Rice Wine Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

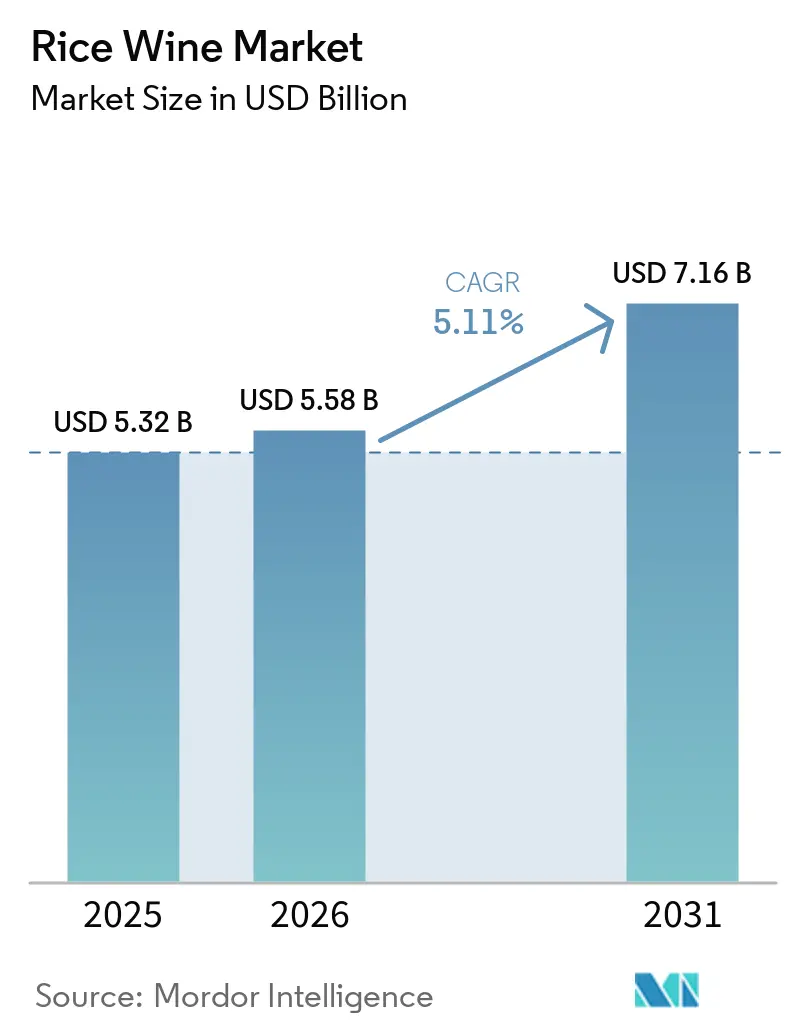

| Market Size (2026) | USD 5.58 Billion |

| Market Size (2031) | USD 7.16 Billion |

| Growth Rate (2026 - 2031) | 5.11% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Rice Wine Market Analysis by Mordor Intelligence

The global rice wine market was valued at USD 5.32 billion in 2025, estimated at USD 5.58 billion in 2026, and is projected to reach USD 7.16 billion by 2031, with a compound annual growth rate (CAGR) of 5.11% during the forecast period of 2026-2031. The market growth is driven by increasing consumer interest in traditional and heritage alcoholic beverages that emphasize authenticity, craftsmanship, and cultural significance. Greater global exposure to Asian culinary traditions has enhanced awareness of rice wine varieties such as sake, makgeolli, and huangjiu. This has facilitated the transition of rice wine from a niche ethnic beverage segment to a broader premium alcohol category. Consumers are showing a growing preference for unique flavor profiles, fermentation heritage, and artisanal production techniques, which is contributing to premiumization and driving demand for higher-value products.

Key Report Takeaways

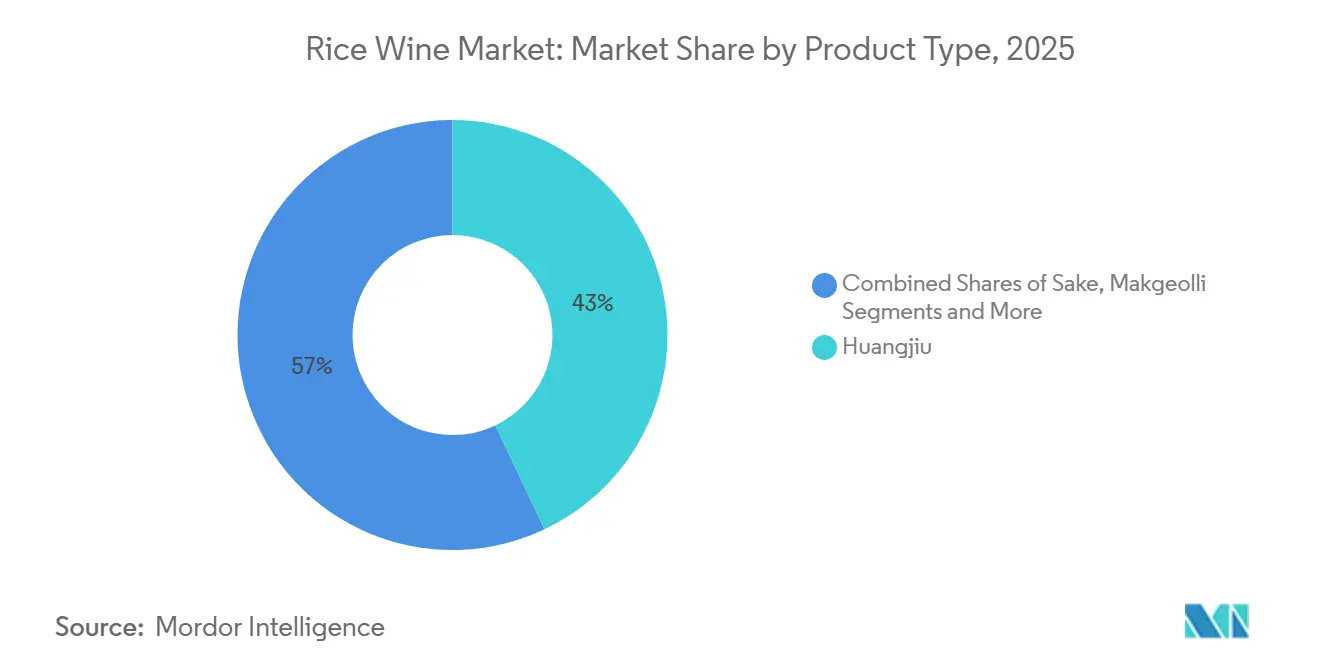

- By product type, huangjiu commanded 42.96% of rice wine market share in 2025 while makgeolli is projected to post the fastest 6.11% CAGR through 2031.

- By packaging, bottles accounted for 78.04% of the rice wine market size in 2025; cans are set to expand at a 6.23% CAGR during 2026-2031.

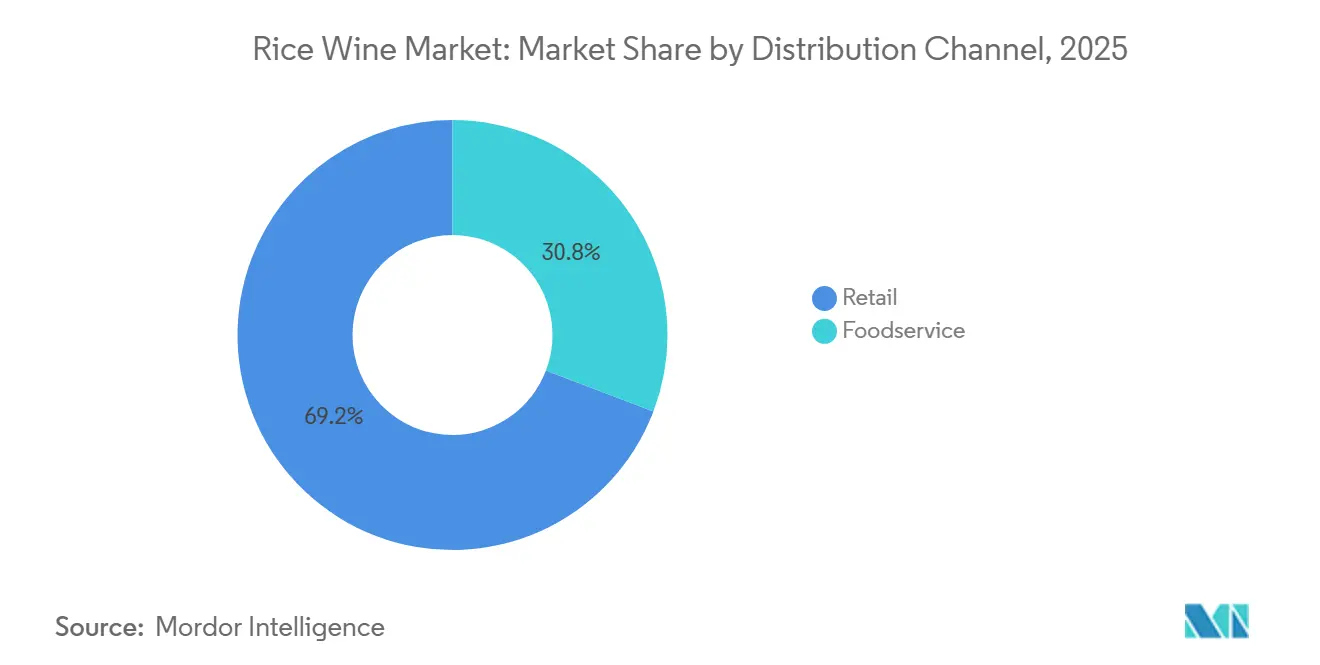

- By distribution channel, retail led with 69.21% value in 2025, whereas foodservice is forecast to grow by 6.06% CAGR to 2031.

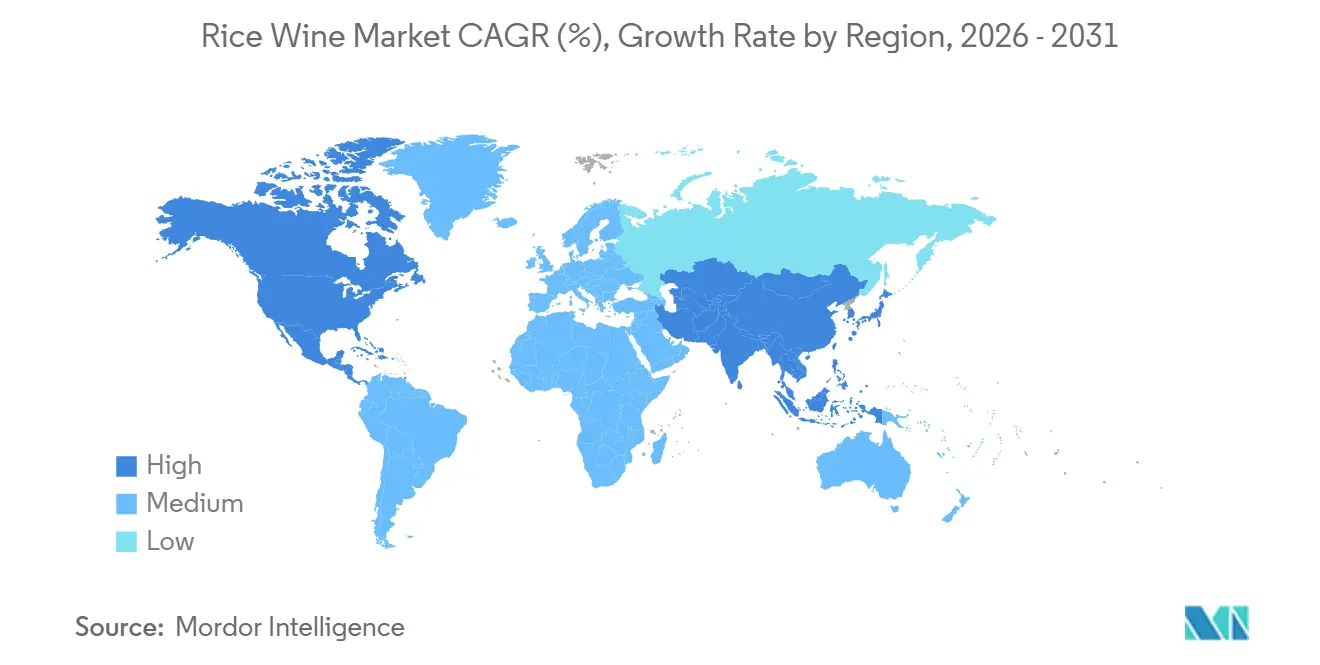

- By geography, Asia-Pacific held 66.07% share in 2025 and will remain the fastest-growing region at 5.81% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Rice Wine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for artisanal and craft rice wines | +1.2% | North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Premiumization and craft beverage movement | +1.5% | Global, concentrated in high-income markets | Long term (≥ 4 years) |

| Growth of culinary tourism and cultural exposure | +0.8% | Asia-Pacific core, spillover to North America an Europe | Medium term (2-4 years) |

| Innovation in flavors and product variants | +0.9% | Global, early adoption in South Korea, Japan, United States | Short term (≤ 2 years) |

| Health perception and functional appeal | +1.0% | North America, Europe, health-conscious segments in Asia | Medium term (2-4 years) |

| Rising influence of social media and pop culture | +0.7% | Global, strongest in markets with K-pop and anime fandoms | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing demand for artisanal and craft rice wines

The growing demand for artisanal and craft rice wines is a significant driver for the global rice wine market. Consumers are increasingly seeking authentic, small-batch, and premium alcoholic beverages with unique flavor profiles and a strong heritage appeal. Similar to trends observed in craft beer and boutique spirits, there is a rising interest in products made using traditional brewing methods, regional rice varieties, and limited-production techniques. This trend is prompting producers to focus on craftsmanship, provenance, and storytelling, which enhances the value of the category and appeals to younger consumers seeking premium and experiential drinking options. Additionally, craft rice wines are benefiting from increased appreciation for fermentation expertise, natural ingredients, and innovative flavor experimentation, helping the segment expand beyond the traditional perception of rice wine as solely a conventional beverage.

Premiumization and craft beverage movement

Premiumization and the craft beverage movement are driving a shift among consumers toward high-quality, authentic, and experience-focused alcoholic beverages. The growing preference for premium products featuring superior ingredients, refined taste profiles, and heritage-driven craftsmanship is prompting producers to reposition rice wine from a traditional category to a sophisticated lifestyle beverage. This trend is particularly prominent among younger urban consumers and premium alcohol buyers who prioritize exclusivity, artisanal production methods, and distinctive brand narratives. In response, manufacturers are introducing high-end rice wine variants with polished rice grades, extended fermentation processes, elegant packaging, and limited-edition releases to meet the demand for premium offerings. For example, Heaven Sake offers Premium Junmai Sake, crafted in Japan by Régis Camus, combining Japanese brewing traditions with luxury beverage expertise. This approach positions sake within the premium international drinks segment, appealing to consumers seeking refined and modern rice wine experiences.

Growth of culinary tourism and cultural exposure

The growth of culinary tourism and cultural exposure is driving increased consumer interest in authentic local food and beverage traditions. International travelers often seek immersive dining experiences and regional specialties, positioning rice wine as an integral part of cultural exploration in destinations with a traditional brewing heritage. Beverages such as sake, makgeolli, and huangjiu, encountered during travel, frequently lead to repeat purchases upon travelers' return, thereby boosting international demand. Culinary tourism also enhances awareness of serving rituals, flavor pairings, and craftsmanship, helping to elevate rice wine from a niche regional product to a premium and experiential category. For example, according to the Japan National Tourism Organization, the number of inbound visitors to Japan is projected to reach approximately 42.68 million in 2025 [1]Source: Japan National Tourism Organization, "Number of international tourists coming to Japan", japan.travel . This significant influx of tourists increases global exposure to sake culture through brewery tours, restaurant experiences, tasting events, and regional food tourism circuits.

Innovation in flavors and product variants

Innovation in flavors and product variants continues to be a significant driver of the global rice wine market, as producers actively diversify offerings to attract younger consumers, first-time drinkers, and evolving taste preferences. Traditional rice wine categories are being revitalized with the introduction of fruit-infused, sparkling, low-alcohol, sweetened, and ready-to-drink variants, enhancing the category's accessibility and versatility. These advancements broaden consumption occasions beyond traditional settings, appealing to consumers seeking novelty, convenience, and contemporary beverage experiences. Flavor-focused diversification not only helps brands overcome barriers associated with unfamiliar traditional taste profiles but also fosters increased trial and repeat purchases across both domestic and international markets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory and import restrictions | -0.9% | North America, Europe, emerging markets with complex customs | Long term (≥ 4 years) |

| Competition from established alcohol categories | -1.1% | Global, most acute in wine-dominant Europe and spirits-heavy North America | Medium term (2-4 years) |

| Complex flavor profiles and acquired taste | -0.6% | North America, Europe, markets with limited Asian cuisine penetration | Medium term (2-4 years) |

| Storage and handling challenges | -0.4% | Global, concentrated in warm climates and markets with underdeveloped cold chain | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Regulatory and import restrictions

Regulatory and import restrictions pose a significant challenge to the global rice wine market, as alcoholic beverage producers must comply with complex and varying regulations across different countries. Exporters of rice wine encounter diverse requirements related to alcohol licensing, customs procedures, product classification, taxation, ingredient disclosure, labeling language, and health-warning mandates. These regulatory disparities can delay market entry, increase administrative expenses, and add operational complexity for producers aiming to expand internationally. Smaller and craft-focused manufacturers are particularly impacted, as they often lack the resources and distribution networks necessary to navigate multiple regulatory systems effectively. Additionally, tariff barriers, customs inspections, and documentation requirements can disrupt supply chains and diminish the competitiveness of imported rice wine compared to locally produced alcoholic beverages.

Competition from established alcohol categories

Competition from established alcohol categories poses a significant restraint on the global rice wine market. Rice wine directly competes with well-established beverages such as grape wine, beer, whisky, vodka, and ready-to-drink cocktails, which benefit from strong consumer familiarity and extensive distribution networks. These categories have built their presence over decades through brand development, mature retail availability, substantial marketing investments, and deeply ingrained consumption cultures across global markets. Consequently, rice wine often struggles to secure shelf space, menu inclusion, and consumer attention, particularly in regions where traditional wine and beer dominate purchasing preferences. Consumers unfamiliar with rice wine tend to favor more recognizable options that align with established taste preferences and social drinking norms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Huangjiu Dominates, Makgeolli Accelerates

Huangjiu accounted for 42.96% of the product-type value in the rice wine market in 2025, driven by its strong cultural heritage, diverse product offerings, and established consumer base. As a traditional alcoholic beverage in China, huangjiu benefits from deep-rooted consumer familiarity and consistent demand tied to heritage and social customs. Its wide range of variants, differing in sweetness, aging methods, and alcohol content, caters to diverse taste preferences, supporting steady consumption and brand loyalty. Additionally, advancements in brewing technology and quality standardization have improved product consistency and enhanced its market positioning, enabling producers to focus on premiumization and differentiation.

Makgeolli is projected to grow at a 6.11% CAGR during 2026–2031, driven by its increasing global popularity as a traditional yet modern alcoholic beverage and its alignment with changing consumer preferences. Originating in South Korea, makgeolli is gaining recognition for its mild alcohol content, slightly sweet and tangy flavor, and approachable taste, making it appealing to new consumers. The segment is further supported by the growing international exposure to Korean culture, which has increased awareness and acceptance of traditional beverages in global markets. Ongoing product innovation, including flavored and sparkling variants, is further enhancing its appeal among younger consumers seeking unique and experiential drinks.

By Packaging Type: Bottles Lead, Cans Gain Momentum

Bottles accounted for 78.04% of packaging value in 2025, driven by their strong compatibility with product preservation requirements, premium positioning, and established consumer familiarity within the rice wine market. Glass bottles, in particular, are highly effective in preserving the stability, aroma, and overall quality of rice wine varieties such as sake and huangjiu, which are sensitive to light, oxygen, and temperature fluctuations. This makes bottled packaging the preferred choice for producers aiming to ensure product consistency and extend shelf life. Furthermore, bottles play a significant role in reinforcing brand image and authenticity, as traditional and premium rice wines are often associated with unique bottle shapes, labeling, and craftsmanship, enhancing their perceived value. The format also accommodates a wide range of sizes and designs, catering to both everyday consumption and premium gifting segments.

Cans are projected to grow at a 6.23% CAGR during 2026–2031, supported by their alignment with convenience-focused consumption trends and modern retail dynamics in the rice wine market. The increasing demand for portable, single-serve, and ready-to-drink formats is driving the adoption of canned packaging, particularly for lighter and more approachable variants such as makgeolli. Cans offer advantages such as ease of handling, lightweight structure, and suitability for on-the-go consumption, making them particularly appealing to younger consumers and urban lifestyles. Additionally, canned formats provide better portion control and eliminate the need for resealing, enhancing usability during casual drinking occasions. From a distribution standpoint, cans are more efficient for storage and transportation, enabling brands to expand their presence across diverse retail channels.

By Distribution Channel: Retail Dominates, Foodservice Outpaces

Retail channels accounted for 69.21% of the distribution value in 2025, driven by their extensive reach, high product visibility, and alignment with everyday purchasing behavior in the rice wine market. Retail formats, including supermarkets, hypermarkets, and online platforms, provide consumers with convenient access to a wide range of rice wine options, enabling product comparison and informed purchasing decisions. The dominance of retail channels is further supported by strong shelf presence, organized product segmentation, and in-store promotions that enhance consumer engagement and encourage impulse buying. Additionally, the rapid growth of e-commerce and digital retail platforms has significantly improved accessibility, allowing consumers to explore and purchase both domestic and imported rice wines with ease. Retail channels also benefit from established supply chains and distribution networks, ensuring consistent product availability across urban and semi-urban markets.

The foodservice channel is projected to expand at a CAGR of 6.06% during 2026–2031, supported by the global growth of out-of-home dining and the increasing integration of rice wine into hospitality offerings. According to the United States Department of Agriculture (USDA), food sales at foodservice outlets reached USD 1.52 trillion in 2024, underscoring the scale and momentum of this channel. This growth is driving greater visibility and consumption of rice wine varieties [2]Source: United States Department of Agriculture (USDA), "Food Service Industry", usda.gov. The rising presence of Asian dining formats and fusion cuisine concepts in foodservice establishments is further accelerating adoption, as operators diversify beverage menus to enhance customer experience and differentiation. Additionally, foodservice venues play a crucial role in consumer education and product trials, introducing rice wine to new audiences through curated menus and experiential dining experiences.

Geography Analysis

Asia-Pacific accounted for 66.07% of the global market value in 2025 and is projected to maintain the fastest regional growth at a CAGR of 5.81% through 2031. This growth is driven by robust domestic consumption in key markets such as China, Japan, and South Korea, coupled with increasing export activities. The region's cultural familiarity with rice wine, including products like sake, makgeolli, and huangjiu, underpins traditional consumption patterns. Additionally, the premiumization and modernization of these beverages are enhancing their appeal both locally and internationally. For example, Japan Customs reported that the export volume of domestically produced sake from Japan reached 31.05 million liters in 2024, up from 29.19 million liters in 2023, indicating rising global demand [3]Source: Japan Customs, "Export volume of refined rice wine (sake) from Japan", customs.go.jp. This combination of strong local consumption and growing international trade solidifies Asia-Pacific's position as the leading and fastest-growing regional market.

North America is the second-largest regional market and the fastest-growing developed region, driven by increasing exposure to Asian food culture and evolving consumer preferences for diverse alcoholic beverages. The proliferation of Japanese and Korean culinary concepts across the United States and Canada has introduced rice wine to a broader audience. Additionally, the rising interest in craft and premium alcoholic beverages has encouraged experimentation with traditional drinks such as sake and makgeolli. Retail expansion, including specialty liquor stores and e-commerce platforms, has further improved accessibility and product availability. These factors collectively support steady market penetration and growth in North America.

In Europe, the rice wine market is concentrated in countries like the United Kingdom, France, and Germany, where Japanese and Korean restaurants serve as key distribution channels and points of consumer exposure. The growing popularity of Asian cuisine and premium dining experiences is driving awareness and trial of rice wine, with foodservice channels playing a pivotal role. Meanwhile, South America and the Middle East and Africa represent smaller but steadily emerging markets. Growth in these regions is supported by the gradual expansion of international restaurant chains, increasing urbanization, and rising exposure to global food and beverage trends.

Competitive Landscape

The rice wine market is moderately fragmented, with a mix of long-established regional producers and emerging craft-focused brands competing in both domestic and international markets. Key players such as Hakutsuru Sake Brewing Co., Ltd., Gekkeikan Sake Co., Ltd., Takara Holdings Inc., Ozeki Corporation, and SakeOne Corporation maintain strong market positions. These companies leverage their brand heritage, extensive brewing expertise, and wide distribution networks to ensure product consistency and quality. Many of these firms, with decades or even centuries of experience, are also focusing on premiumization and global expansion strategies. Meanwhile, smaller regional breweries and craft producers are entering the market with unique offerings, contributing to a competitive and diverse landscape.

Technology is increasingly reshaping the competitive dynamics of the rice wine market, particularly through advancements in brewing processes, quality control, and packaging innovation. Producers are adopting modern fermentation techniques, temperature-controlled systems, and automation to enhance efficiency and maintain consistency at scale while preserving traditional characteristics. Packaging innovations, such as cans and single-serve formats, are enabling brands to target new consumer segments and consumption occasions. Additionally, digital tools are improving supply chain management, traceability, and product standardization, allowing both large and small players to compete more effectively in domestic and export markets.

The rise of direct-to-consumer (DTC) platforms is transforming traditional distribution models, enabling producers to engage directly with end consumers and build stronger brand relationships. Online sales channels, brand-owned websites, and e-commerce marketplaces allow companies to bypass conventional retail markups, expand their geographic reach, and gather valuable consumer insights. This shift is particularly advantageous for niche and premium rice wine brands aiming to establish a global presence without relying solely on distributors.

Rice Wine Industry Leaders

-

Hakutsuru Sake Brewing Co., Ltd.

-

Gekkeikan Sake Co., Ltd.

-

Takara Holdings Inc.

-

Ozeki Corporation

-

SakeOne Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Sake producer Fukuju has introduced its latest product, Fukuju Organic Junmai Daiginjo Yamada-Nishiki, which features a premium positioning alongside sustainably managed production. The rice used, certified 100% organic under the JAS (Japanese Agricultural Standards) system, is sourced from Hyogo Prefecture.

- October 2025: Sake ONO, a modern sake brand, introduced Sake ONO RARE, a blend of two rare Junmai Daiginjos aged together for eight months. This limited-edition release highlights the craftsmanship involved in producing premium sake.

- April 2025: Luxury sake brand Heavensake has introduced new products, including their first prestige line: "Prestige II Assemblage Junmai Daiginjo" and "Label Azul Junmai Ginjo." The bottles are crafted from Arita porcelain by Arita Porcelain Lab, blending modern design with over 220 years of tradition.

Global Rice Wine Market Report Scope

Rice wine is an alcoholic beverage created by fermenting glutinous or regular rice, characterized by a process where mold converts starch into sugars before yeast produces alcohol. The rice wine market is segmented by product type, packaging type, distribution channel, and geography. Based on product type, the market includes sake, huangjiu, makgeolli, futsu-shu, and others. Based on packaging type, the market is segmented into cans and bottles. Based on distribution channel, the market is divided into foodservice and retail, with retail further segmented into supermarkets and hypermarkets, specialty stores, online retail, and other distribution channels. Based on geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The report provides market size and forecasts in both value (USD) and volume (tons) for all the mentioned segments.

| Sake |

| Huangjiu |

| Makgeolli |

| Futsu-shu |

| Others |

| Cans |

| Bottles |

| Foodservice | |

| Retail | Supermarkets and Hypermarkets |

| Specialty Stores | |

| Online Retail | |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Product Type | Sake | |

| Huangjiu | ||

| Makgeolli | ||

| Futsu-shu | ||

| Others | ||

| By Packaging Type | Cans | |

| Bottles | ||

| By Distribution Channel | Foodservice | |

| Retail | Supermarkets and Hypermarkets | |

| Specialty Stores | ||

| Online Retail | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

How large will the rice wine market be by 2031?

The rice wine market size is forecast to reach USD 7.16 billion by 2031, expanding at a 5.11% CAGR from 2026-2031.

Which product category is growing the fastest?

Makgeolli is expected to register the quickest 6.11% CAGR through 2031, outpacing all other rice-wine types

What packaging format shows the highest growth potential?

Cans are set to grow at 6.23% CAGR during 2026-2031, faster than bottles, due to portability and higher recycling rates.

Which region dominates global demand?

Asia-Pacific accounted for 66.07% of global consumption in 2025 and is projected to remain the largest and fastest-growing region through 2031.

Page last updated on: