Palm Oil Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 74.51 Billion |

| Market Size (2031) | USD 92.01 Billion |

| Growth Rate (2026 - 2031) | 4.31% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

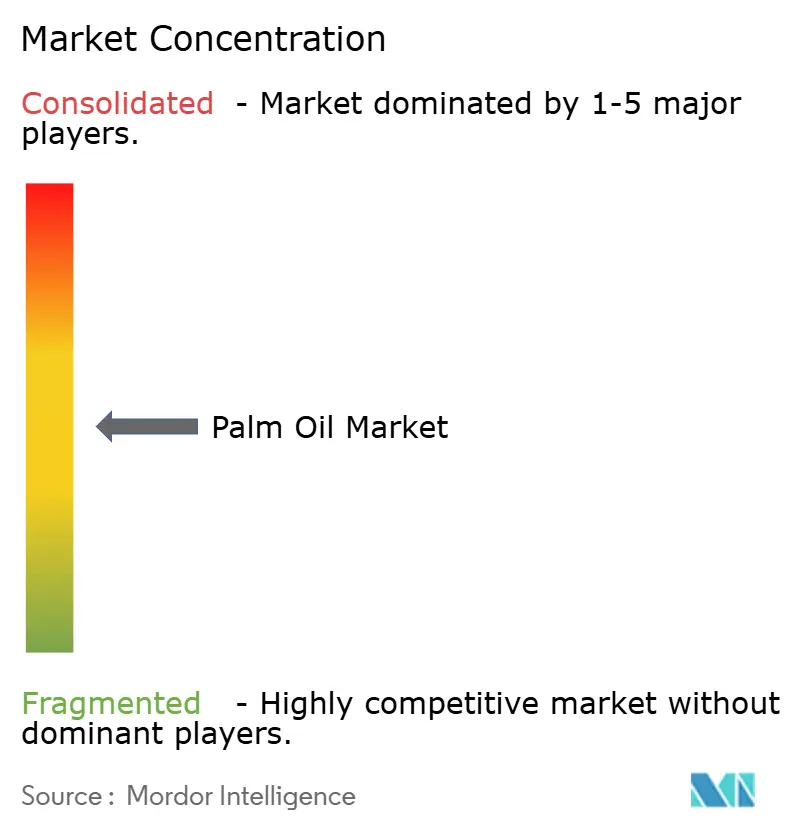

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Palm Oil Market Analysis by Mordor Intelligence

The palm oil market size is expected to increase from USD 71.43 billion in 2025 to USD 74.51 billion in 2026 and reach USD 92.01 billion by 2031, growing at a CAGR of 4.31% over 2026-2031. This growth is primarily driven by strong demand from industries such as food processing, personal care, and oleochemicals. These sectors rely heavily on palm oil for various applications, including cooking, skincare products, and industrial uses. Innovation in palm oil products is playing a significant role in shaping the market. Refined, bleached, and deodorized (RBD) palm oil continues to dominate in frying and bakery applications, while palm kernel oil is increasingly used in cosmetics due to its beneficial properties. Fractionated palm oil derivatives are gaining popularity in specialty fats used for chocolate production and dairy alternatives. Overall, the market remains moderately consolidated, with a mix of established players and emerging competitors.

Key Report Takeaways

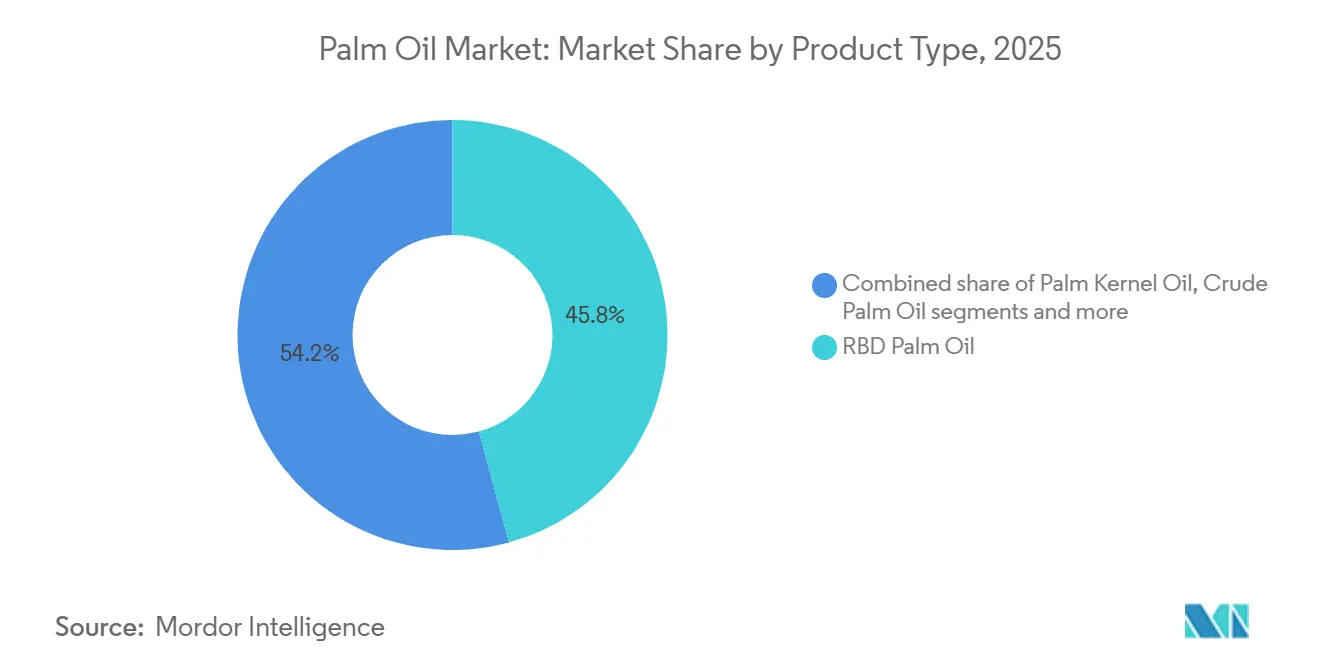

- By product type, RBD palm oil led with 45.76% revenue share in 2025; whereas, palm kernel oil is forecast to register a 5.45% CAGR through 2031.

- By nature, conventional grades held 91.22% of the palm oil market share in 2025, while organic-certified output is projected to post a 5.84% CAGR to 2031.

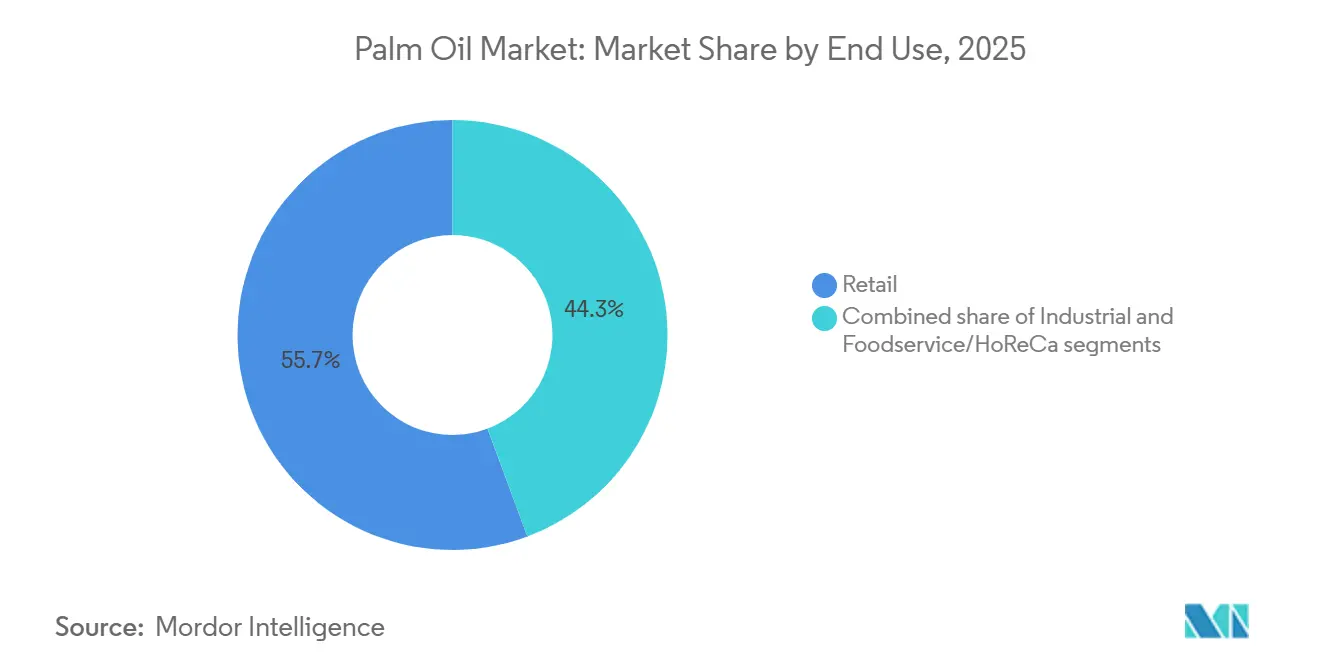

- By end use, retail accounted for 55.67% of demand in 2025, and industrial is advancing at a 6.51% CAGR through 2031.

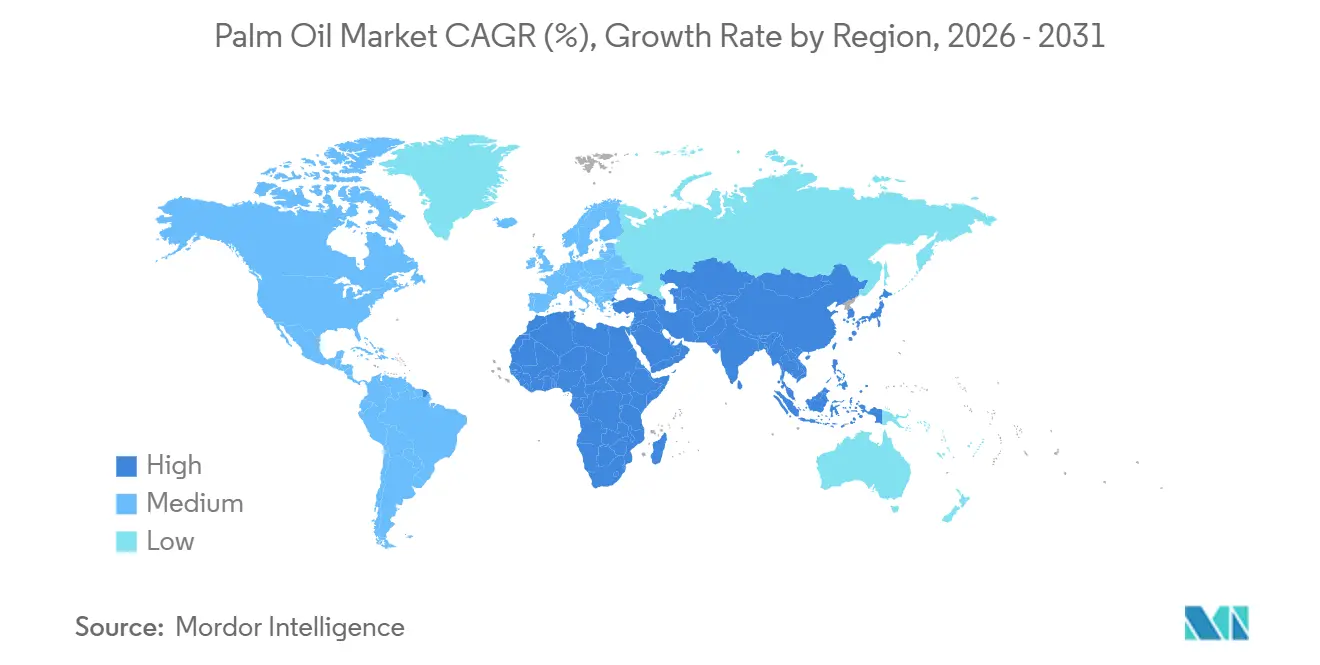

- By geography, Asia-Pacific dominated with a 74.31% share in 2025, whereas the Middle East and Africa will expand at a 5.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Palm Oil Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand for affordable edible oils in emerging economies (India, China, African countries) | +0.8% | Asia-Pacific core, spillover to Sub-Saharan Africa and Middle East | Medium term (2-4 years) |

| Functional advantages including oxidative stability, shelf life, and high-temperature cooking suitability | +0.5% | Global, with concentration in foodservice and QSR sectors across all regions | Long term (≥ 4 years) |

| Strong demand from global food processing industry | +0.9% | Global, led by Asia-Pacific and North America | Medium term (2-4 years) |

| Rising demand from personal care and cosmetics industry | +0.4% | North America, Europe, and premium segments in Asia-Pacific | Long term (≥ 4 years) |

| Increasing adoption in oleochemical production | +0.3% | Asia-Pacific manufacturing hubs, spillover to Middle East | Long term (≥ 4 years) |

| Expansion of foodservice and quick-service restaurant sector for commercial frying | +0.6% | Global, with rapid growth in Asia-Pacific, Middle East, and Latin America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Demand for affordable edible oils, particularly in emerging economies such as India, China, and African countries

Palm oil remains in high demand in emerging economies due to its affordability and reliance on imports, especially for food-related uses. In 2024, India imported USD 8.27 billion worth of palm oil, making it the largest importer globally among 210 countries, as reported by the Observatory of Economic Complexity (OEC)[1]Source: Observatory of Economic Complexity, "Palm Oil in India", oec.world. This highlights its importance in meeting India’s edible oil needs. Palm oil is cheaper than alternatives such as soybean and sunflower oil, making it widely used in products such as instant noodles, bakery items, and vanaspati. Similarly, China is a major importer, driven by growing processed food consumption and a recovering foodservice sector. In Sub-Saharan Africa, countries like Nigeria and Kenya depend heavily on palm oil because it is affordable, has a long shelf life, and performs well in hot climates.

Increasing functional advantages of palm oil, including oxidative stability, longer shelf life, and suitability for high-temperature cooking

Rising global temperatures and prolonged heat exposure are reinforcing demand for palm oil due to its superior oxidative stability and resistance to spoilage under ambient storage conditions. For instance, Australia recorded its hottest 12-month period between April 2024 and March 2025, with average temperatures reaching 1.61°C above the long-term average (34.9°F), reflecting persistent nationwide heatwave conditions and reduced cooling intervals, as reported by Phys.org[2]Source: Phys Org, "Australia Sweats Through Hottest 12 Months On Record: Official Data", phys.org. In such high-temperature environments, palm oil’s naturally stable fatty acid composition enables longer shelf life without refrigeration or hydrogenation, making it particularly suitable for packaged foods, bakery products, and frying applications.

Strong demand from the global food processing industry is fueling market growth

Long-term supply contracts and the food processing industry's growing reliance on palm oil continue to drive steady global demand. In India, the food processing market was valued at INR 30,49,800 crore (USD 354.5 billion) in 2024 and is expected to grow significantly, reaching INR 45,84,415 crore (USD 535 billion) by FY2026, as reported by the India Brand Equity Foundation (IBEF)[3]Source: India Brand Equity Foundation, "Food Processing", ibef.org. This growth is fueled by the increasing popularity of packaged foods, bakery items, and ready-to-eat products, which heavily rely on palm oil. Palm oil is widely used in these products because it is cost-effective, provides stability during cooking, and helps extend shelf life. Palm oil and its derivatives are key ingredients in processed foods like snacks, confectionery, and dairy alternatives. These ingredients are valued for their ability to enhance texture, resist heat, and ensure consistent product quality, making them indispensable in the food processing industry.

Increasing adoption of palm oil in oleochemical production

The growing demand for environmentally friendly and sustainable raw materials is boosting the use of palm oil in the global oleochemical industry. Products derived from palm oil, such as fatty acids, glycerin, and fatty alcohols, are widely utilized in making everyday items like soaps, detergents, cosmetics, pharmaceuticals, lubricants, and various industrial chemicals. These palm-based ingredients are favored because they are renewable, biodegradable, and highly effective in their applications. With stricter environmental regulations and increasing corporate commitments to sustainability, companies are moving away from petroleum-based inputs and adopting palm-based oleochemicals to meet eco-friendly standards and renewable content requirements. Furthermore, palm oil derivatives play a crucial role in creating surfactants, emulsifiers, and polyols, which are essential components in personal care products and flexible foams, further expanding their importance in various industries.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Environmental concerns related to deforestation, biodiversity loss, and greenhouse gas emissions | -0.7% | Global, with acute focus on Indonesia, Malaysia, and European import markets | Long term (≥ 4 years) |

| Increasing regulatory restrictions and sustainability requirements | -0.5% | Europe, North America, with spillover to Asia-Pacific exporters | Medium term (2-4 years) |

| Rising consumer awareness regarding environmental and ethical sourcing | -0.3% | North America, Europe, and urban centers in Asia-Pacific | Medium term (2-4 years) |

| Availability and increasing production of alternative vegetable oils (soybean, sunflower, canola) | -0.4% | Global, with substitution pressure in North America, Europe, and China | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Environmental concerns related to deforestation, biodiversity loss, and greenhouse gas emissions associated with palm oil cultivation

Concerns about deforestation and loss of biodiversity are slowing the growth of the palm oil market as they lead to stricter regulations and higher supply chain compliance demands. The expansion of palm oil plantations, especially in Southeast Asia, has been associated with significant environmental issues such as forest destruction, peatland damage, and increased carbon emissions. These impacts have drawn criticism from governments, environmental groups, and global stakeholders. In response, many major food manufacturers and consumer goods companies are adopting stricter sourcing policies. These policies often require certifications proving that the palm oil is deforestation-free and that the entire supply chain is traceable. However, meeting these requirements poses challenges, particularly for small-scale farmers who may lack the financial and technical resources needed to comply with these evolving sustainability standards.

Increasing regulatory restrictions and sustainability requirements

Strict environmental rules and traceability requirements are making it more expensive and challenging for palm oil exporters to operate, especially in major importing regions like Europe and North America. For instance, the European Union Deforestation Regulation, which will take effect in December 2024, mandates that importers provide detailed geolocation data and verified evidence proving that the palm oil they source does not come from deforested areas. This significantly increases the need for extensive documentation, monitoring, and certification throughout the supply chain. These regulations are particularly tough on small-scale producers, as they often lack access to advanced tools like digital mapping systems and traceability technologies. To comply with these rules and maintain access to international markets, exporters are being forced to invest heavily in satellite monitoring systems, certification programs, and measures to improve supply chain transparency.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Refining Complexity Shapes Margin Structure

RBD palm oil held the largest share of the palm oil market in 2025, accounting for 45.76%. This product segment is widely used in food processing industries due to its neutral taste, long shelf life, and affordability. It is commonly found in cooking oils, bakery items, confectionery, and packaged foods. RBD palm oil is also highly versatile and stable, making it suitable for both household use and large-scale food manufacturing. Its strong demand in emerging markets, particularly in Asia and Africa, has further solidified its position as the leading product segment.

Palm kernel oil is expected to grow at a compound annual growth rate (CAGR) of 5.45% through 2031, driven by its increasing use in personal care, cosmetics, and specialty food products. This oil is rich in lauric acid, which makes it ideal for producing soaps, detergents, surfactants, and oleochemicals. The rising preference for natural and plant-based ingredients in personal care products, along with the expansion of the global cosmetics industry, is boosting its demand. Its functional properties and applications in both food and non-food industries are expected to support its steady growth during the forecast period.

By Nature: Organic Certification Earns Premiums Yet Lacks Scale

Conventional palm oil grades led the market in 2025, contributing 91.22% of the total revenue. This dominance is due to its affordability, easy availability, and widespread use in food, industrial, and biofuel applications. Food manufacturers and industrial users prefer conventional palm oil because it is consistently available, stable in performance, and more cost-effective compared to other vegetable oils. Countries like Indonesia and Malaysia play a key role in its large-scale production, ensuring a steady supply worldwide. Its extensive use in packaged foods, cooking oils, and processed products continues to drive its demand in the market.

Organic palm oil is expected to grow at a CAGR of 5.84% through 2031, as consumers increasingly prefer products that are sustainably sourced and environmentally friendly. Awareness about the negative impacts of deforestation and the importance of ethical sourcing is pushing manufacturers to adopt certified organic palm oil. This trend is further supported by the rising demand for organic and clean-label products in industries such as food, cosmetics, and personal care. Moreover, global brands are making sustainability commitments, and regulatory support is encouraging the adoption of organic palm oil, which is likely to boost its market growth during the forecast period.

By End Use: Food Processing Anchors Volume, Personal Care Lifts Value

The retail segment accounted for 55.67% of palm oil demand in 2025, mainly due to its widespread use in household cooking and food preparation. This demand is particularly strong in developing regions like Asia, Africa, and Latin America, where palm oil is valued for its affordability and long shelf life. Its versatility in cooking and easy availability in packaged forms through supermarkets, hypermarkets, and local stores have made it a popular choice for consumers. Factors such as population growth, urbanization, and rising consumption of edible oils are driving the retail segment's dominance in the market.

The industrial segment is expected to grow at a CAGR of 6.51% through 2031, driven by its extensive use across food processing, cosmetics, personal care, oleochemicals, and biofuels. Palm oil is a key ingredient in the production of processed foods, soaps, detergents, and industrial lubricants due to its cost-effectiveness and functional properties. The rising demand for processed foods and palm-based products in non-food applications is further boosting industrial usage. Moreover, the growing production of biofuels and increasing industrial activities in developing countries are expected to sustain the strong growth of this segment during the forecast period.

Geography Analysis

In 2025, the Asia-Pacific region led the palm oil market, contributing 74.31% of the total revenue. This dominance was driven by high production and consumption levels in Indonesia and Malaysia. Indonesia’s domestic demand grew significantly due to its use in food processing and biodiesel blending programs, ensuring a steady supply-demand balance. Malaysia, on the other hand, remained a major exporter, catering to large import-dependent markets like India and China, which rely on palm oil for food manufacturing and edible oil needs. Countries like Thailand and the Philippines expanded their refining capacities, adding more value to the regional supply chain and solidifying Asia-Pacific’s position as a market leader.

The Middle East and Africa are expected to grow at a CAGR of 5.18% from 2026 to 2031, driven by rising imports to meet increasing edible oil demand. Countries such as Nigeria and Egypt are importing more palm oil due to limited local oilseed production and growing population needs. Gulf Cooperation Council (GCC) nations, including the United Arab Emirates and Saudi Arabia, have become key players by acting as refining and re-export hubs, supported by advanced infrastructure and strong trade networks. The region’s shift toward palm oil as a cost-effective alternative to other vegetable oils is anticipated to further boost market growth during the forecast period.

Europe and North America are relatively mature markets, with stable or slightly declining palm oil consumption. This trend is influenced by stricter regulations on sustainability and deforestation, as well as changing consumer preferences for alternative vegetable oils. Manufacturers in these regions are reformulating products and diversifying oil sources to meet these evolving demands. Meanwhile, Latin America continues to show steady demand, supported by biodiesel programs and industrial applications of palm oil derivatives. While growth in developed regions remains slow, emerging markets in Asia-Pacific and the Middle East and Africa are driving global demand, shaping the future trajectory of the palm oil market.

Competitive Landscape

The palm oil market is moderately consolidated, with major companies like Wilmar International, Bunge Limited, Cargill Incorporated, FGV Holdings Berhad, and Olam Group playing a dominant role. These companies have significant control over the value chain through ownership of large plantations, refining facilities, and well-established global distribution networks. Their ability to manage both upstream and downstream operations efficiently gives them a competitive edge. Vertical integration helps these players reduce costs, minimize supply chain risks, and ensure consistent market access, making them key leaders in the industry.

Sustainability, traceability, and transparency in the supply chain have become essential for competing in the palm oil market. Leading companies are adopting digital tools, certification programs, and sustainable sourcing practices to comply with stricter regulations and meet customer demands. Producing certified and traceable palm oil is now critical for accessing major international markets. Companies are focusing on developing value-added palm oil derivatives for use in food processing, personal care, and industrial applications. This diversification helps them expand their revenue streams and strengthen their market position.

Competition in the palm oil market is expected to grow as companies focus on innovation, sustainability, and operational efficiency to stand out. While traditional palm oil production remains the primary source of global supply, emerging technologies and alternative production methods are gaining attention. At the same time, niche segments like organic and sustainably sourced palm oil are becoming popular among environmentally conscious consumers. Companies with strong commitments to sustainability, integrated operations, and advanced supply chain management are likely to maintain a competitive advantage in the evolving global palm oil market.

Palm Oil Industry Leaders

-

Wilmar International Limited

-

Bunge Limited

-

Cargill, Incorporated

-

Olam Group

-

FGV Holdings Berhad

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Raj Oil Mills Limited launched its new palm oil product PALMRAJ, targeting the domestic edible oil market. The announcement had been made in compliance with SEBI Regulation 30 requirements to both BSE and NSE. The product was categorized as refined palmolein oil and had focused exclusively on domestic consumers rather than international markets.

- October 2024: Daabon UK announced the launch of its carbon-neutral organic palm oil range. The company stated that the carbon-neutral organic palm oil had been produced at Daabon’s CI Tequendama SAS mill, located in northern Colombia. This initiative was part of Daabon’s commitment to sustainability and reducing its environmental impact.

- May 2024: Wilmar Processing, a multinational agribusiness, completed the first operational phase of its R1.27-billion (USD 68 million) edible oils refining plant. The facility, named Wilmar Processing SA, was established within the Richards Bay Industrial Development Zone (RBIDZ) Special Economic Zone in KwaZulu.

- March 2024: India's first integrated oil palm processing unit was established in Arunachal Pradesh. This milestone marked a significant step in the country's efforts to boost domestic palm oil production and reduce dependency on imports.

Global Palm Oil Market Report Scope

Palm oil is an edible vegetable oil derived from the mesocarp (reddish pulp) of the fruit of oil palms. The global palm oil market is segmented by product type, nature, application, and geography. By product type, the market is segmented into palm kernel oil, crude palm oil, RBD palm oil, and fractioned palm oil. By nature, the market is segmented into conventional and organic. By end use, the market is segmented into industrial, foodservice/HoReCa, and retail. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The market sizing has been done in value (USD) and volume (Tons) terms for all the aforementioned segments.

| Crude Palm Oil |

| Palm Kernel Oil |

| RBD Palm Oil |

| Fractioned Palm Oil |

| Organic |

| Conventional |

| Industrial | Food Processing | Bakery and Confectionery |

| Dairy and Dairy Alternatives Products | ||

| RTE/RTC Food Products | ||

| Snacks | ||

| Others | ||

| Personal Care and Cosmetics | ||

| Animal Feed | ||

| Biofuel | ||

| Others | ||

| Foodservice/HoReCa | ||

| Retail | Supermarkets/Hypermarket | |

| Convenience Stores | ||

| Online Retail Stores | ||

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Crude Palm Oil | ||

| Palm Kernel Oil | |||

| RBD Palm Oil | |||

| Fractioned Palm Oil | |||

| By Nature | Organic | ||

| Conventional | |||

| By End Use | Industrial | Food Processing | Bakery and Confectionery |

| Dairy and Dairy Alternatives Products | |||

| RTE/RTC Food Products | |||

| Snacks | |||

| Others | |||

| Personal Care and Cosmetics | |||

| Animal Feed | |||

| Biofuel | |||

| Others | |||

| Foodservice/HoReCa | |||

| Retail | Supermarkets/Hypermarket | ||

| Convenience Stores | |||

| Online Retail Stores | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Rest of North America | |||

| South America | Brazil | ||

| Argentina | |||

| Colombia | |||

| Chile | |||

| Peru | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| Italy | |||

| France | |||

| Spain | |||

| Poland | |||

| Belgium | |||

| Sweden | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| Indonesia | |||

| South Korea | |||

| Thailand | |||

| Singapore | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | South Africa | ||

| Saudi Arabia | |||

| United Arab Emirates | |||

| Nigeria | |||

| Egypt | |||

| Morocco | |||

| Turkey | |||

| Rest of Middle East and Africa | |||

Key Questions Answered in the Report

What is the projected value of the Global palm oil market by 2031?

Forecasts place the Global palm oil market at USD 92.01 billion by 2031, reflecting a 4.31% CAGR from 2026-2031.

Which region will grow fastest through 2031?

The Middle East and Africa are set to register the quickest expansion at 5.18% CAGR as population growth and packaged-food adoption accelerate.

Which product segment is likely to outpace overall market growth?

Palm kernel oil is projected to rise at 5.45% CAGR because of its lauric acid suitability for cosmetics and specialty fats.

What key regulation is reshaping palm oil trade with Europe?

The EU Deforestation Regulation, effective December 2024, requires geolocation proof that shipments are deforestation-free, raising compliance costs for exporters.

Page last updated on: