Infertility Drugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.47 Billion |

| Market Size (2031) | USD 5.93 Billion |

| Growth Rate (2026 - 2031) | 5.83% CAGR |

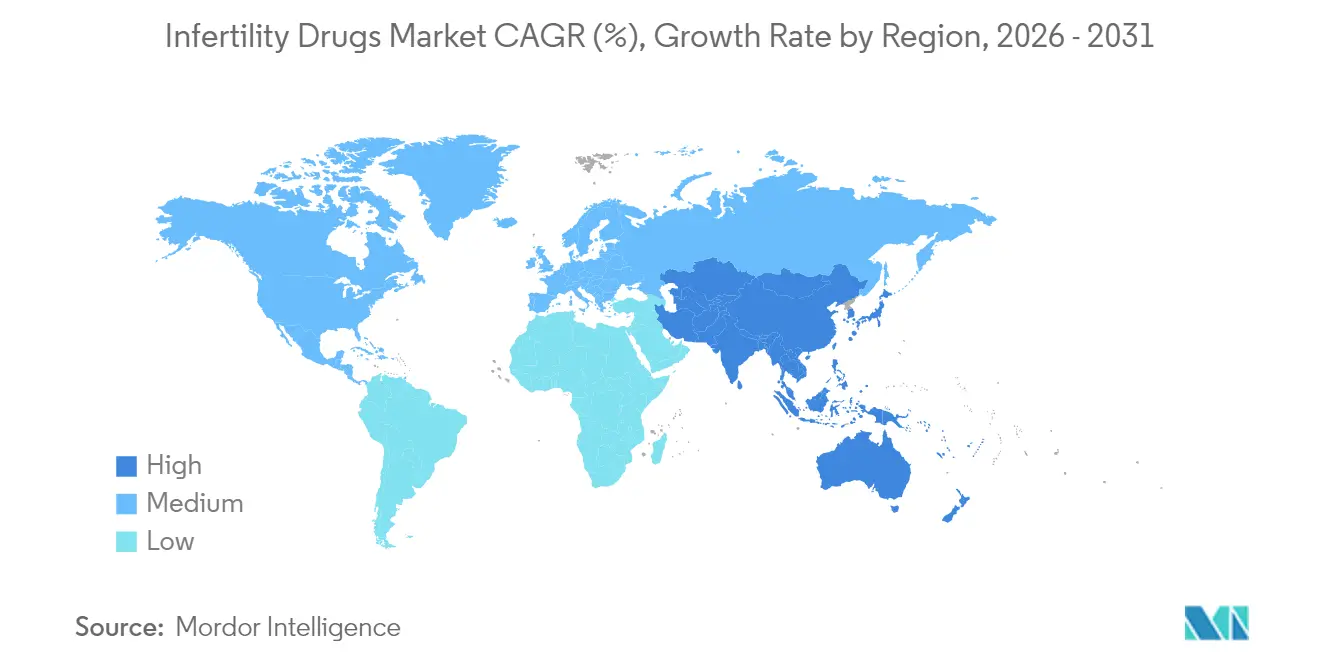

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Infertility Drugs Market Analysis by Mordor Intelligence

The Infertility Drugs Market size was valued at USD 4.22 billion in 2025 and estimated to grow from USD 4.47 billion in 2026 to reach USD 5.93 billion by 2031, at a CAGR of 5.83% during the forecast period (2026-2031). Consistently rising infertility prevalence, wider insurance mandates and rapid progress in assisted reproductive technologies (ART) are the core engines of growth for the infertility drugs market. Demographic shifts toward delayed parenthood have transformed fertility care into an essential health service rather than an elective choice. Reimbursement reforms in North America and Europe are expanding covered lives, while biosimilar introductions are tempering price escalation and stimulating prescribing activity. At the same time, online and specialty pharmacies are reshaping last-mile delivery as telehealth platforms make fertility medications more accessible.

Key Report Takeaways

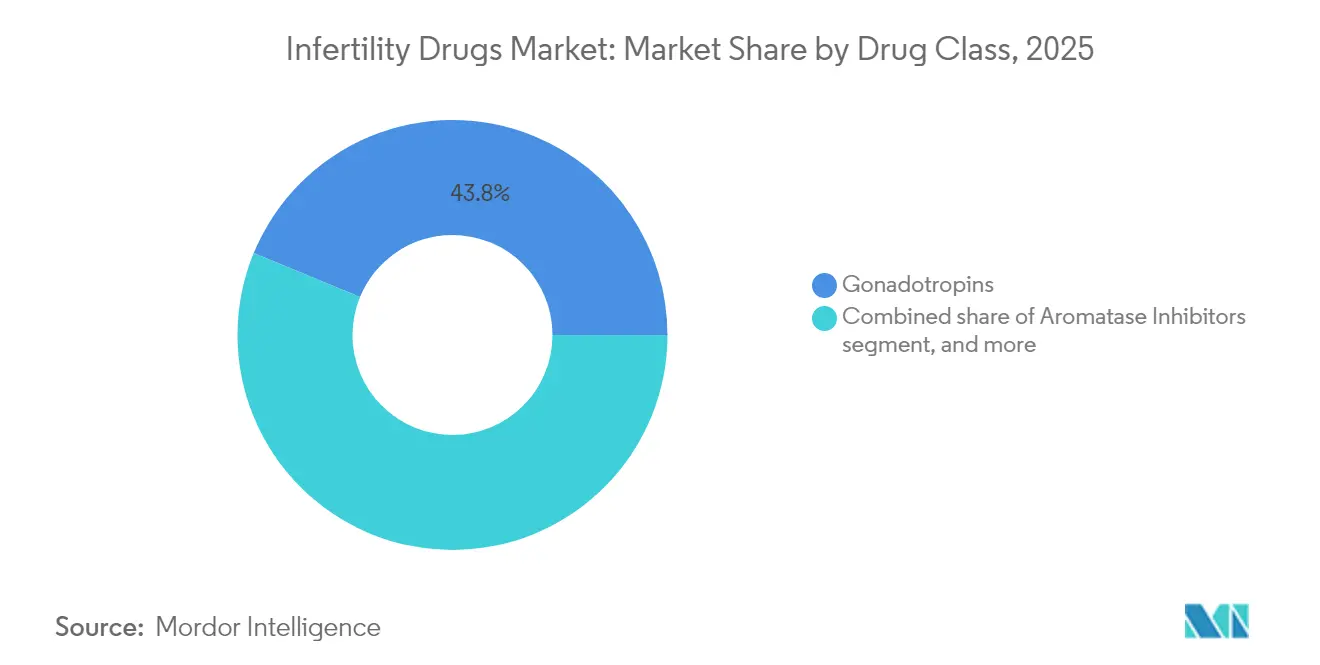

- By drug class, gonadotropins led with 43.78% infertility drugs market share in 2025; aromatase inhibitors are projected to expand at an 8.05% CAGR through 2031.

- By patient gender, female treatments accounted for 70.76% of the infertility drugs market size in 2025, while male therapies are advancing at an 8.62% CAGR to 2031.

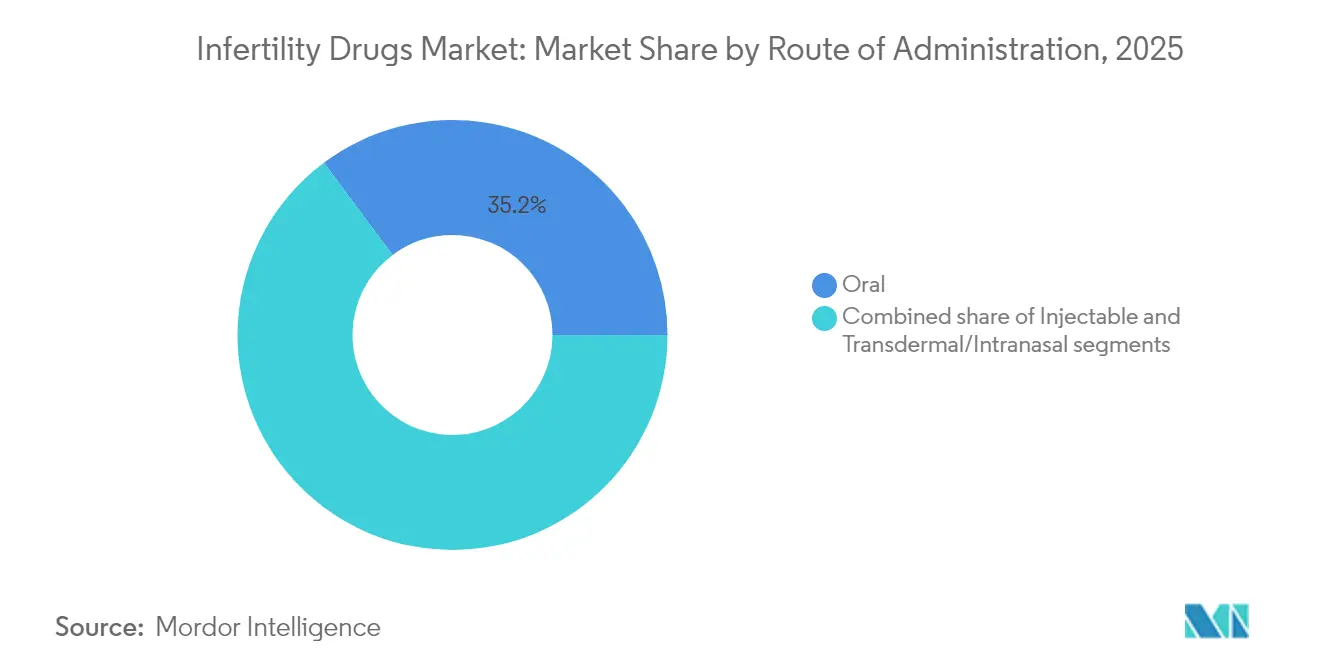

- By route of administration, oral products captured 35.21% of the infertility drugs market size in 2025; injectable formulations are expected to grow fastest at a 8.74% CAGR over 2026-2031.

- By distribution channel, retail pharmacies held 51.62% revenue share in 2025; online and specialty pharmacies are forecast to progress at a 9.28% CAGR through 2031.

- By geography, North America commanded 35.12% of the infertility drugs market size in 2025, whereas Asia-Pacific is the fastest-growing region with a 7.18% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Infertility Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Infertility Prevalence Worldwide | +1.8% | Global (highest impact in APAC and MEA) | Long term (≥ 4 years) |

| Growing Adoption Of Assisted Reproductive Technologies | +1.5% | North America & EU core; expanding in APAC | Medium term (2-4 years) |

| Increasing Government And Private Reimbursement Support | +1.2% | North America, EU, select APAC markets | Short term (≤ 2 years) |

| Advancements In Biosimilar And Novel Hormonal Formulations | +0.9% | Global; regulatory advantages in EU | Medium term (2-4 years) |

| Expanding Access To Fertility Services In Emerging Markets | +0.7% | APAC core; spill-over to MEA and South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Infertility Prevalence Worldwide

Roughly 186 million people live with infertility, and age-standardized prevalence now stands at 1,354.76 per 100,000 in males and 2,764.62 per 100,000 in females, trends linked to delayed childbearing, obesity and lifestyle factors. Asia-Pacific shows the sharpest rise, with secondary infertility surpassing primary infertility and polycystic ovary syndrome (PCOS) acting as a pivotal demand driver. In low-income markets, ART costs exceed 200% of GDP per capita, underscoring untapped demand once health financing improves. Urbanization and shifting career priorities lengthen the window for family planning, embedding infertility therapy in mainstream care pathways. Epidemiological projections anticipate higher infertility incidence through 2036, ensuring sustained need for pharmacologic interventions worldwide.

Increasing Government and Private Reimbursement Support

All EU member states now subsidize at least one IVF cycle, and five nations fund up to six cycles. California’s Senate Bill 729 will compel large-group insurers to cover fertility treatments from July 2025, with small-group plans required to offer coverage options. In the corporate sector, partnerships such as Cigna Healthcare with Progyny offer bundled fertility journeys, reducing out-of-pocket costs from USD 15,000–30,000 to more affordable co-pay levels. Reimbursement expansion across the United States and Europe is steering patient volumes into covered channels and reinforcing the growth of the infertility drugs market.

Advancements in Biosimilar and Novel Hormonal Formulations

Messenger-RNA expression systems are bringing down recombinant hormone production costs, opening a pipeline of lower-priced biosimilars with therapeutic parity. Organon’s licensing of SJ02, a long-acting FSH now under Chinese BLA review, illustrates industry movement toward once-weekly injections that lighten patient burden. Letrozole has overtaken clomiphene citrate as first-line therapy in PCOS, delivering an 8% higher live-birth rate. Novel oral agents such as OXO-001 achieved a 75.9% biochemical pregnancy rate in Phase 2 trials, pointing to non-hormonal modalities that could shift standard protocols. Collectively, these innovations expand physician choice and heighten competition.

Expanding Access to Fertility Services in Emerging Markets

Public–private fertility centers are multiplying across South and Southeast Asia, spurred by government incentives to counteract falling birth rates. China’s national health-care plan added six infertility drugs to the reimbursement list in 2025, cutting average co-pays by 42%[1]National Health Commission of China, “2025 reimbursement list update,” nhc.gov.cn. Gulf states have earmarked dedicated ART budgets and are recruiting foreign embryologists to local hubs. Investment in cold-chain logistics for biologics promises better rural reach, ensuring that the infertility drugs market captures demand in secondary cities across APAC and MEA.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Treatment Costs And Limited Insurance Coverage | -1.4% | Global (highest impact in emerging markets) | Short term (≤ 2 years) |

| Stringent And Divergent Regulatory Approval Pathways | -0.8% | Global with complexity variations by region | Medium term (2-4 years) |

| Social, Ethical, And Cultural Barriers To Treatment Acceptance | -0.6% | MEA, South Asia, parts of Latin America | Long term (≥ 4 years) |

| Drug Safety Concerns Including Ovarian Hyperstimulation Risk | -0.5% | Global; heightened scrutiny in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Treatment Costs and Limited Insurance Coverage

IVF medication prices rose 84% over the past decade, reaching USD 1,279 per cycle and accounting for 35% of total IVF costs, a burden that excludes many low-income patients. Average European IVF cycles cost EUR 4,000–5,000 (USD 4,300–5,400), while public wait lists can stretch to one year in several countries. In low-income regions, ART exceeds 200% of GDP per capita, rendering treatment out of reach. Although biosimilars and insurer mandates are lowering barriers, affordability remains a pivotal short-term restraint for the infertility drugs market.

Stringent and Divergent Regulatory Approval Pathways

Approval timelines vary widely among regulators; FDA biologics reviews have averaged 2,200 days for complex products, complicating patent-term planning[2]United States Federal Register, “Patent term calculation for biologics,” federalregister.gov. The European Medicines Agency cleared only a handful of fertility-related molecules in its 2024 docket, reflecting high evidence thresholds[3]European Medicines Agency, “Medicinal products approved in 2024,” ema.europa.eu. Region-specific clinical trial demands raise development costs and discourage smaller biotechs from global launches. Differing biosimilar rules between the United States and Europe add further uncertainty to market entry strategies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Gonadotropins Hold Leadership Amid Aromatase Inhibitor Momentum

Gonadotropins retained 43.78% infertility drugs market share in 2025, supported by entrenched IVF protocols and physician familiarity. Organon’s Follistim AQ recorded USD 63 million in Q3 2024, a 16% rise year-over-year, illustrating robust baseline demand. Nevertheless, aromatase inhibitors are gaining traction; letrozole’s superior ovulation and live-birth rates have spurred an 8.05% CAGR forecast through 2031. Evidence from randomized trials showing a 13% higher ovulation rate versus clomiphene is accelerating guideline revisions.

Second-tier classes remain relevant. Selective estrogen receptor modulators continue to anchor first-line treatment in resource-constrained settings. Biguanides, particularly metformin, are prescribed adjunctively to improve metabolic parameters in PCOS, though they represent a small revenue slice. Dopamine agonists like cabergoline prevent ovarian hyperstimulation syndrome; comparative trials indicate equivalent efficacy to hydroxychloroquine with better tolerability. As dosing research evolves—sequential 2.5 mg letrozole/FSH protocols have achieved 72.7% cumulative pregnancy versus 59.1% for 5 mg regimens—the infertility drugs market is expected to tilt further toward targeted, lower-dose options.

By Patient Gender: Female Therapies Dominate While Male Care Accelerates

Female indications generated 70.76% of 2025 revenue owing to established clinical pathways and broader drug labels. Demand remains solid for ovulation-induction agents as delayed motherhood becomes common in developed economies. The male segment, however, is catching up with an 8.62% CAGR to 2031, driven by increased screening and destigmatization. Ferring Pharmaceuticals teamed with Posterity Health to roll out a Male Fertility Program, acknowledging that male factors contribute to half of infertility cases.

Therapeutic advances bolster this growth. Weekly low-dose letrozole restored fertility in 12 obese men with hypogonadotropic hypogonadism in a Canadian cohort pilot. Oxidative stress management is another frontier, as antioxidants target the 20-30% of male infertility linked to reactive oxygen species. Bioactive compounds such as resveratrol and curcumin are being explored for patients facing cancer-therapy infertility, especially prepubertal males unable to bank sperm. Simultaneous couple evaluation protocols are shifting prescribing patterns to encompass both partners, expanding the addressable pool for the infertility drugs market.

By Route of Administration: Oral Convenience Meets Injectable Efficacy

Oral formulations controlled 35.21% of global revenue in 2025 and remain popular for first-line PCOS management and adjunctive therapy. Yet injectables post a 8.74% CAGR outlook because ART cycles still rely heavily on subcutaneous or intramuscular gonadotropins. The recent Phase 3 trial of single-injection rhFSH-CTP confirmed comparable clinical pregnancy rates to daily injections with improved adherence, supporting broader rollout.

Product innovation focuses on patient comfort and outcomes. Organon’s once-weekly SJ02 targets convenience without efficacy trade-offs. Oral pipeline molecules such as OXO-001, a non-hormonal endometrial modulator, achieved a 75.9% biochemical pregnancy rate in Phase 2 testing. Transdermal patches and intranasal sprays are at pre-clinical stages but promise needle-free delivery over the long term.

By Distribution Channel: Digital Platforms Challenge Brick-and-Mortar Dominance

Retail pharmacies captured 51.62% of 2025 sales through prescription capture and face-to-face counseling. However, specialty and online pharmacies are forecast to grow 9.28% annually as telehealth adoption rises. The infertility drugs market benefits from virtual consults that compress patient journeys and integrate drug dispensing. Specialty pharmacies differentiate via injection-training services, adherence monitoring and insurance navigation, driving high repeat purchase rates.

Cold-chain logistics capability is a decisive factor because many biologics require 2–8 °C storage. Online distributors investing in validated cold-chain packaging now match hospital pharmacies in product integrity. Younger demographics value discretion and doorstep delivery, making e-commerce the preferred channel for repeat cycles. In regions such as the Middle East & Africa, where retail still commands 68.5% of pharmaceutical value, omnichannel models are emerging to blend in-store pick-up with digital ordering.

Geography Analysis

North America held 35.12% of global revenue in 2025, anchored by insurance mandates and well-resourced IVF centers. California’s upcoming coverage law is expected to add more than 2 million insured lives to the fertility cohort, reinforcing demand momentum. Corporate benefit packages, typified by Cigna–Progyny bundles, are reshaping employer offerings for millennial and Gen-Z workforces.

The Asia-Pacific region is the fastest-growing geography at a 7.18% CAGR through 2031. Declining birth rates in China, Japan and South Korea spur government support for ART, while nations such as Thailand and Malaysia compete for medical tourists. Single-injection rhFSH-CTP trials in Chinese women show clinical parity to western protocols, demonstrating home-grown research strength. Price differentials—USD 10,200 per IVF cycle in Singapore versus USD 2,700 in India—are channeling cross-border patient flows, expanding the infertility drugs market across ASEAN.

Europe presents a mature but still expanding landscape. All EU states now fund at least one IVF cycle, yet only five provide up to six fully reimbursed cycles, driving patients into private clinics to avoid long wait times. Middle East & Africa’s pharmaceutical spend rose to USD 32.6 billion in 2024, but infertility care remains nascent. Demographic infertility in MENA reaches 22.6%, signaling strong future upside if regulatory and financing frameworks improve iqvia.com. South America is at an earlier stage but is seeing rising ART uptake as Brazil, Argentina and Chile expand public financing.

Competitive Landscape

The infertility drugs market is moderately fragmented. Merck KGaA generated EUR 1.5 billion (USD 1.6 billion) from fertility products in 2024, posting 0.8% organic growth despite tough comps. Organon’s women’s health division recorded USD 440 million in 2024, helped by Follistim AQ’s 16% revenue increase. Ferring Pharmaceuticals continues to anchor the injectables space and recently published data on equitable access and gonadotropin selection.

Strategy centers on partnerships and licensing to broaden pipelines quickly. Organon’s deal for SJ02 offers geographic reach in China, while emerging firms like Gameto are advancing induced-pluripotent-cell technology to reduce hormone exposures by 80%. Artificial intelligence in IVF labs is raising success rates and serving as a competitive differentiator. Venture capital appetite is healthy; ReproNovo closed a USD 65 million Series A for leflutrozole (RPN-001) targeting male infertility and nolasiban (RPN-002) for adenomyosis.

Pipeline differentiation is sharpening. Long-acting injectables, oral non-hormonal agents and male-specific therapies are high-priority areas. Biosimilar competition is expected to intensify in Europe first, pressuring price points but widening patient access.

Infertility Drugs Industry Leaders

Ferring Pharmaceuticals Inc

Pfizer Inc.

Merck KGaA

Bayer AG

Novartis AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: ReproNovo raised USD 65 million Series A financing to advance RPN-001 for male infertility and RPN-002 for adenomyosis.

- May 2025: Granata Bio secured investment from Gedeon Richter to scale R&D in fertility therapeutics.

- February 2025: Organon licensed long-acting FSH candidate SJ02 from Bao Pharmaceutical and Centergene Pharmaceuticals.

- January 2025: Gameto received FDA clearance for Phase 3 trial of Fertilo, an iPSC-based egg-maturation therapy.

- January 2025: Cigna Healthcare partnered with Progyny to launch end-to-end fertility benefits for employers.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the infertility drugs market as prescription hormonal and adjunct medications, such as gonadotropins, selective estrogen-receptor modulators, aromatase inhibitors, biguanides, and dopamine agonists, that physicians use to induce or regulate ovulation or to stimulate spermatogenesis in medically diagnosed infertility cases.

Scope exclusion: Over-the-counter fertility supplements, IVF procedure fees, and ART equipment revenues remain outside this value pool.

Segmentation Overview

- By Drug Class

- Gonadotropins

- Selective Estrogen Receptor Modulators (SERMs)

- Aromatase Inhibitors

- Biguanides (Metformin)

- Dopamine Agonists

- Other Drug Classes

- By Patient Gender

- Female

- Male

- By Route Of Administration

- Oral

- Injectable (SC / IM)

- Transdermal / Intranasal

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online & Specialty Pharmacies

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed reproductive endocrinologists, hospital pharmacists, payor medical officers, and regional drug-registry staff across North America, Europe, India, and Brazil. These discussions validated therapy mix shifts, reimbursement ceilings, and pipeline launch probabilities that secondary data alone could not capture.

Desk Research

We began with public health benchmarks from bodies such as the World Health Organization, the U.S. Centers for Disease Control and Prevention, Eurostat, and OECD Health Statistics, which quantify infertility prevalence and treatment cycles. Trade-class data from UN Comtrade and customs dashboards helped us approximate cross-border hormone shipments, while drug-approval dossiers on FDA and EMA portals clarified label indications and generic entry timing. For company-level inputs, D&B Hoovers financials and Dow Jones Factiva newsfeeds supplied revenue splits and launch timelines. Patent intensity around recombinant FSH was gauged via Questel. These sources, among several others, created the documentary spine of our desk research; the list is illustrative, not exhaustive.

A second pass extracted average selling prices from hospital procurement portals and national reimbursement lists, then synced them with volume proxies such as IVF-cycle counts from ESHRE and ART clinic registries in Asia-Pacific. This layering ensured geographic consistency before we advanced to primary verification.

Market-Sizing & Forecasting

We apply a top-down prevalence-to-treated-cohort build that starts with infertility incidence, narrows to pharmacologically treated cases, and multiplies by weighted therapy days and net ASPs. Supplier roll-ups and sampled clinic channel checks provide a bottom-up sense check, allowing us to reconcile gaps and refine region-specific uptake factors. Key variables in the model include female infertility prevalence, ART cycle growth, branded-to-biosimilar price erosion, regulatory reimbursement caps, average treatment length, and pipeline entry timing. Forecasts use multivariate regression supplemented by ARIMA smoothing to project each driver, after which scenario analysis tests high-age-first-birth and reimbursement-expiry shocks.

Data Validation & Update Cycle

Outputs pass three-layer variance checks, peer review, and anomaly alerts before sign-off. Reports refresh every twelve months, with interim updates triggered by major drug approvals or reimbursement shifts. An analyst re-validates the model immediately prior to client delivery.

Why Mordor's Infertility Drugs Baseline Is Dependable

Published estimates often diverge because firms pick different drug baskets, unit metrics, and refresh cadences.

We anchor our baseline on treated-patient volumes and validated ASPs, which are then pressure tested with primary insights.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.22 B (2025) | Mordor Intelligence | - |

| USD 4.0 B (2024) | Global Consultancy A | Includes OTC supplements; applies static ASPs |

| USD 3.4 B (2022) | Industry Data Firm B | Older base year; omits biosimilar erosion |

| USD 3.94 B (2024) | Research Publisher C | Uses clinic revenues blended with drug sales |

Differences arise mainly from scope creep, untimely baselines, or price-mix assumptions. By centering on regulated prescription drugs, refreshing annually, and triangulating every assumption with clinical and trade voices, Mordor delivers a transparent, reproducible starting point for strategic decisions.

Key Questions Answered in the Report

How big is the Infertility Drugs Market?

The Infertility Drugs Market size is expected to reach USD 4.47 billion in 2026 and grow at a CAGR of 5.83% to reach USD 5.93 billion by 2031.

Who are the key players in Infertility Drugs Market?

Ferring Pharmaceuticals Inc, Pfizer Inc., Merck KGaA, Novartis International AG and Bayer AG are the major companies operating in the Infertility Drugs Market.

Which is the fastest growing region in Infertility Drugs Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in Infertility Drugs Market?

In 2025, the North America accounts for the largest market share in Infertility Drugs Market.

Page last updated on: