PC Game Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

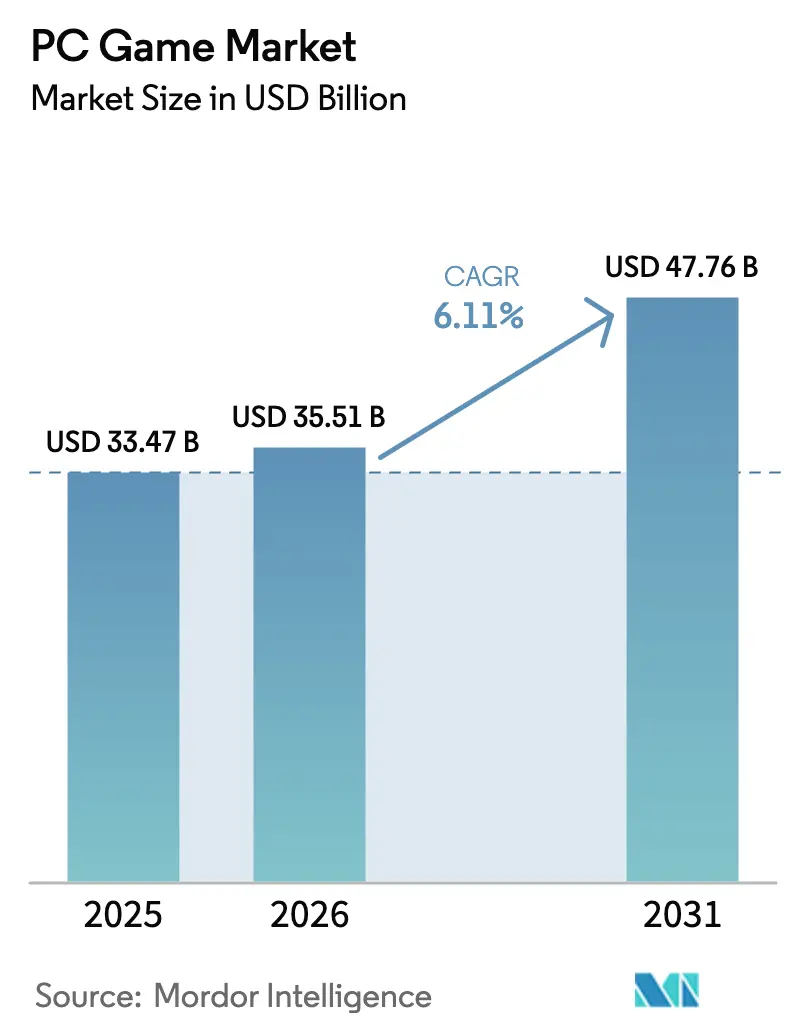

| Market Size (2026) | USD 35.51 Billion |

| Market Size (2031) | USD 47.76 Billion |

| Growth Rate (2026 - 2031) | 6.11% CAGR |

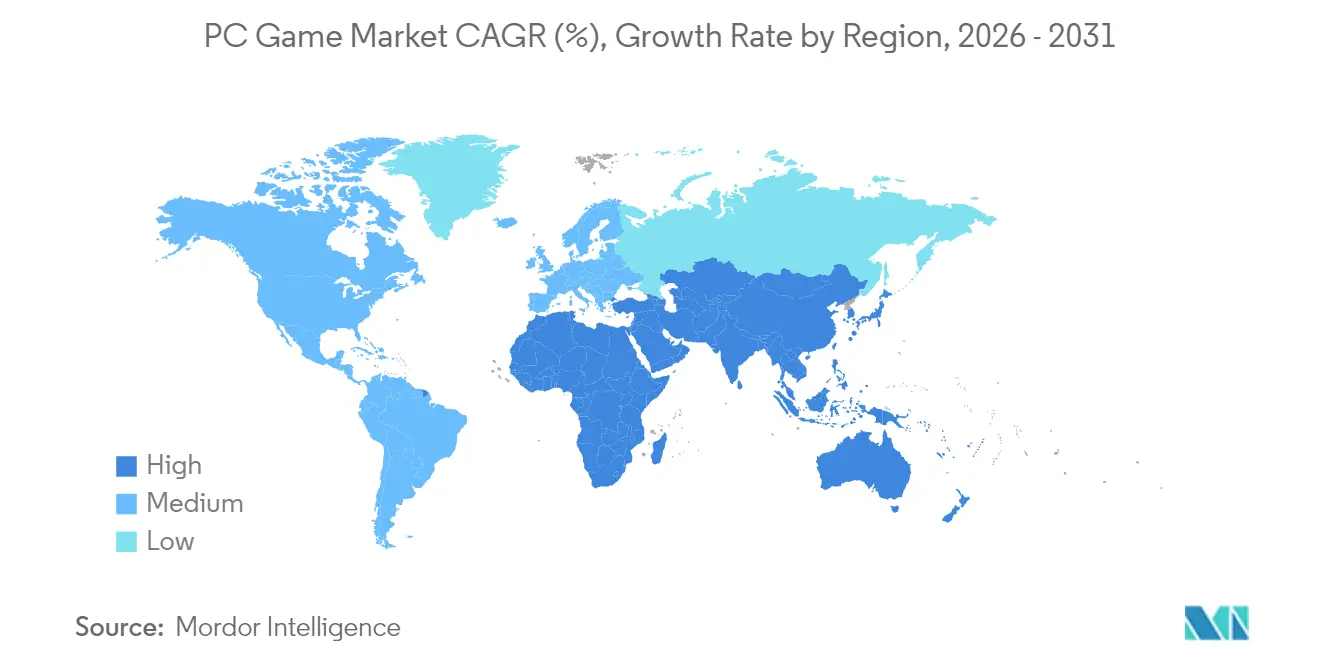

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

PC Game Market Analysis by Mordor Intelligence

The PC Game market size is expected to grow from USD 33.47 billion in 2025 to USD 35.51 billion in 2026 and is forecast to reach USD 47.76 billion by 2031 at 6.11% CAGR over 2026-2031. Success continues to stem from the platform’s open architecture, which absorbs new technologies such as hardware-accelerated ray tracing and machine-learning asset pipelines while keeping development overheads predictable. Publishers now treat the PC as a low-risk incubator that lets mechanics mature on desktop before migrating elsewhere, shortening iteration loops and preserving capital. Revenue diversification is deepening: subscriptions, recurring season passes, and creator-run marketplaces already generate an expanding share of receipts, allowing studios to decouple topline growth from unit shipments. Middleware providers have aligned with this shift by bundling lifetime-value analytics that help teams refine engagement loops without raising user-acquisition budgets, underscoring how data fluency has become a competitive necessity across the PC game market.

Key Report Takeaways

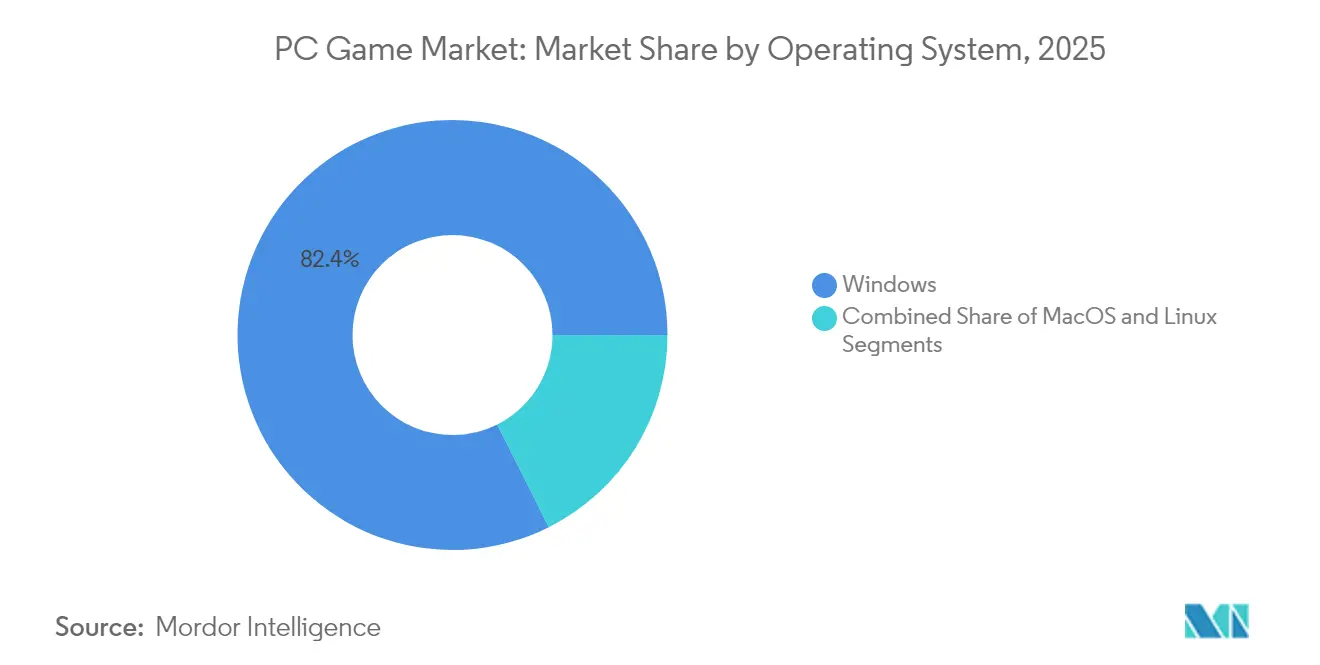

- By operating system, Windows held 82.40% of the PC game market share in 2025, while macOS is forecast to log the fastest CAGR through 2031.

- By revenue model, free-to-play commanded the largest portion of the PC game market size in 2025; subscription services are projected to post the highest CAGR through 2031.

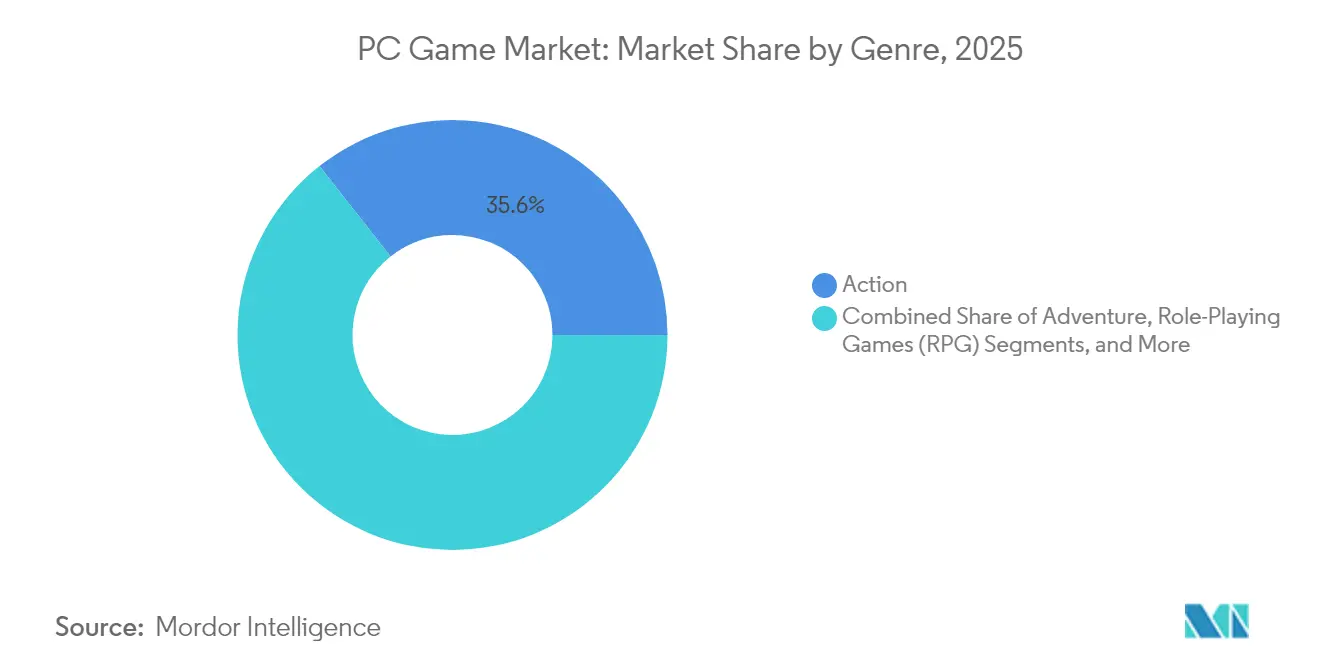

- By genre, role-playing titles outperformed other categories with growth that exceeds the aggregate 6.11% benchmark of the PC game market.

- By geography, Asia-Pacific accounted for nearly 49.95% of the PC game market share in 2025, whereas Europe is on course for the quickest CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of PC Game Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Esports Prize Pools and Sponsorship Deals | +1.2% | Asia-Pacific, with spillover to North America | Medium term (3-4 yrs) |

| Proliferation of High-Refresh-Rate Monitors and GPUs | +0.8% | North America, Europe | Short term (≤2 yrs) |

| Cloud-Gaming Integration with Steam and Epic Stores | +1% | Europe, with global expansion potential | Medium term (3-4 yrs) |

| Cross-Platform Play Incentives | +1.3% | Global | Medium term (3-4 yrs) |

| Monetization of Modding Communities | +0.6% | North America, Europe | Long term (≥5 yrs) |

| Government Subsidies for Game Development Studios | +0.3% | South Korea, China | Medium term (3-4 yrs) |

| Source: Mordor Intelligence | |||

Rising Esports Prize Pools Accelerate Monetization

Prize purses for flagship PC tournaments expanded sharply in 2024-2025, lifting the visibility of competitive titles and driving new downloads. Ubisoft’s Six Invitational allocated USD 3 million and attracted record spectatorship that dwarfed prior seasons [1]Ubisoft Communications, “Six Invitational 2025 Factsheet,” ubisoft.com. Riot Games maintained seven-figure rewards for the League of Legends World Championship, coupling the event with regional fan festivals that converted viewers into first-time players. Local governments in South Korea and mainland China have begun subsidizing arena construction and athlete development, positioning esports as an exportable service industry. These policies enlarge the PC game market by easing venue costs and channelling new sponsorship flows into publisher ecosystems. As prize pools expand, teams invest in dedicated performance analytics that raise competitive standards and showcase the hardware ceiling possible on high-end rigs, encouraging enthusiasts to upgrade components sooner.

High-Refresh-Rate Monitors Fuel AAA Adoption

Late-2024 releases shipped with performance modes tuned for 144 Hz and above, prompting retailers to report sell-through that outpaced earlier forecasts. Influencer streams displaying fluid gameplay at 240 Hz created a perception gap between premium desktops and 60 Hz televisions, reinforcing the PC as the aspirational reference point in the broader gaming landscape. Component vendors staged coordinated launches of GPUs, display cables, and calibration software, lowering integration friction for end users. Studios used telemetry to confirm that players owning high-refresh hardware log longer average sessions, which in turn supports live-service revenue cadence. The combined effect strengthens the PC game market by widening attach rates for monitors and GPUs, ensuring that even mid-tier consumers feel pressure to participate in an upgrade cycle that boosts overall market velocity.

Cloud Gaming Integration Expands European Reach

In 2024, Xsolla introduced an Instant Cloud Gaming sleeve that lets developers ship a streaming build alongside a local installer. [2]Xsolla Press Office, “Instant Cloud Gaming Launch Release,” xsolla.comBy early 2025, European laptop owners without discrete GPUs could access 60-fps sessions during peak hours, minimizing barrier-to-entry concerns. Cloud demos shorten the evaluation phase by replacing static trailers with interactive trials delivered inside storefronts, which lifts conversion rates among undecided shoppers. Publishers also benefit from lower distribution overheads and granular data on user-device performance, informing porting decisions for emerging markets. As broadband coverage improves, cloud hooks will bring incremental audiences into the PC game market without cannibalizing high-spec demand, instead acting as an on-ramp that encourages eventual hardware purchases.

Cross-Platform Play Boosts Free-to-Play Conversion

Seamless progression across desktop, handheld, and mobile extended session durations in 2024-2025, materially improving retention for free players. When cosmetic assets persist across operating systems, perceived long-term value rises, and users display higher willingness to spend. Marketing teams now emphasise account-level loyalty programmes that accumulate rewards irrespective of device, thereby reallocating spend away from platform-specific bundles. The approach elevates the PC game market by positioning desktop as the ecosystem hub—where content updates arrive first and controls remain uncompromised—while still respecting player freedom to shift devices during commutes or travel.

Restraints Impact Analysis of PC Game Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Loot-Box and Micro-transaction Regulations | -0.9% | EU Member States | Short term (≤2 yrs) |

| GPU Supply Constraints and Price Inflation | -0.7% | Global, most severe in North America | Short term (≤2 yrs) |

| Cyber-Fraud and Account Takeovers | -0.3% | Global | Medium term (3-4 yrs) |

| Skilled-Talent Shortage | -0.5% | North America | Long term (≥5 yrs) |

| Source: Mordor Intelligence | |||

Loot Box Regulations Reshape Monetization

Belgium’s outright prohibition on paid loot boxes set a regulatory tone later mirrored in draft policies from other EU members. Publishers responded by rolling out battle passes, event shops, and transparent drop-rate disclosures that soften legislative scrutiny while preserving monetization depth. Clear upfront pricing sustains consumer trust, lowering refund requests and dampening negative social sentiment. Operationally, studios must overhaul back-end tracking to ensure compliance, diverting resources from experimental content. Over the next two years, the need to harmonize strategy across variable national rules will exert downward pressure on the PC game market by delaying feature roll-outs and increasing compliance costs.

GPU Supply Constraints Limit High-End Expansion

Nvidia told investors in November 2024 that reallocating fabrication capacity to its next-generation architecture would tighten 40-series supply through early 2025. Spot shortages prompted some enthusiasts to postpone full-system builds, nudging developers to implement more aggressive dynamic-resolution tools that maintain frame rates on older silicon. Retailers countered inventory gaps with bundled promotions pairing CPUs and memory to spur partial upgrades, but top-tier GPU scarcity still removed high-margin purchases from the channel mix. Although Nvidia later noted that initial shipments “exceeded internal forecasts” in March 2025, lingering availability imbalances continue to restrain the premium slice of the PC game market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

PC Game Market Segment Analysis

By Genre:

Role-Playing Leadership and Experimental HybridsRole-playing games (RPGs) outpaced the overall 6.11% growth of the PC game market, benefiting from blockbuster narrative releases that demonstrated premium pricing viability. Titles shipped with long-form episodic arcs that sustain engagement beyond launch month, smoothing revenue curves for publishers. Advanced dialogue systems and branching questlines showcase how desktop hardware supports real-time decision tracking without compromising performance. Indie studios exploit the genre’s flexible tooling by releasing early-access builds that absorb player feedback, leading to more refined mechanics at official launch. Adventure and simulation genres posted steady gains by lowering skill barriers, attracting older newcomers seeking accessible interfaces. Strategy titles preserved a loyal base thanks to keyboard-mouse precision rarely achievable on console, reinforcing the PC game market as the strategic game stronghold. Hybrid formats such as auto-battlers served as live testbeds for mechanics later transplanted into mainstream franchises, underlining the PC’s role as an experimental crucible. Studios report that cross-genre crossovers raise replayability metrics, supporting battle-pass revenue when content pipelines remain active. Over the forecast, RPG dominance is expected to hold as high-fidelity storytelling remains a unique desktop selling point.

Second-order effects ripple through middleware demand, with dialogue-tree plug-ins and cinematic lighting suites seeing higher attach rates. Asset libraries tuned for fantasy settings command premium prices, giving external artists a route into publisher work-for-hire rosters. Community-led modding further amplifies reach: robust toolkits allow hobbyists to add quests, driving incremental sales years after release. Publishers thus embed creator-friendly frameworks at launch, securing a longer tail for each SKU. Growing integration between tabletop IP and digital campaigns also feeds the PC gaming market by cross-pollinating fan bases and broadening licensing opportunities.

By Revenue Model:

Subscription Momentum and F2P DominanceFree-to-play (F2P) maintained the largest share of the PC game market size in 2025, capitalizing on zero-cost entry and global reach. Cosmetic microtransactions, season passes, and limited-time event shops anchor monetization, while transparent drop rates help navigate EU regulatory scrutiny. Subscription services, however, delivered the highest CAGR during 2025-2026. Platforms that bundle day-one releases with classic back catalogues entice value-oriented players and mitigate piracy. Microsoft highlighted an 8% uplift in content and services and credited PC Game Pass for a record quarter. Publishers maintain shorter content cadences, ensuring new quests or maps land within the monthly billing cycle, which reduces churn. Premium single-purchase titles still confer prestige; award recognitions translate into merchandise sales, book adaptations, and film options. Bundled discovery feeds inside subscription hubs also raise visibility for time-limited paid expansions in F2P worlds, supporting cross-model monetization.

On the cost side, subscriptions require robust cloud infrastructure and predictive analytics that optimize download pre-fetching to avoid bandwidth congestion. Studios allocate budget toward live-ops teams that continuously monitor player sentiment, a capability that smaller indies often outsource, further stratifying the PC game market. Economies of scale help larger platforms negotiate network peering agreements, trimming delivery expenses. Over time, expect consolidation around a handful of subscription brands that double as social hubs connecting communities across multiple franchises.

By Operating System:

Windows Dominance with Niche GrowthWindows retained more than four-fifths of the PC game market share in 2025, supported by deep backward compatibility and frequent driver updates. DirectX 12 Ultimate remains the industry default for advanced features, accelerating the adoption of ray-traced lighting and variable rate shading. Microsoft’s same-day releases on PC strengthen the OS moat because cross-progression with console titles simplifies friend-list migration. Apple’s silicon revisions improved integrated-GPU output and reduced power draw, pushing several publishers to approve simultaneous macOS ports for 2025. The move expands paying audiences without requiring exhaustive optimization cycles. Linux crept upward on Proton compatibility and the Steam Deck’s handheld popularity, encouraging indie teams to include Linux builds at early access. The dispersion underscores how broader OS inclusivity enlarges the PC game market by tapping previously untapped demographics. Engine makers now prioritize Vulkan and Metal back-ends, spreading rendering workloads across APIs and improving multi-platform efficiency.

Security remains a differentiator. Elevated ransomware incidents on Windows prompt some enterprises to subsidize Mac hardware for employee recreation, an indirect boost to macOS installs. In contrast, Linux communities leverage open-source anti-cheat frameworks that attract competitive titles seeking low latency. Over the forecast period, Windows will likely sustain numerical dominance, but incremental growth from macOS and Linux should widen the total addressable base and encourage middleware providers to maintain parity across engines.

By Age Group:

Youth Onboarding and Adult Purchasing PowerUnder-18 users recorded the fastest usage growth between 2024-2025 after schools embedded esports clubs and coding electives that normalize early digital play. Publishers targeting this group introduced parental dashboards with spending thresholds, building brand goodwill that carries into adulthood subscriptions. The 18-35 cohort dominates discretionary spending, gravitating toward premium peripherals and collector editions that signal status on social feeds. Marketing campaigns leverage influencer affiliations aligned with lifestyle brands, reinforcing purchase intent beyond game software itself. Gamers aged 36-50 form a smaller but lucrative niche, favoring strategy titles with short daily loops compatible with work-life balance. Publishers optimize user-interface readability and autosave functions to accommodate intermittent play sessions. The over-50 demographic continues to expand slowly, aided by nostalgia remasters that simplify controls without diluting depth, thereby extending the PC game market among lapsed players. Hardware vendors respond with ergonomic peripherals that reduce strain during lengthy sessions, appealing to older users. Age-specific analytics inform content filters, ensuring chat moderation settings default to conservative for minors, aligning with regulatory requirements.

A broader implication is that generational overlap inside live-service universes demands multichannel communication strategies: younger players prefer short-form video tutorials, while older cohorts favor text-based wikis. Studios that provide both formats see higher engagement across age bands, smoothing monetization curves and diversifying revenue streams.

Geography Analysis

APAC PC Game Market

Asia-Pacific claimed nearly one-half of the PC game market size in 2025, propelled by dense urban broadband and official recognition of esports as a growth lever. China’s streamlined content-approval pipeline in 2025 encouraged domestic giants to invest in AAA PC titles infused with local cultural narratives, balancing export ambitions with home-market resonance. South Korea’s PC-bang operators introduced hourly packages bundled with cloud-streamed game libraries, reducing capital expenditure on constant hardware refresh. Cross-border codevelopment is thriving: Japanese narrative designers pair with Korean real-time-service specialists to craft features that scale across the region’s heterogeneous tastes. Government grants directed toward high-refresh monitor manufacturers lower equipment costs, indirectly expanding the PC game market by making aspirational hardware accessible to mid-income consumers.

North America PC Game Market

North America held the second-largest slice, underwritten by high disposable income and an established enthusiast component scene. Studios headquartered in the region refine live-service blueprints such as battle passes that later inform global best practice. Privacy-centric regulation, particularly concerning minors, forced publishers to redesign data-collection pipelines in 2025, yielding clearer opt-in flows that unexpectedly boosted newsletter subscriptions. Hardware attach rates remain robust: retailers report that bundle promotions featuring GPUs and OLED monitors regularly sell out during major releases. Venture capital interest in middleware targeting analytics and anti-cheat technology signals confidence in the PC game market's sustained relevance.

Europe PC Game Market

Europe’s trajectory accelerated once cloud storefront plug-ins removed the need for high-spec desktops. Laptop owners in France, Spain, and the Nordics streamed 60-fps sessions during prime-time without stutter, demonstrating infrastructure readiness. The Digital Services Act ushered in mandates for real-time toxicity monitoring, prompting studios to adopt AI-driven moderation as a marketing differentiator. Cultural-heritage grants tied to multilingual releases spurred demand for regional indie productions, expanding the PC game market share of story-driven experiences rooted in European folklore. Local hardware assemblers respond by offering certified low-latency routers preconfigured for cloud gaming, fostering an ecosystem that blends hardware and services.

Competitive Landscape

The field is moderately consolidated: a small group of multistudio publishers manages global pipelines while thousands of independents compete for storefront visibility. Microsoft completed its USD 68.7 billion acquisition of Activision Blizzard in 2023 and has since placed same-day PC launches inside its subscription catalogue, compelling rivals to deepen discount windows to maintain competitive parity. The strategy reinforces the brand perception that desktop remains a primary launch platform rather than a secondary port destination. Tencent pursued minority stakes in narrative-driven Western studios during 2024-2025, signaling interest in diversifying away from pure free-to-play expertise. Cloud-platform providers are engineering soft-exclusive deals, financing development in exchange for timed streaming rights that reach lower-spec users, which expands potential audiences while marginally raising fragmentation risk.

Independent studios wield community funding and viral marketing to offset discoverability challenges. A 2025 breakout co-op extraction release recouped its budget within 72 hours after surfacing on a high-profile influencer stream, demonstrating how algorithmic promotion now determines hit velocity. Middleware costs are falling: off-the-shelf back-end services handling matchmaking, storefront integration, and telemetry analytics allow small teams to ship live-service titles once reserved for multinational publishers. However, the deluge of daily releases on major storefronts intensifies the role of recommendation algorithms; platforms that reliably surface high-quality games based on taste wield disproportionate influence over the PC gaming market flow of revenue.

Hardware alliances form a parallel competitive layer. GPU manufacturers provide early silicon samples to studios committing to showcase features such as path tracing, securing day-one driver optimisation and co-marketing budgets. Monitor vendors sponsor esports leagues to promote emerging standards like 540 Hz refresh, tying product launches to competitive milestones. Peripheral companies collaborate with game developers on haptic profiles that reinforce branded ecosystems. These partnerships ensure that technological advancements translate into tangible gameplay improvements, cementing the PC game market’s perception as the bleeding edge of interactive entertainment.

PC Game Industry Leaders

-

Electronic Arts (EA)

-

Ubisoft Entertainment SA

-

Activision Blizzard, Inc.

-

Epic Games, Inc.

-

Square Enix Holdings Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

PC Game Market Companies Covered in this Report

- Electronic Arts Inc.

- Activision Blizzard, Inc.

- Ubisoft Entertainment SA

- Epic Games, Inc.

- Square Enix Holdings Co., Ltd.

- Bandai Namco Entertainment Inc.

- SEGA Corporation

- Valve Corporation

- CD Projekt S.A.

- Tencent Holdings Ltd. (Tencent Games)

- NetEase, Inc. (NetEase Games)

- Paradox Interactive AB

- Remedy Entertainment

- Capcom Co., Ltd.

- Take-Two Interactive Software, Inc.

- Riot Games, Inc.

- Pearl Abyss

- Nexon Co., Ltd.

- Krafton Inc.

- Embracer Group AB

Recent Industry Developments in PC Game Market

- April 2025: Microsoft reported a 5% year-on-year rise in gaming revenue for fiscal Q3, driven by an 8% uplift in content and services, and highlighted PC Game Pass as the principal growth engine.

- March 2025: Nvidia stated that initial shipments of its next-generation GPUs “exceeded internal forecasts,” although retail availability remained tight.

- February 2025: Microsoft disclosed a record quarterly high for subscription revenue, attributing the surge to a 30% jump in PC Game Pass memberships.

- December 2024: Valve confirmed that concurrent Steam users peaked at 39.3 million, the highest figure in the platform’s history.

PC Game Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the global PC game market as every dollar gamers spend on native-PC software, covering full titles, downloadable add-ons, in-game purchases, and catalog subscriptions delivered only to personal computers. According to Mordor Intelligence, revenue that publishers book under console, mobile, browser, or cloud releases is excluded.

Scope exclusion: Spending on gaming rigs, components, peripherals, advertising, esports tickets, and non-PC titles lies outside this assessment.

Segments Covered in This Report

-

By Genre

- Action

- Adventure

- Role-Playing Games (RPG)

- Simulation

- Strategy

- Other Genres

-

By Revenue Model

- Free-to-Play / Freemium

- One-Time Purchase (Premium)

- Subscription-Based

-

By Operating System

- Windows

- MacOS

- Linux

-

By Age Group

- <18 Years

- 18–35 Years

- 36–50 Years

- >50 Years

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

South America

- Brazil

- Argentina

- Rest of South America

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- South Korea

- India

- Rest of Asia-Pacific

-

Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Primary Research

Mordor analysts hold structured discussions with publishers, indie studios, payment processors, esports league managers, and distributors across Asia-Pacific, North America, and Europe. Insights on price drift, new monetization paths, and looming rules let us stress-test desk findings and close gaps.

Desk Research

We begin with national household spend surveys, dashboards from leading digital storefronts, Chinese and US game yearbooks, entertainment-software fact sheets, and UN Comtrade customs flows. Annual reports, earnings call transcripts, and respected media refine numbers, while Dow Jones Factiva and D&B Hoovers supply long-run splits and currency history. The sources named are illustrative; many additional open and paid references guide data capture, cross-checks, and clarification.

Market-Sizing & Forecasting

We rebuild each country's spend with a top-down view of payment settlements and household digital baskets, then split totals by platform share. Targeted bottom-up probes that include publisher roll-ups, sampled price-times-volume checks, and channel sell-through ratios anchor results. Five fingerprints feed a multivariate regression to 2030: active PC players, spend per payer, storefront fee policy, high-refresh GPU uptake, and loot-box rule severity. The base case mirrors interview consensus and updates whenever fresh signals surface.

Data Validation & Update Cycle

Analysts benchmark outputs against historic publisher curves and indicators such as peak concurrent users. Senior reviewers clear anomalies before sign-off; reports refresh annually, and interim tweaks follow material events.

How Mordor Intelligence's PC Game Market Size Compares to Other Published Estimates

Published values often diverge because some groups bundle hardware with software, widen regional baskets, convert at spot rates, or refresh data infrequently. Our disciplined platform-only lens, transparent variables, and yearly cadence keep the baseline tied to spend studios actually record.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 33.47 B | Mordor Intelligence | - |

| USD 39.90 B | Global Consultancy A | Adds browser games and esports receipts, light gray-market adjust |

| USD 86.12 B | Industry Association B | Combines hardware, peripherals, and software |

| USD 68.88 B | Trade Journal C | Follows hardware shipments, omits in-game spend |

These contrasts show that when scope broadens or unit rules shift, totals inflate quickly. By isolating software flows and triangulating them with player counts and supplier disclosures, we deliver a balanced, repeatable baseline buyers can trust.

Key Questions Answered in the Report

What is the current PC game market size?

The PC game market size totaled USD 35.51 billion in 2026 and is set to reach USD 47.76 billion by 2031.

Which revenue model is expanding most rapidly?

Subscription platforms that bundle day-one releases with back catalogues are displaying the fastest CAGR inside the PC gaming market.

Why does Asia-Pacific hold the largest PC game market share?

Dense broadband, government-backed esports programmes, and an entrenched café culture combine to sustain high engagement and spending.

How are European regulations influencing monetization?

Tighter oversight of loot boxes is driving publishers toward transparent mechanics such as battle passes and direct-purchase cosmetic stores.

What hardware trend most influences premium game adoption?

High-refresh-rate monitors are stimulating a rolling upgrade cycle, encouraging GPU and display purchases that support visually ambitious titles.

Will cloud game replace local installations?

Cloud access is broadening reach but functions as a complementary option; local installs remain essential for competitive latency and offline play.

Page last updated on: