Ginger Oil Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

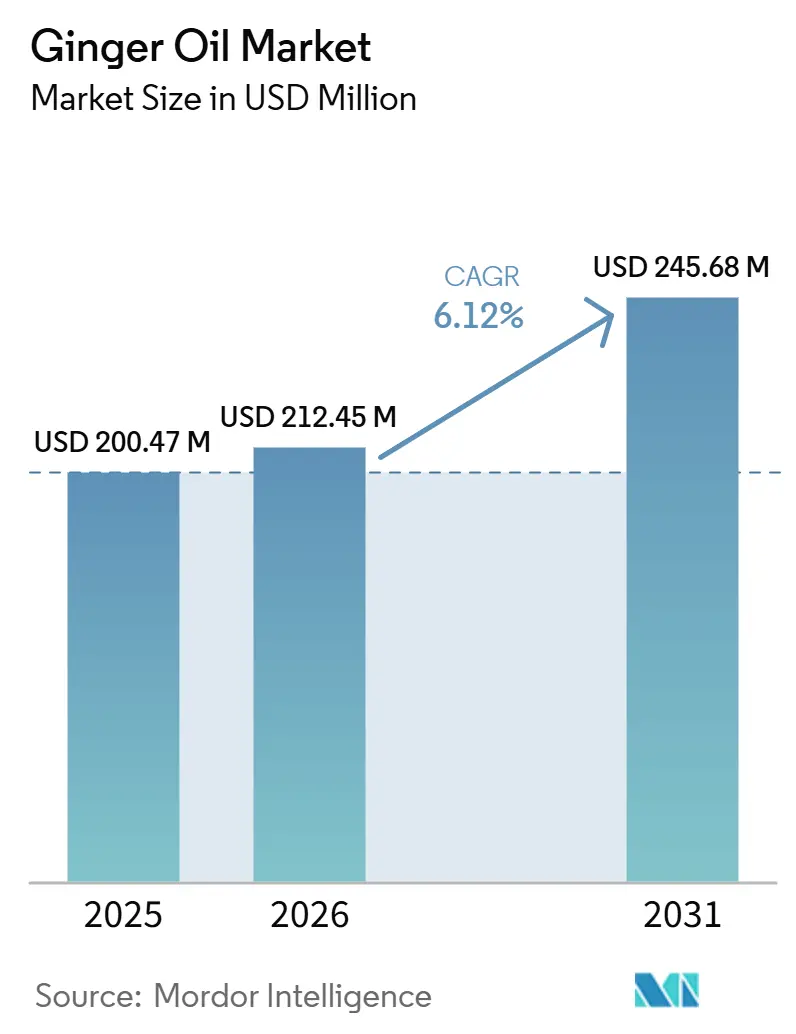

| Market Size (2026) | USD 212.45 Million |

| Market Size (2031) | USD 245.68 Million |

| Growth Rate (2026 - 2031) | 6.12% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ginger Oil Market Analysis by Mordor Intelligence

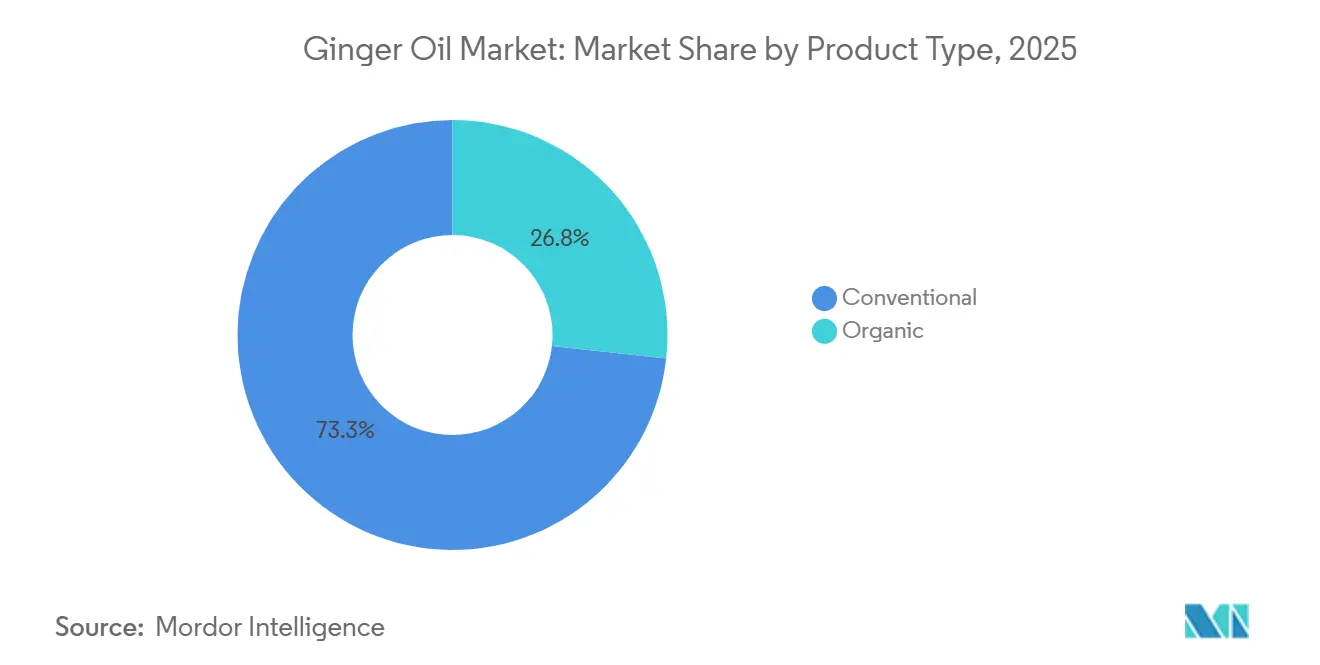

The Ginger oil market size is expected to increase from USD 200.47 million in 2025 to USD 212.45 million in 2026 and reach USD 245.68 million by 2031, growing at a CAGR of 6.12% over 2026-2031. Robust demand for natural flavoring agents in food and beverages, the accelerating shift toward aromatherapy-based wellness routines, and regulatory pressure that favors botanical ingredients underpin this steady expansion. Conventional grades still dominate with 73.25% of 2025 volume, yet certified-organic variants are advancing faster at a 6.59% CAGR, an early signal that traceable premium supply will command future pricing power. Raw-material dynamics remain pivotal: India’s 12% production dip in 2025 coincided with China’s 67.1% export surge, widening the quality gap between high-grade and commodity roots and reshaping procurement strategies for food, pharmaceutical, and cosmetics processors

Key Report Takeaways

- By product type, conventional oil retained 73.25% of the Ginger oil market share in 2025, while organic oil recorded the fastest projected CAGR at 6.59% through 2031.

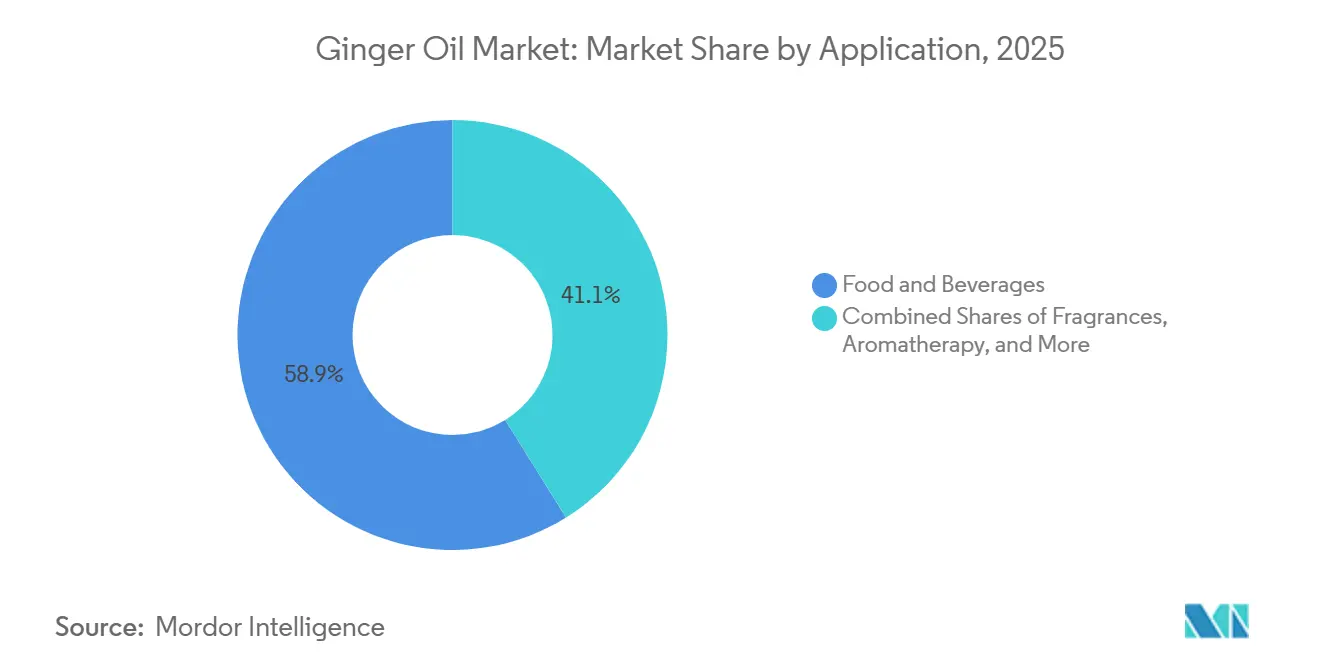

- By application, food & beverages led with 58.85% revenue share in 2025; aromatherapy is forecast to expand at a 7.25% CAGR to 2031.

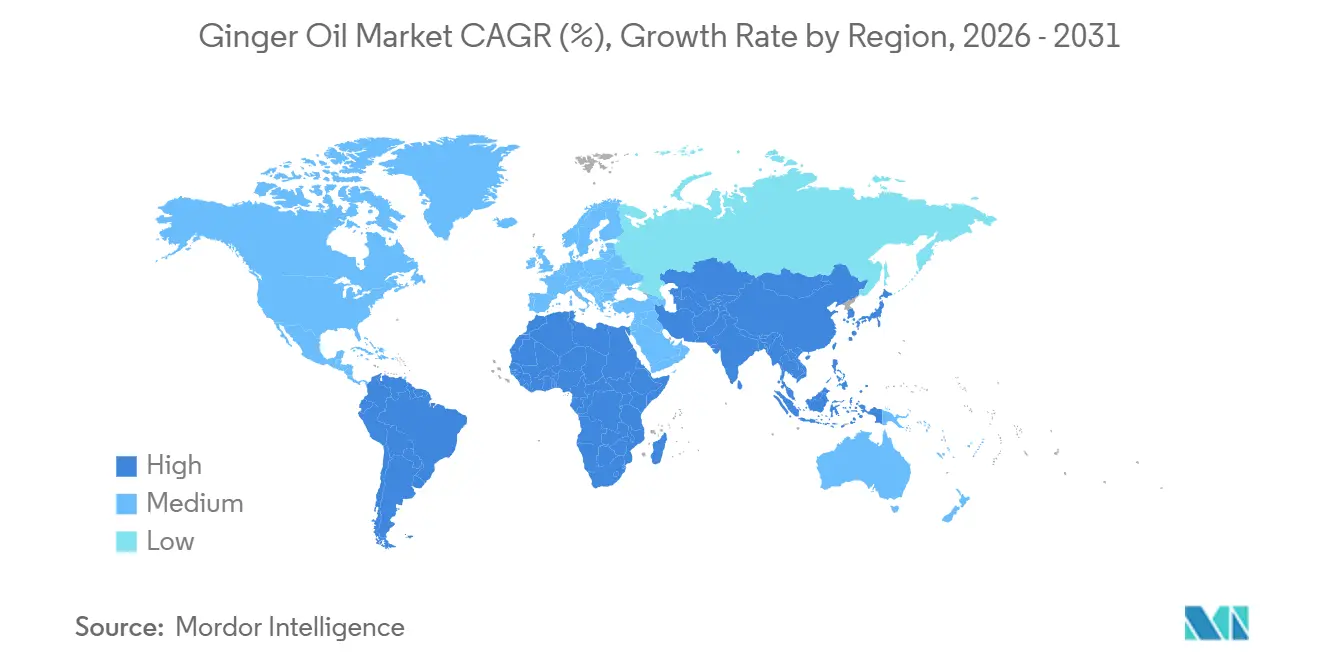

- By geography, Asia-Pacific accounted for 45.65% of the 2025 value; the Middle East & Africa region is expected to post the quickest 7.81% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Ginger Oil Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand For Natural Flavoring Agents In Food And Beverages | +1.2% | Global, with concentration in North America and Europe | Medium term (2–4 years) |

| Increasing Popularity Of Aromatherapy And Wellness Products | +1.0% | North America, Europe, Middle East & Africa | Short term (≤ 2 years) |

| Regulatory Shift Away From Synthetic Additives | +0.8% | Europe, North America | Long term (≥ 4 years) |

| Advanced Extraction Technologies Enhancing Yield And Quality | +0.7% | Asia-Pacific (India, China), Europe | Medium term (2–4 years) |

| Expansion Of Functional Beverages Infused With Ginger Oil | +0.6% | North America, Asia-Pacific | Short term (≤ 2 years) |

| Blockchain-Enabled Farm-To-Oil Traceability Systems | +0.3% | Global, early adoption in Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand For Natural Flavoring Agents In Food And Beverages

Clean-label reformulation mandates are driving food and beverage manufacturers to adopt natural flavoring agents, with ginger oil emerging as a GRAS-listed (Generally Recognized as Safe) ingredient under FDA 21 C.F.R. 101.22. It aligns with both regulatory requirements and consumer expectations for transparency[1]Source: United States Food & Drug Administration, “21 C.F.R. §101.22,” fda.gov. The FDA permits ginger oil produced through steam distillation, organic ethanol extraction, or supercritical CO2 to be classified as a "natural flavor," provided no prohibited synthetic solvents are used. This allows formulators to replace artificial ginger flavors without triggering allergen disclosures or additional labeling requirements. Stoli Group's March 2026 relaunch of Stoli Ginger Beer highlights this trend. The reformulated recipe features natural ginger, chili, and lemon juice, targeting millennials and Gen Z consumers aged 25–40. The brand plans to expand distribution across Southern Europe and China, aiming for a threefold increase in volume, with a focus on on-premise and urban retail channels. Flavor houses report that ginger's "fiery warmth and zesty brightness," derived from gingerol, pairs well with adaptogens (ashwagandha, rhodiola), nootropics, and exotic citrus fruits (yuzu, calamansi) in functional recovery drinks and electrolyte beverages. This compatibility is driving innovation and repeat purchases. Consequently, demand for ginger oil continues to grow as beverage and snack manufacturers seek to differentiate their products with botanical authenticity and complex sensory profiles.

Increasing Popularity Of Aromatherapy And Wellness Products

Aromatherapy's increasing adoption is driving ginger oil consumption beyond its traditional use in spas and clinics, extending into home diffusers, wellness shots, and personal-care products. Brands are leveraging ginger oil's proven anti-inflammatory and antioxidant properties. Peer-reviewed studies demonstrate that 6-gingerol, a key compound in ginger, mitigates endothelial injury by activating Nrf2 and regulating the p38 MAPK–NF-κB signaling pathway. This scientific evidence supports brands' efficacy claims for both topical and inhalation applications. In March 2025, Symrise launched 'SymRelief green', a patented formulation combining biotech-derived bisabolol and organic ginger root extract at a recommended concentration of 0.1%. With clinical validation and certification of 100% Natural Origin Content per ISO 16128, this product targets the sensitive-skin and anti-inflammaging markets. It positions ginger as a cost-effective, multifunctional ingredient for brands focusing on natural, sustainable, and vegan-compliant solutions. The combination of wellness trends, clinical validation, and formulation versatility is driving ginger oil's growth in high-margin personal-care and aromatherapy markets, where it commands premium pricing compared to its traditional role in food flavoring.

Regulatory Shift Away From Synthetic Additives

Regulatory frameworks in Europe and North America are tightening restrictions on synthetic additives, boosting demand for natural essential oils like ginger. From January 2026, the European Commission will require batch-level GC-MS reporting for high-value oils, explicit labeling for synthetic or nature-identical chemicals, and stricter oversight of unsupported health claims. Suppliers must maintain GC-MS and Certificate of Analysis records, secure written purity guarantees in supply chains, and revise marketing claims. These changes benefit vertically integrated producers with in-house labs while disadvantaging brokers lacking traceability. In cosmetics, EU Regulation (EC) No 1223/2009 mandates labeling of fragrance allergens, such as limonene, linalool, geraniol, and eugenol (naturally found in ginger oil), if concentrations exceed 0.001% in leave-on or 0.01% in rinse-off products[2]Source: Oils Live, “EU Regulations for Essential Oil Purity (2026 Update),” oils.live. Heavy metals are also regulated, with limits for lead (<10 mg/kg), arsenic (<2 mg/kg), and cadmium (<5 mg/kg), alongside mandatory safety assessments in Product Information Files, as noted by Allan Chemical Corporation. These regulations are driving a shift from synthetic fragrances to natural oils, which align with consumer preferences for botanical ingredients and meet regulatory definitions of "natural." While compliance costs and supply-chain challenges may impact non-certified suppliers, demand for ginger oil in regulated markets is expected to grow steadily.

Advanced Extraction Technologies Enhancing Yield And Quality

Supercritical CO2 extraction is raising quality standards and reshaping margins in the ginger oil market, though high capital costs limit its adoption. A 2025 study on Peruvian ginger showed that supercritical CO2 at 50°C and 250 bar, with an 8 ft³/h flow rate over 360 minutes, produced oleoresin with 25.99 mg/g dry basis, 171.65 mg gallic acid equivalents per gram, and 254.71 mg/g 6-gingerol content, far exceeding Soxhlet hexane extraction. It also preserved antioxidant capacity (IC50 = 1.02 mg/mL) and maintained polyphenol stability for 180 days at 0°C, 20°C, and 40°C. Another 2025 study comparing steam distillation, ultrasound-assisted steam distillation, enzymatic hydrolysis, and ultrasound-enzyme synergistic assisted steam distillation (UEASD) found UEASD increased essential oil yield and achieved a composition of 48.16% terpenes, 13.16% ketones, and 2.63% aldehydes. Its antioxidant IC50 values (1.84 mg/mL for ABTS, 1.20 mg/mL for DPPH) surpassed vitamin E. These innovations allow processors to charge premiums for high-purity, solvent-free extracts targeting pharmaceutical and nutraceutical markets. However, commercial-scale supercritical CO2 systems, costing over USD 500,000, and the expertise needed for parameter optimization (pressure, temperature, flow rate, fractionation timing) create a divide. Large processors capture quality premiums, while smaller distillers remain confined to lower-margin steam-distilled grades.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility In Raw Ginger Prices And Seasonal Supply Challenges | -1.2% | Global, acute in India and China | Short term (≤ 2 years) |

| High Rejection Rates Due To ISO/AFNOR Purity Standards | -0.8% | Europe, North America | Medium term (2–4 years) |

| Insufficient Capacity For Certified Organic Ginger Oil | -0.6% | Global, most acute in Asia-Pacific and South America | Long term (≥ 4 years) |

| Inconsistent Quality Among Smallholder Processors | -0.5% | Asia-Pacific, Africa, South America | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Volatility In Raw Ginger Prices And Seasonal Supply Challenges

In 2025–2026, raw ginger prices showed significant contrasts. Indian domestic prices for premium washed ginger rose over 15% in October 2025 to INR 4.5–4.7 per kilogram (around USD 0.054–0.056 per kg) due to rainfall-induced harvest delays in Shandong and Henan provinces and a 15% year-on-year drop in old-ginger stocks. Meanwhile, China's export unit prices fell to a 34-month low of CNY 7,548 per tonne (about USD 1,040 per tons) in September 2025. This divergence reflects structural imbalances. India's ginger production dropped by 12% to around 2 million tonnes in 2025–2026 due to reduced acreage, while China's planting area hit a five-year high, with 2025 acreage expected to grow 10–20%, potentially exceeding 433,000 hectares and risking a medium-term oversupply of lower-grade fresh ginger. Erratic monsoons in Kerala and Karnataka caused waterlogging and bacterial wilt outbreaks, while unseasonal frosts in Peru's high-altitude regions reduced organic ginger yields by 30–35%, tightening premium organic supply. For ginger oil processors, price volatility led to margin pressures during cost spikes and inventory losses during price drops. Many are adopting medium-term contracts or vertical integration into cultivation, but these require capital and expertise that small and mid-sized processors often lack.

High Rejection Rates Due To ISO/AFNOR Purity Standards

Stricter purity standards are increasing batch rejection rates, particularly for processors lacking advanced analytical tools. European buyers now require detailed GC-MS profiles to meet ISO and AFNOR chromatographic standards, along with heavy-metal certifications per European Pharmacopoeia limits: lead <5 ppm, cadmium <1 ppm, and mercury <0.1 ppm. A 2025 study on essential-oil standardization for pest management highlighted that retention indices must stay within ±5 units of literature values. Marker compounds like 1,8-cineole and linalool must meet ICH Q2(R1) criteria: linearity R² >0.995, recovery 95–105%, and repeatability RSD <2.5%. Untargeted fingerprints require cosine-similarity thresholds and PCA/PLS-DA chemometric validation, as noted in the International Journal of Herbal Medicine. For ginger oil, this involves quantifying 6-gingerol, 8-gingerol, and α-zingiberene, with batch consistency verified via multivariate analysis. Meeting these standards requires GC-FID and GC-MS systems costing USD 50,000–150,000 and skilled personnel. Smallholder processors in India, Nigeria, and Indonesia often lack these resources, leading to rejection rates of 20–30% when exporting to Europe. Rejected batches are sold at steep discounts in less-regulated markets or reformulated as lower-grade oleoresins, reducing profitability and discouraging quality investments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Organic Certification Bottlenecks Constrain Premium Supply

In 2025, conventional ginger oil led the market with a 73.25% share, driven by its cost-effectiveness and availability in food flavoring, fragrance compounding, and industrial applications. Organic ginger oil, though holding a smaller share, is projected to grow at a 6.59% CAGR through 2031, fueled by demand from certified-organic food, cosmetics brands, and premium aromatherapy channels. The USDA's Strengthening Organic Enforcement rule, effective March 2024, expands certification requirements to brokers, traders, importers, repackers, and private-labelers. This has caused a surge in applications, stretching certifier capacities to 90–120 days or more, with some certifiers pausing new intakes. For ginger oil supply chains, processors must now ensure extraction solvents (steam distillation, organic ethanol, or supercritical CO2) comply with the National List of Allowed and Prohibited Substances, maintain traceability from certified organic farms, and undergo annual inspections. These requirements favor vertically integrated operations over smaller aggregators.

Organic ginger cultivation faces challenges, including a three-year transition period for land to remain free of prohibited substances, strict composting protocols (25:1–40:1 carbon-to-nitrogen ratio, temperature, and turning requirements), and limited OMRI-listed pest-management inputs, leading to 10–20% lower yields than conventional methods. In 2021, Peru, a leading organic ginger exporter with 54,000 tonnes of production, saw a 30–35% yield drop in 2025 due to unseasonal frosts in high-altitude organic plots. This tightened premium organic ginger supply and raised organic ginger oil prices 25–30% above conventional equivalents. However, these efforts remain insufficient to meet growing demand from certified-organic food, cosmetics, and nutraceutical brands.

By Application: Aromatherapy Surges as Wellness Converges with Clinical Validation

In 2025, the Food & Beverages sector accounted for 58.85% of the market, driven by ginger oil's GRAS-listed status as a natural flavoring agent. It is widely used in soft drinks, baked goods, sauces, and functional beverages, offering a distinctive pungency and complementing citrus, herbal, and adaptogenic ingredients. The Aromatherapy & Wellness sector is the fastest-growing, with a 7.25% CAGR projected through 2031, supported by the rising use of essential-oil diffusers, wellness shots, and clinical evidence of ginger oil's bioactive benefits. A 2026 study demonstrated that 6-gingerol alleviates hyperlipidemia-induced endothelial injury through Erk–Nrf2 antioxidant pathways and p38 MAPK–NF-κB anti-inflammatory signaling, reinforcing its use in aromatherapy and topical treatments for cardiovascular and inflammatory conditions.

The Pharmaceuticals & Nutraceuticals segment, though smaller, is advancing with innovations focused on bioavailability and stability. A 2025 study comparing ginger extract capsules (20 mg, 40 mg, 80 mg) and a liquid formulation (1,000 mg extract per 300 mL) found the liquid matrix achieved 23.44% intestinal bioaccessibility for 6-gingerol, compared to 3.15% for powdered extract. The liquid formulation also delivered higher antioxidant capacity, at 11,336.7 µmol Trolox equivalents per unit versus 66.8 µmol for the 80 mg capsule. These results highlight the potential of aqueous and colloidal delivery systems to enhance absorption and efficacy. This has driven demand for high-purity ginger oil and oleoresin suitable for aqueous formulations without precipitation or phase separation. In Personal Care & Cosmetics, ginger oil's antioxidant and microcirculation-enhancing properties are being utilized in anti-aging serums, scalp treatments, and lip plumping products.

Geography Analysis

In 2025, Asia-Pacific held a 45.65% market share, driven by concentrated production in India and China, which together produce about 8 million tonnes of raw ginger annually. In 2024, China exported 465,000 tonnes of fresh ginger, a 67.1% year-on-year increase. Major destinations included the Netherlands (67,200 tonnes), the United States (58,700 tonnes), and Vietnam. However, export unit prices dropped 24.9% to USD 1,440 per tonne due to oversupply from expanded planting in Shandong and Yunnan provinces. This price decline benefited Chinese ginger oil processors, who accessed low-cost feedstock and met rising domestic demand for ginger powder and essential oil. Premium washed-ginger prices remained at USD 0.60–0.63 per 500 grams in October 2025 despite weak export prices. The region's dominance is further supported by its proximity to end-use markets in Japan, South Korea, and Southeast Asia, where ginger oil is used in traditional medicine, functional foods, and personal-care products. Additionally, major flavor and fragrance facilities, including those of Symrise, Givaudan, and Synthite Industries (India), strengthen the region's position.

North America and Europe together account for 35–40% of global ginger oil consumption, driven by clean-label reformulation in food and beverages, regulatory support for natural ingredients, and premium positioning in aromatherapy and cosmetics. The European Commission's January 2026 essential-oil purity update, requiring batch-level GC-MS reporting and clear labeling of synthetic constituents, is accelerating the shift to natural ginger oil in EU food and cosmetics applications, despite higher compliance costs. In the U.S., the USDA's March 2024 Strengthening Organic Enforcement rule extended certification requirements across the supply chain, tightening organic ginger oil supply and increasing lead times for certified-organic ingredients to 90–120 days or more. Buyers are securing multi-year contracts or vertically integrating into certified organic ginger cultivation in Peru, India, and Nigeria. North American beverage innovation continues, with Stoli Ginger Beer relaunching in March 2026 to emphasize natural ginger and target threefold volume growth, and Abba Ginger Drinks launching Ginger Hibiscus with organic ginger root in February 2025.

The Middle East and Africa is projected to grow fastest at a 7.81% CAGR through 2031, driven by rising demand for halal-certified ingredients, higher disposable incomes in Gulf Cooperation Council markets, and increased use of natural aromatherapy and personal-care products. The global halal economy is expected to reach USD 3.36 trillion by 2028, with halal food, cosmetics, and pharmaceuticals driving demand for certified, traceable ingredients[3]Source: Halal Practitioner, “2026 Halal Market Trends,” halalpractitioner.com. Ginger oil suppliers targeting this region must secure halal certification from recognized bodies like JAKIM or SMIIC-accredited certifiers, implement Halal Assurance Systems covering sourcing, production, and logistics, and provide digital traceability to ensure no cross-contamination with non-halal substances. These requirements favor vertically integrated processors and pose challenges for smaller exporters lacking certification infrastructure. South America, led by Peru's organic ginger production (approximately 54,000 tonnes in 2021), is emerging as a premium organic ginger oil supplier. However, unseasonal frosts in 2025 reduced yields by 30–35%, tightening supply and highlighting the region's vulnerability to climate variability and the need for agronomic risk management.

Competitive Landscape

Multinational corporations dominate the ginger oil market, employing vertical integration and sustainable sourcing to carve out competitive advantages. Giants like Givaudan, Symrise, and International Flavors & Fragrances boast extensive product ranges and global reach. In contrast, niche players such as doTERRA and Young Living emphasize direct sales and premium branding. These industry leaders, through vertical integration—encompassing farms, distilleries, and labs—ensure a steady supply and swift product customization for top-tier food and beverage clients. Givaudan's partnership with Dole, aimed at valorising green-banana byproducts, underscores a commitment to sustainability and circularity.

Mid-tier players like doTERRA and Young Living, focusing on direct sales, weave narratives around purity and therapeutic benefits. Their subscription services cultivate brand loyalty, demanding stringent traceability to align with ISO 17025 standards. The industry's competitive landscape is shaped by technology trends, with firms channeling investments into advanced extraction techniques for superior yields and enhanced properties. Givaudan's alliance with Dole Asia Holdings for upcycled ingredients underscores the industry's pivot towards sustainability and circular economy tenets.

While established players solidify their market stance, fresh innovations emerge, with regulatory adherence becoming pivotal for premium segments. The competitive arena buzzes with product unveilings, partnerships, capacity boosts, and strategic buyouts. Companies are not only pouring resources into cutting-edge extraction methods for better yields and purity but are also forging collaborations to bolster traceability and certification, responding to the surging appetite for organic and clean-label ginger oil.

Ginger Oil Industry Leaders

Givaudan SA

Symrise AG

International Flavors and Fragrances Inc.

doTERRA International

Young Living Essential Oils

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: The European Commission published an essential-oil purity update mandating batch-level GC-MS reporting for single-origin oils sold above certain value thresholds, explicit labeling when products contain synthetic constituents or nature-identical aroma chemicals, and stricter oversight of unsupported health or therapeutic claims, with phased timelines and technical assistance for micro-producers during the first two years.

- October 2024: Nutraland USA, a prominent player in the nutraceutical sector, unveils its premium black ginger extract, Actiz!ng, at the SupplySide West (SSW) tradeshow in Las Vegas, NV.

Global Ginger Oil Market Report Scope

| Organic Ginger Oil |

| Conventional Ginger Oil |

| Food & Beverages |

| Pharmaceuticals & Nutraceuticals |

| Personal Care & Cosmetics |

| Aromatherapy & Wellness |

| Fragrance & Perfumery |

| Others (Household Cleaners, Etc.) |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Product Type | Organic Ginger Oil | |

| Conventional Ginger Oil | ||

| By Application | Food & Beverages | |

| Pharmaceuticals & Nutraceuticals | ||

| Personal Care & Cosmetics | ||

| Aromatherapy & Wellness | ||

| Fragrance & Perfumery | ||

| Others (Household Cleaners, Etc.) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

How large will the Ginger oil market be by 2031?

Forecasts indicate the market will reach USD 245.68 million by 2031, reflecting a 6.12% CAGR over 2026-2031.

Which application is growing fastest for ginger oil?

Aromatherapy products are projected to expand at about 7.25% CAGR as wellness routines adopt diffuser blends and topical balms.

Why are organic ginger oil supplies tight?

New U.S. and EU certification rules extend audits to brokers and mandate GC-MS reports, stretching approval queues and capping near-term volumes.

Who are the dominant players in the sector?

IFF, Symrise, dsm-firmenich, and Givaudan together hold roughly two-thirds of global supply, giving the market a moderate concentration profile.

Page last updated on: