Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

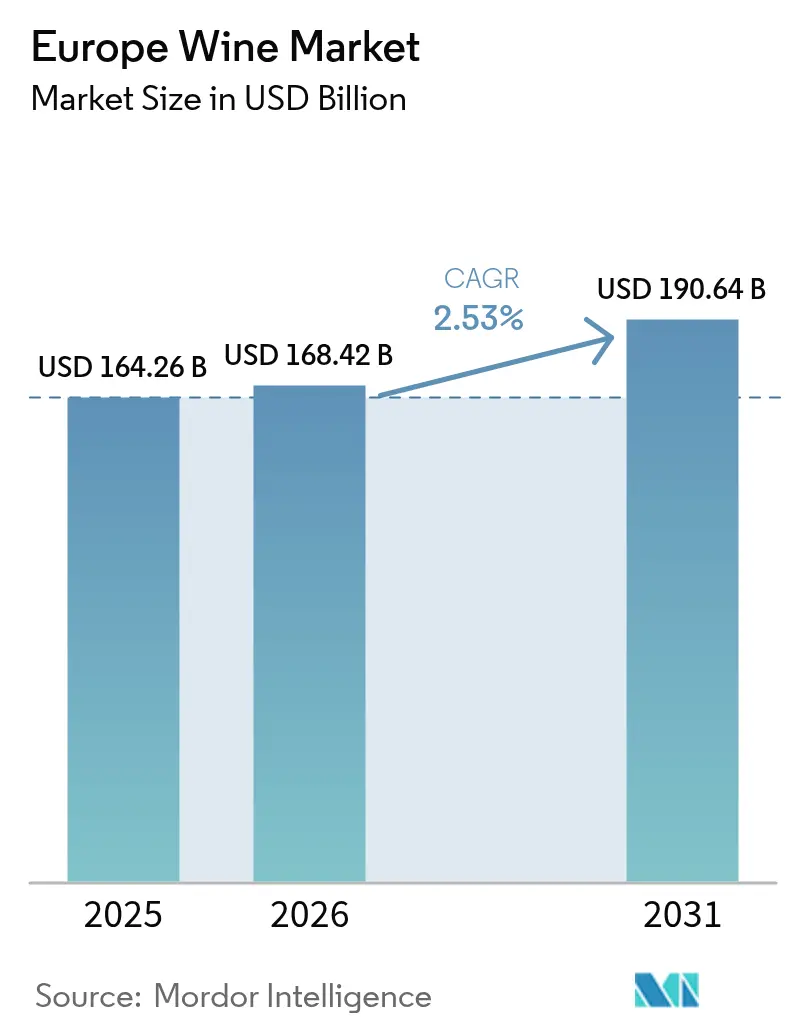

| Base Year Market Size (2025) | USD 164.26 Billion |

| Market Size (2026) | USD 168.42 Billion |

| Market Size (2031) | USD 190.64 Billion |

| Growth Rate (2026 - 2031) | 2.53% CAGR |

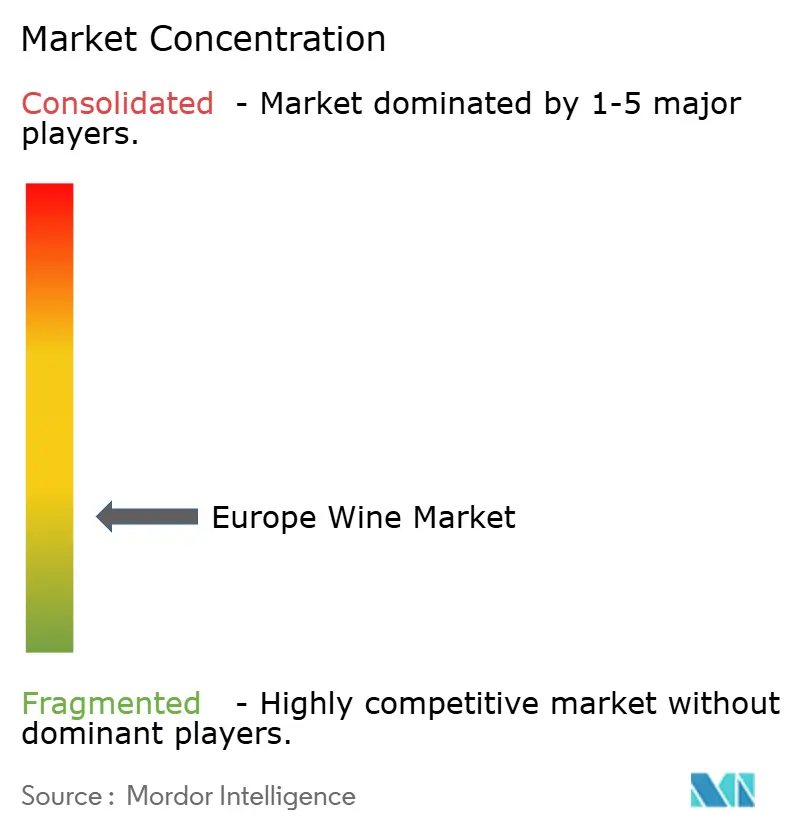

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Wine Market Analysis by Mordor Intelligence

Europe wine market size in 2026 is estimated at USD 168.42 billion, growing from 2025 value of USD 164.26 billion with 2031 projections showing USD 190.64 billion, growing at 2.53% CAGR over 2026-2031. The market demonstrates measured expansion as deeply rooted consumption patterns align with increasing consumer sophistication, particularly in their preference for premium wines and environmentally responsible production methods. The resurgence of the fine dining sector, renewed interest in wine tourism experiences, and the proliferation of digital direct-to-consumer sales platforms have generated substantial revenue diversification opportunities across the European wine industry. Wine producers are responding to stringent EU regulatory requirements and evolving consumer expectations by investing in organic certifications, developing eco-friendly packaging solutions, and implementing QR-code labeling systems to ensure complete supply chain transparency.

Key Report Takeaways

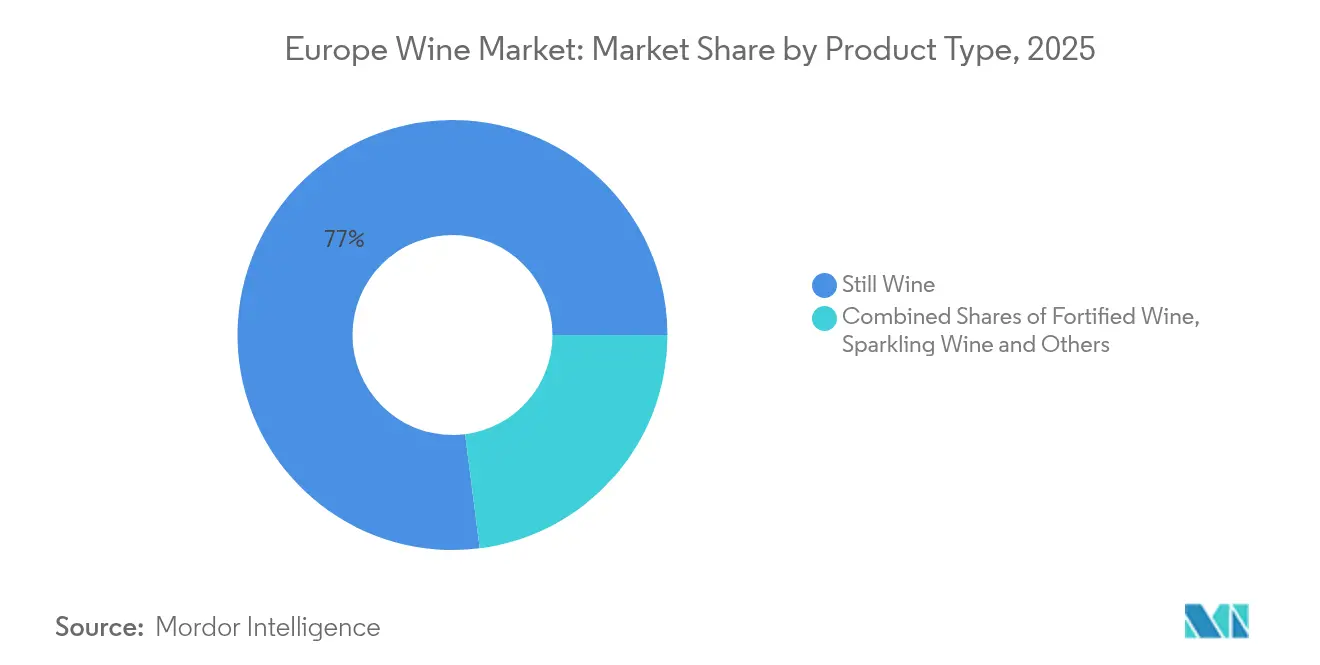

- By product type, Still Wine led with 77.02% of the Europe wine market share in 2025, while Sparkling Wine is projected to expand at a 3.71% CAGR through 2031.

- By color, Red Wine accounted for 45.94% of the Europe wine market size in 2025 and Rosé Wine is set to register the fastest 3.49% CAGR between 2026 and 2031.

- By end user, Women represented 59.68% consumption share in 2025, whereas male consumers will post a 3.55% CAGR through 2031.

- By distribution channel, Off-Trade held 61.98% of value in 2025, yet On-Trade is forecast to grow at 3.66% CAGR during 2026-2031 as wine tourism rebounds.

- By geography, France dominated with a 23.95% share in 2025, while the United Kingdom is set to grow the quickest at a 3.32% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Wine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumer preference for traditional, terroir-driven wines | +0.8% | France, Italy, Spain, Germany | Long term (≥ 4 years) |

| High quality and diverse wine varieties produced in Europe | +0.6% | Global, with concentration in EU core regions | Medium term (2-4 years) |

| Established wine tourism and wine-related experiences attracting consumers | +0.4% | France, Italy, Spain, Portugal | Medium term (2-4 years) |

| Growing popularity of low and non-alcoholic wines | +0.3% | Northern Europe, Germany, UK | Short term (≤ 2 years) |

| Innovation in wine production technologies and vineyard management | +0.2% | EU-wide, with focus on Mediterranean regions | Long term (≥ 4 years) |

| Rising interest in artisan and natural wines | +0.3% | Urban markets across EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Consumer Preference for Traditional, Terroir-Driven Wines

European consumers are showing a strong inclination towards authentic wines that embody the distinct characteristics of their geographic origins and honor traditional production methods, resulting in increased demand for Protected Designation of Origin (PDO) wines. The European Union's geographical indications regulation (EU) 2024/1143 provides enhanced protection measures for wine regions, with 1,085 European wine regions currently producing PDO-labeled wines [1]Source: European Union, “Regulation (EU) 2024/1143,” europa.eu. This comprehensive regulatory framework supports the development of premium wine production, as wines that express their unique terroir characteristics generate substantial profit margins and establish lasting consumer relationships through their rich regional heritage. Recent climate change vulnerability assessments have identified significant exposure risks in regions such as Romania, Croatia, and Italy, potentially increasing the market value of wines produced through traditional methods in these areas. This market development aligns with the evolving consumer behavior that emphasizes informed, quality-focused purchasing decisions, where consumers prioritize wine excellence and authenticity rather than volume consumption.

High Quality and Diverse Wine Varieties Produced in Europe

Europe maintains its dominant market position in fine wine production, representing a substantial majority of global fine wine output. This leadership stems from the region's established viticultural heritage, traditional winemaking expertise, and diverse microclimates that create ideal growing conditions. Italian wine producers project notable sales and export increases, with sparkling wines demonstrating particularly robust revenue performance compared to still wines. The market exhibits a clear divide between price segments, with premium wines experiencing substantial growth while mid-range wines face declining sales, indicating a significant consumer migration toward higher-quality offerings. Regional specialization continues to strengthen, highlighted by Prosecco's remarkable export performance and the impressive expansion of English sparkling wine sales over recent years.

Established Wine Tourism and Wine-Related Experiences Attracting Consumers

Wine tourism continues to drive substantial economic value, particularly exemplified by the French wine industry's contribution to employment and tax revenue through tourism activities. The evolution of wine tourism experiences through digital transformation has enabled wineries to implement innovative technologies, such as QR codes and virtual elements, enhancing visitor engagement while preserving the authentic human connections essential to wine experiences. Research demonstrates distinct preferences among wine tourists, with Italian and Turkish visitors both valuing expert-led tours but differing in their priorities - Italians appreciate winery aesthetics, while Turkish visitors emphasize the importance of pre-visit informational sessions. In the wake of the pandemic recovery, there has been a notable surge in demand for rural tourism experiences, creating opportunities for wine regions that showcase authentic, sustainable encounters with local terroir and cultural heritage.

Growing Popularity of Low and Non-Alcoholic Wines

The no-low alcohol (NOLO) wine market in France has achieved substantial market value, demonstrating robust growth in recent years. Market research shows that a majority of French consumers are actively reducing their alcohol consumption, reflecting a broader shift toward mindful drinking habits. The retail landscape has evolved significantly, with specialized NOLO stores expanding their footprint across France, enhancing product accessibility nationwide. This transformation is particularly noticeable among the younger generation, where a considerable portion of teenagers have chosen complete alcohol abstinence. European wine producers have strategically adapted to these changing consumer preferences by developing dealcoholized options in their portfolios, specifically catering to millennials and Gen Z consumers who seek to balance social engagement with health-conscious lifestyle choices.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory and labeling complexity across different EU member states | -0.4% | EU-wide, particularly affecting cross-border trade | Short term (≤ 2 years) |

| Changing consumer preferences towards beer, spirits, or other beverages | -0.6% | Northern Europe, urban markets | Medium term (2-4 years) |

| Rising cost and availability of agricultural inputs and labor shortages | -0.5% | Mediterranean regions, Eastern Europe | Short term (≤ 2 years) |

| Environmental concerns over water use and pesticide application | -0.3% | Southern Europe, drought-affected regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory and Labeling Complexity Across Different EU Member States

The European Union's comprehensive wine labeling regulations, which took effect on December 8, 2023, introduce mandatory requirements for detailed nutritional information and complete ingredient lists on wine products [2]Source: National Science Foundation, “Enhancing Transparency in the EU Wine Industry,” nsf.org. These requirements present significant compliance challenges for wine producers, particularly due to the diverse language requirements across different member states. Although digital solutions and QR codes offer producers a practical and cost-effective path to compliance, the task of managing multiple regulatory frameworks within EU markets increases operational expenses and establishes substantial market entry barriers, especially impacting small and medium-sized producers. This regulation represents the most substantial modification to wine labeling requirements in more than a century, compelling manufacturers to find an effective balance between maintaining transparent consumer communication and managing their compliance-related expenses. The inconsistent interpretation and enforcement standards among various member states have introduced complications in cross-border trade operations, potentially undermining the unified market advantages that European wine producers have historically benefited from.

Changing Consumer Preferences Towards Beer, Spirits, or Other Beverages

European wine consumption shows a significant downward trajectory compared to previous years, primarily driven by changing preferences among younger consumers who are increasingly gravitating toward alternative alcoholic beverages and non-alcoholic options. The German wine market is experiencing unprecedented challenges, with domestic market share reaching its lowest point as consumers demonstrate a clear preference for affordable imported wines and alternative beverage choices. This shift in consumption patterns extends globally, reflecting fundamental changes in drinking habits influenced by growing health awareness, financial considerations, and evolving lifestyle preferences. The transformation is particularly noticeable in urban markets, where craft beer, premium spirits, and innovative non-alcoholic beverages are actively competing with traditional wine consumption. In response, wine producers are strategically adjusting their product portfolios and marketing approaches to maintain market relevance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Sparkling Wines Drive Premium Growth

Still Wine maintains its commanding position in the market with a 77.02% share in 2025, demonstrating its fundamental importance in European wine consumption and cultural traditions. The category's dominance reflects consumer preferences for traditional wine experiences and its integration into daily dining and social occasions across European households.

Sparkling Wine demonstrates robust market performance with a projected CAGR of 3.71% through 2031, driven by increasing consumer preference for celebratory beverages and growing demand for premium products. Prosecco's remarkable performance, exceeding 1 billion bottles in exports during 2024, highlights its successful penetration into Asian markets and resonance with younger consumer demographics. While Champagne experiences market challenges with a 9% sales reduction in 2024, influenced by economic factors and increased competition from alternative sparkling wines, Crémant shows notable market strength with sales reaching 108 million bottles in 2024.

By Color: Rosé Wines Capture Millennial Preferences

Red wine dominates the European wine market with a 45.94% share in 2025, reflecting its strong cultural significance, particularly in Mediterranean countries. The wine's deep connection to regional gastronomy and traditional dining practices continues to drive consumer preferences, especially in established markets like France, Italy, and Spain, where red wine remains a fundamental element of daily meals and social gatherings.

Rosé wine demonstrates remarkable market dynamics, achieving the highest growth rate at 3.49% CAGR through 2031, despite its smaller volume share. This growth trajectory stems from increasing acceptance among younger consumers who value its adaptability across dining occasions and social settings. White wine maintains its market position between these two categories, benefiting from evolving climate conditions that have enhanced grape quality in regions traditionally known for red wine production, leading to improved white wine offerings across European vineyards.

By End User: Male Consumption Patterns Evolving Rapidly

Women account for 59.68% of wine consumption in 2025, demonstrating their significant influence in household purchasing decisions. Their preference for wine in social gatherings and entertainment venues has established them as the dominant consumer demographic in the global wine market.

Men have emerged as the fastest-growing consumer segment, exhibiting a 3.55% CAGR through 2031. This growth stems from increasing male participation in wine education programs, growing interest in wine and food pairing experiences, and rising demand for premium wine offerings. The wine industry has successfully broadened its consumer base by implementing targeted marketing strategies, positioning wine within the craft beverage category, and highlighting the technical aspects of viticulture and winemaking processes.

By Distribution Channel: On-Trade Recovery Accelerates

Off-Trade channels maintain a dominant position with a 61.98% market share in 2025, operating through an extensive network of specialty liquor stores, supermarkets, and online platforms. These channels have successfully captured consumer preferences by offering convenient shopping experiences and competitive pricing structures, enabling customers to purchase their preferred wines at their own pace and compare options effectively.

On-Trade channels demonstrate robust growth potential with a projected 3.66% CAGR through 2031, fueled by the resurgence of wine tourism activities and substantial expansion in the restaurant industry. The post-pandemic consumer behavior shows a marked shift toward experiential consumption, with On-Trade establishments becoming key venues for premium wine offerings. These venues create immersive environments for wine discovery and education, establishing deeper connections between consumers and brands, which naturally translates into stronger brand loyalty and consistent repeat purchases.

Geography Analysis

The European wine market continues to be dominated by France, which holds a substantial 23.95% market share in 2025. As the region's largest wine economy, France has successfully maintained its leadership position despite facing significant production challenges that resulted in a 22% reduction in output to 37.4 million hectoliters. The country's wine exports remain robust at EUR 12.1 billion in 2024, with a strategic focus on premium segments where traditional terroir authenticity and prestigious AOC designations enable higher profit margins . The French wine industry's strength is further reinforced by its well-developed wine tourism infrastructure and deep-rooted cultural positioning, which effectively supports premiumization strategies even in the face of volume pressures stemming from climate challenges and evolving consumption patterns.

In the evolving European wine landscape, the United Kingdom has established itself as the market's most dynamic performer, projecting a steady growth rate of 3.32% CAGR through 2031. This remarkable growth trajectory is underpinned by increasingly sophisticated consumer preferences and strong premiumization trends. The country's domestic wine industry has shown particular promise in the sparkling wine category, where production achievements have led to a threefold increase in sales over a five-year period, demonstrating the market's significant potential and growing consumer acceptance.Other major European wine producers have demonstrated notable resilience in their production capabilities. Italy has achieved significant market success with a turnover of EUR 14 billion and production volumes reaching 44.07 million hectoliters, representing a 7% increase compared to 2024. Similarly, Spain has shown strong production performance, recording 38.1 million hectoliters, marking an impressive 18% increase from 2024 levels. These figures underscore the robust nature of the European wine industry's production capacity and its ability to adapt to changing market conditions.

Competitive Landscape

The European wine market's fragmented competitive landscape presents significant opportunities for both market consolidation and specialized niche positioning strategies. The industry underwent substantial restructuring throughout 2024-2025, marked by notable corporate transactions. In May 2025, Pernod Ricard executed a strategic divestiture of its wine assets to Australian Wine Holdco Limited, resulting in the formation of Vinarchy. This new entity emerged as a significant market player, generating over 32 million cases in annual production and achieving AUD2 billion in retail sales. In a parallel development during April 2025, Constellation Brands implemented a strategic portfolio transformation, focusing on premium wines priced above USD 15. This involved divesting mainstream brands to The Wine Group while maintaining ownership of high-margin assets, including Robert Mondavi Winery and Kim Crawford. These strategic decisions reflect broader industry shifts toward premiumization and address the fundamental challenge of sustaining growth in markets experiencing volume declines.

The integration of technology has emerged as a crucial factor in determining competitive advantage within the wine industry. Smart farming technologies have demonstrated substantial environmental benefits, achieving a remarkable 75% reduction in pesticide usage and a significant 33.4% decrease in greenhouse gas emissions. The convergence of sustainability initiatives and digital transformation has created valuable opportunities, particularly for smaller wine producers. These businesses can now effectively compete with larger established companies by implementing precision agriculture techniques and utilizing direct-to-consumer digital platforms. The market's fragmented structure continues to benefit regional wine specialists, who maintain their competitive positions through authentic terroir offerings and immersive marketing experiences, while larger industry players concentrate on optimizing their portfolios and expanding their international presence.

The regulatory environment, particularly EU labeling requirements, has established significant barriers for new market entrants. This regulatory framework potentially favors established wine producers who possess the necessary resources and expertise to navigate complex compliance requirements across multiple markets. These requirements have contributed to a gradual consolidation of market share among well-established companies that can effectively manage and adapt to evolving regulatory standards while maintaining operational efficiency.

Europe Wine Industry Leaders

E. & J. Gallo Winery

Constellation Brands

Castel Group

Pernod Ricard SA

Treasury Wine Estates

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: FC Barcelona and Raventós Codorníu have signed a five-season sponsorship agreement that runs until June 30, 2029. Under this agreement, Raventós Codorníu becomes the Official Wine and Cava Partner of Espai Barça, providing premium beverages in the VIP areas of the new Spotify Camp Nou stadium.

- June 2024: Accolade Wines has launched its premium European wine brand, Remastered, into travel retail, featuring Italian varietals Sangiovese and Fiano in modern, eye-catching packaging designed to attract younger consumers.

- May 2024: ALPLA has developed a lightweight, recyclable PET wine bottle that reduces carbon emissions by up to 50% compared to traditional glass bottles, while also lowering costs by up to 30%. The bottle, weighing just 50 grams, is already being used in Austria and supports a Europe-wide bottle-to-bottle recycling loop, with plans to manufacture several million units annually from 2025 using recycled PET (rPET).

Europe Wine Market Report Scope

Wine is a kind of alcoholic beverage prepared by fermenting grapes, where yeast is used in the fermentation process. The different varieties of grapes and various strains of yeasts used in the process give out numerous styles of wine. The Europe wine market is segmented by product type, color, distribution channel, and geography. Based on the product type, the market is segmented into still wine, sparkling wine, and other product types. By color, the market is segmented into red wine, rose wine, white wine, and other wines. Based on the distribution channel, the market is classified as on-trade and off-trade channels. The off-trade channel is further classified into supermarkets/hypermarkets, specialty stores, online retail stores, and other distribution channels. The regional market is also segmented by geography into Spain, the United Kingdom, France, Germany, Italy, and the Rest of Europe. For each segment, the market sizing and forecasts have been done on the basis of value (in USD billion).

By Product Type

| Fortified Wine |

| Still Wine |

| Sparkling Wine |

| Others |

By Color

| Red Wine |

| White Wine |

| Rosé Wine |

By End User

| Men |

| Women |

By Distribution Channel

| On-Trade | |

| Off-Trade | Specialty/Liquor Stores |

| Others Off Trade Channels |

By Country

| Germany |

| United Kingdom |

| Italy |

| France |

| Spain |

| Netherlands |

| Poland |

| Belgium |

| Sweden |

| Rest of Europe |

| By Product Type | Fortified Wine | |

| Still Wine | ||

| Sparkling Wine | ||

| Others | ||

| By Color | Red Wine | |

| White Wine | ||

| Rosé Wine | ||

| By End User | Men | |

| Women | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Specialty/Liquor Stores | |

| Others Off Trade Channels | ||

| By Country | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the current value of the Europe wine market?

It is valued at USD 168.42 billion in 2026 and is projected to reach USD 190.64 billion by 2031.

Which product category is showing the fastest growth across Europe?

Sparkling Wine, supported by booming Prosecco exports, is forecast to record a 3.71% CAGR from 2026 to 2031.

Which geography holds the largest share in European wine sales?

France leads with 23.95% of regional revenue thanks to its AOC portfolio and strong export base.

What channel is expected to outpace the rest for wine sales?

On-Trade outlets such as restaurants and wine bars are projected to grow at a 3.66% CAGR on the back of tourism recovery.

Page last updated on: