Soy Protein Concentrate Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 4.18 Billion |

| Market Size (2031) | USD 5.29 Billion |

| Growth Rate (2026 - 2031) | 4.82% CAGR |

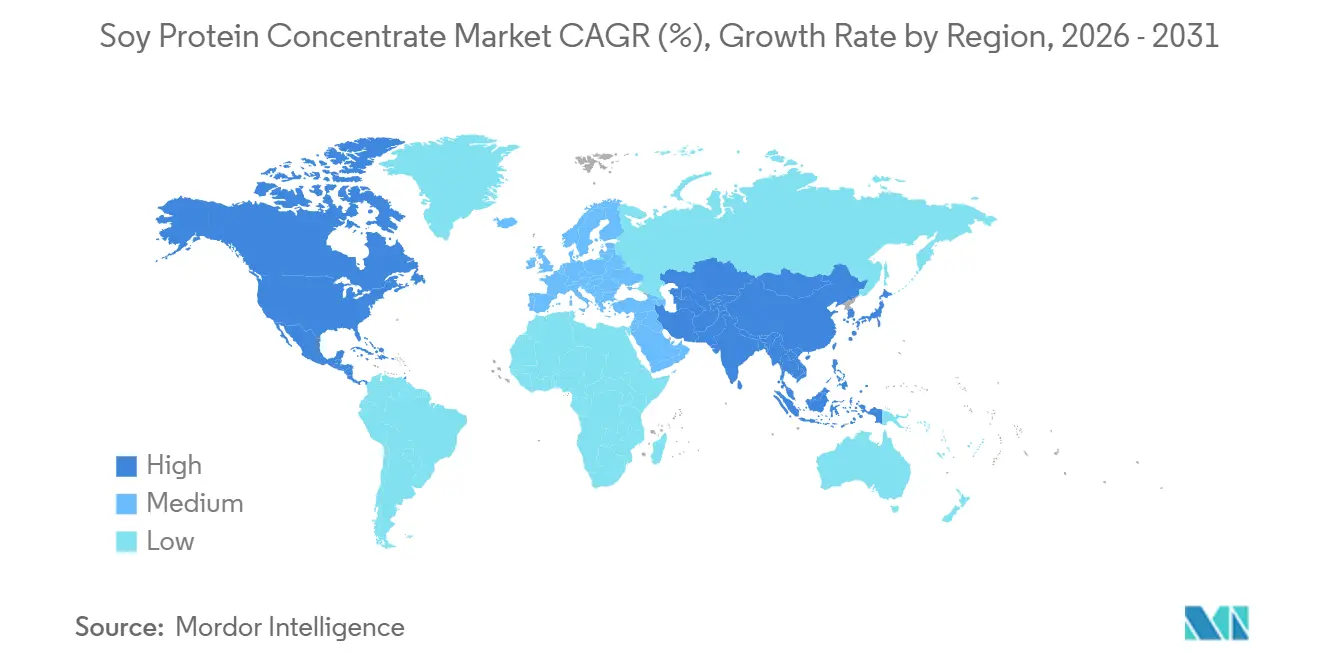

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

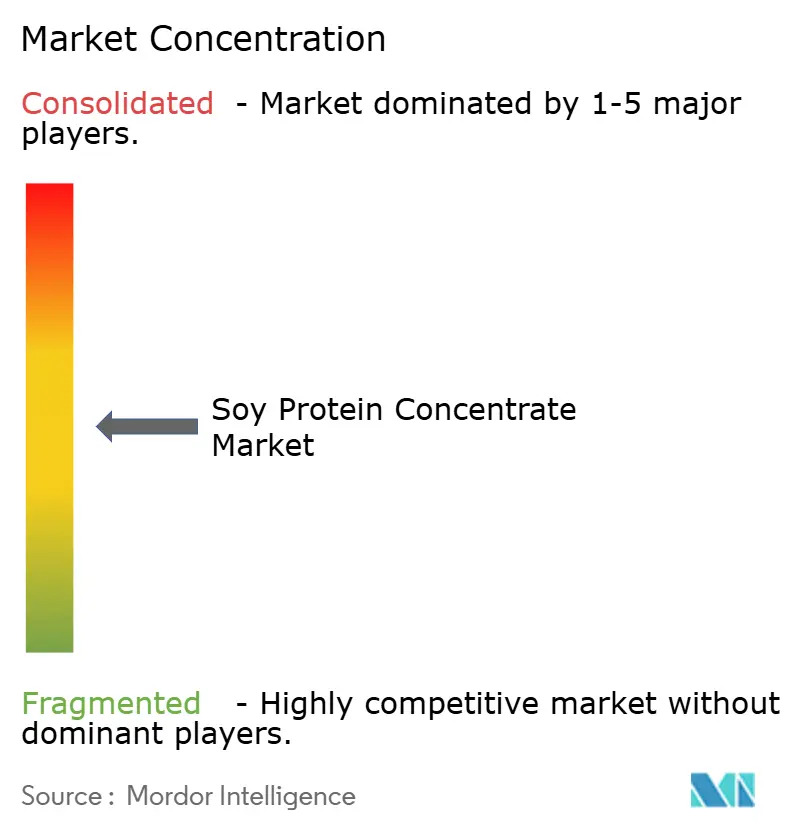

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Soy Protein Concentrate Market Analysis by Mordor Intelligence

The soy protein concentrate market size was valued at USD 4.02 billion in 2025 and is estimated to grow from USD 4.18 billion in 2026 to reach USD 5.29 billion by 2031, at a CAGR of 4.82% over 2026-2031. While demand remains strong for cost-sensitive animal feed, there's a notable surge in clean-label nutritional and health supplements. This trend is not only elevating average selling prices but also motivating processors to pivot towards higher-margin organic and liquid formats. Fluctuating soybean prices are squeezing margins, leading major players to consolidate assets. They're also ramping up digital traceability efforts, aiming to leverage premiums from European Union Deforestation Regulation compliance as a buffer against raw-material inflation. Production is increasingly centered in North America and Brazil, bolstered by new crush capacities that ensure a steady meal supply for soy protein concentrate production. The competitive landscape is moderately intense; while the top four companies command nearly 45% of global capacity, there's a noticeable fragmentation in supply. This is especially evident in premium organic and blockchain-verified niches, where smaller specialists are swiftly making their mark.

Key Report Takeaways

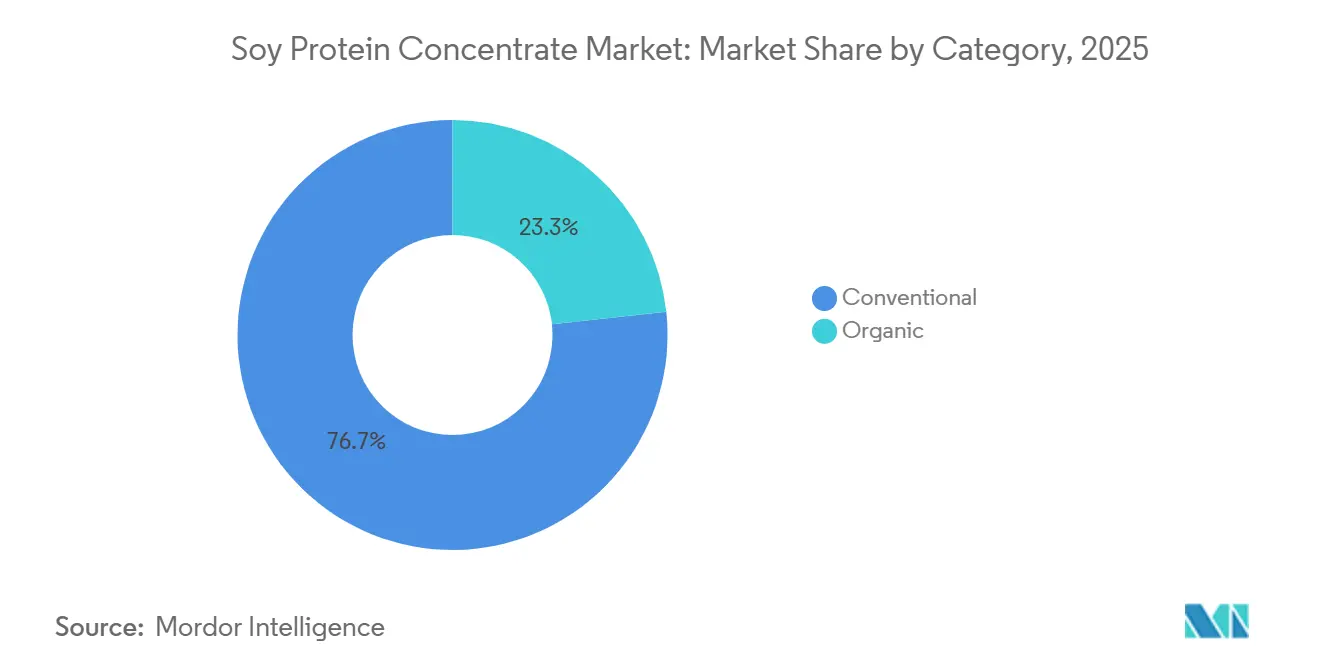

- By category, conventional formulations held 76.72% of 2025 revenue, while organic variants represent the fastest-growing category at a 6.81% CAGR over 2026-2031.

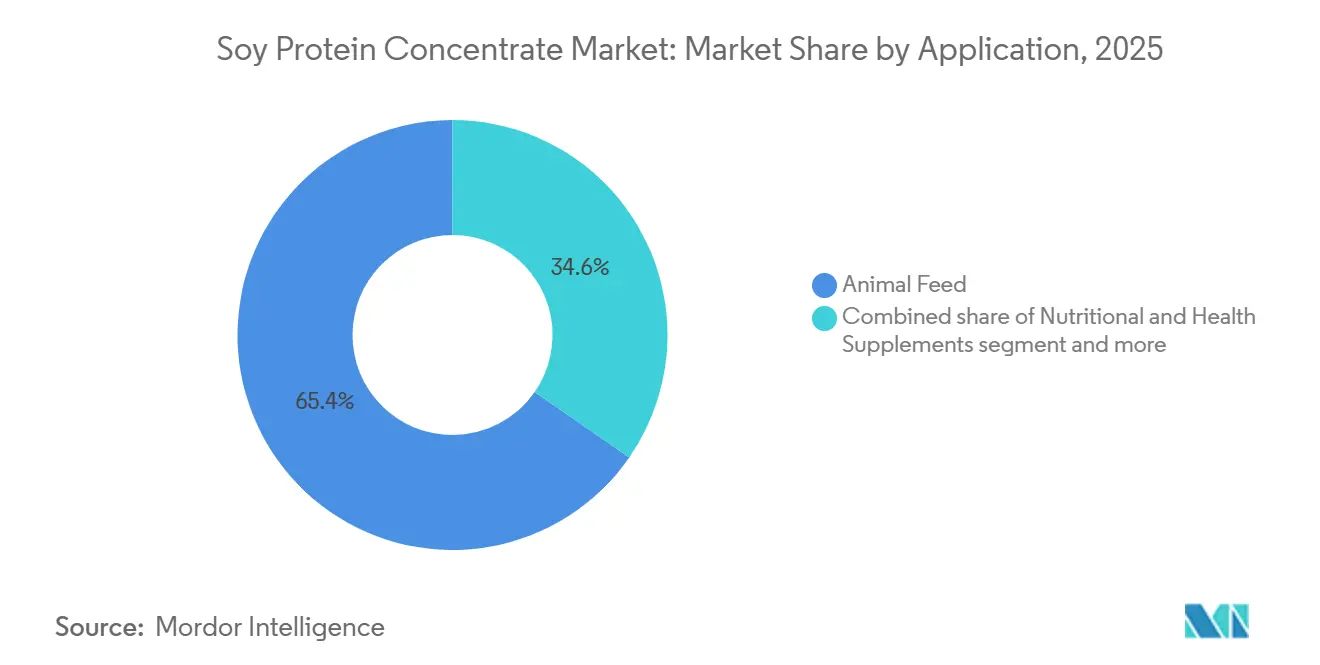

- By application, animal feed commanded 65.36% of 2025 revenue, while nutritional and health supplements are projected to expand at the fastest 5.67% CAGR through 2031.

- By geography, North America led regional demand with 35.40% of 2025 sales, yet Asia-Pacific is forecast to deliver the quickest 5.92% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Soy Protein Concentrate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for plant-based proteins in food products | +1.2% | Global, with a concentration in North America and Europe | Medium term (2-4 years) |

| Expanding use in animal feed and aquaculture industries | +1.5% | Asia-Pacific core (Thailand, Indonesia, Vietnam), spill-over to South America | Long term (≥ 4 years) |

| Clean-label and sustainability positioning | +0.8% | North America and Europe, emerging in urban Asia-Pacific | Medium term (2-4 years) |

| Cost-effective alternative to animal proteins | +0.7% | Global, particularly price-sensitive markets in South America and the Middle East | Short term (≤ 2 years) |

| Surging adoption of liquid SPC in RTD nutrition beverages | +0.6% | North America and Europe, early adoption in China | Short term (≤ 2 years) |

| Blockchain-enabled traceability unlocking premium contracts | +0.4% | Europe (EUDR compliance), North America (voluntary sustainability programs) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Plant-Based Proteins in Food Products

Across the bakery, snack, and dairy alternative sectors, flexitarian diets are revolutionizing protein sourcing. Soy protein concentrate, with its neutral flavor profile and protein content ranging from 65% to 72%, serves as a bridge between the more common soy flour and the premium isolates. Projections from the United States Department of Agriculture for the 2025/26 period anticipate a domestic soybean crush of 2.49 billion to 2.55 billion bushels. This record-setting figure is largely fueled by the rising biodiesel demand for soybean oil, subsequently boosting the availability of soybean meal and protein concentrate. Manufacturers of dairy alternatives are gravitating towards soy protein concentrate, sidelining pea and rice proteins, as soy's PDCAAS score of 1.0, on par with casein, allows for "complete protein" labeling on packaging without the need for amino acid fortification. In a strategic move, Nestlé and Danone have revamped several of their plant-based yogurt SKUs, integrating soy protein concentrate. This shift not only diminishes their dependence on the imported pea protein isolate, which comes with a 15% to 20% price premium and extended lead times, but also underscores the growing preference for soy in the industry.

Expanding Use in Animal Feed and Aquaculture Industries

In Southeast Asia, aquaculture is rapidly transitioning from fishmeal to plant proteins. Thailand's Department of Fisheries highlights that soybean meal now makes up 41% of aquafeed ingredients, with the country's annual demand for soy protein concentrate fluctuating between 33,000 and 44,000 tonnes. Meanwhile, Indonesia's GERPARI program aims to replace 20% to 40% of fishmeal in diets for shrimp and tilapia. This move addresses the nation's heavy reliance on fishmeal imports, which stand at 70%, and the unpredictable landings of Peruvian anchovy. Soy protein concentrate, boasting a protein content of 67% to 72% and better amino acid digestibility than soybean meal, enables feed mills to achieve desired weight gain rates. This advantage also translates to cost savings of USD 30 to USD 50 per tonne in feed formulation. The aquaculture sector within the Association of Southeast Asian Nations produces over 9 million tonnes annually. With a feed consumption exceeding 20 million tonnes, this translates to a protein demand exceeding 6 million tonnes each year. Such figures underscore the strategic advantage of soy protein concentrate in the region's aquaculture landscape.

Surging Adoption of Liquid SPC in RTD Nutrition Beverages

Liquid soy protein concentrate formulations streamline the ready-to-drink beverage manufacturing process by eliminating the reconstitution step. This innovation not only reduces water usage by 12% to 15% but also shortens the batch cycle time by 20 minutes for every 5,000-liter run. Abbott Nutrition, alongside other infant formula producers, is assessing the potential of liquid soy protein concentrate for their soy-based formulas, including Similac Isomil. The use of this concentrate ensures consistent protein dispersion and minimizes foam formation, leading to improved fill accuracy and decreased product loss during aseptic packaging. The U.S. Food and Drug Administration mandates specific standards for infant formulas, including protein digestibility-corrected amino acid scores and certain micronutrient fortifications. Liquid soy protein concentrate not only meets these stringent standards but also provides logistical advantages to co-manufacturers. Unlike powdered ingredients that necessitate dedicated blending equipment and dust-control systems, the liquid form simplifies the process. Furthermore, sports nutrition brands are now infusing liquid soy protein concentrate into high-protein shakes, specifically targeting lactose-intolerant consumers. This demographic, making up 65% to 70% of the global adult population, has been largely overlooked by the predominant whey-based product offerings.

Blockchain-Enabled Traceability Unlocking Premium Contracts

Bunge has implemented Justoken blockchain technology on 375,000 tonnes of Brazilian soy shipments. This move offers European buyers unalterable records detailing farm coordinates, harvest dates, and assessments of deforestation risks. These records help meet the European Union Deforestation Regulation's due diligence requirements, well ahead of the enforcement date set for December 30, 2026. Similarly, Archer Daniels Midland, in collaboration with Farmers Business Network, has rolled out the re:source program. This initiative grants North American soy protein concentrate buyers enhanced traceability, facilitating Scope 3 emissions reporting and adherence to Science Based Targets initiative protocols. Processors lacking blockchain capabilities are seeing price discounts ranging from 5% to 8%. This is largely due to the rising demands for digital traceability from European food manufacturers and halal certifiers in the Middle East. Additionally, Saudi Arabia has embraced the Gulf Standardization Organization's GSO 1354:2022 standard for soy protein products. Effective March 1, 2024, this standard mandates origin documentation and halal certification, solidifying the importance of traceability in contract terms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile soybean commodity prices and supply fluctuations | -0.6% | Global, acute in import-dependent regions (the Middle East, North Africa) | Short term (≤ 2 years) |

| Competition from other plant proteins | -0.5% | North America and Europe, emerging in the Asia-Pacific urban centers | Medium term (2-4 years) |

| Allergenicity and mandatory labeling constraints | -0.3% | Global, stringent enforcement in North America, Europe, and Australia | Long term (≥ 4 years) |

| Deforestation-linked Scope-3 compliance pressure on soy sourcing | -0.4% | Europe (EUDR-driven), North America (voluntary corporate commitments) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile Soybean Commodity Prices and Supply Fluctuations

Forecasts for the 2025/26 marketing year predict U.S. soybean prices will rise to between USD 10.25 and USD 10.30 per bushel, up from USD 9.95 in 2024/25. This increase is attributed to a reduction in planted acreage, with 83.5 million acres in 2025 compared to 87.1 million in 2024, alongside a strong demand for biodiesel feedstock, according to the USDA WASDE Report[3]Source: U.S Food and Drug Administration, "WASDE Report", fda.gov. In Brazil, soybean prices jumped from USD 400 per tonne in 2025 to USD 450 in 2026. This surge is due to tight global stocks and a robust demand from China, which accounted for 58.7% of Brazil's soybean exports in 2025[1]Source: ABIOVE Market Report, “Brazilian Soybean Crush 2026,” ABIOVE.ORG . Processors of soy protein concentrate typically operate on net margins of 3% to 5%. This narrow margin makes them susceptible to spikes in input costs, which they can't always pass on to animal feed customers, especially since these customers often benchmark prices against soybean meal. Weather-related disruptions in Argentina, the world's third-largest soybean producer, have heightened supply volatility. The 2024/25 crop is projected at 48 million tonnes, a decline from the 51 million tonnes seen in previous years, which in turn limits the country's soy protein concentrate production.

Deforestation-Linked Scope-3 Compliance Pressure on Soy Sourcing

Starting December 30, 2026, the European Union Deforestation Regulation requires all soy products, including soy protein concentrate, entering the EU to provide plot-level geolocation data and proof of zero deforestation since December 31, 2020. Operators must submit due diligence statements before customs clearance, facing penalties like product seizure and fines up to 4% of annual EU turnover for non-compliance. Brazilian soy protein concentrate exporters are under heightened scrutiny; data from the United Nations Food and Agriculture Organization reveals that 19% of Brazil's soy expansion from 2000 to 2020 encroached on previously forested areas. In response, processors lacking farm-level traceability are pivoting shipments to non-EU markets. This has led to a split supply chain, with EUDR-compliant soy protein concentrate fetching a premium of 5% to 8%. Meanwhile, North American buyers, including industry giants ADM and Bunge, are voluntarily aligning with these standards. Both have committed to no-deforestation sourcing by 2025, a promise that entails supplier audits, satellite monitoring, and third-party verification. These added measures inflate landed soy protein concentrate prices by an additional USD 8 to USD 12 per tonne.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Category: Organic Certification Drives Premium Positioning

In 2025, conventional soy protein concentrate captured 76.72% of the market revenue, bolstered by established supply chains and lower raw material costs, typically USD 50 to USD 80 per tonne less than their organic counterparts. Its broad acceptance spans animal feed and industrial food applications. Meanwhile, organic soy protein concentrate is on a growth trajectory, expanding at a 6.81% CAGR through 2031. This surge is largely driven by stringent regulations like the European Union's Organic Regulation 2018/848 and the USDA's National Organic Program[2]Source: European Commission, “Organic Regulation 2018/848,” EUROPA.EU . These regulations enforce non-GMO sourcing, mandate pesticide-free cultivation, and impose a three-year land transition period. Furthermore, organic formulations enjoy a retail price premium of 25% to 35% in sectors like dairy alternatives and sports nutrition. Here, consumers equate certification with cleaner ingredients and a commitment to environmental stewardship.

Conventional soy protein concentrate continues to dominate cost-sensitive sectors, including poultry feed, bakery mixes, and processed meats. In these areas, its functional benefits, like water binding, emulsification, and texture enhancement, take precedence over origin claims. On the other hand, organic soy protein concentrate grapples with supply limitations. In 2025, certified soybean acreage in the U.S. was a mere 245,000 acres, accounting for less than 0.3% of total soy plantings. This scarcity restricts processors from scaling production without entering multi-year contracts and offering premium payments to farmers. Brazil's organic soy sector is still in its infancy, boasting fewer than 50,000 hectares under certification. Yet, industry giants like Bunge and Solbar are venturing into organic soy protein concentrate lines, targeting European buyers. These buyers demand both EUDR compliance and organic certification, a dual requirement met by fewer than 10 global suppliers.

By Application: Nutritional Supplements Outpace Commodity Feed

Animal feed, comprising 65.36% of 2025 demand, is projected to grow at a 4.5% CAGR through 2031, below the market average. Rising corn and soybean meal costs are prompting poultry and swine producers to adopt lower-protein diets supplemented with synthetic amino acids. Nutritional and health supplements are growing at 5.67% annually, driven by sports nutrition brands reformulating whey-based products with soy protein concentrate for lactose-free and vegan claims, and infant formula manufacturers expanding soy-based SKUs in regions with high cow's milk protein allergy prevalence (2%-3% of infants globally, per WHO Nutrition). The food and beverage sector is advancing at a 4.9% CAGR, led by bakery and snacks replacing wheat gluten and dairy proteins with soy protein concentrate for clean-label compliance and allergen diversification. Dairy and dairy alternatives dominate this segment, leveraging soy protein concentrate's emulsification properties in plant-based yogurts, creamers, and cheese analogs. Seafood and meat alternatives are the fastest-growing sub-segment, with brands like Nestlé's Garden Gourmet and Unilever's The Vegetarian Butcher using soy protein concentrate for fibrous texture and umami flavor in burger patties and fish-free fillets.

Beverages, including ready-to-drink protein shakes and fortified juices, are adopting liquid soy protein concentrate to streamline manufacturing and improve shelf stability. Bakery applications use soy protein concentrate as a dough conditioner and moisture retainer, extending packaged bread shelf life by 2-3 days. Snack manufacturers blend soy protein concentrate into extruded puffs and bars to boost protein content from 8% to 15% without compromising texture. Sport and performance nutrition products target athletes seeking plant-based protein with complete amino acid profiles. Baby food and infant formula, regulated by the FDA's 21 CFR 107, require minimum protein levels of 1.8 grams per 100 kilocalories. Soy-based formulas like Abbott's Similac Isomil and Nestlé's Alsoy hold 10%-12% of the global infant formula market, serving families with lactose intolerance or vegan preferences. Elderly and medical nutrition products use soy protein concentrate in oral supplements and tube feeds for patients with dysphagia or malnutrition, prioritizing digestibility and low allergenicity.

Geography Analysis

Processing equipment manufacturers increasingly design systems specifically for soy protein concentrate handling, indicating industry commitment to long-term capacity expansion and technological advancement in protein extraction methods. The region's competitive advantage stems from established infrastructure, including dedicated soy protein concentrate production lines and distribution networks that reduce logistics costs compared to imported alternatives. North America leads with 35.40% market share in 2025, benefiting from integrated soybean production and processing infrastructure that enables cost-competitive concentrate manufacturing while maintaining quality consistency across large-scale operations.

Asia-Pacific emerges as the fastest-growing region at 5.92% CAGR, driven by expanding aquaculture industries requiring cost-effective fishmeal alternatives and growing demand for affordable protein sources in processed foods targeting price-sensitive consumer segments. The U.S. Soybean Export Council's 2025 Asia report highlights significant market potential across the region, particularly in processed food applications where soy protein concentrate's cost-performance profile aligns with manufacturer requirements for protein functionality without premium pricing. India's processed food sector expansion creates demand for protein ingredients that enhance nutritional profiles while maintaining competitive pricing in price-sensitive consumer markets. Japan and Australia represent mature markets with sophisticated food processing industries that drive demand for specialized concentrate grades in functional food applications where cost-performance optimization guides ingredient selection.

Europe represents a strategically important market characterized by regulatory support for alternative proteins and consumer preferences for locally-sourced ingredients, though supply constraints may limit growth potential as domestic soybean production remains insufficient to meet processing demand. In South America, countries like Brazil and Mexico are gradually expanding their soy protein concentrate market presence, driven by growing investments in food processing and plant-based protein manufacturing. Growth drivers in the Middle East and Africa include rising consumer awareness of plant-based proteins, increasing demand for affordable and nutritious protein sources amid population growth, and investments in food industry advancements.These geographic features and regional socioeconomic factors shape the gradual but steady rise of soy protein concentrate demand in these markets.

Competitive Landscape

The soy protein concentrate market exhibits moderate concentration, reflecting a competitive environment where established agricultural processors leverage integrated supply chains while specialized protein companies focus on value-added processing and application development. Major players, including ADM, Bunge Global SA, and other integrated agricultural companies, benefit from vertical integration spanning soybean sourcing through concentrate production, enabling cost control and quality consistency that smaller processors struggle to match. Strategic patterns emphasize operational efficiency and technological differentiation rather than pure cost competition, as companies invest in processing improvements and functional property enhancements to create competitive advantages in specific application segments.

These market leaders emphasize sustainability credentials, including non-GMO and environmentally responsible sourcing, aligning with increasing consumer demand for transparent and eco-friendly protein ingredients. Their strategic investments in processing technologies and partnerships aim to enhance product versatility for applications ranging from meat alternatives and dairy substitutes to nutritional supplements and animal feed. Apart from that, they use plant expansion startegies to stay competitive.

Meanwhile, regional players, particularly in Asia-Pacific and Latin America, contribute to a more dynamic and diverse competitive environment by capitalizing on local raw material availability and rising regional health awareness. The market also faces challenges such as raw material price fluctuations and consumer concerns around soy allergies and GMO perception, encouraging companies to differentiate through branding, hypoallergenic formulations, and clean-label product offerings. Overall, the SPC market reflects moderate concentration among a few established firms but continues to witness growing innovation and new entrants driven by escalating global demand for affordable, functional, and sustainable plant-based proteins.

Soy Protein Concentrate Industry Leaders

-

The Scoular Company

-

Foodchem International Corporation

-

Archer Daniels Midland Company (ADM)

-

New Protein Global Inc.

-

Bunge Global SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Bunge Global SA completed the acquisition of IFF's soy protein and lecithin business for an undisclosed sum, adding approximately USD 240 million in annual revenue and production facilities in Memphis, Tennessee.

- May 2025: Bunge unveiled a new line of soy protein concentrates at IFFA, targeting prevalent challenges in the plant-based protein sector. These concentrates aim to provide food manufacturers with a clean taste, neutral color, and a cost-effective solution. Produced at Bunge’s new facility in Morristown, Indiana, these soy protein concentrates align with the company's strategy to bolster its plant-protein portfolio.

- May 2025: In response to the rising global appetite for sustainable, plant-based proteins, Bunge poured EUR 484M into a soy protein facility, solidifying its leadership stance in the burgeoning plant-based protein market. The newly minted facility is set to process an extra 4.5 million bushels of soybeans each year, churning out both soy protein concentrates and textured soy protein concentrate.

Global Soy Protein Concentrate Market Report Scope

Soy protein concentrate (SPC) is a refined plant-based protein derived from dehulled and defatted soybeans. The global Soy protein concentrate market is segmented by category, application, and geography. By category, the market is segmented into conventional and organic. By application, the market is segmented into food and beverages, nutritional and health supplements, and animal feed. The food and beverages segment is further sub-segmented into bakery, snacks, dairy and dairy alternative products, seafood and meat alternative products, beverages, and other food applications. Similarly, the nutritional and health supplements segment is further sub-segmented into sport/performance nutrition, baby food and infant formula, and elderly nutrition and medical nutrition. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The Market Forecasts are Provided in Terms of Value (USD).

| Conventional |

| Organic |

| Food and Beverages | Bakery |

| Snacks | |

| Dairy and Dairy Alternative Products | |

| Seafood and Meat Alternative Products | |

| Beverages | |

| Other Food Applications | |

| Nutritional and Health Supplements | Sport/Performance Nutrition |

| Baby Food and Infant Formula | |

| Elderly Nutrition and Medical Nutrition | |

| Animal Feed |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Peru | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| Category | Conventional | |

| Organic | ||

| Application | Food and Beverages | Bakery |

| Snacks | ||

| Dairy and Dairy Alternative Products | ||

| Seafood and Meat Alternative Products | ||

| Beverages | ||

| Other Food Applications | ||

| Nutritional and Health Supplements | Sport/Performance Nutrition | |

| Baby Food and Infant Formula | ||

| Elderly Nutrition and Medical Nutrition | ||

| Animal Feed | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Peru | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the soy protein concentrate market in 2026?

The soy protein concentrate market size is estimated at USD 4.18 billion in 2026, advancing toward USD 5.29 billion by 2031, according to Mordor Intelligence.

Which segment will grow fastest through 2031?

Nutritional and health supplements are projected to record the quickest 5.67% CAGR through 2031, driven by sports-nutrition shakes and infant-formula reformulations.

What share does animal feed hold within current demand?

Animal feed accounted for 65.36% of 2025 revenue, making it the largest application segment of the soy protein concentrate market.

Why is Asia-Pacific pivotal for future growth?

Asia-Pacific is forecast to post a 5.92% CAGR through 2031, supported by aquafeed demand in Thailand and Indonesia and expanding dairy-alternative uptake in China and India.

Page last updated on: