Lecithin Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

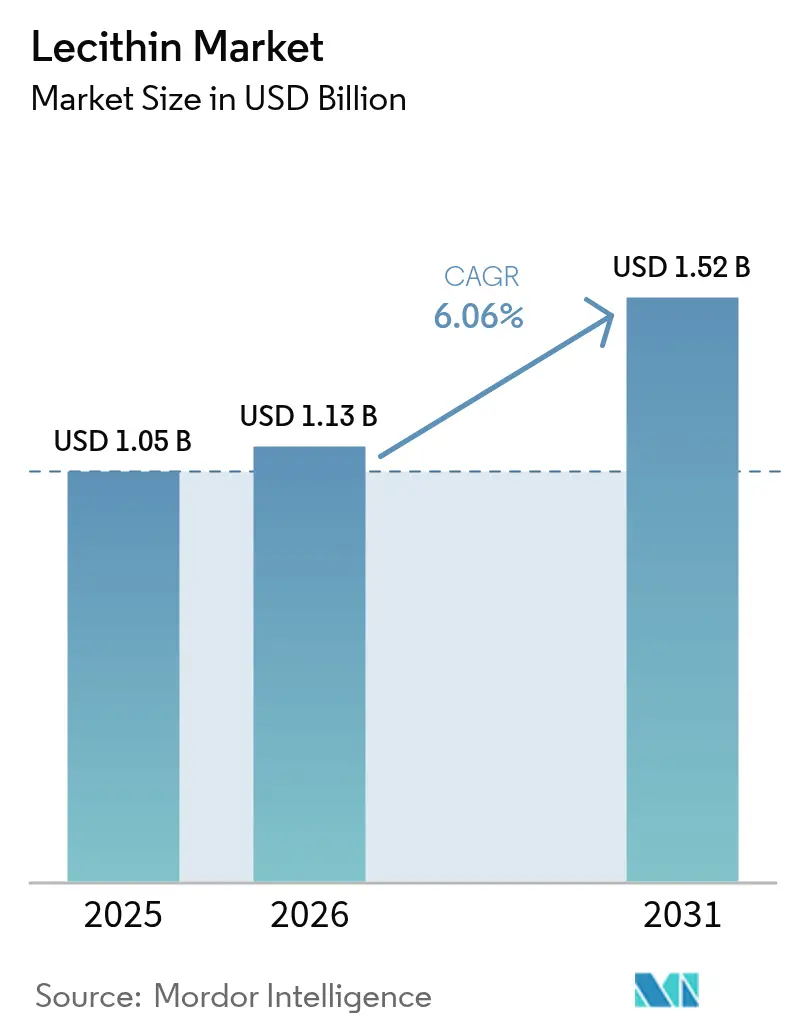

| Market Size (2026) | USD 1.13 Billion |

| Market Size (2031) | USD 1.52 Billion |

| Growth Rate (2026 - 2031) | 6.06% CAGR |

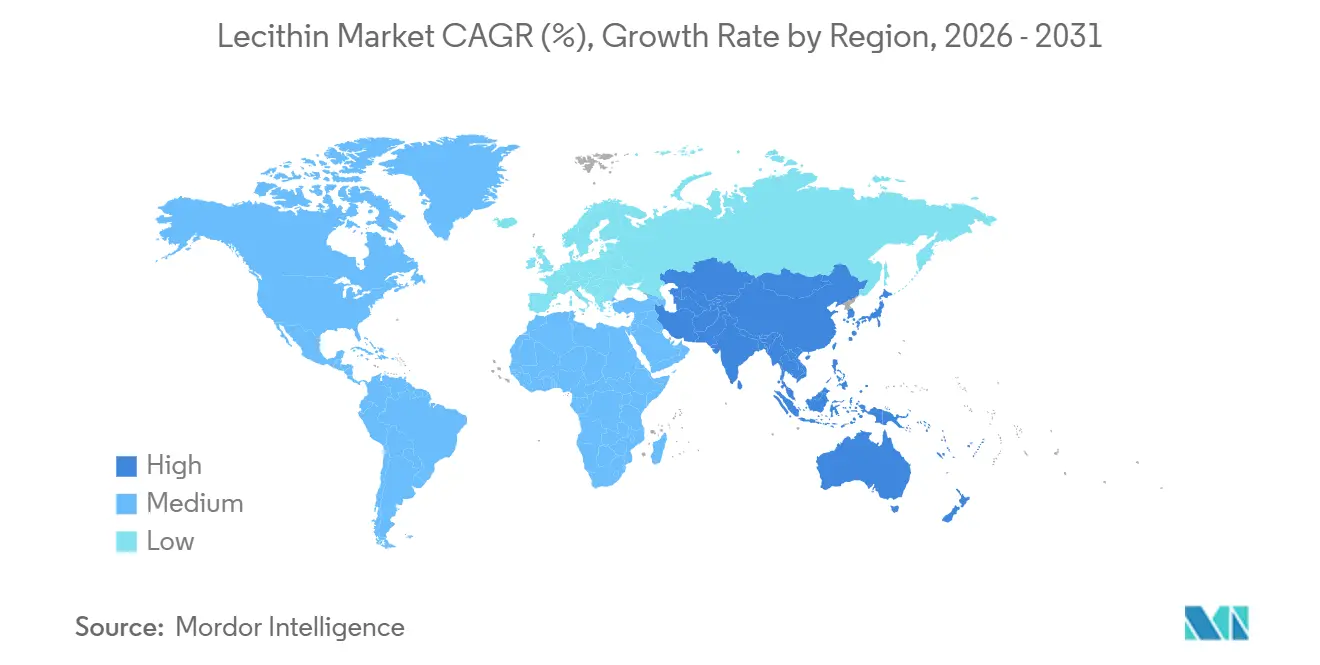

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

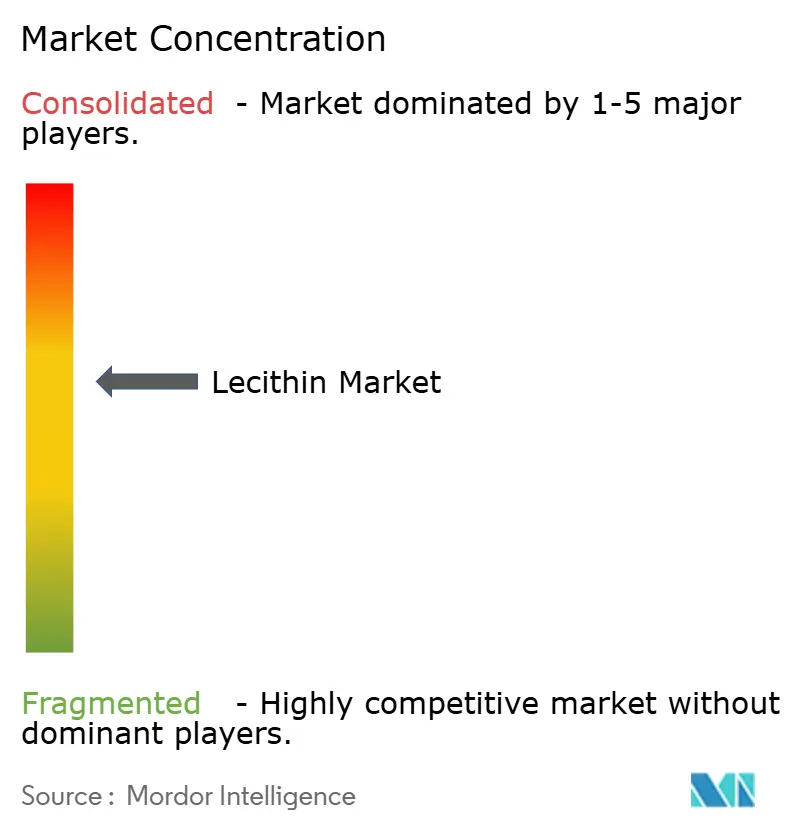

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Lecithin Market Analysis by Mordor Intelligence

The lecithin market size is expected to increase from USD 1.05 billion in 2025 to USD 1.13 billion in 2026 and reach USD 1.52 billion by 2031, growing at a CAGR of 6.06% over 2026-2031. Heightened demand for multifunctional emulsifiers that meet clean-label, allergen-free, and non-GMO requirements is reshaping product development across food, pharmaceutical, and personal-care value chains. Soy‐based ingredients still dominate the lecithin market, yet sustained growth in sunflower-derived alternatives shows that buyers are ready to pay premiums for products that simplify allergen management. Liquid formats remain popular because they integrate easily into continuous processes, although powders are gaining ground wherever supply chains face shelf-life or cold-chain constraints. Producers with vertically integrated crushing, refining, and specialty-ingredient operations are positioned to defend margins as raw-material volatility and competition from synthetic emulsifiers intensify.

Key Report Takeaways

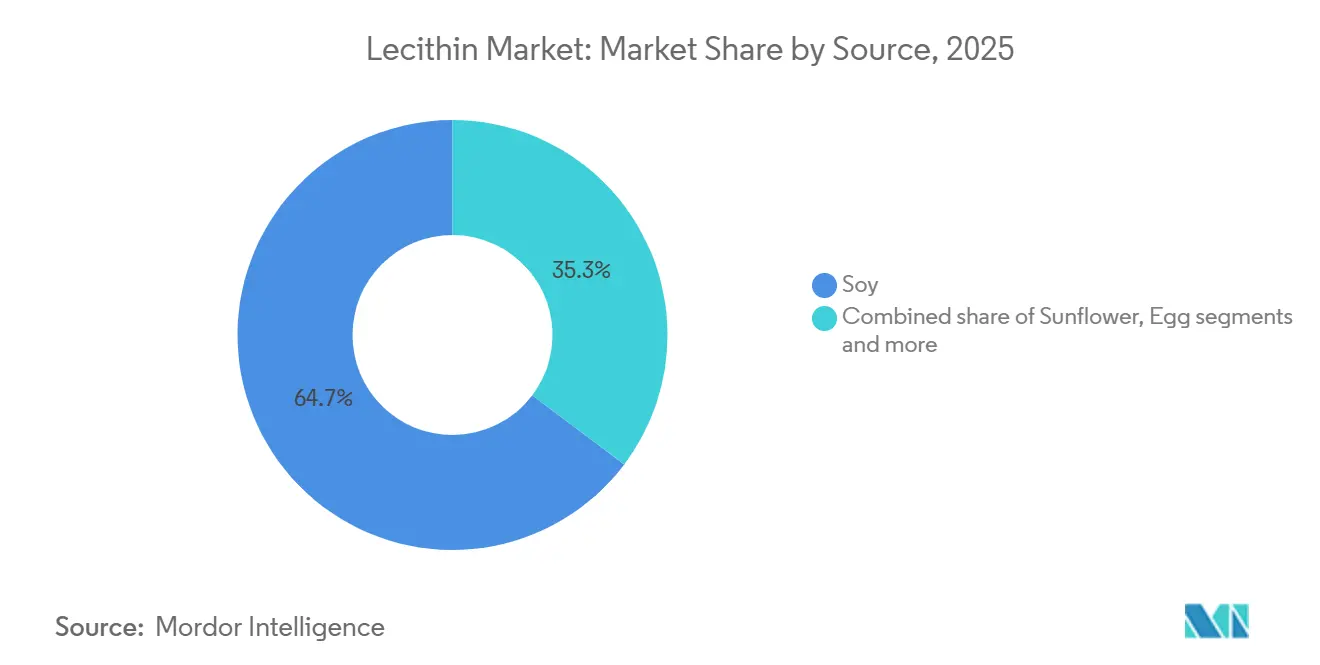

- By source, soy commanded 64.72% of the lecithin market share in 2025, while sunflower is forecast to post the fastest 7.61% CAGR through 2031.

- By grade, food-grade variants delivered 56.58% of 2025 revenue, but pharmaceutical-grade lecithin is advancing at an 8.91% CAGR to 2031.

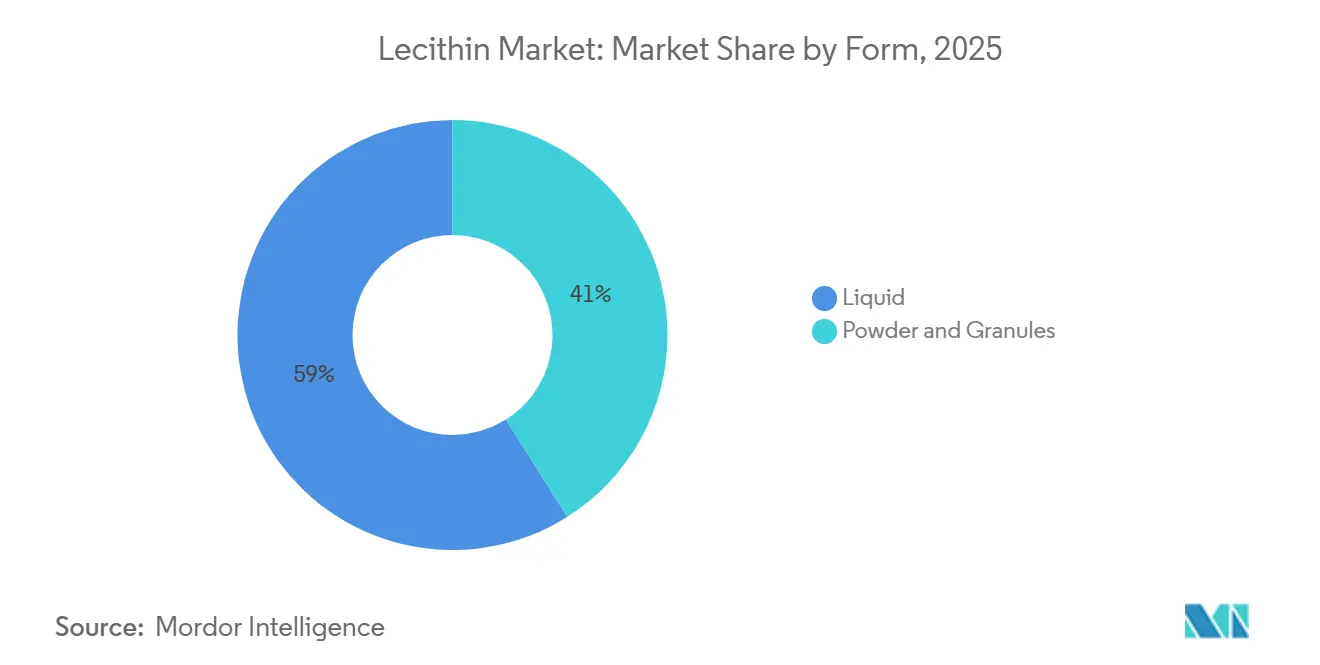

- By form, liquid formats captured 58.97% of volume in 2025; powder and granule formats trail in size yet are expanding at a 7.00% pace to 2031.

- By nature, conventional products held 82.69% of 2025 demand, whereas organic lecithin is moving ahead at an 8.60% CAGR through 2031.

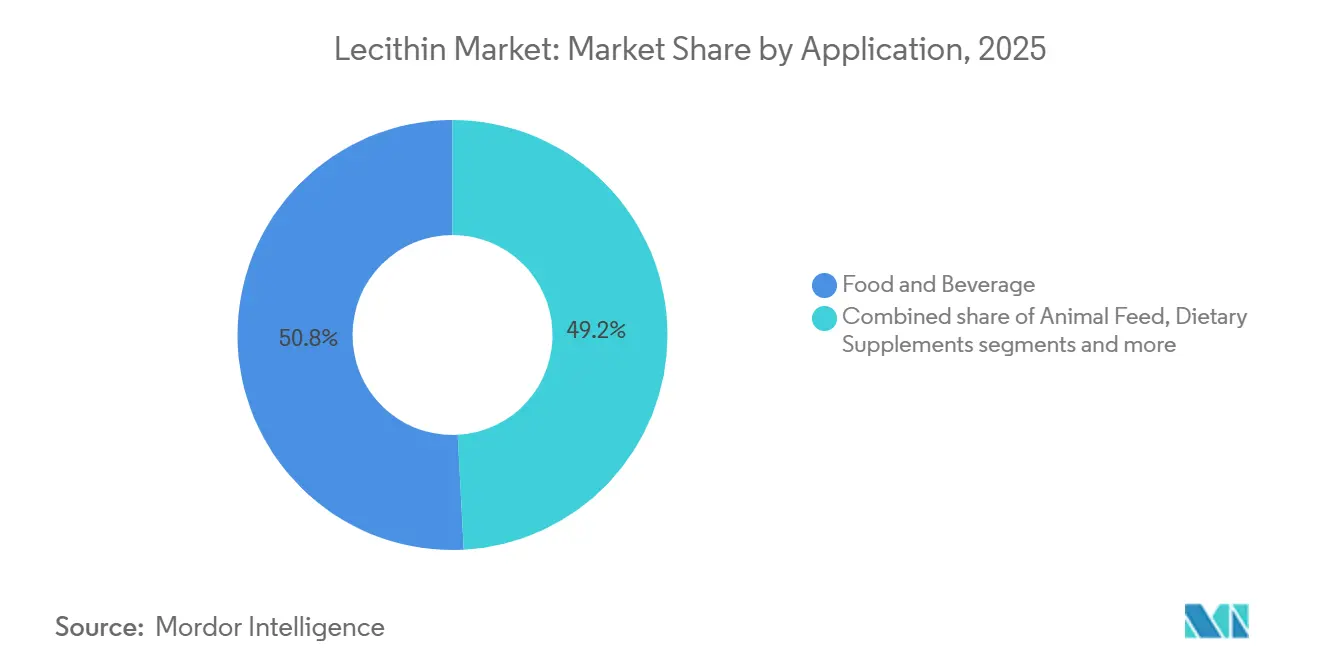

- By application, food and beverage accounted for 50.83% of 2025 consumption, and dietary-supplement use is growing at 8.67% through 2031.

- By geography, North America led with 35.15% revenue in 2025, while Asia-Pacific is projected to grow at 8.32% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Lecithin Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising need for emulsifiers and stabilizers in processed foods | +1.8% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Increased adoption in animal feed applications | +1.2% | Global, particularly strong in Asia-Pacific and South America | Long term (≥ 4 years) |

| Expanding applications in pharmaceutical and nutraceutical industries | +1.5% | North America and Europe leading, Asia-Pacific emerging | Long term (≥ 4 years) |

| Growing demand from plant-based and vegan food sectors | +0.9% | North America and Europe core, expanding to Asia-Pacific | Medium term (2-4 years) |

| Consumer demand for clean-label and natural food ingredients | +0.7% | Global, with premium markets leading adoption | Short term (≤ 2 years) |

| Increased adoption in natural cosmetics formulations | +0.4% | Europe and North America, expanding to Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising use of emulsifiers and stabilizers across processed and convenience foods

Consumer demand for quick, ready-to-eat options is driving the increased use of emulsifiers and stabilizers, such as lecithin, in processed and convenience foods. These ingredients play a critical role in improving texture, shelf life, and sensory appeal, aligning with shifting household spending patterns. For example, the average UK household spent GBP 70.50 per week on food and non-alcoholic drinks in FYE 2024, an 11% increase from GBP 63.50 in FYE 2023, according to the Department for Environment, Food & Rural Affairs [1]Source: Department for Environment, Food & Rural Affairs (DEFRA), "United Kingdom Food Security Digest 2025," gov.uk. This shift reflects tighter budgets prioritizing value-driven convenience over frequent home cooking. Leading manufacturers such as Cargill, with its Topcithin range for industrial emulsions, and ADM, offering soy-based lecithins for bakery and confectionery stabilization, are addressing this demand with clean-label solutions. These products ensure uniform fat dispersion in items like sauces and spreads without altering flavor profiles. Additionally, non-GMO sourcing from sunflower or soy aligns with regulatory requirements in Europe and North America for transparent labeling. This trend supports lecithin adoption, driven by Asia-Pacific's rapid processed food growth and global clean-label momentum.

Stronger penetration in animal nutrition and compound feed formulations

The increasing penetration of lecithin in animal nutrition and compound feed formulations is driving its adoption across livestock, poultry, and aquaculture diets. Lecithin’s natural emulsifying properties and phospholipid-rich profile enhance fat digestibility, nutrient absorption, and feed efficiency, making it a preferred ingredient in modern feed systems. Formulators in the competitive animal nutrition industry are under pressure to improve feed performance while meeting clean-label and sustainability requirements. This has led to rising demand for plant-derived lecithin from suppliers such as Louis Dreyfus Company, offering feed-grade lecithin, and Cefetra, known for soybean lecithin products tailored for animal feed. Lecithin supports energy utilization and improves palatability, aligning with compound feed producers’ objectives to optimize growth rates and herd health. Expanding industrial feed production capacity and a shift toward high-performance additive portfolios are further integrating lecithin into standard feed rations and specialized nutrition blends globally. Additionally, lecithin stabilizes fat-soluble vitamins and feed oils, ensuring product consistency and shelf life. Growing awareness among livestock producers about animal welfare and productivity benefits reinforces its adoption. The increasing integration of precision feeding and feed fortification strategies worldwide is expected to sustain strong demand growth for lecithin in the animal nutrition market.

Rapid expansion of demand from plant-based, vegan, and alternative protein foods

The increasing demand for plant-based, vegan, and alternative protein foods is driving the adoption of lecithin as a key ingredient in food formulations. Manufacturers are leveraging lecithin’s natural emulsifying and texturizing properties to enhance mouthfeel, stability, and sensory quality in products such as meat alternatives, dairy-free spreads, and plant-derived beverages. According to data from The Good Food Institute and the Plant Based Food Association, 6 in 10 or 59% of United States households purchased plant-based foods in 2024, prompting producers to focus on clean-label ingredients that perform effectively in complex plant matrices [2]Source: The Good Food Institute, "U.S. Retail Market Insights for the Plant-Based Industry," gfi.org. Leading ingredient manufacturers, including Cargill with its LECIPRIME, TOPCITHIN, EMULPUR, and EMULTOP product lines, are incorporating lecithin into plant-based burgers and vegan dressings to improve emulsification and shelf stability without compromising vegan standards. Lecithin’s ability to bind oil and water phases enhances texture, product release in cooked or frozen formats, and nutrient delivery in high-protein alternatives, aligning with consumer expectations for quality and sustainability. As plant-based food portfolios expand across retail and food service channels, the reliance on high-performance, non-animal emulsifiers like lecithin continues to grow, reinforcing its strategic importance in alternative protein formulations and driving broader market adoption.

Growing consumer preference for clean-label, non-GMO, and naturally sourced ingredients

Consumer demand for clean-label, non-GMO, and naturally sourced ingredients is reshaping the food and beverage industry, as shoppers increasingly prioritize transparency and healthfulness in product formulations. In 2024, data from the National Science Foundation indicates that over 76% of adults in the United Kingdom read food labels before purchasing, with 82% of individuals aged 18–34 doing so. Nearly 45% of consumers report paying more attention to labels compared to five years ago, while 70% focus on processing and ingredient information [3]Source: National Science Foundation (NSF), "NSF Research Reveals Brits Demand Greater Clarity, Transparency and Standardisation in Food Labelling", nsf.org. This shift has prompted manufacturers to replace synthetic emulsifiers with naturally or organically derived lecithin. Suppliers such as BungeMaxx, which now offers organic lecithins, and Clarkson Specialty Lecithins, known for its non-GMO, organic, and conventional soy and sunflower lecithin, are meeting this demand by emphasizing clean-label attributes. Clean-label positioning has become a competitive imperative, with formulators leveraging lecithin’s multifunctional properties, including emulsification, texture enhancement, and shelf-life stabilization, without compromising ingredient simplicity. By aligning with consumer expectations for minimal processing and transparency, lecithin enables brands to differentiate their products across categories such as baked goods and plant-based dairy alternatives. This alignment between consumer preferences and ingredient innovation is driving lecithin’s adoption, reinforcing its role in formulation strategies that prioritize natural sourcing and label clarity.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fluctuating Raw Material Prices | -1.4% | Global, with particular impact on cost-sensitive applications | Short term (≤ 2 years) |

| Negative consumer perception of GMO ingredients | -0.8% | Europe and North America primarily, expanding to Asia-Pacific | Medium term (2-4 years) |

| Competition from alternative emulsifiers and surfactants | -0.6% | Global, with synthetic alternatives in price-sensitive segments | Long term (≥ 4 years) |

| Limited shelf life of liquid lecithin products | -0.3% | Global, affecting distribution and inventory management | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in raw material availability and pricing

Volatility in raw material availability and pricing continues to challenge lecithin manufacturers, as production remains heavily dependent on oilseed crushing operations and is therefore susceptible to agricultural cycles, weather disruptions, and geopolitical events affecting key feedstocks like soybeans and rapeseed. The USDA reports that U.S. soybean stocks-to-use ratios have tightened for 2024-2025 due to droughts in critical Midwest growing regions, driving up soybean meal and oil prices and compressing lecithin extraction margins. This has forced ingredient manufacturers to operate within narrower profitability windows. Additionally, biofuel mandates in the United States, European Union, and Brazil divert significant quantities of soybean and rapeseed oil toward biodiesel production, limiting the crude oil available for lecithin extraction and exacerbating price volatility across food ingredient supply chains. Processors with limited vertical integration or hedging capabilities face acute margin pressures during periods of elevated oilseed costs, restricting their ability to invest in capacity expansion, product innovation, or long-term supply agreements. As energy policies and climate variability increasingly shape feedstock dynamics, raw material unpredictability remains a critical obstacle for manufacturers striving to balance costs, supply reliability, and global competitiveness.

Intense competition from alternative emulsifiers and multifunctional surfactants

Intense competition from alternative emulsifiers and multifunctional surfactants is reshaping the dynamics of the lecithin market. Ingredients such as mono- and diglycerides, polyglycerol esters, polysorbates, and sucrose esters offer distinct functional benefits, including higher emulsification efficiency at lower inclusion rates, superior heat stability, and neutral flavor profiles, making them highly attractive for complex formulations. Plant-based dairy and alternative protein producers are increasingly adopting precision-fermented emulsifiers and protein-polysaccharide complexes, which deliver comparable or superior texture at competitive costs, directly challenging lecithin's position in these segments. Synthetic emulsifiers, supported by decades of formulation expertise, regulatory approvals, and consistent supply chains, create switching costs for manufacturers hesitant to reformulate legacy products. Lecithin’s limitations, such as susceptibility to oxidation, batch-to-batch variability in phospholipid composition, and natural color contributions that may darken light-colored products, further open the door for competitors offering standardized, colorless, and oxidatively stable alternatives. While enzyme-modified and hydrolyzed lecithin variants address some of these issues, their higher costs and challenges with clean-label positioning limit adoption. To remain competitive in a rapidly evolving food and beverage sector, lecithin manufacturers must invest in research and development to develop high-purity, stable, and versatile formulations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Sunflower Gains as Allergen-Free Demand Accelerates

Soy lecithin held the largest share of the lecithin market in 2025, accounting for 64.72% of the total volume. Its dominance is attributed to robust soybean crush capacity, well-established supply chains, and cost advantages, making it the preferred emulsifier for price-sensitive applications such as animal feed, industrial coatings, and commodity bakery products. Despite the emergence of alternatives, soy lecithin remains a staple in large-scale food production due to its widespread availability and strong position among formulators. Meanwhile, sunflower lecithin is projected to grow at a 7.61% CAGR through 2031, driven by its allergen-free positioning, non-GMO certification, and neutral flavor. These attributes appeal to premium food, dietary supplement, and cosmetic formulators who prioritize ingredient transparency and clean-label simplicity. This shift aligns with increasing consumer demand for allergen-managed and "free from" ingredients, particularly in developed markets where ingredient scrutiny and third-party certifications influence purchasing decisions.

Rapeseed/canola lecithin occupies a niche yet stable position in regions like Canada and Northern Europe, valued for its balanced fatty acid profile and lower erucic acid content. However, its supply is constrained by regional canola harvest cycles and production variability. Egg lecithin, recognized for its high phosphatidylcholine content and superior emulsification performance, commands premium pricing and is favored in pharmaceuticals and cosmetics. Broader adoption is limited by cost, allergen concerns, and complex supply chains. Other sources, such as rice bran and corn lecithins, remain marginal due to lower phospholipid yields and limited extraction infrastructure. Regulatory requirements further shape the market, with USDA organic certification necessitating non-GMO seed sourcing and solvent-free extraction for soy and sunflower lecithin, while egg lecithin must meet strict pasteurization and allergen labeling standards. These factors continue to influence formulation strategies and compliance considerations across the lecithin market.

By Grade: Pharmaceutical Segment Outpaces Food on Liposome Momentum

In 2025, food-grade lecithin dominated global revenue, capturing 56.58% of the market share due to its extensive use in bakery, confectionery, dairy, beverage, and convenience food applications. Its key functionalities, such as emulsification, anti-staling, and texture modification, are essential for maintaining product quality and extending shelf life. Leading suppliers, including American Lecithin Company, offer tailored phospholipid profiles to address specific functional needs in complex food systems, ensuring consistent texture and moisture control. Consumer demand for enhanced sensory attributes in processed foods and efficient formulations continues to drive adoption. Additionally, compliance with stringent regulatory standards for safety and purity supports its widespread use across global supply chains. Industrial-grade lecithin complements this by serving non-food industries, such as paints, coatings, lubricants, and leather processing, where its emulsification and wetting properties are valued, albeit with less stringent regulatory requirements. This tiered grading system enables producers to maximize returns across diverse markets while meeting specific performance and compliance needs.

Pharmaceutical-grade lecithin is expected to grow at a strong 8.91% CAGR through 2031, fueled by its increasing use in lipid-based carriers like liposomes. These carriers improve bioavailability, reduce side effects, and enable targeted drug release. Producing high-purity lecithin for pharmaceutical applications requires adherence to stringent specifications, including low peroxide values, controlled heavy metal content, and defined phospholipid composition, which increases production complexity and costs compared to food and industrial grades. The rising demand for chronic disease therapies, driven by aging populations, and the adoption of liposomal formulations in oncology to enhance therapeutic outcomes further strengthen this segment. Additionally, vaccine developers increasingly utilize lipid nanoparticles (LNPs) incorporating high-quality lecithin fractions as stabilizing phospholipids, underscoring their importance in advanced biopharmaceutical applications. These factors collectively shape the market’s growth trajectory and influence supplier strategies.

By Form: Powder Formats Address Liquid Stability Challenges

Liquid lecithin held the largest share of the market in 2025, accounting for 58.97% of the global volume. Its widespread adoption in bakery, confectionery, and dairy industries stems from its ease of handling, rapid dispersion, and compatibility with continuous processing lines. The ability to emulsify instantly in both aqueous and oil phases makes it indispensable for applications like chocolate coatings, mayonnaise, and salad dressings, where additional hydration steps could disrupt production. Suppliers such as Stern-Wywiol Gruppe, through their SternLecithin® liquid portfolio, address industrial processing needs by offering standardized viscosity and phospholipid profiles. However, liquid lecithin faces challenges related to oxidation and microbial stability, particularly during long-distance transport and storage in warmer climates, influencing procurement strategies in export-driven supply chains.

Powder and granule lecithin formats, projected to grow at a 7.00% CAGR through 2031, are gaining traction due to their extended shelf life, reduced shipping weight, and simplified storage requirements. These formats are particularly favored in tropical and subtropical markets, where liquid lecithin logistics are more complex. Export-oriented manufacturers optimize container utilization and avoid refrigerated transport by using powders, while dietary supplement producers benefit from their suitability for direct compression tableting and capsule filling. Despite these advantages, liquid lecithin remains critical for applications requiring instant emulsification and short processing cycles, reflecting the growing importance of form-factor selection based on logistical and application-specific needs.

By Nature: Organic Variants Capture Premium Positioning

Conventional lecithin held the largest share of the market in 2025, accounting for 82.69% of the total volume. Its dominance is attributed to cost efficiency, broad availability, and compatibility with large-scale processing and established oilseed crushing infrastructure. These factors make it the preferred emulsifier for commodity bakery, confectionery, and feed formulations, particularly in applications where organic certification is not a priority. However, evolving consumer preferences for transparency and sustainable sourcing are driving a shift in procurement strategies, creating opportunities for certified alternatives. Organic lecithin, growing at a CAGR of 8.60% through 2031, benefits from compliance with USDA National Organic Program and EU organic regulations, which mandate non-GMO seeds, solvent-free extraction, and full traceability. While these requirements increase production complexity and costs, resulting in a 15–25% price premium, they also enhance ingredient integrity and market differentiation.

Demand for organic lecithin is concentrated in North America and Western Europe, where retailers like Whole Foods, Sprouts, and Alnatura prioritize certified organic ingredients. Suppliers such as Lecico GmbH support this trend by offering traceable, organic lecithin solutions for food, supplements, and cosmetics. Dietary supplement brands leverage organic lecithin to strengthen clean-label positioning in cognitive health, liver support, and prenatal nutrition, while cosmetic formulators integrate it into natural skincare and haircare products to meet Ecocert, COSMOS, and Natrue standards. These developments align organic lecithin adoption with premiumization trends across food, supplements, and personal care markets, solidifying its role despite higher costs.

By Application: Dietary Supplements Surge on Cognitive Health Validation

Food and beverage applications held the largest share of lecithin consumption in 2025, accounting for 50.83%. Key uses include bakery emulsification, dairy fat dispersion, beverage clouding, and viscosity control in confectionery. Lecithin's anti-staling properties and ability to reduce chocolate viscosity are critical for bakery and confectionery applications. Dairy processors rely on lecithin to prevent phase separation in cheese spreads, whipped toppings, and ice cream. In beverages, lecithin acts as a clouding agent in citrus drinks and nutritional shakes, stabilizing essential oil emulsions and preventing ring formation at the liquid-air interface. Animal feed applications, primarily in poultry and aquaculture, utilize lecithin to enhance lipid digestion, improve pellet binding, and reduce dust during handling.

Dietary supplements are projected to grow at 8.67% through 2031, driven by clinical evidence supporting phosphatidylcholine and phosphatidylserine for cognitive function, memory retention, and liver health. The segment benefits from aging demographics, increased awareness of cognitive health, and the rising demand for nootropic formulations targeting memory, focus, and neuroprotection. Phosphatidylserine-enriched lecithin has gained traction following clinical trials demonstrating improvements in memory recall and cognitive processing speed in elderly populations. However, regulatory restrictions on health claims across jurisdictions limit marketing flexibility. Pharmaceutical and personal care industries also capitalize on lecithin's functional properties, including its role in liposome-based drug delivery and as a natural emulsifier in creams, lotions, and hair conditioners.

Geography Analysis

North America holds the largest share of global lecithin demand, accounting for 35.15% in 2025. This dominance is driven by a well-established clean-label ecosystem, high dietary supplement consumption, and robust regulatory frameworks that support lecithin’s application in food, pharmaceutical, and cosmetic formulations. Ingredient suppliers, such as Cargill, leverage these structural advantages to serve bakery, confectionery, beverage, and nutraceutical manufacturers seeking standardized, label-friendly emulsifiers. The region’s strong adoption of functional foods and supplements fuels demand for high-purity and specialty lecithin grades. Additionally, regulatory clarity on GRAS status and food additive approvals enhances market penetration, reinforcing North America’s leadership in both volume and value terms.

Asia-Pacific is the fastest-growing region, with an 8.32% CAGR projected through 2031. Rising disposable incomes, urbanization, and increased consumption of processed and convenience foods in countries like China, India, and Vietnam are driving demand for functional ingredients. Lecithin’s role in improving texture, stability, and shelf life in food formulations positions it as a key ingredient in the region. Companies such as Wilmar International benefit from integrated oilseed crushing and regional processing capabilities, ensuring localized supply for bakery, confectionery, and dairy producers. The region’s growth reflects a shift toward higher protein intake, modern retail expansion, and packaged food adoption, solidifying its role as a major growth engine for the global lecithin market.

Europe represents a mature market with a focus on premium lecithin products. Stringent allergen labeling, organic certification requirements, and clean-label preferences drive demand for non-GMO, allergen-managed lecithin, particularly sunflower and rapeseed-based variants. These products command higher price points in segments like bakery, chocolate, infant nutrition, and dietary supplements. Meanwhile, South America benefits from proximity to major soybean production hubs, ensuring a steady lecithin supply for domestic and export markets. In the Middle East and Africa, expanding bakery, confectionery, and dairy sectors present opportunities, though adoption is limited by price sensitivity, infrastructure challenges, and competition from lower-cost emulsifiers.

Regulatory Landscape

Lecithins are regulated globally as food additives (commonly referenced as INS/E 322) and must meet jurisdiction-specific identity, purity, and permitted-use conditions across food categories, including infant and young-child nutrition where requirements are tighter. In the United States, lecithin is covered under FDA regulatory frameworks including 21 CFR 184.1400 and appears across food-contact and additive listings, with the GRAS notification pathway used for new or differentiated source materials.

In Europe, the regulatory anchor is the Union list of food additives under Regulation (EC) No 1333/2008, with targeted updates affecting lecithins (E 322). Commission Regulation (EU) 2025/651 (April 2, 2025) authorized lecithins as carriers in glazing agents on cassavas, and Commission Regulation (EU) 2025/2058 (October 14, 2025) updated specific uses of lecithins in foods for infants and young children, reinforcing the need for category-specific compliance and documentation for suppliers serving specialized nutrition customers.

Value Chain Analysis

Lecithin supply is structurally linked to oilseed processing, since it is primarily produced as a co-product of soybean, sunflower, and rapeseed/canola crushing and refining. The value chain starts with seed origination and aggregation, then moves through cleaning and oil extraction, followed by water degumming to separate gums. Those gums are processed further via separation and drying into liquid lecithin, or through additional deoiling to produce powders and granules.

Large agribusinesses such as ADM, Cargill, and Bunge run integrated networks covering origination, crushing, refining, and global logistics, which supports supply consistency for multinational food and nutrition manufacturers. Mid-tier specialists typically differentiate through customized, higher-purity, or certified (non-GMO/organic) lecithins, often relying on identity-preserved sourcing and third-party certifications to pass customer audits. Logistics also vary by form, with bulk liquid moving via tankers and flexi-tanks, while deoiled powders and granules support longer shelf life and easier cross-border shipment, which becomes more relevant as traceability and documentation requirements influence procurement and supplier qualification.

Competitive Landscape

Major agribusiness giants like Archer Daniels Midland (ADM), Cargill, and Bunge are consolidating the global lecithin market. By vertically integrating, from oilseed origination and crushing to lecithin refining, these players ensure steady access to raw materials and stabilize their cost structures. This strategy not only guarantees a consistent lecithin supply for their in-house food ingredient and nutrition divisions but also shields them from fluctuations in the soybean and rapeseed markets. Their global logistics networks and multi-regional production capabilities enable them to meet the demands of multinational food, feed, and pharmaceutical manufacturers. These companies focus on operational efficiency and portfolio diversification rather than price competition. By offering bundled solutions that combine lecithin with proteins, fibers, and specialty oils, they strengthen customer relationships and secure long-term formulation partnerships, aligning with the growing preference for integrated ingredient solutions.

Mid-tier players such as Sternchemie, AAK, and Clarkson Specialty Lecithins differentiate themselves by targeting high-margin niches like pharmaceutical-grade purity, organic-certified lecithins, and customized phospholipid blends. These companies prioritize technical service, regulatory expertise, and formulation support over volume, helping clients address complex purity standards, allergen management, and clean-label compliance. Their specialization-driven strategies cater to pharmaceutical, nutraceutical, and premium food manufacturers seeking consistent performance rather than commodity pricing. This focus on customization reflects the increasing demand for higher-functionality lecithin formats and reinforces the importance of technical collaboration as regulatory scrutiny and formulation complexity rise.

Growth opportunities exist in precision-fermented phospholipids, enzyme-modified lecithins with enhanced emulsification properties, and allergen-free variants for premium plant-based, infant nutrition, and medical applications. These innovations address clean-label trends, allergen concerns, and performance optimization at lower inclusion rates. However, higher processing costs and regulatory challenges create space for differentiated innovation. Smaller, technology-driven firms are exploring these segments to avoid direct competition with major players, while large incumbents monitor these niches for acquisition or partnership opportunities. This evolving landscape highlights how shifting formulation needs and regulatory expectations are reshaping the competitive dynamics of the lecithin market.

Lecithin Industry Leaders

-

Archer Daniels Midland Company

-

Cargill Incorporated

-

Bunge Limited

-

Wilmar International

-

International Flavors & Fragrances, Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

An opportunity is emerging around expanding capacity and product breadth for specialty and premium sunflower and deoiled lecithins that improve allergen management and non-GMO positioning, while leveraging the handling advantages of dry formats. Recent investments illustrate this shift toward specialization and regional supply optionality: the European Bank for Reconstruction and Development (EBRD) provided a EUR 13.5 million loan in May 2026 to LeciForce to construct a premium sunflower lecithin manufacturing facility in Lublin, Poland, and trade coverage in 2026 pointed to capacity expansion and product-line additions at Lecilite Ingredients, including fractionated lecithin. These moves target higher-value applications across food, dietary supplements, and personal care, where formulation performance and label claims are bought alongside emulsification.

Compliance-led sourcing and documentation are also creating room for suppliers that can provide verified origin and certified flows, particularly for soy-linked lecithin supply chains serving Europe. At the same time, industrial demand for enzyme-treated and low-viscosity variants is being addressed through operational upgrades, such as Louis Dreyfus Companys automated specialty feed lecithin production line in Tianjin (launched May 2025), which points to a need for more functional, process-friendly lecithins in feed and food manufacturing. Overall, these developments favor producers and distributors with integrated crushing and refining footprints, quality systems suited to pharma- and supplement-grade specifications, and the ability to supply both liquid and stable dry formats across long-distance trade lanes.

Recent Industry Developments

- March 2026: Bunge completed its acquisition of IFFs soy protein concentrate, lecithin, and soy crush businesses, adding established assets and brands such as Solec. The transaction expands Bunges ingredient portfolio and strengthens upstream-to-downstream control over soy-based derivatives that feed lecithin availability and customization.

- May 2025: Louis Dreyfus Company (LDC) commenced operations at a new automated production line for specialty feed lecithin at its oilseed crushing plant in Tianjin, China, with renewable electricity supply and R&D support from Shanghai. The added capability targets enzymatically treated and low-viscosity lecithin formats, improving LDCs ability to serve performance-driven feed formulations in China and export channels.

- December 2024: Louis Dreyfus Company (LDC) finalized a binding agreement to acquire BASFs Food and Health Performance Ingredients business, which includes activities spanning oils, fats, glycerine, and lecithin. The deal increases LDCs reach in nutritional and functional ingredients and supports broader formulation and supply-chain offerings tied to lecithin-based applications.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the lecithin market covers the value of commercially sold lecithin ingredients used as emulsifiers and functional additives across food, feed, dietary supplements, pharmaceuticals, personal care, and industrial uses, counted at the point of ingredient sale.

Scope exclusions: We exclude finished retail food products that only contain lecithin as an ingredient and we also exclude synthetic emulsifiers that are not lecithin-derived.

Segmentation Overview

-

By Source

- Soy

- Sunflower

- Rapeseed/Canola

- Egg

- Other Sources

-

By Grade

- Food Grade

- Pharmaceutical Grade

- Industrial Grade

-

By Form

- Liquid

- Powder and Granules

-

By Nature

- Conventional

- Organic

-

By Application

-

Food and Beverage

- Bakery and Confectionery

- Dairy Products

- Beverages

- Other Food and Beverage

- Animal Feed

- Dietary Supplements

- Pharmaceuticals

- Cosmetics and Personal Care

- Other Applications

-

Food and Beverage

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research started by mapping lecithin supply routes, key end uses, and the pricing patterns that typically shape lecithin demand across regions. We relied on public sources such as USDA oilseed and crush statistics, FAOSTAT crop and trade series, UN Comtrade import and export data for relevant commodity and ingredient flows, and published standards and guidance from bodies such as FDA and EFSA that influence food and pharma grade usage.

To keep the model grounded, we also reviewed company annual reports and investor presentations for capacity additions, product mix, and demand commentary, then used association and trade-journal updates on clean label emulsifiers and oilseed processing. Patent databases were selectively checked to understand where modification and fractionation activity is picking up. Where available, a paid subscription for company financials and intelligence was used only to cross-check basic revenue ranges and ownership linkages. The sources listed here are not exhaustive, and many other public references were used for data collection, validation, and clarification during the research.

Primary Interviews and Surveys

Primary work focused on interviews and short surveys with ingredient suppliers, distributors, food and feed formulators, and procurement and quality teams who handle lecithin grades and forms in day-to-day buying. Coverage was balanced across major consuming and producing regions (APAC, EMEA, and the Americas) so assumptions on application split, typical dosage ranges, and price movement could be checked, then refined before finalizing the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 16% | APAC: 43% |

| Mid tier: 54% | Functional/Unit leaders: 27% | EMEA: 30% |

| Smaller Players: 20% | Managers: 57% | Americas: 27% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach that reconstructs demand from oilseed processing and ingredient usage, then allocates it into lecithin consumption by grade, form, and application. In practice, crush volumes for soy and sunflower, regional processing intensity, and trade signals were used to shape the available ingredient pool, and then filtered using application adoption patterns discussed by interviewees.

To keep the outputs grounded, we used selective bottom-up checks, including sampled supplier revenue ranges, channel checks on typical price bands, and volume-by-application sanity checks using dosage ranges in key food categories. Key model inputs included oilseed crush and availability trends, shifts between soy and sunflower sourcing, pricing spread between food and pharma grade, liquid versus powder preference in processing, and growth in animal feed and supplement formulation. Forecasts were developed using scenario analysis supported by expert views on raw material volatility, clean label reformulation pace, and regional demand momentum. Where bottom-up checks were incomplete, we used conservative ranges and re-validated implied totals with interview feedback.

Data Validation & Update Cycle

Validation was done by triangulating model outputs against independent signals, including trade direction, oilseed processing trends, and observed price movements by grade and form. Outliers were flagged and reviewed through a second analyst pass, and respondents were re-contacted when assumptions such as application share or price ranges created unusual jumps across years.

The report is refreshed annually, and interim updates are triggered when material events occur, such as sharp oilseed price changes, supply disruptions, or meaningful capacity additions. Before delivery, we run a final review pass so the numbers reflect the latest available public data and the most recent primary feedback.

Mordor Intelligence's Lecithin Market Estimate Compared With Other Published Estimates

Published lecithin market sizes can look far apart even when they are discussing the same ingredient family, because boundaries and counting points differ. The biggest differences usually come from what gets included as lecithin, which end uses are counted, and whether values reflect ingredient sales or broader downstream product value.

Trade flow checks and oilseed processing signals, followed by re-validation of grade-level pricing ranges with interview feedback, are the evidence used to keep Mordor Intelligence's estimate aligned to ingredient-level lecithin demand rather than expanded phospholipid or downstream product scopes. Gaps also appear when some studies mix lecithin with wider phospholipids, use more aggressive price progression, or apply a different currency timing and update cadence, which can move the reported base year value.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.13 B (2026) | |

| Global Consultancy A | USD 0.69 B (2025) | This estimate appears to stay closer to a narrower ingredient revenue pool and may apply stricter exclusions around modified and higher-grade lecithin, which can pull down the total when compared year to year. |

| Industry Publisher B | USD 0.69 B (2025) | The number is directionally consistent with a conservative 2025 base and may rely more on historical pricing bands without fully reflecting grade mix shifts and regional application growth that become visible in more recent validation. |

Overall, the spread is mainly explained by scope boundaries and the year used for the stated market size, then amplified by how pricing and grade mix are treated. By tying the model to observable processing and trade indicators and stress-testing price and usage assumptions with primary feedback, the resulting view stays transparent and repeatable for planning.

Key Questions Answered in the Report

What is the projected value of the lecithin market by 2031?

The lecithin market is forecast to reach USD 1.52 billion by 2031.

Which source is growing fastest within global demand?

Sunflower-derived ingredients are advancing at a 7.61% CAGR through 2031 because of non-GMO and allergen-free positioning.

Why is pharmaceutical-grade lecithin expanding quicker than food-grade?

Liposome and lipid-nanoparticle drug technologies require highly purified phospholipids, pushing pharmaceutical-grade sales up at an 8.91% CAGR.

Which region leads global revenue today?

North America captured 35.15% of 2025 sales, driven by established clean-label trends and strong functional-food consumption.

Page last updated on: