Vulvar Cancer Therapeutics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.74 Billion |

| Market Size (2031) | USD 1.21 Billion |

| Growth Rate (2026 - 2031) | 10.30% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

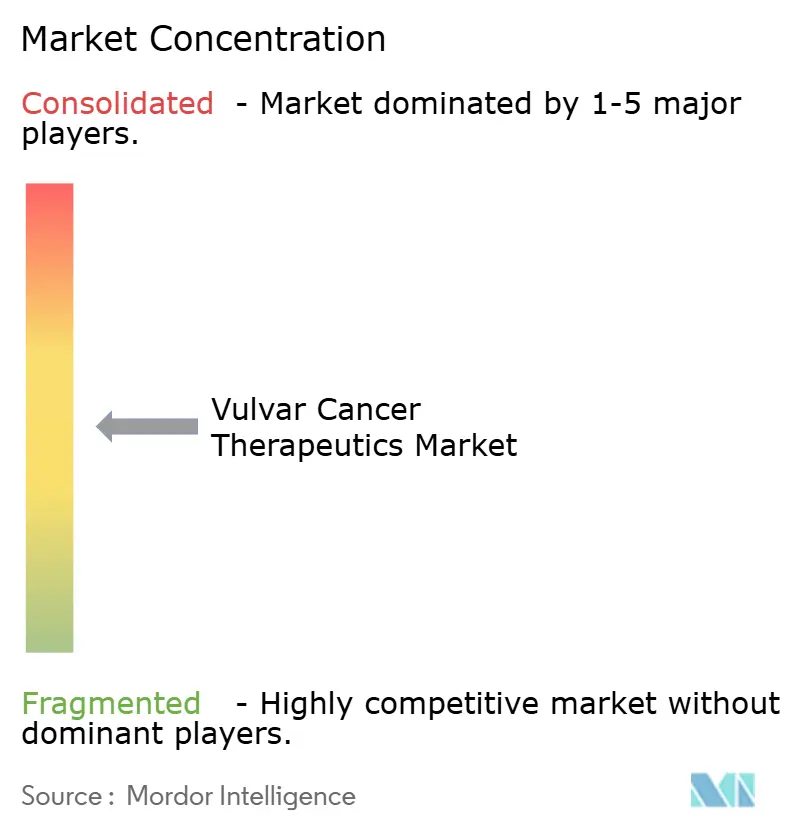

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vulvar Cancer Therapeutics Market Analysis by Mordor Intelligence

The Vulvar Cancer Therapeutics Market size was valued at USD 0.67 billion in 2025 and is estimated to grow from USD 0.74 billion in 2026 to reach USD 1.21 billion by 2031, at a CAGR of 10.30% during the forecast period (2026-2031).

The vulvar cancer therapeutics market is advancing with wider adoption of immune checkpoint inhibitors, a stronger clinical trial pipeline in rare gynecologic cancers, and a rising disease burden linked to HPV-related cases. The National Cancer Institute estimates 7,130 new vulvar cancer cases in the United States in 2026; age-adjusted incidence increased by 0.6% annually from 2014 to 2023, while mortality rose by 1.9% annually from 2015 to 2024.[1]National Cancer Institute, “Cancer Stat Facts, Vulvar Cancer,” SEER, seer.cancer.gov These trends are driving a shift beyond surgery-led care toward organ-sparing multimodal treatment, with chemoradiation and immunotherapy increasingly used in a coordinated manner for advanced disease. Competitive activity remains moderate to high, supported by rare-cancer designations, premium pricing opportunities, label extensions by larger companies, targeted vaccine and combination approaches by smaller developers, and a commercial window through 2031 as older unvaccinated cohorts enter peak treatment years despite the long-term impact of vaccination programs.

Key Report Takeaways

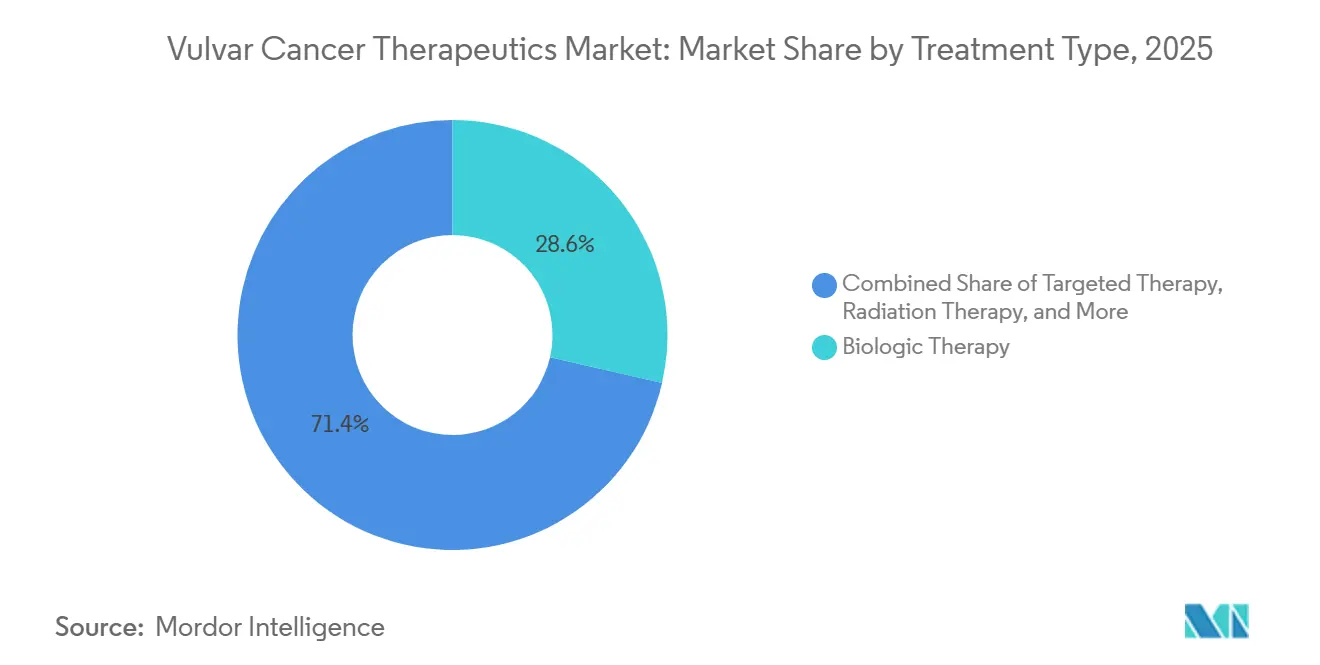

- By treatment type, biologic therapy held 28.58% of revenue in 2025, while immunotherapy is projected to expand at an 11.45% CAGR through 2031 in the vulvar cancer therapeutics market.

- By cancer type, vulvar squamous cell carcinoma accounted for 37.45% of the 2025 market value in the vulvar cancer therapeutics market.

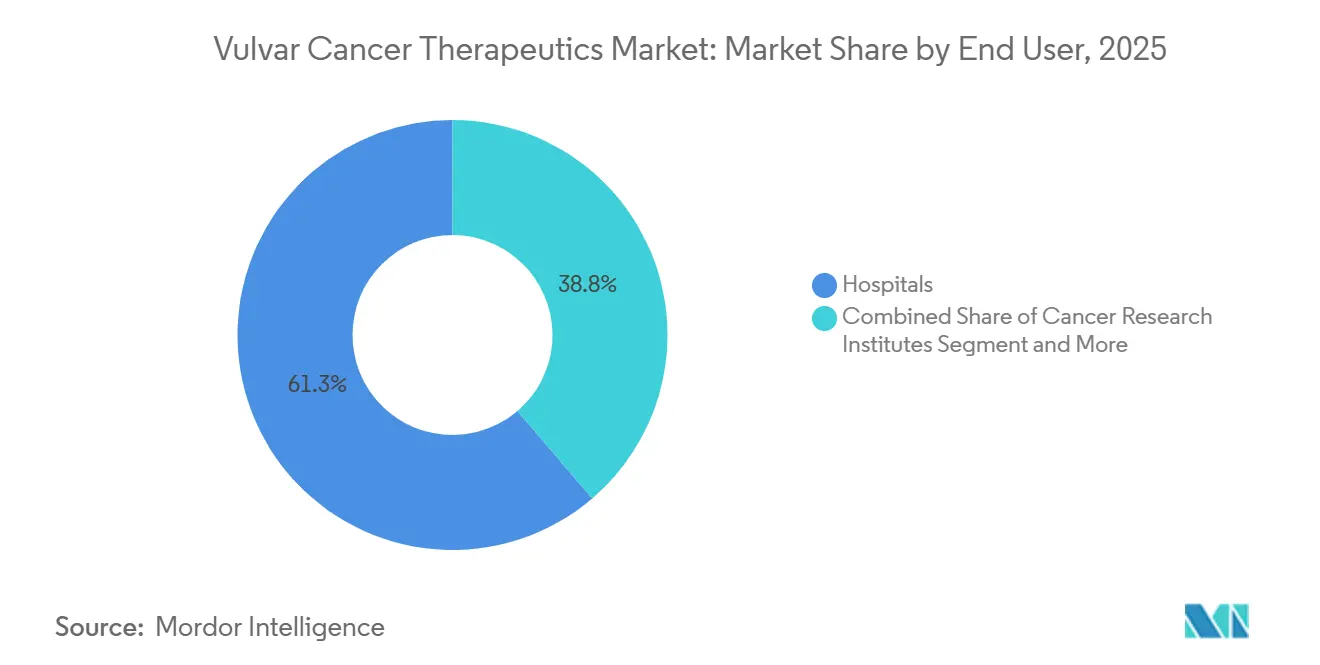

- By end user, hospitals held 61.25% of revenue in 2025, while cancer research institutes are forecast to grow at a 13.10% CAGR through 2031 in the vulvar cancer therapeutics market.

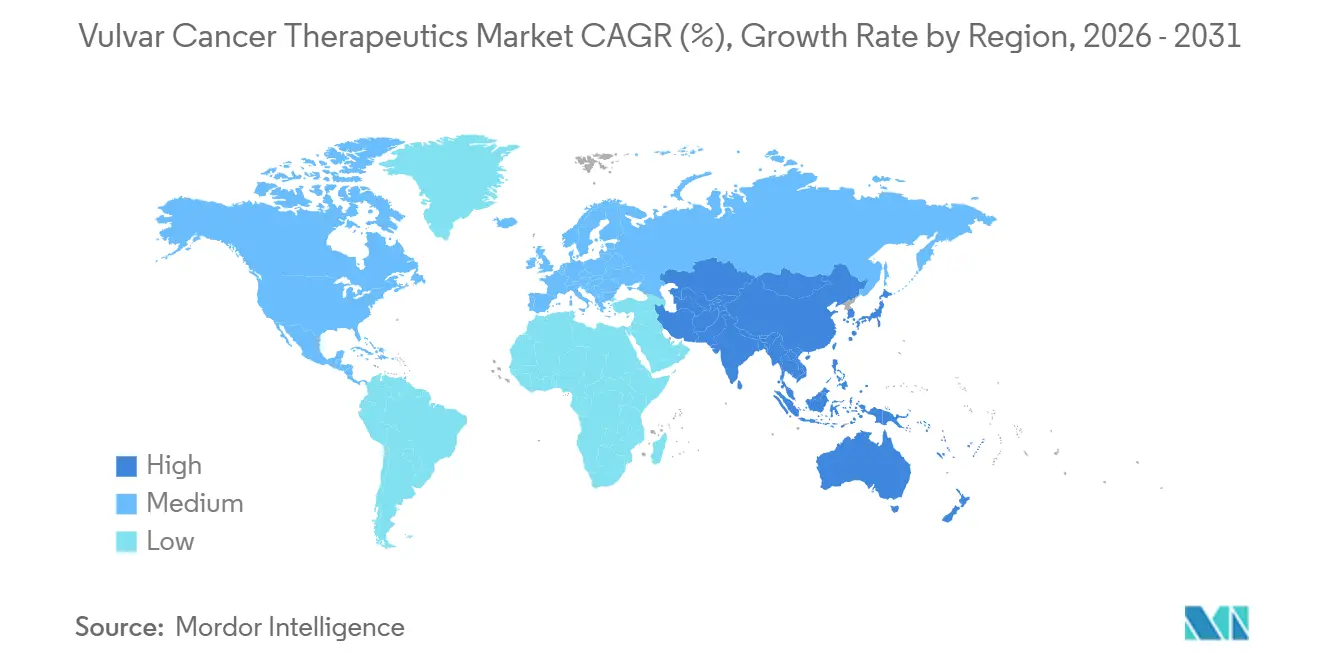

- By geography, North America remained the leading regional contributed 40.30% in 2025, while Asia-Pacific is projected to advance at an 11.56% CAGR through 2031 in the vulvar cancer therapeutics market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Vulvar Cancer Therapeutics Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising HPV-associated vulvar squamous cell carcinoma incidence | +2.1% | Global, with near-term concentration in North America and Western Europe, and a secondary buildout in Asia-Pacific | Medium term (2-4 years) |

| Expanding immunotherapy and biomarker-driven treatment approaches | +2.8% | North America first, followed by spillover into European and Asia-Pacific academic centers | Short term (≤ 2 years) |

| Increasing clinical trial activity in rare gynecologic oncology | +1.4% | North America and Europe, with Asia-Pacific emerging through site activation in Japan, South Korea, and Australia | Medium term (2-4 years) |

| Wider adoption of multimodal treatment pathways in advanced disease | +1.6% | Global, led by North America and high-volume European cancer centers | Medium term (2-4 years) |

| Improved sentinel node and imaging-guided surgical precision | +0.9% | Europe and North America, with early gains in Australia and Japan | Long term (≥ 4 years) |

| Earlier molecular profiling for HPV-independent tumors | +1.1% | North America, Germany, and the Netherlands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising HPV-Associated Incidence Expanding the Treatment Pool

HPV-positive vulvar cancer is expanding the addressable patient base for the vulvar cancer therapeutics market, particularly among older women entering higher treatment-use years. The 55-64 age group recorded a 53% increase in HPV-positive cases between 2000 and 2024, supporting a larger pool of patients likely to require systemic therapy over the forecast period.[2]International Agency for Research on Cancer, “GLOBOCAN 2020, Vulva Fact Sheet,” World Health Organization, gco.iarc.who.int Countries such as Germany, the Netherlands, and Canada have high age-standardized incidence rates, indicating unmet demand in markets with established oncology spending capacity. Vaccination will reduce future disease burden over time, but it is not expected to materially reduce the treated population during this forecast window, as its benefits will emerge later than the current wave of diagnoses.

Expanding Immunotherapy and Biomarker-Driven Treatment Approaches

Immunotherapy remains a key growth driver in the vulvar cancer therapeutics market as it shifts from a limited salvage role to structured treatment pathways. Phase 2 findings expected to be presented at the 2025 ASCO Annual Meeting show that pembrolizumab with cisplatin-sensitized radiation, followed by pembrolizumab maintenance, delivers a 75% objective response rate, a 37.5% complete response rate, and a 70% 6-month recurrence-free survival rate in unresectable vulvar squamous cell carcinoma.[3]O. Yeku et al., “Primary Results of a Phase 2 Study of Cisplatin-Sensitized Radiation Therapy and Pembrolizumab for Unresectable Vulvar Cancer,” Journal of Clinical Oncology, doi.org Evidence from a 2025 systematic review and meta-analysis also supports immune checkpoint inhibitors in advanced vulvar cancer, with encouraging response patterns and manageable toxicity. Biomarker-linked selection is becoming more important, with treatment use increasingly tied to PD-L1, MSI-H, and TMB-H status rather than histology alone.

Increasing Clinical Trial Activity in Rare Gynecologic Oncology

Active development programs are moving the vulvar cancer therapeutics market into a more sustained trial phase, with more than 10 pipeline candidates across combinations, vaccines, and antibody-drug conjugates. The MITO VULVA-01 study is scheduled to begin in March 2026 and enroll 80 patients across 3 cohorts to evaluate pembrolizumab plus lenvatinib 20 mg in locally advanced treatment-naive, metastatic chemotherapy-naive, and platinum-pretreated disease.[4]U.S. National Library of Medicine, “Pembrolizumab Plus Lenvatinib in Vulvar Cancer Patients, MITO VULVA-01,” ClinicalTrials.gov, clinicaltrials.gov This design highlights rising sponsor commitment to tailored study structures in vulvar cancer. A deeper trial base can improve regulatory visibility and support broader commercial uptake.

Wider Adoption of Multimodal Treatment Pathways in Advanced Disease

Multimodal care is strengthening clinical practice in the vulvar cancer therapeutics market as treatment becomes more coordinated across surgery, radiation, and systemic therapy. Referral centers treating advanced disease are integrating sentinel lymph node mapping, precision chemoradiation, and immunotherapy more effectively. As a result, node-positive and unresectable patients are reaching systemic therapy earlier, increasing exposure to biologics and checkpoint-based regimens. Wider adoption of these pathways should support a more consistent treatment model, although uptake will remain faster in healthcare systems with stronger oncology infrastructure.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Small patient pool limiting commercial scale | -1.3% | Global, with the strongest effect in fragmented lower-income markets without centralized referral networks | Long term (≥ 4 years) |

| High treatment cost and reimbursement friction for novel therapies | -1.5% | Europe, Eastern Europe, Middle East and Africa, and South America | Short term (≤ 2 years) to Medium term (2-4 years) |

| Limited labelled indications and sparse pivotal data | -1.2% | Global, with a larger effect in Europe where mature survival data are often required for access | Medium term (2-4 years) |

| Post-surgical morbidity and quality-of-life concerns affecting treatment adherence | -0.8% | Global, with greater impact in under-resourced health systems lacking multidisciplinary support | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Small Patient Pool Limiting Commercial Scale

The small treated population remains a key constraint on the vulvar cancer therapeutics market, influencing trial design, pricing strategy, and dedicated commercial investment. GLOBOCAN estimates 47,336 new vulvar cancer cases globally, while the United States alone is projected to record 7,130 cases in 2026, keeping the patient pool small by oncology standards. This limits the feasibility of large Phase 3 trials and keeps many programs in single-arm or small randomized Phase 2 formats, which can slow reimbursement decisions when payers require mature survival data. Companies may also prioritize tumor-agnostic access routes over disease-specific commercial platforms, limiting the long-term depth of the vulvar cancer therapeutics market.

High Treatment Cost and Reimbursement Friction for Novel Therapies

High treatment costs and reimbursement challenges continue to restrain the vulvar cancer therapeutics market, as novel regimens remain expensive and access varies across major healthcare systems. EFPIA reported in 2025 that Germany reimbursed nearly all EMA-approved cancer medicines within 100 days, while several Eastern European countries took close to 900 days on average, showing how regional delays can limit real-world use after approval. This gap has a stronger impact in vulvar cancer because low patient volumes make each access delay more damaging to early commercial traction. Diagnostic requirements, including PD-L1 CPS scoring, MSI-H testing, and TMB assessment, add further barriers in lower-resource settings, making market growth dependent on diagnostic readiness and payer alignment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Type: Immunotherapy Redefining Second-Line and Multimodal Positioning

Biologic therapy is expected to hold 28.58% of the vulvar cancer therapeutics market share in 2025, while immunotherapy is projected to grow at a CAGR of 11.45% from 2026 to 2031. This indicates an established treatment base for biologics, while immune-based approaches gain faster adoption as clinical practice evolves. Immunotherapy growth is supported by biomarker-led patient selection, broader combination use, and rising relevance in advanced disease. Pembrolizumab remains a key example, supported by Phase 2 results presented in 2025 showing a 75% objective response rate, a 37.5% complete response rate, and a 70% six-month recurrence-free survival rate when combined with cisplatin-sensitized radiation and followed by maintenance treatment.

By Cancer Type: VSCC's Dual Dominance Anchors Market Volume and Innovation Pipeline

Vulvar squamous cell carcinoma is expected to account for 37.45% of the 2025 market value, making it the largest cancer type segment in the vulvar cancer therapeutics market. Its leadership is driven by high case volume and strong research focus, as this histology represents most diagnosed vulvar malignancies and attracts most clinical development activity. VSCC biology and treatment patterns continue to shape major systemic treatment programs, future approvals, treatment guidelines, and pricing logic. The HPV-associated and HPV-independent pathways behave as two distinct biological settings, making treatment selection increasingly linked to subtype, recurrence risk, and expected response to immune-based care, while vulvar melanoma remains relevant due to treatment approaches developed for cutaneous melanoma.

By End User: Cancer Research Institutes Emerging as Commercially Critical Channel

Hospitals are expected to hold 61.25% of revenue in 2025, while cancer research institutes are projected to grow at a CAGR of 13.10% through 2031 in the vulvar cancer therapeutics market. Hospitals lead due to their broad treatment mix, including surgery, radiation, infusion-based chemotherapy, and early institutional use of new systemic therapies. Research-focused settings are expanding faster as rare-cancer development depends on concentrated patient flow, structured trial participation, biomarker testing, and early physician familiarity. High-volume academic programs often adopt new regimens first and generate evidence that later supports broader hospital use.

Geography Analysis

North America is expected to remain the largest regional contributor to the vulvar cancer therapeutics market in 2025, supported by strong oncology infrastructure and wider adoption of biomarker-linked treatment pathways. The United States is the primary driver, with high patient volume and the FDA's tumor-agnostic framework supporting access to pembrolizumab in selected vulvar cancers. The National Cancer Institute projects 7,130 new cases in the United States in 2026, while age-adjusted incidence increased by 0.6% annually from 2014 to 2024 and mortality rose by 1.9% annually from 2015 to 2024. Canada strengthens the regional opportunity, as GLOBOCAN places it among countries with high age-standardized incidence, while Mexico remains an earlier-stage opportunity with expanding infrastructure in major cities but limited access to newer biologics and immunotherapies.

Europe is expected to be the second-largest regional contributor to the vulvar cancer therapeutics market, with Germany, France, and the United Kingdom serving as the main research and treatment centers. France also remains relevant, as the UNICANCER AcSé Immunotherapy program expanded study access for rare dMMR/MSI-H cancers, including vulvar cancer, across 24 French centers from July 2024. However, regional access remains slower than in the United States, as reimbursement bodies often require more mature survival evidence before supporting broad access, and EFPIA documented significant differences in time to availability across European countries.

Asia-Pacific is expected to be the fastest-growing region in the vulvar cancer therapeutics market, with a forecast CAGR of 11.56% from 2026 to 2031. Growth is driven by large patient populations, rising oncology capacity, and stronger regulatory focus on rare-cancer treatment pathways. Japan is gaining visibility through accelerated rare-cancer review mechanisms and deeper institutional research, while South Korea and Australia represent the higher-access tier due to advanced treatment systems and stronger participation in multinational trials. China and India remain the key volume opportunities, as tertiary oncology expansion and private hospital growth improve urban access; GCC countries and South Africa lead the Middle East and Africa, while Brazil and Argentina anchor South America, although reimbursement constraints continue to limit broader commercial penetration across both regions.

Competitive Landscape

The vulvar cancer therapeutics market is moderately concentrated at the company level but remains fragmented by indication, disease stage, and line of therapy. No single product holds a vulvar-cancer-specific label across all major lines of therapy in both the United States and the European Union at the same time. This creates opportunities for large-cap oncology companies and smaller developers to compete through different regulatory and clinical entry points. The market structure reflects a balance between commercial scale and focused niche innovation.

Merck & Co. holds the most visible commercial position, as pembrolizumab benefits from tumor-agnostic treatment relevance and continues to generate supporting evidence in vulvar cancer. The June 2025 Phase 2 readout combining pembrolizumab with cisplatin-sensitized radiation is expected to establish a stronger efficacy benchmark for unresectable vulvar squamous cell carcinoma and reinforce a combination-led strategy in the vulvar cancer therapeutics market. Another strategic move is the March 2026 MITO VULVA-01 study, which is evaluating pembrolizumab plus lenvatinib across three distinct clinical cohorts rather than in a single pooled population. The June 2026 registration of becotatug vedotin with zimberelimab adds another example, bringing an ADC plus immune checkpoint combination into the market for recurrent and metastatic disease.

Smaller innovators are shaping the vulvar cancer therapeutics market through HPV-targeted therapeutic vaccines and differentiated immune strategies. ISA Pharmaceuticals and PDS Biotechnology are pursuing programs designed to prime immune responses more selectively in HPV16-driven tumors, which could create a distinct treatment niche if later-stage results remain supportive. Checkpoint monotherapy has historically shown only modest response rates, leaving room for more active combinations and more targeted immune approaches. A meaningful white space also remains in HPV-independent, p53-mutant disease, where validated targeted options are limited and future differentiation remains possible.

Vulvar Cancer Therapeutics Industry Leaders

Bristol-Myers Squibb Company

Merck & Co., Inc.

F. Hoffmann-La Roche Ltd

GSK plc

Pfizer Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Italy's National Cancer Institute Naples activated the MITO VULVA-01 Phase 2 trial (NCT07290894) to assess pembrolizumab plus lenvatinib 20 mg in 80 vulvar cancer patients across three cohorts, with completion expected in October 2031.

- June 2026: A prospective, multicenter, single-arm trial (NCT07424664) evaluated becotatug vedotin with zimberelimab in 30 patients with recurrent and metastatic vulvar, cervical, and vaginal cancers.

- May 2026: Germany's AWMF published an updated S3 guideline for vulvar carcinoma and its precursors, incorporating immunotherapy into multimodal care for advanced and metastatic disease.

- June 2025: Phase 2 data from NCT04430699 showed pembrolizumab plus cisplatin-sensitized radiation, followed by maintenance pembrolizumab, achieved a 75% objective response rate in unresectable vulvar squamous cell carcinoma.

- June 2025: AGO Research GmbH initiated enrollment in NCT05903833 to evaluate pembrolizumab 400 mg Q6W with lenvatinib 20 mg daily in 42 patients with recurrent, persistent, or metastatic vulvar squamous cell carcinoma, with primary completion expected in October 2027.

Global Vulvar Cancer Therapeutics Market Report Scope

As per the scope of the report, vulvar cancer therapeutics refers to the medical interventions, medications, and procedures used to treat malignancies that develop on the external female genitalia (the vulva). Primary options include surgery, radiation, chemotherapy, targeted therapies, and immunotherapy, which are tailored based on the cancer's stage, type, and the patient's overall health.

The vulvar cancer therapeutics market is segmented by treatment type, cancer type, end user, and geography. By treatment type, the market includes surgery, chemotherapy, radiation therapy, biologic therapy, targeted therapy, and immunotherapy. By cancer type, the market is segmented into vulvar squamous cell carcinoma, vulvar melanoma, adenocarcinoma, basal cell carcinoma, and other vulvar malignancies. By end user, the market is segmented into hospitals, specialty clinics, cancer research institutes, and others. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Surgery |

| Chemotherapy |

| Radiation Therapy |

| Biologic Therapy |

| Targeted Therapy |

| Immunotherapy |

| Vulvar Squamous Cell Carcinoma |

| Vulvar Melanoma |

| Adenocarcinoma |

| Basal Cell Carcinoma |

| Other Vulvar Malignancies |

| Hospitals |

| Specialty Clinics |

| Cancer Research Institutes |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Treatment Type | Surgery | |

| Chemotherapy | ||

| Radiation Therapy | ||

| Biologic Therapy | ||

| Targeted Therapy | ||

| Immunotherapy | ||

| By Cancer Type | Vulvar Squamous Cell Carcinoma | |

| Vulvar Melanoma | ||

| Adenocarcinoma | ||

| Basal Cell Carcinoma | ||

| Other Vulvar Malignancies | ||

| By End User | Hospitals | |

| Specialty Clinics | ||

| Cancer Research Institutes | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of vulvar cancer therapeutics by 2031?

The vulvar cancer therapeutics market is projected to reach USD 1.21 billion by 2031, up from USD 0.74 billion in 2026, at a CAGR of 10.30%.

Which treatment category is growing the fastest in vulvar cancer care?

Immunotherapy is the fastest-growing treatment type, with a forecast CAGR of 11.45% from 2026 to 2031, supported by stronger combination trial results.

Which cancer type drives the largest revenue base?

Vulvar squamous cell carcinoma is the leading cancer type segment and accounted for 37.45% of 2025 market value.

Why is North America ahead in revenue contribution?

North America leads because it combines higher diagnosed case volumes, stronger oncology infrastructure, and earlier use of biomarker-linked treatment pathways.

What is changing treatment practice in advanced vulvar cancer?

Practice is moving toward multimodal care that combines radiation, systemic therapy, and more selective surgery, with pembrolizumab-based combinations showing stronger Phase 2 outcomes.

Which end-user group is expanding the fastest?

Cancer research institutes are the fastest-growing end-user segment, with a 13.10% CAGR through 2031, because rare-cancer trials and early adoption are concentrated there.

Page last updated on: