Cooking Oil Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

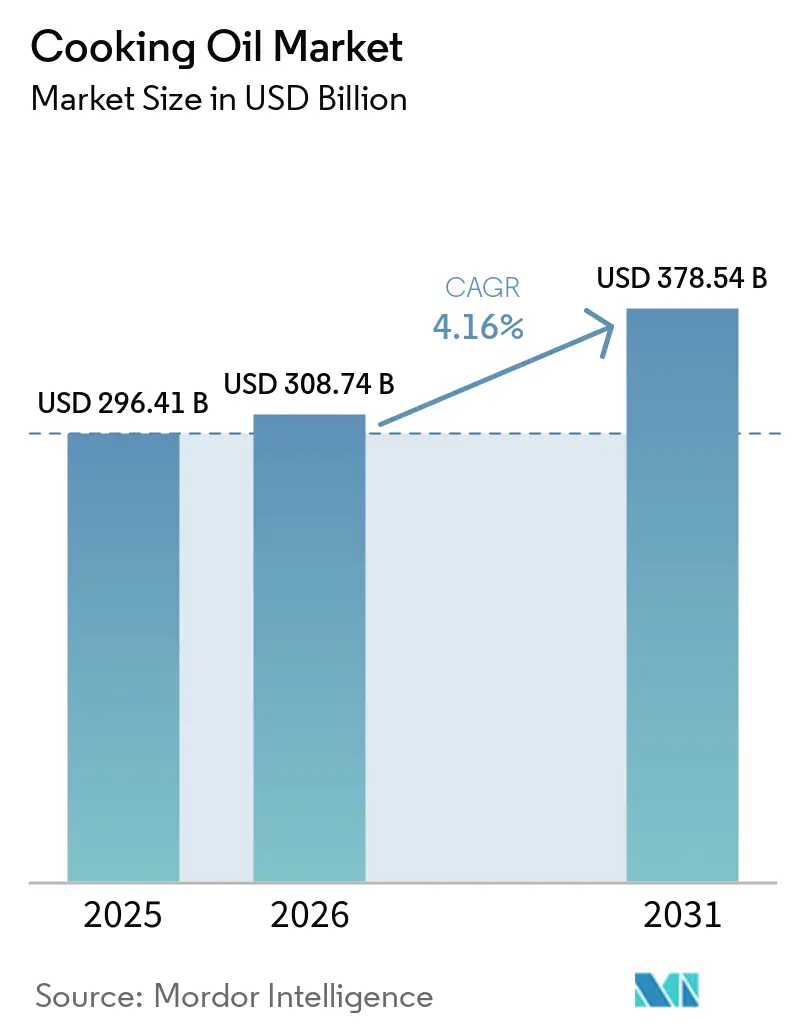

| Market Size (2026) | USD 308.74 Billion |

| Market Size (2031) | USD 378.54 Billion |

| Growth Rate (2026 - 2031) | 4.16% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cooking Oil Market Analysis by Mordor Intelligence

The global cooking oil market size was valued at USD 296.41 billion in 2025 and estimated to grow from USD 308.74 billion in 2026 to reach USD 378.54 billion by 2031, at a CAGR of 4.16% during the forecast period (2026-2031). Market growth is primarily driven by shifting consumer preferences, regulatory updates, and advancements in oil extraction and processing technologies. Factors such as urbanization, varied dietary habits, and the recovery of the foodservice industry further contribute to market expansion, as more consumers seek convenient and diverse food options. The adoption of cold-press and subcritical extraction technologies has enhanced product quality and yield, offering healthier and more sustainable alternatives to traditional methods. Additionally, rising consumer demand for functional, organic, and sustainably certified oils, influenced by updated nutrition labeling regulations in key markets, is shaping the industry by encouraging manufacturers to innovate and meet evolving standards. Significant developments, including the Bunge-Viterra merger, Cargill's processing facility upgrades, and new crushing facility projects, are reshaping global supply chains and the competitive landscape, enabling companies to optimize production and distribution processes to meet growing demand efficiently.

Key Report Takeaways

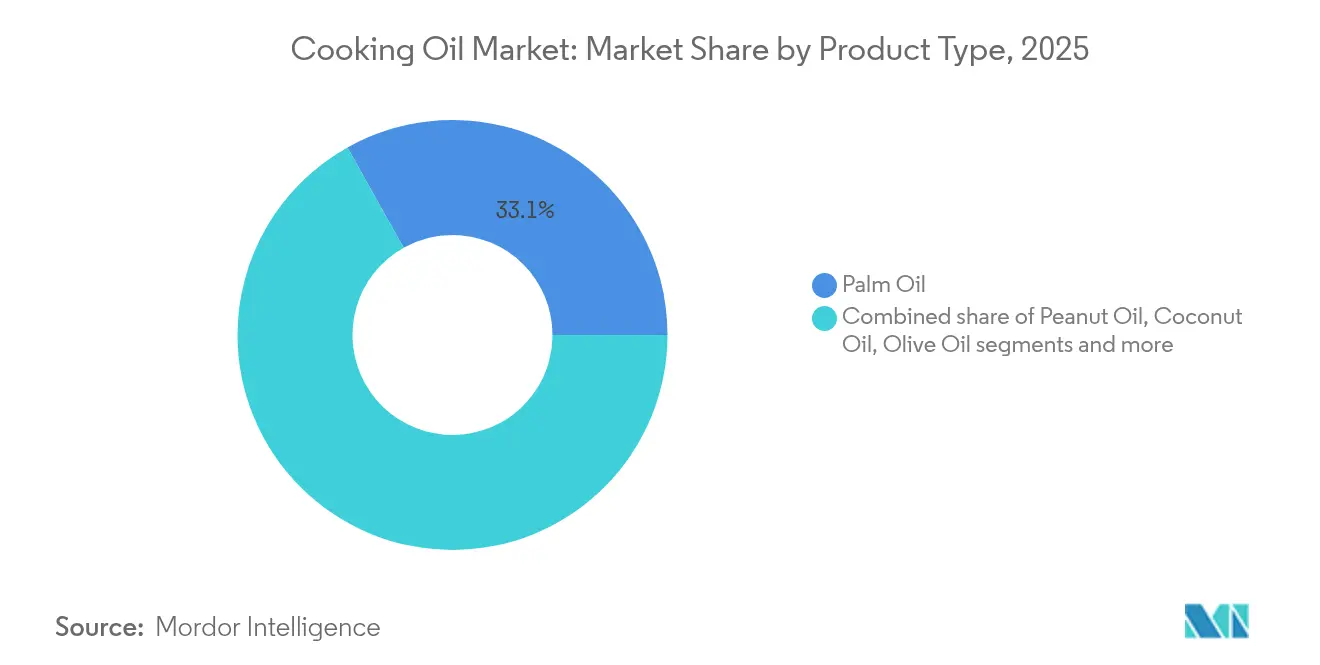

- By product type, palm oil led with 33.12% of cooking oil market share in 2025, whereas coconut oil is projected to post the fastest 4.97% CAGR through 2031.

- By processing type, refined oils accounted for 85.05% of the cooking oil market size in 2025 and are expected to expand at a 4.95% CAGR during the forecast period.

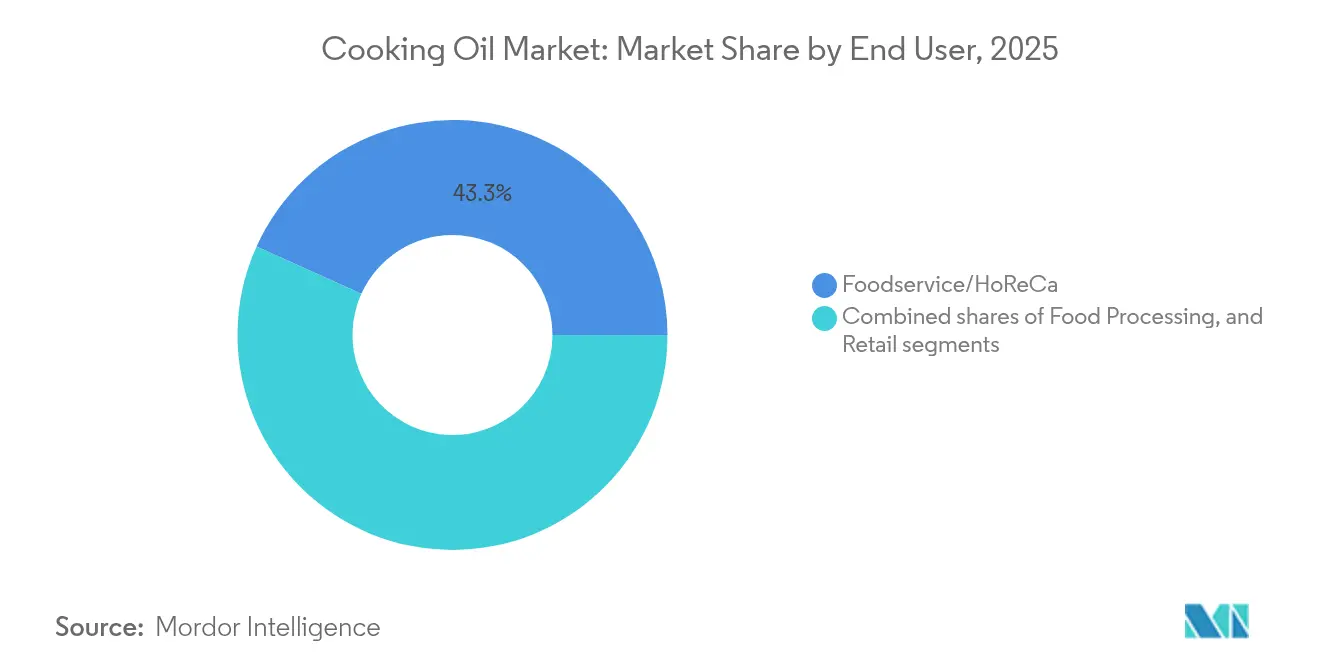

- By end user, the foodservice segment captured 43.25% revenue share in 2025 and is advancing at a 5.46% CAGR up to 2031.

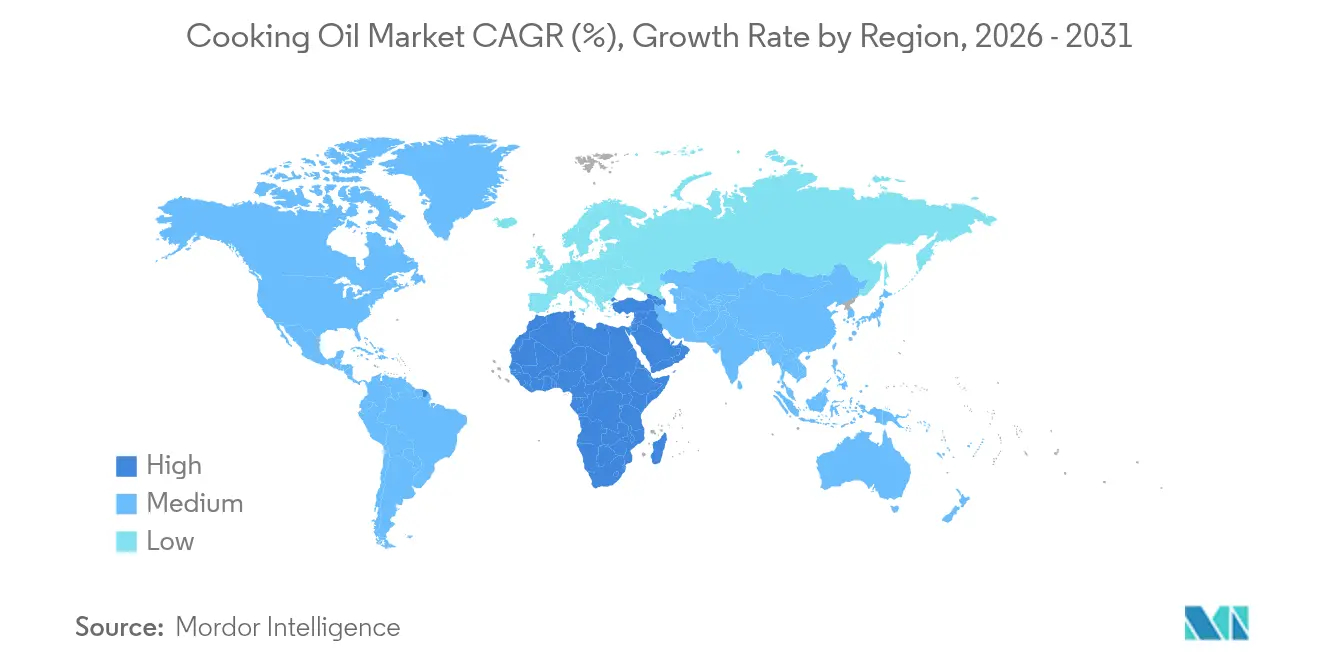

- By geography, Asia-Pacific dominated with 52.70% share in 2025; the region is also forecast to register the highest 5.41% CAGR to 2031, led by China, India, and Indonesia.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cooking Oil Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing consumer preference for healthy and functional oils | +0.8% | Global, with early gains in North America, EU, and urban Asia-Pacific | Medium term (2-4 years) |

| Demand for organic, cold-pressed, and non-GMO cooking oils | +0.6% | North America and Europe core, spill-over to Asia-Pacific premium segments | Long term (≥ 4 years) |

| Growth in fast food and processed food industries boosting cooking oil usage | +1.2% | Global, concentrated in Asia-Pacific, North America, and emerging markets | Short term (≤ 2 years) |

| Rising adoption of sustainable and ethically sourced oils | +0.5% | Europe, North America, with increasing adoption in urban Asia-Pacific | Long term (≥ 4 years) |

| Growing popularity of plant-based and vegan diets encouraging oil consumption | +0.4% | North America, Europe, urban centers in Asia-Pacific | Medium term (2-4 years) |

| Technological advancements in oil extraction improving quality and yield | +0.7% | Global, with leadership in developed markets and technology transfer to emerging regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Consumer Preference for Healthy and Functional Oils

The FDA's revised definition of "healthy," taking effect February 25, 2025, represents a significant shift in food labeling regulations by including oils in its classification, enabling olive oil products to carry healthy food labels for the first time [1]Source: U.S. Food & Drug Administration, “FDA Updated “Healthy” Nutrient Content Claim,” fda.gov. This regulatory update addresses growing consumer interest in oils containing beneficial compounds such as omega-3 fatty acids, antioxidants, and vitamin E, which has created opportunities for manufacturers to develop premium products across various food categories. In the United States, market analysis reveals diverse consumer attitudes toward seed oils, with purchasing decisions increasingly shaped by social media discussions and health-related content. The inclusion of vegetable oils in healthy diet recommendations by the 2025 Dietary Guidelines Advisory Committee provides scientific backing for continued market expansion, particularly benefiting manufacturers of olive, avocado, and specialty seed oils who position their products as functional ingredients with specific health benefits.

Demand for Organic, Cold-Pressed, and Non-GMO Cooking Oils

Soybeans have emerged as the dominant organic oilseed crop within the organic arable land segment, reflecting a significant shift in agricultural production patterns. The organic market's sustained expansion has generated robust demand for premium oils, particularly in Europe and North America, where increasingly informed consumers actively pursue certified organic and non-GMO products for their dietary requirements. The financial analysis of small-scale cold-press extraction operations demonstrates compelling economic viability, with businesses achieving breakeven within 23 months at their specified production volumes and market-driven pricing structures. This accessible business model has created valuable opportunities for local entrepreneurs to establish themselves in the premium oil production market. Responding to these market dynamics, ADM made a strategic move to enhance its European presence in September 2024 through the acquisition of specialized facilities in Hungary dedicated to non-GMO soybean and corn oil production, effectively addressing European consumer preferences while ensuring compliance with the region's comprehensive regulatory framework for genetic modification labeling.

Growth in Fast Food and Processed Food Industries Boosting Cooking Oil Usage

The foodservice sector's robust recovery continues to be a significant driver of edible oil demand, exemplified by major industry players like Ventura Foods, which consumes 2 billion pounds of edible oils annually, with soybean oil representing 65-75% of their total usage as of March 2024. In a notable development, Restaurant Technologies has implemented an innovative approach by transforming used cooking oil into renewable fuels, demonstrating how foodservice operations can embrace circular economy principles while creating new revenue opportunities and addressing environmental responsibilities. The industry is witnessing a strategic shift as commercial kitchens increasingly incorporate beef tallow alongside traditional seed oils, with operators recognizing that tallow's superior heat stability and flavor enhancement capabilities justify its premium cost through extended usage periods. The market dynamics are further shaped by intensifying competition between food manufacturers and biofuel producers for soybean oil resources, where the growing renewable diesel sector not only puts upward pressure on cooking oil prices but also contributes to the expansion of the overall market value.

Rising Adoption of Sustainable and Ethically Sourced Oils

The implementation of the EU's Deforestation Regulation (EUDR) has prompted Malaysia to enhance its sustainability framework through the Malaysian Sustainable Palm Oil (MSPO) 2.0 certification program, reflecting the industry's commitment to environmental responsibility [2]Source: Malaysian Sustainable Palm Oil, “Global Position for Malaysian Palm Oil,” mspo.org.my. While research indicates these regulations impact production efficiency, palm oil demonstrates remarkable resource optimization, with Wageningen University studies confirming that palm oil production delivers more than twice the yield per hectare compared to soybean and rapeseed alternatives. This efficiency advantage, however, faces a practical challenge in the marketplace, where consumers' expressed interest in sustainable palm oil products often does not translate into actual purchasing decisions. This disconnect has emphasized the importance of developing more effective labeling strategies and robust corporate responsibility programs to help consumers align their sustainability values with their buying behavior.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing regulatory scrutiny on labeling, additives, and contaminants | -0.3% | Global, with strictest enforcement in EU, North America, and developed Asia-Pacific | Short term (≤ 2 years) |

| Limited shelf-life and storage challenges for premium unrefined oils | -0.2% | Global, particularly affecting premium segments in developed markets | Medium term (2-4 years) |

| Variable regional dietary preferences limiting uniform demand | -0.4% | Global, with pronounced effects in culturally diverse regions | Long term (≥ 4 years) |

| Risk of adulteration and counterfeit products | -0.5% | Asia-Pacific core, emerging markets with weaker regulatory enforcement | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing Regulatory Scrutiny on Labeling, Additives, and Contaminants

The global cooking oil industry faces increasingly complex regulatory requirements across major markets, reflecting heightened concerns about product quality and consumer safety. The Canadian Food Inspection Agency has implemented rigorous compliance measures for olive oil, requiring manufacturers to ensure their products meet precise international standards for free fatty acid content in 'extra virgin' and 'virgin' classifications [3]Source: Government of Canada, “Canada's regulatory requirements for olive oil,” canada.ca. Similarly, the European Union's introduction of mineral oil hydrocarbon restrictions has created significant operational challenges for vegetable oil producers, particularly regarding MOAH contamination limits in infant formula, with potential expansion to other food categories. In the United States, regional regulations have become more stringent, with Texas implementing comprehensive warning label requirements for 44 food additives starting January 2027, while Louisiana now requires detailed disclosure through QR codes and menu listings for common seed oils such as canola and soybean. These regional and national requirements operate alongside international standards, as evidenced by the Codex Alimentarius Committee's 28th session, which expanded its vegetable oil standards to include emerging products like avocado and Camellia seed oils, necessitating substantial investments in compliance measures by industry participants.

Risk of Adulteration and Counterfeit Products

The 2024 cooking oil contamination scandal in China, involving state-owned Sinograin and Hopefull Grain and Oil Group, revealed that these companies allegedly used unwashed fuel tankers to transport cooking oil. This incident exposed systemic food safety risks and led to government investigations, highlighting the connection between food safety and national stability. The chemical contamination from improper transportation methods created significant health concerns and revealed supply chain vulnerabilities in major production regions with inadequate oversight. This represents China's most significant food safety incident since 2008, affecting consumer confidence in cooking oil products and demonstrating the need for enhanced traceability systems and third-party verification. The premium oil segments, including organic and cold-pressed varieties, face particular challenges from counterfeit products due to their higher profit margins. This situation requires improved authentication technologies and supply chain transparency to ensure product integrity and consumer safety.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Palm Oil Dominance Faces Sustainability Pressures

Palm oil continues to dominate the vegetable oils market, commanding a substantial 33.12% market share in 2025. This prominence stems from its exceptional land use efficiency, yielding 2.9 tonnes per hectare, which sets it apart from competing vegetable oil alternatives in terms of productivity and resource optimization. The market structure reflects a significant geographical concentration, with Indonesia and Malaysia jointly controlling 83% of global production. This duopoly has established these nations as pivotal players in the international vegetable oils trade, influencing global supply dynamics and price mechanisms.

The coconut oil segment presents a compelling growth narrative, exhibiting a robust CAGR of 4.97% through 2031. This expansion is fundamentally driven by evolving consumer preferences in developed markets, particularly in the United States and European Union, where demand for premium coconut oil products continues to strengthen. The market's growth trajectory is further reinforced by increasing Chinese import volumes, which contribute significantly to market momentum. Despite these positive demand indicators, global production capacity remains consistent at 3.22 million metric tons, creating an interesting dynamic between supply stability and growing market demand.

By Processing Type: Refined Oils Lead Through Technology Innovation

Refined oils maintain a dominant position in the market with an 85.05% share in 2025, demonstrating the industry's reliance on processed oil products. The segment's robust growth trajectory, projected at a 4.95% CAGR through 2031, reflects the substantial improvements in processing technologies that enhance both product quality and consumer safety. This advancement is exemplified by Cargill's milestone achievement in January 2024, when it became the first global edible oils supplier to meet World Health Organization trans-fatty acid standards following an investment exceeding USD 8.5 million in facility modernization.

The industry's technological evolution has introduced sophisticated refining methods that benefit both manufacturers and consumers. The implementation of nano-neutralization and enzymatic degumming processes has successfully reduced chemical consumption while simultaneously improving production yields. The transition from traditional single-stage processes to multi-stage bleaching represents a significant advancement in contaminant removal capabilities. In the specialty segment, unrefined oils continue to attract premium market consumers through specialized extraction methods such as cold-press and subcritical technologies. These methods have proven their economic feasibility even in smaller-scale operations, despite facing challenges related to recovery rates and storage requirements.

By End User: Foodservice Sector Drives Market Expansion

The foodservice/HoReCa segment commands a substantial 43.25% market share in 2025, with projections indicating robust growth at a 5.46% CAGR through 2031. This expansion reflects the industry's strong recovery from pandemic-related challenges and demonstrates how consumer preferences are reshaping culinary practices. Restaurant operators are actively diversifying their oil portfolios, moving beyond traditional seed oils to incorporate specialty options like beef tallow. This strategic shift enables businesses to enhance their menu offerings with improved flavor profiles while optimizing their frying operations for better performance and cost efficiency. In the food processing sector, manufacturers are leveraging oils not just as cooking mediums but as essential functional ingredients that carry flavors, enhance texture profiles, and extend product shelf life, particularly in the rapidly expanding plant-based food category.

The retail landscape showcases distinct market dynamics across different channels. Supermarkets and hypermarkets continue to maintain their market leadership through strategic advantages in private label development and bulk purchasing capabilities, offering consumers competitive pricing options. Meanwhile, convenience stores have carved out their niche by focusing on premium, health-oriented oil products that resonate with health-conscious consumers willing to pay higher prices for perceived nutritional benefits. This segmentation reflects the market's ability to serve diverse consumer needs while maintaining profitable operations across different retail formats.

Geography Analysis

Asia-Pacific currently dominates the global vegetable oil market with a substantial 52.70% market share in 2025. This leadership position is primarily attributed to Indonesia and Malaysia's commanding presence in palm oil production, collectively contributing 83% of global output. The region's market strength is further reinforced by significant domestic consumption patterns in China and India. Thailand has established a comprehensive approach to palm oil industry development, implementing supportive government policies including tax incentives and infrastructure subsidies to enhance cultivation practices.

North America is emerging as the fastest-growing region, marked by strategic investments in processing infrastructure. A notable example is Louis Dreyfus Company's USD 375 million investment in Ohio, establishing a state-of-the-art facility capable of processing 175,000 bushels daily and producing 320,000 metric tons of refined soybean oil annually by mid-2026. This expansion demonstrates the region's commitment to increasing domestic processing capabilities and meeting growing market demand.

Europe continues to adapt to market changes, particularly in response to geopolitical tensions affecting sunflower oil supply chains and the implementation of the EU Deforestation Regulation, which has introduced new requirements for palm oil imports and certification. In the Middle East and Africa region, Egypt exemplifies market development potential, targeting 1,000 metric tons of olive oil exports for 2023/24, supported by an extensive cultivation program that has added 23 million olive trees since 2015, showcasing the region's commitment to agricultural diversification and export market development.

Competitive Landscape

The global cooking oil market continues to evolve with moderate consolidation, as companies actively seek competitive advantages through technological advancement, geographic expansion, and product differentiation. This dynamic environment has prompted significant corporate movements, particularly exemplified by Bunge Global SA's strategic merger with Viterra, which has created a formidable presence in the global agribusiness landscape. Bunge's commitment to market growth is further demonstrated by its substantial USD 225 million investment in Louisiana operations, aimed at enhancing vegetable oil production capacity in March 2024.

The industry is witnessing increased collaboration between major players, as illustrated by the partnership between Cargill and CBH Group in their development of advanced oilseed crushing facilities near Perth, Australia. This strategic alliance effectively capitalizes on existing grain terminal infrastructure to create a more efficient supply chain system that serves both domestic and international markets. While the market presents significant opportunities in sustainable certification and premium product segments, the challenges faced in Malaysia's RSPO certification process serve as a practical reminder of the operational complexities that companies must navigate to maintain production efficiency.

The competitive landscape continues to transform as new market participants bring fresh perspectives through specialty oil offerings and innovative extraction technologies. Meanwhile, established industry leaders maintain their market positions by leveraging their extensive distribution networks and economies of scale. This market dynamic plays out against an increasingly complex backdrop of evolving regulatory requirements and shifting consumer preferences, requiring companies to remain agile and responsive to change.

Cooking Oil Industry Leaders

Archer Daniels Midland

Cargill Incorporated

Bunge Global SA

Wilmar International Ltd

Louis Dreyfus Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Bunge Global SA announces merger with Viterra to create a leading global agribusiness company, enhancing oilseed processing capabilities and market reach across multiple geographic regions

- October 2024: Stratas Foods acquires AAK foodservice business in Hillside, New Jersey, for approximately USD 56.55 million, expanding presence in value-added oils, dressings, sauces, and mayonnaise categories

- September 2024: Scoular opens new canola and soybean oilseed crush facility in Goodland, Kansas, processing 11 million bushels annually while Bartlett launches USD 375 million soybean-crushing plant in Cherryvale with 45 million bushel capacity

Global Cooking Oil Market Report Scope

Cooking oil is a liquid fat made of plants, animals, or synthetic materials used in baking, frying, and other cooking processes. It may also be referred to as edible oil because it is used in cold food preparation and flavoring, including salad dressings and bread dips.

The global cooking oil market has been segmented based on type, application, and geography. Based on type, the market studied is segmented into palm oil, rapeseed oil, sunflower oil, peanut oil, and other types. Based on application, the market studied is segmented into bakery and confectionery, snack foods, salads and cooking oils, and other applications. Based on geography, the market studied is segmented into North America, Europe, Asia-Pacific, South America, and Middle East and Africa. For each segment, the market sizing and forecasts have been done based on value (in USD million).

| Palm Oil |

| Soybean Oil |

| Rapeseed/Canola Oil |

| Sunflower Oil |

| Peanut Oil |

| Coconut Oil |

| Olive Oil |

| Corn Oil |

| Others |

| Refined |

| Unrefined |

| Food Processing | |

| Foodservice/HoReCa | |

| Retail | Supermarkets and Hypermarkets |

| Convenience Stores | |

| Online Retail | |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Palm Oil | |

| Soybean Oil | ||

| Rapeseed/Canola Oil | ||

| Sunflower Oil | ||

| Peanut Oil | ||

| Coconut Oil | ||

| Olive Oil | ||

| Corn Oil | ||

| Others | ||

| By Processing Type | Refined | |

| Unrefined | ||

| By End User | Food Processing | |

| Foodservice/HoReCa | ||

| Retail | Supermarkets and Hypermarkets | |

| Convenience Stores | ||

| Online Retail | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the estimated value of the global cooking oil market in 2026?

The market stands at USD 308.74 billion in 2026.

How fast is the cooking oil market expected to grow between 2026 and 2031?

It is forecast to post a 4.16% CAGR, reaching USD 378.54 billion by 2031.

Which product currently contributes the largest revenue share?

Palm oil leads with a 33.12% share of global revenue in 2025.

Which geographic region holds the biggest slice of demand?

Asia-Pacific commands 52.70% of global revenue and shows the strongest 5.41% CAGR outlook.

How are new food-label regulations influencing product development?

FDA and EU rules favor healthier, lower-trans-fat and sustainably certified oils, prompting refiners to reformulate and upgrade processing lines.

Page last updated on: