Black Seed Oil Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

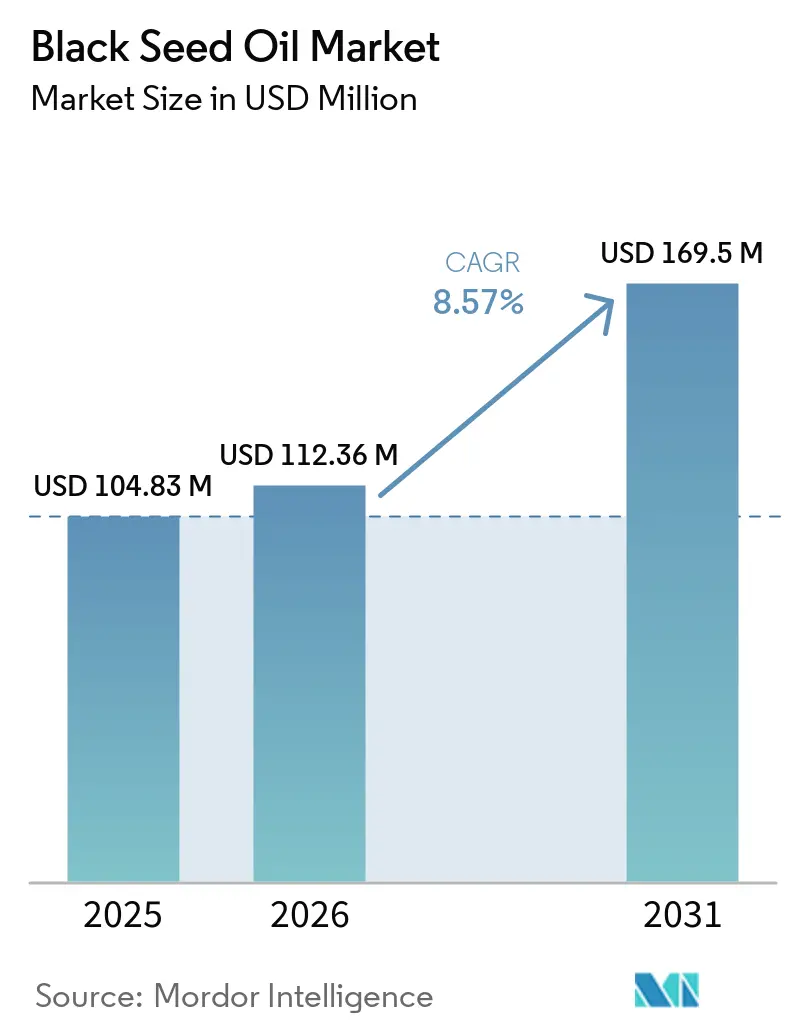

| Market Size (2026) | USD 112.36 Million |

| Market Size (2031) | USD 169.5 Million |

| Growth Rate (2026 - 2031) | 8.57% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Black Seed Oil Market Analysis by Mordor Intelligence

The black seed oil market size was USD 104.83 million in 2025 and is projected to reach USD 169.50 million by 2031, growing at a CAGR of 8.57% during 2026 to 2031. The black seed oil market is moving away from bulk trading and toward ingredient contracts that depend on steady thymoquinone content, batch testing, and traceable sourcing, which is changing how buyers compare suppliers across supplements, cosmetics, and specialty foods. Demand patterns in the black seed oil market are also shifting, because nutraceutical formulators in North America and Europe now look for standardized ingredients with clinical backing rather than relying only on traditional consumption patterns in the Middle East and South Asia. The black seed oil market is becoming more difficult for undifferentiated suppliers, since crop volatility, adulteration concerns, and regulatory differences across the United States, the European Union, and Asia now affect quality control and market access at the same time. Companies with proprietary extraction methods, standardization capabilities, and patent-backed formulations are gaining stronger pricing power, which is pushing the black seed oil market toward a more quality-led competitive structure. This pattern also shows that the next phase of growth in the black seed oil market will depend less on raw volume expansion and more on verified performance, compliance readiness, and premium positioning across multiple end-use channels.

Key Report Takeaways

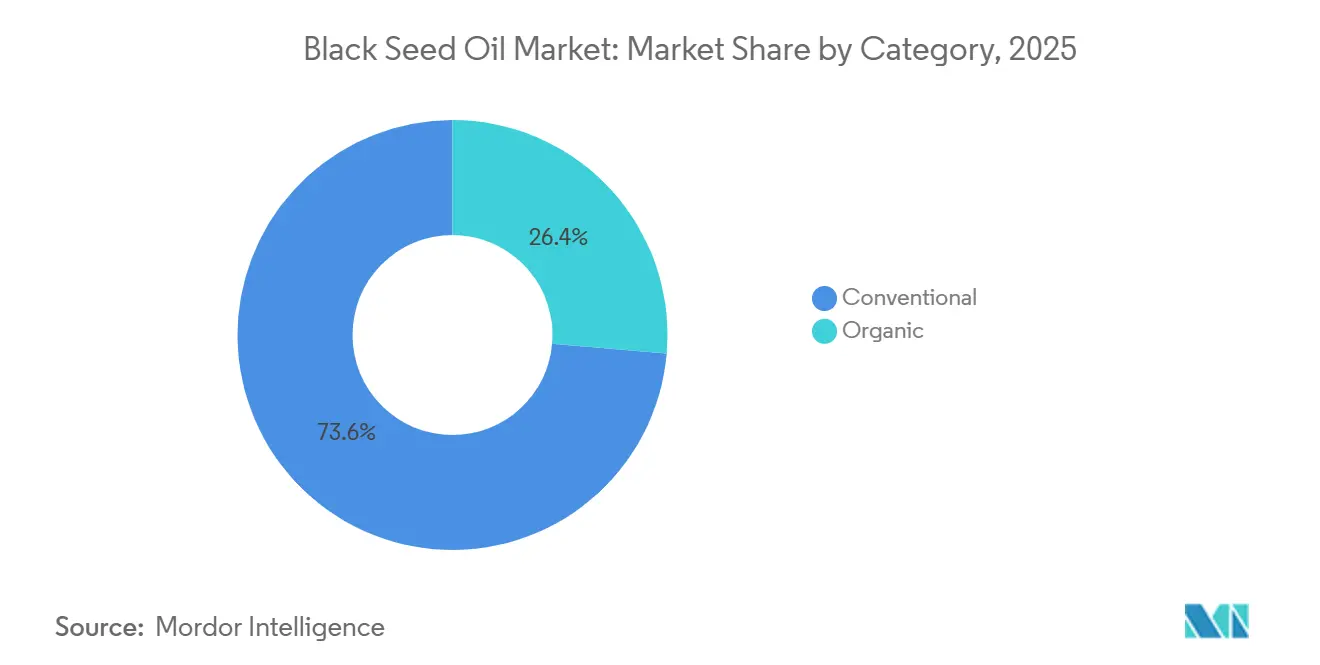

- By category, conventional black seed oil led with 73.62% of the black seed oil market share in 2025, while organic is projected to record the fastest growth at 9.11% CAGR through 2031.

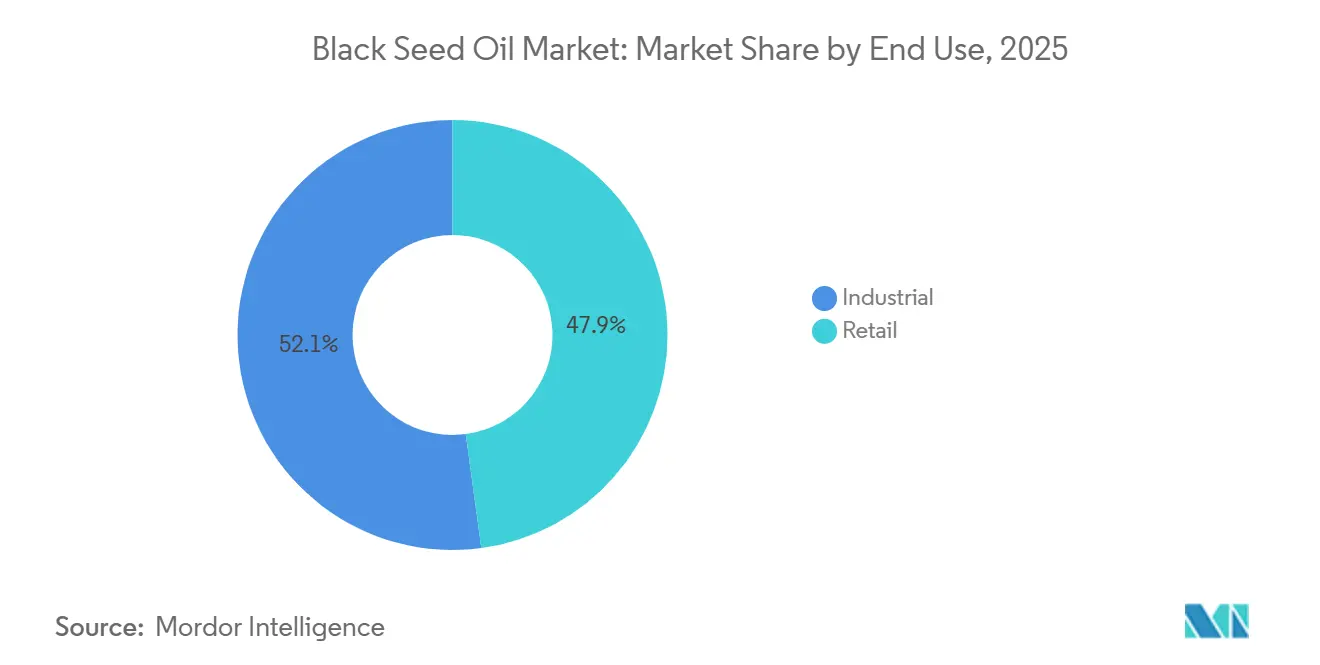

- By end use, the industrial segment held 52.13% of the black seed oil market size in 2025, while the retail segment is forecast to expand at 9.18% CAGR through 2031.

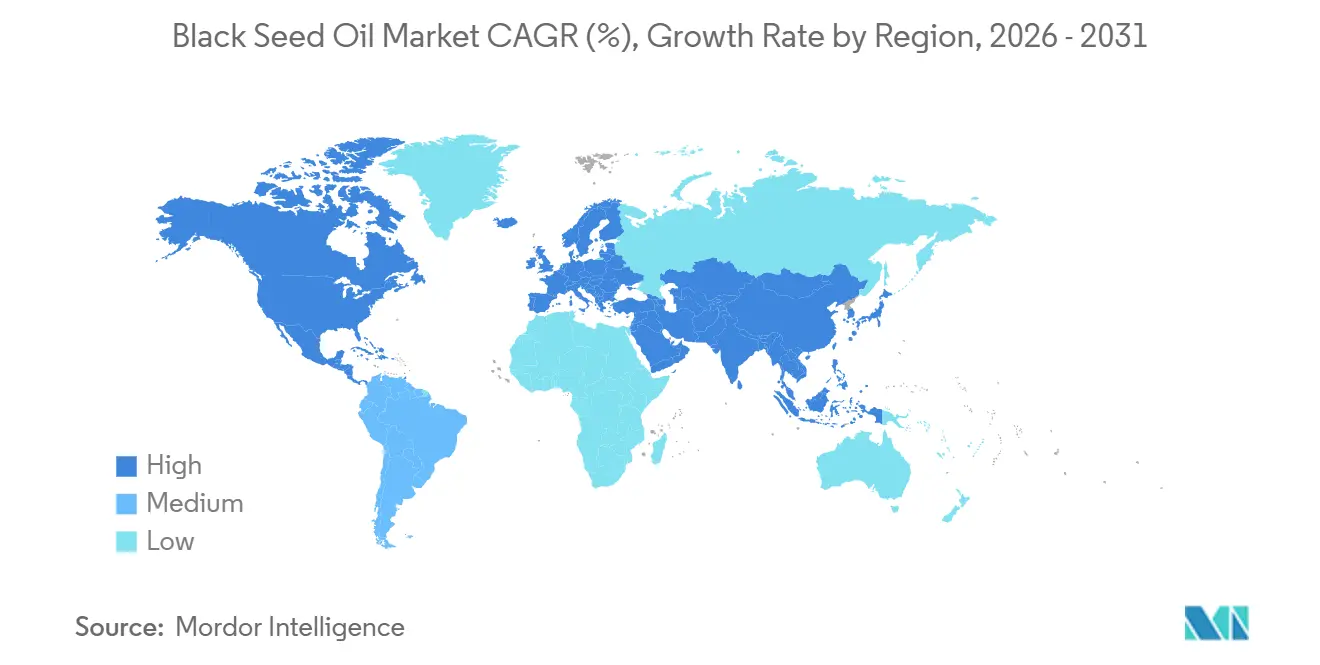

- By geography, Europe accounted for 34.40% share in 2025, while Asia-Pacific is expected to advance at a 938% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Black Seed Oil Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for clean-label botanical supplements | +1.8% | Global, with the strongest pull from North America and Western Europe | Short term (≤ 2 years) |

| Expanded use in standardized supplement formulations | +2.1% | North America, Europe, and Australia | Medium term (2-4 years) |

| Premiumization through thymoquinone standardization | +1.5% | Europe, North America, and the Asia-Pacific premium segment | Medium term (2-4 years) |

| Growth of D2C and marketplace distribution | +1.3% | Global, concentrated in North America, the United Kingdom, and the Gulf states | Short term (≤ 2 years) |

| Strategic shift from synthetic ingredients to organic botanical alternatives | +0.9% | Western Europe, North America, Southeast Asia | Medium term (2-4 years) |

| Advancements in cold-pressed and supercritical CO2 extraction technologies | +0.7% | Europe and the Asia-Pacific industrial processing corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for clean-label botanical supplements

Globally, consumer demand is shifting towards ingredients that are traceable, minimally processed, and devoid of synthetic additives, reshaping the landscape of supplement procurement. Black seed oil, traditionally revered and composed of a single ingredient, resonates perfectly with this evolving preference. A systematic review and meta-analysis, set for 2025, scrutinized 82 randomized controlled trials with over 5,000 participants. Published in a peer-reviewed journal, the findings highlighted that supplementation with Nigella sativa notably enhanced cardiometabolic markers. These included blood pressure, LDL cholesterol, fasting blood sugar, HbA1c, and inflammatory markers like CRP and IL-6. Notably, oil-based supplements outshone their powder counterparts. Such robust clinical evidence is now steering procurement choices. Formulators are increasingly designating Nigella sativa as a favored botanical, placing it alongside established names like turmeric and ashwagandha. This push for clean-label products is especially pronounced in Europe. Here, the EU's Regulation (EU) No. 2019/1381, part of the General Food Law, mandates traceability and risk analysis. This regulation effectively narrows the field to suppliers with certified and credentialed origins[1]Source: CBI, “Entering the European Market for Black Cumin Seed Oil,” CBI, cbi.eu.

Expanded use in standardized supplement formulations

Black seed oil is transitioning from a traditional remedy to a clinically standardized ingredient, carving out a premium niche in the nutraceuticals sector. Buyers in North America and Europe are increasingly demanding specific thymoquinone content: typically 1.0–2.5% for nutraceutical-grade nigella sativa oil and over 3% for pharmaceutical-grade uses. Moreover, third-party testing has become a norm for private-label contracts. By early 2026, over 40 active clinical trials globally were probing thymoquinone's potential benefits for conditions like type 2 diabetes, hypertension, asthma, and non-alcoholic fatty liver disease. This push for standardization is reshaping the industry landscape: while it's elevating capital demands for extraction and quality testing, putting smaller commodity producers at a disadvantage, it's simultaneously fortifying the position of vertically integrated ingredient firms. This trend has garnered validation from Health Canada. In March 2024, the agency greenlit six structure-function claims for a standardized black seed oil ingredient, underscoring a regulatory tilt towards evidence-backed botanical assertions.

Premiumization through thymoquinone standardization

Thymoquinone standardization is reshaping the black seed oil market, turning what was once a price-sensitive commodity into a performance-driven ingredient. TriNutra's ThymoQuin, a US Pharmacopeia-grade product standardized to 3% thymoquinone, boasts an expanding IP portfolio. This portfolio spans composition, bioavailability, and synergistic combinations. Notably, it includes a US patent granted in June 2026 for ThymoQuin's combination with astaxanthin, highlighting their joint anti-inflammatory and antioxidant benefits in research[2]Source: TriNutra, “TriNutra Receives U.S. Patent for ThymoQuin and Astaxanthin Composition,” TriNutra, trinutra.com. On a parallel note, Sabinsa Corporation's Nigellin, derived from solvent-free supercritical fluid extraction and standardized to 5–20% thymoquinone, has secured both COSMOS approval and ECOCERT verification, paving its way into the European natural cosmetics market. This shift in the industry is evident: procurement is now prioritizing the price-per-milligram-of-active-compound over the traditional price-per-liter. As a result, suppliers unable to consistently declare thymoquinone content risk being sidelined from premium accounts, irrespective of their price competitiveness.

Growth of D2C and marketplace distribution

Black seed oil brands, both small-batch producers and patent-backed suppliers, are now sidestepping traditional wholesale channels, thanks to e-commerce and direct-to-consumer models. Data from Amazon's Brand Analytics for early 2026 reveals a significant shift: products topping the "black seed oil organic" search boast monthly sales in the tens of thousands. Notably, the frontrunner surpassed 100,000 orders in just one month, underscoring the category's leap from niche to mainstream. The launches of TriNutra–Dr. Michael Murray on iHerb in September 2024 and TriNutra–Nutritunes on Amazon in August 2025 highlight a strategic move by ingredient innovators. They're not just entering the market; they're building brand equity and clinical credibility through these direct-to-consumer launches. A key insight: subscription models in this channel are more than just a sales tactic. They offer manufacturers a glimpse into predictable demand, enabling them to secure standardized seed contracts months ahead and shield themselves from the volatile swings of Nigella sativa commodity prices.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intense commercial competition from alternative functional plant oils | -0.6% | Global, the highest friction is in North America and Southeast Asia | Short term (≤ 2 years) |

| Supply risk from climate-linked Nigella sativa crop variability | -0.8% | India, Egypt, Turkey, primary producing corridors | Medium term (2–4 years) |

| Regulatory fragmentation and health-claim compliance complexity across markets | -0.7% | North America, Europe, and the Asia-Pacific each operate distinct food-safety and botanical-claim frameworks | Medium term (2–4 years) |

| Product adulteration and authenticity verification challenges in unregulated channels | -1.2% | Global, most acute in online retail and markets with weak import enforcement | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Intense commercial competition from alternative functional plant oils

Black seed oil finds itself vying for shelf space and formulation budgets with an expanding array of functional botanicals. These include sea buckthorn, moringa seed oil, hemp seed oil, and black raspberry seed oil, all touting similar antioxidant and anti-inflammatory benefits. While black seed oil stands out, many of its competitors enjoy advantages: they boast larger cultivation bases, offer a lower price-per-unit, and have established supply chains. This gives procurement teams a strong incentive to pivot to these alternatives, especially when prices for Nigella sativa rise. The challenge is even more pronounced in the cosmetics and personal care arena. Here, formulators frequently test ingredients side-by-side and aren't tied to any single botanical. An often-overlooked competitive angle comes from functional plant oil blends. These blends, marketed under proprietary names, mask their individual ingredients and challenge pure black seed oil, focusing on product claims rather than ingredient clarity.

Supply risk from climate-linked nigella sativa crop variability

India, Egypt, and Turkey, the primary cultivators of Nigella sativa, grapple with unique yet overlapping climate challenges. In India, the 2024 season brought unexpected weather disruptions in Rajasthan and its neighboring states. These anomalies tightened supply balances and pushed wholesale prices higher. Commodity monitoring services highlighted that these in-season irregularities posed challenges for smallholders during harvest and drying operations. Meanwhile, in Egypt, constraints from Nile irrigation and rising temperatures have led to water scarcity, putting pressure on yields. Turkey's Bucak district, despite a significant 120% increase in cultivation and oils boasting up to 8% thymoquinone, is not immune to seasonal weather fluctuations. A 2025 analysis by BCG underscored the importance of mapping climate and geopolitical risks to bolster supply chain resilience in agrifood sectors. Specifically for black seed oil, this heightened awareness translates to a shift in the procurement risk premium from a low to a moderate probability. Consequently, this shift is set to raise the costs of long-term supply contracts, hitting hardest those buyers lacking dual-origin sourcing capabilities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Category: Organic Segment Eroding Conventional's Dominance

In 2025, conventional black seed oil dominated the market, claiming a 73.62% share. Its stronghold is evident across bulk industrial channels and mainstream retail outlets, where price sensitivity drives purchasing decisions. Meanwhile, the organic segment is set to outpace the overall market, with a projected growth rate of 9.11% CAGR from 2026 to 2031, surpassing the market's 8.57% rate. This surge is attributed to organic-certified Nigella sativa supplies from Egypt and India, which are gradually bridging the price gap with their conventional counterparts. In 2024, India's exports of Nigella sativa oil to Europe hit EUR 23 million, despite a slight growth plateau. Concurrently, Egypt's exports to Europe, valued at EUR 2.3 million, featured suppliers offering cold-pressed oil derived from organically farmed seeds, boasting a thymoquinone content of 6–7%.

For conventional producers, the rising organic share signals more than just a market shift; it's a clear indication that organic certification is becoming crucial for accessing premium channels in the EU and North America. The only commercially viable methods for extracting organically certified black seed oil are cold-pressed and supercritical CO2 extraction. This reality amplifies value creation for processors equipped with the necessary capital-intensive extraction infrastructure. Take FLAVEX Naturextrakte GmbH, for example. They produce a certified-organic black cumin CO2 extract, boasting a thymoquinone content of over 3% and holding the DE-ÖKO-013 certification[3]Source: FLAVEX Naturextrakte GmbH, “Black Cumin CO2-to Extract Organic Product No. 122.002,” FLAVEX Naturextrakte GmbH, flavex.com. Their primary targets are European nutraceutical and cosmetics formulators, a strategic positioning that shields them from the volatility of commodity price competition. In Turkey's Bucak district, Nigella sativa cultivation has surged by 120%. These oils, containing up to 8% thymoquinone, double the global average, are now eyeing geographical indication certification. This move could carve out a premium sub-tier within the conventional category.

By End Use: Industrial Usage Anchors Volume; Retail Accelerate Margin Expansion

In 2025, the industrial segment dominated the global black seed oil market with a 52.13% share, driven by widespread utilization across nutraceuticals, dietary supplements, cosmetics, personal care products, and functional foods. Growing consumer interest in natural ingredients and botanical extracts has encouraged manufacturers to incorporate black seed oil into value-added formulations. Industry organizations such as the American Herbal Products Association continue to highlight rising demand for plant-based wellness ingredients. Supporting this trend, several ingredient suppliers expanded standardized black seed oil offerings in 2025 and 2026, targeting supplement and cosmetic manufacturers seeking high-purity, traceable formulations.

The retail segment is projected to grow at a CAGR of 9.18% from 2026 to 2031, making it the fastest-growing end-use category in the global black seed oil market. Growth is supported by increasing consumer awareness of black seed oil’s perceived wellness benefits, alongside expanding e-commerce and health-food retail channels. Government-backed health promotion initiatives encouraging preventive wellness and natural products further support demand. Product innovation is accelerating adoption; in 2025 and 2026, brands such as Amazing Herbs and The Black Seed Oil Co. expanded consumer-focused softgels, liquid oils, and flavored formulations, improving accessibility and attracting a broader retail customer base.

Geography Analysis

In 2025, Europe commanded a dominant 34.4% share of the market, solidifying its top regional position. Major consumer economies in the region bolster demand for herbal supplements, clean-beauty products, and specialty food ingredients. Germany emerges as a key player, boasting robust end-market demand and processing capabilities, notably with FLAVEX Naturextrakte GmbH's supercritical CO2 extraction. The region's stringent compliance standards directly influence supplier selection. Notably, the EU Rapid Alert System for Food and Feed flagged multiple black seed oil shipments in 2024 and 2025, citing contaminants and residue issues. This has nudged buyers towards suppliers with certified origins and documented testing. Thus, Europe's share in the black seed oil market underscores both its demand strength and a regulatory landscape favoring qualified suppliers.

Asia-Pacific is set to outpace others, with a projected 9.4% CAGR from 2026 to 2031, marking it as the fastest-growing regional segment. Unlike Europe, its growth marries traditional cultural use with a modern supplement surge. Demand from the South Asian, Southeast Asian, and Middle Eastern diasporas sustains baseline consumption. Meanwhile, urban wellness trends are gaining traction in Australia, Singapore, and India. India's dual role as a major consumption hub and a pivotal production base shapes the region's black seed oil landscape. India's FSSAI standards for cold-pressed seed oils, effective December 2026, could standardize domestic quality and impact export grades. This regulatory move might enhance quality consistency in the Asia-Pacific black seed oil market, especially for suppliers eyeing premium cross-border sales.

While North America didn't lead in market share, it remains a hotbed for innovation in the black seed oil arena. Growth is driven more by direct-to-consumer sales, clinical endorsements, and ingredient standardization than by traditional usage. Health Canada's March 2024 nod to six structure-function claims for a standardized ingredient bolsters the credibility of evidence-based products on regional shelves. The "Rest of the World," encompassing the Middle East, Latin America, and Africa, showcases a blend of entrenched consumption habits and an underdeveloped value-added product landscape. This scenario paves the way for premium brands and ingredient specialists to penetrate the market, especially through digital channels where trust, education, and clear packaging often outweigh the need for extensive physical distribution. As the black seed oil market diversifies across regions, success hinges on suppliers' ability to align with local regulatory standards, sourcing strategies, and distribution channels.

Competitive Landscape

Three broad tiers structure the black seed oil market, which is moderately fragmented. The first tier consists of ingredient specialists backed by intellectual property (IP), boasting pharmacopoeial positioning, deep certifications, and portfolios backed by clinical evidence. The second tier is made up of regional supplement brands that leverage familiar sourcing and competitive pricing in domestic markets. Emerging processors and online sellers, aiming to transition from commodity oil to more valuable specialty formats, comprise the third tier. This tiered structure keeps the black seed oil market accessible to newcomers. However, reaching the coveted premium positions demands rigorous testing, thorough documentation, and distinct product differentiation. Consequently, the market is competitive, where mere scale doesn't ensure robust margins.

Companies that adeptly blend active-content standardization with solid intellectual property are increasingly claiming the market's top spots. TriNutra stands out as a prime example, curating a portfolio centered on composition claims, bioavailability boosts, and synergistic ingredient blends. In June 2026, a U.S. patent for ThymoQuin paired with astaxanthin underscores a strategic pivot: firms are broadening black seed oil's horizons, venturing into adjacent wellness realms instead of limiting themselves to a singular oil. Meanwhile, Sabinsa carves its niche with Nigellin, leveraging solvent-free supercritical fluid extraction and boasting COSMOS and ECOCERT credentials, bolstering its stance in premium cosmetics and natural health. Such maneuvers highlight a paradigm shift: companies now vie not just for supply access but also for formulation rights, extraction credibility, and certifications tailored to specific channels. In this landscape, these advantages forge sturdier barriers than mere access to raw materials.

Regional and mid-tier players retain significance, leveraging localized sourcing and competitive pricing to maintain their foothold, particularly in domestic retail. Yet, the draft underscores the challenges smaller suppliers encounter when buyers demand specified thymoquinone levels, third-party validations, or premium export certifications. FLAVEX Naturextrakte GmbH showcases another resilience strategy: its certified-organic extract and a sixth consecutive CrefoZert accolade in December 2025 bolster its credibility with discerning European clients who prioritize both financial soundness and quality processes. The black seed oil market grapples with authenticity dilemmas, as adulteration poses a challenge for a product that commands a premium over standard vegetable oils. This predicament amplifies the significance of real-time analysis certificates, enhanced batch transparency, and explicit active-content disclosures. In the coming years, the market is poised to favor companies that simplify verification for buyers while complicating it for lower-quality counterparts.

Black Seed Oil Industry Leaders

TriNutra Ltd

Sabinsa Corporation

FLAVEX Naturextrakte GmbH

SanaBio GmbH

Amazing Herbs

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: CAVU Nutrition launched ThymoQuin Cortisol Support at Natural Products Expo West, the first standalone retail product specifically positioned around cortisol regulation using a standardized black seed oil ingredient. The launch signals commercial validation of stress-wellness positioning for the ingredient category.

- September 2025: TriNutra unveiled the first commercially stable black seed oil powder, ThymoQuin powder, at SupplySide Global, addressing a longstanding stability and potency challenge that had previously limited black seed oil's adoption in tablet, functional food, and powdered beverage formats.

- August 2025: TriNutra and Nutritunes partnered to launch a premium ThymoQuin-based black seed oil supplement on Amazon in both organic and non-organic softgel formats, extending TriNutra's D2C distribution reach in the US market and validating an ingredient-to-brand licensing model.

Global Black Seed Oil Market Report Scope

Black seed oil is an amber-coloured vegetable oil extracted from the dense black seeds of Nigella sativa. The global black seed oil market is segmented by category and end user. By category, the market is segmented into conventional and organic. By end user, the market is segmented into industrial and retail. The industrial segment is further sub-segmented into supplements, cosmetics and personal care, food and beverages, and other industrial uses. Similarly, the retail segment is further sub-segmented into offline retail and online retail. By geography, the market is segmented into North America, Europe, Asia-Pacific, and the Rest of the world. The Market Forecasts are Provided in Terms of Value (USD).

| Conventional |

| Organic |

| Industrial | Supplements |

| Cosmetics and Personal Care | |

| Food and Beverages | |

| Other Industrial Uses | |

| Retail | Offline Retail |

| Online Retail |

| North America |

| Europe |

| Asia-Pacific |

| Rest of the World |

| Category | Conventional | |

| Organic | ||

| End Use | Industrial | Supplements |

| Cosmetics and Personal Care | ||

| Food and Beverages | ||

| Other Industrial Uses | ||

| Retail | Offline Retail | |

| Online Retail | ||

| Geography | North America | |

| Europe | ||

| Asia-Pacific | ||

| Rest of the World | ||

Key Questions Answered in the Report

What is driving black seed oil demand in 2026 and beyond?

Demand is being supported by clean-label supplement preferences, wider use in standardized formulations, and stronger online distribution, while the category is projected to grow at an 8.57% CAGR through 2031.

How large is the black seed oil space expected to become by 2031?

The black seed oil market size is projected to rise from USD 104.83 million in 2025 to USD 169.50 million by 2031.

Which product category leads sales today?

Conventional black seed oil led with 73.62% share in 2025, although organic products are growing faster at a 9.11% CAGR through 2031.

Why is thymoquinone standardization becoming so important?

Buyers increasingly use declared thymoquinone content to compare quality, clinical credibility, and premium positioning, which gives standardized ingredients a stronger edge than undifferentiated bulk oils.

Page last updated on: