Pancreatic Endocrine Tumor Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

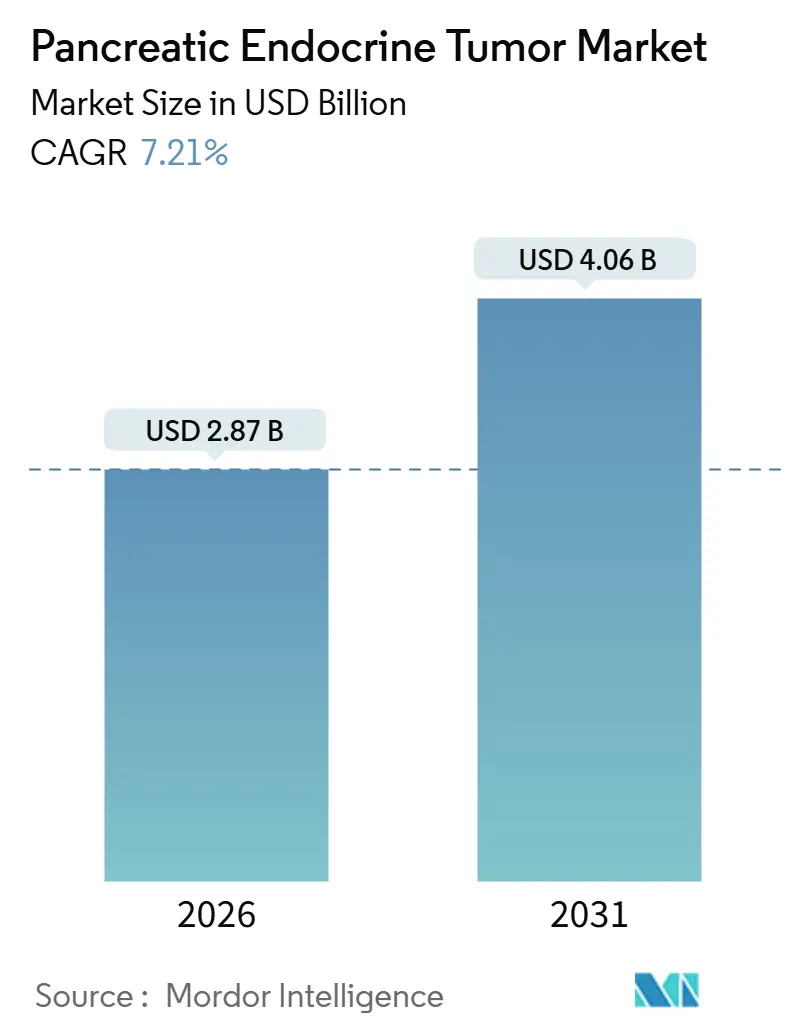

| Market Size (2026) | USD 2.87 Billion |

| Market Size (2031) | USD 4.06 Billion |

| Growth Rate (2026 - 2031) | 7.21% CAGR |

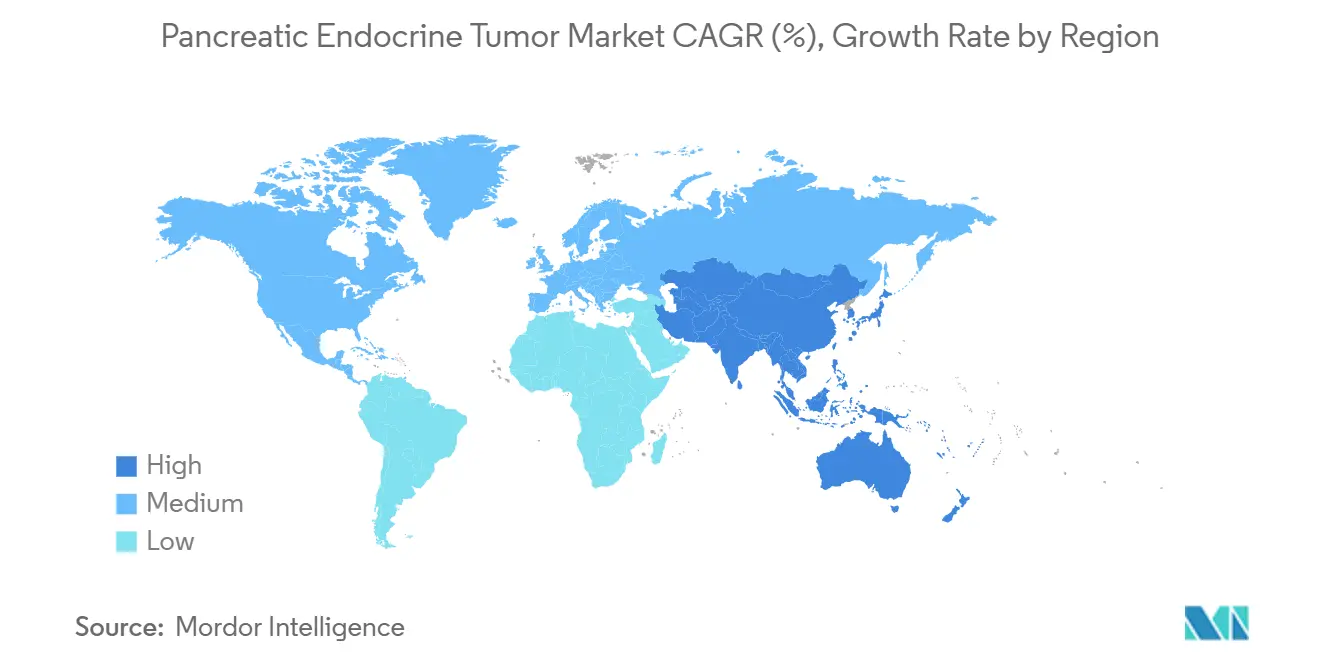

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pancreatic Endocrine Tumor Market Analysis by Mordor Intelligence

The Pancreatic Endocrine Tumor Market size is estimated at USD 2.87 billion in 2026, and is expected to reach USD 4.06 billion by 2031, at a CAGR of 7.21% during the forecast period (2026-2031).

Growth in the market is being driven by three interconnected factors: expedited regulatory approvals for new radionuclide therapies, advancements in precision oncology diagnostics that align patients with targeted treatments, and the proliferation of high-volume centers equipped to implement complex peptide receptor radionuclide therapy (PRRT) protocols. The FDA's approval of ITM-11's new drug application in November 2025 indicates impending competition for Novartis's Lutathera and suggests a shift in the reimbursement framework as a second Lu-177 agent enters U.S. clinics. Precision imaging with Ga-68 DOTATATE PET/CT is expanding from tertiary hospitals to regional networks, enabling earlier and more accurate patient selection for PRRT. Simultaneously, investments in scaled radioisotope production by ITM, Canadian Nuclear Laboratories, and European utilities are enhancing supply chain reliability, although capacity remains insufficient to meet demand. Additionally, increased payer scrutiny is compelling manufacturers to adopt outcomes-based contracts, linking therapy pricing to real-world progression-free survival outcomes.

Key Report Takeaways

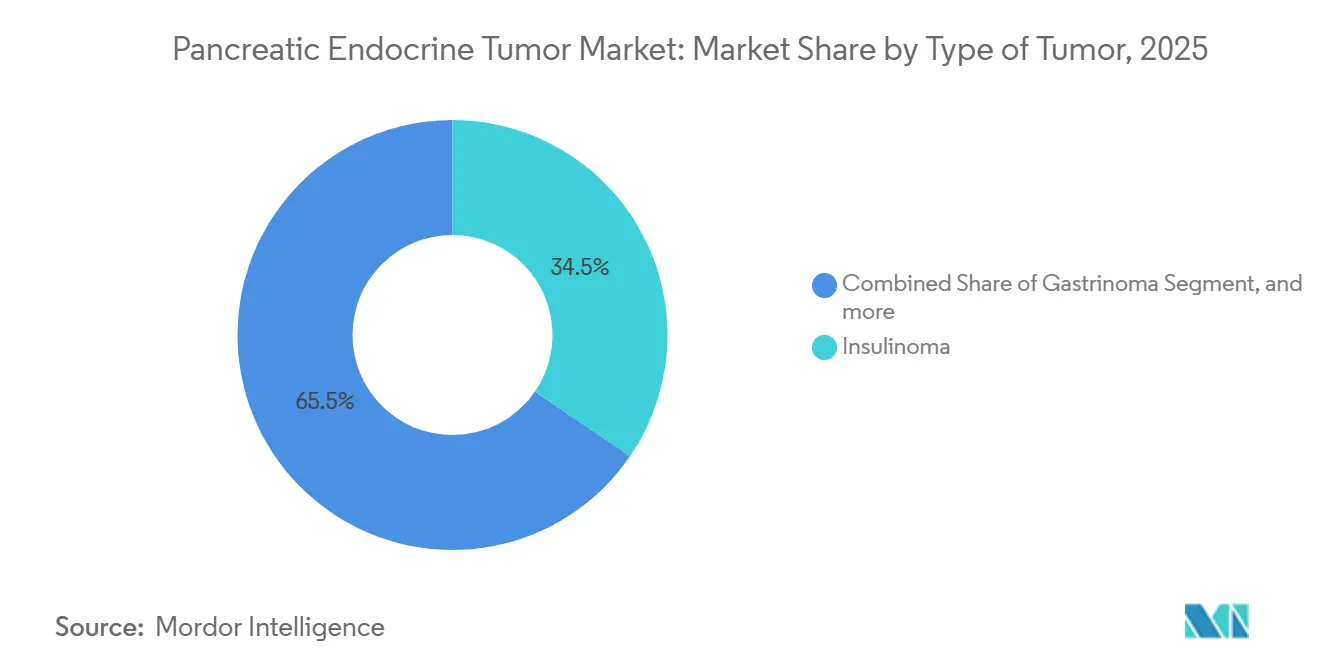

- By tumor type, insulinoma led with 34.54% revenue share in 2025. Gastrinoma is projected to expand at a 9.54% CAGR through 2031.

- By treatment type, surgery held 42.43% of the pancreatic endocrine tumor market share in 2025. Chemotherapy is advancing at a 9.87% CAGR to 2031.

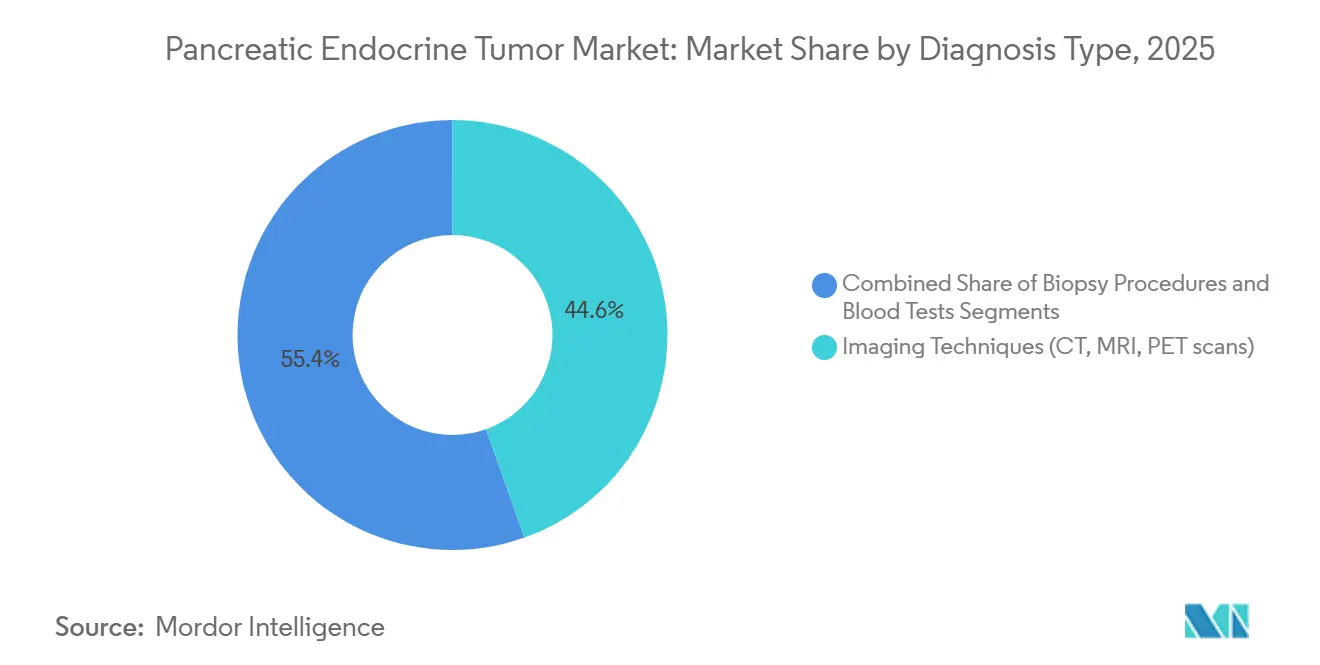

- By diagnosis type, imaging captured 44.56% of the pancreatic endocrine tumor market size in 2025. Blood tests are forecast to rise at a 10.11% CAGR to 2031.

- By end-user, hospitals accounted for 52.45% of 2025 volume, while specialized clinics are growing at a 10.32% CAGR.

- By geography, North America commanded 43.11% revenue in 2025, whereas Asia-Pacific is set to climb at an 8.54% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Pancreatic Endocrine Tumor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Incidence Of Pancreatic Neuroendocrine Neoplasms | +1.8% | Global, with higher detection rates in North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Growing Adoption Of Precision Oncology Approaches | +1.5% | North America & EU lead; APAC core markets (China, Japan, South Korea) accelerating | Medium term (2-4 years) |

| Increasing Availability Of Radionuclide Therapies | +2.1% | North America & EU established; APAC and MEA emerging | Short term (≤ 2 years) |

| Expansion Of Specialized Cancer Centers | +1.2% | North America, Western Europe, select APAC metros (Shanghai, Seoul, Tokyo) | Long term (≥ 4 years) |

| Favourable Regulatory Designations For Orphan Therapies | +0.9% | Global, with FDA and EMA as primary drivers | Short term (≤ 2 years) |

| Growing Investment In Rare Oncology R&D | +1.1% | Global, concentrated in North America and EU biotech hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Pancreatic Neuroendocrine Neoplasms

Annual detection now approaches 6 cases per 100,000 population as cross-sectional abdominal imaging becomes routine and endocrine societies promote hormone-panel screening for high-risk groups[1]Society of Nuclear Medicine and Molecular Imaging, “Global PET/CT Adoption Survey,” snmmi.org. Electronic health record alerts that flag unexplained hypoglycemia or gastrin elevation shorten referral times to imaging, which brings more patients into surgical or systemic-therapy windows when curative intent remains feasible. Greater diagnostic vigilance enlarges the treatable cohort and lengthens time on therapy, supporting steady revenue growth.

Growing Adoption of Precision Oncology Approaches

Routine Ki-67 indexing, somatostatin receptor quantification via Ga-68 DOTATATE PET/CT, and next-generation sequencing panels that identify DAXX, ATRX, and mTOR aberrations allow clinicians to match patients to PRRT, everolimus, sunitinib, or multi-kinase inhibitors with fewer trial-and-error cycles[2]Journal of Nuclear Medicine, “Personalized Dosimetry of 177Lu-DOTATATE,” jnm.snmjournals.org. Dosimetry software that tailors Lu-177 activity to individual tumor burden reduces nephrotoxicity and has improved progression-free survival in prospective studies, strengthening payer confidence in high-cost radionuclide regimens.

Increasing Availability of Radionuclide Therapies

Novartis’s Lutathera validated PRRT in gastroenteropancreatic neuroendocrine tumors, and ITM-11 is poised to follow with Phase III data showing a median progression-free survival of 23.9 months versus 14.1 months with everolimus. Bristol Myers Squibb is advancing RYZ101, a 225Ac-DOTATATE alpha emitter, for Lu-177-refractory disease, creating a sequential radionuclide pathway that can extend systemic control. Investment in no-carrier-added Lu-177 and nascent Ac-225 production aims to reduce backorder risk, though short half-lives still require just-in-time logistics.

Expansion of Specialized Cancer Centers

PRRT delivery involves radiopharmacy compounding, nephro-protective amino acid infusion, and multi-disciplinary tumor boards, prompting referral consolidation into high-volume centers that consistently achieve lower complication rates. Governments in China, Japan, and South Korea are subsidizing radiopharmacy build-outs inside academic hospitals, while U.S. payers reimburse travel to designated centers of excellence, reinforcing the geographic clustering of procedures.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Treatment Costs And Limited Reimbursement | -1.4% | Global, most acute in emerging markets and US commercial payers | Medium term (2-4 years) |

| Diagnostic Challenges Leading To Late Detection | -1.1% | Global, particularly acute in low-resource settings and rural areas | Long term (≥ 4 years) |

| Scarcity Of Radioisotope Supply Chain Infrastructure | -0.8% | Global, with bottlenecks in reactor capacity and distribution networks | Short term (≤ 2 years) |

| Variability In Clinical Management Guidelines | -0.6% | Global, fragmentation higher in regions without centralized NET societies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Treatment Costs and Limited Reimbursement

A full four-cycle PRRT course exceeds USD 200,000 in the United States, and step-therapy policies that mandate prior failure on everolimus or sunitinib postpone access[3]Centers for Medicare & Medicaid Services, “National Coverage Determination for PRRT,” cms.gov. Emerging markets lack the budget room for widespread PRRT coverage, forcing manufacturers to explore outcomes-based contracts or tiered pricing.

Diagnostic Challenges Leading to Late Detection

Small non-functional tumors evade routine CT scans, and lack of standardized high-risk screening means many patients present with metastatic disease that limits curative options. Access to Ga-68 DOTATATE PET/CT remains patchy outside academic centers, hindering early identification.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type of Tumor: Functional Syndromes Drive Gastrinoma Growth

Insulinoma generated the largest 34.54% share in 2025, reflecting urgent surgical demand to halt severe hypoglycemia, and it continues to anchor revenue in the pancreatic endocrine tumor market. Gastrinoma, however, enjoys the fastest 9.54% CAGR as better biochemical screening for Zollinger-Ellison syndrome and swift Ga-68 DOTATATE confirmation shortens time to targeted therapy initiation. Secondary subtypes such as VIPoma, glucagonoma, and somatostatinoma are less common but now benefit from guideline-directed hormonal workups that direct patients to high-volume centers early. The pancreatic endocrine tumor market for non-functional lesions is increasing in parallel as incidental imaging is uncovering previously missed silent tumors.

Molecular profiling is tilting therapeutic choice away from histologic classification toward receptor status and genomic context. DAXX, ATRX, and mTOR mutations guide enrollment in everolimus or cabozantinib, while high somatostatin receptor density flags suitability for PRRT. Ipsen’s move to extend Cabometyx into neuroendocrine tumors on the back of the CABINET study shows how multi-kinase inhibition can capture tumors with low SSTR expression. Over time, tumor-type segmentation may blur as clinicians prioritize molecular markers over hormone secretion patterns.

By Treatment Type: Chemotherapy Gains Momentum in Metastatic Disease

Surgical resection provided 42.43% of 2025 revenue, buoyed by minimally invasive approaches that trim length of stay and postoperative morbidity. Yet systemic chemotherapy is climbing at a 9.87% rate because metastatic incidence is rising and temozolomide-based doublets deliver higher objective response in grade 2–3 tumors. PRRT straddles both targeted therapy and radiation domains, blurring lines as it delivers beta or alpha particles only to SSTR-positive cells.

Combination sequencing dominates decision trees. Clinicians often move from long-acting somatostatin analogs to chemotherapy, then to Lu-177 PRRT, and reserve alpha emitters such as RYZ101 for Lu-177-refractory disease. The pancreatic endocrine tumor market share commanded by radiation therapy will expand once alpha platforms clear Phase III hurdles, as dose-limited kidneys benefit from the shorter path length of alpha particles.

By Diagnosis Type: Blood Tests Emerge as Liquid Biopsy Gains Traction

Imaging still leads with 44.56% share because Ga-68 DOTATATE PET/CT detects sub-centimeter SSTR-positive lesions and informs surgical mapping. Endoscopic ultrasound-guided biopsy remains essential for Ki-67 grading. However, blood tests are on pace for a 10.11% CAGR as chromogranin A, pancreatic polypeptide, and next-generation liquid biopsies move from research into routine surveillance programs.

Combining Ga-68 DOTATATE with FDG PET/CT distinguishes indolent from aggressive disease, guiding the selection of the first-line modality. High FDG uptake with weak SSTR expression suggests a chemotherapy-rich path, whereas the opposite profile points to PRRT. As serial circulating tumor DNA assays mature, they will shrink reliance on repeat imaging, lowering lifetime diagnostic cost and driving earlier therapeutic switches.

By End-User: Specialized Clinics Capture Complex Cases

Hospitals retain the majority, 52.45% volume, because surgery and acute hormone crisis management drive inpatient demand. Yet specialized oncology and endocrine clinics are clocking a 10.32% CAGR as outpatient PRRT suites open inside academic networks. Ambulatory surgical centers are performing laparoscopic enucleations, while telehealth follow-up extends care to rural areas without compromising protocol adherence.

Payers increasingly route complex cases to centers of excellence that maintain integrated radiopharmacy, nuclear medicine, endocrinology, and surgery teams under one roof. This model improves renal safety monitoring and days-to-next-cycle scheduling, supporting superior real-world outcomes that justify bundled-payment contracts.

Geography Analysis

North America accounted for 43.11% of revenue in 2025, driven by dense academic networks, early Ga-68 DOTATATE adoption, and Medicare reimbursement for PRRT. FDA acceptance of ITM-11’s NDA indicates an imminent product launch, which could temper prices but raise procedural costs. Canada reimburses Lutathera province-by-province, while Mexico’s private sector drives radionuclide volume yet still faces isotope shortages.

Europe operates under unified ENETS guidelines and benefits from robust isotope logistics via central reactors in Germany, the Netherlands, and Belgium. Germany and France have the highest treatment volumes, while Italy relies on cross-border referrals from Eastern Europe. European priority review accelerates orphan therapy launches, helping sustain the size of the pancreatic endocrine tumor market across the bloc.

Asia-Pacific posts the fastest 8.54% CAGR through 2031 as China’s National Medical Products Administration greenlights ITM-11 Phase III trials and provincial governments bankroll nuclear-medicine suites. Japan reimburses Lutathera under national health insurance and is expanding alpha-therapy clinical programs. India, Australia, and South Korea are growing from smaller bases, driven by private oncology chains and academic collaborations, but they still wrestle with supply chain lags and uneven payer coverage.

Competitive Landscape

Novartis reigns through Lutathera yet faces encroachment from ITM-11 and alpha programs from Bristol Myers Squibb. ITM’s EUR 188 million raise financed reactor expansion and Ac-225 joint ventures, pointing to vertical-integration defenses smaller firms cannot match. Bristol Myers Squibb is hedging with the ACTION-1 trial, which positions RYZ101 for second-line use when Lu-177 resistance emerges. AstraZeneca’s Fusion acquisition arms it with an alpha platform that can flex into SSTR2 indications once technical hurdles clear.

Barrier to entry centers on radioisotope supply, dosimetry IP, and nuclear-medicine training footprints. Companies that secure isotope pipelines, validate companion diagnostics, and demonstrate lower renal toxicity will win formulary preference as payers pivot to value-based purchasing.

Pancreatic Endocrine Tumor Industry Leaders

Novartis AG

Ipsen Pharma

Pfizer Inc.

Merck & Co., Inc.

Bristol Myers Squibb

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: The European Commission approved Cabometyx (cabozantinib) for adult patients with unresectable or metastatic, well-differentiated pancreatic (pNET) and extra-pancreatic (epNET) neuroendocrine tumors who progressed after prior systemic therapy.

- March 2025: The FDA approved CABOMETYX as a targeted therapy for a specific subset of pancreatic neuroendocrine tumor (PNET) patients, which originate from hormone-producing cells in the pancreas. PNETs are rare, distinct from common pancreatic cancer, and require specialized treatment.

Global Pancreatic Endocrine Tumor Market Report Scope

As per the scope of the report, a pancreatic endocrine tumor, also known as a pancreatic neuroendocrine tumor (PNET), is a rare neoplasm arising from the hormone-producing cells of the pancreas. It can be functional (hormone-secreting) or non-functional, affecting various bodily functions based on hormone production. These tumors are often slow-growing and may present symptoms related to hormone excess or mass effect.

The Pancreatic Endocrine Tumor Market is Segmented by Type of Tumor (Insulinoma, Gastrinoma, VIPoma, Glucagonoma, Somatostatinoma, and Mixed Endocrine Tumors), Treatment Type (Surgical, Chemotherapy, Targeted Therapy, Radiation, and Palliative), Diagnosis Type (Imaging, Biopsy, and Blood Tests), End-User (Hospitals, Specialized Clinics, Ambulatory Centers, and Other), and Geography (North America, Europe, Asia-Pacific, MEA, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Insulinoma |

| Gastrinoma |

| VIPoma |

| Glucagonoma |

| Somatostatinoma |

| Mixed endocrine tumors |

| Surgical Treatments |

| - Chemotherapy |

| - Targeted Therapy |

| - Radiation Therapy |

| - Palliative Care |

| Imaging Techniques (CT, MRI, PET scans) |

| Biopsy Procedures |

| Blood Tests |

| Hospitals |

| Specialized Oncology & Endocrine Clinics |

| Ambulatory Surgical Centres |

| Other end-Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest Of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest Of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest Of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest Of South America |

| By Type of Tumor | Insulinoma | |

| Gastrinoma | ||

| VIPoma | ||

| Glucagonoma | ||

| Somatostatinoma | ||

| Mixed endocrine tumors | ||

| By Treatment Type | Surgical Treatments | |

| - Chemotherapy | ||

| - Targeted Therapy | ||

| - Radiation Therapy | ||

| - Palliative Care | ||

| By Diagnosis Type | Imaging Techniques (CT, MRI, PET scans) | |

| Biopsy Procedures | ||

| Blood Tests | ||

| By End-User | Hospitals | |

| Specialized Oncology & Endocrine Clinics | ||

| Ambulatory Surgical Centres | ||

| Other end-Users | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest Of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest Of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest Of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest Of South America | ||

Key Questions Answered in the Report

How large is the pancreatic endocrine tumor market in 2026?

The pancreatic endocrine tumor market size stands at USD 2.87 billion in 2026 with a 7.21% CAGR toward 2031.

Which treatment option is growing the fastest?

Chemotherapy shows the highest treatment-type CAGR at 9.87% through 2031, driven by next-generation temozolomide-based protocols.

Why is Asia-Pacific the fastest-growing region?

Asia-Pacific benefits from government investment in nuclear-medicine infrastructure and rising detection rates, supporting an 8.54% regional CAGR.

What limits broader PRRT adoption?

High therapy cost, radioisotope supply constraints, and late diagnosis remain the main barriers despite favorable clinical outcomes.

Which companies are likely to disrupt the market next?

ITM Isotope Technologies Munich with ITM-11 and Bristol Myers Squibb with alpha-emitter RYZ101 are positioned to challenge Novartis’s incumbency.

Page last updated on: