Breast Cancer Therapeutics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

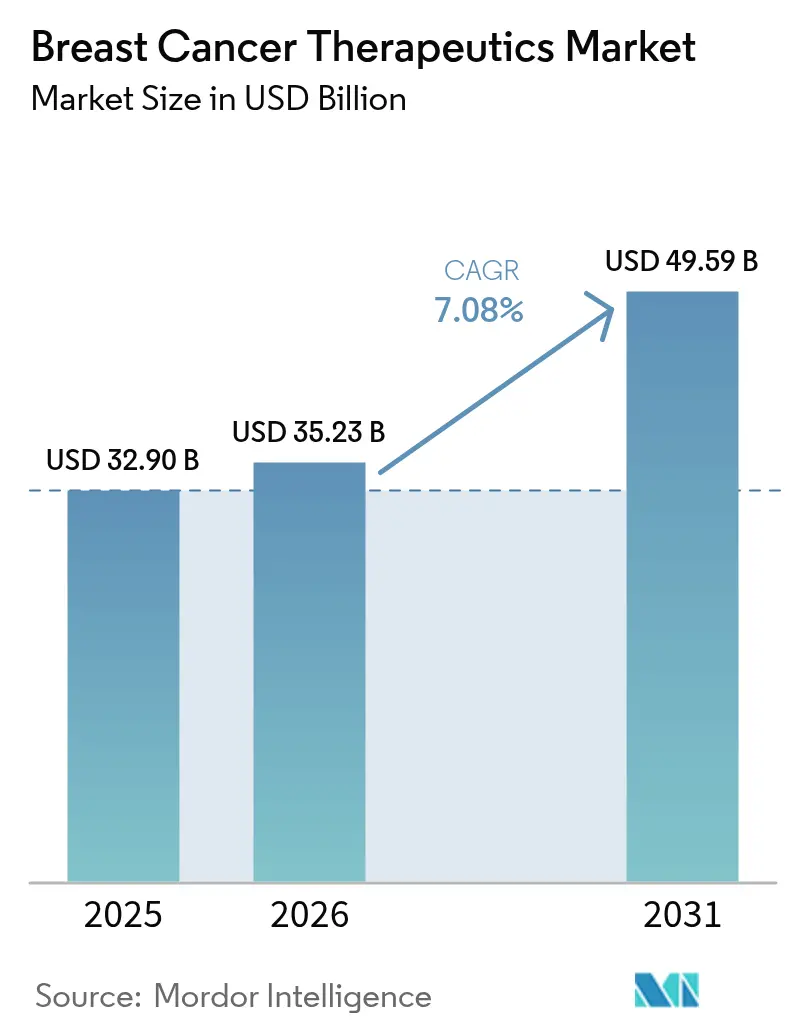

| Market Size (2026) | USD 35.23 Billion |

| Market Size (2031) | USD 49.59 Billion |

| Growth Rate (2026 - 2031) | 7.08% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

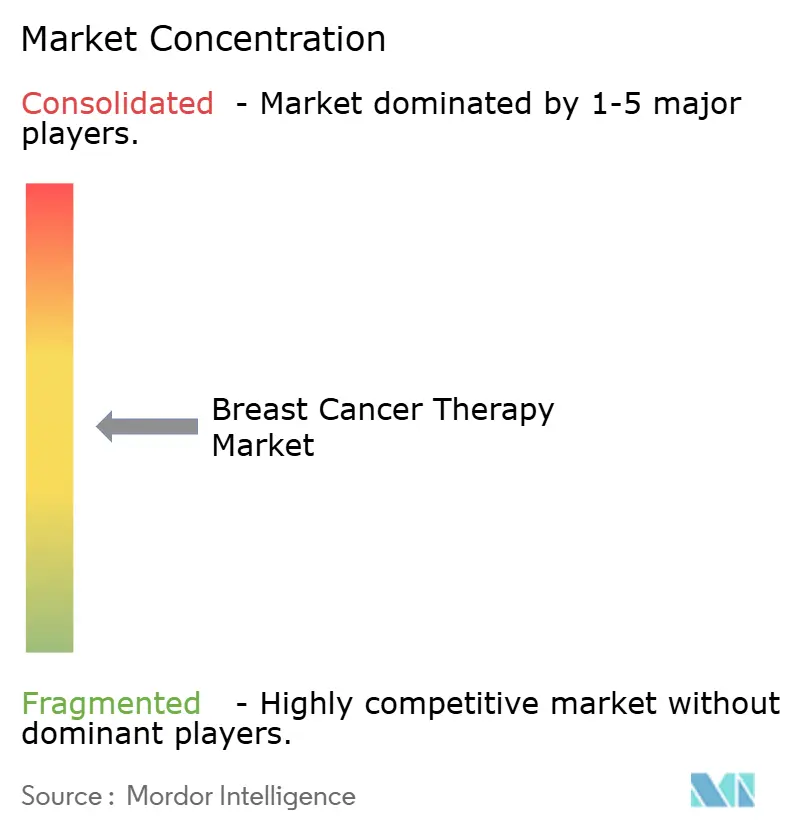

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Breast Cancer Therapeutics Market Analysis by Mordor Intelligence

Breast cancer therapeutics market size in 2026 is estimated at USD 35.23 billion, growing from 2025 value of USD 32.90 billion with 2031 projections showing USD 49.59 billion, growing at 7.08% CAGR over 2026-2031. Consistent incidence growth, accelerated regulatory approvals, and the rapid uptake of antibody–drug conjugates (ADCs) are underpinning sustained demand. The rising use of biomarker-guided treatment, earlier adoption of CDK4/6 inhibitors, and payer acceptance of premium-priced targeted agents are widening the revenue base. Immunotherapy combinations are broadening treatment algorithms, while subcutaneous formulations and e-commerce channels are reshaping care delivery. Despite capacity limits for high-potency payloads and complex multi-regional approvals, substantial R&D investment and AI-enabled discovery pipelines continue to reinforce the long-term outlook of the breast cancer therapeutics market.

Key Report Takeaways

- By therapy, targeted agents held 62.45% of the breast cancer therapeutics market share in 2025, whereas immunotherapy is projected to grow at a 13.95% CAGR through 2031.

- By molecular subtype, HR+/HER2- disease accounted for 64.78% revenue in 2025; triple-negative breast cancer is set to expand at a 12.08% CAGR to 2031.

- By disease stage, metastatic/advanced settings generated 54.15% of 2025 revenue, while early/adjuvant therapy is rising at a 10.44% CAGR.

- By route of administration, subcutaneous delivery is projected to advance at an 11.35% CAGR between 2026 and 2031.

- By geography, North America led with a 38.05% market share in 2025; the Asia-Pacific region is forecast to post a 11.85% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Breast Cancer Therapeutics Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Incidence & Prevalence Of Breast Cancer | +1.8% | Global, with highest impact in Asia-Pacific and Latin America | Long term (≥ 4 years) |

| Rising R&D Spending And Oncology Deal-Making | +1.5% | North America & EU, spill-over to APAC | Medium term (2-4 years) |

| Rapid Uptake Of HER2 / CDK4-6 Targeted Agents | +2.1% | Global, led by developed markets | Short term (≤ 2 years) |

| Growing Access To Screening In Emerging Economies | +1.2% | APAC core, spill-over to MEA and Latin America | Long term (≥ 4 years) |

| AI-Enabled Biomarker Discovery Fast-Tracking Pipelines | +0.9% | North America & EU, early adoption in select APAC markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Incidence & Prevalence of Breast Cancer

Breast cancer ranks as the most frequently diagnosed malignancy worldwide, driving enduring demand for therapeutics. Population ageing and lifestyle shifts are accelerating incidence, particularly in Asia-Pacific markets where urbanisation trends are evident. The MENA region expects a 50% rise in cancer cases by 2040, with breast cancer leading the increase. Earlier detection and improved survival elevate the prevalent patient pool, ensuring persistent growth for the breast cancer therapeutics market as healthcare systems move from reactive to proactive models.

Rising R&D Spending and Oncology Deal-Making

Record oncology investment is fuelling accelerated trials and premium valuations for differentiated mechanisms. Examples include Sanofi’s acquisition of Orano Med and Eli Lilly’s purchase of Radionetics, both aimed at securing next-generation radioligand capabilities. These deals shorten timelines for smaller biotechs and create a cycle where successful launches finance further pipeline expansion, boosting the breast cancer therapeutics market.

Rapid Uptake of HER2/CDK4-6 Targeted Agents

Trastuzumab deruxtecan’s success in HER2-low disease effectively doubles the addressable population [1]Ian Tannock, “Trastuzumab Deruxtecan after Endocrine Therapy in Metastatic Breast Cancer,” New England Journal of Medicine, nejm.org. Ribociclib’s adjuvant approval following the NATALEE study increases early-stage utilisation. Substantial survival gains justify premium prices, accelerating adoption across various care settings and driving growth in the breast cancer therapeutics market.

Growing Access to Screening in Emerging Economies

Government programmes in India and China are scaling mammography availability, shifting diagnosis toward earlier stages, and stimulating demand for adjuvant therapies. AI-driven tools such as CLAIRITY BREAST make risk prediction feasible in routine practice. Earlier detection lengthens treatment duration, strengthening revenue streams for the breast cancer therapeutics market.

Restraints Impact Analysis of Breast Cancer Therapeutics Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adverse Effects & Toxicity Management Costs | -1.4% | Global, with higher impact in cost-sensitive markets | Short term (≤ 2 years) |

| Stringent Multi-Regional Regulatory Timelines | -0.8% | Global, particularly affecting emerging market access | Medium term (2-4 years) |

| Scarcity Of High-Potency ADC Payload Manufacturing | -1.1% | Global, with supply constraints affecting all regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Adverse Effects & Toxicity Management Costs

Complex regimens, such as ADCs, require intensive monitoring and supportive care, which can sometimes double the total treatment expense. FDA’s Project Optimus underscores the need for dose optimisation. Limited supportive infrastructure in lower-income settings dampens uptake, constraining the breast cancer therapeutics market.

Stringent Multi-Regional Regulatory Timelines

Approval lags of 3-4 years persist between first-in-class authorisation and emerging-market access, as observed in Morocco. Distinct country standards increase cost and delay revenue recognition, capping the growth potential of the breast cancer therapeutics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Breast Cancer Therapeutics Market Segment Analysis

By Therapy:

Targeted Agents Cement LeadershipTargeted therapies generated 62.45% of 2025 revenue, underscoring their central role in the breast cancer therapeutics market. Trastuzumab deruxtecan’s expansion into HER2-low disease and inavolisib’s activity in PIK3CA-mutated tumours enlarge eligible cohorts. Immunotherapy, the fastest-growing segment with a 13.95% CAGR, is driven by checkpoint inhibitor-ADC combinations in triple-negative disease. Hormonal approaches remain relevant in HR-positive populations, whereas chemotherapy volumes decrease as tolerability improves with newer treatment modalities. Radiation therapy adoption persists in adjuvant settings, bolstered by advancements such as stereotactic body radiation techniques that minimize exposure and reduce the number of visits. Combination regimens blending modalities are reshaping practice patterns and encouraging the development of companion diagnostics.

Targeted agents are increasingly moving into earlier lines of care, and their superior risk–benefit profile supports continued reimbursement in price-sensitive systems. Developers are leveraging AI to refine patient selection, further improving efficacy signals. The breast cancer therapeutics market size for targeted modalities is projected to rise steadily, reflecting robust pipelines and sustained investment.

By Molecular Subtype:

TNBC AcceleratesHR+/HER2- disease accounted for 64.78% of 2025 spending in the breast cancer therapeutics market. Nonetheless, TNBC is expanding at a 12.08% CAGR, lifted by sacituzumab govitecan and follow-on TROP2 ADCs. HER2-positive disease retains momentum as trastuzumab deruxtecan extends to ultralow expression cohorts. The delineation of quadruple-negative subsets through molecular profiling signals further stratifies the disease.

Clinical data have shifted the perception of TNBC from an orphan subset to a high-value opportunity. Success breeds additional investment in antibody engineering, bispecific constructs, and novel payloads. As biomarker testing becomes routine, developers will tune trial designs, supporting persistent share gains for TNBC therapies within the breast cancer therapeutics market.

By Disease Stage:

Early Intervention SurgesMetastatic disease represented 54.15% of 2025 revenue. Early/adjuvant therapy, however, is climbing at a 10.44% CAGR as ribociclib and other agents prove efficacy before recurrence. Biomarker-guided neoadjuvant regimens push pathologic complete response rates higher, influencing regulatory endpoints.

The stage migration trend expands the breast cancer therapeutics market size at earlier points in the patient journey. Up-front therapy can avert later high-cost lines, shifting value from palliation to cure. Manufacturers that demonstrate long-term survival in adjuvant trials stand to capture significant, durable revenue streams.

By Route of Administration:

Convenience Gains GroundIntravenous products accounted for 49.05% of 2025 turnover. Subcutaneous delivery is projected to expand at an 11.35% CAGR as reformulations reduce chair time and facilitate home administration. Oral targeted therapies also progress, reflecting favourable pharmacokinetics and patient acceptance.

COVID-19 normalised remote care models, reinforcing demand for convenient routes. Payors view at-home options as cost-saving, while patients prefer fewer visits. The breast cancer therapeutics market will reward companies capable of transforming IV biologics into subcutaneous or oral formats without sacrificing efficacy.

By Distribution Channel:

Digital Access ExpandsHospital pharmacies retained 64.60% of sales in 2025. Yet e-commerce is growing 12.05% annually, catalysed by specialty platforms that couple dispensing with digital adherence support. Retail and specialty pharmacies bridge education gaps for oral regimens, while direct-to-patient delivery strengthens manufacturer–patient links.

The channel shift accelerates data capture, generating real-world evidence critical for value-based contracting. Participants in the breast cancer therapeutics market that integrate digital health services into distribution will gain competitive advantage.

Geography Analysis

North America Breast Cancer Therapeutics Market

North America contributed 38.05% of 2025 revenue to the breast cancer therapeutics market, reflecting rapid uptake of novel agents and broad insurance coverage. FDA initiatives such as Project Optimus influence global dosing standards. Biosimilar penetration, notably trastuzumab follow-ons, is curbing spend growth but widening access.

APAC Breast Cancer Therapeutics Market

Asia-Pacific is forecast to grow at 11.85% CAGR, making it the prime expansion engine for the breast cancer therapeutics market. Health-system investment, broader screening, and rising disposable incomes propel volumes in China and India. Japan demonstrates effective biosimilar incentives that drive adoption, while South Korea and Australia act as innovation test beds.

EMEA and South America Breast Cancer Therapeutics Market

Europe’s multi-payer environment tempers pricing but remains sizeable. Health technology assessment requirements elevate the importance of long-term outcomes data. Eastern European modernisation offers incremental upside. The Middle East and Africa lag in access, yet national cancer plans in Saudi Arabia signal improving availability. South America exhibits a mixed performance; Brazil leads the uptake, whereas smaller economies struggle with affordability issues.

Regulatory Landscape

Regulation in the breast cancer therapeutics market is increasingly influenced by accelerated oncology review pathways and the use of biomarker-defined labels across major agencies, including the US FDA, the European Medicines Agency (EMA), and Japan's PMDA. In 2026, label expansion activity focused on targeted agents and antibody-drug conjugates (ADCs). Multiple EMA CHMP positive opinions covered variations for products such as Enhertu, Trodelvy, and Datroway, reflecting broader use across HER2 expression levels and earlier lines of therapy.

The US FDA continues to set development norms through oncology approval notifications and dose-optimization expectations, including Project Optimus, although regional evidence requirements still create access lags between first approvals and emerging-market availability. Japan's 2025 approval of Enhertu for HR-positive, HER2-low or HER2-ultralow unresectable or recurrent breast cancer also highlights how localized regulatory decisions can expand treated populations, reinforcing the need for multi-region clinical evidence and companion diagnostic strategies.

Competitive Landscape

The breast cancer therapeutics market is moderately consolidated. Novartis leverages ribociclib’s adjuvant approval to defend its share in HR-positive disease. AstraZeneca and Daiichi Sankyo continue to expand the indications for trastuzumab deruxtecan, setting a high clinical bar.

ADC development dominates strategic roadmaps, prompting alliances such as Sanofi–Orano Med and Eli Lilly–Radionetics. AI-enabled platforms like CLAIRITY BREAST illustrate how diagnostic technology augments therapy portfolios. Biosimilar incumbents, including Samsung Bioepis and Celltrion, pursue price-volume plays that free payer budgets for next-generation drugs.

Manufacturing scalability for cytotoxic payloads is emerging as a competitive differentiator. Companies that invest in dedicated facilities mitigate supply risk and ensure launch readiness. Meanwhile, digital health partnerships help firms extend beyond the pill, improving adherence and generating actionable data for reimbursement negotiations.

Breast Cancer Therapeutics Industry Leaders

Novartis AG

Merck Co & Inc.

Fresenius Kabi

Pfizer Inc.

Eli Lilly & Co.

- *Disclaimer: Major Players sorted in no particular order

Breast Cancer Therapeutics Market Companies Covered in this Report

- Roche

- Novartis

- Pfizer

- AstraZeneca

- Eli Lilly and Company

- Bristol-Myers Squibb

- Merck

- Johnson & Johnson

- GlaxoSmithKline

- Eisai

- Teva Pharmaceutical Industries

- Fresenius

- Baxter

- Hikma Pharmaceuticals

- Celltrion Healthcare

- Viatris

- Abbvie

- Amgen

- Sanofi

- Bayer

Market Opportunities and Future Outlook

One opportunity area is expansion of high-value regimens into curative-intent settings, supported by 2026 regulatory and pipeline milestones. The FDA's approval of neoadjuvant trastuzumab deruxtecan (T-DXd) for HER2-positive stage II or III breast cancer brings an established ADC earlier in the pathway, where treatment duration and eligible volumes are typically higher, and it increases demand for HER2 testing and infusion capacity across hospital and specialty settings.

Another near-term opening is endocrine and targeted combinations that further segment HR-positive/HER2-negative disease beyond PIK3CA mutation status and emerging resistance markers. In 2026, the FDA accepted Roche's giredestrant NDA under Priority Review for adjuvant ER-positive/HER2-negative early breast cancer, and the FDA approved Celcuity's gedatolisib (REVTORPYK) combinations for HR-positive/HER2-negative locally advanced or metastatic breast cancer without a PIK3CA mutation, creating a treatment option for a large biomarker-defined cohort. Alongside Phase III evidence such as AstraZeneca's SERENA-6 readout for camizestrant plus a CDK4/6 inhibitor in ESR1-mutated advanced disease, these actions point to continued investment in mutation-guided sequencing, broader ESR1/PIK3CA testing, and payer approaches that differentiate value by line of therapy and molecular subgroup.

Recent Industry Developments in Breast Cancer Therapeutics Market

- July 2026: The US FDA approved Celcuity's REVTORPYK (gedatolisib) in combination with fulvestrant, with or without palbociclib, for adults with HR-positive, HER2-negative locally advanced or metastatic breast cancer without a PIK3CA mutation. The decision adds a new targeted option for a defined biomarker-negative subgroup and increases competitive intensity around combination endocrine backbones and CDK4/6 pairing strategies.

- June 2026: The US FDA approved Merck's KEYTRUDA (including KEYTRUDA QLEX) in combination with Gilead's Trodelvy for first-line treatment of unresectable locally advanced or metastatic PD-L1 positive (CPS 10 or greater) triple-negative breast cancer. This action reinforces immunotherapy plus ADC combinations as a frontline standard in an important TNBC subset and influences formulary positioning for premium regimens in metastatic care pathways.

- January 2025: The US FDA approved trastuzumab deruxtecan for HER2-low and HER2-ultralow breast cancer. Broadening the label to lower HER2 expression expands the treatable population and accelerates routine HER2 characterization beyond traditional positive or negative categorization.

Breast Cancer Therapeutics Market Report Scope and Research Methodology

Market Definition and Coverage

For this study, the breast cancer therapeutics market includes prescription drug therapies used to treat breast cancer across early stage and metastatic care, covering branded products and approved biosimilars, and reflecting revenue earned from therapy use in oncology practice.

Scope exclusions: We exclude surgery and radiation procedures or equipment, diagnostic tests and imaging, and over-the-counter symptom relievers.

Segments Covered in This Report

- By Therapy

- Radiation Therapy

- Hormonal Therapy

- Chemotherapy

- Targeted Therapy

- Immunotherapy

- By Molecular Subtype

- HR+ / HER2-

- HER2+

- Triple-Negative (TNBC)

- Quadruple-Negative (QNBC)

- By Disease Stage

- Early / Adjuvant

- Metastatic / Advanced

- By Route of Administration

- Intravenous

- Sub-cutaneous

- Oral

- By Distribution Channel

- Hospital Pharmacies

- Retail & Specialty Pharmacies

- E-commerce

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work was used to set the disease context and to keep assumptions tied to observable signals. We relied on public health and regulatory references such as the World Health Organization, the US Centers for Disease Control and Prevention, the National Cancer Institute, and regulator drug databases such as the FDA and EMA, along with peer-reviewed oncology journals.

To translate treatment adoption into revenue direction, we also reviewed company annual reports, earnings decks, and major press updates on label changes or safety notices. When public disclosures were too high level, we used a paid subscription covering company financials and a patent database to cross check timelines, portfolio focus, and likely pricing pressure points. These desk sources are illustrative only, and many other references were also used for data collection, clarification, and validation.

Primary Interviews and Surveys

Primary inputs came from interviews and structured surveys with oncologists, hospital pharmacy buyers, payer or reimbursement experts, and distribution channel participants across major treatment geographies. This helped us check adoption behavior, dosing practice, and switching logic against the desk assumptions.

For newer modalities, discussions focused on where use is expanding in real clinics, the constraints that limit uptake (such as toxicity management or infusion capacity), and how price and access differ by country. We then used these findings to adjust penetration, persistence, and pricing paths before finalizing the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 15% | APAC: 45% |

| Mid tier: 52% | Functional/Unit leaders: 28% | EMEA: 35% |

| Smaller Players: 18% | Managers: 57% | Americas: 20% |

Market-Sizing & Forecasting

Sizing starts from a top-down treated patient demand pool, where incidence and prevalence signals are translated into therapy-eligible cohorts by care setting and then mapped to likely treatment intensity. We corroborate this with selective bottom-up approximations, mainly through sampled therapy volumes by setting and sanity checks on price per regimen, which helps us adjust totals when utilization looks overstated.

Key inputs used in the model include breast cancer incidence and survival trends, share of patients treated in metastatic versus earlier lines, mix shifts between endocrine therapy, chemotherapy, targeted agents, and antibody drug conjugates, average duration of therapy and discontinuation patterns, and expected price movement from biosimilar entry and access restrictions. Where country level data was uneven, we used proxy countries with similar reimbursement structures and then scaled by population and oncology spend indicators.

For forecasting, we used scenario analysis supported by a lightweight regression-style check on how changes in treated population, therapy mix, and net pricing have historically moved total revenue. Expert feedback was used to set realistic launch ramps, access timing, and the speed of adoption for newer classes, so the forward path does not rely on a single aggressive assumption.

Data Validation & Update Cycle

Outputs are cross checked against independent signals such as epidemiology totals, therapy mix direction, and public pricing or reimbursement moves, then variances are investigated before sign off. When a country level result looks unusual, we recheck the underlying cohort sizing, treatment duration, and pricing logic, and follow up with additional expert touchpoints if the gap is not explainable.

The report is refreshed annually, and interim updates are added when material events occur, such as major approvals, safety warnings, or sudden pricing changes. Before delivery, we complete a final review pass so the numbers reflect the latest available data and the key assumptions remain aligned with current market behavior.

Mordor Intelligence's Breast Cancer Therapeutics Market Size Measured Against Other Published Estimates

Published market numbers for breast cancer therapeutics often do not match because the market boundary is set differently and the inputs are refreshed at different times. The biggest swings usually come from what is counted as a therapeutic product versus adjacent care, and from how net pricing and duration of use are treated.

Incidence and treated patient signals, along with checks on therapy class mix and biosimilar timing, are the evidence used to keep Mordor Intelligence's estimate aligned to prescription therapy revenues and away from broader oncology spending buckets. Differences also show up when a study assumes faster uptake for new modalities, applies list prices instead of net prices, or includes supportive and diagnostic revenues that are not part of drug treatment sales.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 35.23 B (2026) | |

| Industry Publisher A | USD 37.98 B (2026) | Uses a higher 2026 base and may apply broader therapy inclusions and higher pricing progression assumptions, which can lift totals even if treated cohorts are similar. |

| Research Group B | USD 36.50 B (2024) | Anchors to an earlier year and can blend therapy revenues with wider treatment categories, and currency timing and refresh cadence can further shift the reported USD value. |

Looking across the three figures, the spread is mainly explained by year selection, what is included as in-scope therapy revenue, and how pricing is normalized over time. By keeping the build tied to treated cohorts, therapy duration, and realistic net price movement, the final number stays traceable to clear inputs that can be rechecked when market conditions change.

Key Questions Answered in the Report

What is the current value of the breast cancer therapeutics market?

The market generated USD 35.23 billion in 2026 and is forecast to reach USD 49.59 billion by 2031.

Which therapy type holds the largest share?

Targeted agents dominate, accounting for 62.45% of 2025 revenue.

Why is Asia-Pacific the fastest-growing region?

Healthcare infrastructure investment, wider screening and rising incomes are driving a 11.85% CAGR through 2031 in Asia-Pacific.

What is driving growth in triple-negative breast cancer treatments?

Breakthrough TROP2-targeted ADCs such as sacituzumab govitecan are improving outcomes, supporting a 12.08% CAGR for TNBC therapies.

How are subcutaneous formulations influencing the market?

Patient preference for convenience and payer interest in reduced infusion costs are propelling subcutaneous products at an 11.35% CAGR.

Page last updated on: