Small Form Factor (SFF) PC Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

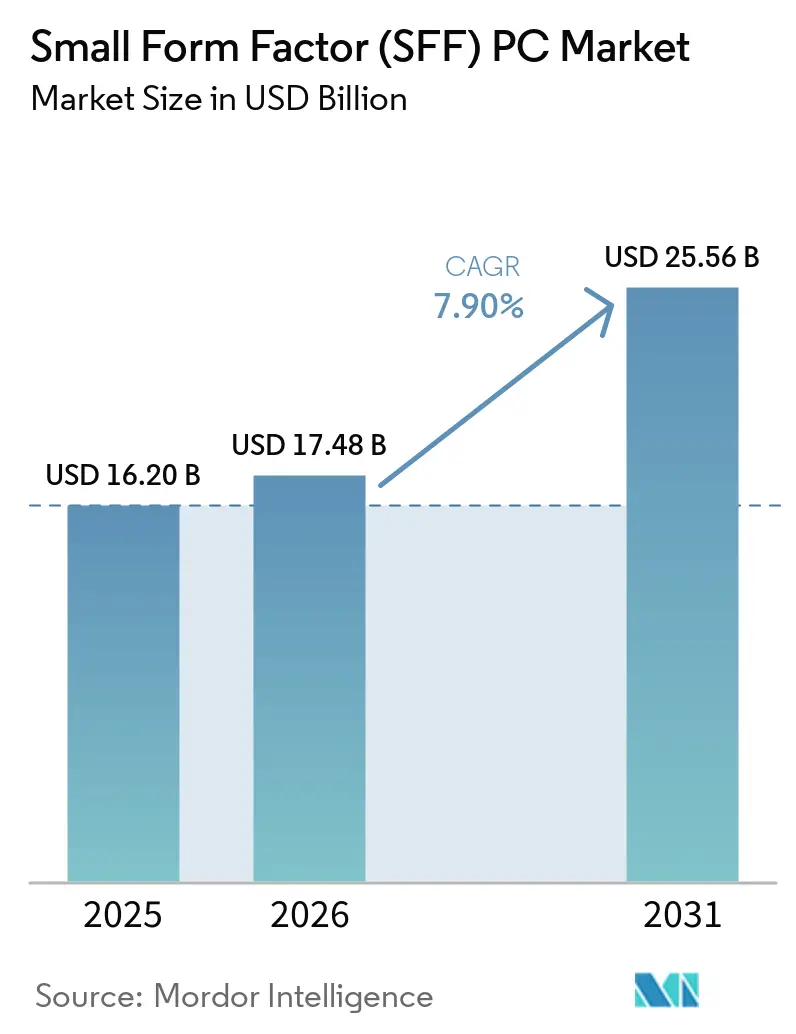

| Market Size (2026) | USD 17.48 Billion |

| Market Size (2031) | USD 25.56 Billion |

| Growth Rate (2026 - 2031) | 7.90% CAGR |

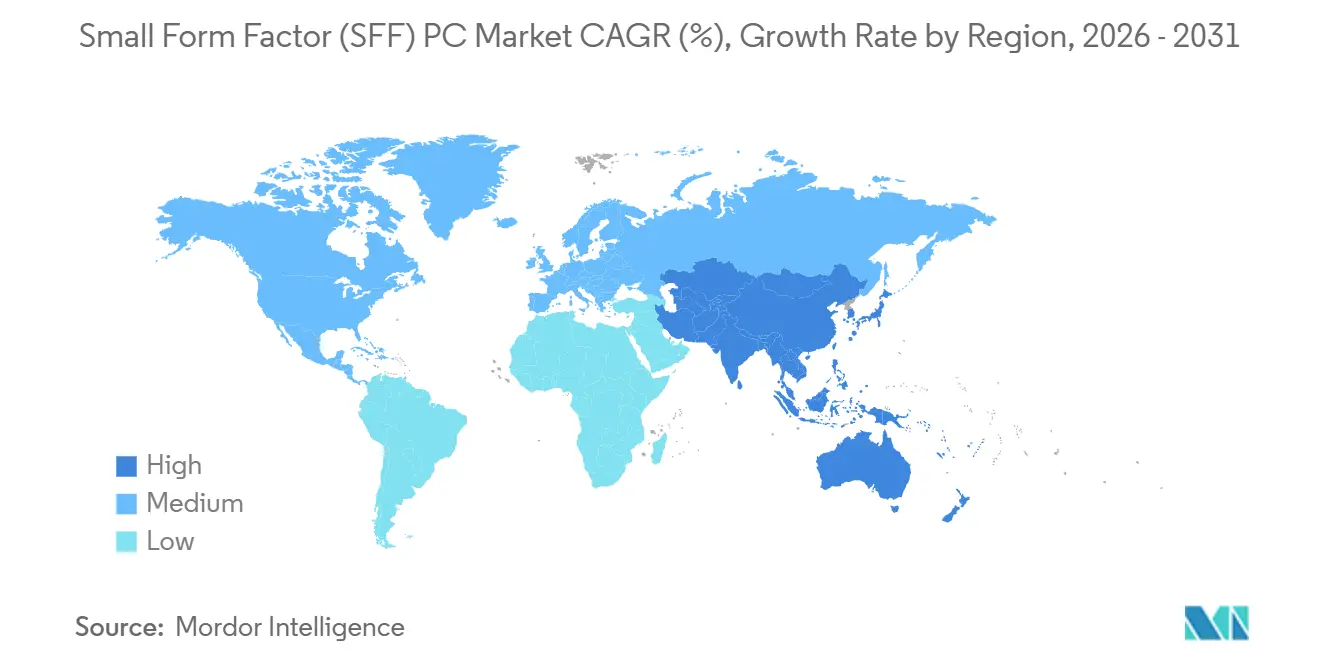

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

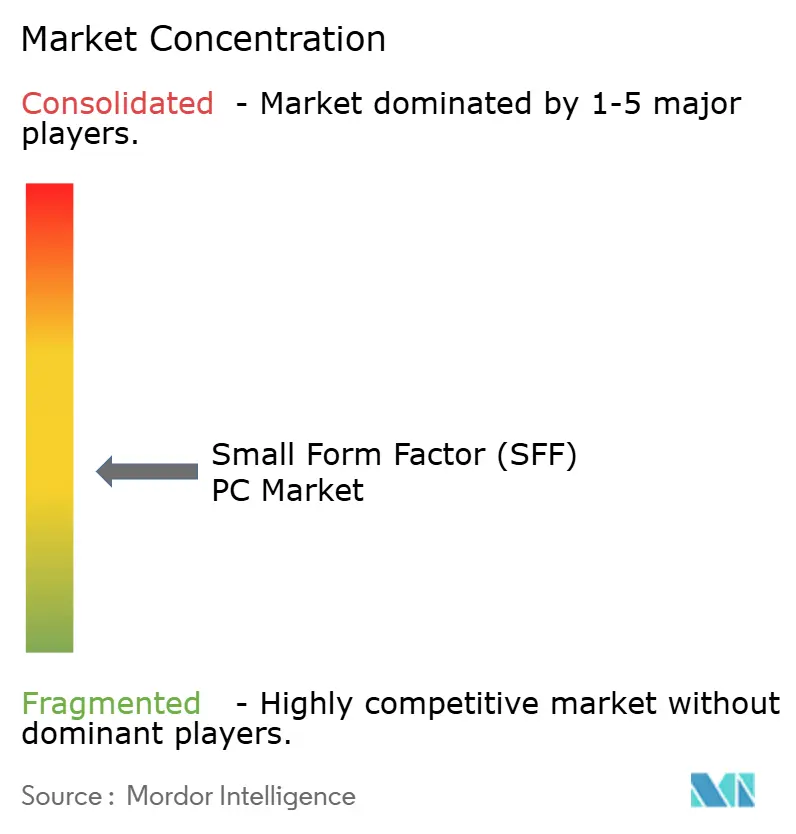

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Small Form Factor (SFF) PC Market Analysis by Mordor Intelligence

The Small Form Factor PC market size increased from USD 16.2 billion in 2025 to USD 17.48 billion in 2026 and is projected to reach USD 25.56 billion by 2031, expanding at a 7.9% CAGR between 2026 and 2031. This upward path reflects a permanent shift toward hybrid work setups, on-device AI adoption, and thermal-design innovation that allows compact systems to match tower-class performance without enlarging power budgets. Enterprises now favor mini-desktops that tuck behind monitors, gamers accept sub-3-liter rigs that hold discrete GPUs, and edge-computing projects standardize on rugged fanless boxes for analytics at the data source. Component vendors continue to prioritize performance-per-watt roadmaps, which sustain the Small Form Factor PC market momentum across consumer, commercial, and industrial settings. Channel dynamics also reinforce growth as integrators bundle hardware with vertical software and support, while e-commerce platforms capture value from enthusiasts and home office buyers.

Key Report Takeaways

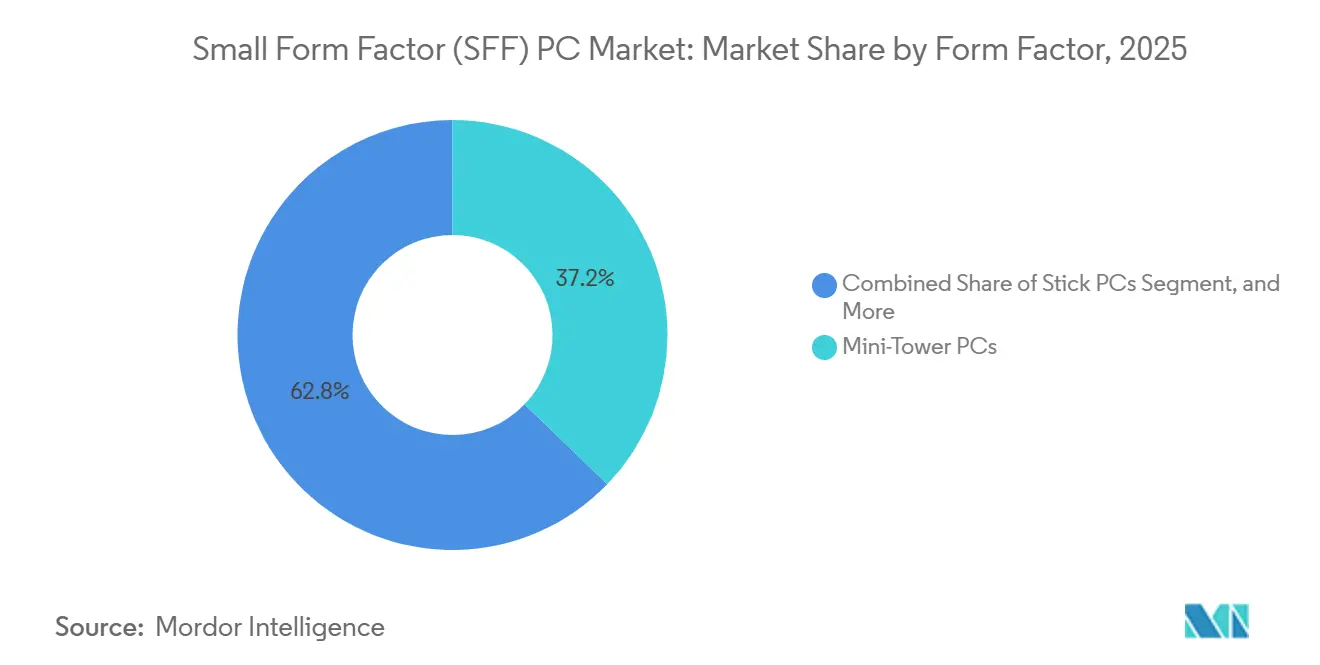

- By Form Factor, Mini-tower PCs held 37.2% of 2025 revenue, whereas stick PCs are advancing at a 10.9% CAGR through 2031.

- By Component, GPUs are expanding at an 11.1% CAGR and are on track to outpace CPUs, which commanded 23.8% of 2025 component revenue.

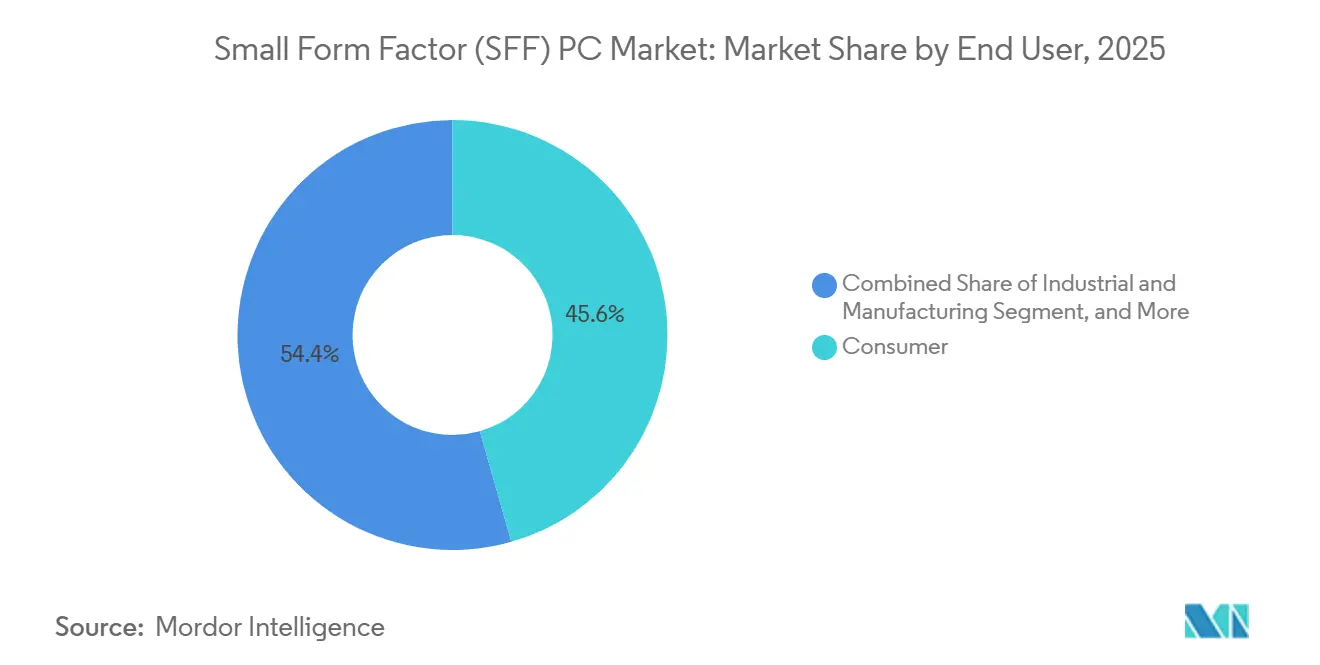

- By End User, Consumer applications led with 45.6% revenue in 2025, but industrial deployments are posting a 10.4% CAGR as factories replace panel PCs with rugged mini systems.

- By Distribution Channel, E-commerce controlled 53.9% of sales in 2025, while direct B2B relationships are growing at a 9.2% CAGR by bundling SFF hardware with vertical software stacks.

- By Geography, Asia-Pacific captured 37.7% of 2025 revenue and is forecast to expand at an 11.3% CAGR as semiconductor localization incentives and OEM clustering accelerate regional supply chains.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Small Form Factor (SFF) PC Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for Home Office Setups Post Pandemic | +1.8% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Rising Popularity of PC Gaming and Esports | +1.5% | Global, led by Asia-Pacific and North America | Medium term (2-4 years) |

| Advances in High-Performance, Low-Power Components | +1.3% | Global | Long term (≥4 years) |

| Shift Toward Space-Saving IT Infrastructure in Enterprises | +1.2% | North America, Europe, Asia-Pacific urban centers | Medium term (2-4 years) |

| OEM Adoption of Compute in Display Digital Signage Deployments | +0.9% | Global retail and transportation hubs | Short term (≤2 years) |

| Government Incentives for Edge Computing Hardware Localization | +0.7% | Asia-Pacific and North America | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Home Office Setups Post Pandemic

Hybrid work has normalized dual-location computing, pushing employees to select systems that fit limited desk real estate without trading performance. Small Form Factor units pair high-core-count CPUs and integrated graphics inside a 2-liter chassis, enabling multi-monitor 4K productivity at home while remaining portable enough for office hot-desks.[1]ASUS Editorial Team, “NUC 16 Pro,” ASUSTeK Computer, asus.com Corporate IT teams prefer these units because shipping, storage, and cooling costs fall versus traditional towers, and employees who enjoy compact desktops at home lobby for identical hardware at work, driving refresh orders toward mini-tower and ultra-small designs.

Rising Popularity of PC Gaming and Esports

Competitive gaming has embraced compact rigs that integrate desktop-class processors and RTX-series GPUs inside sub-3-liter cases. Form-factor guidelines published by NVIDIA in 2024 define GPU length, height, and power ceilings to streamline SFF builds, encouraging adopters to spec full-performance cards without thermal guesswork.[2]NVIDIA Corporation, “SFF-Ready Enthusiast GeForce Card Guidelines,” nvidia.com Esports venues turn to these lighter systems to cut freight and setup time, while content creators value the freed desk space for streaming equipment. Rapid WiFi 7 adoption removes the last tethered advantage of tower PCs, further validating portable gaming desktops.

Advances in High-Performance, Low-Power Components

Processor roadmaps now measure success by performance per watt, which directly benefits Small Form Factor designs that cannot dissipate more than 65 watts without liquid cooling. AMD’s Zen 5-based Ryzen AI PRO 400 Series delivers up to 50 TOPS inside a 28-watt envelope, supporting fanless AI workloads in industrial mini-PCs.[3]Advanced Micro Devices, “AMD Ryzen AI PRO 400 Series Processors,” amd.comIntel’s Core Ultra Series 2 provides up to 96 TOPS in a 0.46-liter BRIX chassis while staying within USB Power Delivery ranges. Solid-state cooling, such as Frore Systems’ AirJet, propagates silent, dust-free operation in stick PCs, narrowing the gap between compact and tower performance envelopes.

Shift Toward Space-Saving IT Infrastructure in Enterprises

Rising office densification compels IT managers to reclaim floor space, so mini-desktops that VESA-mount behind monitors or slot into racks are replacing towers. Dell’s Pro 5 Micro measures 1.2 liters yet includes full enterprise manageability, letting firms deploy zero-footprint workstations and cut cable clutter.[4]Dell Technologies, “Pro 5 Micro,” dell.com HP embeds compute boards into displays, reducing asset counts and easing cleaning protocols in open offices. Lower heat output trims HVAC budgets, and rugged variants allow retailers and factories to position compute at the edge without building dedicated server rooms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Upgrade Flexibility Compared to Full-Tower PCs | -0.8% | Global | Medium term (2-4 years) |

| Thermal Management Challenges in Compact Chassis | -0.6% | Global, acute in gaming and workstation segments | Short term (≤2 years) |

| Price Premium of High-Density Components | -0.5% | Global, stronger in emerging markets | Short term (≤2 years) |

| Rising E-Waste Regulation Compliance Costs for Miniaturized Systems | -0.3% | Europe and United Kingdom, expanding in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Upgrade Flexibility Compared to Full-Tower PCs

SFF motherboards, external power bricks, and soldered memory curtail user upgrades to storage or select SO-DIMMs, forcing entire-unit replacements for major performance gains. Educational buyers and small businesses face a higher total cost when GPU or CPU leaps demand new systems rather than a single part swap. In regions with high import tariffs, the economics of full replacements discourage specification of SFF hardware for long-life deployments.

Thermal Management Challenges in Compact Chassis

Placing desktop-class CPUs and discrete GPUs in sub-3-liter volumes produces heat densities beyond passive cooling limits. Manufacturers resort to high-RPM fans that introduce noise and dust, while fanless industrial units must cap CPU TDPs around 28 watts, excluding powerful GPUs. Solid-state cooling chips and vapor chambers ease the problem but raise bill-of-materials cost, delaying deployment in price-sensitive verticals.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form Factor: Demand Concentrates in Stick and Mini-Tower Designs

Stick PCs hold the fastest trajectory at a 10.9% CAGR as digital signage networks plug HDMI-sized units into displays, removing the need for separate housings. The Small Form Factor PC market size tied to this form factor benefits from fanless layouts that draw power over USB and support 4K playback for point-of-sale kiosks and meeting-room casting. Mini-tower PCs retained 37.2% of 2025 revenue, upheld by enterprise demand for tool-free maintenance and full-height PCIe slots, yet their share will gradually yield to ultra-smalls as thermals improve. Ultra-small and rugged variants empower edge analytics nodes in transportation and manufacturing, adding higher margins through shock-proof casings and extended temperature ratings.

Server-class innovation trickles into consumer cubes where 65-watt desktop CPUs now coexist with laptop-tier RTX GPUs, letting gamers assemble LAN-ready rigs under three kilograms. The Small Form Factor PC market share for stick models stays minor in value terms but leads volume count, as educational programs buy thousands of units to convert old monitors into Chromebox-style endpoints. Healthcare carts and hospital imaging suites migrate toward sub-1.5-liter desktops that mount behind displays to keep aisles free of tower bases, illustrating the application diversity supported by maturing thermal solutions.

By Component: GPU Revenue Surges Ahead of CPUs

GPU shipments are forecast to rise 11.1% each year, eclipsing average system growth because discrete cards or solder-down accelerators now appear in both gaming and AI edge nodes. The Small Form Factor PC market size for GPU-equipped models benefits from NVIDIA’s SFF-Ready program that limits card length and power draw, guaranteeing drop-in fit for mini-ITX builders. CPU revenue still rules the bill of materials at 23.8%, but grows more modestly as integrated NPUs offload AI inference from central cores. DDR5 SO-DIMMs, PCIe 5.0 NVMe SSDs, and tiny GaN power adapters gain share as platform watt density climbs, and solid-state AirJet coolers slide into BOMs for fanless premium builds.

Component suppliers profit from balance-of-system shifts: motherboards for ultrasmalls embed WiFi 7, dual 2.5-gigabit Ethernet, and Thunderbolt 4, raising ASPs despite smaller PCB sizes. Vendors also push external 330-watt adapters for gaming cubes, selling high-margin accessories that lift total revenue per unit. As supply chains localize under CHIPS-funded fabs, North American and Japanese memory producers may shorten lead times for SFF OEMs seeking to hedge geopolitical risk.

By End User: Industrial Deployments Outpace Consumer Units

Industrial and manufacturing buyers are adopting fanless mini-PCs for machine vision, SCADA control, and predictive maintenance analytics at a 10.4% CAGR. The Small Form Factor PC market share for consumer applications remains the largest through 2031, yet growth slows as the home-office surge normalizes. Factories favor rugged aluminum chassis with DIN-rail mounts and extended temperature tolerance, replacing aging panel computers with software-defined boxes that can be re-imaged from the cloud. Commercial offices retrofit call centers and trading floors with VESA-mounted desktops that cut desk clutter and noise, aligning with corporate hot-desking policies.

Healthcare forms a rising secondary vertical as EN 60601-certified mini-systems support imaging workstations and patient-data carts in environments that restrict electromagnetic interference. Education budgets stretch farther by installing stick PCs in libraries and labs, avoiding tower maintenance overhead. Defense and aerospace remain niche yet lucrative, demanding MIL-STD shock and vibration compliance plus supply-chain transparency for security audits.

By Distribution Channel: Integrators Gain on Service Bundles

Direct B2B sales will climb 9.2% yearly as integrators combine hardware, vertical software, and managed services into single invoices for hospitals, retailers, and smart-building operators. Although e-commerce captured 53.9% of 2025 shipments, its share settles as purchase complexity rises and enterprises prefer turnkey deployments with SLAs. Retail storefronts decline but survive on impulse and immediate-pickup transactions in mature markets. System integrators exploit the Small Form Factor PC market size expansion by embedding diagnostic agents and remote-update frameworks, monetizing lifecycle management instead of margin-thin hardware.

Acer’s 2026 investment in Plugable Technologies underscores OEM intent to own the accessory stack around mini-desktops, anchoring customers with bundled docks and cables that ease multi-monitor setups. Chinese online marketplaces amplify price pressure on Western brands, yet integrators differentiate through firmware customization, local support centers, and compliance documentation that bulk buyers need for tenders.

Geography Analysis

Asia-Pacific drove 37.7% of 2025 revenue and is expected to grow 11.3% a year through 2031, propelled by semiconductor incentives in Japan and Taiwan, OEM density in Shenzhen and Taipei, and rising disposable incomes in India. Tokyo’s subsidies for edge-AI hardware and Taiwan’s R and D tax credits encourage locally assembled mini-PCs, shortening supply chains and lowering lead times for regional buyers. Chinese brands such as MINISFORUM leverage Shenzhen’s ecosystem to iterate designs quarterly and price products 20% below multinational peers, widening domestic penetration. India’s digitization of public services and the boom in IT outsourcing fuel demand for compact desktops in call centers and coding hubs despite import duties on components.

North America captures an outsized share of enterprise refresh cycles thanks to CHIPS Act funds that localize CPU and DRAM production and reduce risk of Asian supply disruptions. U.S. businesses replace aging towers with mini-desktops to reduce energy bills and free office real estate, while education districts deploy stick PCs for Chromebook-style labs. Canada follows similar patterns in banking and public administration. Energy-efficiency regulations steer buyers toward low-idle-power designs that meet ENERGY STAR 8.0 targets.

Europe remains a steady adopter, with Germany, France, and the United Kingdom meeting green-procurement criteria that favor compact PCs assembled with recycled plastic and supporting WEEE take-back mandates. The United Kingdom’s 2025 regulatory update lifts producer-responsibility costs for miniaturized electronics, pressuring vendors to optimize packaging and recycling logistics. Southern and Eastern Europe select rugged SFF units for factory upgrades under EU digitalization grants, while Nordic countries pioneer zero-carbon offices that integrate fanless desktops powered by renewable microgrids.

South America, the Middle East, and Africa collectively represent a smaller yet rising slice of the Small Form Factor PC market size. Brazil’s government IT buys low-power mini-PCs for schools to cut utility bills. Saudi Arabia and the United Arab Emirates deploy edge-analytics nodes for smart-city kiosks and surveillance, albeit dependent on imported parts that expose them to shipping volatility. Nigeria and Kenya invest in co-working hubs that rely on compact desktops where power-backup systems favor lower-wattage hardware, though inconsistent grid stability hampers mass adoption.

Competitive Landscape

Competitive rivalry sits at a moderate level as global PC majors vie with specialist brands and ODMs. Dell, HP, Lenovo, ASUS, and Acer translate brand trust and enterprise contracts into volume, while MINISFORUM, Zotac, Simply NUC, and Shuttle differentiate on rapid iteration, enthusiast features, and aggressive pricing. Intel’s decision to exit direct NUC manufacturing in 2023 ceded ground that ASUS and MSI filled with Core Ultra-based cubes, tightening margins in the sub-2-liter niche. AMD partners with MINISFORUM on co-engineered systems that showcase Ryzen AI silicon, ensuring optimized thermals and firmware.

Emergent technology defines the battlefield. Vendors integrating WiFi 7, Thunderbolt 4, and USB4 gain enterprise mindshare, while Frore Systems’ AirJet chips enable silent variants that attract libraries, studios, and medical offices. Chinese e-commerce brands undercut global OEMs by 25-30%, compelling incumbents to lean on service, compliance, and multi-year warranty bundles to protect share. Environmental regulation becomes a moat in Europe, where ISO 14001 certifications and proven recycling channels unlock municipal tenders that exclude non-compliant suppliers.

White-space opportunities include AI-optimized edge appliances under 5 liters, fanless industrial boxes rated from -40 °C to 70 °C, and modular chassis with slide-out GPU carriers that let engineers hot-swap accelerators without exceeding volume limits. HP’s Z8 Fury side-panel expander exemplifies this push toward mid-cycle upgradeability inside compact footprints. As DDR5 and NVMe prices climb on datacenter demand, some vendors hedge by offering barebones kits so buyers can source storage and memory locally, preserving headline price points while sustaining unit velocity.

Small Form Factor (SFF) PC Industry Leaders

ASUSTeK Computer Inc.

Lenovo Group Limited

HP Inc.

Dell Technologies Inc.

Intel Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Acer Gadget invested in Plugable Technologies to expand its USB-C and Thunderbolt accessory lineup and lock peripherals to its mini-PC ecosystem.

- March 2026: HP launched the ZGX Nano deskside and ZGX Fury rack-ready AI workstations plus the Z8 Fury G6i desktop featuring a tool-free Max Side Panel expander, targeting edge-AI deployments.

- January 2026: MSI unveiled the Cubi NUC AI+ 3MG ultra-compact Copilot+ PC with Intel Core Ultra Series 3 processors, WiFi 7, and recycled-plastic chassis.

- November 2025: ASUS Republic of Gamers introduced the ROG GR70 gaming mini-PC integrating Ryzen 9 9955HX3D and RTX 5070 Laptop GPU inside a sub-3-liter case.

Global Small Form Factor (SFF) PC Market Report Scope

The Small Form Factor (SFF) PC Market comprises compact desktop computers designed to deliver full desktop performance within significantly reduced chassis volumes, compared to traditional ATX mid-tower cases. SFF PCs utilize specialized mini-ITX motherboards, low-profile cooling solutions, and compact power supplies while supporting high-end desktop CPUs, GPUs, and upgradeable RAM/storage for gaming, content creation, and professional workstations.

The Small Form Factor PC Report is Segmented by Form Factor (Mini-Tower PCs, Small Desktop PCs, Ultra-Small Form Factor PCs, Stick PCs, Rugged and Industrial SFF PCs), Component (CPU, GPU, Motherboard, Memory, Storage, Power Supply, Cooling System), End User (Consumer, Commercial Office, Industrial and Manufacturing, Healthcare, Education, Media and Entertainment, Defense and Aerospace), Distribution Channel (E-Commerce, Retail Stores, Direct B2B Sales, System Integrators and VARs), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Mini-Tower PCs |

| Small Desktop PCs |

| Ultra-Small Form Factor PCs |

| Stick PCs |

| Rugged and Industrial SFF PCs |

| CPU |

| GPU |

| Motherboard |

| Memory |

| Storage |

| Power Supply |

| Cooling System |

| Consumer |

| Commercial Office |

| Industrial and Manufacturing |

| Healthcare |

| Education |

| Media and Entertainment |

| Defense and Aerospace |

| E-Commerce |

| Retail Stores |

| Direct B2B Sales |

| System Integrators and VARs |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Kenya | |

| Rest of Africa |

| By Form Factor | Mini-Tower PCs | |

| Small Desktop PCs | ||

| Ultra-Small Form Factor PCs | ||

| Stick PCs | ||

| Rugged and Industrial SFF PCs | ||

| By Component | CPU | |

| GPU | ||

| Motherboard | ||

| Memory | ||

| Storage | ||

| Power Supply | ||

| Cooling System | ||

| By End User | Consumer | |

| Commercial Office | ||

| Industrial and Manufacturing | ||

| Healthcare | ||

| Education | ||

| Media and Entertainment | ||

| Defense and Aerospace | ||

| By Distribution Channel | E-Commerce | |

| Retail Stores | ||

| Direct B2B Sales | ||

| System Integrators and VARs | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected value of the Small Form Factor PC market by 2031?

The market is forecast to reach USD 25.56 billion by 2031 according to Mordor Intelligence.

Which component category is growing fastest in Small Form Factor PCs?

The GPU segment is expanding at an 11.1% CAGR as gaming and edge-AI workloads adopt discrete graphics, per Mordor Intelligence.

Which region will lead future growth for compact PCs?

Asia-Pacific is expected to grow at an 11.3% CAGR through 2031, driven by semiconductor incentives and OEM clustering.

Why are industrial users adopting Small Form Factor PCs rapidly?

Factories are replacing panel PCs with rugged fanless units for machine vision and process control, resulting in a 10.4% CAGR for the industrial segment.

What market share did e-commerce hold in 2025 sales?

E-commerce accounted for 53.9% of 2025 revenue in the Small Form Factor PC market.

How does the market concentration look among leading vendors?

The combined share of the top five players sits near 40%, indicating moderate fragmentation according to Mordor Intelligence.

Page last updated on: