Long-Acting PEG-rhG-CSF Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

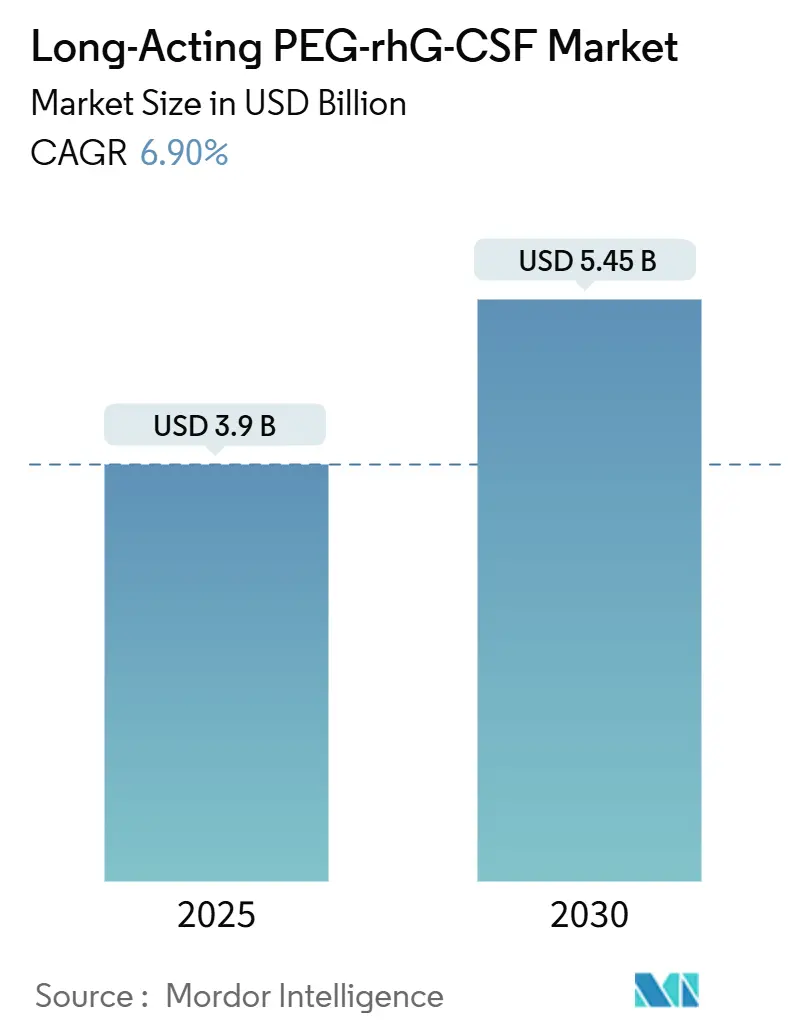

| Market Size (2025) | USD 3.9 Billion |

| Market Size (2030) | USD 5.45 Billion |

| Growth Rate (2025 - 2030) | 6.90% CAGR |

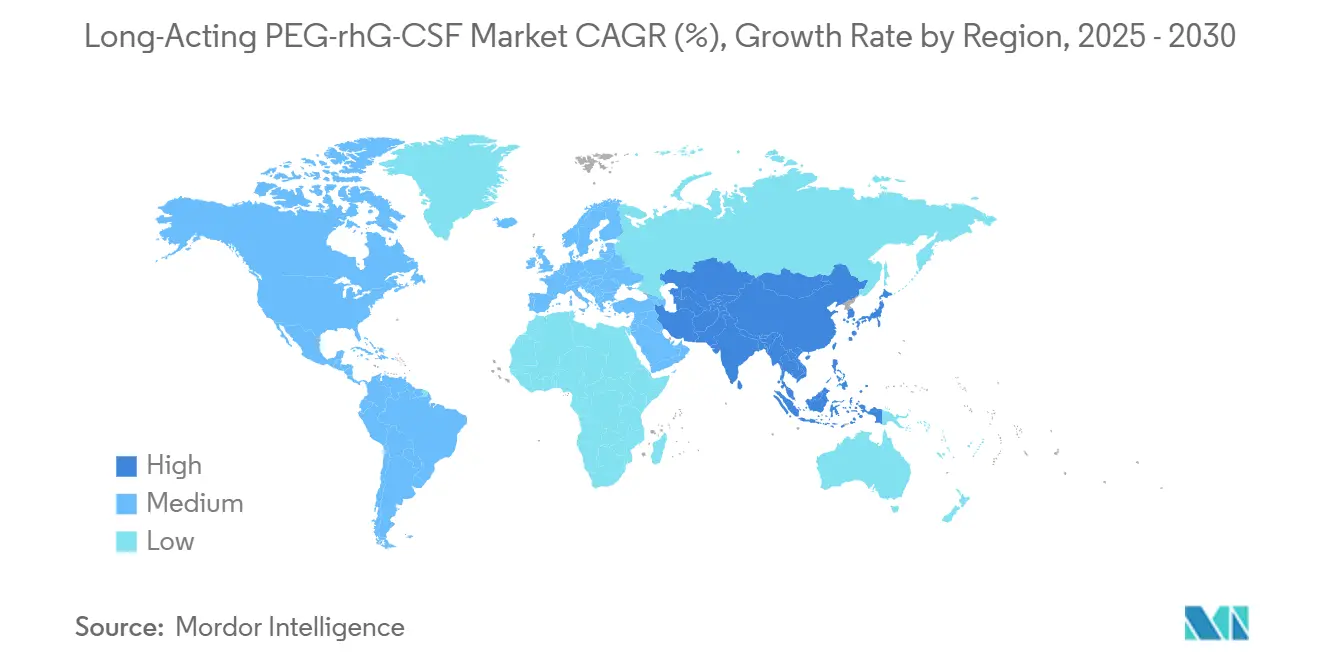

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

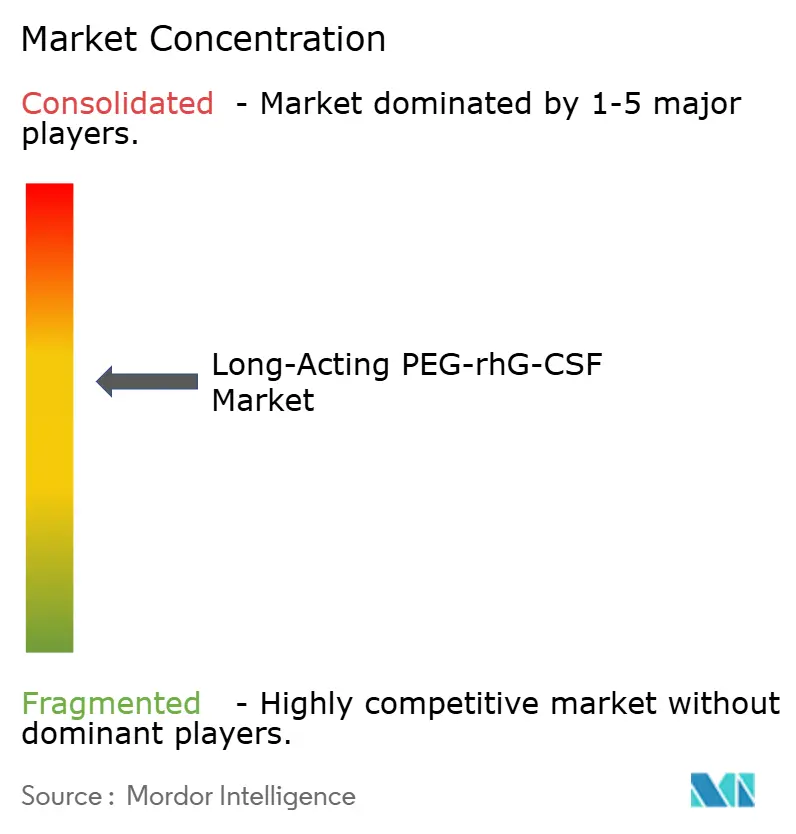

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Long-Acting PEG-rhG-CSF Market Analysis by Mordor Intelligence

The Long-Acting PEG-rhG-CSF Market size is estimated at USD 3.9 billion in 2025, and is expected to reach USD 5.45 billion by 2030, at a CAGR of 6.90% during the forecast period (2025-2030).

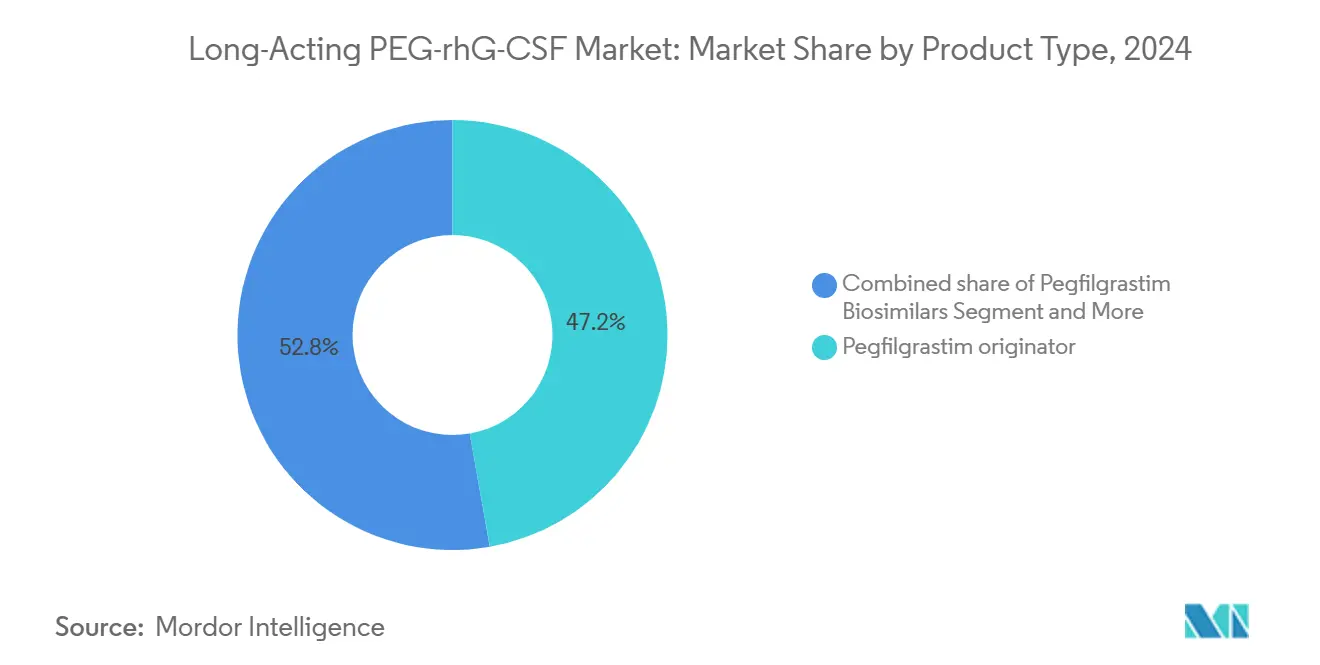

Demand is pivoting toward device-enabled adherence, accelerated biosimilar launches, and reimbursement reforms that favor lower net prices. Pegfilgrastim originator brands held 47.23% market share in 2024, yet their lead is narrowing as interchangeable biosimilars grow 11.15% yearly and disrupt rebate-protected formularies. Prefilled syringes still accounted for 62.17% of delivery-format revenue, but on-body injectors are expanding at 14.55% CAGR because ambulatory oncology models reduce clinic visits and shift prophylaxis to patient homes. Chemotherapy-induced neutropenia drove 77.83% of doses in 2024, while acute radiation syndrome uses, underpinned by federal stockpiling, are rising at 11.23% CAGR and creating a countercyclical revenue stream. North America captured 43.11% of 2024 sales but Asia-Pacific is the fastest-growing region at 12.34% CAGR as China and Japan streamline biosimilar approvals.

Key Report Takeaways

- By product type, pegfilgrastim originators led with a 47.23% long-acting PEG-rhG-CSF market share in 2024; biosimilars are projected to rise at an 11.15% CAGR through 2030.

- By delivery format, prefilled syringes controlled 62.17% of 2024 revenue, whereas on-body injectors are advancing at a 14.55% CAGR to 2030.

- By indication, chemotherapy-induced neutropenia accounted for 77.83% of the long-acting PEG-rhG-CSF market size in 2024, and acute radiation syndrome is expanding at an 11.23% CAGR.

- By distribution channel, Hospital Pharmacies accounted for 54.2% of the long-acting PEG-rhG-CSF market size in 2024, and online pharmacy is expanding at an 15.34% CAGR.

- By geography, North America commanded 43.11% revenue share in 2024, while Asia-Pacific holds the fastest CAGR at 12.34%.

Global Long-Acting PEG-rhG-CSF Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Oncology Pipeline Intensification & Dose-Dense Chemotherapy Protocols | +1.2% | Global, highest in North America and Western Europe | Medium term (2-4 years) |

| Guideline-Mandated Primary FN Prophylaxis ≥20% Risk | +1.5% | Global, led by North America and EU | Short term (≤2 years) |

| Rapid Biosimilar Penetration Lowering ASP and Expanding Access | +1.8% | Europe and Asia-Pacific core, rising in North America | Medium term (2-4 years) |

| Shift to Ambulatory / Home-Based Cancer Care Models | +0.9% | North America and Western Europe | Long term (≥4 years) |

| Device-Enabled Adherence (On-Body Injectors, Autoinjectors) | +1.1% | North America and EU | Medium term (2-4 years) |

| Emerging Same-Day Dosing Evidence Easing Logistics | +0.5% | North America with EU spillover | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Oncology Pipeline Intensification & Dose-Dense Chemotherapy Protocols

Dose-dense regimens such as biweekly AC-T for breast cancer condense treatment intervals, push febrile neutropenia risk beyond 20%, and make single-dose pegfilgrastim essential for primary prophylaxis[1]Centers for Disease Control and Prevention. "Treating Radiation Exposure with Neupogen®." National Center for Environmental Health. January 31, 2025.. FDA cleared 17 new cytotoxic combinations in 2024 that require myelosuppression management, expanding the addressable patient pool for the long-acting PEG-rhG-CSF market. China’s regulator approved 46 novel oncology drugs in the same year, half of which are biologics that will need supportive-care G-CSF, intensifying Asia-Pacific demand. Single-dose prophylaxis cuts clinic visits by 80% versus daily filgrastim and aligns with hospital cost-containment goals. Adherence improves further when on-body injectors automate 24-hour dosing, an advantage in ambulatory settings where patients self-manage schedules.

Guideline-Mandated Primary FN Prophylaxis ≥20% Risk

ASCO, NCCN, and EORTC guidelines now treat primary G-CSF prophylaxis as mandatory once febrile neutropenia risk tops 20%, embedding pegfilgrastim into electronic order sets and limiting prescriber discretion. Medicare Part D reimburses biosimilars at 85% of originator ASP, encouraging payers to adopt lower-cost options and widening patient access. Europe mirrors this stance through national oncology protocols, while India’s National Cancer Grid issued parallel guidance in 2024 even though supply gaps persist outside tier-1 cities. The elderly gain particular benefit after AGIHO extended prophylaxis recommendations in 2024, enlarging the treated population by 30% in aging economies. Concentrated manufacturing, however, means hurricanes or other disruptions can tighten supply and prompt rapid biosimilar substitution.

Rapid Biosimilar Penetration Lowering ASP and Expanding Access

PEG-rhG-CSF prices fell 5%–68% across 20 high-income nations once patents expired and biosimilars entered, narrowing the historic premium over daily filgrastim. WHO’s 2023 Essential Medicines List endorsement underscored the single-dose convenience for low-resource settings, and Europe’s reference-pricing rules force automatic substitution, so biosimilars already hold 35% regional volume. In the United States, rebate contracts still shelter originators, delaying parity by a year or more, yet the Inflation Reduction Act excludes biosimilars from Medicare negotiation, leaving ample price headroom to erode incumbent share after 2026.

Shift to Ambulatory / Home-Based Cancer Care Models

A majority of chemotherapy treatments now occur in outpatient or home environments, making a once-per-cycle dose more practical than 7–10 daily injections. Udenyca Onbody lets patients leave the clinic the same day, then auto-injects 27 hours later, reducing follow-up visits and saving USD 800 per cycle in total costs. Telehealth supports virtual neutrophil monitoring, while home phlebotomy services feed results to oncologists, trimming in-person appointments by 40%. Safety education must improve because splenic rupture, though rare, requires immediate response. Reimbursement misalignment remains a barrier because Medicare’s chemotherapy bundle often omits home-infusion add-ons, disincentivizing providers from shifting volumes outside the clinic.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rebate Walls Sustaining Originator Payer Preference | -0.8% | North America, moderate in EU | Medium term (2-4 years) |

| PEG-Specific Immunogenicity & Splenic-Rupture Safety Concerns | -0.6% | Global, heightened in North America and EU | Short term (≤2 years) |

| IRA / Tender Price Compression Eroding Margins | -0.5% | North America, Europe, Asia-Pacific | Long term (≥4 years) |

| Renal PEG Accumulation Debate in Long-Term Survivors | -0.3% | Global, evidence focus in North America and EU | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rebate Walls Sustaining Originator Payer Preference

Neulasta remains the preferred brand in 60% of U.S. commercial plans because Amgen rebates 40%–50% of list price to pharmacy benefit managers, delaying biosimilar substitution by up to 18 months after approval. The IRA spares biosimilars from Medicare negotiation, so originators lose a pricing shield once exclusivity ends, but commercial markets stay rebate-driven. Coherus counters with outcome-based contracts that refund payers if hospitalization targets are missed, a tactic that won three new regional formularies in 2024. Europe’s reference-pricing laws and automatic substitution policies leave little room for rebate strategies, hence biosimilars there already exceed one-third of volume.

PEG-Specific Immunogenicity & Splenic-Rupture Safety Concerns

Up to 72% of healthy individuals carry anti-PEG antibodies, which can trigger hypersensitivity and cut pegfilgrastim exposure by 41% in positive patients. COVID-19 vaccination raises antibody titers further, prompting FDA to update boxed warnings in 2024 and mandate clearer counseling on splenic rupture signs. No commercial assay yet screens patients systematically, so oncologists discover risk only after reactions occur. Animal data hint at renal PEG accumulation, but human evidence is limited to isolated glomerulonephritis cases, fueling long-term safety debate.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Biosimilars Erode Originator Dominance

Pegfilgrastim biosimilars are scaling at 11.15% CAGR from 2025-2030, outpacing the overall long-acting PEG-rhG-CSF market. The long-acting PEG-rhG-CSF market size for biosimilars is projected to cross USD 3 billion by 2030 as interchangeability designations dismantle rebate defenses [3]FDA/CDER. "LABEL." Revised April 2025. Originators retained a 47.23% share in 2024 but could slide to 35% by 2030 once Medicare negotiation exemptions for biosimilars widen the price gap.

Lipegfilgrastim remains a niche at 8% share, hindered by limited approvals, while eflapegrastim is gaining traction in ambulatory networks that value same-day dosing simplicity. Coherus’s USD 135 million sale of Udenyca to Intas unlocked emerging-market distribution synergies, indicating strategic portfolio realignment among mid-tier players. European uptake is brisk; EMA’s CHMP issued a positive opinion for Dyrupeg in January 2025, pushing the approved biosimilar count to 10 and intensifying price competition.

By Delivery Format: On-Body Injectors Disrupt Prefilled Syringe Hegemony

Prefilled syringes still led revenue in 2024, yet on-body injectors posted the fastest 14.55% CAGR thanks to their ability to automate timing and cut clinic traffic. In the United States, on-body devices captured 12% of volume within six months of launch despite higher unit costs, proving the value proposition resonates where ambulatory care is dominant.

Device innovation tackles cold-chain fragility, keeping drug stable for eight days at room temperature versus four for syringes, reducing wastage in home-infusion networks. Autoinjectors cater to patients with dexterity challenges but lack timing automation, so their growth trails at 7% CAGR. Payers are slowly aligning reimbursement; once parity improves, injector adoption is likely to accelerate further, especially as real-world data show 30% fewer febrile neutropenia admissions relative to syringes.

By Indication: ARS Emerges as Fastest-Growing Niche

Chemotherapy-induced neutropenia dominated 77.83% of 2024 doses, grounded in standard-of-care prophylaxis protocols. Acute radiation syndrome, though small, delivers an 11.23% CAGR as BARDA and other agencies stockpile countermeasures, thereby smoothing revenue across oncology cycles. The long-acting PEG-rhG-CSF market share linked to ARS applications could reach 5% by 2030, reflecting broader federal preparedness budgets.

Stem-cell mobilization is another bright spot, bolstered by Kyowa Kirin’s expanded Japanese approval in 2024 and rising autologous transplant volumes in multiple myeloma. Combined regimens pairing pegfilgrastim with plerixafor cut mobilization failure rates to 5%, enhancing the clinical case for G-CSF use in this segment.

By Distribution Channel: Online Pharmacies Surge Amid Ambulatory Shift

Hospital pharmacies dispensed 54.2% of 2024 volume but are ceding share as care moves outpatient. Online specialty platforms integrating telehealth and cold-chain logistics are growing at 15.34% CAGR, helping rural patients avoid long travel and improving adherence. Specialty oncology clinics grow close behind at 10% as on-body injectors permit same-day discharge.

Retail pharmacists participate cautiously because of cold-chain liability, yet interchangeability rules enable automatic substitution and could lift share once robust temperature-control packaging scales. FDA REMS requirements mandate pharmacist counseling, adding complexity but also building confidence among patients using direct-to-home channels.

Geography Analysis

North America generated 43.11% of 2024 revenue, anchored by strict guideline compliance and Medicare Part D reforms that reimburse biosimilars favorably. The United States alone holds 85% of regional sales and saw Coherus reach 28% share within its first year of injector commercialization, illustrating the disruptive power of device convenience. Canada and Mexico fill the balance, each expanding prophylaxis access through national formularies that now list at least one biosimilar pegfilgrastim at discounted prices. Federal preparedness programs also drive sales; BARDA budgeted USD 290 million for radiation countermeasures in 2025, sustaining demand even when oncology cycles.

Europe captured 32% of global revenue and exhibits the most advanced biosimilar penetration at 35% volume share, a feat propelled by reference-pricing mandates and substitution laws. The “EU-5” nations represent 70% of continental spending, powered by centralized health systems that prioritize cost-effectiveness. EMA’s expanding approval roster keeps competitive pressure high; Dyrupeg’s impending launch takes the biosimilar count to double digits, ensuring continued price erosion. Eastern Europe is emerging, with Poland and Romania opening 12 new cancer centers in 2024, setting the stage for a 9% CAGR through 2030.

Asia-Pacific is the fastest riser at 12.34% CAGR and already contributes one-quarter of worldwide volume. China leads, where CSPC and Qilu each secure over significant domestic share by pricing below Neulasta while enjoying national reimbursement. Japan extended G-Lasta’s label to stem-cell mobilization, capturing transplant-related growth, whereas India, Australia, and South Korea benefit from new prophylaxis guidelines and local biosimilar manufacturing. WHO’s essential-medicine endorsement hastens Southeast Asian adoption as donor programs fund procurement, lifting patient access. The Middle East and Africa remain small at 6% share but GCC oncology investments and South African private-sector pilots point to steady progression.

Competitive Landscape

Market concentration is moderately consolidated: the top five manufacturers, Amgen Inc., Coherus Oncology, Inc, Sandoz AG, Fresenius Kabi AG, and Pfizer Inc. held the majority of 2024 revenue, while the remaining supply fractured among a dozen regional biosimilar firms. Sandoz leverages FDA interchangeable status for Ziextenzo to accelerate pharmacy substitution, whereas Coherus created differentiation with injector convenience and outcome-based rebate models that resonate with cost-conscious payers.

Strategic M&A is reshaping the field. Coherus’s USD 558.4 million divestiture of Udenyca to Intas strengthens the latter’s emerging-market footprint and illustrates consolidation among mid-tier players seeking scale. Biocon’s 2023 acquisition of Viatris’s biosimilars arm and Fresenius Kabi’s partnerships with contract manufacturers enlarge low-cost capacity to serve Asia-Pacific growth.

Innovation focus has shifted from molecule to device. Firms that marry on-body delivery with same-day pharmacokinetics could leapfrog the 24-hour barrier still embedded in many reimbursement rules. Patent cliffs loom: Neulasta’s core patents expired in 2024 and injector patents fall in 2027, inviting aggressive follower launches. Competitive intensity is poised to rise as Chinese entrants seek FDA and EMA nods; their cost advantage could further squeeze margins but also democratize access in low-income regions.

Long-Acting PEG-rhG-CSF Industry Leaders

-

Amgen Inc.

-

Coherus Oncology, Inc

-

Sandoz AG

-

Fresenius Kabi AG

-

Pfizer Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: The EMA’s CHMP issued a positive opinion for Dyrupeg, CuraTeQ’s pegfilgrastim biosimilar, expanding Europe’s approved pool to 10 products

- December 2024: Coherus completed the USD 558.4 million sale of Udenyca to Intas Pharmaceuticals to sharpen strategic focus and unlock emerging-market reach.

- May 2024: Japan authorized Kyowa Kirin's G-Lasta for stem-cell mobilization, broadening its use beyond chemotherapy prophylaxis.

- February 2024: Coherus launched Udenyca Onbody in the United States after FDA clearance, automating 27-hour post-chemotherapy dosing.

Global Long-Acting PEG-rhG-CSF Market Report Scope

As per the scope of the report, Long-Acting PEG-rhG-CSF refers to the pegylated recombinant human granulocyte colony stimulating factor, a modified form of G-CSF designed to stimulate neutrophil production with prolonged duration, allowing once per cycle dosing in chemotherapy induced neutropenia.

The long-acting PEG-rhG-CSF market is segmented by product type, delivery format, indication, distribution channel, and geography. By product type, the market is categorized into pegfilgrastim (originator), pegfilgrastim biosimilars, lipegfilgrastim, and eflapegrastim. By delivery format, it is segmented into prefilled syringe, on-body injector, and autoinjector. By indication, the market is divided into chemotherapy-induced neutropenia, stem-cell mobilisation, and acute radiation syndrome. By distribution channel, the segmentation includes hospital pharmacies, specialty / oncology clinics, online pharmacies, and retail pharmacies. Geographically, the market is segmented across North America, Europe, the Asia-Pacific region, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Pegfilgrastim (originator) |

| Pegfilgrastim Biosimilars |

| Lipegfilgrastim |

| Eflapegrastim |

| Prefilled Syringe |

| On-body Injector |

| Autoinjector |

| Chemotherapy-induced Neutropenia |

| Stem-cell Mobilisation |

| Acute Radiation Syndrome |

| Hospital Pharmacies |

| Specialty / Oncology Clinics |

| Online Pharmacies |

| Retail Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Pegfilgrastim (originator) | |

| Pegfilgrastim Biosimilars | ||

| Lipegfilgrastim | ||

| Eflapegrastim | ||

| By Delivery Format | Prefilled Syringe | |

| On-body Injector | ||

| Autoinjector | ||

| By Indication | Chemotherapy-induced Neutropenia | |

| Stem-cell Mobilisation | ||

| Acute Radiation Syndrome | ||

| By Distribution Channel | Hospital Pharmacies | |

| Specialty / Oncology Clinics | ||

| Online Pharmacies | ||

| Retail Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the long-acting PEG-rhG-CSF market?

The market reached USD 3.9 billion in 2025 and is forecast to grow to USD 5.45 billion by 2030.

Which region is expanding fastest for long-acting PEG-rhG-CSF?

Asia-Pacific is advancing at a 12.34% CAGR thanks to regulatory harmonization in China and Japan.

How quickly are biosimilars gaining share in long-acting PEG-rhG-CSF?

Biosimilars are growing at 11.15% CAGR and are projected to hold 65% of global volume by 2030.

Why are on-body injectors important for long-acting PEG-rhG-CSF delivery?

They automate 27-hour dosing, reduce clinic visits by eliminating next-day returns, and improve adherence, leading to 30% fewer febrile neutropenia admissions.

Page last updated on: