Organic Beverage Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

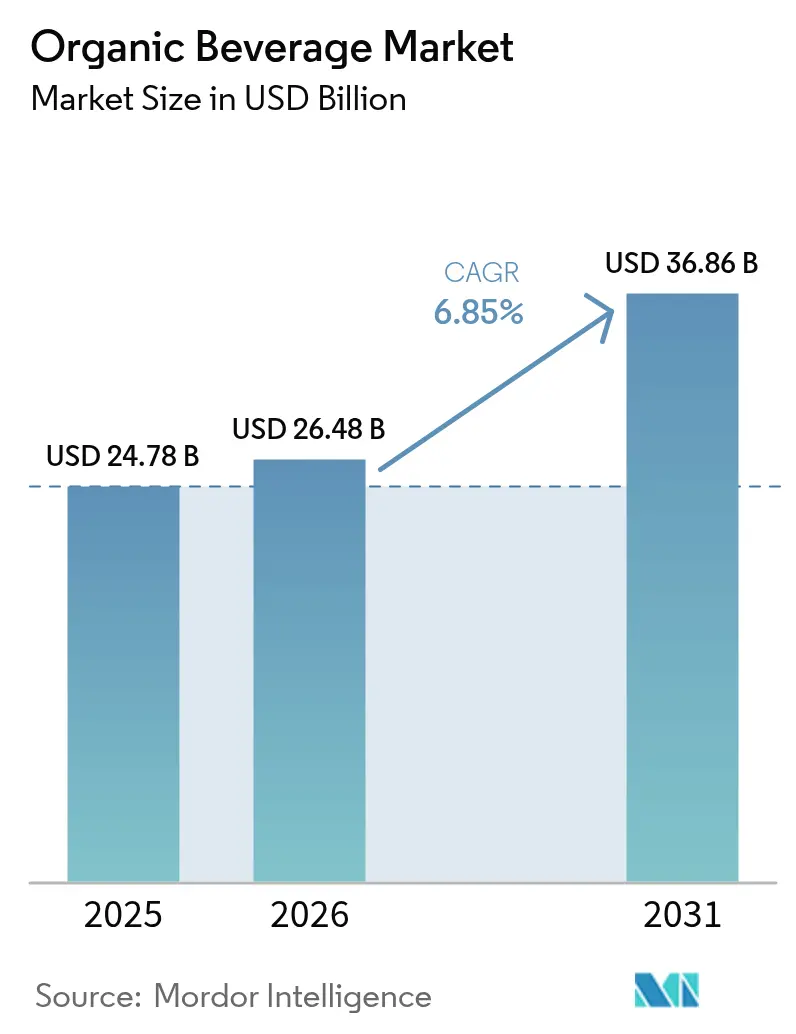

| Market Size (2026) | USD 26.48 Billion |

| Market Size (2031) | USD 36.86 Billion |

| Growth Rate (2026 - 2031) | 6.85% CAGR |

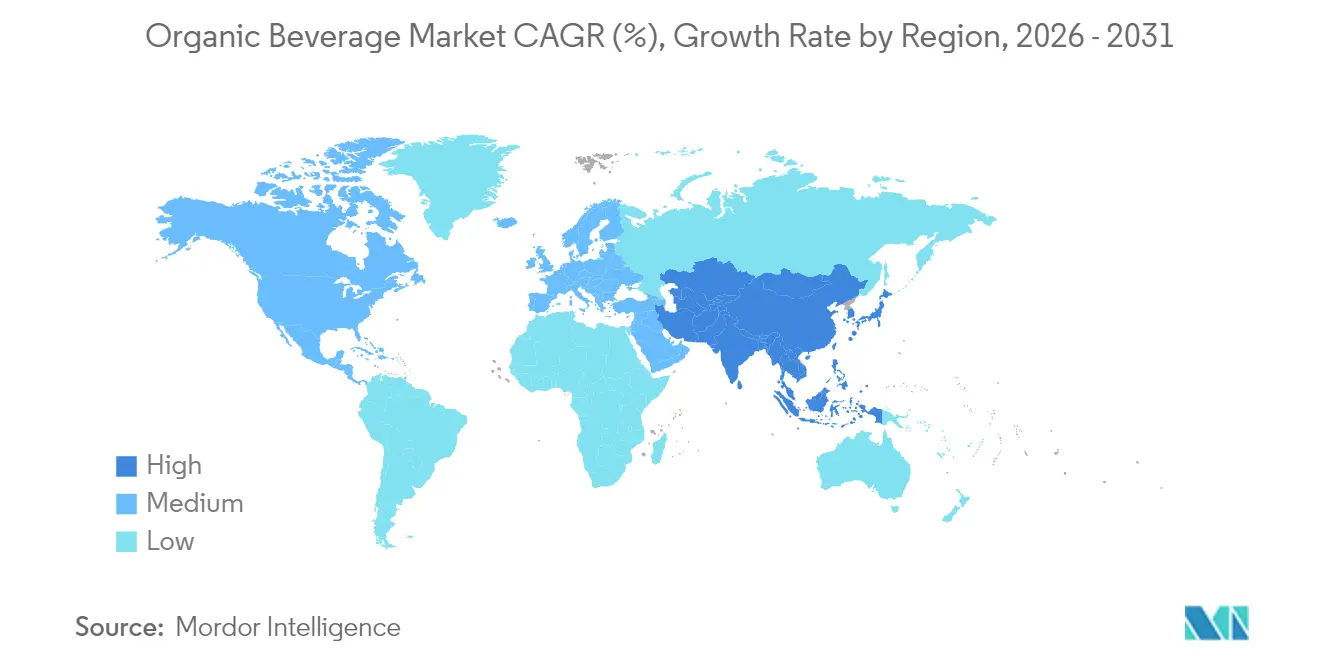

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Organic Beverage Market Analysis by Mordor Intelligence

The organic beverage market size in 2026 is estimated at USD 26.48 billion, growing from 2025 value of USD 24.78 billion with 2031 projections showing USD 36.86 billion, growing at 6.85% CAGR over 2026-2031. Growth rests on a structural shift in consumer priorities toward certified-organic formulations that avoid synthetic additives. PepsiCo’s USD 1.95 billion purchase of Poppi in March 2025 confirms that functional sodas once confined to specialty stores have become strategic for global conglomerates. Regulatory tightening in producer nations, especially India’s eighth-edition National Programme for Organic Production (NPOP), is unlocking export opportunities for certified suppliers while raising compliance hurdles for late adopter. Packaging innovation is accelerating demand; bottles still led volumes in 2024, yet pouches and sachets are eroding that lead owing to lower carbon footprints and portion-controlled convenience. Online retail, propelled by direct-to-consumer models and rapid-commerce apps, is now the fastest growing distribution channel.

Key Report Takeaways

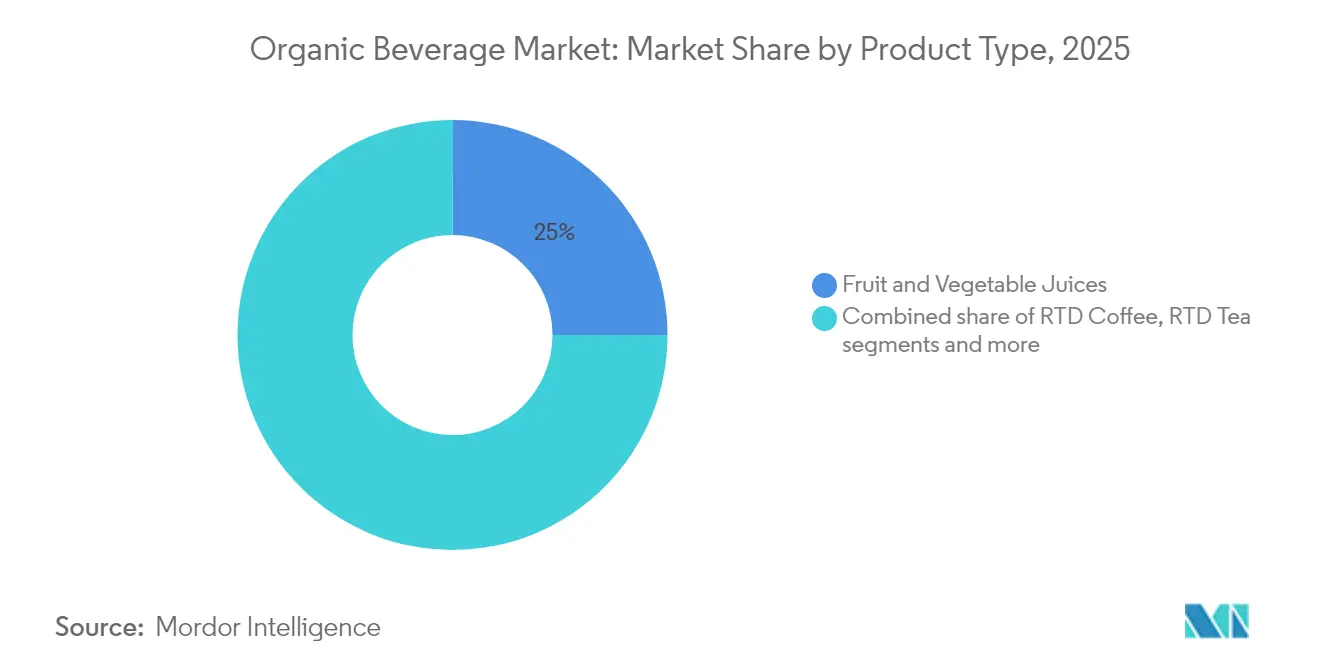

- By product type, fruit and vegetable juices accounted for 24.96% market share in 2025; functional drinks led with an 8.29% CAGR through 2031, outpacing the organic beverage market average.

- By packaging type, bottles retained 43.92% of share in 2025, while pouches and sachets are expanding at a 8.75% CAGR through 2031.

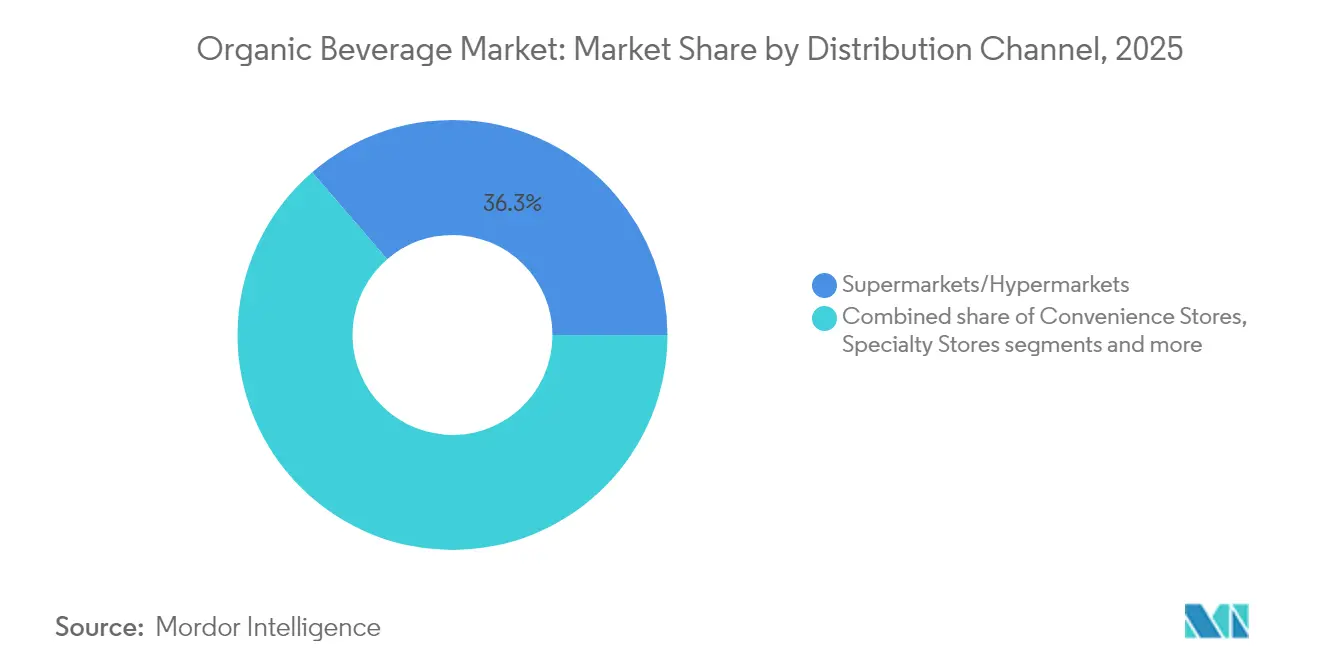

- By distribution channel, supermarkets and hypermarkets held 36.32% organic beverage market share in 2025; online retail posts the highest projected CAGR at 8.96% through 2031.

- By geography, North America captured 35.41% of value in 2025, and Asia-Pacific is forecast to register the fastest regional CAGR at 7.53% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Organic Beverage Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising health and wellness consciousness and desire to avoid synthetic additives and pesticides | +1.5% | Global, with strongest uptake in North America, Western Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Increasing preference for natural, clean-label products | +1.2% | North America and Europe core, expanding to Asia-Pacific urban centers | Short term (≤ 2 years) |

| Growth in plant-based, functional, and fortified drinks (probiotics, herbal, non-dairy) | +1.8% | Global, with rapid adoption in Asia-Pacific and North America | Medium term (2-4 years) |

| Supportive government initiatives and certifications promoting organic farming and products | +0.9% | Asia-Pacific (India, China), Europe, North America | Long term (≥ 4 years) |

| Strong marketing, social media influence, and brand positioning around "organic" and "natural" | +0.8% | Global, particularly North America and Europe | Short term (≤ 2 years) |

| Product innovation in flavors, ingredients, and formats tailored to specific lifestyle needs | +1.3% | Global, with early gains in North America, Western Europe, and Australia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising health and wellness consciousness and desire to avoid synthetic additives and pesticides

Rising health and wellness consciousness drives the organic beverage market as consumers increasingly prioritize natural products free from synthetic additives and pesticides. This shift reflects growing awareness of long-term health risks associated with chemical residues in conventional beverages, prompting demand for certified organic alternatives. According to the Organic Trade Association, 90% of Generation Z consumers (ages 13-28) identify as committed or new organic consumers, accelerating this trend through their influence on purchasing decisions and social media advocacy [1]Source: Organic Trade Association, “2024 U.S. Organic Industry Survey,” ota.com . Parents particularly seek organic juices and teas for children to minimize exposure to harmful substances during critical developmental stages. Wellness trends amplify this preference, positioning organic beverages as functional options supporting immunity, hydration, and detoxification. Moreover retail expansion of organic sections and premium pricing tolerance underscore the segment's robust growth trajectory fueled by health-driven purchasing decisions.

Increasing preference for natural, clean-label products

Increasing preference for natural, clean-label products propels the organic beverage market as consumers reject artificial preservatives, colors, and flavors prevalent in conventional offerings. This demand stems from heightened scrutiny of ingredient lists, with shoppers favoring transparency and minimal processing in juices, teas, and functional drinks. According to research by CBI Ministry of Foreign Affairs, clean-label products are projected to constitute over 70% of portfolios in 2025 and 2026, increasing from 52% in 2021[2]Source: CBI Ministry of Foreign Affairs, “Which trends offer opportunities,” cbi.eu, underscoring the rapid portfolio shift among manufacturers. Clean-label positioning enables premium pricing, as organic certifications signal purity and authenticity to discerning buyers. Younger demographics, particularly millennials and Gen Z, drive this shift through social media influence and ethical consumption values. Retailers respond by expanding organic aisles and highlighting "no additives" claims to capture market share.

Growth in plant-based, functional, and fortified drinks (e.g., probiotics, herbal, non-dairy)

Growth in plant-based, functional, and fortified organic drinks such as probiotics, herbal infusions, and non-dairy alternatives fuels the organic beverage market amid rising demand for health-enhancing options. Consumers seek beverages delivering targeted benefits like gut health, immunity boosting, and stress relief through natural botanicals and superfoods. Plant-based variants, including almond and oat milks, capture share from traditional dairy as lactose intolerance and veganism rise globally. Fortified formulations with vitamins, adaptogens, and nootropics appeal to wellness enthusiasts prioritizing preventive nutrition. This diversification expands category appeal beyond juices into RTD teas and kombuchas with premium pricing power. Manufacturers leverage organic certification to differentiate in crowded functional aisles. The segment's innovation drives double-digit growth, reshaping retail landscapes with expanded shelf space.

Supportive government initiatives and certifications promoting organic farming and products

Supportive government initiatives and certifications promoting organic farming accelerate the organic beverage market by providing financial incentives, subsidies, and standardized labeling that build consumer trust. In the United States, the USDA's Organic Transition Initiative earmarked USD 300 million to assist farmers in transitioning to organic practices, complemented by an additional USD 20 million from the Organic and Transitional Education and Certification Program to alleviate certification costs[3]Source: U.S. Department of Agriculture, “Organic Transition Initiative Fact Sheet,” usda.gov. Programs like USDA Organic, EU Organic Regulation, and national schemes in Asia-Pacific reduce production costs for farmers while ensuring traceability from farm to bottle. These policies expand certified acreage for key crops like fruits, herbs, and tea leaves, stabilizing supply chains for juice and RTD producers. Import/export facilitations under organic equivalence agreements boost cross-border trade, particularly for premium exports from emerging markets. Certifications signal quality and sustainability, justifying premium pricing and appealing to eco-conscious buyers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher production and raw material costs leading to premium shelf prices | -1.1% | Global, with acute pressure in North America and Western Europe | Medium term (2-4 years) |

| Stringent organic certification, labeling rules, and compliance overheads | -0.6% | Global, particularly Europe, North America, and India | Long term (≥ 4 years) |

| Price sensitivity in mass-market consumer segments limiting penetration | -0.9% | Emerging markets in Asia-Pacific, South America, and Middle East and Africa | Short term (≤ 2 years) |

| Risk of inconsistent quality or contamination issues eroding consumer trust | -0.5% | Global, with heightened scrutiny in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Higher production and raw material costs leading to premium shelf prices

Higher production and raw material costs pose a significant restraint to the organic beverage market, contributing to premium shelf prices that can limit consumer accessibility. Organic farming demands stringent practices, including pesticide-free cultivation, crop rotation, and certification processes, which increase input costs compared to conventional agriculture. These costs are further amplified by lower yields, labor-intensive harvesting, and specialized processing techniques that preserve organic integrity. Supply chain complexities, such as limited raw material availability and enhanced quality controls, also drive up expenses. As a result, organic beverages often carry higher retail price points, potentially deterring price-sensitive consumers despite growing health awareness. Retailers face challenges balancing premium pricing with mainstream demand while manufacturers contend with cost pressures affecting margins.

Stringent organic certification, labeling rules, and compliance overheads

Stringent organic certification, labeling rules, and compliance overheads restrain the organic beverage market by imposing rigorous documentation, audits, and traceability requirements that elevate operational costs. Producers must adhere to standards like USDA Organic or EU Organic, involving annual inspections, soil testing, and prohibited substance residue monitoring, which delay market entry for new entrants. Labeling mandates demand precise claims verification, allergen disclosures, and origin tracing, complicating packaging design and increasing regulatory risks. Non-compliance penalties, including product recalls or certification revocation, deter smaller manufacturers with limited resources. These barriers fragment supply chains, as only certified farms qualify, limiting raw material sourcing flexibility. International trade faces additional hurdles from varying regional standards, hindering exports.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Functional Drinks Lead Innovation Wave

Fruit and vegetable juices held the largest market share in the organic beverage market in 2025, accounting for 24.96% of the total market value. This segment's dominance underscores its role as the foundational category driving organic beverage adoption among consumers. Its long-standing popularity stems from widespread consumer trust in the nutritional benefits and natural qualities of fruit and vegetable juices. Many consumers view these juices as a primary entry point into organic products due to their established presence in the market. The consistent demand has been sustained by increasing awareness around health and wellness, as well as the clean-label appeal of these products.

In contrast, functional drinks represent the fastest-growing segment within the organic beverage market, expanding at a robust compound annual growth rate (CAGR) of 8.29% through 2031, outpacing all other product types. This rapid growth is driven by rising consumer interest in beverages that offer additional health benefits such as enhanced immunity, energy, and digestive support. Functional drinks benefit from innovation in ingredients and formulations, integrating botanicals, probiotics, and adaptogens to cater to evolving consumer wellness trends. The segment’s expansion is further accelerated by increased marketing efforts and availability across diverse retail channels. Functional beverages appeal particularly to health-conscious consumers seeking convenience without compromising nutritional value.

By Packaging Type: Flexible Formats Gain Ground

Bottles dominated the organic beverage market's packaging segment in 2025, capturing 43.92% of the total packaging volume. This substantial share reflects the enduring legacy of glass and PET materials, which have long been staples in premium beverage categories. Glass bottles, in particular, convey a sense of luxury and quality preservation, appealing to consumers who prioritize authenticity in organic products. PET bottles offer practicality through lightweight design and recyclability, further solidifying their position in retail and distribution channels. The dominance of bottles is also supported by established supply chains and consumer familiarity with traditional packaging formats. Overall, bottles continue to lead as the preferred choice, balancing tradition with functionality in the organic beverage landscape.

Meanwhile, pouches and sachets are surging ahead as the fastest-growing packaging format in the organic beverage market, achieving a compound annual growth rate (CAGR) of 8.75% through 2031, surpassing all other options. This rapid expansion is fueled by their convenience, portability, and suitability for on-the-go consumption lifestyles. Pouches appeal to eco-conscious consumers with their potential for reduced material use and better recyclability compared to rigid formats. Sachets enable single-serve portions, ideal for trial purchases and emerging markets with price-sensitive buyers. Innovation in flexible packaging technology enhances shelf life and product freshness, driving adoption across diverse organic beverage types. This growth trajectory signals a shift toward more agile, consumer-centric packaging solutions in the evolving organic beverage sector.

By Distribution Channel: E-Commerce Redefines Route-to-Market

Supermarkets and hypermarkets secured the largest share of the organic beverage distribution market in 2025, commanding 36.32% of the total share. Their dominance highlights their critical role as the primary discovery and purchase channels for mainstream consumers seeking organic beverage options. These large-format retail outlets offer wide product assortments, competitive pricing, and convenient one-stop shopping experiences, making them attractive to a broad consumer base. The visibility and promotional capabilities within these stores help drive trial and repeat purchases of organic beverages. Established supply chain networks and strategic partnerships with organic beverage brands further reinforce supermarkets and hypermarkets as the go-to choice for consumers.

Conversely, online retail is the fastest-growing distribution channel within the organic beverage market, expanding at a compound annual growth rate (CAGR) of 8.96% through 2031, outpacing all other channels. The surge in online sales is driven by shifting consumer preferences toward convenience, home delivery, and the ability to access a wider variety of organic beverage brands beyond traditional retail assortments. Digital platforms enable personalized shopping experiences, easy price comparisons, and subscription services, enhancing customer engagement. The increasing penetration of smartphones and improvements in e-commerce infrastructure support this rapid growth. Additionally, online retail is agile in responding to emerging trends and new product launches, allowing brands to quickly reach targeted consumer segments.

Geography Analysis

North America dominated the organic beverage market in 2025, capturing 35.41% of the total market value. This leadership is underpinned by mature regulatory frameworks that ensure consumer trust and product integrity. High per-capita spending on wellness products reflects strong consumer prioritization of health-focused beverages. Established distribution networks facilitate widespread availability across retail channels. The United States stands out as the largest single-country market within the region. Its dominance is propelled by the USDA National Organic Program certification, which bolsters confidence in organic labeling. Strong consumer awareness further drives demand and market penetration in this mature landscape.

Asia-Pacific emerges as the fastest-growing region in the organic beverage market, achieving a compound annual growth rate (CAGR) of 7.53% through 2031. This rapid expansion is fueled by accelerating urbanization, which shifts consumer lifestyles toward convenient, health-oriented products. Rising disposable incomes enable broader access to premium organic beverages among middle-class populations. Government support for organic agriculture enhances local production and supply chain resilience. Increasing health consciousness and preference for natural ingredients amplify demand across diverse markets. This dynamic growth positions Asia-Pacific as a pivotal engine for the global organic beverage industry's future trajectory.

Europe maintains a significant presence in the organic beverage market, supported by stringent EU organic standards and high consumer demand for sustainable products, though it trails North America in overall share. South America shows emerging potential driven by expanding organic farming initiatives in countries like Brazil and growing export capabilities. The Middle East and Africa represent nascent opportunities, with rising urbanization and wellness trends spurring adoption, albeit constrained by infrastructural challenges and lower per-capita incomes. These regions collectively contribute to global diversification, with Europe leading in regulatory maturity, South America in production growth, and Middle East and Africa in untapped consumer bases.

Competitive Landscape

The organic beverage market is characterized by a highly fragmented competitive structure, where no single company holds a dominant position, allowing a diverse array of players to coexist and thrive. This fragmentation arises from the specialized nature of organic production, which demands adherence to stringent certification standards and sustainable sourcing practices across varied regional ecosystems. Multinational giants like PepsiCo and Coca-Cola maintain strong portfolios through acquisitions and organic lines, yet they face stiff competition from niche brands focused on specific product categories or local markets. Regional specialists, such as European artisanal juice producers or Asia-Pacific herbal tea innovators, leverage intimate knowledge of local consumer preferences and supply chains to capture significant shares.

This fragmented landscape presents substantial white-space opportunities for agile brands willing to master the complexities of organic certification and supply chain management. Certification processes, including USDA Organic, EU Organic, and regional equivalents, involve rigorous audits for soil health, pesticide avoidance, and traceability, creating barriers that deter casual participants but reward committed players. Brands that excel here can differentiate through transparent labeling and storytelling, appealing to ethically conscious consumers who prioritize provenance. By forging direct relationships with organic farmers, companies gain advantages in quality control, cost efficiency, and supply stability, mitigating risks from volatile commodity prices and climate impacts.

Ultimately, effective control of the farm-to-shelf supply chain positions brands for long-term competitive advantage in this fragmented market. Vertically integrated models allow for real-time monitoring of cultivation, processing, and distribution, ensuring product integrity and reducing intermediaries that dilute margins. This approach also facilitates rapid response to trends like functional additions or zero-waste packaging, keeping brands ahead of commoditized rivals. Regional specialists often outperform multinationals by embedding in local communities, co-developing flavors, and building loyalty through authenticity. As consumer demand for traceable organics intensifies, mastery of this end-to-end chain becomes a key differentiator, transforming fragmentation from a challenge into a strategic asset for growth-oriented brands.

Organic Beverage Industry Leaders

PepsiCo, Inc.

The Hain Celestial Group, Inc.

Nestlé S.A.

Danone S.A.

The Coca-Cola Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Clean Juice, a top USDA-certified organic juice bar franchise owned by BRIX Holdings, rolled out a limited-time deal: customers could snag signature cold-pressed juices for just 20 cents with any purchase of USD 25 or more. Among the highlighted offerings was the popular "Spicy Peach" blend, crafted from organic peach, apple, orange, lime, and a hint of habanero, all cold-pressed to ensure peak nutrient retention and purity.

- July 2024: Uncle Matt’s Organic, a prominent player in the organic orange juice market, introduced three new ready-to-drink (RTD) refrigerated brewed black tea varieties. These offerings were strategically aimed at the premium tea segment. The lineup featured: Unsweet Tea (boasting 0 calories, 0g sugar, and 60mg caffeine derived from Indian/African black tea); Sweet Tea (with 30 calories and 8g of organic sugar sourced from blue agave and stevia); and Half & Half Black Tea Lemonade (also at 30 calories, but with 4g of organic sugar).

- May 2024: Chameleon Organic Coffee, known for its artisanal bottled cold-brew coffee, expanded its ready-to-drink lineup, introducing four convenient 8 oz. cold-brew cans. Made from 100% organic beans, Chameleon's new canned cold-brew line offers four unique flavors, available in both sweetened and unsweetened variants.

Global Organic Beverage Market Report Scope

Organic beverages are beverages that have no synthetic pesticides, growth hormones, genetic engineering & artificial flavors, colors & preservatives, among other things. Organic Beverage Market is segmented by product type, distribution channels, and by geography. Based on the product type, the market is segmented into, alcoholic beverages and non-alcoholic beverages. Alcoholic Beverages are further segmented into Wine, Beer, Spirits, and Other Alcoholic Beverages, and Non-Alcoholic Beverages are further segmented into Fruit and Vegetable Juices, Dairy, Coffee and Tea, and Other Non-alcoholic Beverages. Based on distribution channel, the market is segmented into, Supermarkets/Hypermarkets, Convenience Stores, Specialist Retailers, and Online Retailers. By geography, the market is segmented into North America, Europe, South America, Asia-Pacific, and Middle-East & Africa. For each segment, the market sizing and forecasts have been done based on value (in USD Million).

| Fruit and Vegetable Juices |

| Dairy-based |

| RTD Coffee |

| RTD Tea |

| Functional Drinks |

| Other Product Types |

| Bottles |

| Cans |

| Cartons/Tetrapacks |

| Pouches/Sachets |

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Specialty Stores |

| Online Retail Stores |

| Other Distribution Channels |

| Noth America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Fruit and Vegetable Juices | |

| Dairy-based | ||

| RTD Coffee | ||

| RTD Tea | ||

| Functional Drinks | ||

| Other Product Types | ||

| By Packaging Type | Bottles | |

| Cans | ||

| Cartons/Tetrapacks | ||

| Pouches/Sachets | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Specialty Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Region | Noth America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of global organic beverage sales and how fast is it growing?

Sales reached USD 26.48 billion in 2026 and are on track to expand at a 6.85% CAGR to USD 36.86 billion by 2031.

Which product segment is expanding the quickest within organic drinks?

Functional beverages, led by probiotic and prebiotic sodas, post the fastest pace at an 8.29% CAGR through 2031.

How dominant are flexible pouches and sachets compared with traditional bottles?

Bottles still hold 43.92% of 2025 volumes, yet pouches and sachets are climbing at a 8.75% CAGR, steadily eroding that lead.

Why is Asia-Pacific attracting so much attention from beverage brands?

The region combines a 7.53% CAGR forecast with supportive certification policies such as India’s upgraded NPOP, creating lucrative opportunities for certified suppliers.

Page last updated on: