Market Overview

| Study Period | 2021 - 2031 |

|---|---|

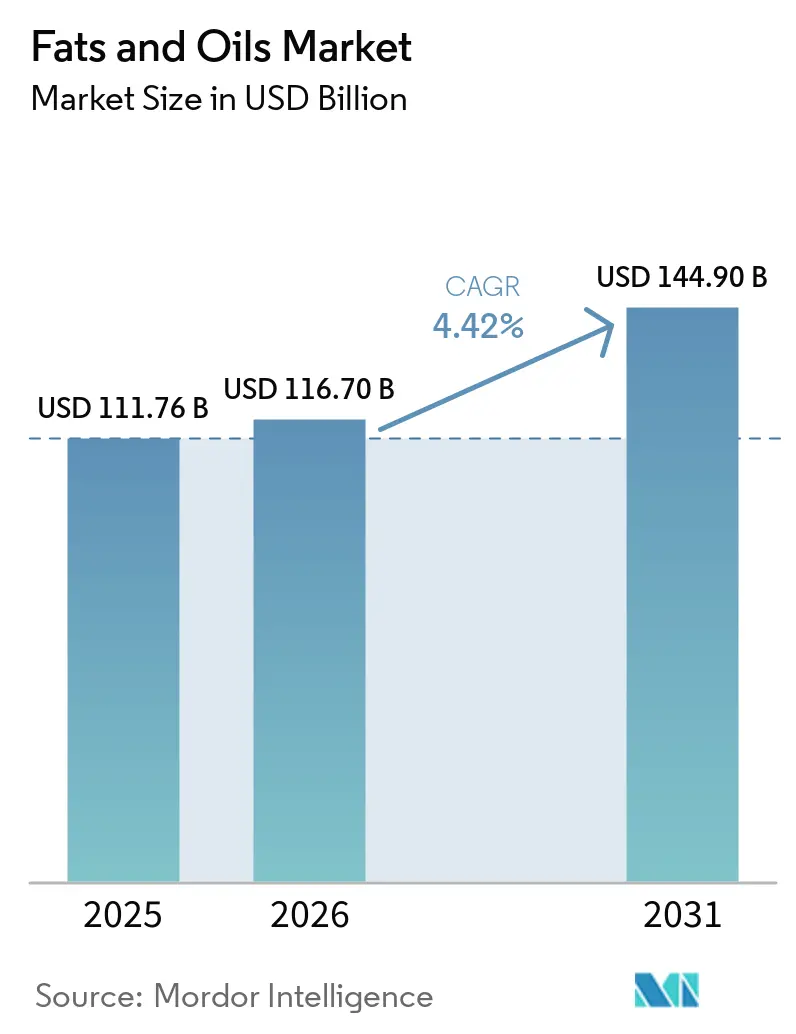

| Market Size (2026) | USD 116.70 Billion |

| Market Size (2031) | USD 144.90 Billion |

| Growth Rate (2026 - 2031) | 4.42% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Fats and Oils Market Analysis by Mordor Intelligence

The Fats And Oils Market size is expected to grow from USD 111.76 billion in 2025 to USD 116.70 billion in 2026 and is forecast to reach USD 144.90 billion by 2031 at 4.42% CAGR over 2026-2031. The market is experiencing steady growth driven by increasing consumption in food applications and rising demand from industrial sectors. The market's expansion is supported by population growth, changing dietary preferences, and the growing adoption of vegetable oils in various applications, including biofuels and personal care products. Additionally, the increasing awareness of health benefits associated with specific oils and fats, coupled with the rising disposable income in developing economies, continues to influence market dynamics.

Key Report Takeaways

- By type, oils led the fats and oils market with 54.92% share in 2025; the same segment is projected to expand at a CAGR of 5.44% through 2031.

- By application, the food segment held 55.51% of the total share in 2025, while animal feed is poised for a 5.01% CAGR from 2026 to 2031.

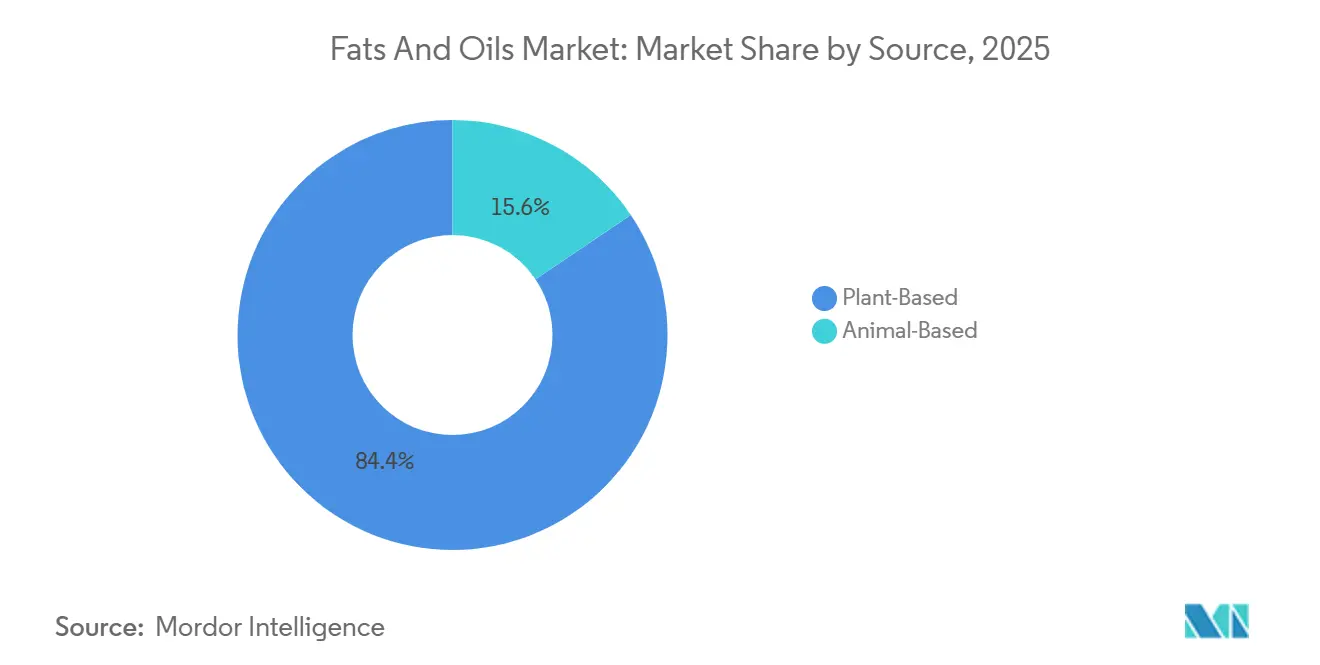

- By source, plant-based products accounted for 84.43% of the market in 2025, and animal-based products posted the fastest 6.43% CAGR for the forecast period (2026-2031).

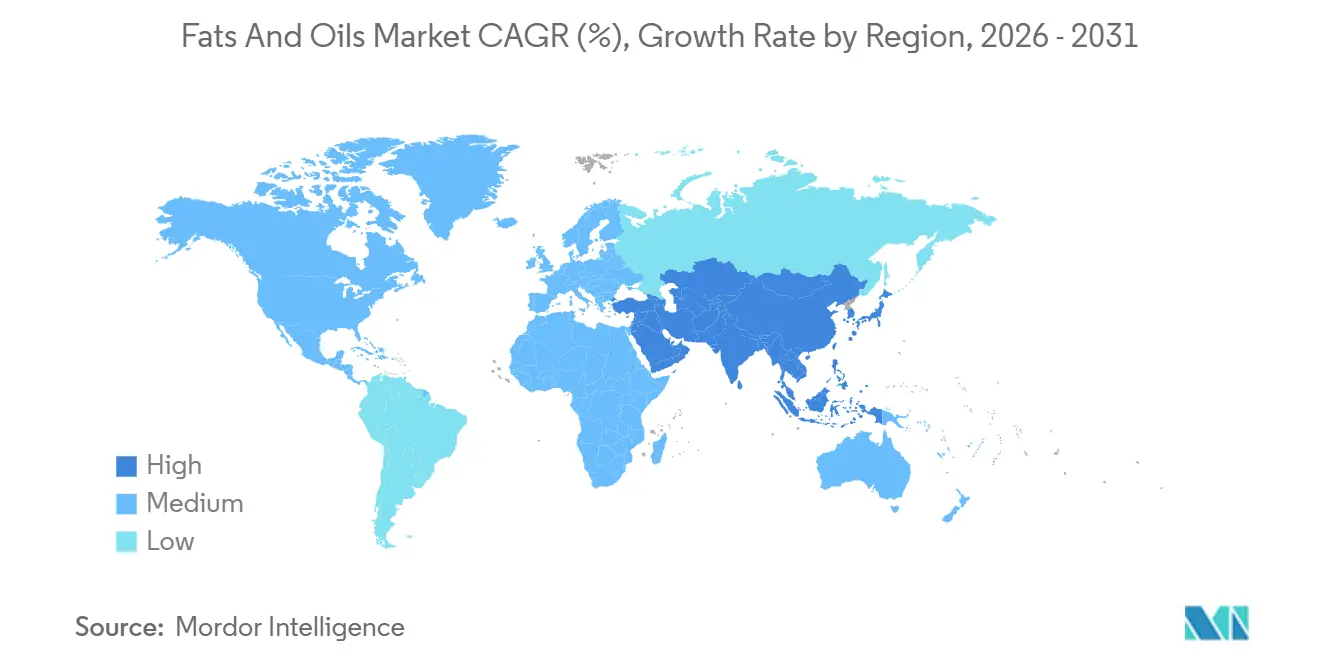

- By geography, Asia-Pacific commanded a 39.89% share of the market in 2025, and the Middle East and Africa are projected to be the fastest-growing regions at a 6.74% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Fats and Oils Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on Market CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Processed and Packaged Food | +1.2% | Asia-Pacific, North America | Medium term (3-4 years) |

| Expanding Applications in Biodiesel Production | +1.5% | North America, Europe, Southeast Asia | Long term (≥5 years) |

| Technological Advancements in Oil Extraction and Processing | +0.8% | Europe, North America (early adoption), Global | Medium term (3-4 years) |

| Increasing Popularity of Plant-Based Diets | +0.7% | North America, Europe, Urban Asia-Pacific | Long term (≥5 years) |

| Growth of the Food Service Industry | +0.6% | Global, with concentration in Urban Centers and Tourist Destinations | Medium term (3-4 years) |

| Growing Health Consciousness Among Consumers | +0.5% | North America, Europe, Urban Asia-Pacific | Medium term (3-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Processed and Packaged Food

Driven by a focus on functional properties and clean label demands, the processed food industry's evolution is reshaping the fats and oils market. In 2024, U.S. processed food exports hit USD 38.84 billion, with Canada, Mexico, the European Union, Japan, and South Korea as primary markets, as reported by the USDA Foreign Agriculture Service [1]Source: United States Department of Agriculture (USDA), Foreign Agricultural Service, "U.S. Processed Food Products Exports in 2024", fas.usda.gov. Manufacturers, like Cargill with its 2022 launch of coconut-based pastry margarine, are crafting specialized fats for bakery uses. These fats aim for precise melting profiles and oxidative stability, all while steering clear of trans fats. Such innovations cater to the rising consumer demand for healthier choices, enabling firms to cut down on saturated fats, uphold product quality, and strategically position their products in premium segments by highlighting enhanced functional and nutritional benefits.

Expanding Applications in Biodiesel Production

The biodiesel market is under pressure due to limited feedstock availability, which has caused production to fall short of its capacity. In the United States, 160 biodiesel plants have a combined capacity of 2.7 billion gallons per year, as reported by the Agricultural Marketing Resource Center [2]Source: Agricultural Marketing Resource Center (AgMRC), "Renewable Energy", agmrc.org . However, this capacity is not fully utilized because of feedstock constraints. To address this issue, companies are turning to alternative feedstocks like waste cooking oils (WCOs), which account for approximately 17 million tons of global supply annually. The industry has introduced advanced pretreatment technologies to improve the quality of degraded oils by reducing their free fatty acid content. These advancements not only make biodiesel production more efficient but also support circular economy practices by repurposing waste materials.

Technological Advancements in Oil Extraction and Processing

Methods like cold-press extraction, supercritical CO2 processing, and enzyme-assisted aqueous extraction are becoming more popular for producing premium oils. These techniques help preserve important compounds such as tocopherols, phytosterols, and polyphenols. According to the American Oil Chemists' Society, cold-pressed sunflower oil showed a 22% higher alpha-tocopherol recovery compared to traditional hexane extraction. This supports claims for products labeled as "virgin" and "unrefined." Additionally, technologies like membrane filtration and molecular distillation are helping to reduce refining losses and energy use. For example, AAK's Karlshamn facility in Sweden achieved a 15% reduction in steam usage per ton of refined oil by using heat integration and enzymatic degumming. These advancements not only lower production costs but also reduce carbon emissions, aligning with corporate sustainability goals and meeting consumer demand for minimally processed ingredients.

Increasing Popularity of Plant-Based Diets

The rising adoption of flexitarian and vegan diets is driving higher demand for plant-based fats in products such as dairy alternatives, meat substitutes, and egg replacers. Coconut oil and shea butter are widely used due to their saturated fat content, which helps recreate the creamy texture of dairy. High-oleic sunflower and canola oils are favored for their neutral taste, making them suitable for plant-based burgers and sausages. According to the U.S. Department of Agriculture, domestic consumption of coconut oil grew by 8% in 2024, with food manufacturers now contributing 65% of the total usage, up from 52% in 2020. Furthermore, oat milk and almond milk producers are incorporating sunflower lecithin and rapeseed oil to enhance emulsion stability and texture. These plant-based ingredients are increasingly replacing traditional dairy fats in coffee creamers and yogurt alternatives.

Restraints Impact Analysis*

| Restraint | (~) % Impact on Market CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fluctuating Raw Material Prices and Supply Chain Disruptions | -0.9% | Import-dependent regions worldwide | Short term (≤2 years) |

| Health Issues Associated with Trans-Fats Consumption | -0.6% | Regions with strict regulations | Medium term (3-4 years) |

| Strict Government Regulations on Trans-Fat Content | -0.7% | North America, Europe, Progressive Asian Economies | Medium term (3-4 years) |

| Environmental Concerns Related to Palm Oil Production | -0.5% | Europe, North America, Environmentally Conscious Markets | Long term (≥5 years) |

| Source: Mordor Intelligence | |||

Fluctuating Raw Material Prices and Supply Chain Disruptions

In April 2025, the FAO oilseed price index rose by 3.7 points (3.5%) compared to the previous month, reaching its highest level in eleven months. Meanwhile, the oilmeal and vegetable oil indices dropped by 1.1 points (1.2%) and 3.7 points (2.3%) respectively. The oils and fats market continues to face significant challenges, driven by factors such as the Russia-Ukraine conflict, which has disrupted sunflower oil supplies, and labor shortages in Malaysia, which have impacted palm oil production. To address these issues, food manufacturers are making adjustments by reformulating products, sourcing oils from different suppliers, and using flexible formulations that allow ingredient substitutions. These ongoing disruptions and supply chain issues are expected to influence market trends and pricing in the near future.

Health Issues Associated with Trans-Fats Consumption

The World Health Organization (WHO) has intensified its efforts to eliminate trans fats globally, leading to significant regulatory changes. So far, 58 countries have implemented strict policies, affecting 47% of the global population. These regulations require manufacturers to replace partially hydrogenated oils (PHOs) with alternatives that can perform the same functions. In the United States, the FDA's final rule, effective December 22, 2023, officially banned PHOs as optional ingredients in food standards. It also revoked previous approvals for their use in products such as margarine, shortening, and bread. This regulatory push has driven innovation in fat structuring technologies. One notable advancement is enzymatic interesterification, which allows the production of trans-fat-free alternatives with specific functional characteristics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Oils Dominate and Outpace Growth

In 2025, the oils segment held a leading 54.92% share of the market and is expected to grow at a faster pace than the overall market, with a projected CAGR of 5.44% from 2026 to 2031, compared to the market's growth rate of 4.42%. This strong growth is driven by the extensive use of vegetable oils across food and industrial applications, especially in biodiesel production. The importance of this segment is evident from significant investments in processing facilities, such as the upcoming oilseed crushing plant near Perth, Australia, developed by Cargill and CBH Group.

The fats segment, although smaller in market share, is seeing notable progress in the development of specialty products. Manufacturers are focusing on creating fats with specific functional benefits while removing trans fats. For example, in September 2024, Volac Wilmar introduced Mega-Fat 70, a rumen-protected fat product designed for dairy cattle. This product, which contains 70% palmitic and 20% oleic fatty acids, is aimed at improving milk production and supporting cattle health.

By Application: Food Sector Leads While Animal Feed Accelerates

In 2025, the food application segment dominated the market with a 55.51% share, emphasizing the importance of fats and oils in processed foods. These components play a vital role in enhancing texture, flavor, and shelf-life. Confectionery, bakery, and dairy products are key contributors to this growth, as manufacturers develop customized fat solutions to meet specific functional demands. Advances in enzymatic interesterification technology have made it possible to produce fats with unique crystallization properties, particularly benefiting high-quality confectionery products. The segment's leading position is driven by the essential role of fats and oils in determining the structure and taste of processed foods.

The animal feed segment is projected to grow at the highest rate, with a CAGR of 5.01% during the forecast period of 2026-2031. This growth is fueled by increasing meat consumption in developing regions and the rising use of fats as energy-dense feed components to improve feed efficiency. Meanwhile, the industrial segment is expanding due to the growing demand for vegetable oils in biodiesel production. However, this increased industrial demand creates competition with food applications, which in turn influences market prices.

By Source: Plant-based Dominates Despite Animal-based Growth

In 2025, plant-based sources are expected to dominate the market, accounting for 84.43% of the share, with vegetable oils leading in both food and industrial uses. Palm oil remains a key player in the global oils market, with prices likely to stay high until mid-2025 due to limited supply and growing demand. Cargill's decision to supply only RSPO-certified palm oil from its U.S. refineries highlights the market's increasing focus on sustainable sourcing[3]Source: Cargill Incorporated, "Cargill’s U.S. oil refineries connect all customers to 100% RSPO-certified palm oil", cargill.com. Soybean oil continues to play a significant role, with Ventura Foods—a joint venture between CHS and Mitsui & Co.—using about 2 billion pounds of edible oils annually, primarily soybean oil, due to its affordability and wide availability.

The animal-based segment, which holds 15.57% of the market share in 2025, is projected to grow at a CAGR of 6.43% from 2026 to 2031. This growth is driven by the rising recognition of the functional benefits of animal fats in specific applications and their critical role in biodiesel production. Innovations like Volac Wilmar's Mega-Fat 70, designed for dairy cattle, showcase the segment's progress. Additionally, Cargill's acquisition of two meat plants from Ahold Delhaize USA reflects its strategy to expand its animal-based product offerings and improve operational efficiency through better value chain integration.

Geography Analysis

In 2025, Asia-Pacific is expected to hold a dominant 39.89% share of the global oils and fats market. This is mainly due to its strong palm oil production and the growing food processing industry. Indonesia and Malaysia play key roles in shaping global market trends through their palm oil industries. The Malaysian Palm Oil Board predicts that crude palm oil prices will range between MYR 4,000 and MYR 4,300 per ton in 2025. Additionally, Indonesia's upcoming 40% biodiesel blending mandate (B40) is likely to impact the global palm oil supply and keep prices high throughout 2025. In India, Adani Wilmar plans to expand its distribution network to 1 million direct outlets within three years, focusing on rural areas, which highlights the region's improving distribution infrastructure.

The Middle East and Africa are forecasted to grow at the fastest rate, with a 6.74% CAGR from 2026 to 2031, despite having a smaller market share currently. This growth is driven by advancements in food processing, increased biodiesel usage, and rising edible oil consumption. North America and Europe remain key markets. In the U.S., the growing biodiesel industry is boosting demand for vegetable oils. Farmers are increasing canola production to meet renewable fuel needs, supported by investments from energy and agriculture companies in farming and processing infrastructure. In Europe, regulations on trans fats and sustainability are encouraging the development of healthier fat alternatives.

South America continues to play a crucial role in the global supply chain through its soybean oil production, with Brazil's agricultural sector making significant contributions to global exports. Cargill's acquisition of SJC Bioenergia in Brazil strengthens its renewable energy operations, showing the increasing link between renewable energy and the oils and fats market. These regional developments underline the interconnected nature of the global market, where policy changes, such as Indonesia's biodiesel mandates, can have a significant impact on global prices and supply availability.

Competitive Landscape

The global oils and fats market is moderately fragmented, creating a competitive environment where regional companies compete effectively with multinational corporations in specific segments. Leading players like Cargill Incorporated, Bunge Limited, and ADM focus on strengthening their supply chains and improving profit margins through vertical integration. These companies are also prioritizing sustainability, as seen in Cargill's commitment to offering only RSPO-certified palm oil from its U.S. refineries.

In addition, companies are investing in advanced technologies, such as enzymatic interesterification, to produce specialty fats with better nutritional value. The market is also witnessing changes driven by acquisitions, such as KD Pharma Group's purchase of DSM-Firmenich's marine lipids business, including the MEG-3 brand and facilities in Peru and Canada, in July 2024.

While large corporations hold a significant share of the market, smaller players are thriving in niche segments, particularly in specialty oils with unique functional or nutritional benefits. In these areas, being able to quickly meet customer demands and adapt operations often gives smaller companies an edge over larger competitors.

Fats and Oils Industry Leaders

-

Cargill Incorporated

-

Bunge Limited

-

Fuji Oil Holding Inc.

-

Archer Daniels Midland Company

-

Olam Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Bertolli is expanded into the butter and spreads category with the launch of Bertolli Spreadable with Butter and Olive Oil, a new four-ingredient blend combining dairy butter and olive oil. The new product, positioned as a Mediterranean-inspired alternative in the spreads segment, contains 57% dairy butter, 23% olive oil, water and salt.

- May 2026: Russian investors announced their plans to launch sunflower oil production in the Chui Region. According to the proposed project, the facility will be able to produce up to 400 tons of refined sunflower oil per day. The plant plans to use modern cold-refining technologies.

- April 2026: Olam Agri launched Mama’s Pride Soya Oil, a refined, heart-healthy cooking oil designed to meet the evolving nutritional needs of Nigerian households. The product comes in a variety of convenient SKUs to suit different household and commercial needs, including PET bottles in 500ml, 1L, and 2L; pouches in 350ml and 1L; and a 25L keg.

- January 2026: Corteva Inc and BP launched Etlas, its new 50:50 joint venture that will produce oil from crops, including canola, mustard, and sunflower, for use in the production of biofuels like sustainable (or synthetic) aviation fuel (SAF) and renewable diesel (RD).

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the fats and oils market as the total value of plant- and animal-derived triglycerides sold in crude, refined, or fractionated form for food, feed, oleochemical, and energy uses within formal supply chains. The valuation is expressed in constant 2025 US dollars at manufacturer gate prices.

Scope exclusion: Synthetic esters, paraffin-based lubricants, and isolated omega-3 EPA/DHA concentrates fall outside our coverage.

Segmentation Overview

-

By Type

-

Fats

- Butter

- Tallow

- Lard

- Specialty Fats

-

Oils

- Soybean Oil

- Rapeseed Oil

- Palm Oil

- Coconut Oil

- Olive Oil

- Cotton Seed Oil

- Sunflower Seed Oil

- Others

-

Fats

-

By Application

-

Food

- Confectionary

- Bakery

- Dairy Products

- Others

- Industrial

- Animal Feed

-

Food

-

By Source

- Plant-based

- Animal-based

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- France

- United Kingdom

- Spain

- Netherlands

- Italy

- Sweden

- Poland

- Belgium

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Indonesia

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Chile

- Columbia

- Peru

- Rest of South America

-

Middle East & Africa

- United Arab Emirates

- South Africa

- Nigeria

- Saudi Arabia

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conduct structured interviews and online surveys with crushers, refiners, packaged-food formulators, biofuel blenders, and agri-commodity traders across Asia-Pacific, Europe, the Americas, and MEA. These conversations validate utilization rates, average selling prices, regulatory inflection points, and forward purchase intentions that secondary data alone cannot reveal.

Desk Research

Our team first assembles production, trade, and consumption fundamentals from widely trusted public datasets such as FAOSTAT, USDA PSD, UN Comtrade, OECD-IEA biofuel outlooks, and WHO nutrition statistics, which give baselines for volumes, price trends, and dietary drivers. Complementary context is gathered from regional trade associations (e.g., FEDIOL, American Soybean Association), customs tariff updates, and peer-reviewed journals tracking processing yields and functional ingredient shifts. To enrich the quantitative core, we parse company filings, investor decks, and reliable press carried on Dow Jones Factiva; firm-level margins and capacity notes are checked in D&B Hoovers. This list is illustrative, not exhaustive, and many additional open and paid sources support data checks.

Market-Sizing & Forecasting

A top-down reconstruction starts with national oilseed crush, rendered fat output, and import-export balances; apparent availability is then aligned with end-use penetration pools (food, feed, industrial) to yield the demand stack. Selective bottom-up cross-checks, sampled supplier roll-ups and channel ASP × volume probes, fine-tune totals. Core variables guiding the model include crush yield ratios, biodiesel mandate percentages, disposable-income indexed edible-oil intake, urban foodservice expansion, and tariff differentials.

Forecasts to 2030 employ multivariate regression that links these drivers to historical value swings, with scenario analysis layering policy or weather shocks. Gaps in bottom-up granularity are bridged by regional proxies and expert consensus before final calibration.

Data Validation & Update Cycle

Outputs undergo three-step variance scans, senior analyst peer review, and sanity checks against external price and trade signals. The study refreshes annually, while material events (for example, harvest shortfalls or policy shifts) trigger interim revisions so clients always access the newest view.

Why Mordor's Fats and Oils Baseline Commands Reliability

Published estimates frequently diverge because firms differ in product mix choices, pricing anchors, and refresh cadence. By centering on triglycerides destined for recorded commercial channels and by indexing all values to constant-year dollars, we reduce double counts and currency noise.

Key gap drivers versus other publishers include our exclusion of specialty nutraceutical lipids, a balanced base-case forecast rather than aggressive demand-push scenarios, and an annual refresh backed by fresh primary inputs.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 116.7 B (2025) | Mordor Intelligence | - |

| USD 271.8 B (2024) | Global Consultancy A | Includes personal-care oleochemicals and assumes uniform ASP escalation without primary validation |

| USD 268.8 B (2024) | Trade Journal B | Uses single-factor price inflation on baseline volumes; limited regional primary checks |

| USD 169.4 B (2024) | Regional Consultancy C | Covers only packaged edible oils yet applies global growth multipliers, creating scope-method mismatch |

In short, our disciplined source selection, mixed-method modeling, and tight update rhythm give decision-makers a balanced, transparent baseline that is traceable to clear variables and repeatable steps.

Key Questions Answered in the Report

What is the projected oils and fats market size for 2031?

The Fats and Oils Market size is expected to reach roughly USD 144.90 billion by 2031, based on current growth forecasts.

Which source type leads the market in 2025?

Plant-based source type leads the market with the largest market share of 84.43% in 2025.

Why is Asia-Pacific so influential in the oils and fats market?

The region combines dominant palm production with expanding consumption in large economies, creating both supply and demand leadership.

How have trans-fat regulations shaped product reformulation?

Global bans on partially hydrogenated oils prompted widespread adoption of enzymatic interesterification, enabling comparable functionality without trans fats.

Page last updated on: