growing popularity of meal kits and plant-based foods.

Why are powdered soy sauce formats gaining traction?

Spray-dried powders cut freight weight and enable precise dosing in snacks and dry mixes, supporting a 5.13% CAGR to 2031.

Page last updated on: