Sunflower Oil Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 33.89 Billion |

| Market Size (2031) | USD 44.79 Billion |

| Growth Rate (2026 - 2031) | 5.74% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Sunflower Oil Market Analysis by Mordor Intelligence

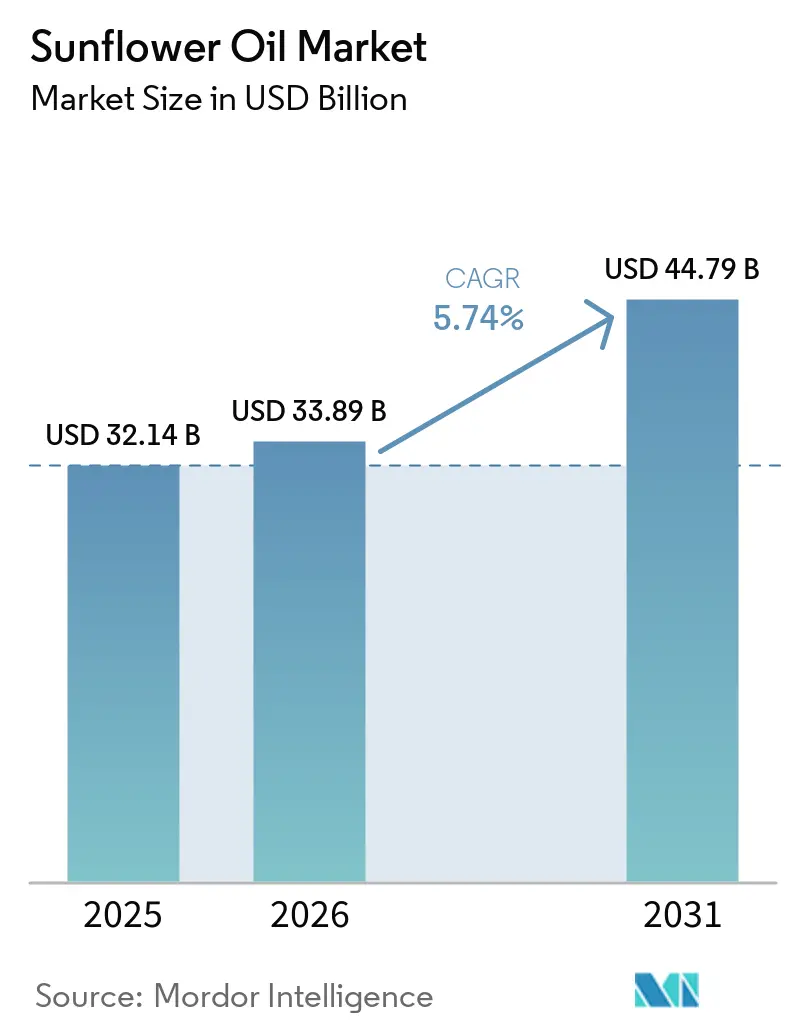

The Sunflower Oil Market size is projected to be USD 32.14 billion in 2025, USD 33.89 billion in 2026, and reach USD 44.79 billion by 2031, growing at a CAGR of 5.74% from 2026 to 2031.

The sunflower oil market growth is increasingly driven by structural shifts rather than short-term pricing trends, supported by palm oil substitution in the European Union following deforestation regulations, expanding biodiesel and renewable diesel mandates in the United States and Brazil that favor high-oleic grades, and recovering export stability from Ukraine. In the sunflower oil market, health-oriented consumer demand continues to reinforce its position as a trans-fat-free edible oil, though rising scrutiny of omega-6 content is accelerating interest in cold-pressed and high-oleic variants. At the same time, supply chain uncertainties and geopolitical risks are pushing buyers toward diversified sourcing, while intensified competition among integrated processors and agribusiness players is encouraging innovation and value-added applications beyond traditional bulk sales.

Key Report Takeaways

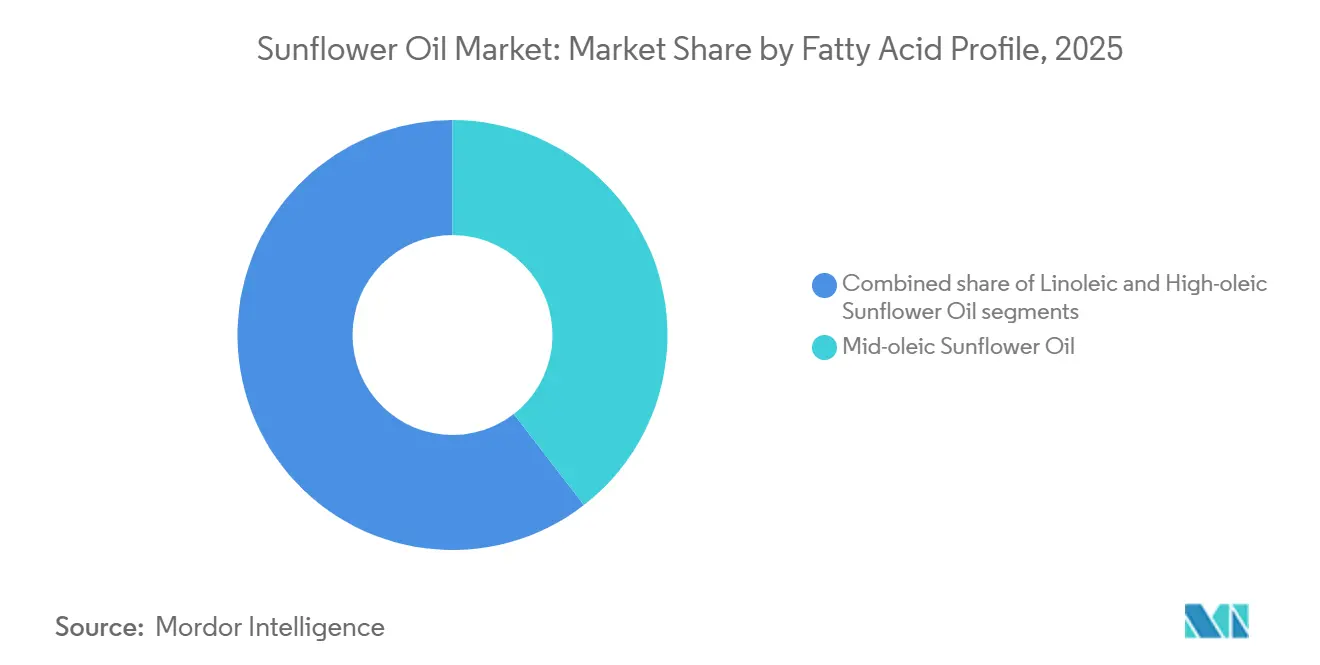

- By fatty acid profile, mid-oleic sunflower oil led with 39.52% of sunflower oil market share in 2025, while high-oleic variants are projected to grow at 6.84% CAGR to 2031.

- By processing, refined oil accounted for 65.74% share of the sunflower oil market size in 2025, while posing the segment-high 5.82% CAGR through 2031.

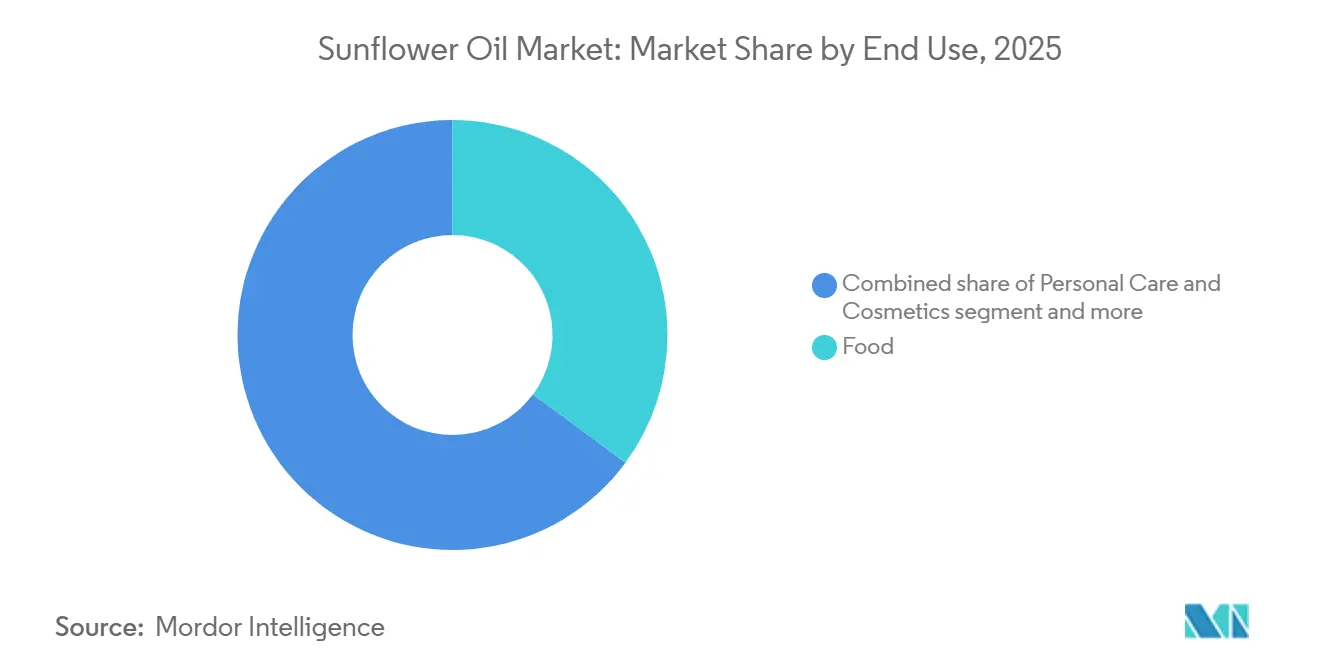

- By end use, the food industry captured 35.12% share of the sunflower oil market size in 2025; personal care and cosmetics applications register the fastest 6.72% CAGR during 2026–2031.

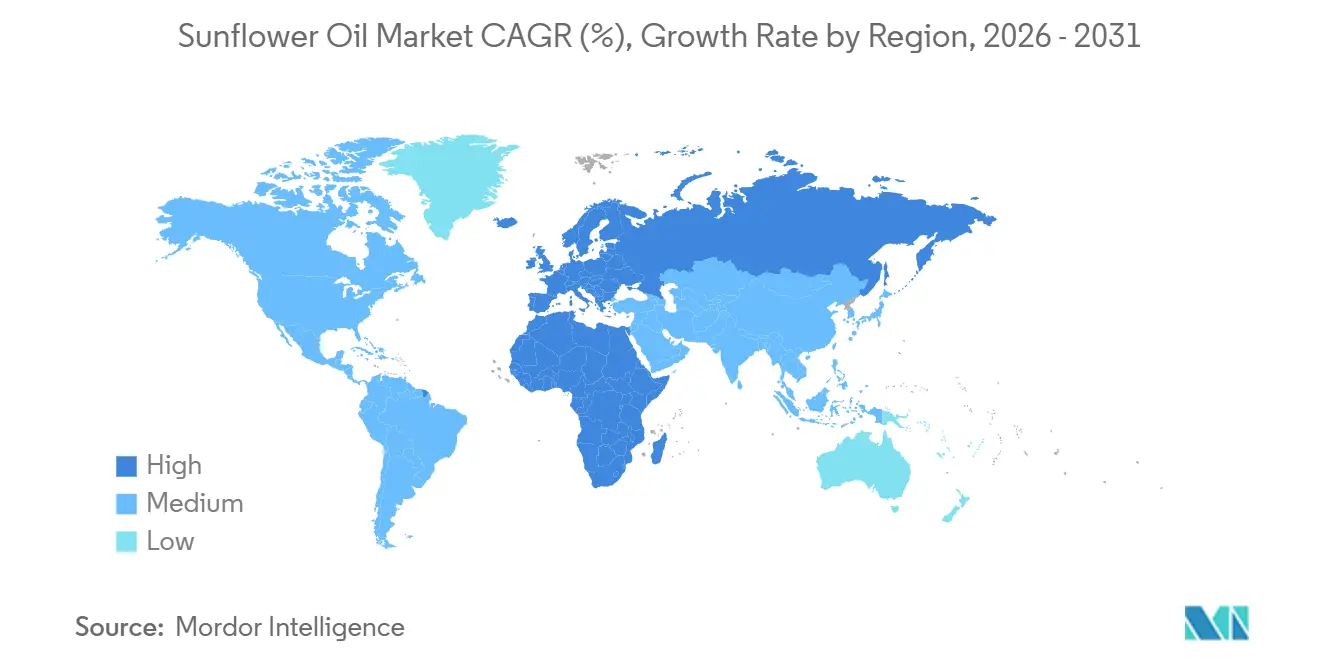

- By geography, Europe commanded 47.83% revenue share in 2025; whereas Middle East and Africa segment is expected to advance at an 8.15% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Sunflower Oil Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer awareness of heart-healthy cooking oils | +0.8% | Global, strongest in North America and Western Europe | Medium term (2-4 years) |

| Shift away from trans-fats in food processing | +1.1% | North America, Europe, Brazil, Asia-Pacific, Middle East and Africa | Short term (≤ 2 years) |

| Growing demand for high-oleic sunflower oil for frying stability | +1.3% | North America, Europe quick-service chains, urban China and India | Medium term (2-4 years) |

| Biodiesel mandates boosting vegetable-oil demand | +0.9% | United States, Brazil, Europe, Argentina | Long term (≥ 4 years) |

| Cold-pressed uptake in premium personal care | +0.4% | Western Europe, North America, Japan, South Korea, urban China | Long term (≥ 4 years) |

| Scope-3 decarbonization driving palm-oil substitution | +0.7% | European Union, United Kingdom, North America supply chains | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising consumer awareness of heart-healthy cooking oils

Sunflower oil’s market expansion is closely tied to its positioning as a heart-supportive cooking oil, supported by its high unsaturated fat content and natural presence of vitamin E. Health authorities continue to recommend replacing saturated fats with vegetable oils to help reduce LDL cholesterol and overall cardiovascular risk, reinforcing its credibility among nutrition-conscious consumers. Notably, the International Food Information Council’s 2024 survey found that 46% of United States shoppers consider seed oils healthy, while 28% actively avoid them, highlighting how digital narratives have polarized consumer perceptions [1]International Food Information Council, "Americans' Perceptions Of Seed Oils", ific.org. Despite this divide, demand for high-oleic variants is rising, reflecting a shift toward premium and functionally differentiated offerings. With cardiovascular diseases remaining a leading global health concern, organizations such as the World Health Organization continue to emphasize healthier dietary fat choices. As a result, sunflower oil remains well positioned in retail channels, benefiting from both scientific endorsement and evolving consumer preference for better-for-you cooking solutions.

Shift away from trans-fats in global food processing

Tightening global regulations on partially hydrogenated oils have significantly reshaped edible oil demand, reinforcing sunflower oil’s structural growth. By the middle of 2024, dozens of nations covering a substantial share of the global population had enforced formal limits on trans-fats, driving extensive product reformulations across bakery, confectionery, and snack segments in alignment with guidance from the World Health Organization. In Brazil, the implementation of a 2% trans-fat ceiling in 2023 pushed biscuit and processed food manufacturers to shift from hydrogenated soybean oil toward high-oleic sunflower oil to maintain functional performance without hydrogenation. Similarly, India is set to enforce a comparable 2% limit by 2025, unlocking sizeable incremental demand within its vast edible oil market. These regulatory interventions are not temporary adjustments but long-term structural shifts that embed sunflower oil more deeply into food manufacturing supply chains. Its favorable fatty acid composition, neutral sensory profile, and strong oxidative stability make it a technically viable and label-friendly solution. As health claims become more tightly regulated and consumer scrutiny intensifies, sunflower oil benefits from alignment with clean-label and better-for-you positioning. Consequently, policy-driven reformulation is expected to sustain durable demand momentum for sunflower oil over the forecast period.

Growing demand for high-oleic sunflower oil for frying stability

Rising preference for high-oleic sunflower oil is reshaping demand patterns across the edible oils industry, particularly in commercial foodservice and packaged food manufacturing. Its enhanced oxidative stability allows restaurants to extend fryer usage cycles to around 72 hours, lowering oil disposal volumes and cutting operating costs significantly. According to data from the United States Department of Agriculture, global high-oleic sunflower oil production reached approximately 3.2 million metric tons in MY 2024/25, reflecting strong year-on-year growth [2]United States Department of Agriculture Economic Research Service, "Oil Crops Outlook", ers.usda.gov. On the supply side, breeding advancements by Instituto Nacional de Tecnología Agropecuaria (INTA) in Argentina have introduced high-oleic hybrids with elevated oleic acid content and improved disease resistance, encouraging acreage expansion. Foodservice trials in major Asian quick-service outlets have demonstrated reduced oil replacement frequency, generating savings in labor and logistics. Moreover, regulatory backing from the European Food Safety Authority for cholesterol-lowering phytosterol claims has strengthened its functional positioning. Combined agronomic innovation, operational efficiencies, and health-forward marketing advantages continue to reinforce the premium growth trajectory of high-oleic sunflower oil.

Cold-pressed oil uptake in premium personal-care

The surge of clean-label and premium beauty labels is accelerating the use of cold-pressed sunflower oil, particularly due to its high linoleic acid content that supports skin barrier restoration. Brands such as Typology have incorporated cold-pressed variants into targeted serums, demonstrating measurable improvements in acne-prone skin over sustained usage. Western Europe and North America together account for a majority of cosmetic-grade sunflower oil demand, reflecting mature consumer acceptance of plant-based emollients. Cold-pressed oils command a notable price premium since their extraction method preserves tocopherols and phytosterols that enhance antioxidant performance. Large FMCG players like Unilever have expanded the proportion of plant-derived oils in personal-care formulations, responding to both regulatory pressure and evolving consumer preferences. In Asia, regulatory tailwinds such as Japan’s 2024 quasi-drug approval by Ministry of Health, Labour and Welfare have opened new avenues for medicated skincare applications using sunflower oil. Growing demand for transparent sourcing and minimally processed ingredients further reinforces its positioning in sustainable beauty. Social media advocacy and dermatologist-backed claims are also strengthening consumer trust in botanical actives. Collectively, these developments are establishing cosmetic-grade sunflower oil as a high-growth segment within the broader personal-care ingredients market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Geopolitical disruptions affecting supply chains in Russia and Ukraine | -1.2% | Europe, Middle East, North Africa, Asia-Pacific importers | Short term (≤ 2 years) |

| Price competition from soybean and palm oil alternatives | -0.9% | South Asia, Southeast Asia, Sub-Saharan Africa | Medium term (2-4 years) |

| Traceability expenses linked to the EU deforestation regulation | -0.5% | Europe importers; Ukraine, Russia, Argentina exporters | Medium term (2-4 years) |

| Yield fluctuations driven by localized climate variability | -0.6% | Ukraine, Russia, Argentina, Turkey | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Geopolitical disruptions affecting supply chains in Russia and Ukraine

The Russia–Ukraine conflict has significantly reshaped the global sunflower oil trade, as both countries represent a dominant share of export supply. Periodic disruptions to Black Sea shipping routes have triggered sharp price fluctuations, creating uncertainty across international markets. Although Ukraine continues to harvest substantial volumes, processing facilities in major production hubs have been operating below optimal capacity due to power shortages and labor constraints. Leading processors have experienced margin pressures as logistics and risk-related expenses escalated. The fragile supply environment means that any renewed escalation could quickly tighten global availability, forcing importing countries to shift toward substitutes such as soybean or palm oil at higher prices. These developments have intensified volatility, strained downstream sectors like food processing and retail, and disrupted procurement planning. Overall, prolonged geopolitical instability acts as a key restraint on the sunflower oil market by limiting supply reliability, inflating costs, and increasing long-term uncertainty across the value chain.

Price competition from soybean and palm oil alternatives

The sunflower oil market continues to face headwinds due to its structurally higher pricing compared to competing edible oils. In 2024, global price benchmarks showed sunflower oil trading at a notable premium over soybean and crude palm oil, creating a cost gap that limits its competitiveness in price-sensitive markets. This disparity has constrained its uptake in large importing nations such as India, where consumers and retailers increasingly favor more affordable palm oil options despite strong overall edible oil demand. Policy interventions, including Indonesia’s price-capping measures on cooking oils, have further reduced shelf space for higher-priced sunflower variants. In export-driven sunflower oil markets like Argentina, narrowing tax advantages on soybean oil have incentivized crushers in China and Brazil to pivot toward soybean processing, intensifying substitution pressure. Demand elasticity estimates also suggest that even moderate relative price increases can significantly dampen sunflower oil consumption in emerging economies. Moreover, soybean and palm oils benefit from larger-scale production, stronger global supply chains, and broader application across food processing and biofuel sectors. Collectively, these dynamics reinforce competitive substitution and challenge sunflower oil’s ability to expand market share in cost-driven segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fatty Acid Profile: Mid-Oleic Variants Drives Market Positioning

In 2025, mid-oleic sunflower oil holds the leading position in the global sunflower oil market, accounting for 39.52% of total share. Its dominance is supported by a well-balanced fatty acid composition that offers improved oxidative stability while maintaining a neutral flavor profile suitable for diverse food applications. The segment is widely used in baked snacks, breakfast cereals as spray oils, and blended shortenings, particularly in formulations that avoid trans fats. Food manufacturers favor mid-oleic oil for its versatility across retail and industrial segments, where both performance and cost efficiency are critical. This adaptability across multiple value chains enables it to retain the broadest base within the market.

High-oleic sunflower oil is expected to register the fastest growth, expanding at a CAGR of 6.84% from 2026 to 2031, driven by rising demand for high-performance frying oils. Its superior oxidative stability supports extended frying cycles in restaurants and large-scale foodservice operations, reducing oil disposal frequency and operational costs. Meanwhile, linoleic sunflower oil continues to serve price-sensitive retail packs and industrial margarine applications, though its volume share is gradually declining amid the shift toward specialty fatty acid profiles. Collectively, evolving fatty acid preferences are reshaping segment dynamics without diminishing overall sunflower oil demand.

By Processing: Refined Oil Segment Dominates with Accelerated Market Growth

Refined sunflower oil accounted for 65.74% of the market share in 2025, making it the largest segment, and it is also projected to register the fastest growth at a 5.82% CAGR through 2031. Its dominance is supported by high extraction efficiency and the ability to deliver uniform quality at scale. Through solvent extraction followed by refining, bleaching, and deodorizing, the oil delivers a neutral taste, longer shelf life, and a stable smoke point suited for industrial frying, baking, and packaged food applications. These standardized functional properties also make it suitable for biodiesel production, where cost efficiency and specification consistency are key procurement drivers.

In contrast, unrefined and cold-pressed sunflower oil cater to a smaller but premium segment driven by demand for minimally processed and clean-label products. Mechanical extraction preserves natural tocopherols, phenolics, and characteristic flavor compounds, supporting premium positioning in retail and personal care markets. According to the Government of India’s edible oil quality standards (Agmarknet), cold-pressed/virgin sunflower oil is permitted a maximum acid value of 4.0 mg KOH/g oil compared to 0.6 mg KOH/g for refined oil, with higher allowable peroxide values, reflecting their distinct regulatory classification [3]Directorate of Marketing & Inspection, "Agmark Standards", dmi.gov.in. Lower extraction efficiency and greater dependence on seed quality restrict large-scale expansion, allowing refined oil to retain dominance in bulk food processing and biodiesel applications.

By End Use: Food Industry Dominates, while Personal Care and Cosmetics Accelerates

In 2025, the food industry accounts for the largest share of the sunflower oil market, capturing 35.12% of total demand. Its leadership is supported by extensive usage across bakery, confectionery, savory snacks, and canned food production, where sunflower oil is valued for its neutral flavor profile and functional stability. Consistent household consumption and strong penetration in packaged food manufacturing further reinforce its dominance. Demand is also sustained by consumers’ preference for plant-based and perceived healthier edible oils, ensuring the segment remains the backbone of overall market revenue.

On the other hand, the personal care and cosmetics segment is projected to be the fastest expanding application, registering a CAGR of 6.72% through 2031. Growth is fueled by increasing incorporation of sunflower oil as a natural emollient in skincare serums, cleansing balms, and hair care formulations. Further, steady offtake from HoReCa channels and organized retail supports baseline consumption, while biodiesel programs, particularly in major producing and consuming countriesprovide an additional structural demand layer. Together, these diversified end-use segments, including foodservice, retail, industrial, and energy applications, create a balanced growth environment and reduce reliance on any single market stream.

Geography Analysis

In 2025, Europe accounted for the largest share of the global sunflower oil market, representing 47.83% of total revenue. The region’s dominance is underpinned by strong consumption centers such as Germany and the Netherlands, among others. A substantial portion of the European Union’s imports continues to originate from Ukraine, making the region sensitive to supply-side risks in the Black Sea region. At the same time, evolving EU traceability and sustainability regulations have increased compliance costs across fragmented supply chains, favoring integrated processors capable of meeting farm-level certification standards. Southern European countries such as Spain and Italy are expanding premium and cold-pressed sunflower oil segments, while leading processors including LIPSA are strengthening certified sourcing commitments to secure retail contracts focused on sustainability.

The Middle East & Africa region is projected to be the fastest-growing sunflower oil market, advancing at a CAGR of 8.15% between 2026 and 2031. Rising import requirements in Egypt, alongside expanding packaged food consumption in Nigeria, are supporting regional demand growth. In the Gulf, Saudi Arabia is strengthening food security through strategic edible oil reserves, allocating a notable portion to sunflower oil to reduce reliance on palm oil imports. Meanwhile, Jebel Ali in Dubai continues to reinforce its role as a re-export gateway, with volumes increasing as global traders adjust logistics routes amid geopolitical disruptions.

Asia-Pacific is driven primarily by large-volume imports into China and India. China’s purchases rose following improved freight connectivity with Russia, while India expanded procurement to stabilize domestic edible oil prices and manage inflationary pressures. In North America, steady demand is supported by both food consumption and renewable fuel initiatives. The forthcoming renewable diesel facility developed by Bunge and Chevron in Louisiana is expected to integrate significant volumes of vegetable oil blends into biofuel production streams. Meanwhile, South America continues to enhance global supply depth, with Argentina expanding sunflower acreage and exportable oil output, reinforcing its position as a key supplier alongside Brazil.

Competitive Landscape

The global sunflower oil industry reflects moderate consolidation, with a group of multinational agribusinesses controlling a substantial share of export-oriented crushing capacity. Companies such as Archer Daniels Midland Company, Cargill Incorporated, Kernel Holding S.A., Wilmar International Ltd, and Bunge Limited anchor the competitive landscape through vertically integrated models that span origination, processing, refining, and global distribution. Their strategic focus has expanded beyond traditional edible oil markets toward renewable fuel integration, proprietary high-oleic seed development, and geographic risk diversification, particularly to reduce reliance on the Black Sea region. Cross-industry collaborations, including energy-linked ventures, further strengthen long-term demand visibility and offtake security.

In parallel, regionally focused companies continue to exert meaningful influence by leveraging proximity advantages and localized sourcing ecosystems. Firms such as Kernel and Avril Group concentrate on building strong farmer networks and traceable supply chains tailored to European and neighboring markets. Investments in digital agriculture tools, including satellite monitoring and soil-sensor technologies, are enhancing yield predictability and input efficiency, strengthening competitiveness despite smaller global footprints. Rapid compliance with sustainability frameworks and certification standards has enabled such players to secure contracts in traceability-sensitive markets, particularly within the EU.

At the strategic level, competitive differentiation is increasingly defined by three pillars: technological sophistication, sustainability alignment, and supply-chain integration. Advanced refining capabilities improve oil stability and extend shelf life, while proprietary high-oleic hybrids respond to growing demand for healthier, functional cooking oils. Simultaneously, internationally recognized sustainability certifications enhance access to premium retail and industrial buyers. Companies able to combine operational scale with innovation and environmental credentials are best positioned to capture value in higher-margin segments and navigate ongoing shifts in trade flows, energy policy linkages, and evolving consumer expectations.

Sunflower Oil Industry Leaders

-

Archer Daniels Midland Company

-

Bunge Limited

-

Wilmar International Ltd.

-

Cargill, Incorporated

-

Kernel Holding S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Fortune Sunflower Oil rolled out a new “17% less oil absorption” proposition to promote lighter, healthier cooking, showcased through regional TVCs and updated packaging in southern Indian markets. The campaign aims to help consumers enjoy traditional foods with reduced oil intake without compromising on taste.

- September 2025: Louis Dreyfus Company completed the acquisition of grains and oilseeds assets in Hungary and Poland from Viterra, strengthening its Central European operations. The deal enhances LDC’s sunflower seed crushing and processing capabilities, reinforcing its position in the European sunflower oil market.

- July 2025: Bunge and Viterra completed their long-planned merger, creating a premier global agribusiness solutions company that integrates grain trading, oilseed processing and broader agricultural value chains. The combined firm aims to better connect farmers to markets and customers worldwide with expanded capabilities across food, feed and fuel supply chains.

Global Sunflower Oil Market Report Scope

Sunflower oil, a pale yellow semi-drying or drying fatty oil, is extracted from the seeds of the common sunflower. It is primarily utilized in food, personal care products, varnishes, and paints.

The global sunflower oil market is categorized by type and application. The types include linoleic oil, mid-oleic oil, and high-oleic oil. Applications span across food, biofuels, and personal care. The report also provides a geographical analysis of the market, focusing on both developed and emerging regions, namely North America, Europe, Asia Pacific, South America, and the Middle East and Africa.

Market sizing is presented in USD value terms for all segments mentioned above.

| Linoleic Sunflower Oil |

| Mid-oleic Sunflower Oil |

| High-oleic Sunflower Oil |

| Refined |

| Unrefined/Cold-Pressed |

| Food | Bakery and Confectionery |

| Savory Snacks | |

| Ready Meals | |

| Canned Foods | |

| Other Food Applications | |

| Foodservice/HoReCa | |

| Retail | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retail Stores | |

| Other Retail Channels | |

| Biodiesel | |

| Personal Care and Cosmetics | |

| Other End Use |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Fatty Acid Profile | Linoleic Sunflower Oil | |

| Mid-oleic Sunflower Oil | ||

| High-oleic Sunflower Oil | ||

| By Processing | Refined | |

| Unrefined/Cold-Pressed | ||

| By End Use | Food | Bakery and Confectionery |

| Savory Snacks | ||

| Ready Meals | ||

| Canned Foods | ||

| Other Food Applications | ||

| Foodservice/HoReCa | ||

| Retail | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Retail Stores | ||

| Other Retail Channels | ||

| Biodiesel | ||

| Personal Care and Cosmetics | ||

| Other End Use | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the sunflower oil market?

The global sunflower oil market is valued at USD 33.89 billion in 2026.

How fast is demand for high-oleic sunflower oil growing?

High-oleic grades benefit from a 6.84% CAGR through 2031, supported by frying-stability advantages.

Which region buys the most sunflower oil?

Europe leads with a 47.83% revenue share, driven by mature processing infrastructure and consumer preference for vegetable oils.

Why is sunflower oil attractive for biodiesel producers?

Renewable-diesel programs reward low-carbon feedstocks, and sunflower oil offers favorable cold-flow properties and certified sustainability.

Page last updated on: