Endometrial Cancer Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

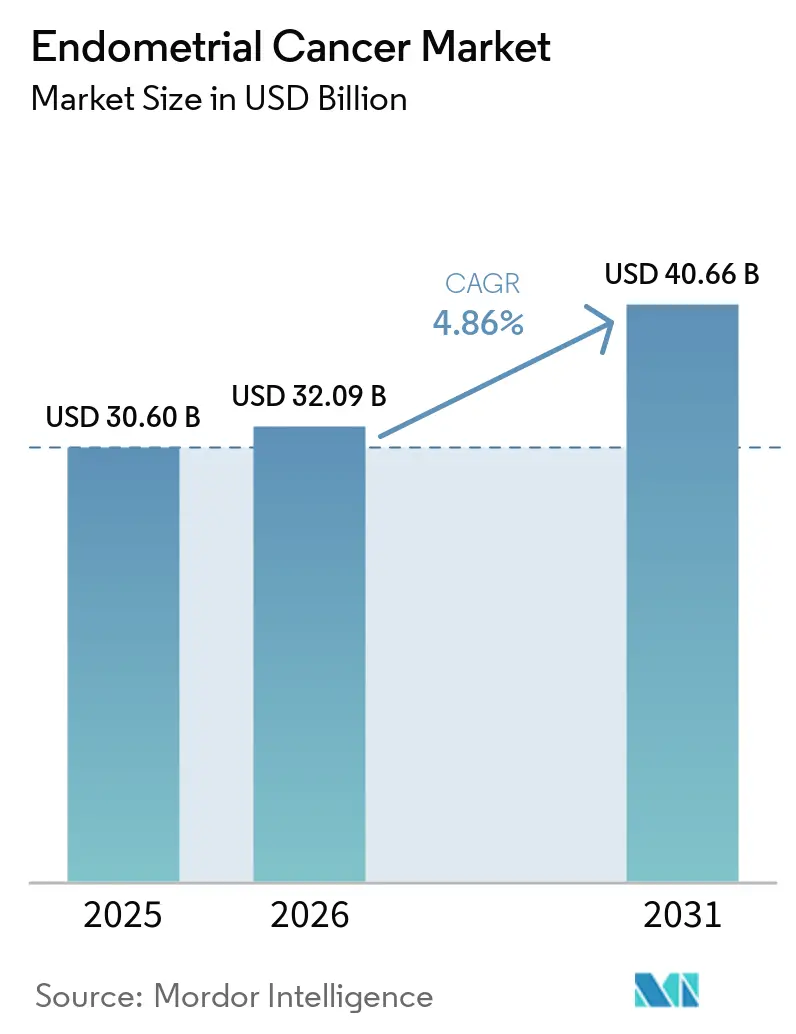

| Market Size (2026) | USD 32.09 Billion |

| Market Size (2031) | USD 40.66 Billion |

| Growth Rate (2026 - 2031) | 4.86% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Endometrial Cancer Market Analysis by Mordor Intelligence

The endometrial cancer market size is expected to grow from USD 30.60 billion in 2025 to USD 32.09 billion in 2026 and is forecast to reach USD 40.66 billion by 2031 at 4.86% CAGR over 2026-2031. Growth is propelled by the rapid uptake of immunotherapy-chemotherapy combinations that markedly improve overall survival, wider molecular testing that guides targeted prescribing, and supportive reimbursement policies in high-income countries. Diagnostic innovation—including artificial-intelligence image analysis and proteomic biomarker panels—broadens early detection while minimally invasive procedures make screening more acceptable to patients. Meanwhile, supply chain investments in domestic radioisotope production ease bottlenecks for imaging and brachytherapy, ensuring treatment capacity keeps pace with rising incidence. Competitive dynamics are dominated by three checkpoint inhibitors, and their combination trial programs sustain a high rate of new label expansions that reinforce brand loyalty across oncology networks.

Key Report Takeaways

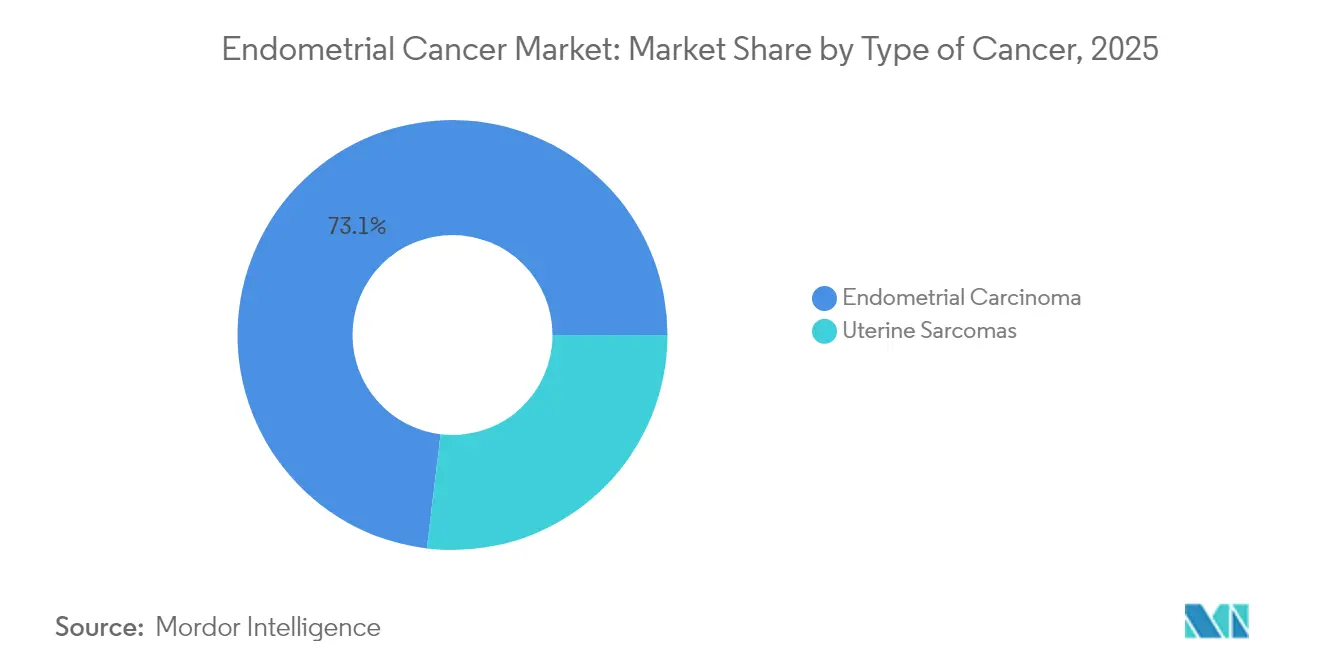

- By type of cancer, endometrial carcinoma led with 73.10% revenue share of the endometrial cancer market size in 2025, while uterine sarcomas are projected to expand at a 7.84% CAGR through 2031.

- By type of therapy, chemotherapy maintained 44.78% share of the endometrial cancer market size in 2025; immunotherapy is advancing at a 8.78% CAGR through 2031.

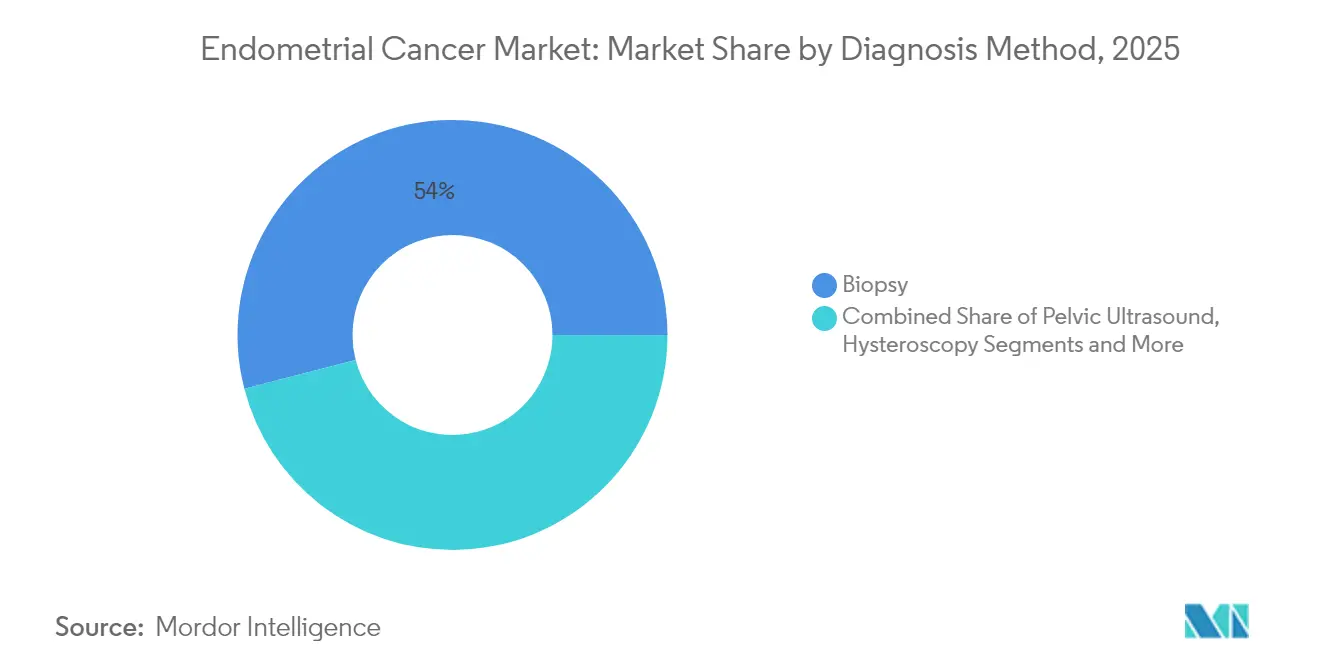

- By diagnosis method, biopsy captured 54.02% of endometrial cancer market share in 2025 and hysteroscopy is set to grow at a 7.76% CAGR to 2031.

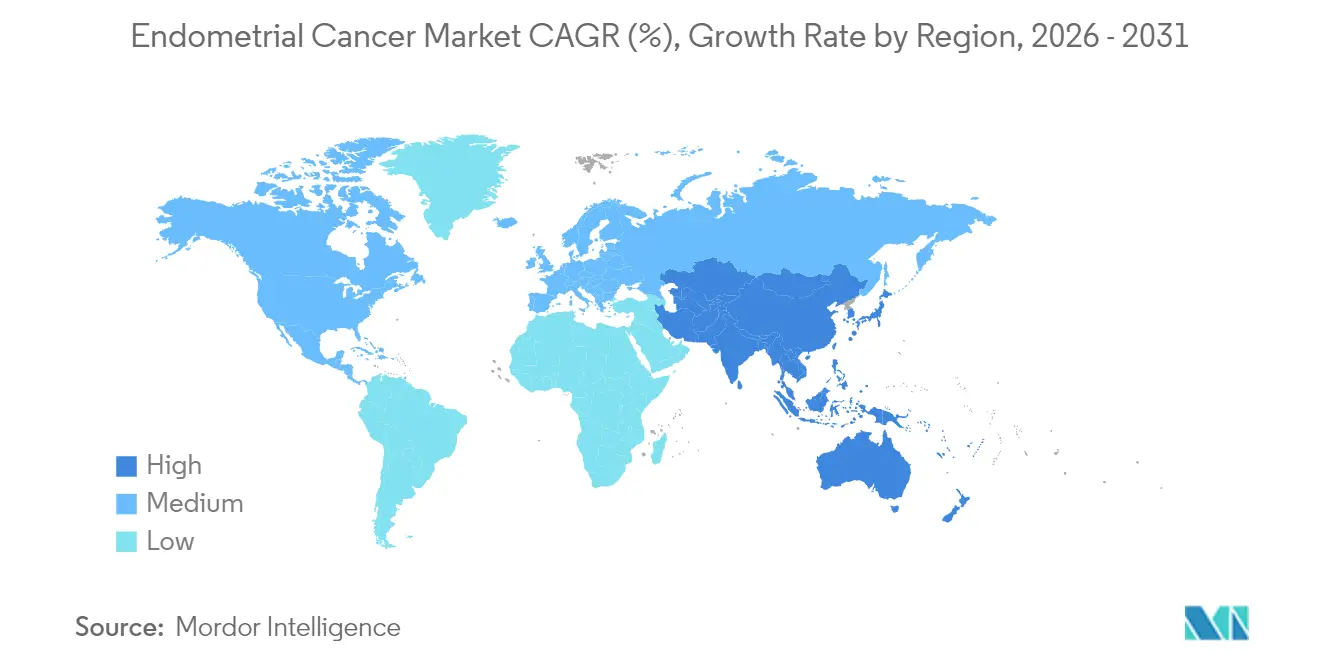

- By geography, North America held 37.25% of the endometrial cancer market size in 2025, while Asia-Pacific records the fastest CAGR at 8.93% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Endometrial Cancer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence linked to obesity & ageing | +1.2% | Global; strongest in NA & EU | Long term (≥ 4 years) |

| Rapid adoption of immunotherapy–chemotherapy combinations | +1.8% | North America & EU lead; APAC follows | Medium term (2-4 years) |

| Favourable reimbursement for targeted therapies | +0.9% | North America & Western Europe | Medium term (2-4 years) |

| Growth in minimally-invasive diagnostic procedures | +0.7% | Global, quicker in developed markets | Short term (≤ 2 years) |

| Outpatient shift for brachytherapy expanding access | +0.4% | North America & Europe, emerging in APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence Linked to Obesity & Ageing Women

Global increases in obesity and longer female life expectancy enlarge the treated population, straining oncology services and creating sustained demand for therapies and diagnostics. Metabolic comorbidities such as diabetes and hypertension raise surgical risk and complicate perioperative management, encouraging earlier adoption of systemic therapy options. Endometrial thickness readings above 14 mm quadruple concurrent malignancy risk, prompting more frequent gynecologic oncology referrals for staging. Healthcare systems respond by scaling multidisciplinary clinics and leveraging tele-oncology to manage rising caseloads, especially in suburban and rural settings. Insurers increasingly recognize obesity-linked risk, approving preventive screening benefits that feed newly diagnosed cases into the treatment pipeline. As high-BMI cohorts enter the 60-65 year age band, the endometrial cancer market is set for long-run expansion.

Rapid Adoption of Immunotherapy–Chemotherapy Combinations

Three checkpoint inhibitor combinations won regulatory clearance between January 2024 and March 2025, each showing superior survival to platinum doublet chemotherapy. Dostarlimab plus carboplatin-paclitaxel extended median overall survival to 44.6 months versus 28.2 months for chemotherapy alone[1]Center for Drug Evaluation and Research, “FDA expands endometrial cancer indication for dostarlimab-gxly with chemotherapy,” fda.gov. Pembrolizumab regimens improved progression-free survival by 70% in mismatch-repair-deficient tumors, while durvalumab cut disease-progression risk by 58% in the DUO-E trial. Such data reset clinical expectations, and national guidelines now recommend combination therapy as frontline care for advanced disease. The shift forces expansion of molecular testing, because biomarker-guided eligibility determines reimbursement and optimizes outcomes. Rapid approvals in Canada and the European Union illustrate global harmonization, enabling multinational trial readouts to convert swiftly into commercial revenue.

Favourable Reimbursement for Targeted Therapies

North American and Western European payers now reimburse immunotherapy combinations for biomarker-selected cohorts, narrowing patient copayments and accelerating adoption. Policies from private insurers such as Premera specify mismatch-repair-deficient status for dostarlimab coverage, embedding molecular biology into reimbursement language. Similar reimbursement frameworks supporting HER2-positive Breast Cancer Treatment have demonstrated the value of biomarker-driven oncology care, encouraging broader adoption of precision medicine approaches across multiple cancer types. Manufacturers offset residual out-of-pocket expenses through generous assistance programs—Pfizer Oncology Together covers up to USD 25,000 annually, and GSK’s schemes support uninsured patients. In emerging economies, managed-entry agreements using value-based pricing shorten previous four-year delays to market entry. As payers increasingly reward therapies delivering durable responses, the endometrial cancer market benefits from faster patient throughput.

Growth in Minimally-Invasive Diagnostic Procedures

Transvaginal ultrasound now offers MRI-comparable accuracy for myometrial-invasion assessment, while office hysteroscopy identifies malignancy in 2.6% of asymptomatic postmenopausal women. Artificial-intelligence algorithms reach 99.26% diagnostic accuracy from histopathology images, trimming pathology turnaround times. Proteomic biomarker panels in cervico-vaginal fluid achieve 91% sensitivity, presenting non-invasive screening alternatives. These innovations reduce patient anxiety, increase compliance, and shift diagnostic work toward outpatient settings, broadening patient reach and bolstering the endometrial cancer market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High treatment costs of novel agents | -0.8% | Global; acute in emerging markets | Medium term (2-4 years) |

| Drug-related toxicities limiting adherence | -0.5% | Global | Short term (≤ 2 years) |

| Radio-isotope supply constraints | -0.3% | Global; acute in Europe & Asia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Treatment Costs of Novel Agents

Checkpoint inhibitor combinations command premium list prices, leading to incremental cost-effectiveness ratios above USD 150,000 per quality-adjusted life year for mismatch-repair-proficient tumors. Pharmacoeconomic studies show dostarlimab plus chemotherapy requires a 15% price trim to meet willingness-to-pay thresholds in China[2]Gengwei Huo et al., “Cost-effectiveness of dostarlimab plus chemotherapy,” Frontiers in Pharmacology, frontiersin.org. Recurrent-disease management adds USD 84,562 in excess annual costs per patient compared with non-recurrent cases. In lower-income regions, reimbursement delays of up to seven years exacerbate survival gaps, constraining the endometrial cancer market despite clinical breakthroughs.

Drug-Related Toxicities Limiting Adherence

Grade-3 or higher immune-related adverse events—such as severe anemia, pneumonitis, and endocrine dysfunction—necessitate dose holds or discontinuation in up to 18% of patients receiving combination regimens. Oncology pharmacists emphasize early recognition protocols and multidisciplinary management algorithms to contain toxicity-related drop-out. Sites lacking specialist support hesitate to initiate immunotherapy, dampening uptake in community hospitals and limiting full realization of the endometrial cancer market potential.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type of Cancer: Carcinoma Dominance Drives Sarcoma Innovation

Endometrial carcinoma anchored the endometrial cancer market with a 73.10% revenue share in 2025, supported by the largest patient pool and extensive evidence for checkpoint inhibitor combinations. Uterine sarcomas, though accounting for a minority of cases, are on an 7.84% CAGR trajectory as precision-surgery techniques and off-label targeted agents improve outcomes. Carcinosarcoma guidelines now recommend dostarlimab-based regimens, reflecting solid survival benefits across mismatch-repair status. Advanced adenocarcinoma responds especially well to pembrolizumab plus carboplatin-paclitaxel, which demonstrated a 70% progression-free survival gain, consolidating physician preference. Molecular sub-typing reveals p53-like NSMP tumors with unexpectedly aggressive behavior; these lesions are enrolling rapidly in next-generation trials exploring double-checkpoint blockade.

AI-enabled histopathology platforms flag high-risk clones previously misclassified, allowing earlier systemic therapy. Lenvatinib-pembrolizumab, studied in carcinosarcoma case series, achieved disease-control rates above 60% with manageable hypertension and fatigue, offering a salvage option when platinum regimens fail. With biomarker testing now routine, therapeutic choice shifts from histology to mutation-based algorithms, deepening segmentation and pushing demand for companion diagnostics within the endometrial cancer market.

By Type of Therapy: Immunotherapy Surge Challenges Chemotherapy Hegemony

Chemotherapy still delivered 44.78% of treatment revenue in 2025, maintaining its footing by pairing with immune checkpoint inhibitors and remaining the default for biomarker-negative patients. Immunotherapy, however, charts the steepest curve, posting a 8.78% CAGR that is forecast to exceed radiation revenue by 2028. Dostarlimab plus chemotherapy cut mortality risk by 31%, prompting many centers to adopt immunotherapy in first-line protocols. The endometrial cancer market size attached to immunotherapy thus expands rapidly as additional combinations earn approval.

Radiation therapy modernizes in parallel: adaptive planning, MRI-guided brachytherapy, and outpatient dosing together shorten courses while protecting organs at risk, preserving a strong albeit slower-growing role. Targeted small-molecule inhibitors and hormonal agents occupy niche indications such as ER-positive recurrent tumors or PI3K-mutant sarcomas. Artificial intelligence decision-support systems aggregate genomic, imaging, and toxicity data, recommending personalized sequencing that improves adherence and minimizes overlapping toxicities. These digital tools further catalyze rational immunotherapy uptake, helping physicians navigate a widening pipeline without inflating adverse-event burden.

By Diagnosis Method: Biopsy Leadership Faces Hysteroscopy Innovation

Tissue biopsy produced 54.02% of diagnostic revenue in 2025 and retains gold-standard status because it yields material for histology and next-generation sequencing—both prerequisites for immunotherapy reimbursement. Yet hysteroscopy’s 7.76% CAGR signals rising preference for see-and-treat pathways that combine direct visualization with targeted tissue removal. Disposable hysteroscopes and improved pain control increase in-office adoption, and reimbursement codes now mirror colonoscopy fee schedules, supporting wider insurer acceptance.

Transvaginal ultrasound, long the frontline triage test, delivers staging clues such as myometrial-invasion depth that approach MRI accuracy at lower cost. AI-enhanced image analysis boosts diagnostic specificity, reducing false positives that previously triggered unnecessary biopsies. Meanwhile, proteomic panels and methylated-DNA tampon assays reach sensitivity thresholds that qualify them as adjuncts for population screening, potentially lowering reliance on invasive sampling. As such non-invasive screens mature, they feed more early-stage cases into surgical queues, further enlarging the endometrial cancer market.

Geography Analysis

North America led the endometrial cancer market size with 37.25% share in 2025 on the strength of broad immunotherapy insurance coverage, high screening penetration, and concentration of specialized oncology centers. Uptake of molecular diagnostics is near-universal, and Health Canada’s 2025 approvals of pembrolizumab and dostarlimab within weeks of each other confirm swift regulatory throughput. Price negotiation mechanisms such as Outcomes-Based Agreements ensure timely public-payer listing while managing budget impact.

Europe remains an innovation-friendly but cost-aware environment. The CHMP’s positive opinion for dostarlimab expansion to all advanced cases sets the stage for continent-wide reimbursement, yet national bodies scrutinize cost-effectiveness ratios, sometimes mandating risk-sharing deals before inclusion. Eastern European markets show slower uptake, but EU cohesion funds now subsidize molecular pathology labs, closing access gaps.

Asia-Pacific exhibits the fastest 8.93% CAGR through 2031, reflecting both demographic pressure and government action. Japan and South Korea integrate immunotherapy into national guidelines, while China leverages domestic manufacturing to lower prices and accelerate approvals via the Hainan Real-World Evidence pilot. A broader disease burden study predicts continuous incidence growth until 2050, especially in women aged 60-64, underscoring sustained demand.

In South America, expanding private insurance and medical-tourism flows influence adoption patterns. Patients from Andean and Central American countries often travel to Brazil for checkpoint inhibitors unavailable locally. Sub-Saharan Africa faces the largest care gaps; 92% of providers surveyed report outbound medical travel for gynecologic oncology, spotlighting unmet need. International aid programs that sponsor pathology-lab upgrades are beginning to narrow the diagnostic divide, which will translate into measurable market growth over the next decade.

Competitive Landscape

Three checkpoint inhibitors—dostarlimab, pembrolizumab, and durvalumab—anchor the treatment algorithm, producing a moderately concentrated endometrial cancer market. Each manufacturer supports extensive trial networks exploring triplet combinations with PARP inhibitors, tyrosine-kinase inhibitors, or novel HER2 vaccines, reinforcing first-mover advantages. GSK published RUBY Part 2 data extending overall-survival gains to mismatch-repair-proficient patients, broadening eligible cohorts. Merck leverages its global KEYNOTE platform to test pembrolizumab plus lenvatinib in early-stage high-risk disease, aiming to expand into the adjuvant setting. AstraZeneca is recruiting for durvalumab-olaparib front-line studies targeting HR-deficient signatures.

Smaller developers pursue niche indications. ImmunityBio’s Anktiva plus AdHER2DC vaccine targets HER2-positive subsets, while Entero Therapeutics engineers nanoparticle immunoconjugates delivering dual payloads in sarcoma models. Diagnostics firms integrate machine learning with digital pathology, offering companion-software modules that predict immune-phenotype from H&E slides, potentially guiding single-agent versus double-agent checkpoint therapy. Partnerships between pathology start-ups and big pharma align reimbursement codes for AI-read services, creating a new competitive axis beyond therapeutics.

Company strategy also extends to supply chain resilience. Novartis’ USD 200 million isotope facility on the US West Coast hedges against European export disruptions, guaranteeing supply for its theragnostic portfolio and enabling bundled radioligand–immunotherapy offerings. Cross-industry collaboration between imaging vendors and pharma aims to co-develop predictive PET tracers that identify early immunotherapy responders, enhancing treatment value.

Endometrial Cancer Industry Leaders

Elekta AB

Karyopharm Therapeutics

Eisai Co., Ltd.

GSK plc

Siemens Healthineers (Varian)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Health Canada expanded Jemperli (dostarlimab) plus chemotherapy approval to all adults with primary advanced or first recurrent endometrial cancer, the first immuno-oncology regimen to show overall survival gain across mismatch-repair status.

- March 2025: Health Canada approved KEYTRUDA (pembrolizumab) with carboplatin-paclitaxel for primary advanced or recurrent endometrial carcinoma following positive KEYNOTE-868 data.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our analysis treats the endometrial cancer market as all revenues generated worldwide from diagnostic procedures (biopsy, imaging, hysteroscopy, and molecular panels) and therapeutic interventions (surgery, radiation, chemotherapy, hormone, targeted, and immuno-oncology drugs) used to manage malignant tumors arising in the uterine endometrium. Mordor Intelligence tracks value at manufacturer selling price for therapeutics and at provider billing price for diagnostics, then aggregates by region, cancer stage, and treatment line.

Scope exclusion: non-malignant endometrial hyperplasia, benign gynecologic procedures, and general supportive-care drugs are left outside this study.

Segmentation Overview

- By Type of Cancer

- Endometrial Carcinoma

- Adenocarcinoma

- Carcinosarcoma

- Squamous Cell Carcinoma

- Other Types

- Uterine Sarcomas

- Endometrial Carcinoma

- By Type of Therapy

- Immunotherapy

- Radiation Therapy

- Chemotherapy

- Other Therapies

- By Diagnosis Method

- Biopsy

- Pelvic Ultrasound

- Hysteroscopy

- CT Scan

- Other Methods

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews with oncologists, gyneco-surgeons, radiologists, payers, and pharmaceutical portfolio managers across North America, several EU nations, China, India, and Brazil helped us verify line-of-therapy uptake rates, average selling prices, and likely launch timelines for late-stage assets. These conversations also clarified regional diagnostic penetration and typical hospital mark-ups, letting us fine-tune desk-based assumptions.

Desk Research

Mordor analysts began with incidence and prevalence datasets from GLOBOCAN, CDC SEER, Eurostat, and Japan's National Cancer Center, which frame patient pools. Regulatory and reimbursement cues were drawn from FDA, EMA, PMDA, and CMS notes, helping us timestamp price shifts for key approvals such as dostarlimab and pembrolizumab. Cost inputs benefited from hospital charge masters, peer-reviewed journals in Gynecologic Oncology, and trade association briefs from the Society of Gynecologic Oncology. Paid libraries including D&B Hoovers for company revenue splits, Dow Jones Factiva for deal flow, and Questel for patent activity strengthened competitive insights. The sources listed illustrate the breadth consulted; many additional public and subscription feeds informed datapoint validation.

Market-Sizing & Forecasting

To build 2025 baselines, we applied a top-down "incidence × treatment rate × cost per treated patient" construct, cross-checking totals with sampled bottom-up tallies from leading drug label sales, biopsy kit shipments, and hysterectomy volumes. Key levers in the model include obesity-linked incidence drift, immunotherapy adoption curves, generic erosion on platinum regimens, procedure pricing in private hospitals, and health-insurance coverage ratios. Forecasts through 2030 are generated through multivariate regression blended with scenario analysis, where incidence trends, drug pipeline success probabilities, and payer cost controls act as drivers. Expert panels provided consensus ranges that anchor variable trajectories. Data gaps in smaller geographies are bridged by proxy indicators such as endometrial cancer share of gynecologic cancers and GDP-adjusted therapy affordability.

Data Validation & Update Cycle

Outputs undergo variance checks against historical series and anonymized hospital charge data; anomalies trigger re-runs before senior analyst sign-off. Reports refresh every twelve months, with mid-cycle edits when material events, such as major drug approvals, pricing reforms, or epidemiology revisions, occur. Prior to publication, an analyst recontacts key sources to ensure our clients receive the latest vetted view.

Why Mordor's Endometrial Cancer Baseline Commands Confidence

Published estimates often differ because firms pick diverse service mixes, price points, and refresh cadences.

Key gap drivers: some studies omit diagnostics, others freeze exchange rates or apply aggressive pipeline uptake. Mordor's scope unites both care segments, employs rolling currency conversion, and updates inputs annually, producing a balanced middle-path number.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 30.6 B (2025) | Mordor Intelligence | - |

| USD 28.9 B (2023) | Global Consultancy A | Therapeutics only, earlier base year, static FX |

| USD 25.1 B (2022) | Industry Journal B | Excludes Asia minor markets, limited pipeline uptake |

In sum, by knitting epidemiology, real-world pricing, and timely approvals into one transparent model, Mordor delivers a dependable baseline that decision-makers can trace, interrogate, and replicate with ease.

Key Questions Answered in the Report

What is the current size of the endometrial cancer market?

The endometrial cancer market size stood at USD 32.09 billion in 2026 and is projected to reach USD 40.66 billion by 2031.

Which therapy class is growing fastest in endometrial cancer treatment?

Immunotherapy combinations lead growth with a 8.78% CAGR through 2031, driven by significant survival benefits demonstrated in multiple phase III trials.

Which region is expected to post the highest market growth?

Asia-Pacific records the fastest regional CAGR at 8.93% to 2031, supported by expanding healthcare access and government oncology initiatives.

How dominant are immunotherapy drugs in the competitive landscape?

Three checkpoint inhibitors—dostarlimab, pembrolizumab, and durvalumab—hold a combined 70% revenue share, giving them leadership but leaving opportunities in niche subtypes.

What are the main cost barriers to novel treatments?

Incremental cost-effectiveness ratios for some combinations exceed USD 150,000 per quality-adjusted life year, prompting payers to negotiate price discounts or restrict use to biomarker-selected patients.

How are diagnostics evolving in endometrial cancer?

AI-enabled histopathology and proteomic biomarker panels deliver accuracy above 90%, while office hysteroscopy and transvaginal ultrasound offer minimally invasive options that streamline early detection workflows.

Page last updated on: