Soy Protein Isolate Market Size and Share

Market Overview

| Study Period | 2026 - 2031 |

|---|---|

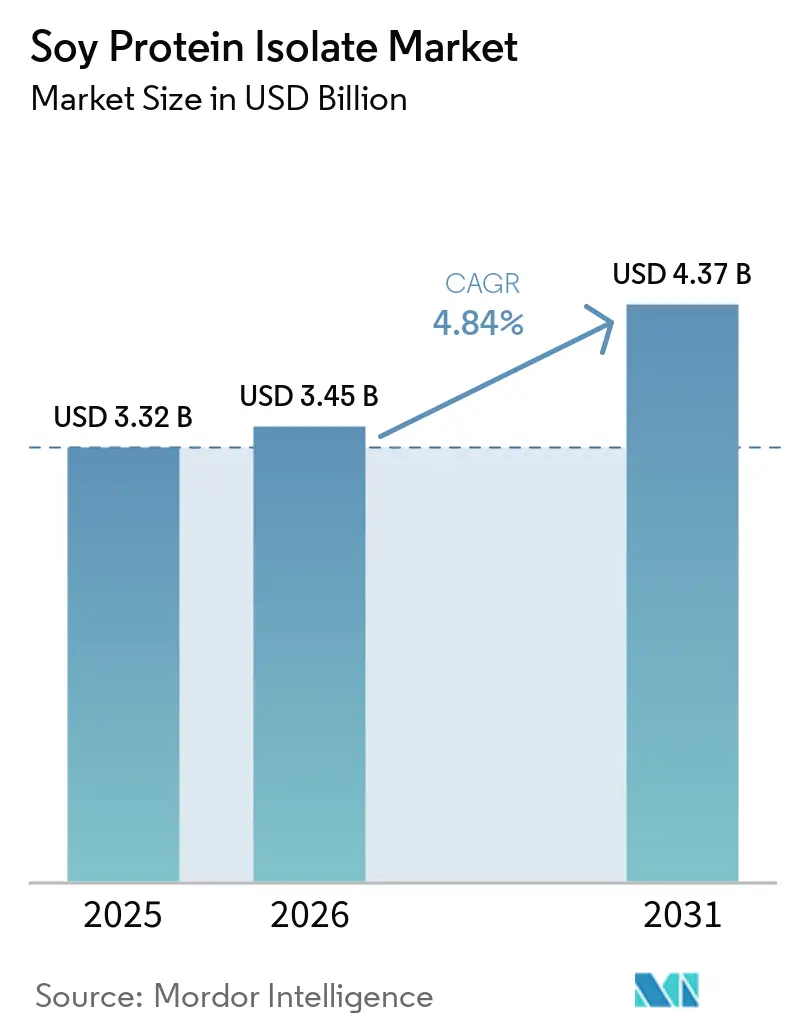

| Market Size (2026) | USD 3.45 Billion |

| Market Size (2031) | USD 4.37 Billion |

| Growth Rate (2026 - 2031) | 4.84% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Soy Protein Isolate Market Analysis by Mordor Intelligence

The soy protein isolate market size is expected to increase from USD 3.32 billion in 2025 to USD 3.45 billion in 2026 and reach USD 4.37 billion by 2031, growing at a CAGR of 4.84% over 2026-2031. This growth trajectory reflects the accelerating shift toward plant-based nutrition solutions driven by health consciousness, environmental sustainability concerns, and regulatory support for alternative protein sources. The market's expansion is particularly pronounced in developed economies where consumers increasingly prioritize functional nutrition and clean-label ingredients, while emerging markets demonstrate growing adoption of protein fortification in traditional food systems. The FDA's introduction of the Animal Food Ingredient Consultation program in 2024 has streamlined regulatory pathways, particularly benefiting companies developing novel protein applications for both human nutrition and animal feed sectors[1]Source: U.S Food and Drug Administration, "FDA Enforcement Policy for AAFCO-Defined Animal Feed Ingredients", fda.gov. Soy protein isolate is valued for its high protein content with minimal carbohydrates and fats, making it a popular ingredient in meat alternatives, dairy substitutes, nutritional supplements, and sports nutrition products. In summary, the soy protein isolate market is expanding steadily worldwide, driven by health and sustainability trends, regional demand variations, and increasing adoption in diverse food and beverage products.

Key Report Takeaways

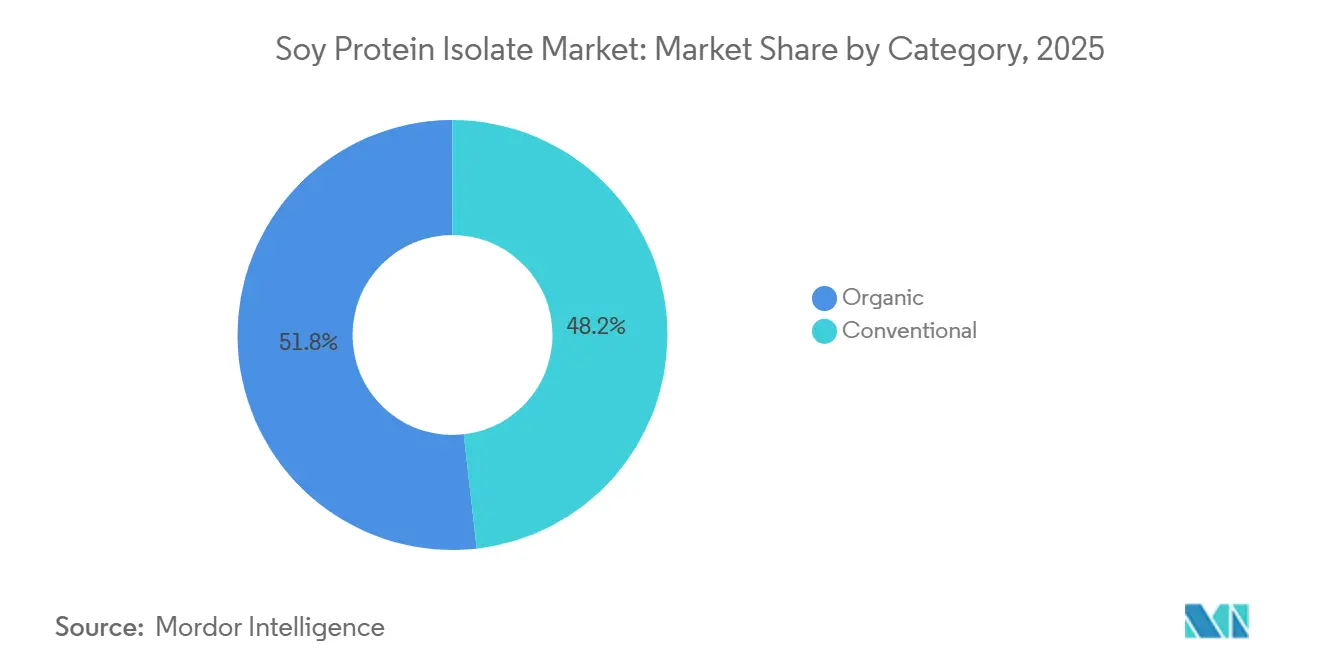

- By category, conventional grade held 77.12% of the soy protein isolate market share in 2025, whereas organic variants are projected to expand at an 8.03% CAGR through 2031.

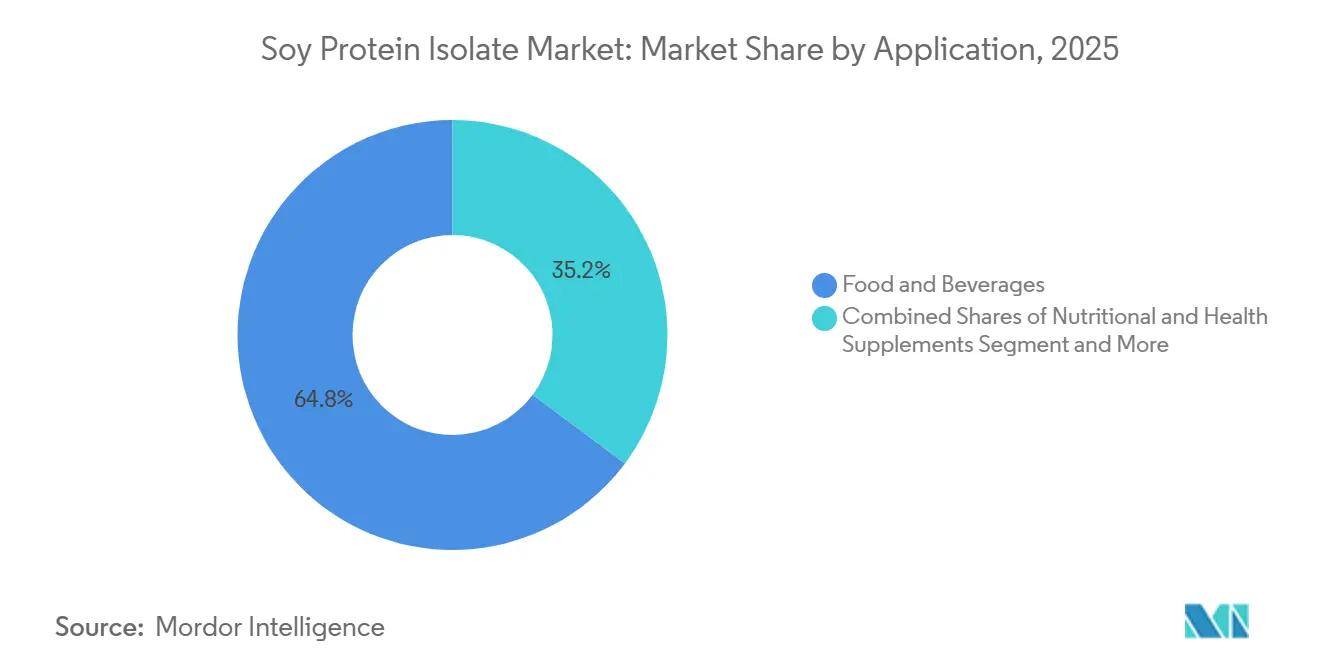

- By application, food and beverages captured 64.81% of the soy protein isolate market in 2025, while nutritional and health supplements are forecast to post a 7.95% CAGR over 2026-2031.

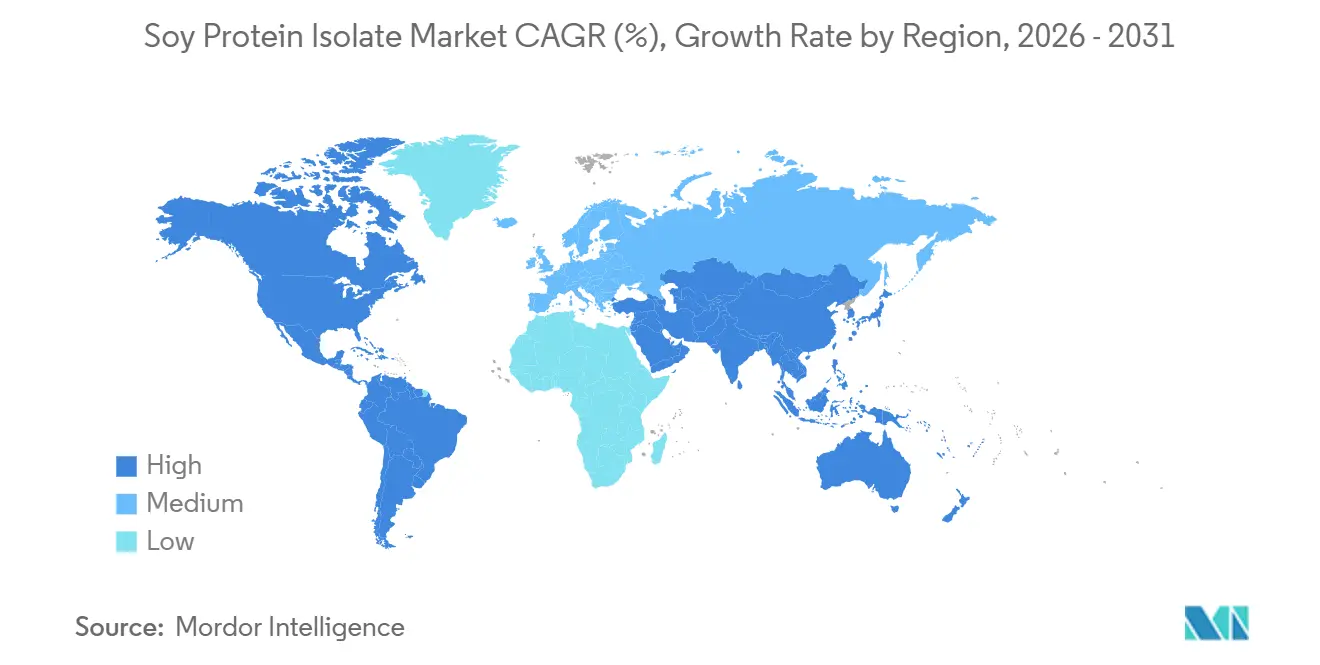

- By geography, North America led with 33.40% revenue contribution in 2025, yet Asia-Pacific is set to register the fastest regional growth at a 7.58% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Soy Protein Isolate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for plant-based proteins in mainstream food and beverages | +1.2% | Global, with North America and Europe leading retail penetration, Asia-Pacific emerging in foodservice | Medium term (2-4 years) |

| Accelerating uptake in meat-alternative formulations | +0.9% | North America and Europe core markets; Asia-Pacific adoption is accelerating in urban centers (China, Singapore, India) | Short term (≤ 2 years) |

| Functional advantages in sports and active nutrition | +0.7% | North America, Europe, and Australia/New Zealand; Asia-Pacific growth in premium urban segments | Medium term (2-4 years) |

| Expansion of soy-based ingredients in emerging Asian markets | +1.1% | Asia-Pacific core (China, India, Thailand, Indonesia); spillover to the Middle East and Africa | Long term (≥ 4 years) |

| Commercialization of low-allergen, non-GMO Identity Preserved soy isolates | +0.5% | North America and Europe (clean-label demand); Japan and South Korea (non-GMO preference) | Long term (≥ 4 years) |

| Extrusion and micro-encapsulation tech improving texture and mouthfeel | +0.6% | Global, with innovation hubs in North America, Europe, and Japan; technology transfer to Asia-Pacific manufacturers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Plant-Based Proteins in Mainstream Food and Beverages

Flexitarian diets are pushing plant proteins into the mainstream, with soy protein isolate making inroads into areas once dominated by dairy. By 2025, plant-based foods accounted for 13% of total protein sales in North America. This shift came as mainstream brands reformulated their products, incorporating soy isolates to cut costs and reduce carbon footprints, as highlighted by the Good Food Institute in 2024[2]Source: Good Food Institute, “2024 State of the Industry: Plant-Based Proteins,” gfi.org. In January 2026, Califia Farms introduced its Simple and Organic Soymilk, boasting just three ingredients: organic soybeans, water, and sea salt. With 8 grams of protein per serving, it's positioned to rival dairy milk in protein content while offering a more economical choice than almond and oat alternatives. This evolution is prompting beverage formulators to adjust their procurement strategies, recognizing that soy isolates provide a complete amino acid profile and boast a carbon footprint 7 to 70 times lighter than their animal protein counterparts, based on life-cycle assessments from IFF. Regulatory shifts are bolstering this momentum; while the FDA has broadened its GRAS notices for plant proteins to encompass pea, chickpea, and fava bean isolates, soy's decades of safety data and well-established supply chains grant it a distinct first-mover edge.

Accelerating Uptake in Meat-Alternative Formulations

After first-generation pea-protein burgers fell short on texture and binding, meat analog manufacturers have turned to soy protein isolate as their primary structural protein. In 2026, Rival Foods, in collaboration with THIS, introduced a plant-based steak to the UK market. Utilizing Shear Cell technology, they crafted fibers boasting 30 grams of protein per 100 grams, surpassing beef's protein density. Notably, this was achieved without artificial binders, and the product is now stocked in major retailers like Tesco, Waitrose, Sainsbury's, Morrisons, and Ocado. This move signifies a strategic shift: although the product description omits a mention of soy isolate, its protein density and clean-label stance resonate with high-purity isolate formulations. Such formulations empower manufacturers to champion "no artificial additives" claims while still achieving a meat-like texture. In 2025, Tyson Foods made a quiet yet significant move, investing in five plant-protein startups. Among these was a precision agriculture firm focused on enhancing pea and soy protein yields for food-grade uses. This investment underscores a notable trend: even processors traditionally centered on beef are now diversifying, eyeing the legume protein supply chains. Tyson's foray into upstream agronomy hints at a strategic foresight: an anticipation of tightening supplies or potential quality fluctuations in soy isolates as demand continues to rise. A key player in this evolution is extrusion technology. DSM-Firmenich's Vertis texturized vegetable proteins, leveraging the ModulaSENSE flavor-masking platform, have pushed the envelope. They've enabled soy isolate inclusion rates exceeding 20% in whole-muscle analogs, all without the dreaded off-notes.

Functional Advantages in Sports and Active Nutrition

Sports nutrition brands are turning to soy protein isolate to meet clean-label demands while ensuring muscle-protein synthesis rates match those of whey. In March 2026, IFF's Supro soy protein isolate earned a heart-health endorsement in Australia and New Zealand. This recognition stems from studies indicating that a daily intake of 20 to 25 grams can enhance blood lipid profiles. This positions soy as a dual-benefit ingredient, promoting both cardiovascular and muscle health. This regulatory achievement holds strategic weight: it empowers ready-to-drink (RTD) protein beverages and nutrition bars to tout structure-function claims, sidestepping the allergen concerns tied to dairy. This opens up valuable shelf space in mainstream grocery and convenience outlets. Clinical research underscores that Supro, when taken post-exercise, rivals whey protein in boosting muscle gains and strength, all while boasting a significantly lower environmental footprint. But the benefits of soy isolates aren't limited to protein quality. They also offer emulsification and fat-binding traits, enhancing mouthfeel in low-fat products and minimizing the need for additional gums or stabilizers. In 2025, West Life rolled out 16-gram protein smoothie blends, boasting shelf stability and non-GMO verification. These blends found their way to shelves at Whole Foods, ShopRite, Walmart, and Amazon. As an estimated 68% of the global population grapples with lactose intolerance, the allure of clean-label, allergen-friendly, and performance-equivalent products is steering sports nutrition formulators away from whey concentrates. A 2025 survey by the International Food Information Council revealed that 42% of consumers prioritized allergen concerns in food safety[3]Source: International Food Information Council, “2025 Food & Health Survey,” ific.org . Yet, mentions of soy allergens were notably sparse, with only four instances. This indicates that soy's allergen profile poses fewer commercial challenges compared to the widespread issues of lactose intolerance in dairy.

Expansion of Soy-Based Ingredients in Emerging Asian Markets

Chinese and Indian manufacturers are ramping up their soy protein isolate production, aiming to cater to their growing flexitarian populations and to seize a larger export share from North American suppliers. Yuwang Group boasts a soybean processing capacity of 600,000 metric tons, allocating 130,000 metric tons for soy protein isolate and another 20,000 metric tons for texturized vegetable protein. With FDA and BRC certifications, Yuwang exports to over 60 countries. Recognized as a National Green Factory in 2018, Yuwang also chairs the China Soy Protein Association, underscoring its pivotal role in the nation's push for protein self-sufficiency, a move seemingly backed by the government. Xinrui Group, a veteran in soy protein production with over 23 years of experience, showcased its offerings at Vitafoods Asia 2025. The group holds a suite of certifications including ISO 9001, ISO 22000, HACCP, Halal, and Kosher, strategically targeting Middle Eastern and Southeast Asian markets where Halal compliance is paramount. In India, Epic Powder is carving a niche as a production hub. They've adopted air classification and micronization technology for soy protein isolate production, achieving a 30% reduction in energy consumption compared to traditional wet extraction methods. Meanwhile, Fuji Oil reported net sales of YEN 35.5 billion (around USD 240 million) for soy-based ingredients in fiscal year 2023. With 83% of their soybeans traceable to primary collection points and being a member of RTRS since 2020, Fuji is well-positioned to align with the European Union's Deforestation Regulation requirements. The overarching trend indicates a shift in the global supply landscape: Asian producers are not just competing on price anymore. They're making significant investments in certifications and traceability, aiming for premium market access. This strategy is tightening the margins for North American suppliers, who have traditionally enjoyed premium pricing for their non-GMO and organic claims.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Soy-allergen labeling and consumer perception challenges | -0.3% | Global, with heightened sensitivity in North America and Europe due to allergen-labeling regulations | Short term (≤ 2 years) |

| Soybean price and supply-chain volatility | -0.8% | Global, with acute impact in import-dependent regions (Europe, the Middle East, parts of Asia); South American weather events drive volatility | Short term (≤ 2 years) |

| Deforestation/sustainability scrutiny on soy sourcing | -0.5% | Europe (EUDR compliance), North America (corporate ESG mandates), spillover to Asia-Pacific as multinational buyers enforce standards | Medium term (2-4 years) |

| Off-flavor at high inclusion rates, limiting application levels | -0.4% | Global, particularly affecting meat alternatives and high-protein beverages, where soy isolate inclusion exceeds 15% | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Soy-Allergen Labeling and Consumer Perception Challenges

Despite soy's low clinical prevalence, some formulators view allergen labeling requirements as a marketing liability. The FDA's FALCPA mandates that soy, recognized as a major allergen, be plainly listed immediately after or within the ingredient list. Similarly, the EU's Food Information to Consumers Regulation emphasizes the need for typographical prominence. Manufacturers, adhering to the EU's 2026 allergen management requirements, must adopt comprehensive allergen management programs. These include physical line segregation, validated cleaning protocols, employee training, and thorough documentation. Failure to manage these controls can lead to recalls, fines, and significant reputational harm. Notably, while allergen concerns topped food-safety worries at 42% in a 2025 survey by the International Food Information Council, soy was mentioned only 4 times. This underscores a minimal consumer perception of soy as an allergen, especially when juxtaposed with concerns over peanuts, tree nuts, and shellfish. Strategically, while allergen labeling poses a compliance cost, it doesn't constrain demand. However, it does create a perception gap: some brands, aiming to sidestep allergen declarations, are shifting from soy isolates to pea or rice proteins. Yet, this comes with a caveat: achieving the same functionality with pea proteins demands higher inclusion rates. Consequently, the market is splitting: cost-sensitive formulators are accommodating allergen labeling, while premium brands, at a higher ingredient cost, are chasing an allergen-free image.

Soybean Price and Supply-Chain Volatility

In 2026, soy protein isolate prices ranged from USD 2,800 to USD 4,200 per metric ton, driven by soybean futures volatility linked to South American weather and U.S.-China trade dynamics. Brazil's 2025/26 soybean harvest reached a record 177–178 million metric tons, temporarily easing crush margins. However, global stocks tightened as the U.S. Renewable Fuel Standard increased biodiesel blending, reducing meal availability for protein extraction, according to USDA reports. Rising soybean oil prices incentivized crushers to prioritize oil extraction, compressing soy protein isolate supply despite increased raw bean availability. U.S.-China trade tensions further amplified volatility, redirecting South American beans to China and tightening supplies for North American and European crushers, who faced higher costs for premium non-GMO and Identity Preserved beans. Production costs for soy protein isolate ranged from USD 1,900 to USD 3,000 per metric ton, with raw material costs accounting for 60–75% of finished isolate costs. This cost sensitivity made isolate pricing highly responsive to soybean futures, compressing margins for food manufacturers unable to pass on price increases. In response, companies like Archer Daniels Midland pursued vertical integration, completing a USD 300 million expansion of its Decatur, Illinois facility in Q1 2025 to consolidate crush and protein extraction, capturing margins across the value chain.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Category: Organic Premiums Drive Niche Growth

In 2025, conventional soy protein isolate held 77.12% market share due to cost advantages and established supply chains. Organic soy protein isolate is projected to grow at 8.03% annually from 2026 to 2031, driven by clean-label mandates and retailer sustainability goals. Organic certification, requiring compliance with USDA or EU standards, prohibits synthetic pesticides, GMOs, and irradiation, reducing yields by 20–30% and increasing raw soybean costs by 30–50%. At the isolate level, smaller processing runs, dedicated equipment, and certification audits raise organic isolate prices 40–60% above conventional ones. Despite this, organic isolates are gaining traction in premium segments like sports nutrition, infant formula, and plant-based meats. Califia Farms' Simple and Organic Soymilk, launched in January 2026 at USD 5.99–6.99, highlights the premium potential of organic products in retail.

Conventional isolates dominate animal feed, commodity bakery, and processed meat applications, where the cost per gram of protein is critical. Bunge's BungePurePro Soy 70N family, with 69% protein, targets cost-sensitive aquaculture feed formulators prioritizing digestibility and anti-nutritional factor removal. Prairie AquaTech's ME-PRO, a fermented soybean protein powder with 73.4% crude protein, is available in GMO and non-GMO variants, showing segmentation within conventional isolates. The EU's Farm to Fork strategy, aiming for 25% organic farming by 2030, is expected to boost organic soybean supply and reduce premiums. Organic isolates are projected to capture 10–15% of market volume by 2031 as supply chains scale, while conventional isolates will continue dominating bulk applications prioritizing cost and functionality.

By Application: Nutritional Supplements Outpace Food and Beverages

In 2025, food and beverages accounted for 64.81% of soy protein isolate demand, driven by meat alternatives, dairy replacements, and baked goods. From 2026 to 2031, nutritional and health supplements are projected to grow at 7.95% annually, fueled by sports nutrition reformulations and rising infant formula demand in Asia. Meat and seafood alternatives are the fastest-growing sub-segment, supported by Rival Foods' partnership with THIS to launch plant-based steaks in UK supermarkets in 2026, offering 30 grams of protein per 100 grams. Dairy products and alternatives are adopting soy isolates to enhance protein density and reduce costs. OATSIDE introduced NOBO Soy in Singapore in March 2026, featuring 4.2 grams of protein per 100 milliliters from non-GMO soy. Bakery applications use soy isolates for dough conditioning and protein fortification but face off-flavor challenges above 10% inclusion rates. Snacks are a high-growth sub-segment, with Tyson Foods investing in a snack brand using pea, fava, and chickpea blends. Beverages, particularly RTD protein drinks, are reformulating with soy isolates to meet clean-label mandates; West Life's 16-gram protein smoothie blends are distributed through Whole Foods, Walmart, and Amazon.

Nutritional and health supplements are growing due to sports nutrition brands shifting from whey to soy for allergen-free and vegan markets, rising demand for soy-based infant formulas in China and India for lactose-intolerant infants, and elderly nutrition products targeting muscle maintenance. In March 2026, IFF's Supro soy protein isolate received a heart-health claim in Australia and New Zealand, enabling nutrition bars and RTD beverages to promote cardiovascular benefits. Stricter FDA regulations now require soy-based infant formulas to demonstrate amino acid bioavailability equivalent to breast milk, favoring soy isolates over concentrates due to higher protein purity. Elderly and medical nutrition products are adopting soy isolates for complete amino acid profiles in calorie-restricted diets to prevent sarcopenia. In animal feed, aquaculture demand for fishmeal substitutes is driving growth. Hamlet Protein's HP AquaSure improves hepatosomatic index and intestinal health in salmon and trout. The U.S. Soybean Export Council reports soy protein isolate can replace fishmeal at inclusion rates below 20% for carnivorous fish and above 50% for omnivorous species.

Geography Analysis

In 2025, North America held 33.40% of the soy protein isolate market, supported by the U.S.'s integrated crush-to-isolate infrastructure and Canada's non-GMO soybean production. However, margin compression persists as Asian manufacturers expand capacity and lower prices. Archer Daniels Midland invested USD 300 million in its Decatur, Illinois, facility to consolidate crush and protein extraction, but closed its Bushnell, Illinois, plant as part of a USD 500 to USD 700 million cost-cutting program targeting USD 200 to USD 300 million in annual savings. Bunge's USD 550 million Morristown facility, opened in autumn 2025, focuses on premium soy protein concentrate production. Mexico is emerging as a re-export hub, importing soy isolates from the U.S. and Canada for reformulation into foods for Latin American markets. The regulatory environment remains stable, with FDA GRAS status for soy proteins and IFF's March 2026 heart-health claim approval in Australia and New Zealand expected to influence Health Canada, opening opportunities for functional foods.

Asia-Pacific is projected to grow at 7.58% annually from 2026 to 2031, driven by capacity expansions in China and India, rising flexitarian consumption, and cost advantages in bulk isolate production. Yuwang Group processes 600,000 metric tons of soybeans, dedicating 130,000 metric tons to soy protein isolate, exporting to over 60 countries. Xinrui Group, with over 23 years in soy protein production and multiple certifications, targets Middle Eastern and Southeast Asian markets where Halal compliance is critical. Japan's Fuji Oil reported YEN 35.5 billion (USD 240 million) in soy-based ingredient sales in 2023, with 83% soybean traceability and RTRS membership since 2020, aligning with EU Deforestation Regulation requirements. India is scaling production with Epic Powder's energy-efficient air classification and micronization technology. Thailand, Indonesia, and South Korea import isolates from China and Japan for domestic manufacturing. Australia and New Zealand, though smaller markets, benefit from IFF's March 2026 heart-health claim approval, differentiating soy from pea and rice proteins.

Europe, South America, and the Middle East and Africa account for the remaining market share. Europe faces supply-chain restructuring due to EUDR compliance, which increases costs by 10 to 15%. Germany, France, and the UK lead consumption, driven by plant-based meat and dairy alternatives, while processors consolidate to manage traceability costs. In 2025, 54% of EU soy imports met FEFAC sustainability guidelines. Brazil and Argentina dominate South American production, exporting isolates to North America and Europe, while domestic consumption rises as local brands reformulate with soy proteins. ADM's 2021 acquisition of Sojaprotein in Serbia highlights the value of non-GMO production. The Middle East and Africa, as net importers, see demand led by the UAE, Saudi Arabia, and South Africa, with Halal and Kosher certifications favoring suppliers like Xinrui Group. Emerging markets such as Nigeria and Egypt are incorporating soy isolates into institutional foodservice and processed food manufacturing.

Competitive Landscape

The soy protein isolate market exhibits moderate concentration with established players leveraging vertical integration and processing scale to maintain competitive advantages. Market leaders focus on application-specific product development and strategic partnerships with food manufacturers to secure long-term supply relationships. ADM's sustainability initiatives, including greenhouse gas emission reductions of 14.7% in Scope 1+2 and expansion of regenerative agriculture programs across 2.8 million acres, demonstrate how companies are differentiating through environmental stewardship while maintaining operational efficiency.

The competitive landscape is increasingly shaped by technological innovation in processing methods and regulatory compliance capabilities, with companies investing in advanced extraction techniques and quality systems to meet evolving food safety standards. Emerging opportunities exist in specialized applications where functional performance requirements favor soy protein's established properties over newer alternatives. Leading global players such as Archer Daniels Midland (ADM), Bunge Global SA, Incorporated, and International Flavors & Fragrances Inc. dominate via strategies like extensive distribution networks, and strong research and development capabilities. These companies focus on ingredient innovation to enhance texture, nutritional quality, and clean-label appeal, catering to growing demand in sectors like meat alternatives, dairy replacements, sports nutrition, and functional foods.

The industry's moderate fragmentation creates acquisition opportunities for companies seeking to expand processing capacity or geographic reach, while also enabling smaller players to establish niche positions in premium segments like organic or specialty formulations. Patent activity in processing technologies and application-specific formulations indicates continued innovation investment, though the mature nature of basic soy protein isolation limits breakthrough opportunities compared to newer protein sources. Challenges such as raw material price volatility and GMO concerns prompt companies to differentiate through innovation, branding, and strategic partnerships. Overall, the SPI (Soy Protein Isolate) market is moderately concentrated among a few key players but is witnessing increasing competition and innovation driven by rising plant-based protein demand worldwide.

Soy Protein Isolate Industry Leaders

-

Archer Daniels Midland Company (ADM)

-

International Flavors & Fragrances Inc.

-

Bunge Global SA

-

Ocean Health Co., Ltd.

-

Mitsubishi International Food Ingredients, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Bunge completed its acquisition of International Flavors & Fragrances' soy protein concentrate, lecithin, and soy crush businesses, consolidating the Response, Alpha, Procon, and Solec brands under one portfolio for an undisclosed sum reported at USD 240 million in revenue

- January 2026: Califia Farms launched Simple and Organic Soymilk, featuring only three ingredients, including organic soybeans, water, and sea salt, with 8 grams of protein per serving, directly competing with dairy milk on protein density and undercutting almond and oat alternatives on cost per gram of protein.

- April 2025: Archer Daniels Midland completed a USD 300 million expansion of its Decatur, Illinois, facility, consolidating crush and protein extraction operations to improve efficiency and reduce costs as part of a broader USD 500 to USD 700 million cost-cutting program targeting USD 200 to USD 300 million in annual savings.

Global Soy Protein Isolate Market Report Scope

Soy protein isolate (SPI) is the most highly refined and purified form of soy protein available, containing at least 90% protein on a moisture-free basis. The global soy protein isolate market is segmented by category, application, and geography. By category, the market is segmented into conventional and organic. By application, the market is segmented into food and beverages, nutritional and health supplements, and animal feed. The food and beverages segment is further sub-segmented into bakery, snacks, dairy and dairy alternative products, seafood and meat alternative products, beverages, and other food applications. Similarly, the nutritional and health supplements segment is further sub-segmented into sport/performance nutrition, baby food and infant formula, and elderly nutrition and medical nutrition. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The Market Forecasts are Provided in Terms of Value (USD).

| Conventional |

| Organic |

| Food and Beverages | Bakery |

| Snacks | |

| Dairy and Dairy Alternative Products | |

| Seafood and Meat Alternative Products | |

| Beverages | |

| Other Food Applications | |

| Nutritional and Health Supplements | Sport/Performance Nutrition |

| Baby Food and Infant Formula | |

| Elderly Nutrition and Medical Nutrition | |

| Animal Feed |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Peru | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| Category | Conventional | |

| Organic | ||

| Application | Food and Beverages | Bakery |

| Snacks | ||

| Dairy and Dairy Alternative Products | ||

| Seafood and Meat Alternative Products | ||

| Beverages | ||

| Other Food Applications | ||

| Nutritional and Health Supplements | Sport/Performance Nutrition | |

| Baby Food and Infant Formula | ||

| Elderly Nutrition and Medical Nutrition | ||

| Animal Feed | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Peru | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How fast is the soy protein isolate market expected to grow through 2031?

The soy protein isolate market size is forecast to expand at a 4.84% CAGR from 2026 to 2031, reaching USD 4.37 billion by the end of the period.

Which region will post the highest growth in demand?

Asia-Pacific is projected to record the fastest regional CAGR at 7.58% to 2031, driven by Chinese and Indian capacity expansions and rising flexitarian diets.

What segment currently holds the largest soy protein isolate market share?

Conventional grade dominates with a 77.12% share in 2025, reflecting cost advantages in large-volume applications.

Which application area is expanding most rapidly?

Nutritional and health supplements are forecast to grow at a 7.95% CAGR as sports nutrition, infant formula, and elderly-nutrition products adopt soy isolates.

Page last updated on: