Ovarian Cancer Drugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

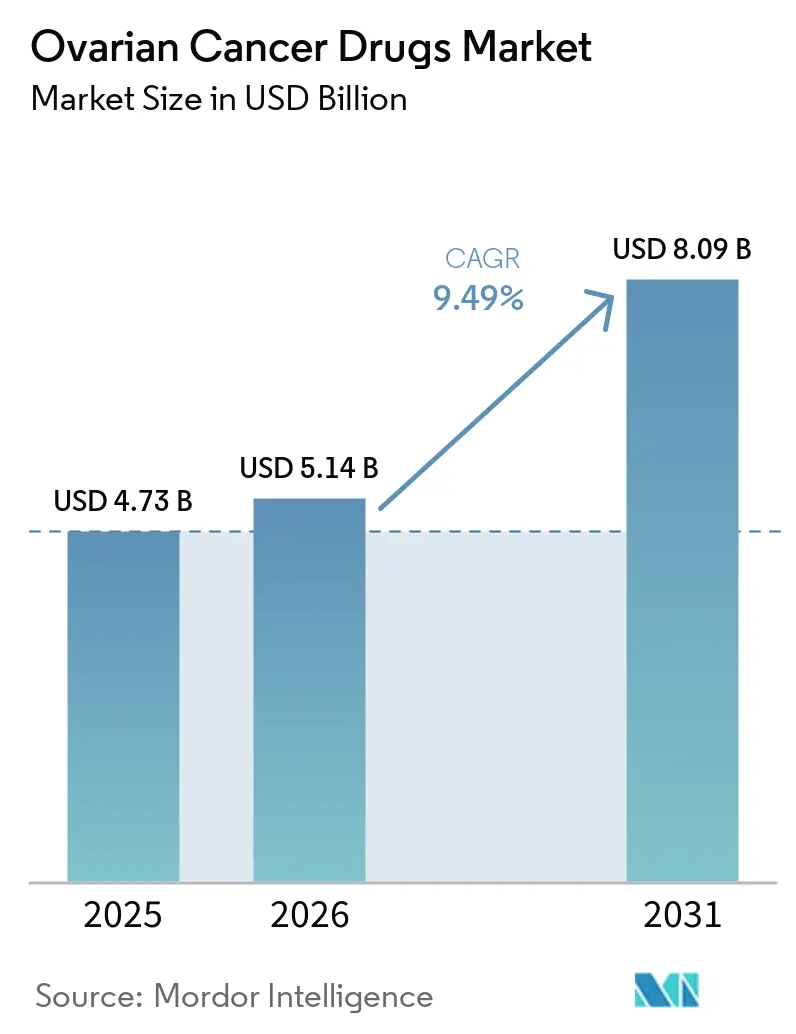

| Market Size (2026) | USD 5.14 Billion |

| Market Size (2031) | USD 8.09 Billion |

| Growth Rate (2026 - 2031) | 9.49% CAGR |

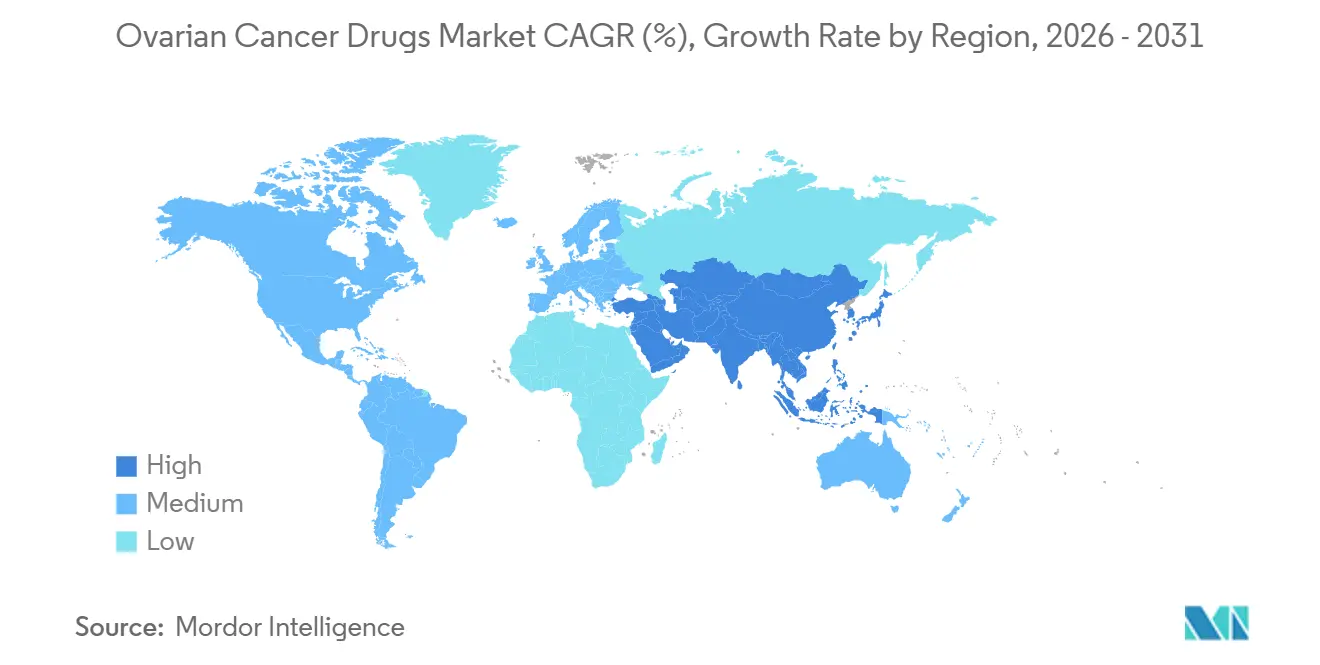

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ovarian Cancer Drugs Market Analysis by Mordor Intelligence

The Ovarian Cancer Drugs Market size is expected to grow from USD 4.73 billion in 2025 to USD 5.14 billion in 2026 and is forecast to reach USD 8.09 billion by 2031 at 9.49% CAGR over 2026-2031.

The ovarian cancer drugs market is being shaped by a faster regulatory cycle in biomarker-linked treatment settings, and that is widening treatment use in platinum-resistant disease and maintenance therapy. The ovarian cancer drugs market is also moving toward tighter alignment between drug approvals and companion diagnostics, which is changing prescribing pathways earlier in the patient journey. Competitive activity in the ovarian cancer drugs market remains concentrated around branded targeted therapies, while newer entrants are focusing on narrower molecular niches that can still support premium pricing. The ovarian cancer drugs market is also seeing stronger growth potential in outpatient and ambulatory care settings as oral maintenance drugs become more common and infusion workflows become more standardized. A parallel pressure is emerging from resistance, reimbursement scrutiny, and future generic exposure, which means commercial value is shifting toward next-generation agents, stronger sequencing strategies, and survival-backed evidence packages.

Key Report Takeaways

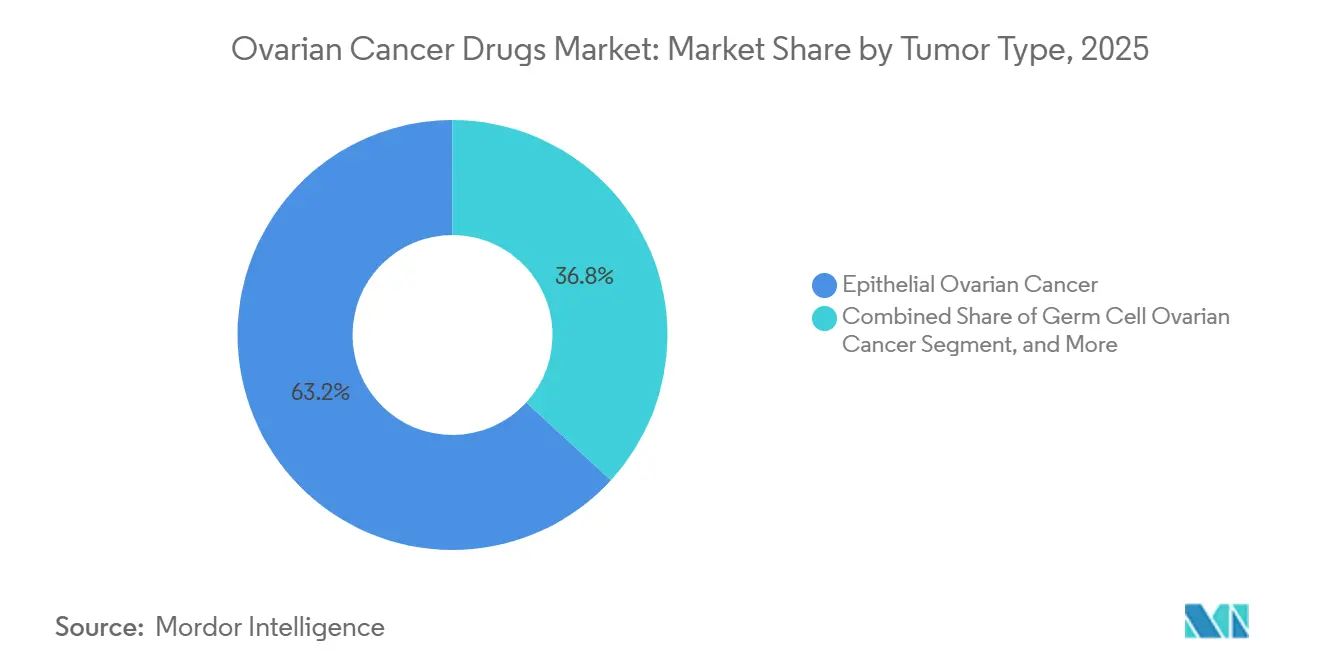

- By tumor type, epithelial ovarian cancer led with 63.21% of revenue in 2025, while germ cell ovarian cancer is forecast to expand at a 9.81% CAGR through 2031.

- By drug type, PARP inhibitors held 42.83% of revenue in 2025, while VEGF and VEGFR inhibitors are projected to grow at an 11.43% CAGR through 2031.

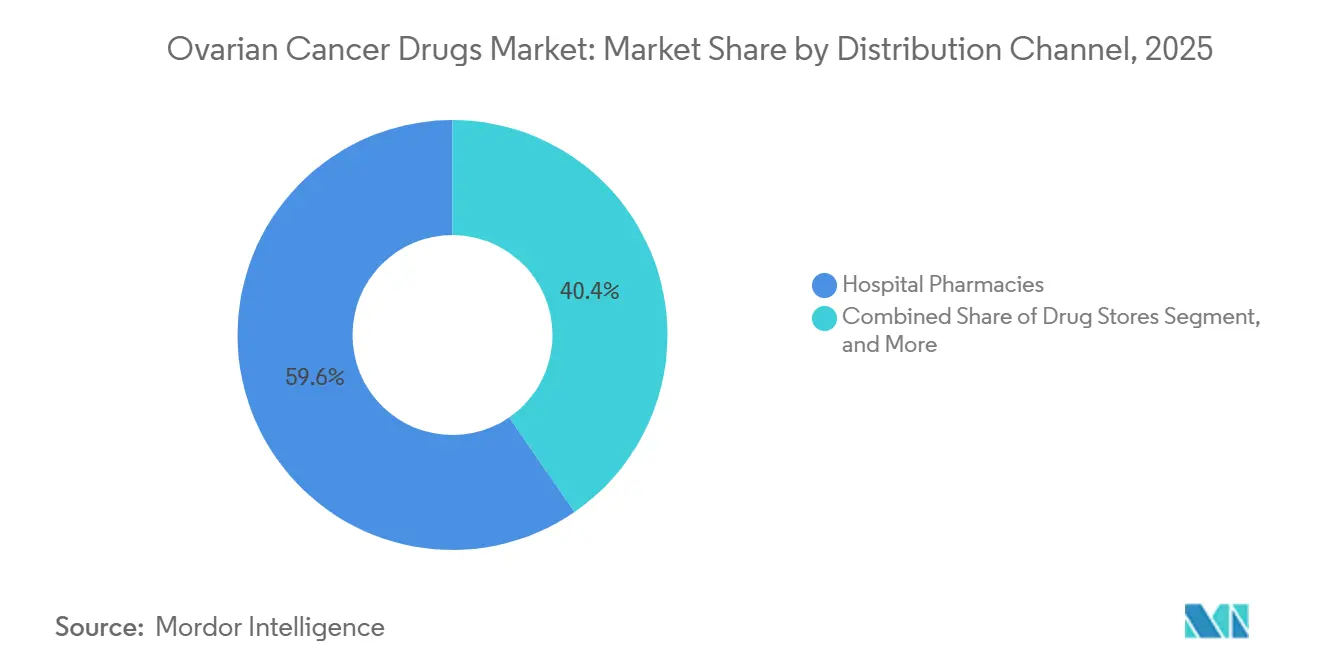

- By distribution channel, hospital pharmacies accounted for 59.64% of revenue in 2025, while drug stores are projected to advance at a 10.55% CAGR through 2031.

- By end user, hospitals held 54.23% of revenue in 2025, while oncology clinics are forecast to record the highest CAGR at 12.41% through 2031.

- By geography, North America held 39.41% of the ovarian cancer drugs market share in 2025, while Asia-Pacific is projected to expand at an 11.26% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Ovarian Cancer Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising BRCA and HRD-Guided PARP Inhibitor Use | +2.5% | Global, led by North America and Europe | Medium term (2-4 years) |

| Expansion of FRα-Targeted ADC Adoption in Platinum-Resistant Disease | +2.2% | North America and EU core, spill-over to APAC | Short term (≤ 2 years) |

| Earlier-Line Use of Maintenance Combination Regimens | +1.5% | Global, concentrated in HRD-positive patient populations | Medium term (2-4 years) |

| Broader Molecular Testing and Companion Diagnostics Access | +1.1% | North America and EU core, spill-over to APAC and MEA | Medium term (2-4 years) |

| Pipeline Readouts in KRAS-Mutant, CCNE1-Amplified, and Rare Subtypes | +0.8% | North America with EU and China gaining traction | Long term (≥ 4 years) |

| Real-World Evidence Support for Sequencing After First PARP Exposure | +0.6% | North America and EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising BRCA and HRD-Guided PARP Inhibitor Use

The ovarian cancer drugs market continues to benefit from broader HRD-linked treatment eligibility in frontline and maintenance settings. FDA clearance of MyChoice CDx for niraparib in March 2026 strengthened the diagnostic basis for selecting HRD-positive patients and raised the number of patients who can be identified for PARP therapy under formal testing workflows.[1]U.S. Food and Drug Administration, “List of Cleared or Approved Companion Diagnostic Devices In Vitro and Imaging Tools,” U.S. Food and Drug Administration, fda.gov Long-run survival evidence has also kept PARP inhibitors central to treatment planning for BRCA-mutated disease, especially where maintenance therapy is established in routine care. At the same time, resistance research is showing that patient selection alone will not determine future uptake because treatment sequencing and prior chemotherapy exposure can influence later PARP response.[2]Catherine J. Macdonald, Alice McWhirter, Aruna Vaidyanathan, et al., “Identification of Novel Drug-Specific PARP Inhibitor Resistance Mechanisms in Ovarian Cancer Implications for Clinical Practice,” British Journal of Cancer, nature.com That makes the ovarian cancer drugs market more dependent on how physicians combine biomarker data with line-of-therapy decisions. It also supports continued investment in diagnostic depth, sequencing strategy, and follow-up evidence for long-duration maintenance use.

Expansion of FRα-Targeted ADC Adoption in Platinum-Resistant Disease

The ovarian cancer drugs market is gaining a new growth layer from FRα-targeted antibody drug conjugates in platinum-resistant disease. Stronger survival evidence for mirvetuximab soravtansine has reinforced the role of FRα-directed treatment in a setting that previously had few differentiated options with durable benefit. This matters because platinum-resistant disease carries a high unmet need and often drives rapid adoption when a therapy shows both clinical activity and clearer patient selection. The ovarian cancer drugs market is also showing that reimbursement and health technology assessment now shape uptake as much as trial data, especially when premium-priced biologics move from approval to funded access. That raises the commercial importance of value demonstration after approval, particularly in systems where survival and quality-of-life evidence guide access. It also means developers with targeted assets need pricing flexibility, biomarker clarity, and region-specific access planning to scale volume.

Earlier-Line Use of Maintenance Combination Regimens

The ovarian cancer drugs market is seeing stronger use of combination maintenance regimens in earlier treatment lines. Frontline data for niraparib plus bevacizumab and prior evidence for olaparib plus bevacizumab support continued use of PARP and antiangiogenic combinations in biomarker-selected patients.[3]“Bevacizumab in Ovarian Cancer Therapy Current Advances, Clinical Challenges, and Emerging Strategies,” Frontiers in Bioengineering and Biotechnology, frontiersin.org These regimens are extending the role of bevacizumab-class therapy beyond a single treatment phase and making it a backbone across multiple care settings. That shift matters commercially because it keeps value inside the same treatment journey rather than relying on isolated line-by-line demand. It also broadens the ovarian cancer drugs market by supporting use in patients who may still derive benefit after earlier PARP exposure, provided combination strategies remain clinically workable. The result is a market where regimen architecture is becoming as important as the individual product profile.

Broader Molecular Testing and Companion Diagnostics Access

The ovarian cancer drugs market is moving toward a testing-first framework in which several biomarkers are assessed near diagnosis rather than after treatment failure. FDA approvals across companion diagnostics for ovarian cancer have added structure to this shift and are increasing the role of BRCA, HRD, FRα, and PD-L1 testing in routine decision making. This matters because the commercial reach of a drug now depends not only on label scope, but also on whether testing is available, reimbursed, and integrated into pathology workflows. The ovarian cancer drugs market is therefore becoming more tiered across health systems, since treatment eligibility can vary even where guidelines appear similar on paper. Broader multi-gene testing also encourages earlier channel alignment between diagnostics firms, hospitals, and specialty oncology providers. Over time, treatment uptake is likely to follow the strength of testing infrastructure as closely as it follows drug availability.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Emergence of PARP Resistance and Cross-Resistance | -3.2% | Global | Short term (≤ 2 years) |

| High Annual Therapy Cost and Reimbursement Pressure | -2.8% | EU, especially Netherlands, Germany, Canada | Medium term (2-4 years) |

| Biomarker Fragmentation Shrinking Eligible Patient Pools | -1.4% | Global, most acute in strict CDx-requirement markets | Medium term (2-4 years) |

| Hematologic and Ocular Toxicity Limiting Long-Term Use | -0.9% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Emergence of PARP Resistance and Cross-Resistance

The ovarian cancer drugs market faces a clear growth constraint from faster characterization of PARP resistance mechanisms. Recent research identified multiple resistance pathways, including homologous recombination repair restoration, replication fork stabilization, and drug efflux changes, which means resistance is now better defined and harder to ignore in treatment planning. Additional work has also shown that PARP inhibitor-resistant tumors may develop distinct biological vulnerabilities, which confirms that resistance is not a single event and cannot be managed with a uniform response. Commercially, this reduces the number of effective lines available for the same drug class and limits the duration of revenue that each patient can generate. The ovarian cancer drugs market is therefore being pushed toward next-generation assets and better-defined sequencing logic rather than repeat use of the same class after progression. That pressure also increases the value of companion biomarkers and real-world monitoring tools that can identify which patients still benefit from continued targeted treatment.

High Annual Therapy Cost and Reimbursement Pressure

The ovarian cancer drugs market is also constrained by rising payer scrutiny over premium-priced therapies. Reimbursement restrictions in Europe and cost-effectiveness reviews in Canada show that not all clinically relevant drugs will translate into broad funded access, especially outside the most biomarker-enriched patient groups. This is important because access pressure affects realized pricing, treatment duration, and the speed of geographic expansion even after regulatory approval. The ovarian cancer drugs market is therefore moving toward a model where evidence packages must support survival value, quality-of-life outcomes, and long-term affordability in parallel. Companies are likely to face wider use of outcomes-linked reimbursement and deeper post-launch evidence requirements in publicly funded systems. That will keep commercial opportunity strongest in patient groups where benefit is clear, measurable, and defensible under tighter review.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Tumor Type: Epithelial Histology Anchors Revenue While Rare Subtypes Draw Investment

Epithelial ovarian cancer held 63.21% of revenue in 2025 and remained the largest tumor type in the ovarian cancer drugs market. This concentration reflects the clinical weight of high-grade serous disease across induction, maintenance, and relapse treatment pathways. Epithelial tumors also carry the largest share of BRCA-mutated and HRD-positive patients, which keeps precision therapies most relevant in this segment. As a result, the ovarian cancer drugs industry continues to direct most commercial and clinical effort toward epithelial disease. This concentration also gives drug makers a clearer route to scale because testing, treatment algorithms, and evidence generation are all more mature in this setting.

Germ cell ovarian cancer is projected to grow at a 9.81% CAGR through 2031, making it the fastest-growing tumor type sub-segment in the ovarian cancer drugs market. Growth here is tied less to current volume and more to improved molecular characterization of rare subtypes that were historically treated with broader chemotherapy approaches. Targetable findings in dysgerminoma and related tumors are supporting incremental use of more precise treatments, even though chemotherapy still delivers strong responses in many patients. Stromal tumors are also drawing attention because their hormone-linked biology creates room for more specialized development paths. The ovarian cancer drugs industry is therefore widening beyond epithelial disease, but these rare subtypes remain smaller commercial opportunities that depend heavily on testing depth, referral patterns, and specialist center adoption.

By Drug Type: PARP Inhibitor Share Meets Antiangiogenic Acceleration

PARP inhibitors held 42.83% of revenue in 2025, which gave them the leading position in the ovarian cancer drugs market share by drug type. Their strength comes from established use in first-line maintenance, clear biomarker links, and long follow-up data that continue to support benefit in selected patients. Companion diagnostic progress has also reinforced this class by improving patient identification and keeping prescribing tied to formal testing pathways. That combination of label breadth and diagnostic support keeps PARP inhibitors central to the ovarian cancer drugs market even as resistance pressures rise. Older cytotoxic classes still matter clinically, but they offer less room for pricing power or product differentiation because most value has shifted toward targeted therapy.

VEGF and VEGFR inhibitors are projected to grow at an 11.43% CAGR through 2031, giving them the fastest expansion profile among drug classes in the ovarian cancer drugs market size mix. Their outlook is supported by broader use of bevacizumab combinations, rising access to lower-cost versions in price-sensitive regions, and pipeline activity around new antiangiogenic combinations. This class benefits from relevance across multiple treatment stages rather than a narrow single indication. Other drug types, including ADCs and immunotherapy-led regimens, are also adding momentum, but they remain more fragmented by mechanism and patient selection. Over the forecast period, the ovarian cancer drugs market is likely to reward drug classes that combine broader eligibility with manageable evidence, access, and toxicity burdens.

By Distribution Channel: Hospital Pharmacies Dominate, Specialty Retail Channels Accelerate

Hospital pharmacies accounted for 59.64% of revenue in 2025 and remained the largest dispensing route in the ovarian cancer drugs market. This lead reflects the fact that many leading treatments still require institutional administration, infusion support, dosing oversight, and adverse-event monitoring. Biologics and complex regimens continue to anchor procurement inside hospitals because contracts, cold-chain handling, and clinical supervision are easier to coordinate there. The ovarian cancer drugs market also continues to favor hospital-based dispensing, where new premium therapies first enter use under specialist oversight. This channel position is therefore not just about volume, but also about how new therapies are governed and financed in real practice.

Drug stores are projected to grow at a 10.55% CAGR through 2031, making them the fastest-growing distribution channel in the ovarian cancer drugs market. Oral maintenance therapy is the main driver because PARP inhibitors and other take-home agents fit more naturally into specialty pharmacy workflows than infusion-led hospital dispensing. That changes payer processing, refill behavior, and patient cost management because the route shifts from procedure-linked billing to pharmacy benefit administration. The channel transition also supports a wider role for specialty retail networks in adherence management and high-touch patient support. Over time, the ovarian cancer drugs market will likely see a more balanced split between hospital and pharmacy channels as oral targeted treatment expands in maintenance settings.

By End User: Hospitals Lead Volume, Oncology Clinics Gain Share Through Oral Maintenance

Hospitals held 54.23% of revenue in 2025 and remained the main end-user setting in the ovarian cancer drugs market. They continue to dominate because first-line treatment, surgery-linked care coordination, and complex relapse management are still centered in hospital systems. Academic centers also shape early adoption because they host clinical trials and often influence pathway changes before broader community uptake. This keeps hospitals central not only for current volume, but also for future product positioning and evidence development. In practical terms, the ovarian cancer drugs market still depends heavily on hospital-based specialists to start treatment and define subsequent patient flow.

Oncology clinics are forecast to grow at a 12.41% CAGR through 2031 and represent the fastest-growing end-user segment in the ovarian cancer drugs market size outlook. Their growth reflects the spread of oral maintenance treatment, pressure to reduce inpatient burden, and wider use of outpatient infusion protocols. Clinics are becoming more important in both mature and emerging markets because they offer lower-cost care settings without removing specialist oversight. This is especially relevant where targeted therapies can be prescribed and monitored without full hospital admission. The ovarian cancer drugs market is therefore shifting part of its commercial center of gravity toward ambulatory oncology, while research institutes and distributor-led models remain supportive channels in more specialized or regionally fragmented care systems.

Geography Analysis

North America held 39.41% of revenue in 2025 and remained the largest regional contributor to the ovarian cancer drugs market. The region benefits from dense clinical trial activity, wider use of BRCA and HRD testing, and a regulatory environment that often delivers earlier access to new therapies. The United States continues to act as the first major launch market for many ovarian therapies, which supports earlier revenue capture and stronger physician familiarity. This position also reinforces North America’s role in setting treatment pathways that later influence adoption elsewhere.

Europe remained the second-largest regional block in the ovarian cancer drugs market, but access conditions vary sharply across countries. Regulatory coordination helps align approvals, yet reimbursement timing and health technology review still create uneven treatment availability. That matters because a therapy may be approved across Europe but still reach patients at different speeds depending on local funding decisions. The ovarian cancer drugs market therefore expands more slowly in Europe than its clinical innovation would suggest, especially for high-cost therapies that need stronger value arguments.

Asia-Pacific is projected to expand at an 11.26% CAGR through 2031 and is the fastest-growing regional segment in the ovarian cancer drugs market size outlook. China is central to that growth because reimbursement support for multiple PARP inhibitors and broader molecular testing infrastructure are improving practical access. Domestic manufacturing and biosimilar competition are also likely to expand the use of antiangiogenic therapy while lowering realized pricing in some channels. Japan and South Korea add momentum through strong oncology centers, structured testing pathways, and high participation in specialist care. The ovarian cancer drugs market is also broadening gradually in the Middle East and Africa as governments invest in oncology capacity. South America remains more selective in access, with stronger bevacizumab uptake than PARP penetration because affordability and advanced biomarker testing still limit broader targeted therapy use.

Competitive Landscape

The ovarian cancer drugs market remains moderately concentrated, with AstraZeneca, GSK, AbbVie, and F. Hoffmann-La Roche holding visible positions across PARP inhibitors, ADCs, and antiangiogenic therapy. These companies benefit from established brands, broad clinical evidence, and stronger ties to specialist treatment centers. Even so, the ovarian cancer drugs market is becoming more crowded in platinum-resistant disease because new entrants are targeting narrower molecular populations with differentiated mechanisms. That is reducing the chance that one treatment class or one company can dominate every high-value segment.

Strategic moves in the ovarian cancer drugs market show how leaders are trying to protect current franchises while preparing for the next wave of competition. GSK advanced niraparib through combination development after the FIRST trial met its primary progression-free survival endpoint in first-line advanced ovarian cancer, which supports a broader role for its PARP platform. AstraZeneca has defended the olaparib franchise while also moving next-generation PARP1-selective development forward, which reduces dependence on a single aging asset base. Daiichi Sankyo and AstraZeneca also initiated the phase 3 DESTINY-Ovarian01 trial of ENHERTU plus bevacizumab in first-line maintenance, showing how major players are pushing into HER2-expressing and HRD-negative gaps.

The ovarian cancer drugs market also has clear white-space opportunities that continue to attract challengers. CCNE1-amplified disease, CDH6-expressing platinum-resistant tumors, and HRD-negative maintenance remain important openings because approved targeted options are still limited. That gives emerging developers room to compete without displacing the largest incumbents across the whole treatment pathway. At the same time, companion diagnostic requirements raise the cost and complexity of entry because drug development is increasingly tied to testing partnerships and biomarker validation. This means the ovarian cancer drugs market is likely to stay moderately concentrated at the top, while becoming more segmented and more competitive in smaller molecular niches.

Ovarian Cancer Drugs Industry Leaders

Amgen Inc.

AstraZeneca plc

Eli Lilly and Company

Novartis AG

Pfizer Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: The FDA approved pembrolizumab (KEYTRUDA) and KEYTRUDA QLEX plus paclitaxel, with or without bevacizumab, for PD-L1+ platinum-resistant epithelial ovarian cancer, becoming the first and only approved PD-1 inhibitors for this indication; KEYNOTE-B96 data showed a 28% reduction in risk of progression and 24% reduction in risk of death.

- December 2025: Daiichi Sankyo and AstraZeneca initiated the DESTINY-Ovarian01 phase 3 trial of ENHERTU (trastuzumab deruxtecan, T-DXd) plus bevacizumab as first-line maintenance therapy in HER2-expressing advanced ovarian cancer, following a safety run-in that confirmed tolerability, with intent to address the HRD-negative patient population that currently lacks an approved maintenance option.

- September 2025: The FDA granted Breakthrough Therapy Designation to R-DXd for CDH6-expressing platinum-resistant ovarian cancer in patients previously treated with bevacizumab, representing the second BTD under the USD 750 million Daiichi Sankyo–Merck collaboration and the first BTD for a CDH6-targeted ADC in any tumor type.

Global Ovarian Cancer Drugs Market Report Scope

The ovarian cancer drugs market encompasses the pharmaceuticals and biologic therapies used to diagnose, manage, and treat tumors originating in the ovaries.

The Ovarian Cancer Drugs Market is segmented by tumor type, drug type, distribution channel, end user, and geography. By tumor type, the market covers Epithelial Ovarian Cancer, which includes Serous Carcinoma, Endometrioid Carcinoma, Clear Cell Carcinoma, and Mucinous Carcinoma. It also encompasses Germ Cell Ovarian Cancer, such as Dysgerminoma, Yolk Sac Tumor, Teratoma, and Embryonal Carcinoma. In addition, Stromal Cell Ovarian Cancer includes Granulosa Cell Tumor, Sertoli-Leydig Cell Tumor, Thecoma, and Fibroma. By drug type, the market features Alkylating Agents, Mitotic Inhibitors, VEGF and VEGFR Inhibitors, PARP Inhibitors, and Other Drug Types. By distribution channel, drugs are supplied through Hospital Pharmacies, Drug Stores, and Other Distribution Channels. By end user, the market serves Hospitals, Oncology Clinics, Specialty Cancer Centers, and Research Institutes.

Geographically, the market spans North America (United States, Canada, Mexico), Europe (Germany, United Kingdom, France, Italy, Spain, Rest of Europe), Asia-Pacific (China, Japan, India, Australia, South Korea, Rest of Asia-Pacific), Middle East & Africa (GCC, South Africa, Rest of Middle East & Africa), and South America (Brazil, Argentina, Rest of South America).

| Epithelial Ovarian Cancer | Serous Carcinoma |

| Endometrioid Carcinoma | |

| Clear Cell Carcinoma | |

| Mucinous Carcinoma | |

| Germ Cell Ovarian Cancer | Dysgerminoma |

| Yolk Sac Tumor | |

| Teratoma | |

| Embryonal Carcinoma | |

| Stromal Cell Ovarian Cancer | Granulosa Cell Tumor |

| Sertoli-Leydig Cell Tumor | |

| Thecoma | |

| Fibroma |

| Alkylating Agents |

| Mitotic Inhibitors |

| VEGF and VEGFR Inhibitors |

| PARP Inhibitors |

| Other Drug Types |

| Hospital Pharmacies |

| Drug Stores |

| Other Distribution Channels |

| Hospitals |

| Oncology Clinics |

| Specialty Cancer Centers |

| Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Tumor Type | Epithelial Ovarian Cancer | Serous Carcinoma |

| Endometrioid Carcinoma | ||

| Clear Cell Carcinoma | ||

| Mucinous Carcinoma | ||

| Germ Cell Ovarian Cancer | Dysgerminoma | |

| Yolk Sac Tumor | ||

| Teratoma | ||

| Embryonal Carcinoma | ||

| Stromal Cell Ovarian Cancer | Granulosa Cell Tumor | |

| Sertoli-Leydig Cell Tumor | ||

| Thecoma | ||

| Fibroma | ||

| By Drug Type | Alkylating Agents | |

| Mitotic Inhibitors | ||

| VEGF and VEGFR Inhibitors | ||

| PARP Inhibitors | ||

| Other Drug Types | ||

| By Distribution Channel | Hospital Pharmacies | |

| Drug Stores | ||

| Other Distribution Channels | ||

| By End User | Hospitals | |

| Oncology Clinics | ||

| Specialty Cancer Centers | ||

| Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the expected value of the ovarian cancer drugs market by 2031?

The ovarian cancer drugs market is forecast to reach USD 8.09 billion by 2031, rising from USD 5.14 billion in 2026 at a 9.49% CAGR.

Which drug class leads ovarian cancer treatment revenue today?

PARP inhibitors led with 42.83% of revenue in 2025 because they are firmly established in maintenance therapy and supported by biomarker-led prescribing.

Which region is growing fastest for ovarian cancer therapies?

Asia-Pacific is projected to grow at an 11.26% CAGR through 2031, supported by wider reimbursement access and expanding molecular testing capacity.

Why are companion diagnostics becoming more important in ovarian cancer care?

Companion diagnostics are increasingly linked to drug access because BRCA, HRD, FRα, and PD-L1 testing now shape patient eligibility and prescribing pathways.

What is the biggest challenge for PARP inhibitor growth?

Resistance is a major challenge because cross-resistance and shorter effective treatment duration can limit repeat class use after progression.

Which care setting is gaining the fastest traction for treatment delivery?

Oncology clinics are forecast to grow fastest at a 12.41% CAGR through 2031 as oral maintenance therapy and outpatient care pathways expand.

Page last updated on: