Industrial Oils Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

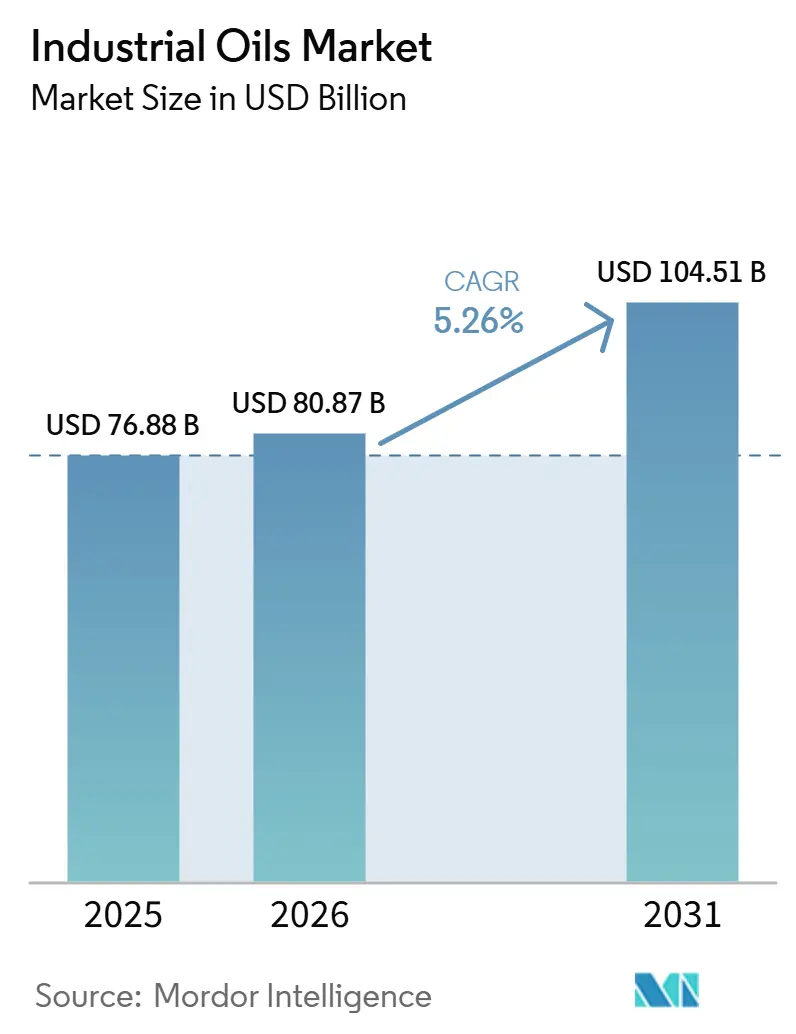

| Market Size (2026) | USD 80.87 Billion |

| Market Size (2030) | USD 104.51 Billion |

| Growth Rate (2026 - 2031) | 5.26% CAGR |

| Fastest Growing Market | South America |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Industrial Oils Market Analysis by Mordor Intelligence

The industrial oils market size was valued at USD 76.88 billion in 2025 and estimated to grow from USD 80.87 billion in 2026 to reach USD 104.51 billion by 2031, at a CAGR of 5.26% during the forecast period (2026-2031). The industrial oils market is expanding because biofuel policy is driving larger volumes of vegetable oils into energy use, while regulated end uses such as cosmetics and pharmaceuticals are demanding cleaner, better-documented inputs. The industrial oils market is also benefiting from wider substitution of fossil-derived materials in specialty applications, especially where plant-based oils offer compliance and performance advantages under stricter product and sourcing rules. Competitive behavior is shifting as large processors build scale through consolidation, while specialty suppliers focus on traceability, certification, and application-specific grades that are harder to replace. This leaves the industrial oils market with a balanced growth profile where policy support, downstream processing, and tighter procurement standards are all raising the value of dependable feedstock access and compliant production systems. The same forces are also increasing pressure on procurement teams, as buyers now need to manage price risk, regulatory documentation, and supply continuity simultaneously.

Key Report Takeaways

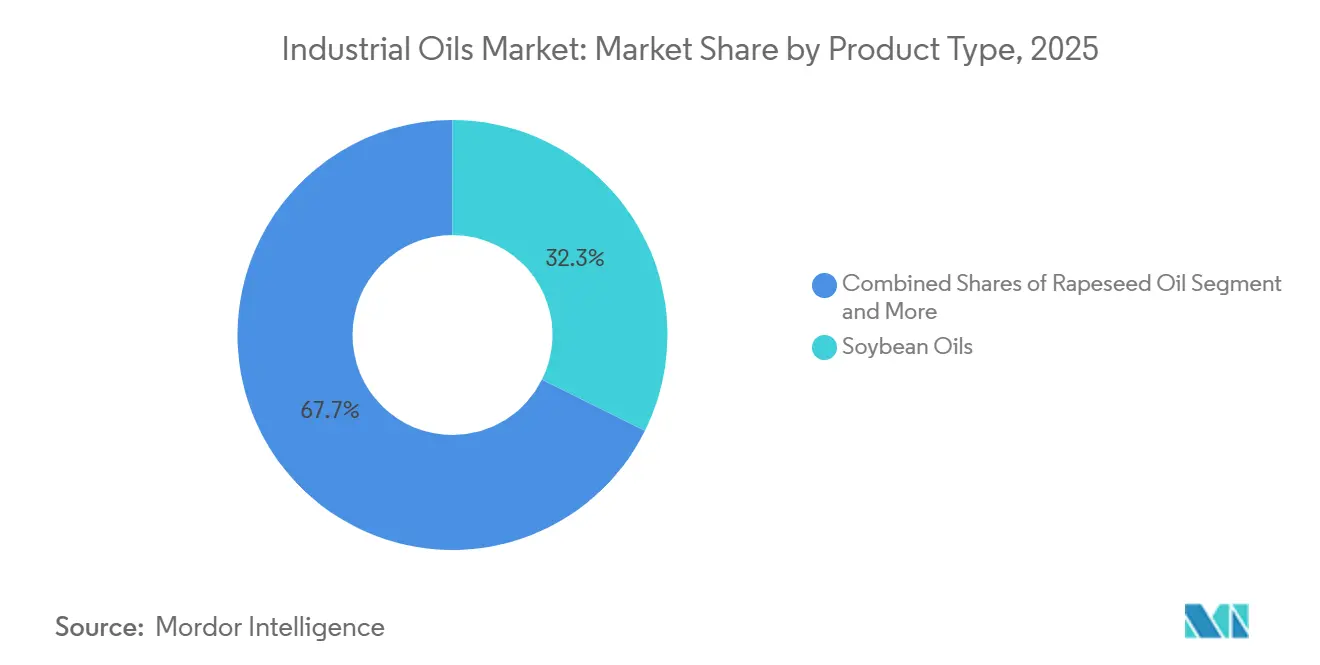

- By source type, soybean oils led with 32.34% of the industrial oils market share in 2025, while rapeseed oils are expected to grow at a 6.72% CAGR through 2031.

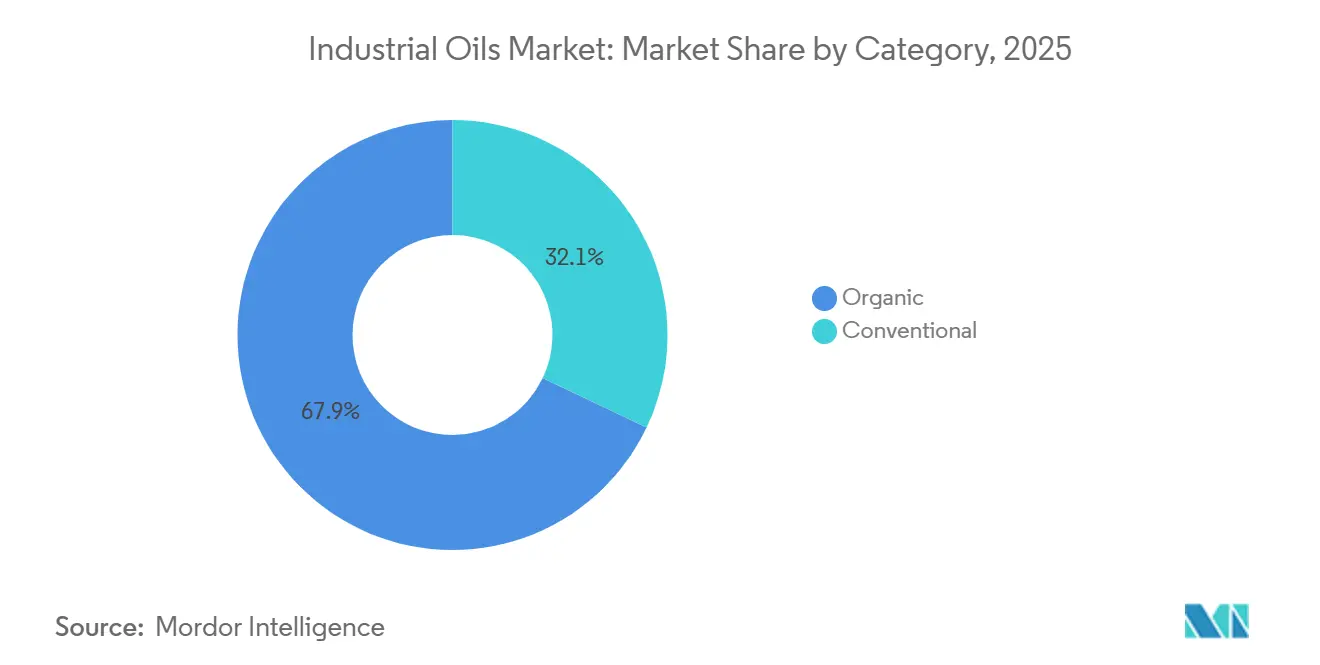

- By category, conventional grades accounted for 82.79% of the industrial oils market in 2025, while organic grades expanded at a 7.15% CAGR through 2031.

- By end use, biofuels accounted for 32.08% of the industrial oils market share in 2025 and are also projected to advance at a 6.59% CAGR through 2031.

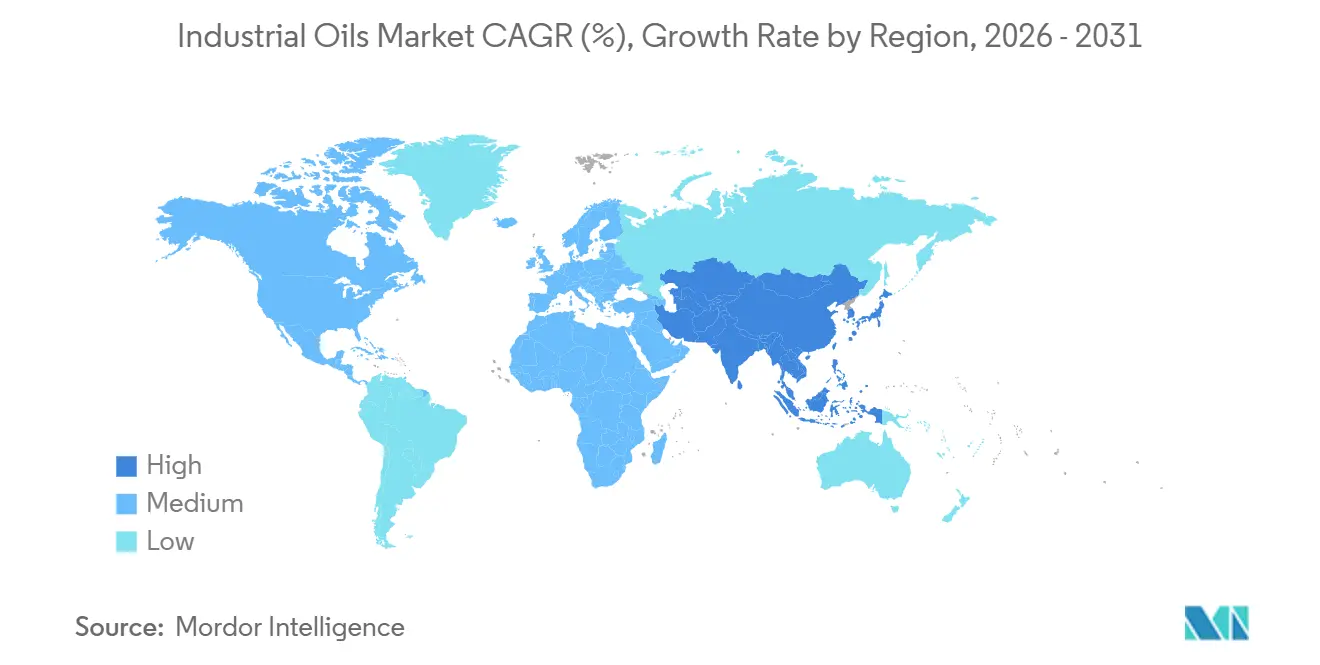

- By geography, Asia-Pacific led with 42.59% of 2025 sales, whereas South America is projected to register the fastest growth, at a 6.87% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Industrial Oils Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Bio-Based and Low-Carbon Industrial Oils | +1.4% | Global, led by EU, USA, Indonesia, Brazil | Short term (≤ 2 years) |

| Tightening End-Use Specifications in Food, Cosmetics, and Pharmaceuticals | +0.8% | North America and Europe | Medium term (2-4 years) |

| Substitution of Fossil-Derived Inputs in Process and Specialty Applications | +1.2% | Global | Medium term (2-4 years) |

| Growth in Oleochemical and High-Value Downstream Processing Capacity | +0.9% | Asia-Pacific core, spillover to South America | Long term (≥ 4 years) |

| OEM Push for Higher-Purity and Application-Specific Oil Grades | +0.5% | North America, Europe, Japan | Medium term (2-4 years) |

| Traceable Feedstock Sourcing as a Procurement Differentiator | +0.4% | Global, with early intensity in Europe and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Bio-Based and Low-Carbon Industrial Oils

The industrial oils market is seeing a clear shift toward plant-based feedstocks as fuel, chemical, and industrial users move away from fossil-linked inputs. In the United States, soybean oil use in biomass-based diesel production reached 6.1 billion pounds from October 2025 through March 2026, which shows how strongly energy demand is pulling on edible oil supply chains. USDA also projected global vegetable oil industrial use at 58.8 million metric tonnes for MY 2026/27, confirming that this demand shift is broad rather than limited to one country or policy system[1]Source: U.S. Food and Drug Administration, “Cosmetic Ingredients,” U.S. Food and Drug Administration, fda.gov. Indonesia had already absorbed 14.2 billion liters of palm biodiesel under its B40 program in 2025, demonstrating how domestic blending policy can reallocate large volumes of feedstock within a producing country. As the industrial oils market adjusts to these changes, processing assets that once served only food demand are increasingly treated as part of energy and low-carbon infrastructure. That raises the value of certified, scalable, and policy-aligned oil supply more than simple volume growth would suggest.

Tightening End-Use Specifications in Food, Cosmetics, and Pharmaceuticals

The industrial oils market is also being shaped by stricter product specifications in regulated end uses, especially where purity and ingredient traceability now influence supplier qualification. In the United States, FDA oversight under the cosmetics framework requires stronger ingredient documentation and safety support, which affects how vegetable oil inputs are selected for personal care formulations. In Europe, Regulation (EC) 1223/2009 continues to support closer scrutiny of cosmetic ingredients, which increases the need for verified quality and consistent composition in oil-derived inputs[2]Source: European Union, “Regulation (EC) 1223/2009 on Cosmetic Products,” EUR-Lex, eur-lex.europa.eu . Croda’s 2025 annual report showed the company continuing to build on high-purity lipid systems for pharmaceutical and personal care uses, reflecting the premium being placed on refined, specification-led materials. In practical terms, this means the industrial oils market is no longer divided only by feedstock type or price. It is increasingly divided by whether a supplier can meet documentation, consistency, and regulatory access requirements that buyers now treat as standard.

Substitution of Fossil-Derived Inputs in Process and Specialty Applications

Rapeseed and palm-based derivatives are actively displacing mineral oils and petrochemical fluids in transformer fluids, process lubricants, coatings, and specialty chemical manufacturing. Cargill's approximately USD 30 million investment to triple the European production capacity of its FR3® natural ester dielectric fluid at Gouda, Netherlands, in March 2026 directly reflects the accelerating substitution of mineral transformer oil with bio-based alternatives, driven by European grid expansion programs. In Germany, Verbio is deploying a new ethenolysis plant, expected to be operational in 2026, to produce 32,000 tonnes of rapeseed oil-derived specialty oleochemicals for motor, transmission, and wind turbine applications, a direct fossil-lubricant substitution at an industrial scale. The less-obvious implication is that the buildout of EV charging infrastructure and the expansion of renewable energy substations are likely to accelerate demand for natural ester-based transformer fluids beyond traditional utility maintenance cycles, creating a durable structural pull that is not visible in conventional biofuel demand forecasts.

Growth in Oleochemical and High-Value Downstream Processing Capacity

The industrial oils market continues to gain from deeper downstream processing, because value creation is moving beyond simple crushing and refining. Southeast Asia remains central to oleochemical activity, while other producing regions are seeking to retain more value by processing feedstocks closer to their origins. Brazil’s Fuels of the Future policy path is encouraging a broader industrial base around soybean oil, since each increase in the biodiesel blend rate draws more oil into domestic use and supports investment logic across the chain. Bunge’s decision to build a new oilseed processing plant in Destrehan, Louisiana, through its joint venture with Chevron, also shows that processing investment is following renewable fuel and industrial demand expectations in North America. As a result, the industrial oils market is being supported not only by end-use growth but also by a larger installed base of facilities that can channel oils into higher-value industrial applications. Over time, that makes regional processing depth almost as important as raw crop supply.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Feedstock Availability and Price Spreads | -1.5% | Global | Short term (≤ 2 years) |

| Sustainability Compliance and Certification Costs | -0.8% | Europe and North America | Medium term (2-4 years) |

| Performance Trade-Offs Versus Petrochemical Alternatives | -1.2% | Global | Long term (≥ 4 years) |

| Supply Chain Concentration in Key Oilseed Origins | -0.9% | Asia-Pacific and South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Feedstock Availability and Price Spreads

The industrial oils market remains exposed to feedstock volatility because policy-led demand is rising faster than supply flexibility in several major oilseed systems. France’s Ministry of Agriculture noted that more than 27% of global rapeseed, 24% of soybean, and 17% of palm oil were directed to biofuels in 2024, which shows how much of the oil pool is already committed to energy use[3]Source: French Ministry of Agriculture, “Tout Savoir sur les Biocarburants,” French Ministry of Agriculture, agriculture.gouv.fr. In Brazil, each 1 percentage-point increase in the biodiesel blend rate requires around 400,000 additional tonnes of soybean oil, which means even small policy shifts can materially tighten availability for other industrial uses. When this policy pressure overlaps with weather and disease risks and uneven crop cycles, price spreads can widen quickly across oils and regions. That creates a more challenging operating environment for mid-sized processors and industrial buyers without global origination options. In the industrial oils market, volatility is therefore not just a procurement issue. It shapes margins, contract behavior, and the ability to commit to long-term industrial supply.

Sustainability Compliance and Certification Costs

The industrial oils market also faces a cost burden from sustainability compliance, as certification requirements are becoming more detailed while premiums are not always reliable. BASF stated that it shifted its 100% certified key palm derivatives target to 2030, citing limited market availability of certified palm kernel oil and economic feasibility concerns. RSPO’s updated certification system adds greater rigor to verification and monitoring, improving credibility but also increasing operational demands across the chain. For smaller processors and buyers in margin-sensitive applications, audit costs, segregation requirements, and extra documentation can erode the commercial case for bio-based sourcing. This is especially relevant in the industrial oils market, where some end uses can absorb certification costs and others cannot. The result is a gradual tilt toward larger, integrated suppliers that can spread compliance spending across a broader asset base.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Soybean and Rapeseed Oils Redefine the Feedstock Hierarchy

Soybean oils accounted for 32.34% of the market in 2025, making them the largest product type in the industrial oils market size profile that year. This leadership reflects deep crush capacity across China, the United States, and Brazil, along with the strong pull from biomass-based diesel and biodiesel programs. USDA showed that U.S. soybean oil use in biomass-based diesel reached 6.1 billion pounds from October 2025 through March 2026, while global oilseed trade projections continued to support high soybean relevance in industrial channels. USDA also projected global soybean and oilseed flows at levels that support continued availability for both energy and non-energy uses, even though demand competition remains intense. Palm oil remains central to Southeast Asian oleochemical systems, but its rising use in domestic biodiesel programs is changing the supply available for export-oriented industrial processing. Sunflower and cottonseed oils continue to serve narrower roles where formulation, regional crop patterns, or end-use requirements matter more than sheer volume.

Rapeseed oils are projected to grow at a 6.72% CAGR through 2031, which makes them the fastest-growing product type in the industrial oils market. Their momentum comes from a favorable policy setting in Europe, where transport decarbonization and renewable feedstock rules continue to support crop-based biodiesel and related industrial demand. RED III set the broader framework for renewable transport energy expansion, while member-state implementation is influencing commercial pull for rapeseed-based pathways. USDA reporting on EU biofuel mandates also showed that changes in member-state treatment of waste-based routes are improving the relative position of crop-based rapeseed biodiesel in key markets such as Germany and the Netherlands. That gives rapeseed oil a stronger industrial growth path than a simple food-versus-fuel comparison would suggest. It also helps explain why the industrial oils industry is seeing more value shift toward conversion and downstream specialization rather than only raw oil output.

By Category: Conventional Grades Anchor the Base, Organic Premiums Lift Growth

Conventional grades held 82.79% of the market in 2025, which means they still formed the operating base of the industrial oils market. Their position is supported by lower cost, wider supply availability, and established use across biofuels, paints and coatings, feed, and other volume-driven applications. Buyers in these segments often prioritize dependable throughput and price efficiency, which keeps conventional soybean, palm, and mixed vegetable oils in regular use. This part of the industrial oils market remains highly exposed to feedstock reallocation, because any policy-driven diversion toward fuel can narrow availability for non-fuel industrial customers. Conventional grades, therefore, remain dominant, but their pricing and margin conditions are becoming less predictable. That is making supply security and sourcing flexibility more important than they were in earlier cycles.

Organic grades accounted for 17.21% of the market in 2025 and are projected to grow at a 7.15% CAGR through 2031, making them the fastest-moving category in the industrial oils market. The demand is not limited to premium food positioning, as regulations and buyer standards also support verified and segregated oil sourcing for cosmetics and pharmaceutical applications. In Europe, cosmetic ingredient rules continue to reinforce the need for documented composition and quality consistency, while in the United States FDA oversight has increased the focus on ingredient support and supplier accountability. Croda’s work in high-purity and specialty lipid systems shows that growth in premium oils increasingly comes from technical and regulatory use cases rather than simple brand positioning. That makes the category more durable than a narrow luxury trend. It also shows how the industrial oils industry is becoming more segmented by documentation and application fit.

By End-Use: Biofuels Set the Pace While Regulated Uses Create Premium Niches

Biofuels held 32.08% of the market in 2025 and also posted the fastest growth, with a 6.59% CAGR through 2031, giving them the leading role in the industrial oils market share outlook. This position is grounded in policy rather than in discretionary demand, making it one of the strongest demand anchors in the full market structure. USDA projected global vegetable oil industrial use at 58.8 million metric tonnes for MY 2026/27, with growth supported by large biofuel programs in countries such as Indonesia, Brazil, and the United States. Brazil’s biodiesel blending path also illustrates how fuel policy converts directly into soybean oil demand, with each 1 percentage-point increase requiring around 400,000 additional tonnes. That kind of policy-backed demand gives biofuels pricing protection that other end uses do not always have. It is one reason the industrial oils market is being reorganized around energy-linked allocation.

The other end uses are smaller in volume, but they matter because they shape margin quality and supplier specialization in the industrial oils market. Cosmetics and personal care, pharmaceuticals, and food applications are increasingly influenced by purity standards, traceability, and ingredient performance. Croda’s June 2026 collaboration with NovoArc to expand its pharmaceutical-grade lipid offering showed how suppliers are building around higher-value formulations rather than commodity oil alone. Paints and coatings still provide a useful non-fuel outlet, especially where bio-based resins and lower-emission formulations support industrial oil demand. Animal feed remains tied to the broader crush system, because stronger soybean processing raises meal output while also affecting oil supply balance. Together, these end uses do not overturn biofuel leadership, but they create profitable niches that can matter more than share alone.

Geography Analysis

Asia-Pacific accounted for 42.59% of the industrial oils market in 2025, maintaining its lead among regions. The region combines Indonesia and Malaysia’s importance in palm oil with China’s position as the largest soybean crusher, making it the most influential area for both feedstock supply and downstream industrial use. Indonesia’s 2025 biodiesel program had already absorbed 14.2 billion liters of palm biodiesel under B40, demonstrating how quickly domestic policy can reshape feedstock allocation across Asia-Pacific. India also showed strong policy execution by reaching its E20 ethanol blending target ahead of schedule in June 2025, reinforcing the region’s willingness to use biofuel policy as an industrial demand lever. At the same time, RSPO’s tighter certification rules are adding a stronger compliance layer to palm-based supply chains across the region. That favors larger integrated producers and makes scale, documentation, and traceability more valuable in the industrial oils market.

South America is projected to be the fastest-growing region, with a 6.87% CAGR through 2031, and the industrial oils market there is being driven mainly by Brazil’s soybean and biodiesel systems. Brazil’s Fuels of the Future framework is reinforcing a steady pull on soybean oil, with each step-up in blending creating visible demand for domestic processing and industrial use. This keeps the region closely tied to both agricultural output and energy policy, which is why South America is growing faster than more mature markets. Europe remains equally important, but for different reasons, because the industrial oils market there is shaped more by regulation, formulation, and value-added processing than by raw feedstock abundance. France continues to direct a large share of rapeseed oil toward biodiesel, and official material from the French Ministry of Agriculture shows how deeply biofuels are embedded in agricultural oil use. RED III and related member-state changes are also supporting the commercial case for rapeseed pathways in transport and industrial applications. As a result, Europe does not lead by volume, but it remains central to technology adoption, sourcing discipline, and high-specification demand.

North America remains anchored by soybean oil and canola oil, and the industrial oils market there is increasingly linked to renewable diesel and biomass-based diesel expansion. USDA continued to show strong soybean oil use in U.S. biomass-based diesel, while Canada’s canola oil crush outlook also pointed to rising use in renewable fuel channels. Bunge and Chevron’s Destrehan processing investment captures this regional pattern, because it is built around oilseed processing for renewable fuel feedstocks rather than traditional commodity throughput alone. The Middle East and Africa remain more mixed in structure, with demand centered on imports for food-grade, cosmetic, and pharmaceutical uses rather than a fully developed processing base. Saudi Arabia and the UAE are important buyers of specialty oils, while South Africa shows the most developed oleochemical demand profile in the region. Nigeria, Egypt, and Morocco are moving more slowly because local processing depth and feedstock security are still limited. This leaves North America as an investment-led supply region, while the Middle East and Africa remain more selective and import dependent in the industrial oils market.

Competitive Landscape

The industrial oils market is led by a group of large agricultural processors and traders, but it is not so concentrated that specialty suppliers are pushed to the margins. Companies such as Cargill, Wilmar, Bunge, and ADM have strong advantages in origination, crushing, refining, and logistics, which gives them clear leverage in large-volume contracts and feedstock management. Bunge’s completion of the Viterra merger in July 2025 was the clearest recent example of this scale strategy, since it expanded the company’s global operating footprint and reinforced its position across oilseed handling and processing. ADM’s USD 103 million modernization of its Decatur operations in 2026 showed the same logic in a different form, with capital directed toward throughput, operating efficiency, and supply reliability in a major soybean processing base. Wilmar’s 2025 annual report also pointed to a more selective capital posture, which suggests its next phase is less about basic capacity buildout and more about extracting value from an already extensive network.

Alongside these scale players, the industrial oils market has a second competitive track made up of companies that sell technical fit, documentation, and formulation value rather than only volume. Croda is a strong example, because its specialty lipids and pharmaceutical delivery focus place it closer to regulated product development than to bulk oil trade. Its June 2026 collaboration with NovoArc further strengthened that position by expanding the pharmaceutical-grade lipid portfolio used in advanced delivery applications. BASF’s public comments on certified palm derivative availability also show that compliance-led sourcing has become a strategic issue for large downstream chemical players, not just a branding topic. Cargill’s certification framework points in the same direction, because verified palm sourcing is now part of how suppliers secure access to demanding buyers. In these segments of the industrial oils market, supplier durability depends on regulatory readiness and qualification discipline as much as on feedstock scale.

This split creates a landscape where the biggest companies do not automatically dominate every profit pool in the industrial oils market. Large processors are strongest where procurement scale, freight control, and crush economics matter most, while specialty suppliers are stronger where purity, certification, and application-specific performance carry more weight. That is why strategic moves are diverging, with Bunge using merger scale, ADM upgrading core processing infrastructure, and Croda expanding into higher-value pharmaceutical lipid systems. Buyers are therefore facing a market where vendor choice depends heavily on end use. A biofuel producer may prioritize feedstock reach and contract security, while a pharmaceutical or cosmetic buyer may place more value on documentation and formulation consistency. That difference is likely to remain important because regulation and procurement scrutiny are becoming tighter rather than looser. In effect, the industrial oils market is growing more competitive at both the commodity end and the specialty end, but the basis of competition is no longer the same across those two spaces.

Industrial Oils Industry Leaders

Cargill, Incorporated

Wilmar International Ltd

Archer Daniels Midland (ADM)

The Scoular Company

Bunge Global SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Cargill invested EUR 56 million across three Belgian facilities, including a EUR 21 million modernization of its Izegem vegetable oil bottling plant, the largest in its European network, nearly doubling production capacity and installing new automated foodservice lines

- June 2026: Croda International's Avanti Polar Lipids subsidiary entered a strategic collaboration with NovoArc GmbH to expand its pharmaceutical-grade lipid portfolio beyond 2,000 products, strengthening the supply of high-purity vegetable oil-derived excipients for pharmaceutical research globally.

- February 2026: ADM announced a USD 103 million investment to modernize key facilities at its Decatur, Illinois headquarters, creating at least 50 new full-time jobs and sustaining over 1,000 existing positions, reinforcing its position as a high-throughput soybean processing hub for biofuel and industrial oil supply.

- July 2025: Bunge Global SA completed its USD 8.2 billion merger with Viterra Limited, creating a company with operations across more than 50 countries, 56 oilseed crushing plants, 47 oil refineries, and over 300 processing and storage facilities globally.

Global Industrial Oils Market Report Scope

Industrial oils are vegetable-based or other plant-derived oils used as raw materials in a wide range of industrial applications, including food processing, biofuels, pharmaceuticals, personal care, and manufacturing. The industrial oils market is segmented by product type, category, end use, and geography. By product type, the market includes soybean oil, palm oil, rapeseed oil, sunflower oil, cottonseed oil, and other industrial oils. Based on category, the market is divided into organic and conventional products. By end use, the market covers biofuel, paints and coatings, cosmetics and personal care, pharmaceuticals, animal feed, food and beverages, and other industrial applications. By geography, the report covers North America, Europe, Asia-Pacific, South America, and the Middle East and Africa, with market size and forecasts provided for each region. For each segment, market sizing and forecasts have been done on the basis of value (USD million) and volume (Liters).

| Soybean |

| Palm |

| Rapeseed |

| Sunflower |

| Cottonseed |

| Others |

| Organic |

| Conventional |

| Biofuel |

| Paints and Coatings |

| Cosmetics and Personal Care |

| Pharmaceuticals |

| Animal Feed |

| Food and Beverages |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Rest of Middle East and Africa |

| By Product Type | Soybean | |

| Palm | ||

| Rapeseed | ||

| Sunflower | ||

| Cottonseed | ||

| Others | ||

| By Category | Organic | |

| Conventional | ||

| By End-Use | Biofuel | |

| Paints and Coatings | ||

| Cosmetics and Personal Care | ||

| Pharmaceuticals | ||

| Animal Feed | ||

| Food and Beverages | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is driving growth in industrial oils through 2031?

Growth is being led by biofuel blending policies, broader use of plant-based inputs in industrial applications, and tighter quality requirements in cosmetics and pharmaceuticals. The market is projected to reach USD 104.51 billion by 2031 at a 5.26% CAGR.

Which product type leads demand today?

Soybean oils held the largest share at 32.34% in 2025, supported by strong crush capacity and heavy use in biomass-based diesel and biodiesel.

Which product type is growing the fastest?

Rapeseed oils are projected to grow the fastest at a 6.72% CAGR through 2031, helped by renewable transport policy and stronger crop-based biodiesel economics in Europe.

Why is biofuels the most important end use?

Biofuels held 32.08% of demand in 2025 and also had the fastest growth at 6.59% CAGR, because blending rules create stable and policy-backed demand for vegetable oils.

Page last updated on: