Cancer Supportive Care Drugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

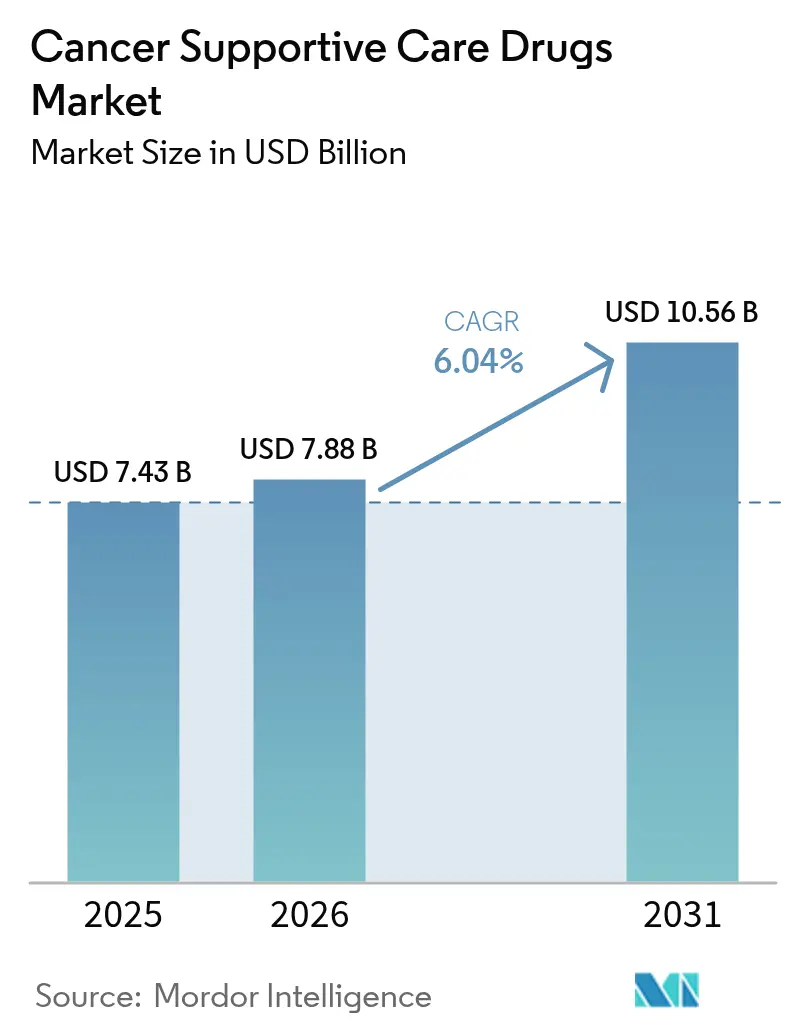

| Market Size (2026) | USD 7.88 Billion |

| Market Size (2031) | USD 10.56 Billion |

| Growth Rate (2026 - 2031) | 6.04% CAGR |

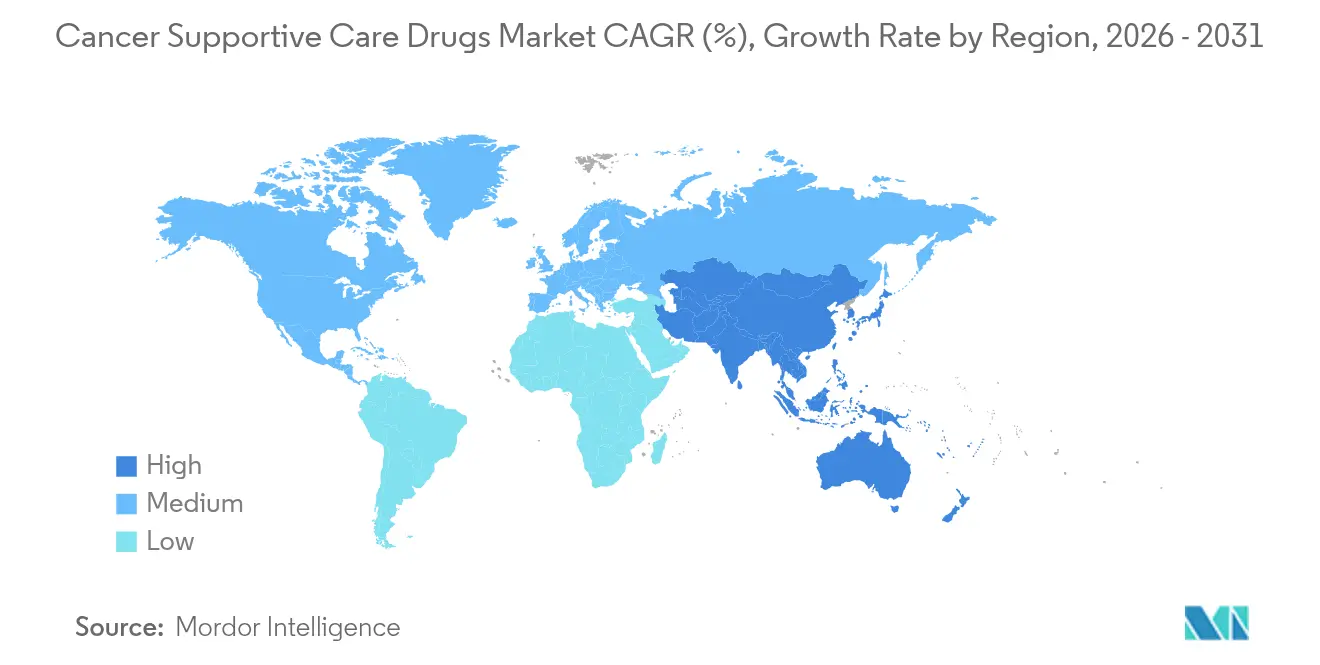

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cancer Supportive Care Drugs Market Analysis by Mordor Intelligence

The cancer supportive care drugs market size in 2026 is estimated at USD 7.88 billion, growing from 2025 value of USD 7.43 billion with 2031 projections showing USD 10.56 billion, growing at 6.04% CAGR over 2026-2031. This expansion reflects rising global cancer incidence, wider use of multi-agent chemotherapy, and regulatory tailwinds for lower-priced biosimilars. Growing acceptance of value-based reimbursement encourages earlier, protocol-driven use of supportive therapies, while patient demand for self-administered formulations fuels innovation in oral and subcutaneous products. Competitive pressure intensifies as biosimilar G-CSFs and bone-protective agents win rapid uptake, trimming acquisition costs without sacrificing efficacy. At the same time, payers and providers focus on reducing hospital readmissions, a goal closely tied to more consistent supportive care adherence. These converging factors sustain a healthy outlook for the cancer supportive care drugs market through 2030.

Key Report Takeaways

- By drug class, G-CSFs held 34.62% of the cancer supportive care drugs market share in 2025, while topical agents are projected to advance at an 8.28% CAGR to 2031.

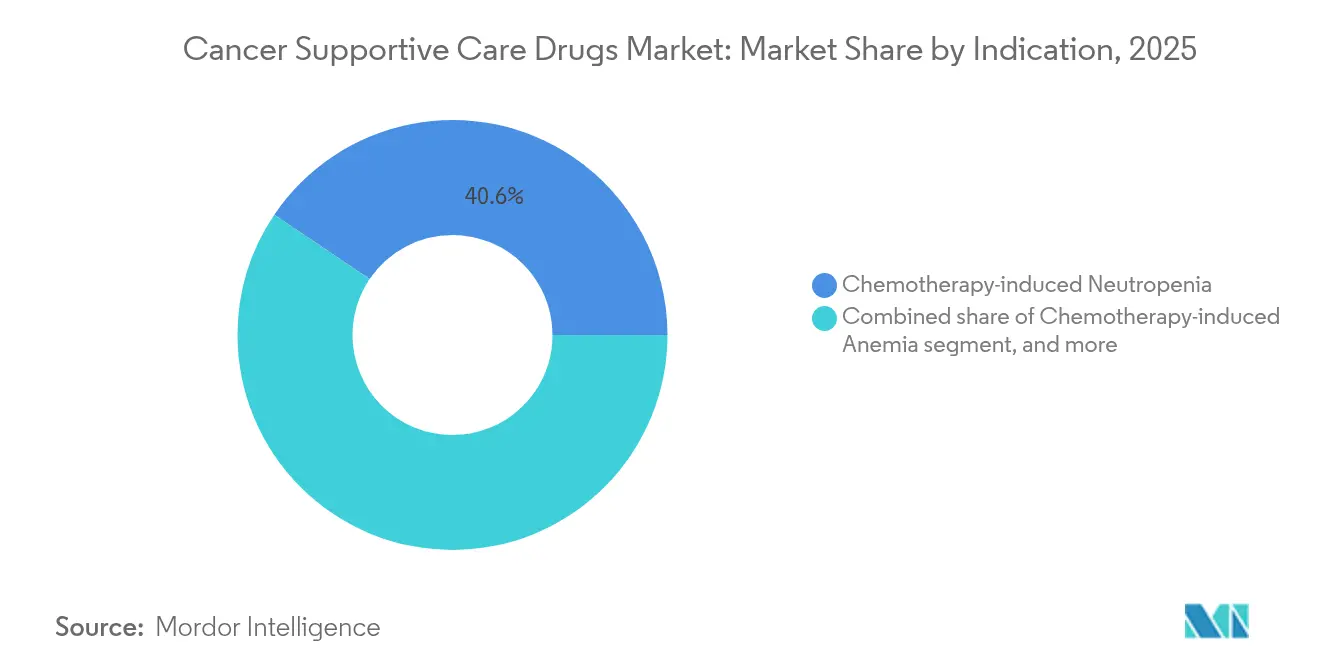

- By indication, chemotherapy-induced neutropenia accounted for 40.55% of demand in 2025; chemotherapy-induced anemia treatments are set to expand at an 8.52% CAGR through 2031.

- By distribution channel, hospital pharmacies commanded 51.76% of the cancer supportive care drugs market size in 2025, whereas online pharmacies are tracking a 9.12% CAGR between 2026-2031.

- By geography, North America led with 42.61% revenue share in 2025; Asia-Pacific is forecast to rise at a 7.31% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cancer Supportive Care Drugs Market Trends and Insights

Driver Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing burden of cancer worldwide | +1.8% | Global, highest in Asia-Pacific and aging Western populations | Long term (≥ 4 years) |

| Rising adoption of chemotherapy and combination regimens | +1.5% | North America and Europe with advanced oncology infrastructure | Medium term (2-4 years) |

| Introduction of cost-effective biosimilars | +1.2% | Europe and North America leading; expanding to Asia-Pacific | Short term (≤ 2 years) |

| Shift toward value-based oncology care models | +0.9% | North America primary, Europe secondary adoption | Medium term (2-4 years) |

| Expansion of oral and subcutaneous formulations enabling home care | +0.8% | Developed markets initially; global rollout | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Burden of Cancer Worldwide

New cases are rising sharply: IARC projects 28.4 million annual diagnoses by 2040, a 55% jump from 2020. Younger patients—those under 50—saw a 79% surge in cancer incidence between 1990 and 2019, leading to longer survival horizons and repeated treatment cycles. These demographic shifts lengthen exposure to myelosuppressive regimens, elevating demand for G-CSFs, antiemetics, and anemia therapies across the cancer supportive care drugs market. Economic pressure is equally significant; Europe alone spent EUR 199 billion on cancer in 2018, with EUR 32 billion earmarked for oncology medicines. Asia-Pacific growth is pronounced, exemplified by China’s projected USD 12.7 billion oncology spend by 2026, reinforcing a sizeable runway for supportive care uptake.

Rising Adoption of Chemotherapy and Combination Regimens

Combination protocols now dominate frontline therapy for solid tumors and hematologic malignancies, raising grade 3-4 hematologic toxicities by 40-60% versus monotherapy[1]Scientific American staff, “Combination regimens reshape toxicity patterns,” Scientific American, scientificamerican.com. The result is steady utilization of prophylactic G-CSFs, erythropoiesis-stimulating agents, and next-generation antiemetics. Emerging antibody-drug conjugates, such as trastuzumab deruxtecan, layer unique pulmonary and gastrointestinal toxicities onto conventional adverse-event profiles, widening the clinical remit of the cancer supportive care drugs market. As oncologists integrate targeted agents with backbone chemotherapy, supportive care protocols broaden to encompass both cytotoxic and immune-mediated side-effect prevention.

Shift Toward Value-Based Oncology Care Models

The CMS Enhancing Oncology Model saved USD 6 million while maintaining quality metrics during its initial rollout. Such frameworks reward practices that avert emergency visits via proactive toxicity management, elevating the strategic value of antiemetics, growth factors, and pain control agents. Venture funding tracks this trend: Thyme Care secured USD 95 million to build analytics-driven care navigation that embeds guideline-directed supportive therapies. As adoption spreads to commercial payers, drug manufacturers must demonstrate real-world outcome gains to protect formulary positioning in the cancer supportive care drugs market.

Expansion of Oral and Subcutaneous Formulations Enabling Home Care

Development pipelines emphasize at-home dosing, from oral antiemetics that mitigate delayed nausea to on-body injector G-CSF systems that free patients from next-day clinic visits. These innovations align with pandemic-accelerated preferences for remote care and reduce facility overheads. Early launches in North America and Europe showcase adherence improvements, and the convenience premium supports modest pricing flexibility. Over the long term, improved quality-of-life metrics underpin formulary inclusion, reinforcing sustainable volume growth for the cancer supportive care drugs market.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Emergence of targeted and immuno-oncology therapies with lower toxicity | −1.4% | Global; strongest in high-income regions | Medium term (2-4 years) |

| Safety concerns around opioid misuse and ESA-linked thrombotic events | −0.8% | North America primary concern; increasing global awareness | Short term (≤ 2 years) |

| Pricing pressures from reference-pricing and tender systems | −0.6% | Europe, parts of Latin America, and select Asia-Pacific procurement hubs | Medium term (2-4 years) |

| Growing use of digital symptom management reducing pharmacologic demand | −0.5% | Developed markets with high telehealth penetration | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Emergence of Targeted and Immuno-Oncology Therapies with Lower Toxicity

Immune checkpoint inhibitors and precision small-molecule inhibitors frequently spare bone marrow, leading to 60-70% lower neutropenia rates compared with traditional chemotherapy. Consequently, G-CSF volumes may moderate in regions where these modalities become first-line standards. Nonetheless, the supportive care mandate evolves rather than disappears: immune-related adverse events demand corticosteroids, endocrine replacement, and dermatologic agents that occupy adjacent therapeutic niches within the cancer supportive care drugs market. Manufacturers that pivot pipelines toward these emerging needs can offset erosion in legacy categories.

Safety Concerns Around Opioid Misuse and ESA-Linked Thrombotic Events

US oncology opioid prescriptions fell markedly, with the share of patients receiving no opioids rising. Regulatory scrutiny over misuse, combined with heightened prescriber liability, drives down median daily morphine equivalents, contributing to slower growth—or outright contraction—in the pain-management segment. Parallel caution surrounds erythropoiesis-stimulating agents after thrombotic signal detection, prompting risk-evaluation strategies that cap dosing and tighten patient selection. These pressures temper overall expansion of the cancer supportive care drugs market despite widening disease burden.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Biosimilar-Powered Growth in Core Categories

G-CSFs represented 34.62% of the cancer supportive care drugs market in 2025, underscoring their pivotal role in neutropenia prophylaxis. The segment’s resilience stems from predictable chemotherapy-induced marrow suppression across tumor types and strong endorsement in clinical guidelines. Rapid biosimilar uptake compresses unit prices but expands treatment penetration, keeping revenue on an upward trajectory. Topical agents, including steroid mouthwashes and barrier gels for mucositis, post an 8.28% CAGR to 2031 by addressing toxicities that gain visibility as survival lengthens. ESAs remain essential for anemia unresponsive to transfusion yet face moderate headwinds from safety labeling. Antiemetics sustain incremental gains, supported by fixed-dose combination launches targeting delayed emesis. Bisphosphonates and denosumab biosimilars grow steadily alongside rising skeletal-related-event risk in aging populations. Meanwhile, opioid demand softens, mirroring changing pain-control paradigms. Collectively, these trends illustrate how clinical-practice evolution and reimbursement shifts continually reshape the drug-class landscape within the cancer supportive care drugs market.

In revenue terms, the cancer supportive care drugs market size for G-CSFs is projected to expand briskly through the forecast horizon, even as price competition intensifies. Conversely, opioid revenues diminish due to lower average daily doses despite stable patient counts, validating payer emphasis on risk-mitigating alternatives. Continuous innovation in topical and subcutaneous formats helps manufacturers diversify beyond commoditized injectables, anchoring sustainable double-digit growth in newer subclasses.

By Indication: Heightened Focus on Quality-of-Life Endpoints

Chemotherapy-induced neutropenia retained 40.55% share of the cancer supportive care drugs market in 2025 thanks to its universal prevalence and compelling clinical consequences. Infectious complications drive longer hospital stays, reinforcing prophylactic intervention economics. Anemia therapies grow faster at 8.52% CAGR, propelled by mounting evidence that hemoglobin optimization enhances functional status and supports dose intensity. Nausea and vomiting management remains a foundational pillar, yet evolving emetogenic profiles prompt more nuanced antiemetic layering. Bone-loss protocols gain traction as metastatic survivorship extends beyond five years for many solid tumors, especially breast and prostate cancer. Pain management indicates gradual pivot toward multimodal regimens combining non-pharmacologic interventions with lower opioid exposure, a trend set to influence the cancer supportive care drugs market size for analgesics.

Supportive care for emerging toxicities tied to antibody-drug conjugates—such as interstitial lung disease—broadens the indication slate, hinting at pipeline opportunities. Over the forecast period, the cancer supportive care drugs market share for anemia therapies is set to climb, narrowing the gap with neutropenia interventions as payers relax ESA restrictions under stringent monitoring programs.

By Distribution Channel: Omnichannel Access Redefines Patient Experience

Hospital pharmacies controlled 51.76% of the cancer supportive care drugs market size in 2025, leveraging embedded clinician relationships and on-site infusion centers. Their dominance persists in acute-care settings where immediate adverse-event resolution is imperative. Retail chains cater to stable patients on maintenance antiemetics or oral pain agents, benefiting from convenience and loyalty programs. Online pharmacies, expanding at 9.12% CAGR, address growing preference for home delivery, particularly among immunocompromised individuals seeking to minimize hospital exposure. Telepharmacy consultation tools bolster adherence, while transparent pricing resonates with value-oriented consumers. Specialty pharmacies integrated within large health systems consolidate high-touch services, such as temperature-controlled logistics for biologics and insurance-navigation support. These models collectively enhance therapeutic continuity, reinforcing the omnichannel nature of the cancer supportive care drugs market.

Over time, the cancer supportive care drugs industry expects digital channels to capture incremental share as regulatory frameworks mature around e-prescribing of controlled substances. Yet hospital dispensaries remain critical for first-cycle chemotherapy support, illustrating the enduring coexistence of centralized and decentralized distribution paradigms.

Geography Analysis

North America accounted for 42.61% of global revenue in 2025, underpinned by advanced oncology infrastructure and widespread insurance coverage that reimburses high-cost biologics. Value-based pilots such as the Enhancing Oncology Model demonstrate measurable savings, encouraging replication across commercial payers and fortifying guideline-aligned supportive care uptake.

Europe stands as the second-largest regional market. Aggressive biosimilar procurement cut cancer-medicine prices by up to 97.8% in select countries, broadening access and curbing budget impact. National health systems devote substantial outlays—EUR 32 billion in 2018—for oncology drugs, evidencing strong political commitment to supportive therapy coverage. Reimbursement variability across member states prompts manufacturers to tailor pricing strategies, but widespread HTA frameworks ensure cost-effectiveness remains front-of-mind.

Asia-Pacific is the fastest-growing region with a 7.31% CAGR, energized by demographic aging, expanding middle classes, and broader insurance penetration. China’s oncology expenditure is on course to reach USD 12.7 billion by 2026, while India liberalizes foreign-direct-investment norms to spur domestic biologics manufacture. Government screening programs and rising diagnostic literacy heighten early detection rates, translating into larger treated cohorts and sustained demand in the cancer supportive care drugs market.

Latin America and the Middle East & Africa constitute smaller but steadily advancing markets. Procurement consortia in Brazil and Mexico negotiate volume-based discounts that align with biosimilar entry timelines. Meanwhile, Gulf Cooperation Council members invest in tertiary cancer centers, importing protocol-driven supportive care as part of broader medical-tourism aspirations. Collectively, these geographies add incremental volume that bolsters global growth momentum.

Competitive Landscape

Competition is moderate, with diversified multinationals relying on extensive portfolios and lifecycle management to defend share. Amgen reported 19% revenue growth in 2024, buoyed by oncology assets such as BLINCYTO and the recent launch of IMDELLTRA, a first-in-class DLL3-targeting bispecific. The company also agreed to grant Sandoz US entry for denosumab biosimilars no later than May 2025, illustrating a pragmatic approach to patent-expiry dynamics.

Roche and Johnson & Johnson leverage integrated pipelines that span cytotoxics, monoclonals, and supportive agents, enabling bundled contracting. J&J’s AKEEGA, combining a PARP inhibitor with standard hormonal therapy, cut prostate-cancer progression risk by 50%, indirectly extending the need for anemia and bone-health support. Pfizer advances novel cachexia therapy ponsegromab, with early trials showing 2-6 lb weight gain versus placebo loss[3]National Cancer Institute press office, “First-in-class cachexia therapy shows promise,” cancer.gov, addressing an unmet supportive niche.

Biosimilar specialists such as Viatris and Fresenius Kabi intensify price competition, while digital-health entrants like Thyme Care secure venture backing to integrate remote toxicity monitoring into payer workflows. Strategic alliances proliferate: Geisinger partnered with OncoHealth to embed real-time supportive-care guidance, and Amazon-owned PillPack expands oncology fulfillment capabilities. These moves underscore the ecosystem’s pivot toward service-drug hybrids that optimize outcomes and contain costs within the cancer supportive care drugs market.

Cancer Supportive Care Drugs Industry Leaders

Amgen Inc.

Novartis AG

Merck & Co. Inc

Johnson & Johnson

F. Hoffmann-La Roche AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Amgen’s Q1 revenue rose 9% to USD 8.1 billion; BLINCYTO sales jumped 52% to USD 370 million and IMDELLTRA reached USD 81 million after positive survival data in small cell lung cancer.

- May 2025: Sandoz finalized a deal with Amgen to launch denosumab biosimilars Jubbonti and Wyost in the United States by 31 May 2025 following FDA clearance.

- April 2025: Oncology News Central highlighted declining opioid use in cancer care, with median daily morphine-equivalent doses falling from 37.5 mg to 7.5 mg between 2016-2021.

- February 2025: Amgen’s FY 2024 results showed a 19% revenue rise, featuring LUMAKRAS approval for KRAS G12C-mutated colorectal cancer and Nplate progression for chemotherapy-induced thrombocytopenia.

- January 2025: Oncology Nursing Forum published evidence that multimodal interprofessional pain management significantly reduces moderate-to-severe cancer pain and improves quality of life.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the cancer supportive care drugs market as the worldwide sales of prescription pharmacologic agents that prevent or lessen therapy-related adverse events in oncology patients, ranging from granulocyte colony-stimulating factors and antiemetics to analgesics and bone-modifying agents. These drugs neither shrink tumors nor prolong survival directly; rather, they uphold treatment adherence and quality of life.

Scope exclusions include nutritional supplements, counseling services, durable medical equipment, and radioprotective devices, which are outside the study.

Segmentation Overview

- By Drug Class

- G-CSFs

- ESAs

- Antiemetics

- Bisphosphonates

- Opioids

- NSAIDs

- Topical Agents

- Other Drug Classes

- By Indication

- Chemotherapy-induced Neutropenia

- Chemotherapy-induced Anemia

- Nausea & Vomiting

- Cancer-related Bone Loss

- Cancer Pain

- Oral & Dermal Mucositis

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interview oncologists, oncology pharmacists, group purchasing heads, and payor medical directors across North America, Europe, Asia-Pacific, and key emerging markets. These conversations test incidence-to-treatment ratios, biosimilar uptake curves, and discounting practices, allowing us to reconcile desk findings with on-ground behavior.

Desk Research

Our analysts first compile publicly available macro and micro data. Core inputs come from tier-one bodies such as IARC cancer registries, WHO Global Health Observatory, U.S. FDA and EMA drug approval databases, OECD health statistics, and country-level customs records that flag import volumes of pegfilgrastim, palonosetron, and similar agents. Corporate 10-Ks, investor decks, and hospital formulary price lists supply real-world ASP signals. Subscription resources like D&B Hoovers and Dow Jones Factiva provide company revenue splits. This list is illustrative, not exhaustive.

Market-Sizing & Forecasting

Using a top-down structure, we rebuild demand from national chemotherapy patient pools, multiplying treated-case counts by supportive-care penetration rates and average standardized daily doses, which are then valued using region-specific ASPs. Select bottom-up checks, such as supplier roll-ups and sampled hospital purchase audits, anchor the totals. Variables such as cancer incidence growth, regimen intensity shifts, biosimilar price erosion, opioid prescription restrictions, and evolving payer guidelines feed the multivariate regression that projects figures through 2030. Gap cells in bottom-up data are bridged with averaged proxy prices vetted by primary experts.

Data Validation & Update Cycle

Outputs move through multi-analyst variance checks; anomaly flags trigger re-contacts, and senior review precedes sign-off. Our models refresh every twelve months, with mid-cycle amendments if regulatory, reimbursement, or supply shocks occur.

Why Mordor's Cancer Supportive Care Drugs Baseline Earns Trust

Published estimates often differ because firms pick unlike scopes, base years, and price assumptions.

Key gap drivers here include inclusion of adjunct services, omission of biosimilar erosion, or reliance on manufacturer list prices instead of net spend.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 7.43 B (2025) | Mordor Intelligence | - |

| USD 21.89 B (2024) | Regional Consultancy A | bundles home infusion services and nutritional products |

| USD 21.54 B (2025) | Global Consultancy B | uses manufacturer ex-factory prices, no biosimilar discount |

| USD 13.64 B (2022) | Trade Journal C | applies uniform global ASP, ignores opioid access limits |

These comparisons show that when scope is tightened to prescription drugs and realistic net prices, Mordor's figure provides a balanced, transparent baseline that decision-makers can replicate and trust.

Key Questions Answered in the Report

What is the expected size of the cancer supportive care drugs market by 2031?

The market is projected to reach USD 10.56 billion by 2031, growing at a 6.04% CAGR.

Which drug class currently leads the cancer supportive care drugs market?

G-CSFs lead with 34.62% share, driven by their critical role in neutropenia prophylaxis.

Why are biosimilars important in supportive oncology?

Biosimilars already account for 81% of prescriptions in key categories and cut prices by up to 67%, expanding patient access and reducing healthcare costs.

Which region is growing fastest in the cancer supportive care drugs market?

Asia-Pacific is advancing at a 7.31% CAGR, propelled by aging populations and widening insurance coverage.

How are value-based care models influencing supportive drug use?

Programs like the CMS Enhancing Oncology Model reward practices that deploy supportive therapies to prevent costly complications, driving more consistent use of growth factors and antiemetics.

What safety concerns are limiting opioid growth in cancer care?

Rising scrutiny of misuse has lowered median morphine-equivalent doses and increased reliance on multimodal pain strategies, constraining opioid revenue growth in supportive care.

Page last updated on: