Grapeseed Oil Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 0.72 Billion |

| Market Size (2031) | USD 0.98 Billion |

| Growth Rate (2026 - 2031) | 6.36% CAGR |

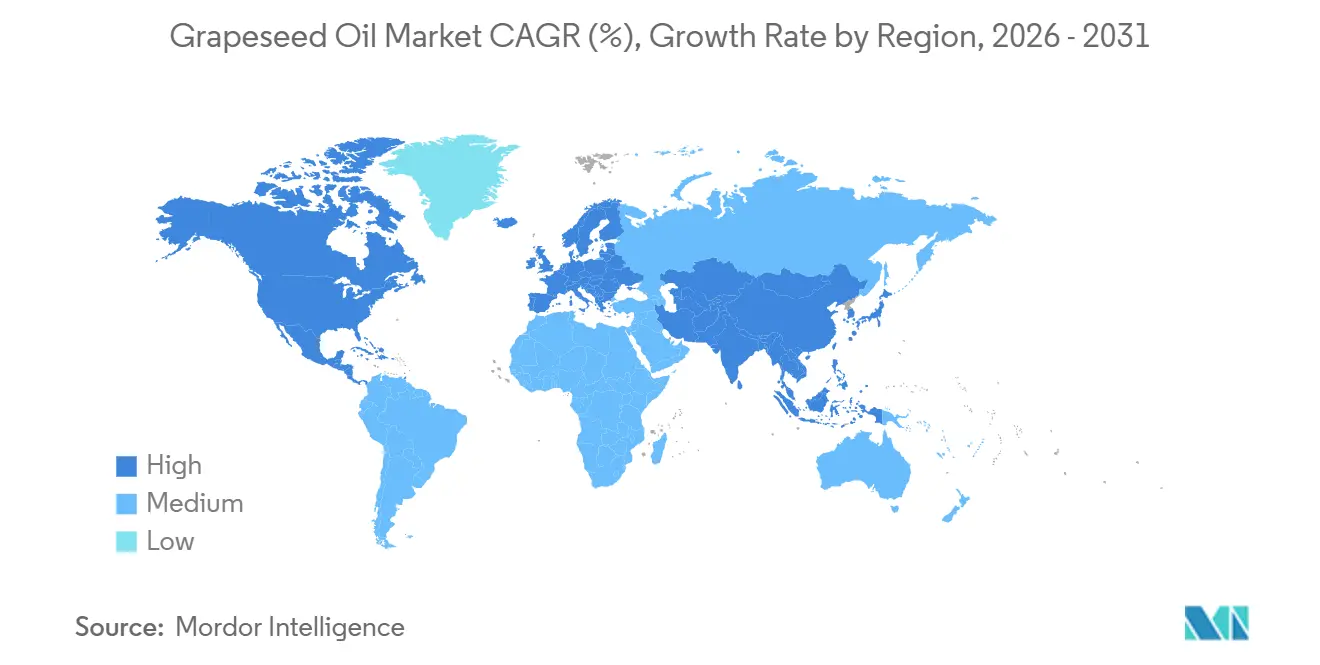

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

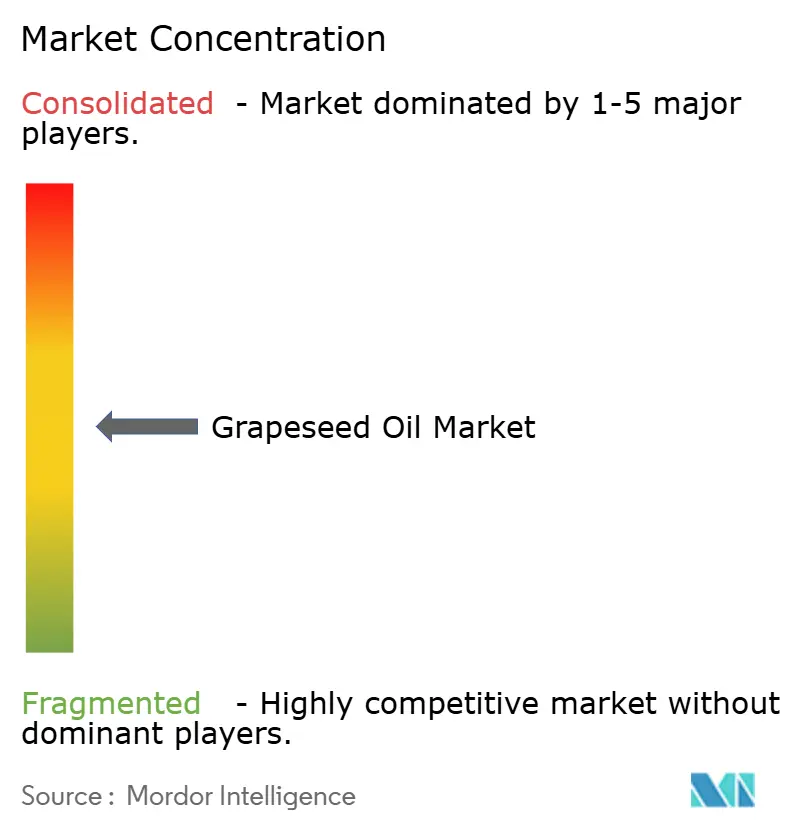

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Grapeseed Oil Market Analysis by Mordor Intelligence

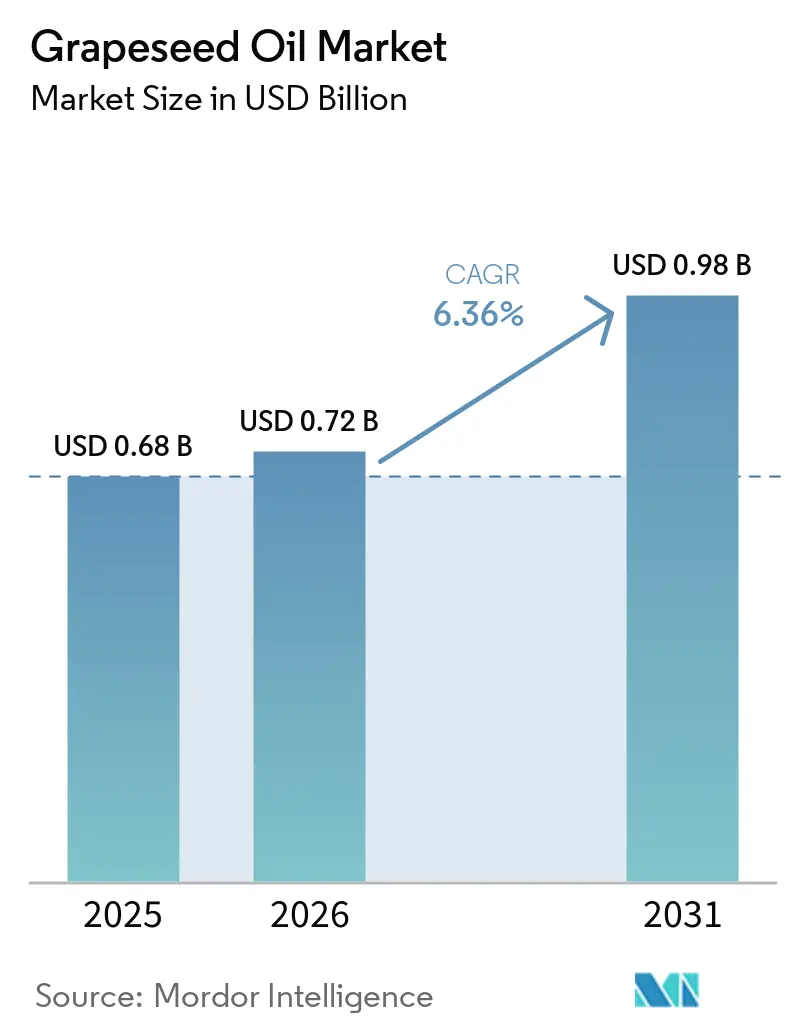

The grapeseed oil market was valued at USD 0.68 billion in 2025 and is projected to reach USD 0.98 billion by 2031, expanding at a CAGR of 6.36% during the 2026–2031 forecast period. The market currently stands at USD 0.72 billion in 2026, driven by increasing demand for functional plant-based oils across food processing, personal care, and nutraceutical applications. Growth is supported by grapeseed oil's unique lipid profile, particularly its linoleic acid content, which constitutes 60–76% of total fatty acids. Grapeseed oil's neutral flavor, light texture, and relatively high smoke point make it versatile for various cooking methods, including sautéing, roasting, frying, and baking. This versatility has led to its adoption among households, foodservice operators, and food manufacturers. Additionally, the oil is gaining traction in premium skincare, haircare, massage oils, and cosmetic formulations due to its emollient properties and the growing consumer preference for naturally derived ingredients. The increasing demand for clean-label products and plant-based formulations is further broadening its application across multiple end-use industries.

Key Report Takeaways

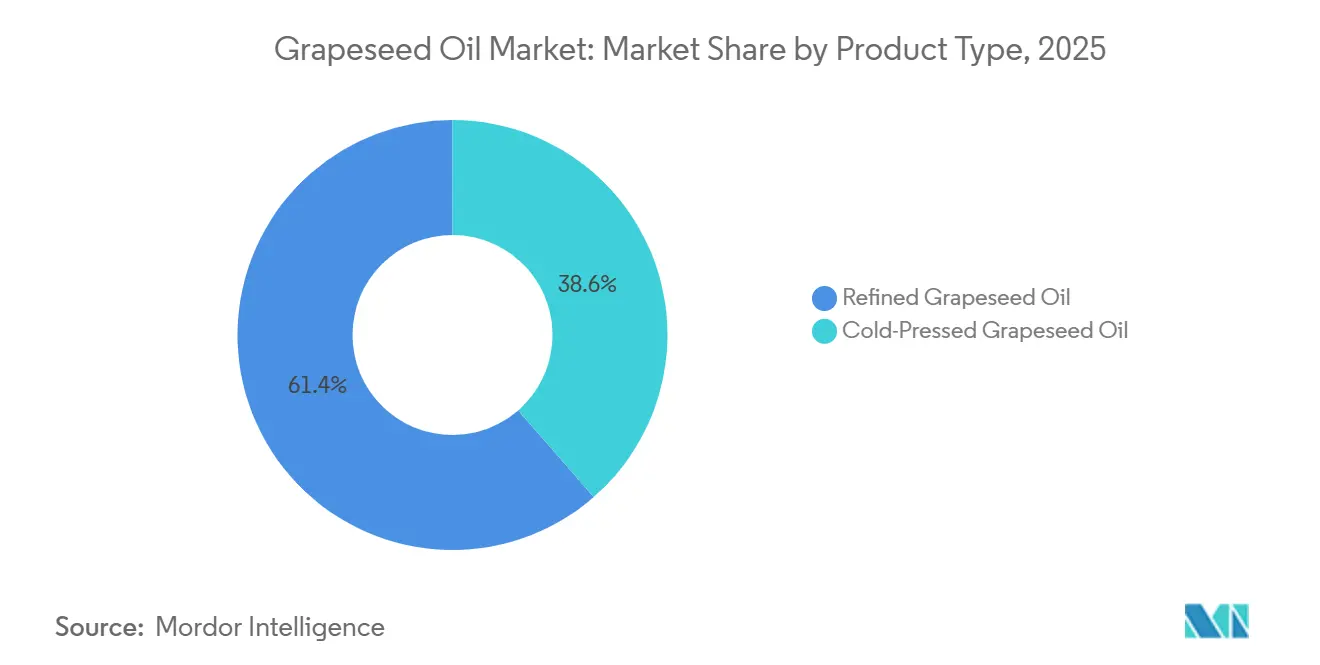

- By product type, refined grapeseed oil captured 61.41% of the 2025 market, while cold-pressed grapeseed oil is advancing at a 6.99% CAGR through 2031.

- By nature, conventional oils retained an 83.33% share of the grapeseed oil market size in 2025, while the organic segment is forecast to grow at a 7.16% CAGR through 2031.

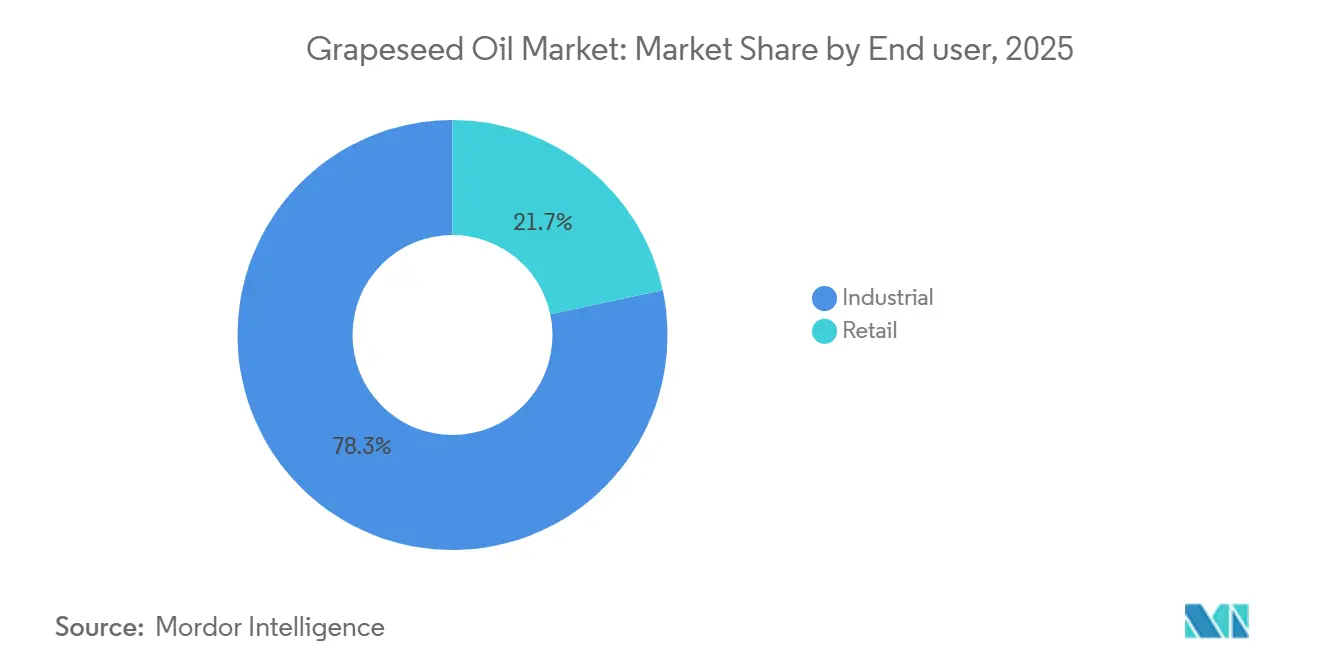

- By end user, industrial commanded 78.34% of demand in 2025, whereas retail is expanding fastest at 6.87% CAGR between 2026-2031.

- By geography, North America accounted for 33.02% of 2025 revenue, but Asia-Pacific is the fastest-growing region, with a 7.11% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Grapeseed Oil Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for heart-healthy cooking oils | +1.8% | Global, concentrated in North America and Northern Europe | Medium term (2-4 years) |

| Clean label and plant-based beauty adoption | +1.2% | North America, Western Europe, Japan | Medium term (2-4 years) |

| Premiumization in functional and gourmet foods | +0.8% | North America, Western Europe, East Asia | Long term (≥ 4 years) |

| Growing demand for clean-label and naturally derived ingredients | +0.7% | Global, early gains in European Union and North America | Short term (≤ 2 years) |

| Byproduct utilization from winemaking waste streams | +0.5% | European Union wine belt (France, Spain, Italy), South America (Chile, Argentina), South Africa | Long term (≥ 4 years) |

| Increasing use in nutraceuticals | +0.6% | North America, East Asia, emerging adoption in South Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising demand for heart-healthy cooking oils

The increasing prevalence of cardiovascular health concerns is prompting consumers to adopt healthier dietary practices, thereby driving demand for heart-friendly cooking oils such as grapeseed oil. Renowned for its high levels of polyunsaturated fatty acids, particularly linoleic acid, grapeseed oil is being increasingly utilized in home cooking, foodservice, and packaged food formulations. This trend reflects a growing consumer preference for alternatives to oils with less favorable fat profiles. The emphasis on preventive health and nutrition-focused food choices is bolstering the market position of specialty plant-based oils that support heart-health objectives. The rising incidence of coronary heart disease (CHD) further underscores this trend. In the financial year ending March 2025, approximately 1.9 million individuals, representing 3% of the population, were diagnosed with CHD by general practitioners (GPs) in England [1]Source: Office for Health Improvement and Disparities, "Cardiovascular disease profiles: short statistical commentary", gov.uk. As awareness of cardiovascular health risks grows, consumers are paying closer attention to the nutritional properties of cooking oils and food ingredients. This increasing preference for healthier fat sources is driving demand for grapeseed oil across both retail and industrial food applications, contributing to consistent market growth.

Clean label and plant-based beauty adoption

The growing preference for clean-label and plant-based beauty products is driving the expansion of the grapeseed oil market. Consumers are increasingly attentive to the ingredients in skincare and haircare products, favoring naturally derived, plant-based components over synthetic options. This trend is prompting cosmetic manufacturers to use botanical oils that meet consumer demands for transparency, sustainability, and simplicity in formulations. Grapeseed oil is becoming more prominent in beauty and personal care applications due to its lightweight texture, moisturizing benefits, and versatility in various skincare and haircare formulations. It is widely incorporated into facial serums, moisturizers, body oils, hair treatments, and massage products as brands diversify their natural and clean-label product lines. With the rising demand for plant-based beauty solutions, grapeseed oil is anticipated to see broader application as a multifunctional ingredient in the global personal care market.

Premiumization in functional and gourmet foods

The increasing trend of premiumization in functional and gourmet foods is driving the demand for grapeseed oil, particularly among consumers prioritizing high-quality ingredients that offer both culinary performance and perceived wellness benefits. Grapeseed oil is gaining recognition as a premium specialty oil due to its mild flavor, versatility in cooking, and favorable fatty acid profile. Food manufacturers, gourmet brands, and specialty retailers are incorporating grapeseed oil into premium dressings, marinades, sauces, functional foods, and health-focused formulations to meet the preferences of consumers willing to pay a premium for differentiated, value-added products. The robust growth of the functional food market further reinforces this trend. In Europe, the United Kingdom accounts for 23% of functional and fortified food and beverage sales, followed by Germany (16%), France (12%), Spain (10%), and Italy (9%)[2]Source: Glanbia Nutritionals, "Opportunities in Fortifying Functional Food and Beverage in Europe", glanbianutrition.com . As consumers increasingly seek products that combine nutrition, functionality, and premium quality, the demand for specialty ingredients like grapeseed oil is expected to grow. This trend is particularly prominent in Europe, where manufacturers are leveraging grapeseed oil's plant-based origin and premium positioning to enhance the appeal of both food and wellness-oriented products.

Growing demand for clean-label and naturally derived ingredients

The increasing consumer preference for clean-label and naturally derived ingredients is a key factor driving the grapeseed oil market. Consumers are paying closer attention to ingredient lists and prefer products made with recognizable, minimally processed, and plant-based components. This trend is particularly evident among younger demographics, such as Gen Z and Millennials. These groups are willing to spend 20–30% more on products labeled as organic, natural, high-protein, or free from artificial ingredients[3]Source: Ingredion, "Less mystery, more meaning: Clean labels win consumer preference", ingredion.com. Grapeseed oil, being a naturally derived product from grape seeds, aligns with these clean-label preferences and is increasingly used in food, nutraceutical, and personal care applications. To address the growing demand for ingredient transparency, natural sourcing, and simplified labels, manufacturers are incorporating grapeseed oil into premium product formulations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Seasonal dependence on grape harvest volumes | -1.2% | European Union wine belt (France, Italy, Spain), South America, South Africa | Short term (≤ 2 years) |

| Strong competition from established premium oils | -1.0% | Global, intensified in North America and Western Europe | Medium term (2-4 years) |

| Regulatory ambiguity and health claim restrictions limiting marketing flexibility | -0.6% | Global, with notable impact in the European Union and the United States markets | Long term (≥ 4 years) |

| Concerns regarding solvent-based extraction methods | -0.5% | Western Europe (EFSA mandate), North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Seasonal dependence on grape harvest volumes

Seasonal dependence on grape harvest volumes poses a significant challenge for the grapeseed oil market, as the oil is primarily derived from grape seeds, a by-product of wine and grape-processing activities. The availability of raw materials is closely tied to annual grape harvest yields, which are subject to fluctuations caused by weather conditions, vineyard diseases, droughts, and other agricultural factors. These variations in grape production directly impact the supply of grape seeds available for oil extraction, creating difficulties for manufacturers in maintaining consistent production volumes. This reliance on harvest cycles often results in supply constraints and raw material availability issues, particularly in key grape-producing regions. Grapeseed oil producers have limited control over the generation of grape seeds, making them vulnerable to fluctuations in wine production and grape processing activities. As demand for grapeseed oil grows across food, nutraceutical, and personal care applications, the industry's dependence on seasonal grape harvests may lead to supply-side pressures, restricting market growth and affecting long-term supply stability.

Strong competition from established premium oils

Strong competition from established premium oils presents a notable restraint on the grapeseed oil market. Grapeseed oil competes with a wide range of specialty and health-focused oils, including olive oil, avocado oil, coconut oil, flaxseed oil, and walnut oil, many of which benefit from stronger consumer awareness, established health perceptions, and broader retail availability. These competing oils often have well-developed brand recognition and loyal consumer bases, making it challenging for grapeseed oil to differentiate itself and expand market share. The competitive landscape is further intensified by continuous product innovation and marketing investments from leading premium oil brands. Consumers seeking functional, gourmet, or wellness-oriented oils are often presented with multiple options that share similar positioning on natural sourcing, healthy fats, and culinary versatility. As a result, grapeseed oil manufacturers must invest in consumer education, product differentiation, and premium branding to effectively compete against more established specialty oil categories, which can limit adoption and slow market penetration in certain regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Cold-Pressed Grades Emerging as the Margin Growth Driver

Refined grapeseed oil accounted for 61.41% of the market in 2025, primarily due to its extensive use in high-volume industrial applications such as commercial kitchen frying, food ingredient processing, bulk cosmetics manufacturing, and industrial blending. Its RBD (refined, bleached, deodorized) processing compatibility, extended shelf life, and consistent fatty acid composition make it the preferred choice for large-scale formulation buyers seeking reliable supply at contracted volumes. This dominance highlights its critical role in meeting the demands of industrial buyers.

Cold-pressed grapeseed oil is expected to grow at a CAGR of 6.99% during 2026–2031, the fastest among all product types. This growth is driven by demand in premium food retail, clean beauty formulations, and direct-to-consumer health channels that emphasize minimal processing and preserved micronutrient content. The increasing consumer preference for natural and minimally processed products further supports the expansion of cold-pressed grapeseed oil in these segments.

By Nature: Organic Segment Outpacing Market Growth Across All Geographies

Conventional grapeseed accounted for 83.33% of the nature segment in 2025. This dominance is attributed to its cost efficiency, widespread availability from European and South American winery co-products, and established supply chain relationships with bulk industrial buyers in food processing and commercial cosmetics. However, organic grapeseed oil is expected to grow at a CAGR of 7.16% during 2026–2031, surpassing the overall market growth by 80 basis points.

This growth in organic grapeseed oil is driven by mandatory organic sourcing requirements from European clean beauty brands, North American premium grocery chains, and nutraceutical formulators, alongside an increasing number of organically certified vineyards. The price gap between organic and conventional grades is particularly significant in the cosmetics industry. COSMOS ORGANIC-certified cold-pressed oil supports price premiums that more than compensate for the higher costs associated with sourcing from certified winery operations.

By End User: Industrial Dominance Anchored Across Sub-Sectors, Retail Accelerating

Industrial end-users accounted for 78.34% of the grapeseed oil market in 2025, with key industrial sub-categories including food and beverages, cosmetics and personal care, and dietary supplements. In the food and beverages segment, grapeseed oil is utilized as a frying medium, a base for salad dressings, a component in marinades, and a functional gourmet ingredient in commercial kitchens, food manufacturing, and private-label grocery products. In cosmetics and personal care, the oil is primarily used as a carrier oil in serums, face moisturizers, and hair care products, valued for its light texture and high skin absorption rate. The dietary supplements sub-segment is experiencing growth, particularly in North America and East Asia, where grapeseed oil is used both as a standalone antioxidant supplement and as a carrier for fat-soluble bioactives.

The retail segment, the fastest-growing end-use category with a CAGR of 6.87% during 2026–2031, is driven by increasing direct-to-consumer wellness spending, the expansion of specialty food e-commerce, and the premiumization of cooking oils for household use. This growth reflects changing consumer preferences toward healthier and higher-quality cooking oils, alongside the rising popularity of specialty food products. Additionally, the retail market benefits from advancements in e-commerce platforms, which have made premium grapeseed oil products more accessible to consumers globally.

Geography Analysis

North America held 33.02% of the global grapeseed oil market in 2025, representing the largest regional share. This dominance is supported by a strong health-conscious consumer base, a well-established premium specialty food retail infrastructure, and a robust cold-pressed grapeseed oil industry concentrated in California's wine regions. The United States leads in demand, with foodservice and premium specialty retail channels accounting for the highest volumes. Canada is experiencing growing adoption of organic grapeseed oil in natural food grocery stores, while Mexico shows emerging industrial demand in food processing.

The Asia-Pacific region is the fastest-growing grapeseed oil market, with a projected CAGR of 7.11% during the forecast period. Growth is driven by rising disposable incomes, expanding food processing industries, and increasing demand for premium plant-based oil ingredients in the cosmetics sector. China and India together account for over 55% of the region's grapeseed oil volume, with food and beverage processing being the primary application. Japan and South Korea represent high-value markets, where cold-pressed and premium cosmetic-grade grapeseed oil are growing at an annual rate of approximately 9–11%, fueled by their use in nutraceuticals and premium skincare products.

Europe serves as both the leading production hub and a significant consumption market for grapeseed oil. The region produces the majority of globally traded refined and cold-pressed volumes, primarily from the wine-producing regions of France, Spain, Italy, Germany, and the Netherlands. France, Italy, and Spain collectively contribute 65–75% of the European Union's grapeseed oil production. Meanwhile, the Netherlands and Germany play critical roles as refining, blending, and re-export distribution centers for both European and global markets.

Competitive Landscape

The grapeseed oil market is moderately fragmented, with the top five producers accounting for an estimated 40–50% of Europe's refined oil processing capacity. Key integrated players, including Borges Agricultural and Industrial Edible Oils, Tampieri Group, Mediaco Vrac, Alvinesa Natural Ingredients, and Gustav Heess, benefit from vertically integrated supply chains. These supply chains encompass winery pomace sourcing, solvent and cold-press extraction, refining, and export logistics, providing a structural competitive advantage.

Smaller and mid-sized producers focus on differentiation through organic certification, geographic indications (such as Napa Valley and French AOC wine regions), and COSMOS compliance. These strategies target premium cosmetics and specialty food segments, where price sensitivity is relatively lower. Technology is also becoming a competitive factor. Producers adopting supercritical CO2 extraction, a solvent-free method that yields cosmetic and nutraceutical-grade oils, achieve price premiums of 50–100% over conventional refined oils. This method also offers potential protection against stricter regulations on hexane-extracted products.

Opportunities exist in pharmaceutical-grade oil for excipient and topical drug delivery applications. Compliance with European Pharmacopoeia and US Pharmacopoeia specifications creates significant technical barriers to entry, supporting stable, high-margin demand in this segment. Additionally, a disruptive trend is emerging with direct partnerships between wineries and oil processors. This model bypasses commodity trading intermediaries, enabling traceability documentation that supports premium clean-label claims in both food and personal care markets.

Grapeseed Oil Industry Leaders

-

Borges Agricultural and Industrial Edible Oils, S.A.U.

-

Tampieri Group

-

Group Mediaco

-

Gustav Heess Oleochemische Erzeugnisse GmbH

-

Oleificio Salvadori S.r.l.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: IMAGE Skincare has expanded its physician-developed IMAGE MD medical-grade skincare line with three new clinically proven products focused on skin longevity, barrier repair, and post-procedure recovery. The new products include the Biotech Longevity Crème, featuring an NAD+ booster and proprietary XOSM™ technology to address visible signs of aging; the Barrier Recovery Balm, formulated to restore the skin barrier and soothe sensitive or compromised skin; and the Gentle Cleansing Balm, an oil-based cleanser with grapeseed oil and botanical ingredients for gentle cleansing and recovery support.

- March 2026: Pietro Coricelli, an Italian edible oils company, has introduced a new range of seed oils tailored for specific cooking applications, reflecting the increasing consumer demand for specialized and functional cooking oils. The portfolio includes sunflower oil, high-oleic sunflower oil for frying (Friggiamo), corn oil, peanut oil, and Viviamo, a premium blend of avocado oil, grapeseed oil, and sunflower oil, designed for consumers seeking wellness-oriented and lighter oil options.

- May 2025: Tampieri Financial Group, an Italian agri-food company specializing in vegetable oils and animal feed products, has acquired 100% of Italcol S.p.A., a producer of crude oils derived from sunflower seeds, grapeseeds, rapeseed, and virgin olive pomace. This acquisition enhances Tampieri's position in the vegetable oils market by expanding its raw material sourcing capabilities, product portfolio, and processing expertise.

Global Grapeseed Oil Market Report Scope

| Refined Grapeseed Oil |

| Cold-Pressed Grapeseed Oil |

| Conventional |

| Organic |

| Retail | |

| Industrial | Food and Beverages |

| Cosmetics and Personal Care | |

| Dietary Supplements | |

| Other Industrial Applications |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Spain | |

| Italy | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Thailand | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Refined Grapeseed Oil | |

| Cold-Pressed Grapeseed Oil | ||

| By Nature | Conventional | |

| Organic | ||

| By End user | Retail | |

| Industrial | Food and Beverages | |

| Cosmetics and Personal Care | ||

| Dietary Supplements | ||

| Other Industrial Applications | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Spain | ||

| Italy | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Thailand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size and growth outlook of the grapeseed oil market?

The grapeseed oil market was valued at USD 0.68 billion in 2025 and reached USD 0.72 billion in 2026. It is projected to grow to USD 0.98 billion by 2031, registering a CAGR of 6.36% during the forecast period from 2026 to 2031.

Which product type accounts for the largest share of the grapeseed oil market?

Refined grapeseed oil accounted for the largest share, representing 61.41% of the global market in 2025.

Which segment is expected to grow the fastest in the grapeseed oil market?

Cold-pressed grapeseed oil is anticipated to be the fastest-growing product type, with a CAGR of 6.99% during the 2026–2031 period.

Which region dominates the grapeseed oil market, and which region is expected to witness the highest growth?

North America held the largest share of the grapeseed oil market in 2025, accounting for 33.02% of total revenue.

Page last updated on: