Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 352.34 Billion |

| Market Size (2026) | USD 360.3 Billion |

| Market Size (2031) | USD 402.93 Billion |

| Growth Rate (2026 - 2031) | 2.26% CAGR |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

US Wine Market Analysis by Mordor Intelligence

US wine market size in 2026 is estimated at USD 360.3 billion, growing from 2025 value of USD 352.34 billion with 2031 projections showing USD 402.93 billion, growing at 2.26% CAGR over 2026-2031. Driven by changing consumer preferences and a pronounced tilt towards premiumization, the U.S. wine market is on an upward trajectory. Younger consumers are increasingly favoring higher-quality wines, often opting for boutique or vineyard-specific labels that promise distinct character and authenticity. Innovations such as canned formats and resealable bottles are making sparkling and rosé wines more accessible, elevating their appeal beyond just celebratory moments. In response to this burgeoning demand, leading producers like E. & J. Gallo and The Duckhorn Portfolio are broadening their premium offerings. While still wines continue to anchor the market, sparkling variants are swiftly gaining traction. Rosé, celebrated for its versatile flavor, is becoming a top choice for trend-savvy drinkers. The market's momentum is further highlighted by gender and retail trends: female consumers currently dominate wine purchases, yet male consumption is on the rise. Distribution is largely led by off-trade channels, such as grocery and specialty stores, but there's a notable resurgence in on-trade venues like restaurants and wine bars, emphasizing the experiential nature of modern wine drinking.

Key Report Takeaways

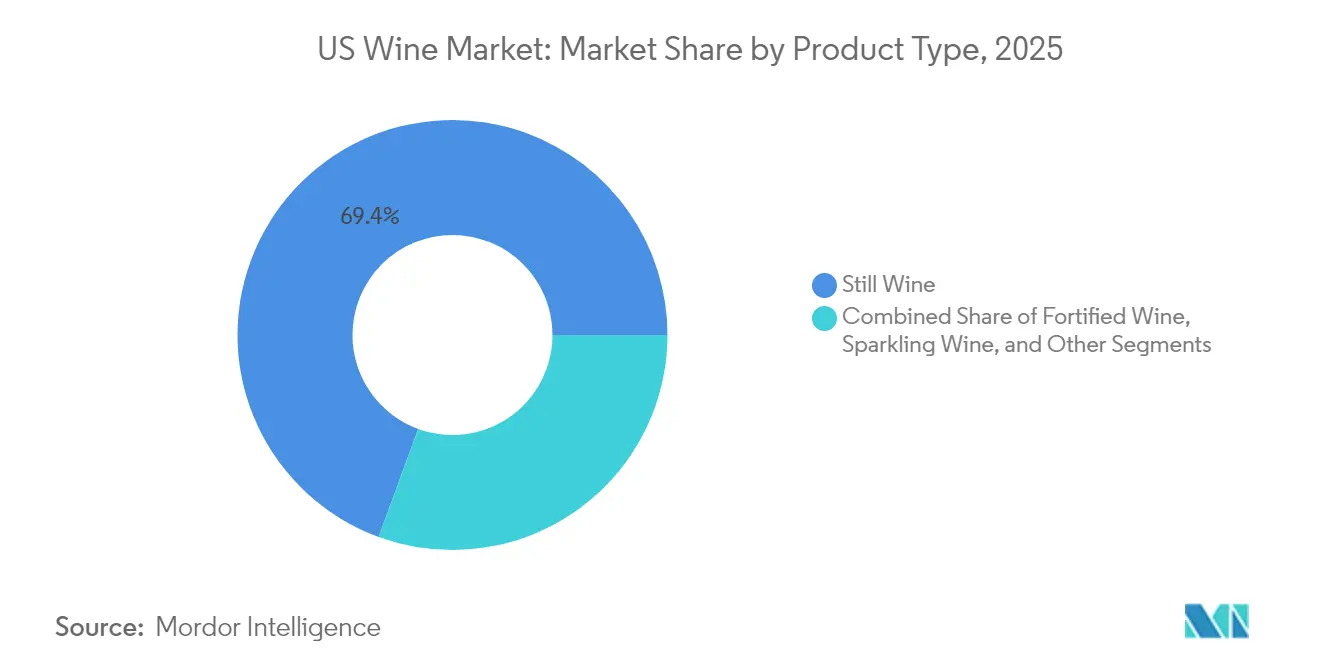

- By product type, still wine led with 69.42% of the US wine market share in 2025; sparkling wine is projected to grow at a 2.69% CAGR to 2031.

- By color, red wine held 44.32% revenue share in 2025, while rosé is forecast to expand at a 2.88% CAGR through 2031.

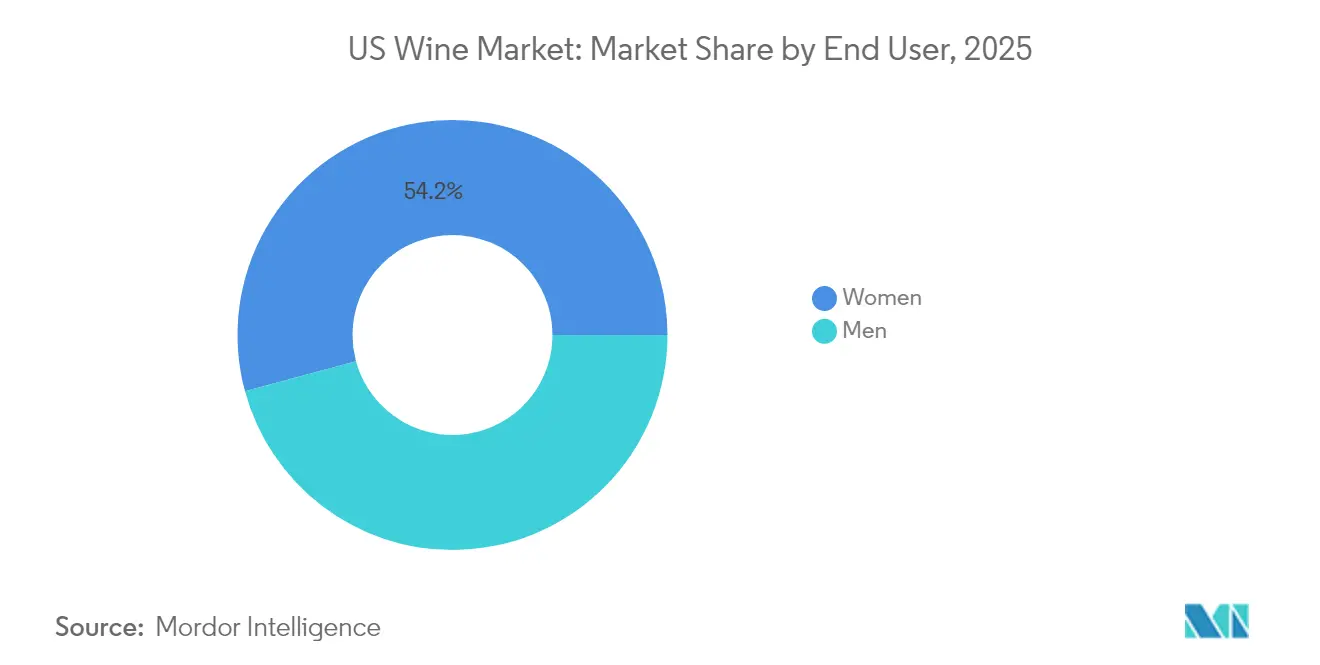

- By end user, women accounted for 54.21% of the US wine market size in 2025; men are expected to record the highest CAGR of 3.14% during 2026-2031.

- By distribution channel, the off-trade segment captured 56.87% share of the US wine market size in 2025; the on-trade channel is advancing at a 2.41% CAGR through 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

US Wine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing tourism and hospitality impact positive growth | +0.4% | National, with concentration in California, Washington, Oregon, and New York | Medium term (2-4 years) |

| Rising consumer preference for low alcohol products | +0.5% | National, with higher impact in urban centers | Long term (≥ 4 years) |

| Surge in demand for premium and super premium wine | +0.7% | National, with concentration in high-income urban areas | Medium term (2-4 years) |

| Product diffrentiation in terms of raw material | +0.3% | National, with higher impact in urban centers | Medium term (2-4 years) |

| Innovative packaging formats attract new consumer segments. | +0.2% | National, with higher impact among younger consumers | Short term (≤ 2 years) |

| Wine subscription services create steady demand. | +0.3% | National, with concentration in tech-savvy demographics | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing tourism and hospitality impact positive growth

As the hospitality sector rebounds, the U.S. wine market is witnessing a vigorous upswing, largely driven by the pivotal roles of restaurants and bars. Today's on-premise wine programs have undergone a significant transformation, now prioritizing curated selections that highlight distinctive varietals and boutique domestic producers. Notable mentions include Napa Valley's Silver Oak and vineyards from Oregon's Willamette Valley. This evolution presents premium wineries with a golden chance to engage a more discerning clientele that values quality over mere quantity. As consumers increasingly link wine consumption in upscale dining to notions of indulgence and cultural significance, premium wines are witnessing a surge in popularity, with patrons justifying their elevated price points. Concurrently, wine tourism in regions such as Sonoma, Paso Robles, and the Finger Lakes is experiencing a renaissance. Wineries are expanding their offerings beyond the conventional tastings, introducing immersive experiences. These range from chef-led food pairings and vineyard hikes to blending workshops and sustainability tours. Such enhancements resonate with the U.S. populace's rising appetite for authentic, experiential, and eco-conscious travel. By investing in these initiatives, wineries are not only drawing in affluent visitors but also bolstering brand loyalty and ensuring their foothold in an experience-centric market.

Rising consumer preference for low alcohol products

As health and wellness take center stage in consumer preferences, the U.S. wine market is witnessing a significant surge in demand for low- and no-alcohol wine options. This trend resonates strongly with younger demographics, especially Gen Z, who are pursuing moderation without sacrificing flavor or social experiences. In response, wineries are crafting a new wave of low-alcohol wines that rival the complexity and quality of their traditional counterparts. Notably, producers like Giesen and Fre Wines have rolled out alcohol-removed wines, maintaining varietal character to cater to health-conscious consumers. These innovations are making waves in both retail and on-premise channels, with sommeliers and beverage directors integrating low-alcohol options into their curated wine lists. Moreover, transparent labeling practices and wellness-centric branding bolster consumer trust and informed choices. The Alcohol and Tobacco Tax and Trade Bureau's (TTB) push for nutritional labeling is further propelling this shift, offering consumers clear insights into caloric and alcohol content for more informed purchases [1]Source: The Alcohol and Tobacco Tax and Trade Bureau (TTB), "Notice No. 237: Alcohol Facts Statements in the Labeling of Wines, Distilled Spirits, and Malt Beverages,"regulations.gov. Consequently, a premium segment of mindful wine options is emerging, aligning with modern lifestyles. Wineries that adeptly blend craftsmanship with health-forward innovations, such as organic, lower-calorie, or low-ABV selections, are poised to captivate today's discerning consumers, who seek both elevated and responsible drinking experiences.

Surge in demand for premium and super premium wine

The U.S. wine market's premium and super-premium segments continue to demonstrate resilience, even as overall market volumes decline. According to the Bank of Montreal Wine Market Report, wines priced between USD 20-50 recorded a notable 12% increase in sales in 2024. This growth reflects a significant shift in consumer preferences, with a stronger focus on quality over quantity across various demographic groups. The Silicon Valley Bank report further supports this trend, highlighting robust performance for wineries offering wines in the USD 30-80 price range, while lower-priced segments face ongoing volume challenges[2]Source: Silicon Valley Bank (SVB), "Constellation Brands and Premiumization: Holding A Mirror to the Wine Industry,"svb.com. In response to these shifting market dynamics, leading companies like Constellation Brands are strategically enhancing their luxury wine portfolios. Through acquisitions of premium producers such as Sea Smoke and Domaine Curry, they aim to capitalize on the growing demand for high-quality wines. The premium segment's sustained growth is fueled by increasing consumer interest in wines that emphasize distinctive terroir characteristics, environmentally sustainable production methods, and compelling brand stories. These attributes not only justify premium pricing but also strengthen customer loyalty, positioning the premium and super-premium segments as pivotal growth drivers in the evolving U.S. wine market landscape.

Product diffrentiation in terms of raw material

Innovation in grape selection, sustainable practices, and region-specific production is driving product differentiation in the U.S. wine market. Producers are branching out from traditional varietals like Cabernet Sauvignon and Chardonnay, experimenting with lesser-known grapes such as Albariño, Tempranillo, and Tannat. These grapes not only offer distinctive flavor profiles but also adapt better to changing climate conditions. This trend is notably pronounced in regions like Texas Hill Country and New York’s Finger Lakes, where the local terroir is crafting unique wine identities. Sustainability has emerged as a key pillar of premium positioning. Wineries such as Bonterra and Benziger Family Winery are at the forefront, championing organic and biodynamic farming methods. These sustainable practices cater to the rising demand for eco-friendly products and bolster vineyard resilience and wine complexity. Additionally, a supportive regulatory framework fosters controlled innovation, enabling producers to uphold quality standards while exploring creative avenues. Collectively, these dynamics are transforming the U.S. wine landscape, equipping producers to align with shifting consumer preferences and environmental imperatives, all while retaining a competitive edge in a mature and diverse market.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent government regulations | -0.5% | National, with varying impact by state | Long term (≥ 4 years) |

| Rising consumer inclination towards other alcoholic beverages | -0.7% | National, with higher impact among younger demographics | Medium term (2-4 years) |

| Supply chain disruptions and increased transportation costs | -0.3% | National, with higher impact in import-dependent regions | Short term (≤ 2 years) |

| Labor shortages in vineyards and production | -0.4% | California, Washington, Oregon, New York | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent government regulations

The U.S. wine industry operates within a complex regulatory framework that significantly influences market growth and innovation potential. The post-prohibition three-tier distribution system creates market access barriers, with smaller producers particularly struggling to establish distribution channels through major wholesalers. The regulatory landscape continues to expand with the TTB's introduction of mandatory allergen labeling requirements, which include a five-year implementation timeline. Further regulatory changes loom as the Consumer Federation of America advocates for comprehensive labeling requirements, encompassing nutritional information and enhanced health warnings, changes that would increase production costs and potentially reshape consumer perceptions. The regulatory complexity intensifies at the state level, where 18 states maintain direct control over alcohol sales, while other states implement varying licensing systems[3]Source: Zara Law Office, "Your Winery’s Passport to the American Market,"zaralawny.com. This regulatory environment creates an uneven playing field, particularly impacting small and medium-sized wineries that constitute the majority of the industry. These smaller operations, unlike their larger counterparts with established compliance teams, often lack the necessary resources to efficiently navigate the extensive regulatory requirements.

Rising consumer inclination towards other alcoholic beverages

The US wine market is facing increasing competition as alternative alcoholic beverages, particularly ready-to-drink (RTD) cocktails and craft spirits, continue to gain traction, especially among younger consumers. This trend is most evident among Gen Z and younger Millennials, who exhibit a preference for variety and frequently switch between alcohol categories depending on social settings and personal preferences. Traditionally, wine has been associated with formal dining and food pairings, but this conventional image struggles to connect with younger audiences who prioritize casual, social drinking experiences and a diverse range of flavors. Additionally, the perceived complexity of wine, including its varietals, tasting notes, and pairing rules, often intimidates new consumers, making it less accessible compared to the convenience and simplicity of RTDs and flavored malt beverages.This evolving consumption behavior underscores the urgent need for wine producers to adapt their strategies, such as simplifying product offerings, enhancing marketing efforts, and embracing innovation, to align with the changing preferences of modern consumers and maintain their competitive edge in a dynamic market landscape.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Still Wine Dominates Amid Shifting Preferences

In 2025, still wine dominates the U.S. wine market, holding a commanding 69.42% share. Classic varietals like Cabernet Sauvignon, Pinot Noir, and Chardonnay bolster its leadership. The segment is witnessing a premiumization trend, as demand from consumers gravitates towards refined, terroir-driven expressions. Producers such as Duckhorn and Stag’s Leap Wine Cellars are seizing this opportunity, offering high-quality selections that resonate with consumer desires for authenticity and craftsmanship. Furthermore, innovations in sustainable viticulture and the rise of direct-to-consumer models are fortifying the position of premium still wines, appealing to consumers who value quality, origin, and environmental responsibility.

Sparkling wine is emerging as the fastest-growing segment in the U.S. wine market, with projections indicating a 2.69% CAGR from 2026 to 2031. This surge is attributed to the category's evolving role in casual settings, transcending its traditional association with celebrations. Sparkling wines, especially Prosecco, Cava, and domestic sparkling rosé, have gained traction among younger consumers due to their lighter profiles, lower alcohol content, and enhanced drinkability. Brands like La Marca and Chandon are spearheading this growth, leveraging innovative formats like mini bottles and cans, alongside lifestyle-centric marketing that strikes a chord on social media.

By Color: Red Wine Challenged by White's Resurgence

In 2025, red wine commands a significant 44.32% share of the U.S. wine market, solidifying its status as a core category. Its enduring appeal stems from its rich flavor profile, versatility in food pairings, and a loyal consumer base. Varietals like Cabernet Sauvignon, Pinot Noir, and Merlot bolster its prominence, remaining favorites in both retail and dining establishments. As consumer preferences shift, producers are innovating, introducing styles with softer tannins, reduced alcohol content, and vibrant fruit profiles. Wineries such as Meiomi and Josh Cellars are leading this charge, presenting approachable red blends that resonate with both novices and connoisseurs. Furthermore, red wine's association with health benefits, particularly its links to heart health when consumed in moderation, underscores its continued relevance among health-conscious consumers.

Rose wine emerges as the U.S. wine market's fastest-growing segment, eyeing a CAGR of 2.88% from 2026 to 2031. Its ascent is fueled by its all-year-round allure, eye-catching presentation, and versatility across diverse occasions. Once relegated to seasonal status, rosé has cemented its place as a lifestyle choice, gracing everything from brunch tables to outdoor soirées. Its refreshing taste and moderate alcohol content appeal to younger, multicultural audiences who lean towards simpler, more sociable wine experiences. Brands like Whispering Angel and La Fête du Rosé have harnessed this trend, leveraging inclusive branding and robust social media strategies. The rosé category adeptly straddles the line between entry-level and premium markets, with top-tier producers from Provence and Napa broadening their rosé offerings to cater to surging demand. This adaptability and cultural significance position rosé as a pivotal growth driver in the dynamic U.S. wine scene.

By End User: Women Lead While Men Show Stronger Growth

In 2025, women assert their dominance in the global wine market, commanding a 54.21% share of the consumer base. Their influence transcends mere consumption volume, actively shaping trends across varietals, regions, and price tiers. With a keen interest in exploring new wine styles and origins, women are driving growth in both the premium and super-premium segments. Brands such as Kim Crawford and Cakebread Cellars have adeptly connected with this demographic, leveraging storytelling, lifestyle branding, and immersive experiences like vineyard events and sommelier-led tastings. These traits resonate with experience-driven marketing strategies. In response, wineries are curating offerings that emphasize emotional connection, exclusivity, and transparent sourcing, all aimed at bolstering brand loyalty.

On the other hand, the male segment of wine consumers is on the rise, with a forecasted CAGR of 3.14% from 2026 to 2031. This uptick is fueled by shifting perceptions of wine, bolstered by marketing that underscores craftsmanship, bold flavors, and food pairings, elements that resonate with male drinkers. Brands such as 19 Crimes and Orin Swift are making waves with their unique packaging, heritage-centric storytelling, and tailored digital content. Furthermore, producers are tapping into gender-neutral and male-centric formats, introducing premium canned wines and exclusive limited-edition releases. Initiatives like curated tasting experiences, direct-to-consumer subscriptions, and social events are bridging traditional gender divides, positioning wine as a formidable competitor to beer and spirits.

By Distribution Channel: Off-Trade Dominates as On-Trade Recovers

In 2025, off-trade channels dominate the U.S. wine market, accounting for 56.87% of total sales. This trend, bolstered during the pandemic by a rise in at-home consumption, persists as consumers lean towards convenience, value, and accessibility. The growth of e-commerce platforms and direct-to-consumer (DTC) wine subscriptions has amplified this off-trade momentum, allowing wineries to forge direct connections with their clientele. Within this realm, specialty liquor stores hold a pivotal position, trailing only grocery chains. These stores set themselves apart by providing curated selections, expert sommelier guidance, and exclusive labels from esteemed producers like Orin Swift and Daou

Conversely, on-trade channels encompassing bars, restaurants, and hotels command a smaller market share but are poised for growth, projected at a 2.41% CAGR from 2026 to 2031. This uptick is largely attributed to the resurgence of the hospitality sector, with patrons increasingly desiring immersive wine experiences. To cater to this demand, establishments are refining their wine offerings, spotlighting boutique producers, low-intervention wines, and lesser-known varietals. For instance, many restaurants now present wines from up-and-coming regions like Paso Robles and Finger Lakes, expertly paired with dishes that accentuate the wine's unique character.

Geography Analysis

Distinct consumption trends, production strengths, and regulatory environments shape the substantial regional diversity of the U.S. wine market. According to the U.S. Department of the Treasury, the United States is a major wine producer, with California accounting for the vast majority of production. Dominating the premium wine space, Napa Valley wines bolster California's global reputation for quality. While the state grapples with structural oversupply and adapts to evolving climate regulations, like the California Climate Corporate Data Accountability Act, it remains a benchmark for innovation, sustainability, and luxury positioning.

Washington and Oregon have solidified their status as pivotal centers for premium and ultra-premium wines. As the second-largest wine-producing state, Washington boasts robust high-end offerings, showcasing resilience amid broader market shifts. Meanwhile, Oregon's global acclaim for Pinot Noir and commitment to environmentally responsible practices further cements its boutique identity. On the East Coast, regions such as New York’s Finger Lakes and Virginia are emerging as vibrant contributors to the national wine narrative, celebrated for their terroir-driven styles and increasing critical acclaim.

While these emerging regions hold promise, they grapple with structural challenges, notably the three-tier distribution system that can hinder direct market access for smaller or newer wineries. Yet, this landscape also offers opportunities for up-and-coming producers, direct-to-consumer innovators, and niche investors. With consumers increasingly valuing regional authenticity and immersive brand experiences, wineries can thrive by establishing community-driven tasting rooms, harnessing digital platforms, and prioritizing quality over volume. Recent court rulings on interstate shipping hint at a more open regulatory environment, presenting a strategic entry point for the next generation of regional wine leaders.

Competitive Landscape

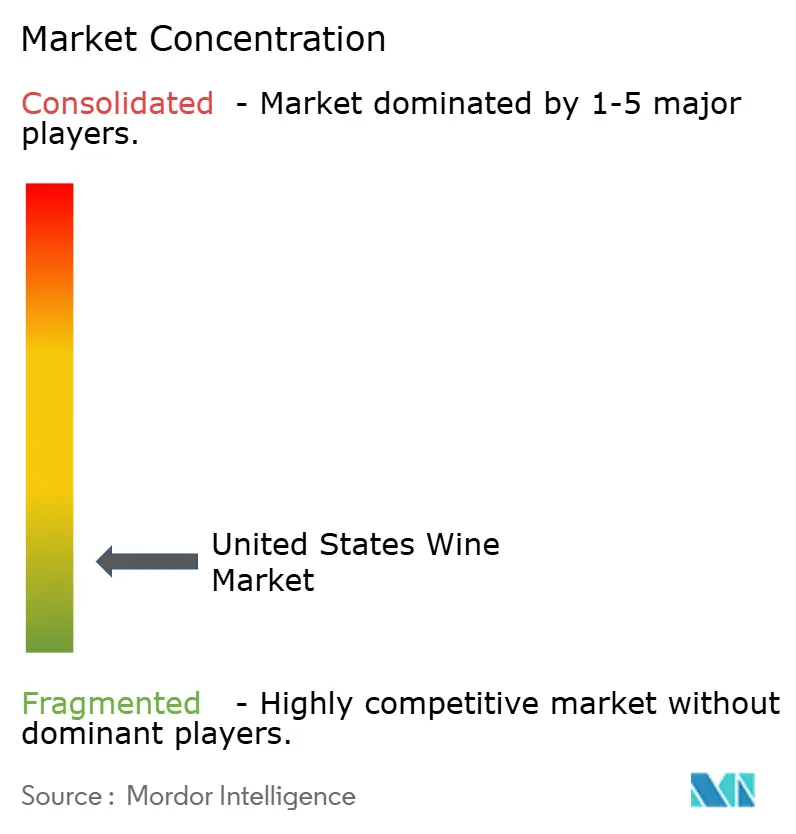

The U.S. wine market is highly fragmented. The Wine Group, Constellation Brands, E. & J. Gallo Winery, Jackson Family Wines, and Trinchero Family Estates dominate in volume sales. However, the market's richness and innovation largely stem from over 11,000 small and mid-sized wineries. Many of these smaller entities cater to regional preferences and niche audiences. This fragmentation fosters a lively ecosystem of product differentiation, especially in premium, organic, biodynamic, and locally produced wine categories. As consumers increasingly seek authentic, artisanal, and sustainable wines, these smaller producers have cultivated dedicated followings, even with their limited distribution.

Producers are now prioritizing value over volume, marking premiumization as a key industry trend. Constellation Brands underscores this shift, having divested from lower-priced wines to hone in on luxury labels like Sea Smoke and Domaine Curry. Similarly, GALLO has strategically acquired upscale wineries such as Rombauer and Massican, signaling its commitment to high-end offerings. These strategic maneuvers resonate with a broader consumer appetite for quality, provenance, and exclusivity.

There's a burgeoning opportunity to engage younger, digitally-savvy consumers. By weaving sustainability narratives, introducing innovative formats like canned and single-serve wines, and leveraging digital platforms that champion personalization and transparency, the market can capture this demographic. While tech-driven disruptors and direct-to-consumer (DTC) brands challenge traditional sales paradigms, they grapple with scaling issues, hindered by intricate regulatory frameworks and the stronghold of established players. Yet, their pioneering approaches are steadily transforming the U.S. wine landscape, reshaping discovery, purchasing, and overall experience.

US Wine Industry Leaders

-

The Wine Group

-

Constellation Brands, Inc.

-

E. & J. Gallo Winery

-

Jackson Family Wines Inc.

-

Trinchero Family Estates

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Cakebread Cellars, one of Napa Valley's premier family-owned wineries, launched brand, Bezel. Bezel offers vibrant, fruit-forward wines that blend more than 50 years of the Cakebread family's winemaking expertise with the Central Coast region's unique terroirs, according to the brand. The new brand's portfolio includes Cabernet Sauvignon, Chardonnay, Pinot Noir and Sauvignon Blanc.

- September 2024: Albertsons launched its own private label alcohol line called Bee Lightly as the newest addition to its Own Brands wine portfolio. According to the brand, the new line is notable for its flat bottle package design made from 100% recycled polyethylene terephthalate (PET).

- September 2024: Valdo, the renowned Prosecco producer from Valdobbiadene, launched Aquarius Blanc de Blancs in the U.S. market, a sparkling wine crafted from Garganega and Glera grapes and distinguished by its delicate floral and tropical fruit notes. The bottle features a unique, tactile design created in collaboration with Ceci Johnson of Ceci New York, using hand-painted artistry and organic pigments for a striking, textured finish.

- April 2024: Bonny Doon Vineyard launched its new wine in Frugalpac’s Frugal Bottle a sustainable bottle made from 94% recycled paperboard with a carbon footprint six times lower than glass, available at Whole Foods Market. According to the brand, the bottles are assembled and filled at Monterey Wine Company in California, which has installed the country’s first Frugal Bottle Assembly Machine, enabling local production.

US Wine Market Report Scope

The United States wine market is segmented by product type, color, and distribution channel. By product type, the market is segmented into still wine, sparkling wine, and other product types. By color, the market is segmented into red wine, rose wine, white wine, and other colors. Based on the distribution channel, the market is classified as on-trade and off-trade channels. The off-trade channel is further classified into supermarkets/hypermarkets, specialty stores, online retail channels, and other distribution channels. For each segment, the market sizing and forecasts have been done based on value (in USD million).

By Product Type

| Fortified Wine |

| Still Wine |

| Sparkling Wine |

| Others Wine Types |

By Color

| Red Wine |

| White Wine |

| Rose Wine |

By End User

| Men |

| Women |

By Distribution Channel

| On-Trade | |

| Off-Trade | Specialty/Liquor Stores |

| Others Off Trade Channels |

| By Product Type | Fortified Wine | |

| Still Wine | ||

| Sparkling Wine | ||

| Others Wine Types | ||

| By Color | Red Wine | |

| White Wine | ||

| Rose Wine | ||

| By End User | Men | |

| Women | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Specialty/Liquor Stores | |

| Others Off Trade Channels | ||

Key Questions Answered in the Report

What is the current value of the United States wine market?

The market is valued at USD 360.3 billion in 2026 and is projected to grow to USD 402.93 billion by 2031.

Which product type is expanding the fastest?

Sparkling wine is forecast to register a 2.69% CAGR between 2026 and 2031, thanks to wider consumption occasions and interest from younger adults.

What role do low-alcohol wines play in future demand?

Low- and no-alcohol options align with moderation trends, especially among Gen Z, and are expected to add incremental value as nutritional labeling boosts transparency.

Which distribution channel will grow most quickly?

On-trade outlets should post a 2.41% CAGR to 2031 as hospitality rebounds and experiential dining drives curated wine programs.

Page last updated on: