Lecithin and Phospholipids Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.95 Billion |

| Market Size (2031) | USD 2.41 Billion |

| Growth Rate (2026 - 2031) | 4.23% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Lecithin and Phospholipids Market Analysis by Mordor Intelligence

The lecithin and phospholipids market size is expected to grow from USD 1.87 billion in 2025 to USD 1.95 billion in 2026 and reach USD 2.40 billion by 2031, registering a CAGR of 4.23% during 2026-2031. Growth is supported by rising demand from food manufacturing, pharmaceutical delivery systems, and personal care formulations. Food companies are increasingly using plant-derived lecithin and phospholipids as alternatives to synthetic emulsifiers, especially in products that emphasize clean-label claims. These ingredients help improve texture, stability, and shelf life in several food and beverage products. In pharmaceuticals, drug developers are increasingly using lipid-based systems for mRNA therapeutics, oncology products, and biologics because these systems improve drug delivery and support more effective formulations. Personal care brands are also using phospholipids as carriers for skin and hair actives, as they support biocompatibility and clean-label positioning. This makes them useful in products such as creams, lotions, serums, and hair care formulations. The market is moderately consolidated, with leading players including Cargill, Inc., Archer Daniels Midland Company, Wilmar International, among others.

Key Report Takeaways

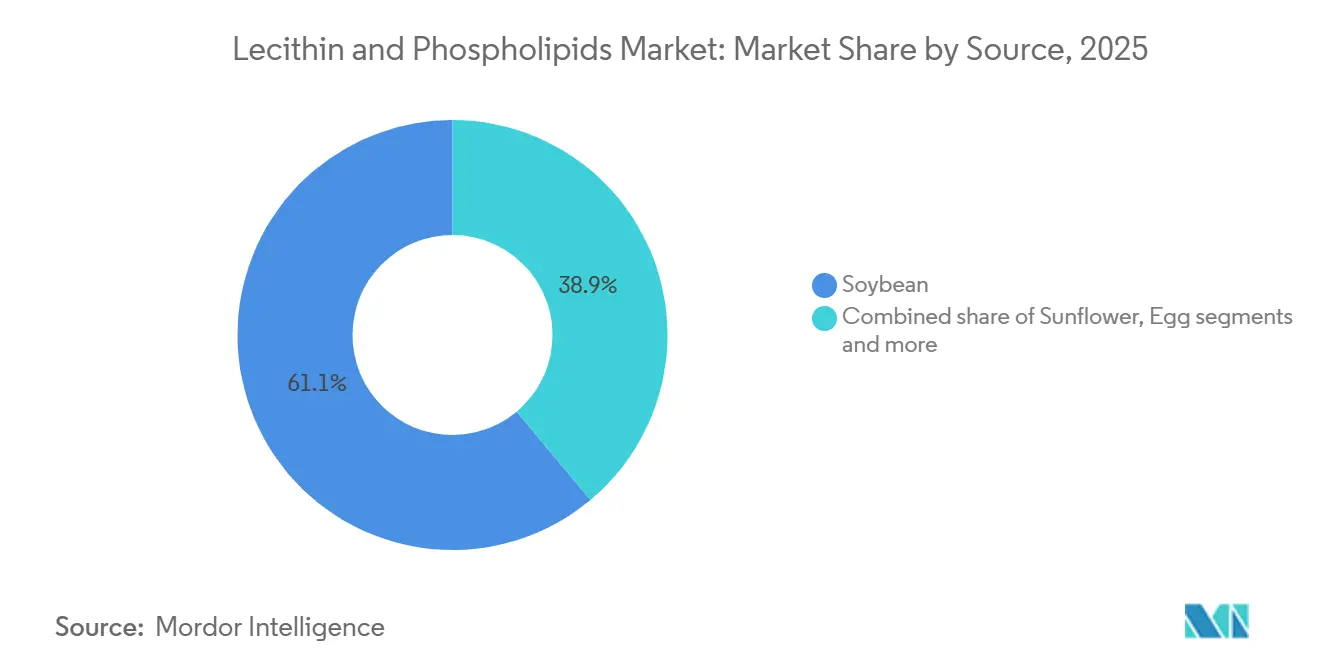

- By source, soy-derived lecithin led with 61.08% revenue share in 2025, while sunflower lecithin is forecast to expand at 8.48% CAGR through 2031.

- By form, liquid lecithin held 86.21% revenue share in 2025, while powder lecithin is projected to grow at 9.21% CAGR through 2031.

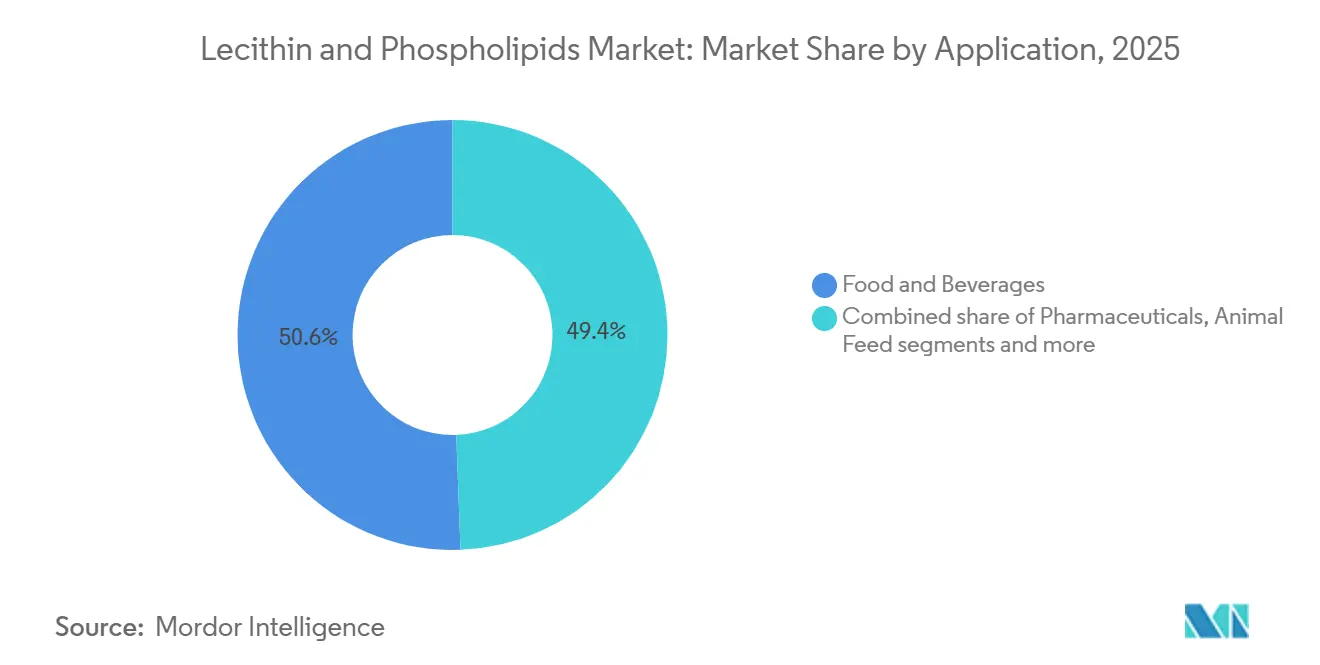

- By application, food and beverages accounted for 50.60% revenue share in 2025, while pharmaceuticals are expected to record the highest CAGR of 7.95% through 2031.

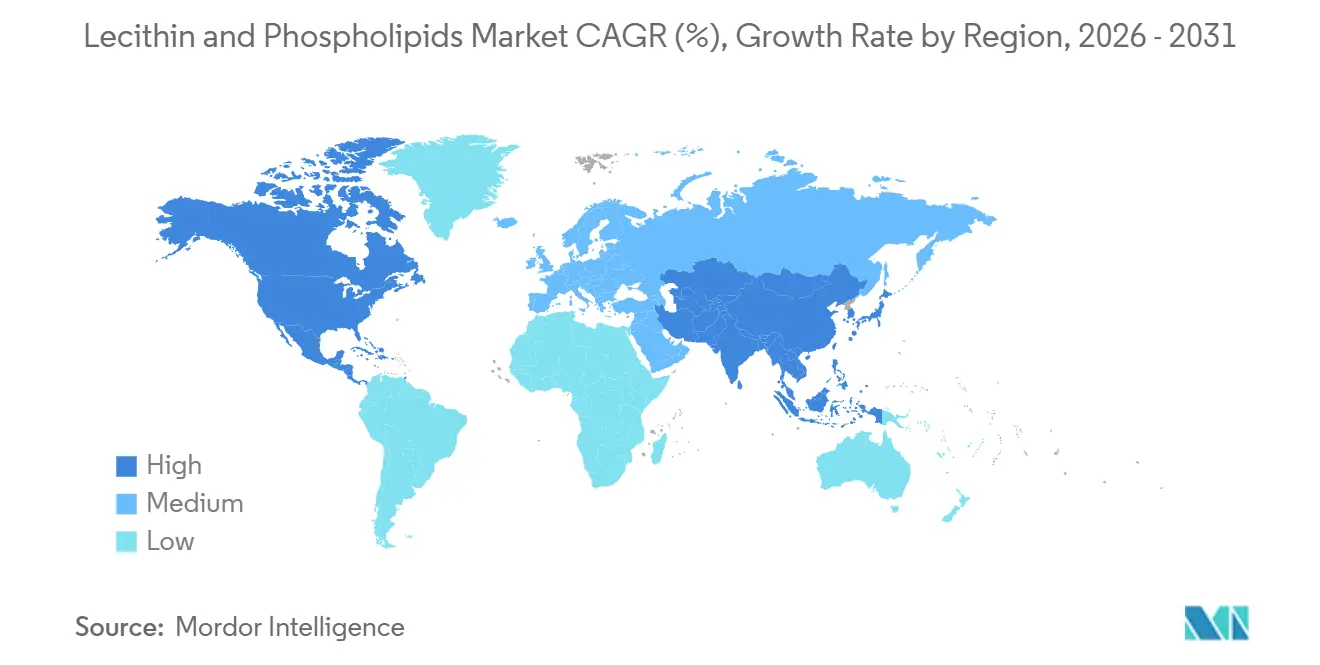

- By geography, North America held 31.10% revenue share in 2025, while Asia-Pacific is projected to grow at 7.66% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Lecithin and Phospholipids Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing demand for clean-label and natural ingredients | +0.8% | Global | Short term (≤ 2 years) |

| Expansion of processed food and convenience food industry | +0.7% | Asia-Pacific core, spill-over to Middle East | Medium term (2–4 years) |

| Strong growth in nutraceutical and functional food markets | +0.6% | North America and Europe | Medium term (2–4 years) |

| Rising adoption of pharmaceutical drug delivery applications | +0.7% | North America and Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Growing preference for plant-based and non-GMO products | +0.5% | Europe and North America | Short term (≤ 2 years) |

| Increasing incorporation into natural and organic cosmetic formulations | +0.3% | Europe, North America | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Increasing demand for clean-label and natural ingredients

The rising demand for clean-label and natural ingredients is a key driver of the lecithin and phospholipids market. Food, nutraceutical, and personal care manufacturers are increasingly using naturally sourced emulsifiers because consumers prefer products with simple, familiar, and easy-to-understand ingredient labels. Lecithin supports this shift because it is derived from plant or egg sources and helps improve emulsification, stabilization, and dispersibility across a wide range of products without being perceived as a highly synthetic additive. This makes it suitable for applications such as bakery products, confectionery, dietary supplements, infant nutrition, and personal care formulations. Consumer preference also supports this trend, with 71% of global consumers preferring gradual results from natural sources and showing a willingness to pay more for them, according to Asia Food Journal in October 2025[1]Source: Asia Food Journal, "Natural Ingredients And Emotional Drivers: Key Factors Reshaping The Global Nutrition Market", asiafoodjournal.com. As a result, food and supplement companies are using more lecithin, especially sunflower and soy varieties, in reformulated products with clean-label, non-GMO, and premium wellness positioning.

Rising adoption of pharmaceutical drug delivery applications

The growing use of lecithin and phospholipids in pharmaceutical drug delivery is driving the market for these ingredients. Phospholipids help drug makers improve how medicines are carried, absorbed, and stabilized in the body, especially in products such as liposomal formulations, injectable emulsions, parenteral nutrition products, and other advanced drug delivery systems. Demand is rising as pharmaceutical manufacturing expands worldwide, particularly for affordable generic medicines and complex formulations that need safe and effective delivery ingredients. This trend is also supported by India’s strong position in the pharmaceutical industry. According to the Press Information Bureau of India in March 2026, India is the world’s largest supplier of generic medicines, accounting for around 20% of global supply and producing about 60,000 generic brands across 60 therapeutic categories[2]Source: Press Information Bureau of India, "India’s Pharmaceuticals in Global Healthcare", pib.gov.in. As the production of injectables, critical care medicines, specialty drugs, and other advanced formulations increases, manufacturers are expected to use more lecithin and phospholipids, as these ingredients are functional, biocompatible, and suitable for high-quality pharmaceutical applications.

Growing preference for plant-based and non-GMO products

The growing preference for plant-based and non-GMO products is driving demand in the lecithin and phospholipids market, as food, nutraceutical, and personal care manufacturers seek ingredients that align with consumer expectations for cleaner, more transparent labels. Many consumers now prefer products made with plant-based ingredients and want to avoid genetically modified sources, which is increasing the use of sunflower- and rapeseed-based lecithin as alternatives to soy-based lecithin. These ingredients are especially useful in vegan, allergen-conscious, and clean-label formulations because they help improve texture, stability, and product quality while supporting non-soy and non-GMO claims. The trend is also supported by the expanding global plant-based consumer base: according to the World Animal Foundation, there are about 88 million vegans worldwide out of a global population of more than 8.3 billion[3]Source: World Animal Foundation, "How Many Vegans Are in the World in 2026? Latest Vegan Stats", worldanimalfoundation.org. As more brands launch vegan-friendly, plant-based, and clean-label products, the demand for plant-derived lecithin and phospholipids is expected to grow further.

Increasing incorporation into natural and organic cosmetic formulations

The growing use of lecithin and phospholipids in natural and organic cosmetics is driving the market for these ingredients. Cosmetic brands use these ingredients in skin care products, liposomal topical systems, and barrier-repair products because they help mix oil and water, improve moisture retention, support skin barrier function, and deliver active ingredients more effectively. Their natural origin also makes them suitable for premium products that promote clean-label, plant-based, and skin-friendly claims. Sunflower-derived phospholipids are gaining attention because they support non-GMO and vegan positioning, which is becoming more important in natural and organic personal care products. While cosmetics remain a smaller application area than food or pharmaceuticals, it offers a high-value growth opportunity for suppliers that can provide specialty phospholipids with consistent quality, strong performance, and formulation support.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production cost of specialty phospholipids | -0.6% | Global | Long term (≥ 4 years) |

| Volatility in raw material availability and pricing | -0.5% | Global, particularly South America and Asia-Pacific | Short term (≤ 2 years) |

| Consumer skepticism toward genetically modified ingredients | -0.4% | Europe and North America | Medium term (2–4 years) |

| Shorter shelf stability of liquid lecithin formats compared to dry | -0.3% | Tropical regions, emerging markets | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High production cost of specialty phospholipids

High production costs for specialty phospholipids remain a key restraint on the global lecithin and phospholipids market, especially in pharmaceutical, nutraceutical, and other high-specification applications. Compared to standard food-grade lecithin, specialty phospholipids need more advanced processing to achieve higher purity, better consistency, and specific performance requirements. These processes include fractionation, solvent extraction, molecular distillation, and, in some cases, chromatographic separation, all of which increase manufacturing costs. Costs rise further because suppliers must meet strict pharmacopoeial standards, operate cGMP-compliant facilities, support Drug Master Files, and complete repeated customer qualification and audit processes. These requirements demand skilled technical teams, specialized equipment, strong quality control systems, and detailed documentation. As a result, only a limited number of companies can produce these high-purity ingredients at the required standard.

Volatility in raw material availability and pricing

Raw material availability and pricing remain a key challenge for the lecithin and phospholipids market. Lecithin is mainly produced during soybean and sunflower oilseed crushing, so its supply depends heavily on crop output, weather conditions, and edible oil market trends. Poor soybean harvests in South America, disruptions in major sunflower-growing regions, or sudden changes in vegetable oil prices can raise input costs and make supply less predictable. This issue is more serious for non-GMO and identity-preserved lecithin because these supply chains depend on fewer approved sources and are often concentrated in specific regions. As a result, manufacturers and buyers face higher cost pressure and supply risk. To manage these challenges, companies are using more dual sourcing, entering longer-term supply contracts, and improving inventory planning to ensure steady availability for food, feed, pharmaceutical, and nutraceutical applications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Sunflower Lecithin Erodes Soy's Historical Lead

Soy lecithin is expected to lead the lecithin and phospholipids market by 2025, with a 61.08% market share. This is mainly due to the strong global infrastructure for soybean processing, which ensures a consistent supply of raw materials and cost-efficient production. Soy lecithin is widely used across industries such as food, feed, and pharmaceuticals, as well as in industrial applications, because of its ability to emulsify, stabilize, and disperse ingredients. Furthermore, it is available in various forms, including liquid, deoiled, and modified lecithin, making it versatile for both large-scale and specialized applications.

Sunflower lecithin is expected to grow rapidly, with a CAGR of 8.48% over 2026–2031, making it one of the fastest-growing segments in the market. This growth is driven by the rising demand for non-GMO, allergen-free, and clean-label ingredients, especially in premium food, nutraceutical, and personal care products. Many manufacturers are turning to sunflower lecithin to reduce reliance on soy-based alternatives and meet consumer preferences for healthier options. Its increasing popularity is further supported by new product developments, broader applications, and growing regulatory approvals in health-conscious and food-related sectors.

By Form: Powder Gains as Liquid Faces Precision Dosing Demands

Liquid lecithin accounted for 86.21% of the lecithin and phospholipids market by form in 2025, highlighting its extensive use in large-scale food and feed production. Its popularity is due to its easy integration into manufacturing systems, compatibility with oils and fats, and cost-effectiveness across products such as bakery items, confectionery, margarine, instant foods, and animal feed. Additionally, liquid lecithin is widely available from sources such as soy, sunflower, and rapeseed, supported by well-established supply chains. Its ability to perform multiple functions, including emulsification, viscosity control, and stabilization, makes it a preferred choice for high-volume industrial applications.

Powder lecithin is expected to grow at a compound annual growth rate (CAGR) of 9.21% from 2026 to 2031, driven by its increasing use in pharmaceuticals, nutraceuticals, and premium food products. This format is ideal for applications that require higher phospholipid concentrations, precise dosing, and better handling, such as dry blends, capsules, sachets, infant nutrition, and dietary supplements. Powdered lecithin offers advantages such as improved stability, lower moisture content, and easier storage, making it suitable for specialized formulations. The rising demand for de-oiled and specialty lecithin products with enhanced dispersibility and standardized content further supports its growth as a high-value option in the market.

By Application: Pharmaceutical Demand Elevates Market Value Mix

The food and beverage sector held the largest share of the lecithin and phospholipids market in 2025, accounting for 50.60% of the applications. This dominance is due to the extensive use of lecithin in various roles, such as an emulsifier, stabilizer, release agent, and instantizing aid. It is widely used in products such as bakery items, confectionery, dairy, infant nutrition, convenience foods, and beverages. Lecithin is valued for its ability to improve texture, extend shelf life, and enhance processing efficiency. The growing preference for clean-label and functional ingredients in packaged foods continues to drive demand in this segment.

The pharmaceutical sector is expected to be the fastest-growing application area for lecithin and phospholipids, with a projected CAGR of 7.95% from 2026 to 2031. This growth is fueled by the increasing use of high-purity phospholipids in advanced drug delivery systems, liposomal formulations, injectable emulsions, parenteral nutrition, and softgel capsules. These ingredients are highly regarded for their biocompatibility and for improving the stability and bioavailability of active pharmaceutical ingredients. As the pharmaceutical industry moves toward more specialized formulations and lipid-based delivery systems, the demand for lecithin and phospholipids in this sector is expected to rise significantly.

Geography Analysis

North America accounted for 31.10% of the lecithin and phospholipids market in 2025. The region benefits from a large food processing industry, a well-developed packaged food market, and a strong pharmaceutical manufacturing base. The United States is the main demand center in the region. Lecithin is widely used in bakery, confectionery, infant nutrition, and convenience food products, while phospholipids are increasingly used in biopharmaceutical and lipid-based drug delivery applications. Europe also remains a major market, supported by strong demand for non-GMO and specialty lecithin in food, nutraceutical, and pharmaceutical applications, as well as continued investment in sunflower lecithin and clean-label ingredient production.

Asia-Pacific is projected to be the fastest-growing regional market, with a 7.66% CAGR from 2026 to 2031. China and India are leading this growth as pharmaceutical manufacturing expands, supplement consumption rises, and demand for processed foods increases. China is strengthening its position in the production of pharmaceutical-grade phospholipids and advanced lipid materials. India is seeing higher demand driven by rising disposable incomes, a wider organized retail presence, and growing interest in health-focused formulations. Japan remains a technically advanced market in the region, supported by steady demand for phosphatidylcholine-rich products in nutraceutical and functional health applications, while Southeast Asia and Australia are growing through processed food, animal nutrition, and aquaculture feed applications.

South America and the Middle East and Africa are smaller but important markets in the global lecithin and phospholipids industry. South America is closely linked to the soybean value chain, with Brazil and Argentina playing key roles in global soy lecithin production and export supply. The region is more important as a source of commodity-grade lecithin than as a high-value demand center, although local food and feed uses continue to support consumption. The Middle East and Africa are gradually growing as food manufacturing, ingredient imports, and organized procurement systems expand across GCC countries and South Africa. Demand in these markets is supported by the growth of packaged foods, feed sector development, and rising interest in functional food and nutrition ingredients.

Competitive Landscape

The lecithin and phospholipids market is moderately consolidated. Key companies in the market include Cargill, Inc., Archer Daniels Midland Company, Bunge Limited, Wilmar International, and Sternchemie GmbH & Co. KG. Large agribusiness ingredient suppliers compete through strong oilseed processing capabilities, wide sourcing networks, and global distribution reach. Specialty phospholipid manufacturers focus on higher-purity products and ingredients designed for specific applications. As a result, competition varies by source, grade, and end use.

Food- and feed-grade lecithin is mainly driven by production scale, cost efficiency, and supply reliability. In contrast, pharmaceutical and nutraceutical phospholipids depend more on technical expertise, strict quality standards, and formulation support. Large integrated companies such as Cargill, ADM, Bunge, and Wilmar compete strongly in mainstream lecithin applications. Specialist companies such as Lipoid GmbH, Sternchemie, and Croda International focus on differentiated phospholipid systems, high-purity formats, and regulatory support. This creates a clear difference between suppliers of commodity lecithin and producers of high-value specialty phospholipids.

The strongest growth opportunities are in non-GMO sunflower lecithin, pharmaceutical-grade phospholipids, and modified or fractionated lecithin for premium applications. Suppliers are investing in extraction, enzymatic modification, purification, and fractionation technologies to improve product quality and functionality. These technologies help increase phospholipid concentration and support use in advanced delivery systems and clean-label formulations. Europe remains an important center for specialty phospholipid development. At the same time, manufacturers in India and China are expanding their role in pharmaceutical-grade and nutraceutical-grade lecithin ingredients, increasing competition in higher-value parts of the market.

Lecithin and Phospholipids Industry Leaders

-

Cargill, Inc.

-

Archer Daniels Midland Company

-

Bunge Limited

-

Sternchemie GmbH & Co KG

-

Wilmar International

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Lekithos introduced sunflower lecithin granules, adding a dry, free-flowing option to its existing portfolio of liquid, powder, and capsule formats, designed for convenient use in smoothies, yogurt, and cereals, and promoted as 100% pure, non-GMO, glyphosate-tested, and allergen-free.

- June 2025: Austrade launched a non-GMO hydrolyzed sunflower lecithin powder for functional beverage manufacturers, promoting it as a clean-label emulsifier to address formulation challenges in beverage systems.

- May 2025: Louis Dreyfus Company launched a new automated production line for specialty feed lecithin in Tianjin, China. This facility, located at its existing oilseeds crushing site, operated entirely on renewable electricity.

- April 2024: VAV Lipids announced that its upgraded EU cGMP-certified Ratnagiri facility capacity to produce 6,000 kg of pharmaceutical egg yolk lecithin annually, accounting for approximately 7% of the estimated global demand.

Global Lecithin and Phospholipids Market Report Scope

Lecithin and phospholipids, whether naturally derived or synthetic, are lipid-based emulsifying agents utilized in food, nutraceutical, pharmaceutical, feed, and personal care applications. They serve purposes such as emulsification, stabilization, dispersibility, and the delivery of active ingredients. The global lecithin and phospholipids market comprises source, form, application, and geography. Based on the source, the market is classified into soybean, sunflower, rapeseed, egg, and others. Based on form, the market is classified into powder and liquid. Based on application, the market is classified into food and beverages, dietary supplements, pharmaceuticals, and animal feed. Based on geography, the market is classified into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The market forecasts are provided in terms of value (USD).

| Soybean |

| Sunflower |

| Rapeseed |

| Egg |

| Others |

| Powder |

| Liquid |

| Food and Beverages | Bakery and Confectionery |

| Diary and Dairy Alternatives | |

| Meat and Meat Alternatives | |

| Beverages | |

| Other Food and Beverages | |

| Dietary Supplements | |

| Pharmaceuticals | |

| Animal Feed |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Italy | |

| Netherlands | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Rest of Middle East and Africa |

| By Source | Soybean | |

| Sunflower | ||

| Rapeseed | ||

| Egg | ||

| Others | ||

| By Form | Powder | |

| Liquid | ||

| By Application | Food and Beverages | Bakery and Confectionery |

| Diary and Dairy Alternatives | ||

| Meat and Meat Alternatives | ||

| Beverages | ||

| Other Food and Beverages | ||

| Dietary Supplements | ||

| Pharmaceuticals | ||

| Animal Feed | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Italy | ||

| Netherlands | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the forecast value of the lecithin and phospholipids market by 2031?

The lecithin and phospholipids market is expected to reach USD 2.41 billion by 2031, rising from USD 1.95 billion in 2026, projected to grow at a CAGR of 4.23% over 2026-2031.

Why is sunflower lecithin gaining share against soy-based products?

Sunflower lecithin is benefiting from its natural non-GMO profile, lower allergen concerns, and broader regulatory acceptance, including the FDA’s 2026 no-questions response for GRN No. 1267.

Which application is expanding the fastest through 2031?

Pharmaceuticals are projected to be the fastest-growing application, with an 7.95% CAGR through 2031, supported by liposomal drugs, lipid nanoparticles, and wider use in mRNA and biologics pipelines.

Why are powder lecithin formats growing faster than liquid forms?

Powder lecithin is projected to grow at 9.21% CAGR because it offers better phospholipid concentration, more precise dosing, and easier ambient transport than liquid lecithin.

Page last updated on: