Consumer Desktop PC Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 21.11 Billion |

| Market Size (2031) | USD 31.47 Billion |

| Growth Rate (2026 - 2031) | 8.31% CAGR |

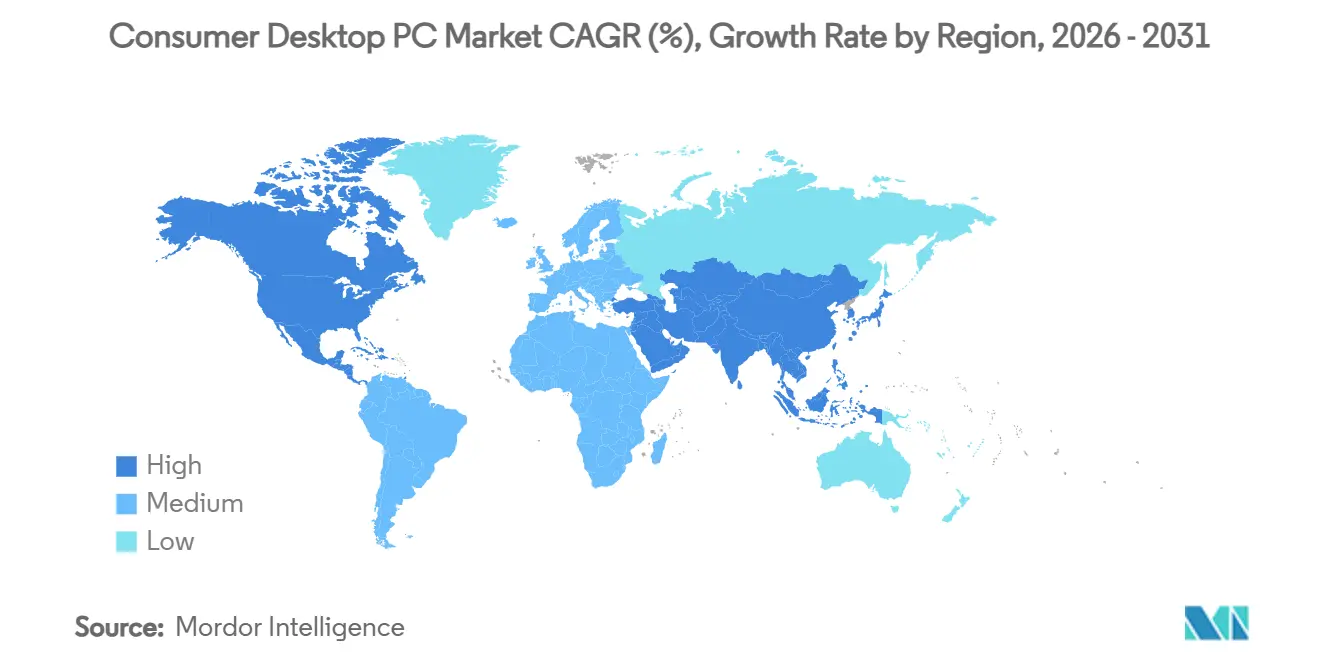

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

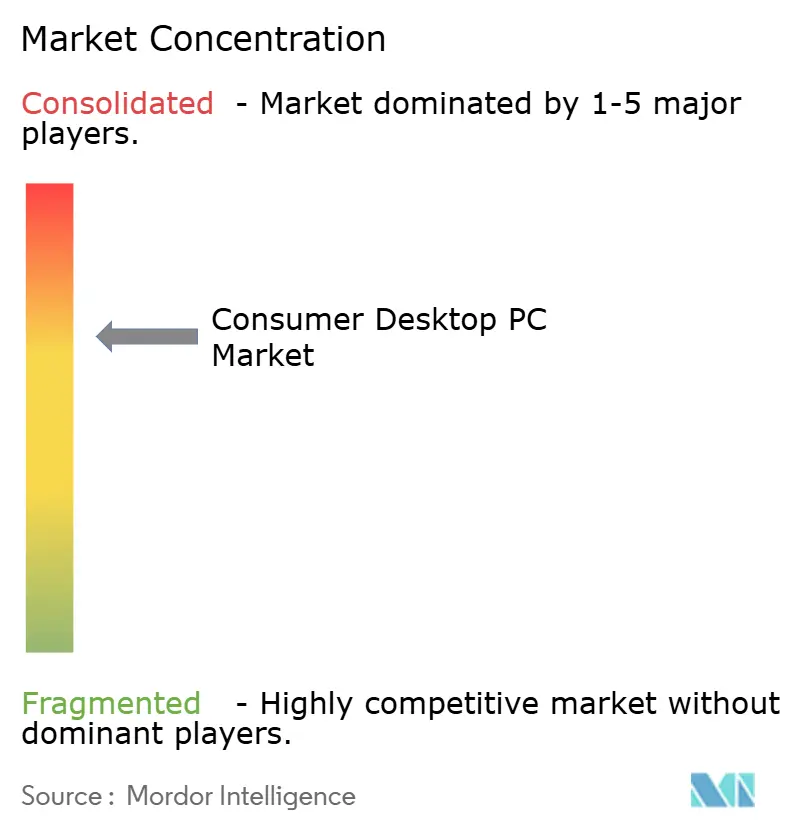

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Consumer Desktop PC Market Analysis by Mordor Intelligence

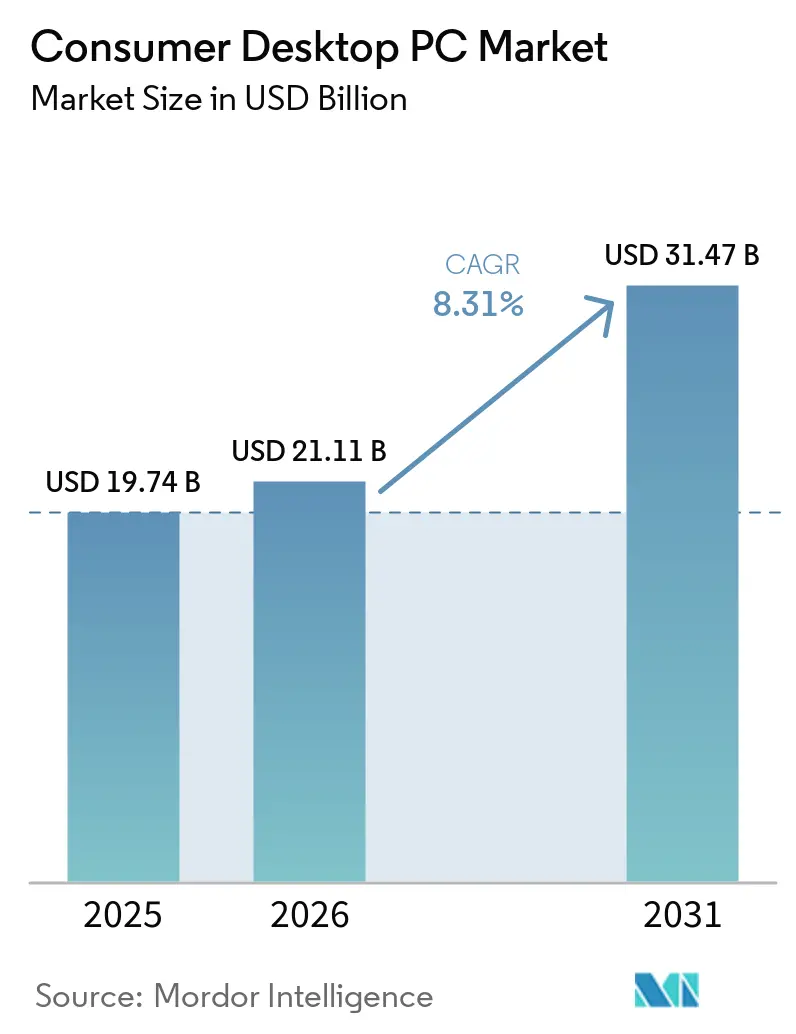

The consumer desktop PC market size is projected to be USD 19.74 billion in 2025, USD 21.11 billion in 2026, and reach USD 31.47 billion by 2031, growing at a CAGR of 8.31% from 2026 to 2031. Replacement activity linked to the Windows 10 end-of-support deadline, the migration toward AI-capable hardware featuring integrated neural processing units, and tariff-driven inventory restocking in North America are converging to lift demand. Desktop shipments climbed 14.4% year over year to 59 million units in 2025, outpacing notebooks and underscoring the category’s renewed relevance. Component suppliers are prioritizing high-bandwidth memory for data-center accelerators, a shift that inflates desktop bill-of-materials but also raises the value of mid-range and premium configurations built for on-device inference and 4K gaming. Intensifying urbanization in Asia-Pacific and the popularity of compact gaming rigs are driving the adoption of mini and small-form-factor designs, while online retail configurators are broadening buyer reach and compressing channel margins.

Key Report Takeaways

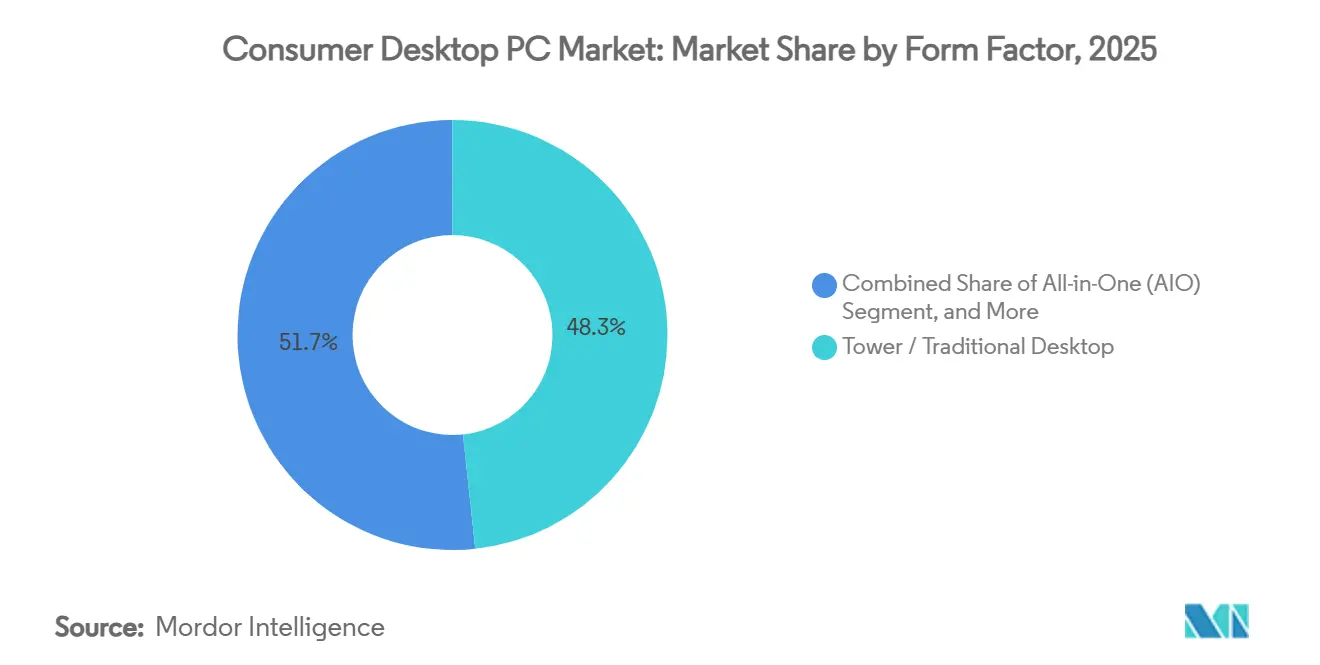

- By form factor, tower and traditional desktops led with 48.32% of the consumer desktop pc market share in 2025, while mini and small form factor systems are forecast to expand at a 10.21% CAGR through 2031.

- By processor architecture, x86 devices held 96.12% of the consumer desktop PC market in 2025, yet ARM-based models are projected to grow at a 9.12% CAGR during 2026-2031.

- By price band, mid-range systems captured 44.32% of the consumer desktop pc market share in 2025, whereas premium configurations above USD 1,200 are anticipated to scale at a 9.84% CAGR during the forecast period.

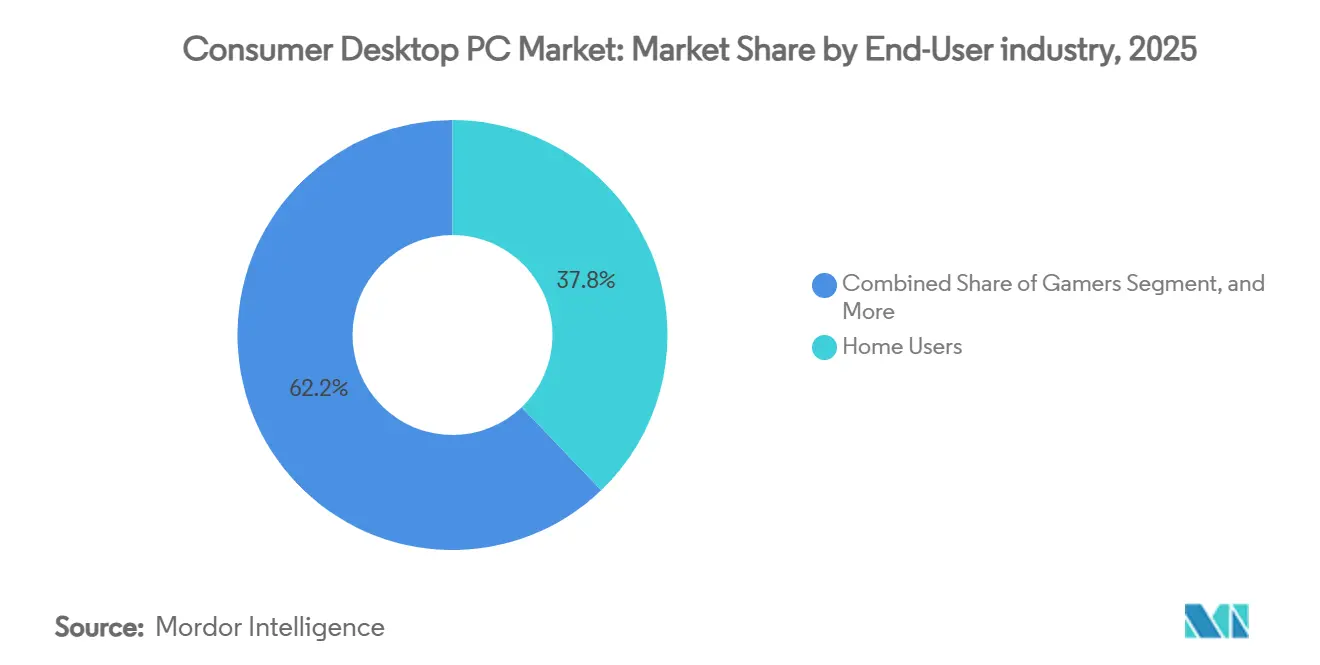

- By end user, gamers are the fastest-growing segment, with a 10.43% CAGR, overtaking the 37.83% share held by home users in 2025.

- By sales channel, online retail is set to advance at a 10.33% CAGR, eroding the 47.41% offline share recorded in 2025.

- By geography, North America accounted for 42.84% of the consumer desktop PC market in 2025, but Asia-Pacific is expected to register the fastest growth at an 8.94% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Consumer Desktop PC Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Windows 10 End-of-Support-Driven Replacement Cycle | +2.2% | Global, concentrated in North America and Europe | Short term (≤ 2 years) |

| Rising Demand for High-Performance Gaming PCs | +1.6% | Global, led by North America, Europe, and Asia-Pacific gaming hubs | Medium term (2-4 years) |

| Enterprise Adoption of AI-Capable Desktops | +1.4% | North America and Europe enterprise segments, expanding to Asia-Pacific | Medium term (2-4 years) |

| Growth in Remote and Hybrid Work Models | +1.0% | Global, particularly North America and Europe | Long term (≥ 4 years) |

| Surge in Creative Workstation Builds | +0.9% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Government Subsidies for Domestic CPU Ecosystems | +0.7% | Asia-Pacific core, primarily China and India | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Windows 10 End-of-Support-Driven Replacement Cycle

Microsoft terminated mainstream support for Windows 10 in October 2025, leaving over 1 billion consumer and enterprise devices vulnerable to rising Extended Security Update fees. This shift has prompted many enterprises, particularly those with stringent compliance requirements, to expedite their hardware refresh cycles. These organizations aim to avoid the escalating security surcharges, which are set to double annually, by transitioning to serviceable tower desktops that allow for easier component replacements. The resulting surge in device replacements is expected to peak through 2026 before gradually declining. However, this trend is already driving significant growth in the market, with North America and Western Europe experiencing the most notable impact.

Rising Demand for High-Performance Gaming PCs

NVIDIA’s RTX 5090, priced at USD 1,999, and RTX 5070, available at USD 549, have established new performance benchmarks for 4K and 8K gaming, catering to high-end gaming enthusiasts. Similarly, AMD’s Radeon RX 9070 XT, priced at USD 649, has made AI-enhanced upscaling technology more accessible to a broader audience. The growing popularity of esports venues in South Korea and Japan, along with the increasing demand for streaming workstations capable of encoding 4K60 video, continues to drive consumers toward desktops equipped with multi-slot GPUs and advanced cooling systems. Furthermore, the global ITX gaming case segment, projected to reach USD 745 million by 2025, underscores the ongoing trend toward compact yet high-performance gaming rigs.[1]NVIDIA, “GeForce RTX 50 Series Product Specifications,” nvidia.com

Enterprise Adoption of AI-Capable Desktops for On-Device Processing

Dell, HP, and Lenovo have recently updated their commercial product lines by incorporating Intel Core Ultra and AMD Ryzen AI processors. These processors can deliver up to 50 TOPS (Tera Operations Per Second) of local inference, enabling businesses to run advanced tools such as copilots and generative-image applications directly on their premises. This on-premises capability provides significant advantages, including enhanced privacy and reduced latency, which are critical for many organizations. Initial pilot programs have demonstrated notable cost savings when compared to the recurring expenses associated with perpetual cloud-based operations. These promising results are expected to drive broader adoption and deployment of these technologies across various industries through 2028.

Growth in Remote and Hybrid Work Models Sustaining Desktop Demand

Hybrid schedules have stabilized at nearly half of knowledge-worker days in North America and Europe. This shift has led to an increased demand for home office setups that are both efficient and cost-effective. Home offices are now commonly equipped with dedicated desktops that support dual-monitor setups, video-conference peripherals, and local storage arrays. These configurations offer performance and cost efficiency that laptops often fail to match. Additionally, the growing adoption of online configurators has significantly reduced the barriers to purchasing and upgrading components, making it easier for users to customize their systems to meet specific needs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevane | Impact Timeline |

|---|---|---|---|

| Rising Component Costs Due to Memory Realignment | -1.8% | Global, with acute pressure in North America and Europe | Short term (≤ 2 years) |

| Competition from High-End Laptops | -1.2% | Global, notably North America and Europe | Medium term (2-4 years) |

| Import Tariff Volatility | -0.9% | North America, secondary ripple in South America | Short term (≤ 2 years) |

| Limited Upgradeability of All-in-One Desktops | -0.5% | Global, focused in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Component Costs Due to Memory Realignment

DRAM prices surged 171% year-over-year in 2025, driven by fabricators reallocating production capacity to high-bandwidth modules for AI servers. This shift in focus has led memory to now account for 35% of the total bill of materials for a typical desktop. As a result, OEMs are facing tighter profit margins, and rising costs have pushed the prices of entry-level desktop systems above USD 650 in several emerging economies, making affordability a growing concern in these markets.[2]TrendForce, “DRAM Market Report Q4 2025,” trendforce.com

Intensifying Competition from High-End Laptops with Desktop-Class Performance

Intel Core Ultra 200S and AMD Ryzen 9000 mobile CPUs have significantly reduced the performance gap between mobile and desktop processors, offering comparable computing power. Additionally, RTX 4090-equipped notebooks now deliver up to 90% of the frame rates typically achieved by high-performance desktop towers. This advancement makes high-end laptops a viable alternative for professionals who prioritize portability and require a single, travel-friendly device for work and creative tasks. As a result, many professionals may justify the higher cost of these laptops, leading to a decline in desktop volumes within corporate environments and creative studios.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form Factor: Compact Builds Challenge Tower Dominance

Tower and traditional systems accounted for 48.32% of the consumer desktop PC market share in 2025. However, mini and small-form-factor models are projected to grow at a compound annual growth rate (CAGR) of 10.21%. Urban buyers in cities like Tokyo, Seoul, and Shanghai increasingly prefer compact designs due to space constraints and aesthetic preferences. The latest mini-ITX motherboards have advanced to support flagship CPUs and dual-slot GPUs without experiencing thermal throttling, making them a viable option for high-performance computing in smaller setups.

ASUS’s relaunch of the Intel NUC range and the growing popularity of boutique gaming rigs featuring tempered-glass micro-ATX cases further highlight this trend. On the other hand, all-in-one desktops continue to face challenges due to their perceived lack of upgradeability, which limits their appeal to specific enterprise niches where maintaining clean and organized workspaces is prioritized over lifecycle flexibility. Meanwhile, workstation towers remain a lucrative high-margin segment, particularly for CAD and 3D rendering applications, driven by the performance capabilities of Threadripper PRO and Xeon W CPUs.

By Processor Architecture: ARM Gains Momentum Amid x86 Scale

The consumer desktop PC market for x86 machines significantly outperformed alternatives in 2025, maintaining its dominance. However, ARM-based desktops are projected to grow at a robust 9.12% CAGR, driven by strategic government initiatives in countries like China and India. These nations are implementing procurement incentives, offering up to 20% of bid value to promote the adoption of homegrown silicon. Notable players such as Loongson, with its 3C6000 processors, and Zhaoxin, with its KX-7000 series, have already secured early government contracts, demonstrating their market potential. Additionally, advancements in Windows on ARM, particularly in x86 emulation, are addressing compatibility concerns, making these systems more appealing to buyers in sectors like education and civil service.

Despite these advancements, broader commercial adoption of ARM-based desktops remains contingent on the development and maturity of the software ecosystem. Nevertheless, the growth of ARM highlights a deliberate effort by governments and industries to achieve supply-chain sovereignty and reduce reliance on external technologies. Meanwhile, RISC-V architecture, though promising, is still in its prototype phase, with no mass-market desktop launch expected before 2029. This delay limits its immediate influence on the desktop PC market, keeping its impact minimal in the short term.

By Price Band: Premium Builds Capture AI and Gaming Upside

Mid-range desktop PCs priced between USD 600 and USD 1,200 accounted for 44.32% of the consumer desktop PC market in 2025. This segment continues to dominate due to its balance of affordability and performance, appealing to a wide range of consumers. However, premium desktop PCs priced above USD 1,200 are projected to grow at a compound annual growth rate (CAGR) of 9.84% during the forecast period. This growth is driven by increasing demand for high-performance systems capable of handling intensive tasks such as 4K gaming and advanced generative AI workflows. Recent GPU launches, including the NVIDIA RTX 5090 with 32 GB GDDR7 memory and the AMD Radeon RX 9070 XT with 16 GB VRAM, are fueling this demand by offering cutting-edge graphics capabilities and enhanced processing power.

Entry-level PCs, traditionally defined as systems priced below USD 600, are facing significant cost pressures due to rising DDR5 memory prices. These cost increases are pushing budget-conscious consumers to explore alternatives, such as refurbished or second-hand desktop towers, or to delay their purchases altogether. Additionally, compliance with Energy Star 9.0 standards, which mandate lower idle power consumption, has introduced additional costs for manufacturers. While premium buyers more easily absorb these added expenses, they pose a challenge for the entry-level segment, which is more price-sensitive. As a result, the entry-level market is experiencing a shift in consumer behavior, with affordability becoming a critical factor in purchasing decisions.

By End-User Industry: Gamers Propel the Fastest Growth

Home users accounted for 37.83% of the market share in 2025, but the gaming segment is projected to grow at a 10.43% CAGR, driven by increasing investments in esports sponsorships and the monetization of streaming platforms. The introduction of technologies like DLSS 4 multi-frame generation and FSR 4 upscaling has significantly reduced the entry barriers for GPUs in competitive gaming, encouraging gamers to upgrade their systems more frequently to stay competitive.

Creative professionals are also adopting similar high-performance hardware to support demanding workloads, such as Adobe Firefly for generative design and Autodesk Arnold for rendering tasks. Meanwhile, small and medium-sized businesses (SMBs) continue to favor desktop towers equipped with standard ATX boards, as these systems offer cost-effective upgrade options to meet evolving business needs. On the other hand, enterprises prioritize security features and deployment uniformity, increasingly opting for AI-ready CPUs to enhance operational efficiency, particularly during the ongoing Windows 10 refresh cycle.

By Sales Channel: Online Retail Disrupts Traditional Distribution

Offline chains accounted for 47.41% of sales in 2025, but online outlets are expected to grow faster, with a projected CAGR of 10.33%. This growth is fueled by shifting consumer preferences toward digital platforms and the increasing convenience of online shopping. Dell’s strategic decision to sell desktops through Walmart and the inclusion of 200 boutique SKUs in Best Buy’s third-party marketplace underscore a significant transition toward utilizing mass digital storefronts to expand market reach and cater to diverse customer needs.

Direct-to-consumer builders, such as System76 and Origin PC, continue to thrive by prioritizing extensive customization options and fostering strong community engagement, which resonates well with their target audience. At the same time, value-added resellers are striving to defend their market share by offering specialized services, including imaging and on-site deployment. However, the growing adoption of cloud-based device management tools is gradually reducing integration complexities, presenting both challenges and opportunities for these resellers to adapt and innovate in a competitive landscape.

Geography Analysis

Asia-Pacific is on course for an 8.94% CAGR through 2031, supported by India’s INR 170 billion (approximately USD 2.05 billion) incentive program for IT hardware and China’s USD 70 billion AI and chip subsidy package. Production footprints in Tamil Nadu and Karnataka expand sharply as Foxconn and Flex localize assembly to capture duty benefits. Municipal procurement policies in China, granting a 20% price advantage to domestic CPUs, accelerate ARM desktop adoption in government offices.

North America remains the largest single market, with a 42.84% share in 2025. Section 301 tariffs on Chinese semiconductors were raised to 50% in late 2024, prompting inventory pulls, but ongoing diversification into Mexico and Vietnam eases longer-term risk. Hybrid work patterns are driving demand for home-office towers that pair multi-monitor support with local AI acceleration. Europe ranks second by revenue. EU Ecodesign mandates taking effect in 2027 will raise power-supply costs, yet sustainability labeling could steer eco-conscious consumers toward desktops that promise lower standby draws. Regional gaming hubs in Germany, Poland, and the Nordics continue to see steady upgrades as 240 Hz monitors proliferate.

South America is highly price-sensitive and remains susceptible to fluctuations in foreign exchange rates. However, a niche market of enthusiasts in Brazil continues to support a modest yet resilient boutique-builder scene, catering to specific consumer demands. Meanwhile, the Middle East and Africa are still in the early stages of market development, with procurement efforts primarily focused on public-sector digitization initiatives. These include Saudi Vision 2030, which aims to diversify the economy and enhance public services, and the UAE Smart Government initiatives, which focus on leveraging technology to improve governance and citizen engagement.

Competitive Landscape

Lenovo, HP, and Dell accounted for moderate to high shares of global shipments in 2025, reflecting moderate market consolidation. However, the consumer desktop PC market still provides opportunities for niche players and specialists to carve out their space. Lenovo achieved shipments of 71 million units, driven by aggressive promotional campaigns and strategic pricing in the Asia-Pacific region. HP followed closely with 57 million units, leveraging its strong presence in North America, particularly through government contracts. Dell, on the other hand, recorded shipments of 42 million units, supported by a surge in small and medium-sized business (SMB) refresh cycles. These figures highlight the competitive dynamics among the leading players while leaving room for smaller competitors to address specific market needs.

Strategic focus centers on AI-capable endpoints. Dell’s OptiPlex 7420 AIO with Intel Core Ultra NPU targets cost-conscious enterprises; HP’s Elite Mini 800 G9 offers compact form factors with NPU integration; and Lenovo’s ThinkCentre neo Ultra Gen 2 undercuts rivals in SMB channels. Apple disrupts price-performance norms by leveraging vertical silicon control in the Mac mini M4 at USD 599, appealing to creative users seeking a macOS ecosystem.

Boutique and gaming brands, including ASUS ROG, MSI, Razer, Corsair, CyberPowerPC, and iBuyPower, leverage overclock-ready motherboards, RGB aesthetics, and influencer marketing to carve enthusiast niches. Supply-chain pressures from DRAM inflation favor vertically integrated players or firms with long-term supply contracts. Tariff-induced relocation to Vietnam and India requires near-term capital outlays but promises margin recovery as new capacity stabilizes.

Consumer Desktop PC Industry Leaders

Lenovo Group Limited

HP Inc.

Dell Technologies, Inc.

Apple Inc.

ASUSTeK Computer Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Micron confirmed its exit from consumer DRAM modules to reallocate wafer capacity toward HBM3 for AI accelerators.

- January 2026: China’s 20% domestic CPU price preference for public procurement took effect, boosting orders for Loongson and Zhaoxin desktops.

- March 2025: AMD debuted the Radeon RX 9070 XT and RX 9070 GPUs based on the RDNA 4 architecture at USD 649 and USD 549, respectively.

- February 2025: NVIDIA launched the RTX 5070 Ti and RTX 5070 GPUs using Blackwell architecture with DLSS 4 support.

Global Consumer Desktop PC Market Report Scope

The Consumer Desktop PC Market refers to the global industry focused on the design, manufacture, distribution, and sale of desktop personal computers intended primarily for individual and consumer use, including entertainment, gaming, content creation, home productivity, and light professional workloads. These systems are optimized for performance, customization, affordability, and user experience, spanning a wide range of configurations and capabilities.

The Consumer Desktop PC Market Report is Segmented by Form Factor (Tower/Traditional Desktop, All-in-One, Mini/Small Form Factor, Gaming/Performance Rigs, and Workstation Desktops), Processor Architecture (x86, ARM, and RISC-V), Price Band (Entry-Level, Mid-Range, and Premium), End-User Industry (Home Users, Gamers, Professionals and Creators, Small and Medium Businesses, and Enterprises), Sales Channel (Online Retail, Offline Retail, Direct-to-Consumer, and Value-Added Resellers), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Tower / Traditional Desktop |

| All-in-One (AIO) |

| Mini / Small Form Factor |

| Gaming / Performance Rigs |

| Workstation Desktops |

| x86 |

| ARM |

| RISC-V |

| Entry-Level (<USD 600) |

| Mid-Range (USD 600- USD 1,200) |

| Premium (>USD 1,200) |

| Home Users |

| Gamers |

| Professionals & Creators |

| Small & Medium Businesses |

| Enterprises |

| Online Retail |

| Offline Retail |

| Direct-to-Consumer |

| Value-Added Resellers |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Form Factor | Tower / Traditional Desktop | ||

| All-in-One (AIO) | |||

| Mini / Small Form Factor | |||

| Gaming / Performance Rigs | |||

| Workstation Desktops | |||

| By Processor Architecture | x86 | ||

| ARM | |||

| RISC-V | |||

| By Price Band | Entry-Level (<USD 600) | ||

| Mid-Range (USD 600- USD 1,200) | |||

| Premium (>USD 1,200) | |||

| By End-User Industry | Home Users | ||

| Gamers | |||

| Professionals & Creators | |||

| Small & Medium Businesses | |||

| Enterprises | |||

| By Sales Channel | Online Retail | ||

| Offline Retail | |||

| Direct-to-Consumer | |||

| Value-Added Resellers | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the consumer desktop pc market today?

The consumer desktop pc market size stands at USD 21.11 billion in 2026 and is projected to reach USD 31.47 billion by 2031.

What growth rate is expected for consumer desktop PCs over the next five years?

The sector is forecast to expand at a CAGR of 8.31% from 2026 to 2031, propelled by Windows 10 replacement cycles and AI-capable hardware adoption.

Which form factor is growing the fastest?

Mini and small form factor desktops lead with a projected 10.21% CAGR as urban buyers favor compact systems for gaming and productivity.

Why are DRAM prices impacting desktop PC pricing?

Memory makers have shifted wafer capacity toward high-bandwidth modules for AI servers, driving DDR5 costs 171% higher year-over-year and raising desktop bill-of-materials.

What region offers the highest future growth potential?

Asia-Pacific is expected to post an 8.94% CAGR through 2031, supported by manufacturing incentives in India and semiconductor subsidies in China.

Are laptops expected to replace desktops entirely?

High-end laptops now deliver near-desktop performance, but desktops retain advantages in upgradeability, cooling, and total cost of ownership for gamers, creators, and hybrid-work home offices.

Page last updated on: