Organic Soy Protein Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

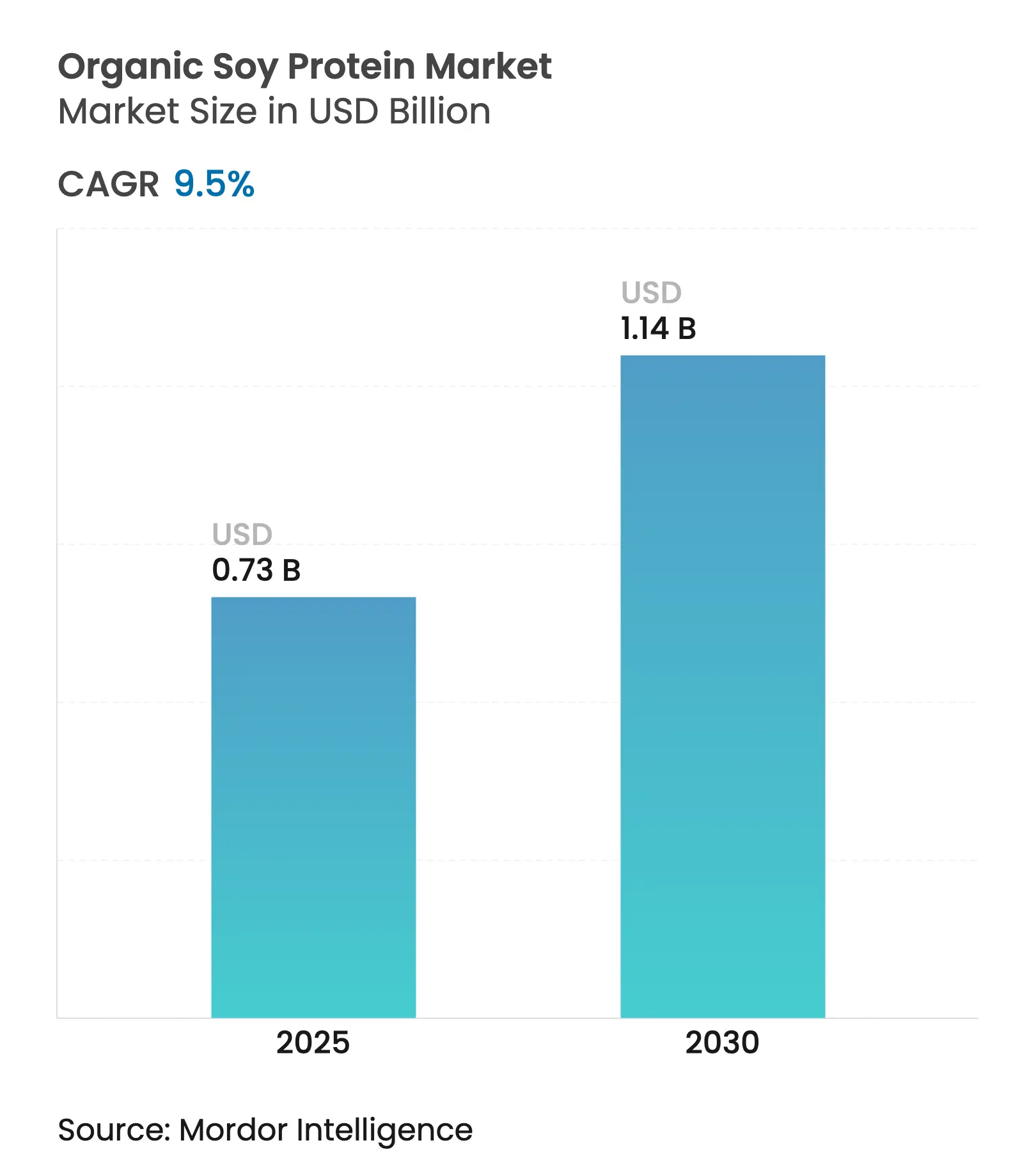

| Market Size (2025) | USD 0.73 Billion |

| Market Size (2030) | USD 1.14 Billion |

| Growth Rate (2025 - 2030) | 9.50 % CAGR |

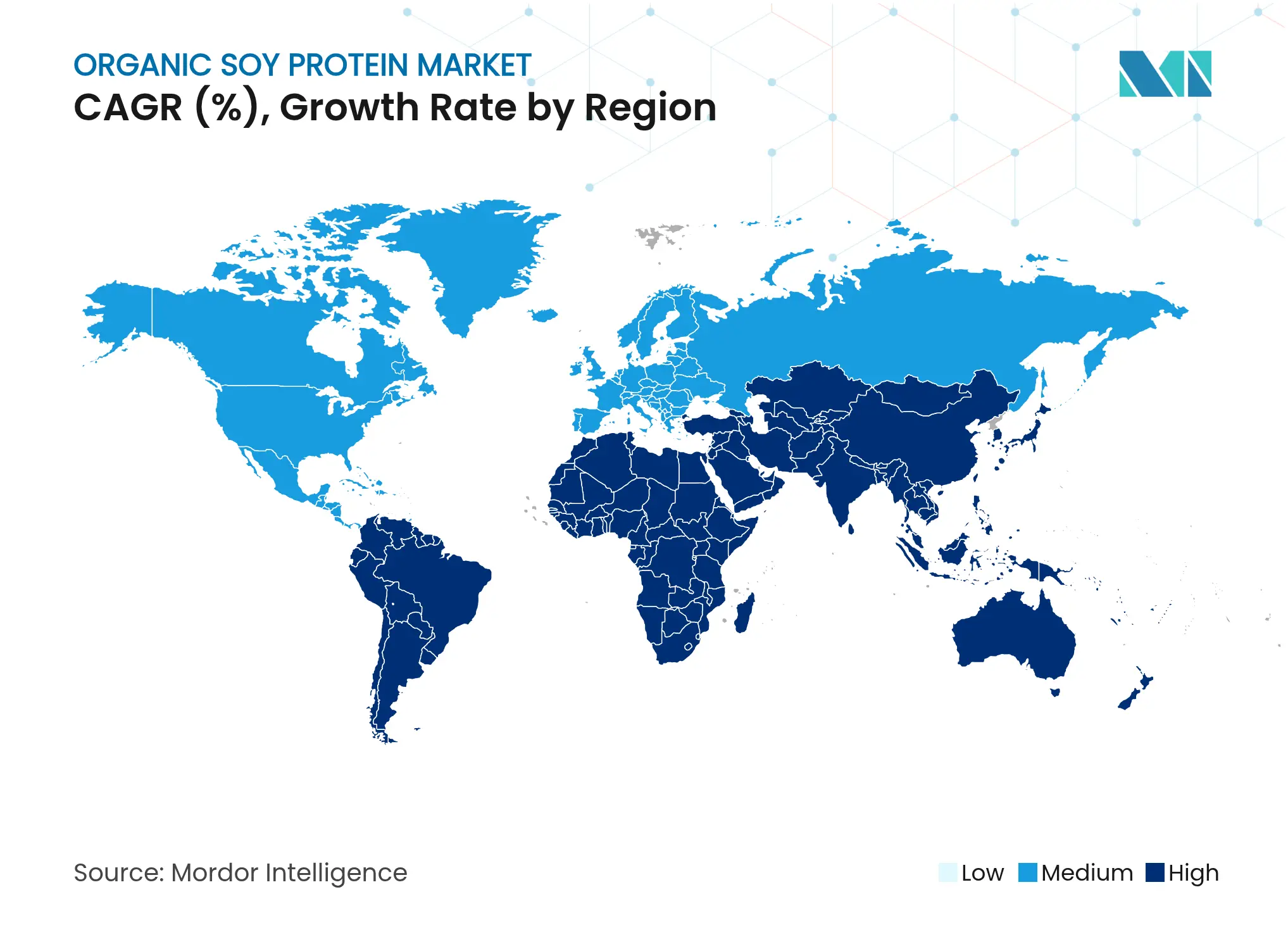

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Organic Soy Protein Market Analysis by Mordor Intelligence

The organic soy protein market is estimated to be USD 0.73 billion in 2025 and is forecast to rise to USD 1.14 billion by 2030, advancing at a 9.50% CAGR. Rising demand for plant-based protein, supportive FDA health-claim regulations, and continuous innovation in extraction technology underpin this momentum. Manufacturers reformulate mainstream foods with soy protein to meet clean-label expectations, while supply-chain realignment toward South American crushing hubs lowers processing costs and improves margin resilience. Firms also leverage soy protein's complete amino-acid profile to fill nutritional gaps in sports nutrition, medical foods, and infant formula. Regulatory clarity from the FDA's 2025 draft guidance on labeling plant-based alternatives further accelerates new-product launches that prominently feature soy protein. The increasing consumer awareness of sustainable protein sources and environmental concerns has positioned organic soy protein as a preferred choice in the market. Additionally, the growing adoption of organic soy protein in plant-based meat alternatives and dairy substitutes continues to expand market opportunities.

Key Report Takeaways

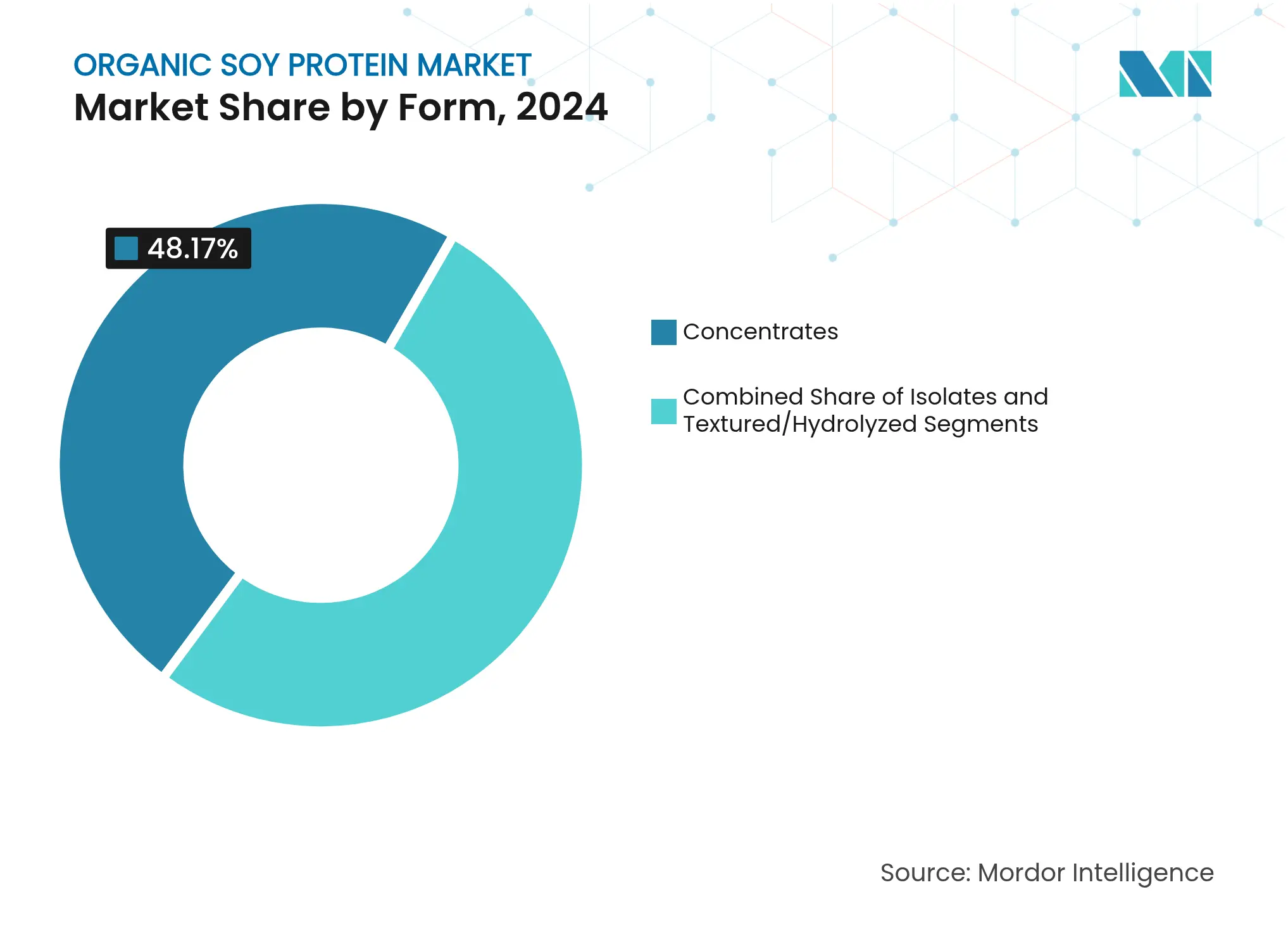

- By form, concentrates commanded 48.17% of soy protein market share in 2024, whereas isolates led growth with a 10.29% CAGR to 2030.

- By application, food and beverage held 34.47% of the soy protein market size in 2024; the supplements segment is expanding at an 11.23% CAGR through 2030.

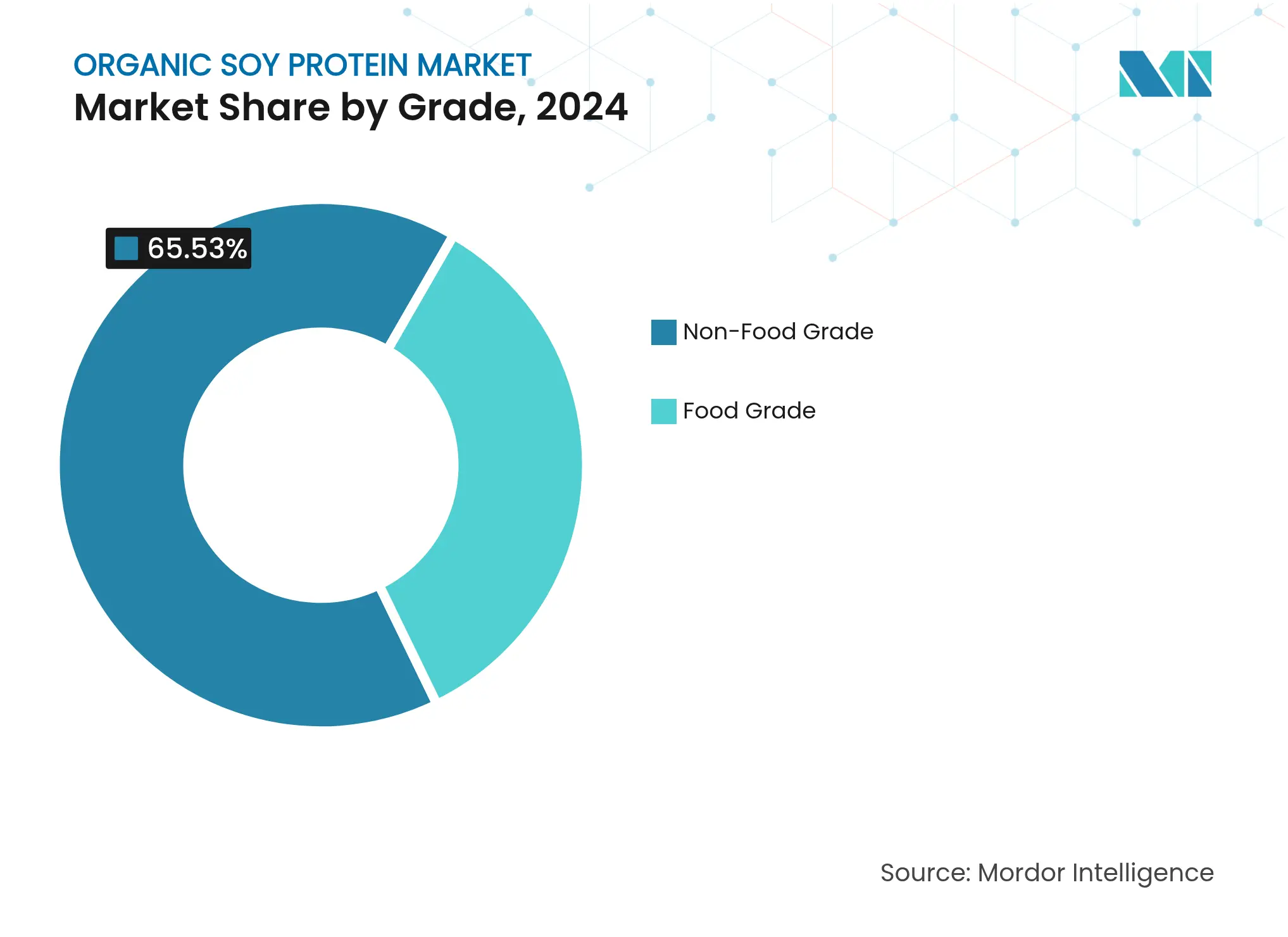

- By grade, food-grade products accounted for 34.47% share of the soy protein market size in 2024, while non-food-grade products are rising at a 10.48% CAGR.

- By geography, North America led with 38.65% of soy protein market share in 2024; Asia-Pacific is projected to grow at an 11.78% CAGR to 2030.

Global Organic Soy Protein Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) %Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising demand for clean-label and organic products Rising demand for clean-label and organic products | +2.1% | North America, Europe premium markets | Medium term (2-4years) | (~) %Impact on CAGR Forecast:+2.1% | Geographic Relevance:North America, Europe premium markets | Impact Timeline:Medium term (2-4years) |

Growing popularity of plant-based protein Growing popularity of plant-based protein | +1.8% | Global, led by North America and Asia-Pacific | Long term (≥4years) | |||

Increased application in sports and functional nutrition Increased application in sports and functional nutrition | +1.4% | North America and Europe core, expanding to Asia-Pacific | Short term (≤2years) | |||

Increasing use of soy protein in infant formula Increasing use of soy protein in infant formula | +1.2% | Global, with regulatory advantages in Asia-Pacific | Medium term (2-4years) | |||

Support from the government and organic certification bodies Support from the government and organic certification bodies | +0.9% | North America and Europe, emerging Asia-Pacific | Long term (≥4years) | |||

Expansion of vegan and flexitarian diets Expansion of vegan and flexitarian diets | +1.1% | Global, culture-specific variance | Long term (≥4years) | |||

| Source: Mordor Intelligence | ||||||

Rising demand for clean label and organic products

Consumer scrutiny of food ingredient lists has intensified the shift toward recognizable, minimally processed components, positioning soy protein as a preferred alternative to synthetic additives in food formulation. The USDA organic certification process, while requiring 3-year transition periods and higher production costs, generates price premiums of USD 6-9 per bushel for organic soybeans compared to conventional varieties. The certification cost burden, ranging from USD 400,000 to USD 890,000 for relabeling compliance, creates barriers for smaller processors while benefiting established players with scale advantages according to FDA (Food and Drug Administration). Processing innovations that eliminate hexane extraction, such as aqueous extraction methods, address consumer concerns about chemical residues while maintaining protein functionality. The trend toward clean label formulations particularly benefits soy protein isolates, which offer neutral taste profiles that enable manufacturers to reduce artificial flavoring while maintaining product palatability.

Growing popularity of plant-based protein

The plant-based protein market has evolved from niche health food applications to mainstream food manufacturing, with soy protein offering a complete amino acid profile that provides advantages in formulation compared to other plant proteins. The Asia-Pacific region shows significant market growth potential due to traditional consumption patterns of soy-based foods and halal certification benefits. Soy protein's environmental benefits, including reduced land and water usage compared to animal protein production, align with companies' environmental, social, and governance (ESG) commitments. Food manufacturers increasingly utilize soy protein to meet protein content requirements under FDA labeling guidelines for plant-based alternatives. Recent technological developments in processing methods, such as high hydrostatic pressure treatments, have enhanced soy protein's functional properties, enabling its use in premium plant-based products where texture and mouthfeel are essential.

Increased application in sports and functional nutrition

The convergence of sports nutrition and mainstream food categories has elevated soy protein's profile beyond traditional protein powder applications, with 82% of consumers having tried soy products according to ADM's market research. Regulatory support strengthens this trend, with the FDA's continued endorsement of soy protein's cardiovascular benefits providing marketing advantages over newer plant proteins lacking established health claims. The sports nutrition segment particularly benefits from soy protein isolates' rapid absorption rates and leucine content, which matches whey protein's muscle protein synthesis capabilities while addressing lactose intolerance concerns affecting 68% of the global population [1]National Institute of Diabetes and Digestive and Kidney Diseases, "Definition & Facts for Lactose Intolerance", niddk.nih.gov. Processing innovations that enhance solubility and reduce off-flavors, such as enzymatic hydrolysis techniques that achieve 50-70% degree of hydrolysis, enable incorporation into ready-to-drink beverages where taste and texture are paramount. The functional food trend intersects with GLP-1 therapy adoption, where high-protein formulations become essential for maintaining muscle mass during weight loss, creating new market opportunities for soy protein in medical nutrition applications.

Increasing use of soy protein in infant formula

Soy protein isolate's role in infant nutrition has evolved beyond allergy management to become a mainstream alternative, with U.S. infants consuming soy-based formulas and higher adoption rates in countries like New Zealand and Israel. The American Academy of Pediatrics' endorsement of soy protein formulas as safe and effective alternatives to cow's milk formulas provides regulatory confidence that supports market expansion [2]Healthy Children, "Choosing a Baby Formula", healthychildren.org. Technical advances in soy protein isolate production, including membrane ultrafiltration and enzymatic processing, have improved digestibility while reducing anti-nutritional factors like phytates that previously limited mineral absorption. The Indonesian Pediatrics Association's recognition of soy isolate protein formula as a safe alternative for cow's milk protein allergy management demonstrates growing international acceptance beyond traditional Western markets. Market dynamics favor soy protein isolates over concentrates in infant formula applications due to higher protein purity and reduced allergenicity, with processing costs justified by premium pricing in this specialized segment.

Restraints Impact Analysis

| Restraint | (~) %Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Availability of other plant-based proteins Availability of other plant-based proteins | -1.6% | North America and Europe | Medium term (2-4years) | (~) %Impact on CAGR Forecast:-1.6% | Geographic Relevance:North America and Europe | Impact Timeline:Medium term (2-4years) |

Rising soy allergies in consumers Rising soy allergies in consumers | -0.8% | North America and Europe | Long term (≥4years) | |||

High cost of organic certification and production High cost of organic certification and production | -1.0% | North America and Europe premium markets, emerging in Asia-Pacific | Medium term (2-4years) | |||

Price volatility and import dependency Price volatility and import dependency | -1.2% | Global, with acute impact in China and import-dependent regions | Short term (≤2years) | |||

| Source: Mordor Intelligence | ||||||

Availability of other plant-based proteins

The plant protein market has seen increased competition against soy protein, particularly from pea protein, which offers benefits such as being allergen-free and having a neutral taste that simplifies food formulation. This shift is part of a broader market trend where companies like Bunge are expanding their protein portfolios to include faba, lentil, and mung proteins to address diverse functional and nutritional needs. Investment trends show increased funding for alternative protein sources rather than traditional soy applications, which may constrain soy protein's growth in new market segments. Regulatory developments support this diversification, as demonstrated by Health Canada's guidelines on pea protein safety and the FDA's draft labeling requirements for plant-based alternatives, which create uniform standards across protein sources. While soy protein historically held a cost advantage in processing, this gap has narrowed as alternative protein production has increased, though soy protein retains its position in areas requiring complete amino acid profiles and established regulatory compliance, especially in infant nutrition.

Rising soy allergies in consumers

FDA regulations classify soy as a major allergen, requiring mandatory labeling that affects product adoption, especially in processed foods where allergen-free claims offer market advantages. FDA's allergen labeling enforcement, exemplified by recalls such as the Daiso biscuit case for undeclared soy, demonstrates the regulatory oversight impacting manufacturing processes. Processing facilities handling multiple allergens face cross-contamination risks, resulting in higher compliance costs and operational challenges, particularly for small manufacturers without dedicated allergen-free production lines. Rising consumer awareness of food allergies, including soy sensitivities, influences product formulation decisions across market segments. The widespread use of soy in processed foods, both as a primary ingredient and processing aid, requires comprehensive allergen management and supply chain transparency, which increases procurement costs. However, manufacturers benefit from well-established soy allergen control protocols, providing operational stability compared to emerging plant protein alternatives.

Segment Analysis

By Form: Isolates Drive Premium Applications

Protein concentrates dominate the market with a substantial 48.17% share in 2024, maintaining their position as the preferred choice in the protein ingredients segment. Their widespread adoption is primarily driven by cost-effectiveness compared to other protein forms. These concentrates are particularly valuable in conventional food applications where moderate protein content is sufficient. The ability of protein concentrates to meet functional requirements while keeping production costs manageable makes them attractive to food manufacturers. Additionally, their versatility and ease of incorporation into various food products contribute to their continued market leadership.

Isolates represent the fastest-growing segment with a 10.29% CAGR through 2030, driven by their use in sports nutrition and infant formula applications where protein purity exceeds 90% [3]Science Direct, "Whey proteins processing and emergent derivatives: An insight perspective from constituents, bioactivities, functionalities to therapeutic applications", sciencedirect.com. The production process requires approximately 3 tons of defatted soybeans to produce 1 ton of isolate, with premium pricing compensating for higher manufacturing costs. New processing methods, such as gas-supported screw-pressed techniques, enhance isolate functionality while reducing environmental impact compared to hexane extraction. FDA regulations support isolate market growth by permitting specific health claims for products containing at least 6.25 grams of soy protein per serving. The market shows a trend toward premium products, with isolates gaining value in applications where functional properties justify higher costs, while concentrates remain dominant in cost-sensitive food manufacturing.

Note: Segment shares of all individual segments available upon report purchase

By Application: Supplements Accelerate Growth

The food and beverage segment dominates the soy protein market with a 34.47% share in 2024, primarily due to its widespread adoption in various food applications. Soy protein's established regulatory status and functional properties make it a preferred choice in bakery products, dairy alternatives, and meat substitutes. The ingredient's versatility and nutritional profile contribute to its growing acceptance across different food categories. The USDA's revised guidelines now permit tofu and soy yogurt inclusion in school meal programs, significantly expanding institutional market opportunities. According to these guidelines, 2.2 ounces of tofu containing 5 grams of protein can be credited as 1 ounce of meat alternative, further strengthening soy protein's position in institutional food service.

Supplements represent the fastest-growing application at 11.23% CAGR, driven by sports nutrition trends and medical nutrition applications that require specific protein bioavailability and amino acid profiles. The overlap between food and supplement categories creates opportunities for functional foods with high protein concentrations while maintaining food-like taste and texture. Infant formula applications command premium pricing and require specialized processing to meet safety and nutritional standards, despite lower volumes. The regulatory environment supports supplement applications, as FDA draft guidance on plant-based alternatives provides clear pathways for protein content claims.

By Grade: Food Grade Maintains Dominance

Food-grade soy protein holds a 34.47% market share in 2024, supported by established food safety protocols and regulatory approvals across food and beverage applications. The USDA requirements for alternate protein products specify a minimum 18% protein content and 80% biological quality compared to casein, establishing clear standards for food-grade product development. The stringent quality control measures and documentation requirements ensure consistent product quality and safety across all food applications. Consumer demand for plant-based protein alternatives has further strengthened the position of food-grade soy protein in premium food products and nutritional supplements. The market favors food-grade products in applications requiring regulatory compliance and consumer acceptance, while non-food-grade products compete in commodity applications based on price.

Non-food grade applications demonstrate a 10.48% CAGR, with increased adoption in animal feed formulations and industrial uses where lower purity requirements provide cost benefits. The processing differences between grades reflect varying quality control needs, as food-grade products require additional testing and documentation to comply with FDA food additive regulations. The biotechnology regulatory framework, overseen jointly by EPA, FDA, and USDA, imposes additional compliance requirements for genetically modified soy proteins, affecting grade classification and market positioning. Advances in processing technology, including new soy protein concentrates with enhanced functionality, are reducing traditional grade distinctions as manufacturers develop application-specific products.

Geography Analysis

North America holds 38.65% share of the global soy protein market in 2024, supported by established processing infrastructure and regulatory frameworks. The region's integrated supply chains connect soybean production with processing facilities, though transportation infrastructure limitations in production areas increase logistics costs. The FDA's health claim approvals for soy protein products and USDA organic certification programs create market opportunities, despite higher production costs. North American market maturity encourages premium application development, exemplified by Green Bison Soy Processing's (ADM-Marathon joint venture) investments in renewable diesel integration.

Asia-Pacific demonstrates the highest growth rate at 11.78% CAGR through 2030, primarily due to China's focus on domestic protein production and traditional acceptance of soy-based foods. China's 90% dependency on soybean imports presents supply vulnerabilities, which the government addresses through domestic production incentives and protein alternatives. Singapore's regulatory leadership in cultivated meat and plant-based alternatives, combined with regional investments in alternative protein research, supports market growth. China's shift from U.S. to Brazilian soybean imports due to tariffs influences regional supply chain strategies.

Europe prioritizes domestic protein production through policy initiatives and funding programs to reduce import reliance. Germany's EUR 38 million investment in sustainable protein development demonstrates regional commitment. The market favors sustainably sourced soy protein products, while facing competition from regional alternatives like pea and faba proteins. Brazil, as the global soybean production leader, encounters infrastructure limitations affecting processing development. The Middle East and Africa show potential for growth due to increasing populations and protein demand, but face processing infrastructure and regulatory constraints.

Competitive Landscape

Market Concentration

The soy protein market exhibits significant fragmentation, indicating substantial consolidation opportunities as established players leverage scale advantages in processing technology and supply chain integration. Some of the key players include Archer Daniels Midland Company, SunOpta Inc., Bunge Limited, Cargill Incorporated, among others. Major processors like ADM and Cargill, Incorporated, pursue vertical integration strategies, combining soybean crushing with protein isolation and downstream product development to capture value across the supply chain.

Strategic partnerships increasingly focus on technology integration rather than traditional capacity expansion, exemplified by Cargill's collaboration with ENOUGH to develop mycoprotein alternatives that complement existing soy protein portfolios. Processing innovation emerges as a key differentiator, with companies investing in proprietary extraction methods that improve functional properties while reducing environmental impact. Opportunities exist in specialized applications where soy protein's complete amino acid profile provides advantages over alternative plant proteins, particularly in medical nutrition and infant formula segments, where regulatory barriers favor established ingredients.

Emerging disruptors focus on processing technology rather than raw material control, with companies like Benson Hill developing enhanced soybean varieties that deliver higher protein content and improved yield potential. Patent activity in soy protein processing, including high hydrostatic pressure treatments and enzymatic modification techniques, indicates continued innovation focus on functional property enhancement. Market dynamics favor companies with integrated supply chains and technical capabilities to develop application-specific products, while commodity processors face margin pressure from raw material price volatility and competition from alternative protein sources.

Organic Soy Protein Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Bunge introduced a new range of soy protein concentrates at IFFA, with a planned launch in fall. These concentrates address key challenges in the plant-based protein market by offering neutral color, clean taste, and cost efficiency for food manufacturers. The production of these soy protein concentrates takes place at Bunge's facility in Morristown, Indiana, aligning with the company's expansion of plant-protein products.

- March 2025: New Protein International, based in Ontario, is developing Canada's first large-scale soybean processing facility in Sarnia. The company, co-founded by farmer Martin Vanderloo, aims to process 70,000 tonnes of soybeans annually, producing more than 17,000 tonnes of soy protein and food-grade byproducts. The facility will employ over 100 people and support Canada's domestic soy protein production capabilities while offering export opportunities.

- September 2024: Scoular is set to begin operations at its new canola and soybean oilseed crush facility in October. The facility will serve producers targeting renewable fuels markets and animal feed protein meal markets. The facility has been retrofitted to process 11 million bushels of oilseeds annually.

Table of Contents for Organic Soy Protein Industry Report

1. Introduction

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising Demand for Clean Label and Organic Products

- 4.2.2Growing Popularity of Plant-Based Protein

- 4.2.3Increased Application in Sports and Functional Nutrition

- 4.2.4Increasing Use of Soy Protein in Infant Formula

- 4.2.5Support from Government and Organic Certification Bodies

- 4.2.6Expansion of Vegan and Flexitarian Diets

- 4.3Market Restraints

- 4.3.1Availability of Other Plant-Based Proteins

- 4.3.2Rising Soy Allergies in Consumers

- 4.3.3High Cost of Organic Certification and Production

- 4.3.4Price Volatility and Import Dependency

- 4.4Supply-Chain Analysis

- 4.5Regulatory Outlook

- 4.6Technological Outlook

- 4.7Porter’s Five Forces Analysis

- 4.7.1Threat of New Entrants

- 4.7.2Bargaining Power of Buyers

- 4.7.3Bargaining Power of Suppliers

- 4.7.4Threat of Substitutes

- 4.7.5Competitive Rivalry

5. Market Size and Growth Forecasts (Value)

- 5.1By Form

- 5.1.1Concentrates

- 5.1.2Isolates

- 5.1.3Textured/Hydrolyzed

- 5.2By Application

- 5.2.1Food and Beverages

- 5.2.1.1Bakery and Confectionery

- 5.2.1.2Snacks

- 5.2.1.3Dairy and Dairy Alternative Products

- 5.2.1.4Meat/Poultry/Seafood and Meat Alternative Products

- 5.2.1.5Beverages

- 5.2.1.6Other Food Applications

- 5.2.2Supplements

- 5.2.2.1Sport/Performance Nutrition

- 5.2.2.2Baby Food and Infant Formula

- 5.2.2.3Elderly Nutrition and Medical Nutrition

- 5.2.3Animal Feed

- 5.2.4Personal Care and Cosmetics

- 5.3By Grade

- 5.3.1Food Grade

- 5.3.2Non-Food Grade

- 5.4By Geography

- 5.4.1North America

- 5.4.1.1United States

- 5.4.1.2Canada

- 5.4.1.3Mexico

- 5.4.1.4Rest of North America

- 5.4.2Europe

- 5.4.2.1Germany

- 5.4.2.2United Kingdom

- 5.4.2.3Italy

- 5.4.2.4France

- 5.4.2.5Spain

- 5.4.2.6Netherlands

- 5.4.2.7Poland

- 5.4.2.8Belgium

- 5.4.2.9Sweden

- 5.4.2.10Rest of Europe

- 5.4.3Asia-Pacific

- 5.4.3.1China

- 5.4.3.2India

- 5.4.3.3Japan

- 5.4.3.4Australia

- 5.4.3.5Indonesia

- 5.4.3.6South Korea

- 5.4.3.7Thailand

- 5.4.3.8Singapore

- 5.4.3.9Rest of Asia-Pacific

- 5.4.4South America

- 5.4.4.1Brazil

- 5.4.4.2Argentina

- 5.4.4.3Colombia

- 5.4.4.4Chile

- 5.4.4.5Peru

- 5.4.4.6Rest of South America

- 5.4.5Middle East and Africa

- 5.4.5.1South Africa

- 5.4.5.2Saudi Arabia

- 5.4.5.3United Arab Emirates

- 5.4.5.4Nigeria

- 5.4.5.5Egypt

- 5.4.5.6Morocco

- 5.4.5.7Turkey

- 5.4.5.8Rest of Middle East and Africa

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Strategic Moves

- 6.3Market Ranking Analysis

- 6.4Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1Archer Daniels Midland Company

- 6.4.2SunOpta Inc.

- 6.4.3Devansoy Inc.

- 6.4.4Sonic Biochem

- 6.4.5Bunge Limited

- 6.4.6Cargill, Incorporated.

- 6.4.7Foodchem International Corporation

- 6.4.8GROUPE BERKEM

- 6.4.9The Scoular Company

- 6.4.10Laybio

- 6.4.11ORGANIC PROTEIN

- 6.4.12Wilmar International Ltd.

- 6.4.13Shiv Health Foods LLP (Prowise)

- 6.4.14Eklavya Biotech Private Limited

- 6.4.15Chaitanya Agro Biotech Pvt. Ltd.

- 6.4.16International Flavors & Fragrances Inc

- 6.4.17Sun Nutrafoods

- 6.4.18Bioway Organic Ingredients CO., LTD.

- 6.4.19FUJI OIL CO., LTD.

- 6.4.20Farbest Brands (Farbest-Tallman Foods Corporation)

7. Market Opportunities and Future Outlook

Global Organic Soy Protein Market Report Scope

The organic soy protein market is diversely segmented by product type into concentrates, isolates, and textured protein. Organic soy proteins are differentiated by their use in Bakery and Confectionery, Meat Extenders and Substitutes, Nutritional Supplements, Beverages and other applications. Moreover, the organic soy protein market can be segmented on the basis of geography.