Corn Oil Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

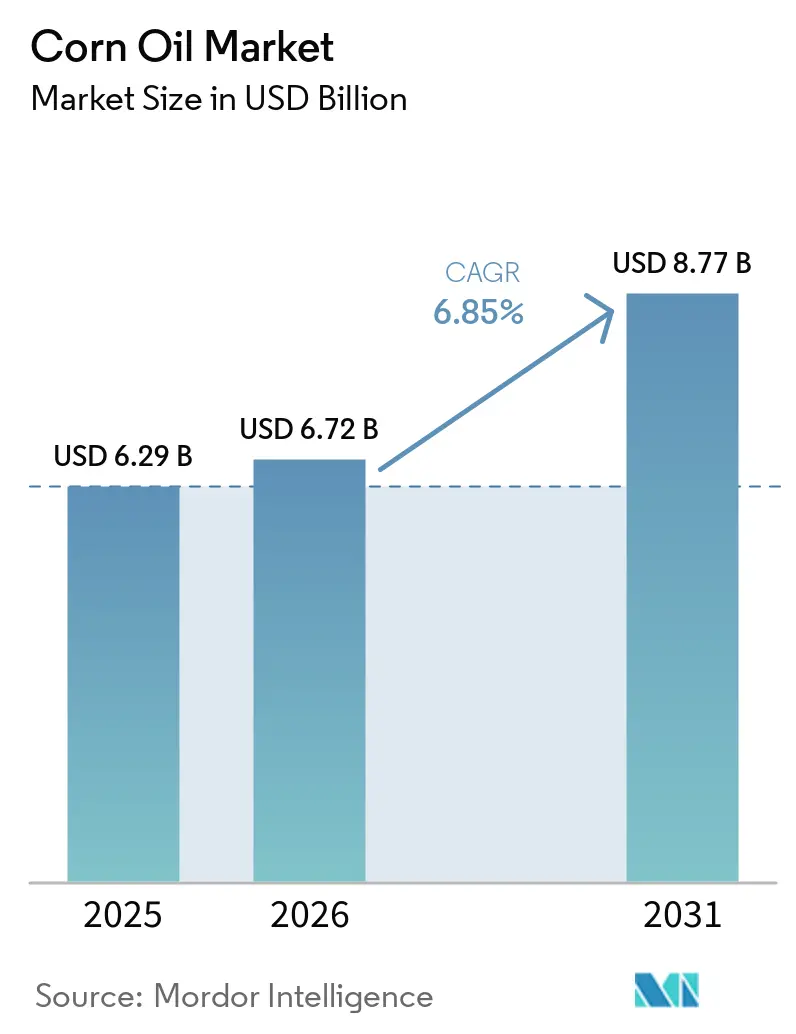

| Market Size (2026) | USD 6.72 Billion |

| Market Size (2031) | USD 8.77 Billion |

| Growth Rate (2026 - 2031) | 6.85% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Corn Oil Market Analysis by Mordor Intelligence

The Corn Oil Market size was valued at USD 6.29 billion in 2025 and is estimated to grow from USD 6.72 billion in 2026 to reach USD 8.77 billion by 2031, at a CAGR of 6.85% during the forecast period (2026-2031). Corn oil remains in demand due to its use in food and renewable diesel production. In the U.S., changing "healthy" labeling rules have made it more appealing to consumer-packaged-goods makers. From 2022 to 2025, renewable diesel production doubled, increasing the use of distiller's corn oil in biofuels and reducing price volatility linked to food demand. Quick-service restaurants favor corn oil for its 450 °F smoke point, which extends fry life, and its neutral flavor, which ensures consistent menus. Breeding programs are also creating high-oleic and tocotrienol-rich hybrids, opening premium markets with higher margins. These factors stabilize margins despite feedstock price changes and drive ongoing investments by refiners, ethanol plants, and food manufacturers in corn oil extraction technology.

Key Report Takeaways

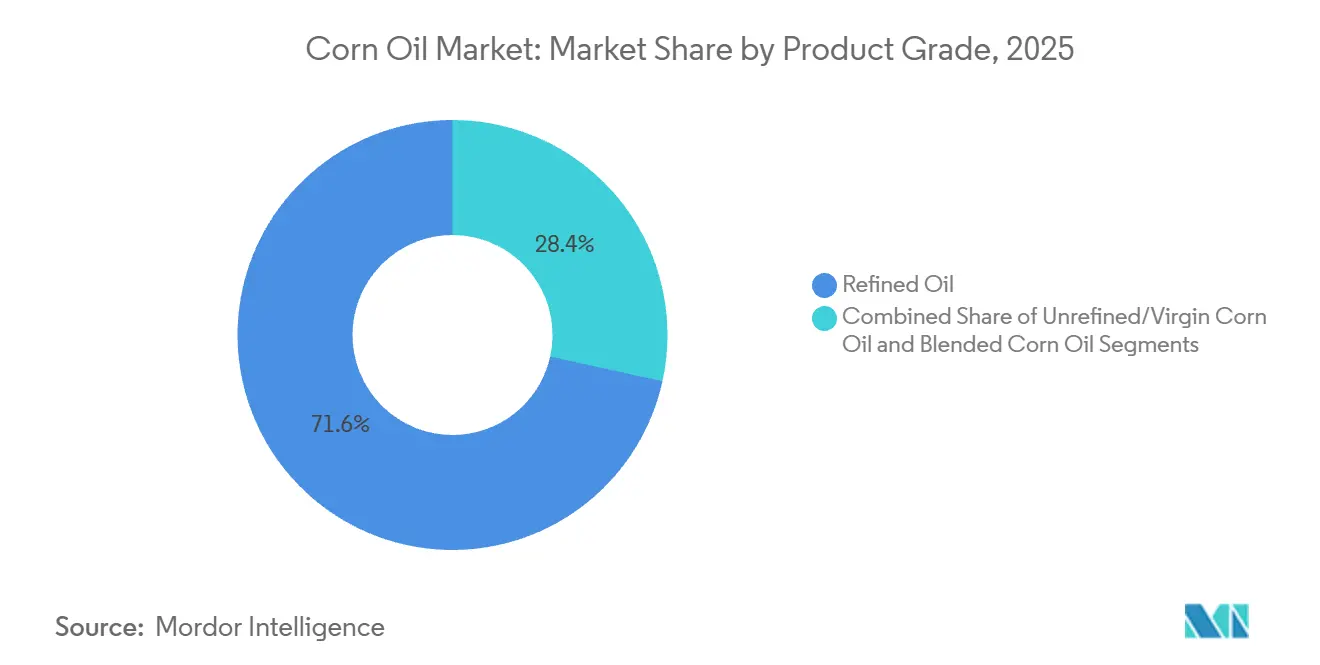

- By product grade, refined corn oil led with 71.55% of the corn oil market share in 2025, and blended formulations are projected to expand at a 7.06% CAGR through 2031.

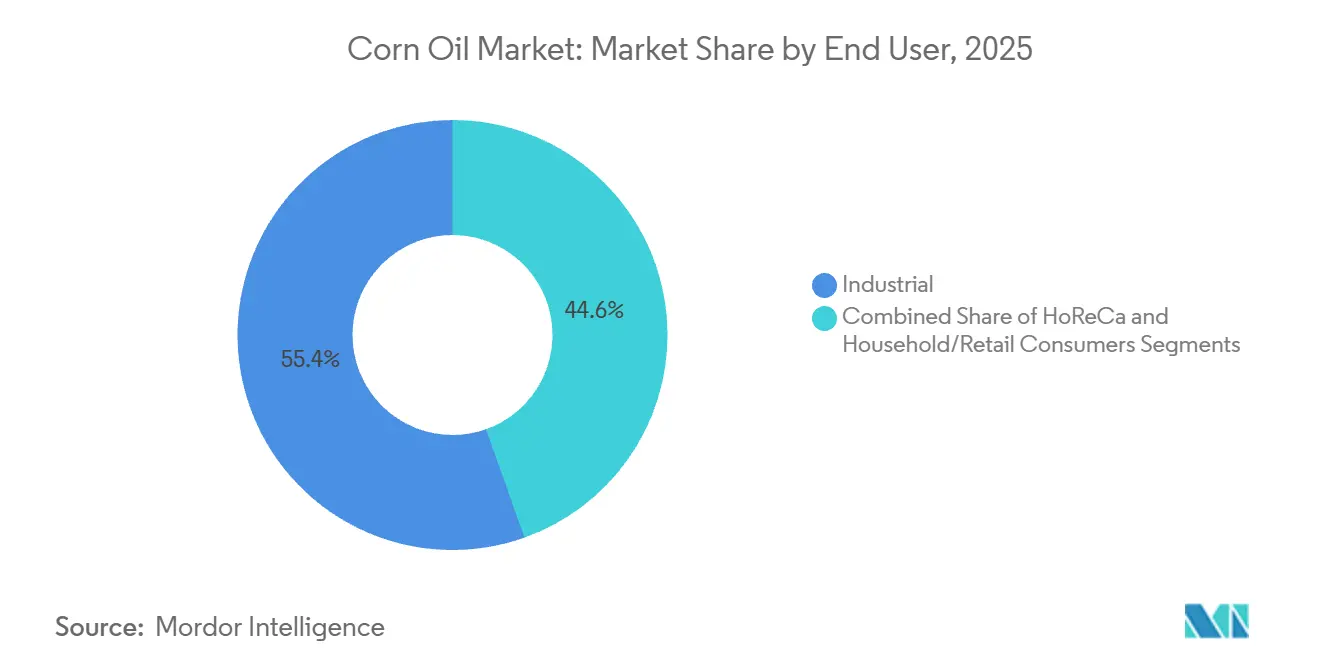

- By end user, the industrial segment accounted for 55.43% of the corn oil market size in 2025, and HoReCa is forecast to record a 7.85% CAGR between 2026 and 2031.

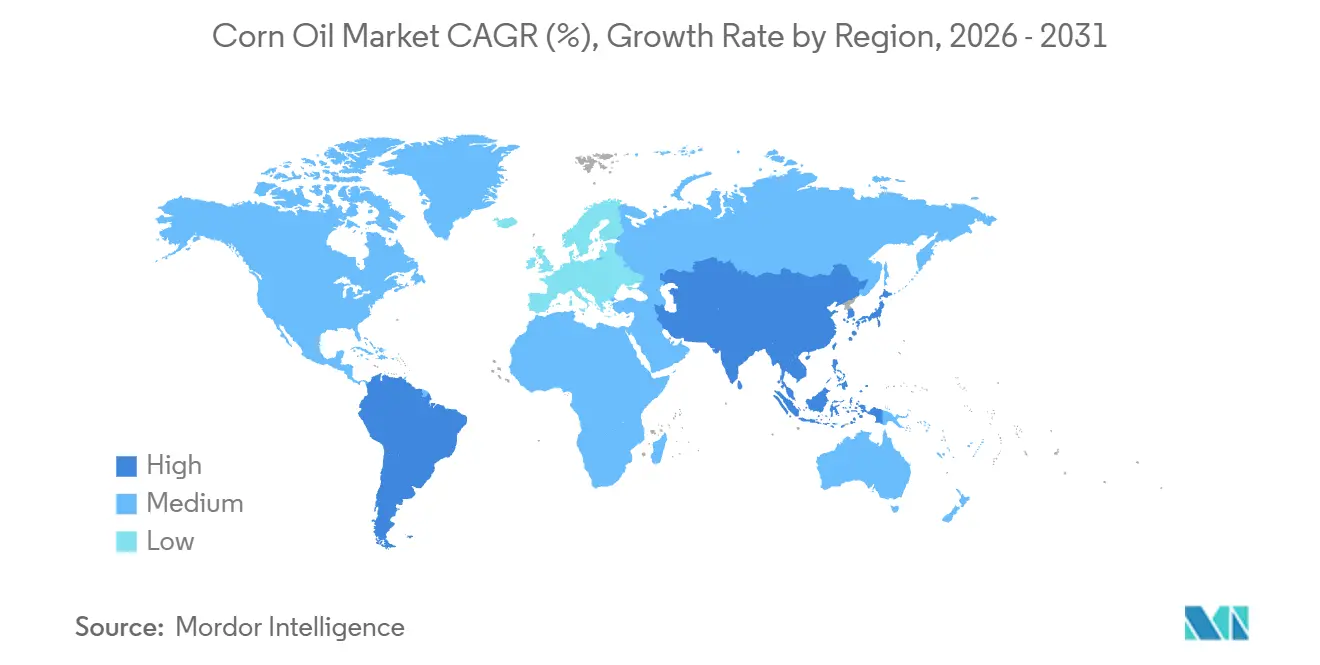

- By geography, North America held 37.74% of the corn oil market share in 2025, and the Asia-Pacific is set to grow at a 7.33% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Corn Oil Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Processed and packaged foods are increasingly favoring heart-healthy edible oils | +1.2% | Global with focus on North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Distillers are ramping up their corn oil usage, due to bio- and renewable-diesel blending mandates | +1.8% | North America (primary), Europe (emerging), Brazil (nascent) | Short term (≤ 2 years) |

| Quick-service restaurants are pivoting to oils with higher smoke points for frying | +0.9% | North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Emerging markets are witnessing a boom in packaged and convenience foods | +1.4% | Asia-Pacific, South America, Middle East & Africa | Long term (≥ 4 years) |

| High-oleic and tocotrienol-rich hybrids are being commercialized, carving out premium niches for corn oil | +0.7% | North America, Europe, Japan | Long term (≥ 4 years) |

| Rise of organic and non-GMO corn oil segments | +0.5% | North America, Western Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Processed and Packaged Foods Favoring Heart-Healthy Edible Oils

Driven by heightened consumer awareness of cardiovascular health risks, food manufacturers are reformulating their products, leveraging the unsaturated fat profile of corn oil as a competitive edge over palm and coconut oil. Dietitian highlights the FDA's endorsement of a qualified health claim for oils, including high-oleic corn oil, that boast at least 70% oleic acid content, bolstering its heart-health narrative[1]Source: Today’s Dietitian, “New Qualified Health Claim for Oils High in Oleic Acid,” todaysdietitian.com. Food processors are increasingly turning to corn oil for shelf-stable applications, capitalizing on its superior oxidative stability over other vegetable oils, all without the need for hydrogenation. This momentum is further fueled by manufacturers catering to a growing consumer preference for clean-label products, steering clear of trans fats and artificial preservatives. The packaged foods industry's pivot towards corn oil underscores a broader acknowledgment: cardiovascular health claims not only meet regulatory standards but also command premium pricing in the market.

Distillers Ramping Up Corn Oil Usage Due to Bio- and Renewable-Diesel Blending Mandates

Renewable diesel capacity growth is rapidly shifting distillers corn oil (DCO) from animal feed to fuel markets. The EPA's Renewable Fuel Standard set the 2026 biomass-based diesel target at 3.35 billion gallons, with D4 RINs trading above USD 1.00 per gallon in early 2026. This has pushed ethanol plants to maximize oil extraction. In 2025, POET's 35 facilities produced 1 billion pounds of corn oil, all allocated for renewable diesel. POET's January 2026 announcement of a Shelbyville expansion aims to add 72 million pounds annually by late 2027. Alto Ingredients' Pekin, Illinois facility extracted 78,000 tons of corn oil in 2025, a sharp rise after centrifuge upgrades. Valero's ethanol segment reported DCO prices increasing to USD 0.58 per pound in 2025 from USD 0.48 in 2024, a 21% rise due to renewable diesel agreements. The price gap between feed-grade and fuel-grade DCO is reshaping dry-mill economics, disadvantaging facilities without oil-extraction centrifuges as DCO values now exceed distillers grains premiums.

Quick-Service Restaurants Pivoting to Higher Smoke-Point Frying Oils

QSR chains prioritize oils that ensure consistent flavors and withstand long frying cycles without forming off-flavors or excessive polar compounds. Refined corn oil, with a smoke point of 232°C (450°F), offers a cost-performance balance, sitting between soybean oil and high-oleic sunflower or canola oils. Studies show conventional corn oil, with over 50% linoleic acid, produces more volatile aldehydes and oxidized compounds after 75 frying cycles at 180°C, requiring frequent oil changes or filtration. To address this, QSR operators blend corn oil with canola or high-oleic soybean oil, as seen in Conagra's Mazola Corn Plus, which extends fry life while maintaining brand identity. This trend is dividing the market: pure refined corn oil remains popular in retail and light-duty foodservice, while blended and high-oleic oils dominate high-volume frying operations.

Rise of Organic and Non-GMO Corn Oil Segments

Certification premiums and retailer mandates are driving distinct supply chains for organic and non-GMO corn oil, but growth is limited by the small amount of certified corn acreage and the costs of identity-preserved handling. USDA organic certification requires corn to be grown without synthetic pesticides or GMOs, yet organic corn acreage in the U.S. remains minimal, concentrated in regions like the Upper Midwest where segregation infrastructure exists. Non-GMO Project Verified labeling appeals to health-conscious consumers and supports retailer private-label strategies in natural and organic markets, but it increases costs for processors who must source non-GMO corn, maintain separate processing lines, and undergo audits. Organic corn oil typically costs 30–50% more than conventional grades, limiting sales to specialty grocers and e-commerce. Growth is driven by brand differentiation, as smaller oil marketers use organic and non-GMO certifications to secure premium shelf space, targeting consumers who value transparency and are less price-sensitive.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Corn feedstock price volatility linked to weather and trade shocks | -0.8% | Global, with acute exposure in North America (primary corn belt), Argentina, Brazil | Short term (≤ 2 years) |

| Intense price competition from substitute soybean, canola, and palm oils | -1.1% | Global, especially Asia-Pacific (palm), Europe (canola), South America (soy) | Medium term (2–4 years) |

| Regulatory uncertainty regarding health claims and biodiesel mandates | -0.4% | North America (EPA RFS, FDA), Europe (EU RED III, EFSA), Brazil (ANP) | Medium term (2–4 years) |

| Oxidative instability and formation of harmful compounds during frying | -0.6% | Global, with heightened scrutiny in Europe (EFSA limits on polar compounds), North America (FDA GRAS reviews) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Intense Price Competition from Substitute Soybean, Canola, and Palm Oils

In the vegetable oil market, high substitutability often leads to downward pressure on corn oil prices whenever alternative oils are more cost-effective. With soybean oil commanding a 60% share of the U.S. seed oil market, it enjoys scale economies that corn oil producers find hard to replicate. Meanwhile, palm oil, benefiting from tropical production advantages, can price aggressively on the international stage, as highlighted by Farm Progress. According to World Grain, the U.S. is expanding its soybean crush capacity, processing 6 million tons in November 2024, marking a 5.4% year-over-year increase[2]Source: World Grain, “U.S. Soybean Crush Capacity on the Rise,” world-grain.com. This boost in capacity not only augments the soybean oil supply but also intensifies competitive pressures. Canola oil, sharing a similar fatty acid profile with corn oil, directly competes for health-conscious consumers. At the same time, palm oil's cost edge poses a challenge to corn oil in industrial applications where price sensitivity reigns. For corn oil to maintain its premium positioning, it must showcase performance or health benefits that convincingly justify its higher price over commodity alternatives.

Regulatory Uncertainty Regarding Health Claims and Biodiesel Mandates

Shifting policies on heart-health labeling and renewable fuel volumes create uncertainty in demand forecasts and investment decisions. The U.S. FDA has not approved a qualified health claim for corn oil, unlike canola or olive oil, limiting marketers to less impactful messaging about vitamin E and phytosterols. In biodiesel, the EPA's Renewable Volume Obligations (RVOs) under the Renewable Fuel Standard face political and legal challenges. The 2026 biomass-based diesel mandate of 3.35 billion gallons was finalized only after litigation over previous shortfalls, complicating planning for ethanol producers investing in DCO extraction. Europe's RED III directive adds sustainability criteria favoring waste and advanced feedstocks over crop-based oils, potentially restricting corn oil's use in renewable diesel in EU markets. This fragmented regulation forces corn oil suppliers to balance edible and fuel markets without assurance of profitable demand in either channel.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Grade: Refined Oil Dominates Processing Applications

In 2025, refined corn oil dominated the market with a 71.55% share, driven by its cost-effectiveness and versatility in industrial frying, retail bottling, and ingredient use. Its neutral flavor and long shelf life outweigh the nutrient losses from refining. The refining process removes impurities like free fatty acids and pigments, producing oil with peroxide values below 1.0 meq/kg and free fatty acid content under 0.05%, meeting food-grade standards. Its high smoke point (around 232°C) and low oxidation make it ideal for foodservice, reducing oil changes and labor costs. In retail, its 10–20% lower price compared to canola or high-oleic sunflower oil appeals to budget-conscious consumers. Unrefined and virgin corn oils, rich in nutrients, remain niche products due to their darker color, stronger flavor, and lower smoke points, limiting their use in industrial and mainstream foodservice settings.

Blended corn oil formulations are forecast to grow at 7.06% CAGR during 2026-2031, the fastest rate among product grades, as processors engineer fatty-acid profiles to balance oxidative stability, cost, and functional performance. These products typically merge corn oil with other vegetable oils, striking a balance between cost and performance for specific applications. The premium pricing of unrefined grades highlights a consumer trend: a readiness to invest more for perceived naturalness and the retention of nutrients. This trend persists even in the face of limited scientific backing for health benefits over their refined counterparts. Cargill's proactive move to eliminate industrially produced trans-fatty acids from its global edible oils portfolio underscores a broader industry commitment to health-centric product development[3]Source: Cargill, “High Oleic Oils Portfolio,” cargill.com. Furthermore, advancements in processing technology are refining extraction methods, ensuring they not only uphold beneficial compounds but also align with stringent food safety standards. This evolution bolsters the growth trajectory of premium corn oil segments.

By End User: Industrial Applications Drive Volume Growth

In 2025, the industrial segment commands a 55.43% share of the corn oil market, underscoring its varied applications. These range from biodiesel production and animal feed supplements to processes in chemical manufacturing. Among these, biodiesel and biofuel applications are the most rapidly expanding. Notably, the production capacity for renewable diesel is set to double from 2022 to 2025, driving a consistent demand for corn oil feedstocks, as highlighted by the U.S. Energy Information Administration[4]Source: U.S. Energy Information Administration, “U.S. Renewable Diesel Capacity Surpasses Biodiesel,” eia.gov. Within the industrial realm, the food and beverage sector plays a pivotal role. Processed foods, in particular, lean on corn oil for its neutral flavor and extended shelf stability. Meanwhile, the pharmaceutical and cosmetic industries tap into corn oil's emollient properties and biocompatibility, albeit in smaller volumes compared to its fuel and food uses.

The HoReCa (foodservice) sector is expected to grow at a 7.85% CAGR from 2026 to 2031, the fastest among end-user segments. This growth is driven by quick-service restaurants and institutional kitchens switching from partially hydrogenated oils to non-GMO or blended formulations that balance cost, performance, and health benefits. In June 2024, the EPA approved POET Shelbyville's RFS pathway, recognizing corn oil as a coproduct of dry-mill ethanol and requiring strict monitoring of feedstock and energy flows. This approval supports DCO's dual-use potential and helps ethanol plants optimize coproduct use between fuel and food markets. Foodservice growth is also supported by QSR chains using blended corn-canola oils, which last longer for frying and reduce harmful compounds compared to pure soybean or corn oils. Studies show oils with balanced PUFA and MUFA content produce fewer harmful byproducts after 50+ frying cycles at 180°C.

Geography Analysis

In 2025, North America led the corn oil market with a 37.74% share, supported by 15 billion bushels of corn, over 200 ethanol plants, and well-funded crushers. U.S. renewable fuel standards and Canada's Clean Fuel Regulations drive demand, while efficient logistics in the Corn Belt keep costs competitive despite tighter ocean-freight spreads. However, export challenges persist as Brazil's safrinha crop grows and Asian buyers diversify suppliers.

Asia-Pacific is expected to grow fastest, with a 7.33% CAGR through 2031. India's ethanol blending policy has shifted it from a corn exporter to a major domestic consumer, creating demand for corn oil coproducts. China's processed food industry increasingly uses neutral-flavored oils, while Indonesia and Malaysia expand biodiesel programs, potentially incorporating corn oil. Supply gaps are boosting imports from the Americas, highlighting trade dependencies. Europe sees steady mid-single-digit growth, driven by Renewable Energy Directive targets and food-safety standards favoring traceable oils. Anti-dumping measures on Chinese biodiesel have also increased European demand for North American corn oil, strengthening trans-Atlantic trade.

Partnerships like the Bunge-Repsol program are improving feedstock security and reducing risks from corn-price changes. While olive oil traditions in Southern Europe limit corn oil's market share, industrial demand is growing. Brazil's Mato Grosso is expanding corn ethanol production, creating domestic extraction opportunities that could challenge U.S. exporters. Local crushers are exploring Argentina's untapped capacity and lower labor costs, positioning it as a potential supplier for Asia. The Middle East and Africa show promise as urbanization boosts packaged-food demand, though infrastructure and currency issues limit short-term growth.

Competitive Landscape

The corn oil market is highly consolidated, with ADM, Cargill, Bunge, Louis Dreyfus, and Wilmar dominating the corn oil market, controlling a large share of global crushing and refining capacity. Their strong farm networks secure grain directly from the source, while multi-seed plants switch between soybean, canola, and corn based on margins. Integrated trading desks help manage price risks, stabilizing earnings despite commodity volatility.

Industry strategies focus on vertical integration and renewable-fuel diversification. For instance, Chevron and Bunge's joint venture ensures a steady supply of low-carbon feedstock for Chevron’s diesel units, strengthening ties between oil companies and agribusinesses. Louis Dreyfus opened a 320,000 metric ton plant in Ohio, signaling confidence in North America's biofuel market. Meanwhile, ADM reduced its trading operations in China, cutting 700 jobs to focus on higher-margin special oil products.

Regional players like Flint Hills Resources, POET, and Green Plains are improving profitability by using enzymatic recovery to enhance distillers' corn oil streams, reducing costs compared to larger competitors. Specialty producers target health-conscious consumers in Europe and North America with organic, non-GMO, and high-oleic products. Equipment suppliers like Alfa-Laval and GEA offer modular systems that help mid-scale ethanol plants integrate oil recovery, lowering entry barriers. The market combines the purchasing power of major players with innovations from smaller, tech-driven disruptors.

Corn Oil Industry Leaders

Archer Daniels Midland Co.

Cargill Inc.

Bunge Global SA

Wilmar International Ltd.

Louis Dreyfus Company BV

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: POET announced a USD 203 million expansion of its Shelbyville, Indiana, bioprocessing facility, doubling annual ethanol capacity from 98 million to 193 million gallons and corn oil output from 36 million to 72 million pounds, with completion targeted for Q4 2027. The project will add 20 full-time positions and create demand for an additional 32 million bushels of corn annually, strengthening POET's position as the world's largest biofuels producer and a leading supplier of corn oil for renewable diesel feedstock.

- July 2025: Flint Hills Resources committed USD 50 million to upgrade its Fairmont ethanol plant, adding technology that will yield nearly 20 million lb of distillers' corn oil annually.

- March 2025: Cenovus Energy's Minnedosa Ethanol Plant achieved full-scale distillers corn oil production, generating approximately 11,000 liters daily for renewable diesel applications.

- January 2025: Chevron and Bunge officially launched their renewable-fuel feedstock joint venture, pooling processing and refining expertise.

Global Corn Oil Market Report Scope

| Refined Corn Oil |

| Unrefined (and Virgin) Corn Oil |

| Blended Corn Oil |

| Industrial | Food and Beverage Industry |

| Biodiesel and Biofuel | |

| Pharmaceuticals | |

| Cosmetics and Personal Care | |

| Industrial and Chemical | |

| Animal Feed | |

| Household/Retail Consumers | |

| HoReCa (Foodservice) |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Grade | Refined Corn Oil | |

| Unrefined (and Virgin) Corn Oil | ||

| Blended Corn Oil | ||

| By End User | Industrial | Food and Beverage Industry |

| Biodiesel and Biofuel | ||

| Pharmaceuticals | ||

| Cosmetics and Personal Care | ||

| Industrial and Chemical | ||

| Animal Feed | ||

| Household/Retail Consumers | ||

| HoReCa (Foodservice) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the estimated value of the global corn oil market in 2026?

The market is pegged at USD 6.72 billion in 2026.

Which region is expected to post the quickest growth through 2031?

Asia-Pacific is forecast to advance at a 7.33% CAGR, the fastest among all regions.

Which product grade shows the strongest growth outlook?

Blended corn-oil formulations are projected to expand at a 7.06% CAGR through 2031.

What factor is driving the bulk of industrial corn-oil demand?

Renewable-diesel mandates are absorbing increasing volumes of distillers corn oil from ethanol plants.

Page last updated on: