Mini PC Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 23.14 Billion |

| Market Size (2031) | USD 29.11 Billion |

| Growth Rate (2026 - 2031) | 4.70% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mini PC Market Analysis by Mordor Intelligence

The Mini PCs market size is projected to expand from USD 22.1 billion in 2025 and USD 23.14 billion in 2026 to USD 29.11 billion by 2031, registering a 4.7% CAGR between 2026 to 2031. Measured headline growth hides a dual-speed reality in which mainstream desktop-replacement models stagnate while purpose-built configurations for gaming, edge inference, and digital signage capture outsize value. As enterprises redesign networks around edge computing nodes, compact boxes with dedicated neural processing units are replacing latency-prone cloud round-trips, especially on factory floors and in retail analytics. Energy-efficiency mandates in the United States Environmental Protection Agency Energy Star 9.0 program and the EU Ecodesign Directive favor devices that idle below 50 watts, tilting budgets toward the Mini PCs market. Meanwhile, semiconductor shortages that peaked in 2024 have eased, yet lingering risk premiums continue to compress margins for vendors shipping low-end models. Across the forecast horizon, innovation in processor architecture, particularly hybrid x86 and ARM designs with integrated AI engines, is expected to widen the performance-per-watt gap over tablets and ultrabooks, protecting the Mini PCs market from complete erosion in consumer segments.

Key Report Takeaways

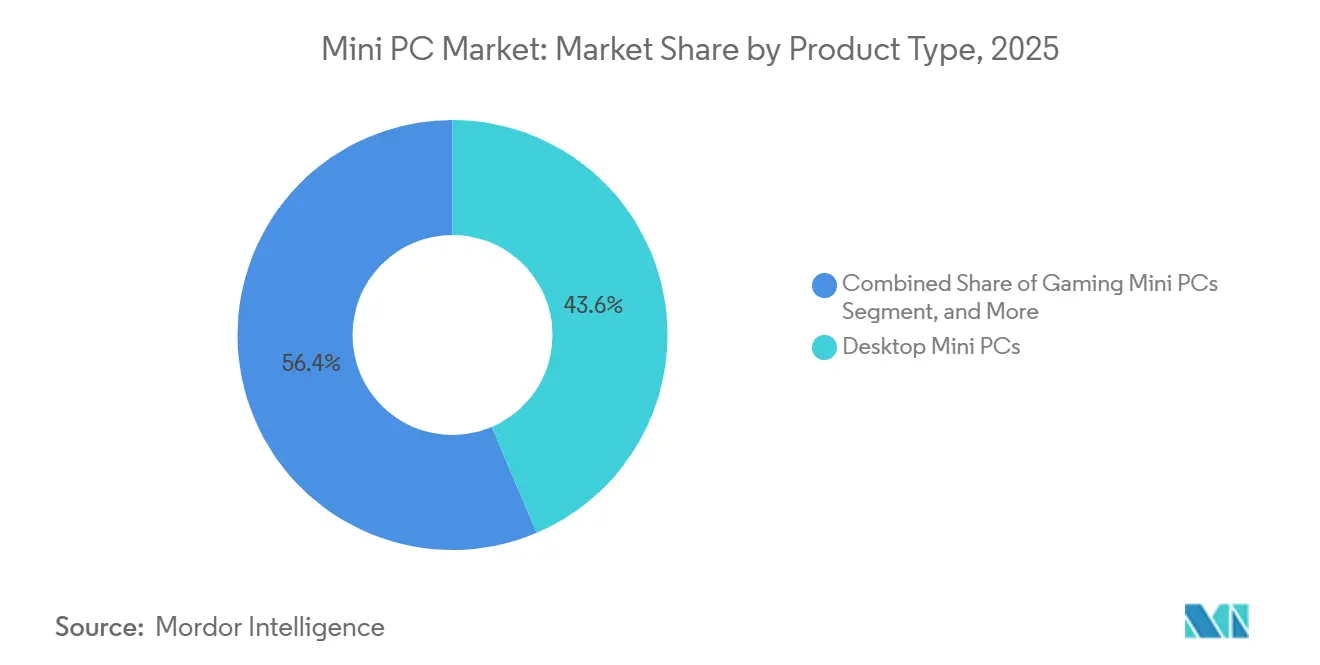

- By product type, desktop models led with 43.60% of the Mini PC market share in 2025, while gaming configurations are projected to advance at a 10.20% CAGR through 2031.

- By end user, the consumer segment held 38.10% of the Mini PC market share in 2025, while the Healthcare segment is projected to advance at a 9.80% CAGR through 2031.

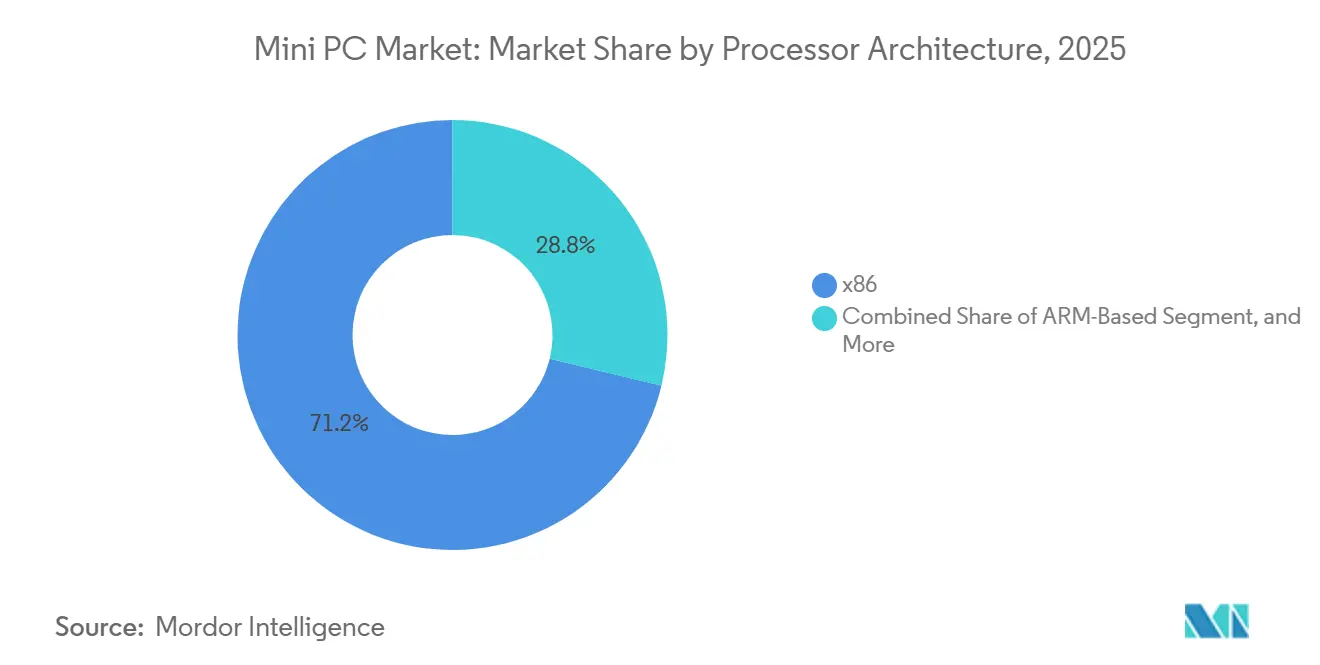

- By processor architecture, x86 devices held 71.20% Mini PCs market size of the Mini PC market in 2025; ARM-based systems are expanding at an 8.90% CAGR through 2031.

- By distribution channel, online retail represented 52.20% of of the Mini PC market in 2025, and that stream is growing at a 7.60% CAGR as direct-to-consumer models scale.

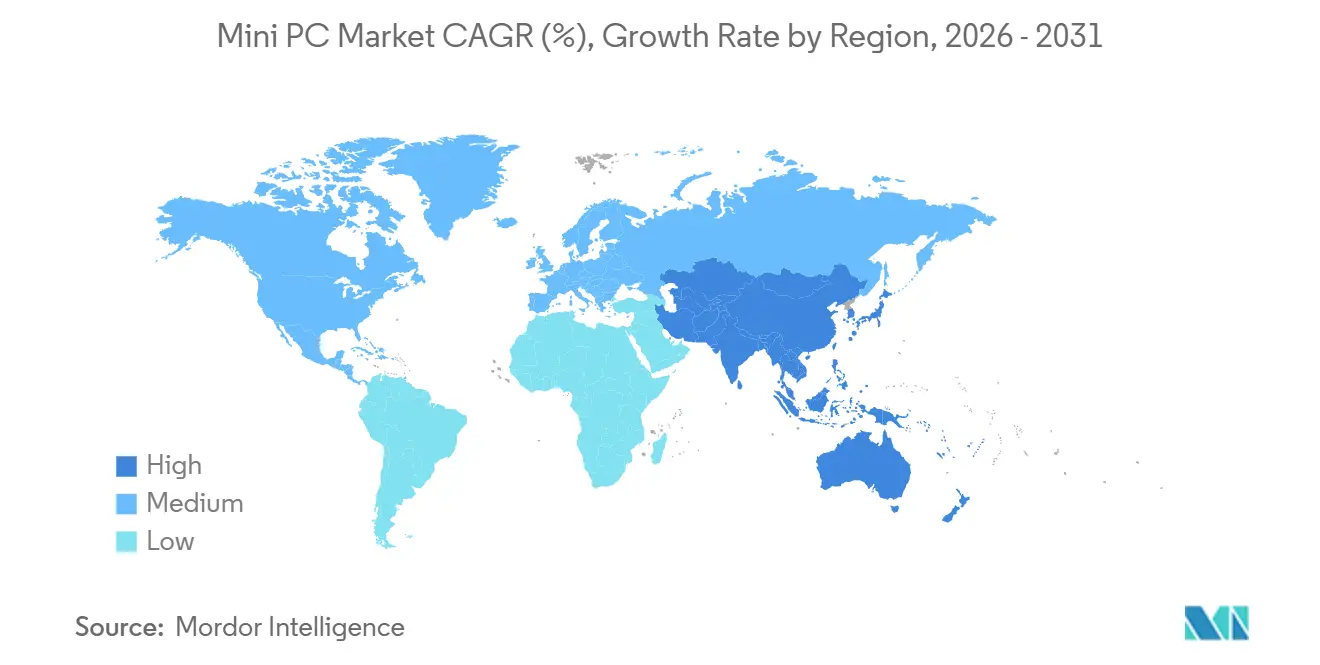

- By geography, North America controlled 28.60% Mini PCs market share in 2025, whereas Asia-Pacific is forecast to post a 7.80% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Mini PC Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Adoption of Edge Computing Across Enterprise Sectors | +1.2% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Growing Demand for Space-Saving Computing Solutions in Smart Homes and Offices | +0.9% | Global, led by Asia-Pacific urban centers | Short term (≤ 2 years) |

| Price-Performance Improvements in x86 and ARM Processors | +0.8% | Global | Medium term (2-4 years) |

| Proliferation of Digital Signage Networks in Developing Markets | +0.6% | Asia-Pacific core, spillover to Middle East and Africa | Long term (≥ 4 years) |

| Government Incentives for Energy-Efficient IT Hardware | +0.5% | North America and Europe, emerging in Asia-Pacific | Medium term (2-4 years) |

| Emerging DIY Gaming Communities Adopting Barebone Mini PCs | +0.4% | Global, concentrated in North America, Europe, and South Korea | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Edge Computing Across Enterprise Sectors

Factory automation lines, autonomous mobile robots, and point-of-sale analytics increasingly rely on local inference to circumvent the 100-200 millisecond delays typical of cloud round-trips. Mini PCs fitted with Intel Xeon 6 or AMD Ryzen AI processors now deliver 10-15 TOPS of on-device neural throughput, meeting real-time quality-inspection requirements without external connectivity.[1]Intel Corporation, “Intel Xeon 6 Processor Family Product Brief,” intel.com Data-sovereignty regulations in the European Union and China compel manufacturers to process sensitive telemetry on-premises, further anchoring compute at the network edge. Power-density ceilings at hyperscale facilities reinforce the shift because every relocated inference workload frees megawatts of constrained data-center capacity. The resulting architectural pivot supports sustained demand for rugged, fanless enclosures that mount near sensors inside manufacturing cells. Through 2031, enterprises are expected to roll out distributed fleets of edge-tuned Mini PCs, locking in a multi-year replacement cycle for high-reliability devices.

Growing Demand for Space-Saving Computing Solutions in Smart Homes and Offices

Urban real-estate costs exceeding USD 100 per square foot spur corporate IT teams to reclaim desk area with sub-one-liter systems. Apple’s Mac mini M4 measures 12.7 cm square, idles at five watts, and sets the design benchmark for silent performance desktops. Similar footprints let remote workers tuck devices behind monitors, eliminating cable sprawl and fan noise in shared living spaces. Energy bills also drop; swapping a 150-watt tower for a 25-watt mini workstation can save roughly USD 70 per endpoint per year, material for small businesses running hundreds of nodes. Aesthetic minimalism resonates with modern office layouts that emphasize collaborative workspaces over cubicle rows, reinforcing the Mini PCs market as the logical successor to bulky towers. The preference for clutter-free environments is accelerating refresh cycles in professional studios, call centers, and co-working facilities alike.

Price-Performance Improvements in x86 and ARM Processors

Intel 14th-generation Core chips and AMD Ryzen 7000 parts inject desktop-grade horsepower into one-liter chassis while holding bill-of-material outlays steady, erasing the premium once associated with tiny form factors.[2]Advanced Micro Devices, “AMD Ryzen 7000 Series Desktop Processors,” amd.com On the RISC side, Qualcomm’s Snapdragon X Elite introduces Oryon CPU cores that rival x86 single-thread throughput at 40% lower power draw, enabling fanless Mini PCs that double as portable development stations.[3]Qualcomm Technologies, “Snapdragon X Elite Platform Overview,” qualcomm.com Shrinking transistor nodes at 5 nm and 3 nm, lower leakage currents, and amplifying generational gains with minimal thermal overhead. Because heat sinks scale with wattage, every efficiency win frees enclosure volume for additional NVMe storage or improved airflow. The upshot is a new price band USD 500 to USD 700where 4K video editing, CAD modeling, and light AI inference are all achievable, democratizing advanced compute for design studios and engineering teams.

Proliferation of Digital Signage Networks in Developing Markets

Transit authorities and big-box retailers in India, Indonesia, and the Gulf states are replacing static posters with centrally managed 4K displays, each powered by a stick PC or fanless brick that survives ambient temperatures above 40 °C. Rugged aluminum heat spreaders and conformal-coated boards enable 24/7 playback without airflow, ensuring up to seven-year deployment life. Because content updates cut printing costs by 70% and unlock dynamic pricing, capital payback occurs within 18 months, sustaining a long pipeline of projects funded by advertising budgets. Emerging smart-city programs bundle device procurement with fiber backhaul, creating bulk orders that favor ODMs capable of sub-USD 150 price points at volume. As these networks scale across railway corridors and convenience-store chains, the installed base of specialized signage Mini PCs is forecast to swell, cushioning the overall Mini PCs market against slowdowns in consumer refreshes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from Tablets and Small Form-Factor Laptops | -0.7% | Global, most acute in consumer segments | Short term (≤ 2 years) |

| Limited Expandability and Thermal Constraints | -0.5% | Global | Medium term (2-4 years) |

| Semiconductor Supply Chain Volatility | -0.4% | Global, acute for smaller vendors | Short term (≤ 2 years) |

| Fragmented After-Sales Service Networks in Emerging Economies | -0.3% | Asia-Pacific, Middle East, Africa, South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Competition from Tablets and Small Form-Factor Laptops

Detachable tablets running ARM silicon now deliver laptop-class performance plus 5G radios and all-day batteries, displacing entry-level desktops in homes and classrooms. IDC shipment trackers show tablet volumes holding above 130 million units in 2025, signaling a durable appetite despite slowing PC replacements. Consumer buyers weighing a USD 400 convertible against a Mini PC plus monitor, keyboard, and webcam often choose the integrated route, shrinking the addressable base for low-cost boxes. Hybrid workers add to the squeeze because a single ultraportable device serves both office and travel needs, whereas a stationary mini requires a secondary laptop for mobility. The substitution risk is most pronounced in price-sensitive geographies where households own just one computing product, tightening growth in the broader Mini PCs market through 2027.

Limited Expandability and Thermal Constraints

Soldered CPUs, fixed GPUs, and sparse PCIe lanes limit upgrades to memory and storage, forcing full box replacements rather than incremental refreshes. In sub-one-liter enclosures, a 65-watt processor quickly saturates heat pipes, prompting fans to ramp beyond 40 decibels and still triggering 15% clock-throttling during multi-hour renders. Enthusiasts who value overclocking or multi-drive RAID hesitate to trade openness for space savings, capping the ceiling for high-end configurations. Fanless industrial models face the flip side: TDP caps of 15-25 watts eliminate participation in GPU-accelerated workloads. Enterprises trying to standardize SKUs across departments confront SKU sprawl because no single mini configuration satisfies both creative and clerical workloads. These physical realities dampen the Mini PCs market trajectory, especially in segments where longevity and modularity are procurement priorities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Desktop Dominance Meets Gaming Disruption

Desktop variants contributed 43.60% Mini PCs market share in 2025, supplying corporate refresh cycles with compact boxes that slide into existing device-management stacks. Their lower idle power and 80% smaller volume versus towers reduce operating expenditures and free desk space, perks that resonate in finance and call-center rollouts. Momentum, however, is flattening because thin clients and cloud desktops absorb workloads that once required local horsepower. Gaming-oriented units are the growth catalyst, rising at a 10.20% CAGR on the back of DIY communities that squeeze discrete GPUs into two-liter shells without sacrificing 144 Hz gameplay. ODMs such as Minisforum iterate every nine months, bundling USB4 eGPU docks for future-proofing and steering share away from legacy tower rigs.

The Mini PCs market size for industrial SKUs is expanding steadily yet quietly as manufacturers bolt fanless slabs to conveyor belts and inspection cameras. Rugged fanless models, often with M12 connectors and MIL-STD-810 shock certification, anchor deployments in oilfields and mining camps where vibration would shatter spinning drives. Barebone kits appeal to system integrators who preload Linux, extra COM ports, or fieldbuses for CNC machines. Finally, stick PCs occupy the tiniest niche, powering hotel TVs and thin digital kiosks where sub-USD 150 budgets trump performance. Across the spectrum, commoditization at the desktop tier is steering vendors toward differentiated thermals, ruggedization, or gaming aesthetics to preserve margin.

By End User: Healthcare Outpaces Consumer Segments

Healthcare workloads are racing ahead at a 9.80% CAGR, turning telemedicine carts and Picture Archiving and Communication System stations into primary growth vectors within the Mini PCs market. Fanless aluminum casings mitigate infection risk by eliminating dust-laden vents, a feature attractive to hospital procurement teams. HIPAA audit logging is simpler when devices run standard operating systems that IT departments already patch, further lifting adoption. In diagnostic imaging centers, compact boxes sit directly behind 8-megapixel radiology monitors, shrinking cable runs and improving ergonomics during lengthy reading sessions. While consumer share remains sizeable at 38.10%, it weathered attrition in 2025 as tablets ate into entry-level demand.

Commercial office fleets form a steady middle ground, replacing towers with slim chassis that mount under sit-stand desks. Industrial and manufacturing buyers lean on wide-temperature parts and redundant Gigabit Ethernet to keep assembly lines humming. Education trends are more muted because Chromebooks consume a growing slice of student computing budgets. Retail and hospitality installations employ Mini PCs to drive menu boards and self-service checkouts, but tablet-based mobile point-of-sale rigs add competitive pressure. Government and defense contracts require FIPS-validated encryption modules and tamper-evident screws, nudging specialized vendors into this regulated but predictable revenue stream.

By Processor Architecture: ARM Challenges x86 Hegemony

x86 silicon commanded 71.20% of the 2025 Mini PCs market size, anchored by decades of Windows and Linux software heritage. Yet ARM is posting an 8.90% CAGR as Qualcomm and Apple showcase workloads that equal or exceed Core-i7 class scores while operating at half the wattage. Microsoft’s expanded catalog of ARM-native Office, Teams, and Adobe apps suggests software inertia is crumbling, a precondition for broader enterprise pilots. Lower-power chips enable silent rigs for trading floors and recording studios where fan noise is unwelcome. Over time, hybrid compute strategies, packing efficiency cores, performance cores, and dedicated NPUs onto the same die, blur the former architecture divide.

Other architectures, mainly RISC-V, trail distantly but win design-ins for ultra-secure gateways and cost-squeezed IoT endpoints. Future Mini PCs market share rebalancing will hinge less on instruction-set politics and more on task-optimized silicon blocks, whether AI tensor engines or media coders. Intel’s inclusion of low-power E-cores in desktop packages hints at convergence, proving both camps have accepted heterogeneous design as the route to balanced thermal envelopes in miniature shells.

By Distribution Channel: E-Commerce Reshapes Value Chains

Online storefronts captured 52.20% revenue in 2025 and are compounding at a 7.60% CAGR, propelled by comparison engines, influencer reviews, and drop-ship logistics that bypass traditional wholesalers. Mini PCs market participants from Shenzhen can undercut established OEMs by 30-40% because single-area mega-factories fold board population, chassis stamping, and final assembly into vertical flows. For consumers, next-day delivery and liberal return policies replicate big-box immediacy without floor-space costs. On the flip side, returns management and warranty shipping dampen profitability, prompting premium brands to launch direct sites that bundle optional on-site service for enterprise buyers.

Brick-and-mortar chains remain relevant among corporates needing same-day swaps and volume-priced peripherals. Value-added resellers thrive in complex rollouts such as mall-wide signage or factory supervisory control layers where bespoke imaging, rack mounting, and service-level agreements justify consulting fees. Even as pure online share climbs, hybrid click-and-collect models emerge, letting buyers inspect units in person before committing. The distribution chessboard, therefore, is fluid, but the gravitational pull of lower channel margins keeps reallocating volumes to e-commerce.

Geography Analysis

Asia-Pacific is the velocity engine of the Mini PCs market, recording a 7.80% CAGR through 2031 on the back of manufacturing clusters in China, Taiwan, and South Korea that shave 40% off landed costs. Government smart-city initiatives in India and Indonesia are ordering fleets of signage players and edge gateways, often stipulating sub-USD 300 price caps achievable only with local supply-chain density. Shenzhen’s integrated ecosystem lets vendors spin refreshed boards inside 30 days, beating Western development timelines and funneling first-mover advantage into global online listings. Consumer uptake in Japan and South Korea is similarly robust because space constraints in urban apartments make desk-footprint a purchasing criterion.

North America held a mature 28.60% Mini PCs market share in 2025, but is flattening as device penetration tops 80%. Growth pockets persist in edge inference pilots at retail chains and in the booming e-sports subculture that prizes LAN-party-friendly rigs. Energy-efficiency rebates under state-level incentive programs accelerate the replacement of tower desktops with 35-watt small-form PCs in municipal offices. Yet substitution by laptops in education and enterprise mobility slows unit additions, especially beyond the corporate refresh window.

Europe’s outlook is moderate, governed by tight energy regulations that make sub-50-watt idle a compliance must. The EU Ecodesign Directive that became enforceable in 2024 prompts companies to phase out legacy towers, benefiting low-TDP mini boxes.[4]European Commission, “Ecodesign Requirements for Computers and Servers,” europa.eu Eastern European contract manufacturers also climb the value ladder, assembling barebones under private-label Western brands to dodge high shipping costs from Asia. The Middle East and Africa, small in absolute terms, leverage construction booms and hospitality mega-projects that embed smart kiosks and room-control hubs powered by stick PCs. South America’s traction concentrates in Brazil’s consumer segment and Chilean fintech corridors, though high import tariffs continue to inflate street prices by up to 35%, capping upside.

Competitive Landscape

The five largest vendors combine for under 35% share, leaving the Mini PCs market with a concentration score of 6 out of 10. Apple maintains its dominance in the premium segment by vertically integrating silicon, operating systems, and retail channels. This strategy enables Apple to achieve 40-50% margins even on sub-one-liter desktops. ASUS and MSI, on the other hand, target the gaming community by incorporating NVIDIA RTX 4070 graphics cards into 2.5-liter chassis, complemented by RGB-lit aluminum designs. Meanwhile, Lenovo, HP, and Dell leverage their enterprise account control by bundling Intel vPro and TPM 2.0 security features with global next-business-day service, effectively countering price competition from ODMs.

Shenzhen-based assemblers like Beelink and Trigkey adopt a rapid refresh cycle, updating SKUs every six months. These companies often ship BIOS betas that tech enthusiasts can flash at home, prioritizing early access to new processors over polished user experiences. Consolidation within the market remains selective. For instance, ASUS acquired Intel’s NUC line in 2023, while Minisforum carved out a niche in the workstation segment by offering high-capacity DDR5 support. Compliance has emerged as a critical competitive factor, with Energy Star 9.0 standards and expanded EU right-to-repair regulations favoring designs that feature easily replaceable SSDs and accessible panel screws.

Strategic opportunities in the Mini PCs market lie in ruggedized edge inference devices. These products, equipped with military-spec enclosures and conformal coatings, are designed for deployment in challenging environments such as drilling platforms or freezer warehouses. Another growth area is AI appliances tailored for retail loss prevention. These devices come pre-installed with computer-vision stacks, enabling grocers to reduce shrinkage without the need to overhaul backend software. As the market evolves, these specialized applications are expected to drive innovation and open new revenue streams for vendors.

Mini PC Industry Leaders

Shenzhen New Experience Technology Co., Ltd.

ZOTAC Technology Limited

Shuttle Inc.

Azulle Tech Inc.

ECS Elitegroup Computer Systems Co Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: GMKtec launched NucBox K17 AI mini PC featuring Intel Core Ultra processor and up to ~97 TOPS AI performance, supporting multi-8K displays and edge AI workloads.

- March 2026: NZXT launched H2 Mini PC lineup with high-end AMD/Intel processors and RTX GPUs, targeting compact gaming and creator markets.

- January 2026: Qualcomm released a firmware update that unlocks NPU-based real-time language translation on Snapdragon X Elite mini PCs, enhancing on-device AI capabilities for customer-service kiosks.

- October 2025: ASUS introduced a new AI-integrated Mini PC series, enhancing user interaction and performance through AI capabilities.

Global Mini PC Market Report Scope

The Mini PCs Market refers to compact, small form factor desktop computing devices that integrate essential hardware components such as processors, memory, storage, and connectivity into a space-efficient chassis. These systems are designed to deliver standard desktop performance while minimizing size, power consumption, and physical footprint. Mini PCs are widely used across consumer, enterprise, and industrial applications, including home computing, office workstations, digital signage, and edge computing environments. The market includes standalone mini desktops, thin clients, and embedded compact systems.

The Mini PCs Market Report is Segmented by Product Type (Desktop Mini PCs, Industrial Mini PCs, Gaming Mini PCs, Barebone Mini PCs, Rugged Fanless Mini PCs, Stick PCs), End User (Consumer, Commercial Offices, Industrial and Manufacturing, Healthcare, Education, Retail and Hospitality, Government and Defense), Processor Architecture (x86, ARM Based, Other Processor Architectures), Distribution Channel (Online E-Commerce, Offline Retail, Direct B2B or VAR Sales), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Desktop Mini PCs |

| Industrial Mini PCs |

| Gaming Mini PCs |

| Barebone Mini PCs |

| Rugged Fanless Mini PCs |

| Stick PCs |

| Consumer |

| Commercial Offices |

| Industrial and Manufacturing |

| Healthcare |

| Education |

| Retail and Hospitality |

| Government and Defense |

| x86 |

| ARM Based |

| Other Processor Architectures |

| Online E Commerce |

| Offline Retail |

| Direct B2B or VAR Sales |

| North America | United States |

| Canada | |

| South America | Brazil |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Rest of Africa |

| By Product Type | Desktop Mini PCs | |

| Industrial Mini PCs | ||

| Gaming Mini PCs | ||

| Barebone Mini PCs | ||

| Rugged Fanless Mini PCs | ||

| Stick PCs | ||

| By End User | Consumer | |

| Commercial Offices | ||

| Industrial and Manufacturing | ||

| Healthcare | ||

| Education | ||

| Retail and Hospitality | ||

| Government and Defense | ||

| By Processor Architecture | x86 | |

| ARM Based | ||

| Other Processor Architectures | ||

| By Distribution Channel | Online E Commerce | |

| Offline Retail | ||

| Direct B2B or VAR Sales | ||

| By Geography | North America | United States |

| Canada | ||

| South America | Brazil | |

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

Key Questions Answered in the Report

How large will the Mini PCs market be in 2031?

It is projected to reach USD 29.11 billion by 2031 based on the current 4.7% CAGR.

Which end-user segment is growing fastest for mini PCs?

Healthcare leads with a 9.80% CAGR through 2031, driven by telemedicine stations and PACS upgrades.

What share do desktop mini PCs hold today?

Desktop variants accounted for 43.60% of 2025 revenue within the Mini PCs market.

Why is Asia-Pacific expanding faster than North America?

Regional manufacturing scale, sub-USD 300 price points, and smart-city signage projects are pushing a 7.80% CAGR in Asia-Pacific.

Are ARM-based mini PCs gaining on x86 models?

Yes, ARM devices are growing at an 8.90% CAGR as Qualcomm and Apple chips offer similar performance at lower power.

What is the main restraint on further mini PC adoption?

Competition from tablets and ultrabooks, which bundle mobility and displays into single devices, is trimming near-term consumer demand.

Page last updated on: