Rose Oil Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

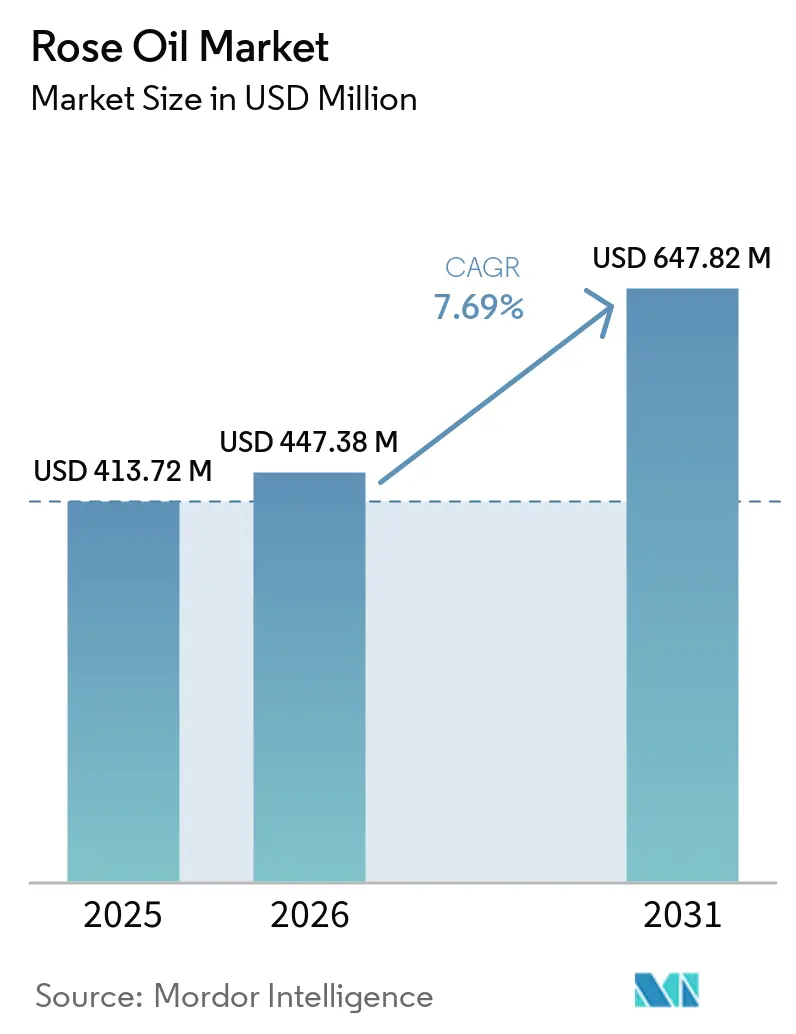

| Market Size (2026) | USD 447.38 Million |

| Market Size (2031) | USD 647.82 Million |

| Growth Rate (2026 - 2031) | 7.69% CAGR |

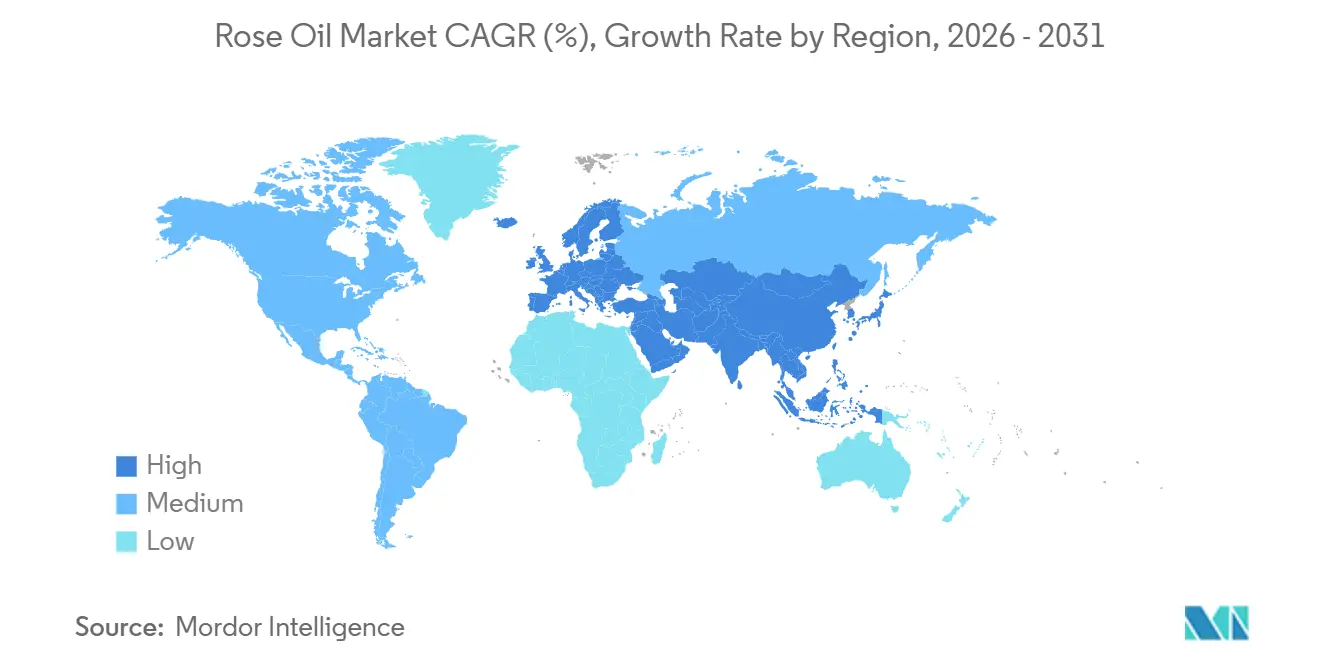

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

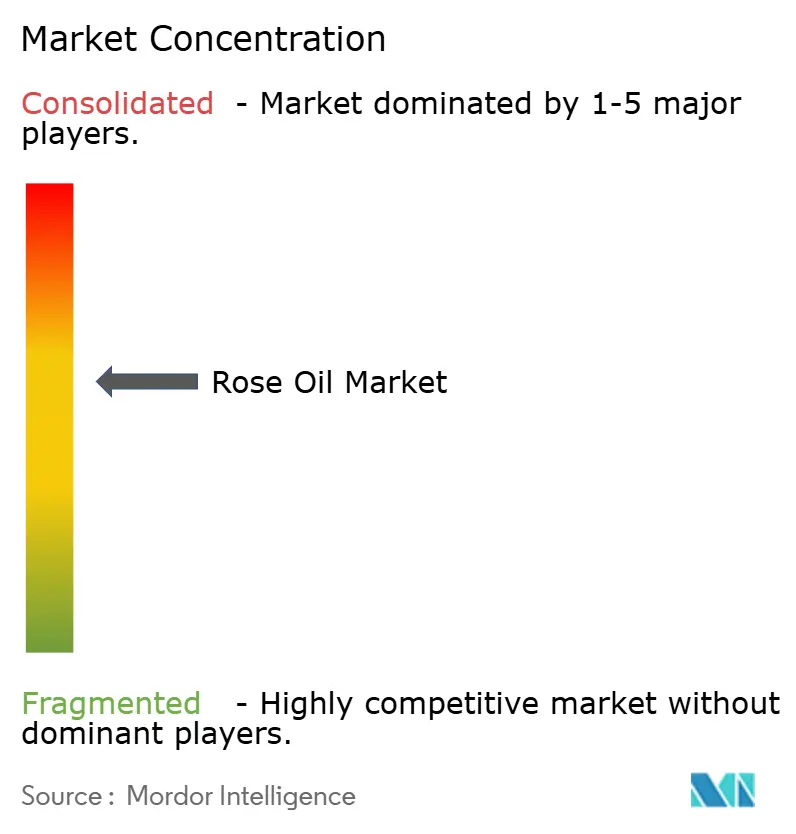

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Rose Oil Market Analysis by Mordor Intelligence

The rose oil market size is projected to expand from USD 413.7 million in 2025 and USD 447.4 million in 2026 to USD 647.8 million by 2031, registering a CAGR of 7.7% between 2026 and 2031. The rising demand for rose oil can be attributed to fragrance, skincare, and wellness brands increasingly opting for verified botanical ingredients over synthetic ones. This trend is particularly pronounced in premium formulations, where consumers are willing to pay a premium for authenticated inputs from Rosa damascena and Rosa centifolia, often highlighting origin stories in their product positioning. The dynamics of the rose oil market are also influenced by a constrained supply in Bulgaria and Turkey. Here, weaker harvests in 2025 heightened supply risks, prompting buyers to forge long-term sourcing relationships. In response, major fragrance houses are channeling investments into cultivation, processing, and traceability. This strategy not only secures access to authenticated raw materials but also amplifies their competitive edge beyond mere buying scale. Concerns over adulteration have further narrowed procurement channels, favoring suppliers who meet stringent quality verification standards. This focus on quality has led to elevated premiums for compliant producers throughout the rose oil market.

Key Report Takeaways

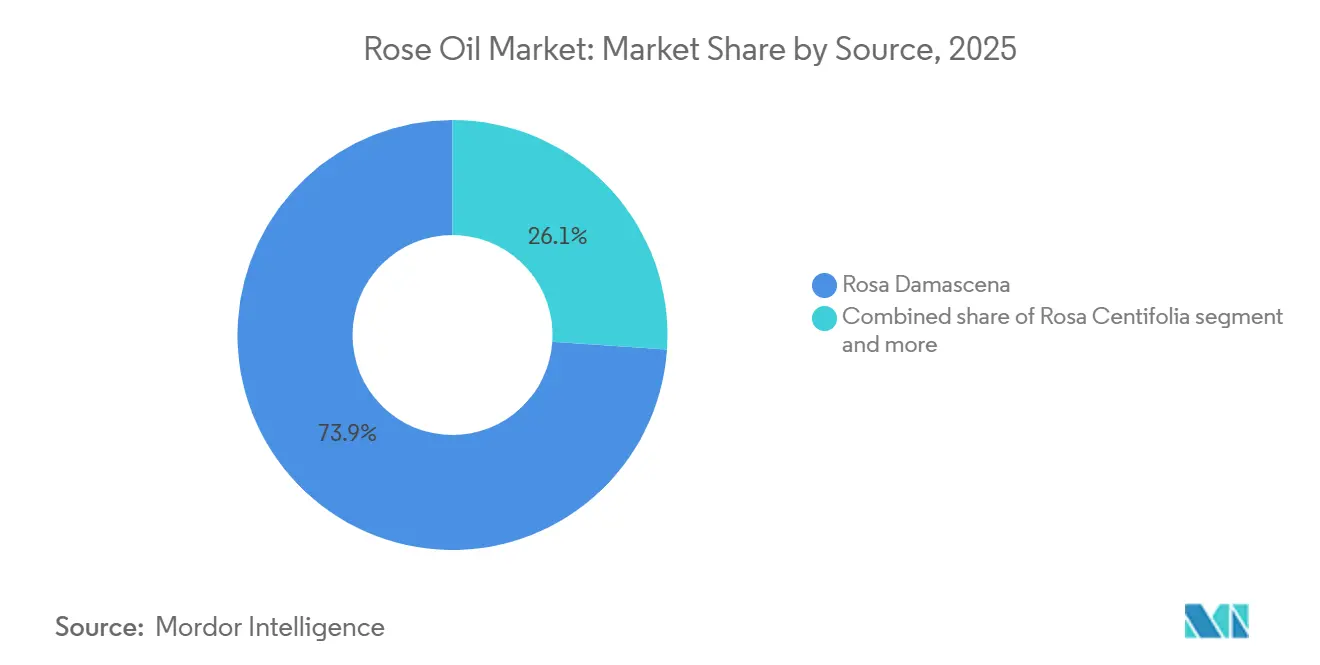

- By source, Rosa Damascena accounted for the largest share of the rose oil market, at 73.9% in 2025, while Rosa Centifolia is projected to grow at the fastest CAGR of 8.3% during 2026-2031.

- By nature, conventional products retained 83.6% share of the rose oil market in 2025, whereas organic products are forecast to expand at a 9.1% CAGR through 2031.

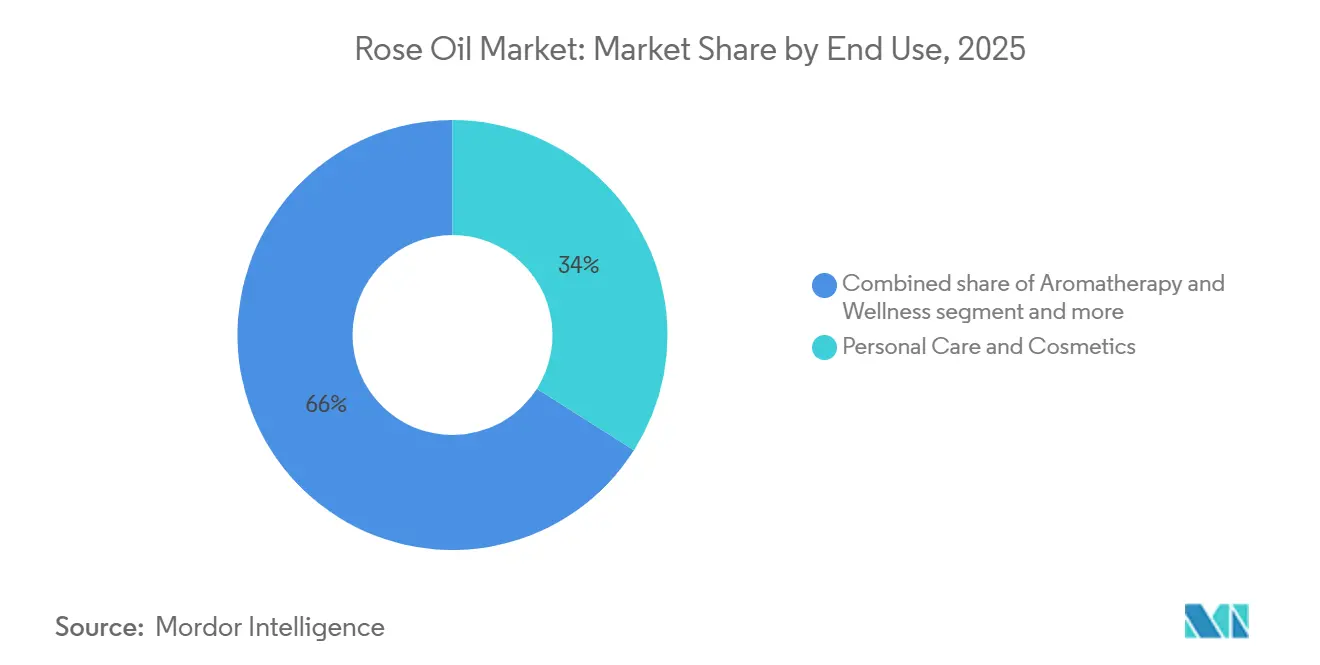

- By end use, personal care and cosmetics accounted for the largest share of the rose oil market, at 34.0% in 2025, while aromatherapy and wellness is projected to grow at the fastest CAGR of 8.7% during 2026-2031.

- By geography, Europe accounted for the largest share of the rose oil market, at 36.4% in 2025, while Asia-Pacific is projected to grow at the fastest CAGR of 9.0% during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Rose Oil Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Natural and Organic Fragrance Ingredients | +2.1% | Global, with demand concentration in North America and Europe | Medium term (2–4 years) |

| Expansion of Premium Skincare and Niche Perfumery | +1.8% | Europe and North America core; spill-over to the Asia-Pacific and MEA | Medium term (2–4 years) |

| Growth in Aromatherapy and Self-Care Consumption | +1.4% | The Asia-Pacific and North America strongest, growing in all regions | Short term (≤ 2 years) |

| Clean-Label Positioning in Functional Cosmetics and Wellness | +1.1% | Europe and North America, expanding to the Asia-Pacific | Medium term (2–4 years) |

| Yield Optimization Through Advanced Extraction and Fractionation | +0.6% | Europe (Bulgaria, Turkey, France), Asia-Pacific (China) | Long term (≥ 4 years) |

| Traceability and Ethical Sourcing as a Brand Differentiator | +0.4% | Europe (REACH/CSRD compliance), North America, and the Asia-Pacific premium markets | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising demand for natural and organic fragrance ingredients

Fragrance brands are increasingly prioritizing certified botanical ingredients, elevating them from mere lifestyle choices to essential formulation standards. A May 2026 report by Les Echos highlighted a resurgence in the production of Rosa centifolia in the Grasse naturals ecosystem. Once teetering on the brink of extinction at just 59 tonnes in 2011, production has seen a revival, thanks to investments from several major fragrance houses returning to the region. This turnaround signals a strong institutional belief in the sustained demand for natural ingredients. Regulatory factors play a role in this rebound: the EU's REACH registration and the new CSRD reporting mandates are making it almost obligatory for high-end formulations to use source-verified botanical ingredients[1]Source: European Union, “REACH and Corporate Sustainability Reporting Rules,” European Union, europa.eu, which means brands lacking certified natural supply chains risk being sidelined from European luxury procurement. This shift is not just significant; it's reviving Rosa centifolia from the brink of obsolescence to active cultivation.

Expansion of premium skincare and niche perfumery

Globally, premium and niche perfumeries are outpacing mass-market fragrances, driven by high-income consumers' preference for provenance-driven, single-origin formulations. Rose oil, a staple heart note in luxury perfumes, commands a premium. In 2024, certified rose oil prices from Bulgaria, as reported by BCCI Bulgaria, ranged between USD 9,500 and USD 16,050 per kilogram, underscoring buyers' commitment to authenticated origins. Givaudan's strategic move in 2026 to acquire a majority stake in Eurofragance, a fine fragrance house, added approximately CHF 185 million in pro forma annual sales to its portfolio. This underscores the trend of major fragrance groups amplifying their fine fragrance offerings to tap into this lucrative segment. Furthermore, a notable shift in vertical integration is evident: luxury brands and their ingredient suppliers, like Lancôme with its 7-hectare rose production in Grasse and IFF's 2026 experimental field for LMR Naturals, are vying for limited cultivation spaces in traditional heritage-growing zones.

Growth in aromatherapy and self-care consumption

According to the World Health Organization, more than 40% of adults in developed nations are turning to complementary therapies, with aromatherapy leading the pack[2]Source: World Health Organization, “Traditional, Complementary and Integrative Medicine,” World Health Organization, who.int. Rose essential oil uniquely marries therapeutic benefits with a touch of luxury, a rare combination in the realm of raw materials. This unique positioning is fueling the rise of rose oil in professional spas, home diffusion products, and wellness brands, all of which have emerged in just the last five years. A key growth trend often overlooked is the shift from synthetic-based aromatherapy to certified natural oils. Spa and wellness procurement managers are elevating their standards, leading to a surge in demand for both food-grade and therapeutically standardized rose oil. Highlighting this industry's shift, Robertet is set to launch AQ3Rose CROP-G in 2025, a biotech ingredient sourced from Rosa chinensis, underscoring a move towards functional alternatives that cater to budget-conscious aromatherapy volumes without sacrificing sensory quality.

Clean-label positioning in functional cosmetics and wellness

Clean-label formulations are expanding beyond the food industry. The EU's evolving Cosmetics Regulation framework, coupled with NATRUE certification standards, is spearheading systematic reformulations in skincare. This is especially evident in anti-aging and brightening product lines, where the benefits of rose oil, known for its antioxidant and skin-conditioning properties, are now clinically validated. A 2025 study published in MDPI highlighted the high bioactivity and anti-aging potential of Rosa damascena petal extract. This not only underscores the scientific backing of rose-derived actives but also reaffirms their established sensory appeal. In January 2024, Bulgarian Rose Karlovo achieved EU organic certification for its entire product lineup. This milestone underscores a pivotal shift: brand-level certification is now the gold standard for premium formulation buyers, overshadowing traditional ingredient-level claims. The strategic takeaway? Conventional rose oil producers lacking third-party certifications may see their profit margins shrink. This is especially true as European mass-prestige cosmetics increasingly demand organic or NATRUE-certified inputs in their procurement specifications.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Petal-to-Oil Conversion Requirements | -1.8% | Global supply-side; most acute in Bulgaria and Turkey | Long term (≥ 4 years) |

| Harvest Seasonality and Weather Sensitivity | -1.4% | Europe (Bulgaria), Turkey (Isparta), MEA (Morocco) | Short term (≤ 2 years) |

| Adulteration Risk and Quality Verification Costs | -0.8% | Global; concentrated in Europe, North America, and the Asia-Pacific importing regions | Medium term (2–4 years) |

| Small Cultivation Footprint and Supplier Concentration | -0.5% | Bulgaria, Turkey, and Morocco are all highly concentrated production zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High petal-to-oil conversion requirements

To produce just 1 kilogram of rose otto, steam distillation of Rosa damascena demands around 3 to 5 tonnes of freshly harvested petals. This ratio remains largely unchanged, irrespective of agricultural inputs or processing efficiency. Such a structural trait limits supply elasticity, rendering rose oil particularly susceptible to demand spikes and subsequent price hikes. While peer-reviewed research is validating advanced extraction methods like supercritical CO2, ultrasound-enhanced polyol techniques, and natural deep eutectic solvents, their widespread commercial adoption is hindered by high capital costs and the necessity for immediate processing of freshly harvested petals. This scenario suggests that yield optimization benefits will predominantly favor well-capitalized producers with state-of-the-art distillery setups, potentially exacerbating the divide between artisan smallholders and larger industrial producers in the foreseeable future.

Harvest seasonality and weather sensitivity

Every spring, oil-bearing roses have a narrow harvest window of just 4–6 weeks. This window is limited to a specific geographic area where the right combination of soil, climate, and variety enhances the concentration of aromatic compounds. Such a tight timeframe poses significant risks: unfavorable weather during this short period can wipe out an entire region's annual supply. The 2025 harvest in Bulgaria highlighted this fragility. A record cold snap in May, coupled with an April frost and hail during the picking season, slashed the output to 6,607 tonnes, a stark drop from the previous year's over 10,000 tonnes. Field yields were also estimated to be 20–30% lower than in 2024. Meanwhile, Turkey's Isparta region faced a 30–35% yield decline due to agricultural frost, as reported by Gülbirlik's General Director in a 2025 press statement. When both Bulgaria and Turkey, the two primary producing nations, suffer simultaneously, as they did in 2025, spot price fluctuations intensify. Buyers then confront an 18–24-month delay before the supply stabilizes, a consequence of the perennial crop's production cycle.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Rosa Damascena Dominance Masks a Shifting Supply Mix

In 2025, Rosa Damascena dominated the rose oil market, capturing a notable 73.91% share. This stronghold is attributed to its prominent role in fine fragrances and luxury skincare, bolstered by a robust infrastructure spanning Bulgaria's Plovdiv, Stara Zagora, and Pazardzhik regions, as well as Turkey's Isparta province. The species' leadership is anchored in its established chromatographic profile. Notably, as per ISO 9842:2024 standards, citronellol and geraniol, which fragrance houses prioritize for formulation consistency, typically constitute 60–75% of its composition[3]Source: International Organization for Standardization, “ISO 9842:2024 Oil of Rose,” ISO, iso.org. In 2024, Bulgaria boasted 73 rose processors and 53 distilleries, collectively exceeding an annual capacity of 15,000 tonnes. Concurrently, Turkey's Isparta region, as reported by Gülbirlik, Turkey's national rose and rose oil cooperative, was responsible for roughly 65% of the global rose oil output. While this concentrated infrastructure in Bulgaria and Turkey curtails supply flexibility, it simultaneously bestows Bulgarian-origin roses with Protected Geographical Indication (PGI) premiums, establishing price floors that rival regions can't match.

Rosa Centifolia is emerging as the fastest-growing segment, projected to grow at an 8.26% CAGR from 2026 to 2031. This surge is fueled by a revival of centifolia cultivation in Grasse, catering to niche and luxury perfumery markets. Meanwhile, Rosa Gallica, traditionally favored for rose absolute in French perfumery, carves out a niche segment, buoyed by its heritage appeal and demand from EU artisan fragrance makers. Other rose species are seeing traction from budding producers in Morocco, Iran, India, and China. Notably, Morocco's Kelaa M'Gouna region is steadily making its mark in the mid-market formulation arena. However, it's essential to note that Rosa Centifolia's resurgence isn't solely a commercial endeavor. It's being bolstered by substantial investments from major fragrance houses in Grasse's agricultural infrastructure, underscoring a strategy centered on supply security over mere economic gains.

By Nature: Organic Sub-Segment Pulls Ahead on Certification Momentum

In 2025, the Conventional segment dominated the rose oil market, accounting for 83.62% of the market share. This trend underscores the historical prevalence of steam-distilled production in Bulgaria and Turkey, regions where certified organic protocols have yet to be consistently implemented. Yet, the Organic sub-segment is on the rise, boasting a CAGR of 9.11% for the period of 2026–2031, marking it as the fastest-growing segment. This surge is largely fueled by heightened certification demands from EU cosmetics buyers, direct-to-consumer wellness brands, and manufacturers of aromatherapy products. Alteya Organics, situated in Bulgaria's Rose Valley and boasting certifications from USDA, NATRUE, and EU Organic, exemplifies the type of producer reaping the rewards. With buyers increasingly seeking third-party verified organic status, authenticated by Bulgaria's Government-appointed Research Institute for Roses, Aromatic, and Medicinal Plants, Alteya's credentials grant it a distinct edge in securing premium brand contracts. Further illustrating this trend, Bulgarian Rose Karlovo clinched its EU organic certification for its entire product lineup in January 2024. This move underscores a brand-level certification strategy, one that mid-tier Bulgarian producers are adopting to bolster their market position against rising competition from Turkey and Morocco.

In today's market, the organic premium transcends mere marketing allure; it's evolving into a non-negotiable procurement criterion across various high-value sectors. European regulations on clean-label cosmetics, in tandem with NATRUE's multi-tiered certification standards, are progressively refining the pool of suppliers eligible for elite formulation contracts. Producers entrenched in conventional methods, without a roadmap to transition to organic or secure third-party certifications, risk being relegated to commodity-grade applications. These include food flavoring, household products, and budget-friendly aromatherapy blends, arenas where pricing leverage is notably diminished. Moreover, transitioning to organic not only aligns producers with EU organic cosmetics regulations but also amplifies their growth potential, given the regulatory weight behind the burgeoning organic segment.

By End Use: Personal Care Leads, Aromatherapy Disrupts

By 2025, the Personal Care and Cosmetics sector commanded a 34.01% share of the rose oil market, leveraging rose oil's dual role as both a sensory and active ingredient in high-end serums, facial oils, and toners. Backed by 2025 MDPI research, rose oil's properties, ranging from antioxidant activity to skin-barrier conditioning and anti-aging effects, empower brands to market it as both a potent active and a clean-label fragrance, capitalizing on its functional and sensory appeal. Fine Fragrances and Perfumery, with rosa damascena as the quintessential heart note, continues to hold a pivotal share. This segment reaps benefits from the global expansion of niche perfumery channels, especially among affluent consumers in Europe and the Asia-Pacific. Meanwhile, the Pharmaceuticals and Food and Beverage sectors enjoy stable, albeit niche, demand, be it in MEA's rose-water culinary traditions or in wellness-focused aromatherapy pharmaceuticals. Household Products see modest growth, driven by a premium natural-fragrance positioning in home care lines.

Aromatherapy and Wellness is emerging as the fastest-growing segment, boasting an 8.73% CAGR for 2026–2031. This surge is propelled by heightened mental health awareness, a growing embrace of holistic wellness, and the premiumization of therapeutic home products. Notably, the WHO highlights that over 40% of adults in developed nations have adopted complementary therapies, underscoring a demand that transcends fleeting consumer trends. A key distinction in this segment's growth is the increasing sophistication of buyers. They're opting for GCMS-verified, therapeutic-grade oils over commodity-grade ones, driving up average selling prices and positioning this segment as the most lucrative growth avenue for discerning producers.

Geography Analysis

In 2025, Europe commanded a dominant 36.4% share of the rose oil market, solidifying its status as the leading regional contributor by value. This prominence is attributed to the region's robust supply infrastructure, its historic perfumery roots, and stringent regulations governing natural cosmetic ingredients. Key markets like France, Germany, and the UK, home to major fragrance houses and a premium beauty demand, play a pivotal role. The significance of Grasse, with its intertwined cultivation, extraction, and fragrance development, underscores the region's investment returns. Initiatives like Givaudan’s Campus 52 naturals project and IFF’s 2026 experimental field highlight Europe's strategy: fortifying its foothold in the rose oil market by directly managing natural ingredient ecosystems, moving beyond mere procurement.

Asia-Pacific is emerging as the fastest-growing region in the rose oil market, projected to grow at a robust 9.0% CAGR from 2026 to 2031. Countries like China, South Korea, Japan, and India are witnessing a surge in demand, driven by rising disposable incomes and an increasing appetite for premium beauty, natural wellness, and traceable fragrance ingredients. China plays a dual role in the trade landscape: it's not only an emerging producer, delving into research-led extraction, but also a significant importer of Bulgarian and Turkish rose oil, catering to its premium market. Meanwhile, Japan and South Korea prioritize certified-origin oils, and India benefits from its expanding domestic personal care sector and a rich tradition in rose processing.

While South America remains a smaller player in the rose oil market, countries like Brazil, Colombia, and Argentina are increasingly gravitating towards natural fragrance ingredients for their domestic personal care production. The Middle East and Africa witness consistent demand, especially from the UAE, Saudi Arabia, Egypt, Morocco, and Turkey, where the cultural significance of rose-based perfumery and cosmetics runs deep. Morocco, with its established Rosa damascena production in Kelaa M’Gouna, plays a dual role as both a supplier and consumer. Turkey is particularly noteworthy, boasting a blend of robust domestic demand and significant production capabilities, with Gülbirlik highlighting that the Isparta region alone accounts for nearly 65% of the global rose oil output.

Competitive Landscape

While the rose oil market starts off fragmented at the cultivation stage, it quickly consolidates as the material transitions into processing, trading, blending, and formulation. In 2024, Bulgaria boasted 2,989 rose growers, a scenario mirrored by smallholder structures in Turkey, Morocco, and other producing nations. Despite this extensive base of growers, major fragrance players like Givaudan, DSM-Firmenich, IFF, Robertet, and Symrise wield significant influence over downstream demand. They do this by managing sourcing relationships, setting technical standards, and ensuring customer access in the realms of fine fragrance and prestige cosmetics. Consequently, while many producers engage in the supply chain, only a select few dictate the qualification, blending, and sale of the most valuable volumes. This dynamic results in a rose oil market characterized by widespread raw material production but a concentrated capture of premium value.

Recent strategic maneuvers highlight major players' shift towards securing supply over merely competing on price. In May 2026, IFF launched a new experimental field for LMR Naturals in Grasse, emphasizing the direct cultivation of key perfumery species, including rose. Givaudan's unveiling of Campus 52 in Grasse, a center for natural fragrances, will process over 100 ingredients, notably Rose de Mai, bolstering its dominance in natural development and sourcing. Similarly, Symrise's collaboration with Groupe Neroli in Grasse underscores the value of cultivation partnerships, enhancing access to certified-origin supplies.

Robertet is pivoting through innovation, as evidenced by its AQ3Rose CROP-G partnership, signaling a keen interest in rose-derived biotech ingredients. These ingredients are particularly sought after in applications where natural supplies are either costly or scarce. Concurrently, the introduction of ISO 9842:2024 and broader authentication mandates is escalating operational costs for those lacking robust quality systems, thereby sidelining marginal suppliers. Concerns over adulteration further amplify the advantage for companies offering stringent testing and traceability, especially when catering to premium clientele in Europe, North America, and Asia-Pacific. Thus, while the rose oil market remains accessible to smaller producers, the most advantageous positions are increasingly occupied by suppliers and fragrance houses adept at blending provenance, certification, and long-term sourcing strategies.

Rose Oil Industry Leaders

Givaudan SA

Firmenich International SA

Symrise AG

International Flavors & Fragrances Inc.

Robertet SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: LMR by IFF inaugurated a new experimental field in Grasse, France, preserving the cultivation of iconic perfumery species, including rose alongside jasmine, tuberose, and iris. The facility was acquired from farmer Constant Viale and combines organic farming practices with biodiversity initiatives, positioning IFF-LMR to secure Grasse-origin rose and other naturals for premium fragrance formulations.

- April 2026: Givaudan acquired a majority stake in Eurofragance, a Barcelona-based fine fragrance house representing approximately CHF 185 million in proforma incremental annual sales. The deal, subject to regulatory processes, strengthens Givaudan's fine fragrance footprint in high-growth regional markets and is part of its 2030 strategy to expand local and regional customer reach.

- February 2026: Givaudan announced a CHF 55 million (EUR 60.3 million) investment in Campus 52, a new centre of excellence for natural fragrance ingredients in Grasse, scheduled to open in Q1 2028. The facility will consolidate agronomy, innovation, operations, and perfumery under one site and will process more than 100 natural ingredients, including Rose de Mai and jasmine.

Global Rose Oil Market Report Scope

Rose oil is the volatile essential oil extracted from the fresh petals of various rose species. The Rose oil Market is segmented by source, nature, end use, and geography. By source, the market is segmented into Rosa damascena, Rosa centifolia, Rosa gallica, and other rose species. By nature, the market is segmented into conventional and organic. By end use, the market is segmented into personal care and cosmetics, fine fragrances and perfumery, aromatherapy and wellness, food and beverage, pharmaceuticals, household products, and other end uses. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The Market Forecasts are Provided in Terms of Value (USD).

| Rosa Damascena |

| Rosa Centifolia |

| Rosa Gallica |

| Other Rose Species |

| Conventional |

| Organic |

| Personal Care and Cosmetics |

| Fine Fragrances and Perfumery |

| Aromatherapy and Wellness |

| Food and Beverage |

| Pharmaceuticals |

| Household Products |

| Other End Uses |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Peru | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| Source | Rosa Damascena | |

| Rosa Centifolia | ||

| Rosa Gallica | ||

| Other Rose Species | ||

| Nature | Conventional | |

| Organic | ||

| End Use | Personal Care and Cosmetics | |

| Fine Fragrances and Perfumery | ||

| Aromatherapy and Wellness | ||

| Food and Beverage | ||

| Pharmaceuticals | ||

| Household Products | ||

| Other End Uses | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Peru | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the rose oil business and how fast is it growing?

The rose oil market stood at USD 447.4 million in 2026 and is forecast to reach USD 647.8 million by 2031 at a 7.7% CAGR.

Which source segment leads global demand for rose oil?

Rosa Damascena led the source mix with 73.9% share in 2025 because it has the strongest perfumery profile and the deepest production base in Bulgaria and Turkey.

Why is organic rose oil gaining attention faster than conventional supply?

Organic is projected to grow at a 9.1% CAGR through 2031 because buyers in cosmetics, wellness, and aromatherapy increasingly want third-party certification and traceable origin.

Which end-use category generates the most revenue for rose oil suppliers?

Personal Care and Cosmetics held 34.0% of demand in 2025, supported by rose oil’s role in skincare, facial oils, toners, and premium beauty formulations.

Page last updated on: