Luxury Wines And Spirits Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

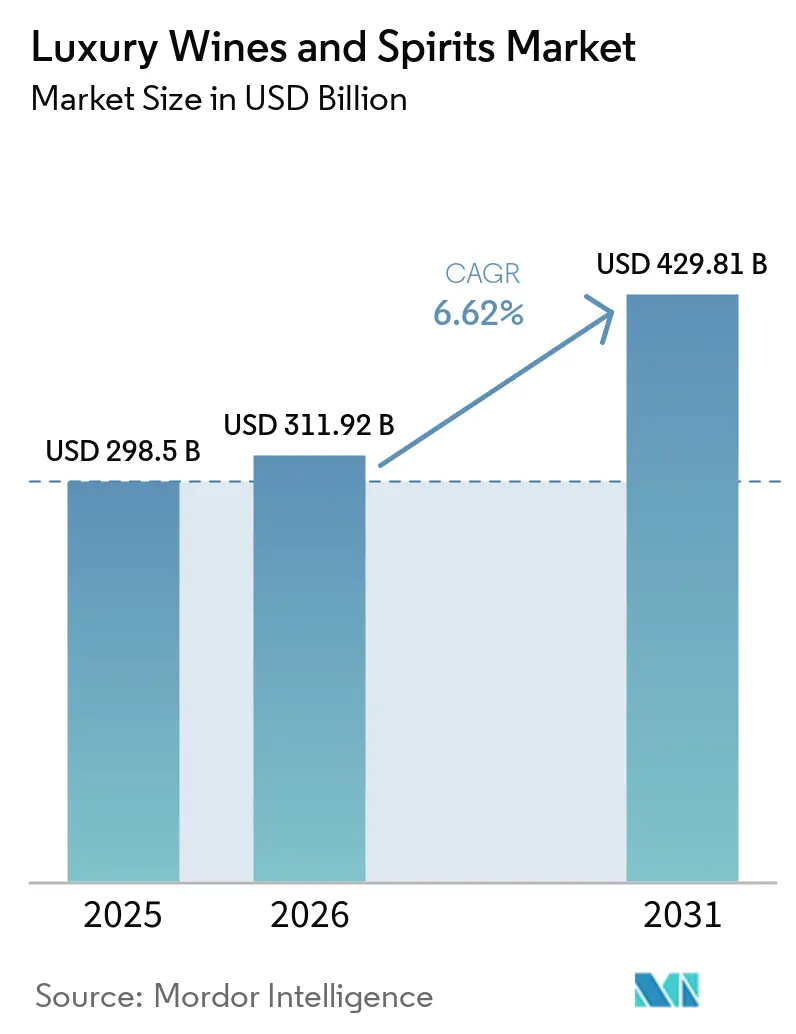

| Base Year Market Size (2025) | USD 298.5 Billion |

| Market Size (2026) | USD 311.92 Billion |

| Market Size (2031) | USD 429.81 Billion |

| Growth Rate (2026 - 2031) | 6.62% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Luxury Wines And Spirits Market Analysis by Mordor Intelligence

The luxury wines and spirits market size is expected to increase from USD 298.5 billion in 2025 to USD 311.9 billion in 2026 and reach USD 429.8 billion by 2031, growing at a CAGR of 6.6% over 2026-2031. This market thrives on the concentrated wealth at its pinnacle, a trend of premiumization among younger affluent consumers, and the burgeoning influence of travel on luxury purchases. Unlike the broader alcohol sector, the luxury tier showcases a pronounced pricing resilience, safeguarding its value even amidst waning aspirational demand. Opportunities are burgeoning in India and across Asia, where the embrace of premium spirits lags behind Western markets. However, challenges loom: U.S. tariffs on European wines and spirits, effective February 24, 2026, exert significant margin pressure, and climate risks cast a long shadow over the economics of ultra-premium vineyards[1]Source: DP&F Law, "Alcohol Beverage Importers Continue to Navigate Uncertainty Despite Supreme Court Decision on IEEPA Tariffs", dpf-law.com. In this competitive landscape, players are shifting focus from mere volume pursuits to strategic moves like portfolio pruning, selective brand investments, and refined channel executions.

Key Report Takeaways

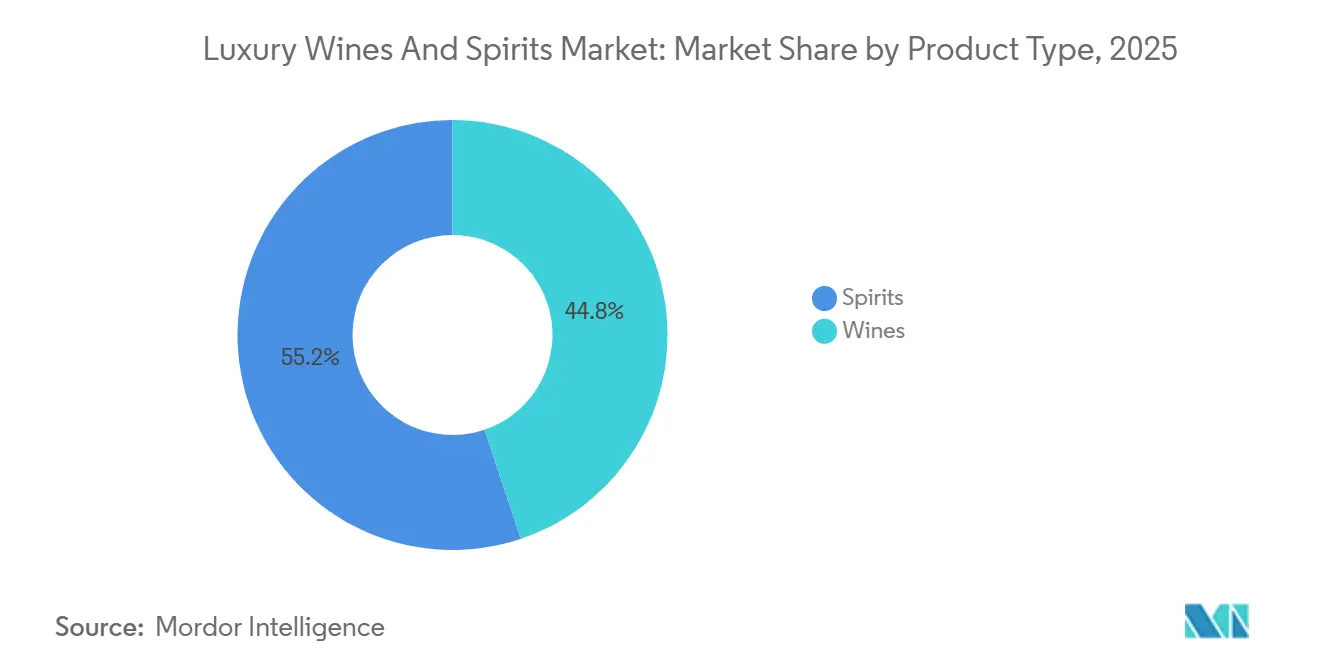

- By product type, spirits led with 55.7% share of the luxury wines and spirits market size in 2025, and luxury wines are forecast to expand at 6.8% through 2031.

- By end user, men held 59.4% of the luxury wines and spirits market share in 2025, and women are projected to record the highest CAGR at 7.3% through 2031.

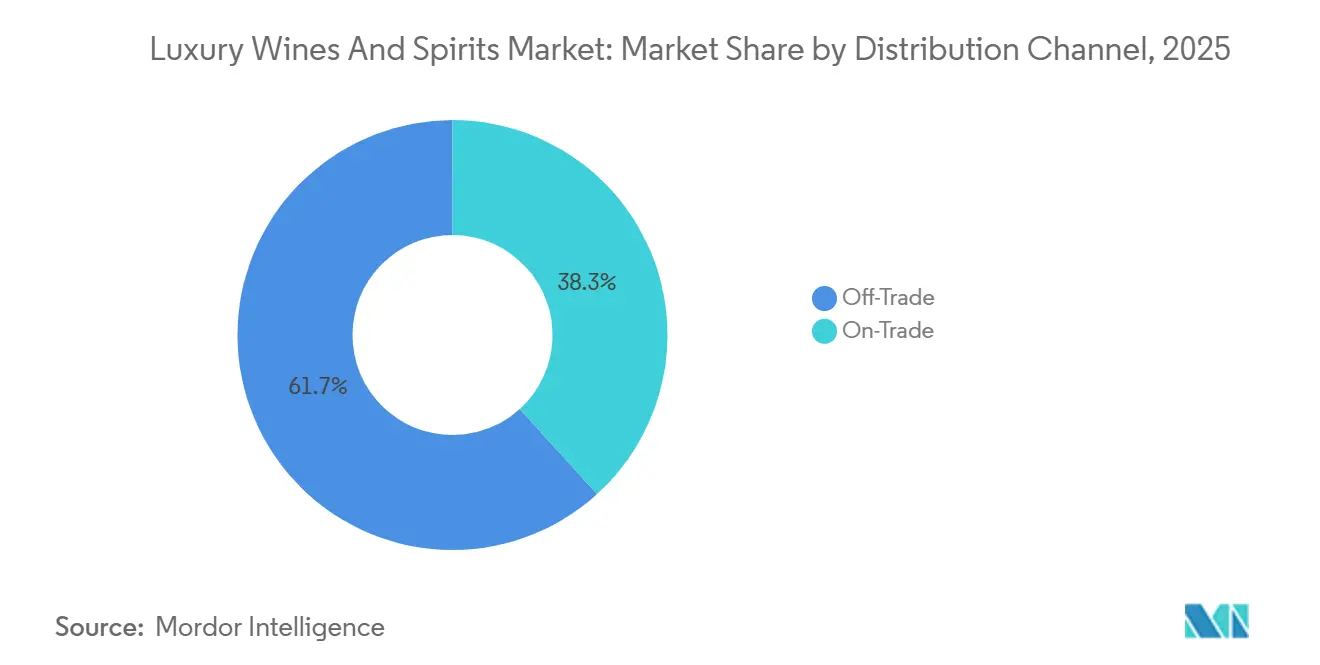

- By distribution channel, off-trade held 62.4% of revenue in 2025, and on-trade is expected to grow fastest at 7.3% through 2031.

- By geography, Europe accounted for 35.4% of the luxury wines and spirits market share in 2025, and Asia-Pacific is set to expand at 8.1% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Luxury Wines And Spirits Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing high-net-worth individual (HNWI) population and wealth expansion | +2.0% | Global, with concentrated gains in North America, Asia-Pacific, and GCC | Long term (≥ 4 years) |

| Premiumization and trading-up trends among affluent millennials | +1.5% | Global, with the strongest impulse in North America, Europe, and urban Asia-Pacific | Medium term (2–4 years) |

| Rising demand in emerging Asian markets | +1.2% | Asia-Pacific core (India, China, Japan, Vietnam, Malaysia), spill-over to Middle East and Africa | Medium term (2–4 years) |

| Expansion of luxury travel retail channels | +0.7% | Global: highest impact in the UAE, Singapore, Istanbul, and Hong Kong airports | Short term (≤ 2 years) |

| Sustainability-driven "rare cask" programs boosting ultra-premium pricing | +0.5% | North America and Europe, with growing traction in Japan and Singapore | Medium term (2–4 years) |

| "Experiential" luxury and tourism | +0.6% | Global: highest in Southeast Asia, GCC, and European wine tourism belts | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Growing High-Net-Worth Individual (HNWI) Population and Wealth Expansion

The growing concentration of wealth among high-net-worth individuals (HNWIs) is significantly strengthening demand for luxury wines and spirits, as affluent consumers increasingly prioritize exclusivity, provenance, and premium drinking experiences. According to the U.S. Federal Reserve’s Distributional Financial Accounts, the top 1% of Americans controlled nearly 31% of total household wealth in 2025, reflecting an unprecedented concentration of disposable capital toward ultra-premium consumption categories. This wealth accumulation has accelerated premiumization trends across the alcohol industry, with luxury wine houses and spirits producers expanding high-end portfolios targeted at affluent consumers in metropolitan markets such as New York, Miami, and Los Angeles. Product innovation further demonstrates this shift. For instance, in 2024, Treasury Wine Estates strengthened its luxury positioning through strategic investments and the expansion of premium vineyards. In 2025, the company launched “Treasury Collective,” a dedicated global premium wine division focused on luxury-led growth and consumer-centric innovation. By 2026, luxury portfolio performance from brands such as Penfolds and DAOU continued driving revenue growth, highlighting resilient demand for prestige wines despite broader market moderation.

Premiumization and Trading-Up Trends Among Affluent Millennials

In 2025, millennials led the way in luxury spending, outpacing all other generational cohorts. Their mantra of "drink better, less often" is not just curbing volume but significantly boosting the value of each transaction. This shift is evident in the surging popularity of ultra-premium cask programs and aged expressions, which are now favored over standard SKUs. Wealth management research highlights this trend, noting that 50% of next-gen high-net-worth individuals (HNWIs) are making passion investments, blending personal interests with anticipated financial gains. Take, for example, Gordon & MacPhail's Connoisseurs Choice Heritage Collection, debuting in March 2026 at GBP 18,000 for a set of five single malts. Additionally, Artisan Casks rolled out entire maturing casks in May 2026, starting at GBP 60,000[2]Source: Fred Minnick, "Artisan Casks Rolls Out 2026 Scotch Cask Portfolio", fredminnick.com. Such price tags, once deemed niche just five years prior, now attract a wave of younger collectors. This millennial trading-up trend is reshaping the market, creating a barbell demand structure that favors brands with distinct positioning at either end.

Rising Demand in Emerging Asian Markets

Emerging Asian markets, notably India, China, Vietnam, Thailand, and Southeast Asia, are fueling a surge in the global luxury wines and spirits market. This growth is spurred by rapid urbanization, a trend towards premiumization, a burgeoning affluent population, and shifting consumption preferences among the youth. The International Wine and Spirits Research (IWSR) reported that in 2024, India solidified its position as a pivotal market for beverage alcohol globally. The country witnessed not only a rise in total beverage alcohol volumes but also a notable uptick in value. Categories like premium whisky, imported spirits, and luxury offerings showcased particularly robust growth. Echoing this sentiment, the Asia-Pacific International Spirits and Wines Alliance (APISWA) underscored the growing significance of imported wines and spirits in ASEAN economies. This growth is bolstered by increased spending from the middle class and a surge in luxury consumption driven by tourism. Reflecting this regional demand, 2024 saw a robust expansion of premium blended Scotch and Indian single malts across Asia. By 2025, luxury spirit brands were ramping up limited-edition launches and experiential retail strategies, specifically targeting Asia's affluent consumers. Projections for 2026 indicated that imported spirits in India were set to grow at an impressive 8% CAGR, continuing through 2029, underscoring Asia's pivotal role in the global luxury alcohol narrative.

Expansion of Luxury Travel Retail Channels

As international passenger traffic surges, luxury travel retail channels are emerging as a pivotal growth driver for the global luxury wines and spirits market. Enhanced airport retail infrastructures and exclusive duty-free product launches are fueling increased consumer spending on premium alcoholic beverages. The International Air Transport Association (IATA) reported a 10.4% year-over-year rise in global passenger traffic for 2024, surpassing pre-pandemic figures. Notably, international traffic saw a 13.6% uptick, bolstering footfall in airport duty-free stores and cruise retail outlets. The rebound in premium-class travel has further amplified luxury alcohol purchases, with IATA noting an 11.8% rise in international business and first-class travel in 2024. Capitalizing on this trend, luxury spirits companies are rolling out travel-exclusive products and innovative retail concepts. In 2024, they collaborated with Avolta to unveil a permanent premium Absolut installation at Stockholm Arlanda Airport, underscoring the push towards experiential luxury retailing. In 2025, they debuted “The Departure Lounge” concept at the TFWA World Exhibition, aiming to boost traveler engagement and elevate premium spirits sales in airport settings. That same year, Pernod Ricard unveiled The Chuan Pure Malt Whisky Travel Exclusive Edition in global duty-free outlets, specifically targeting affluent Asian consumers. By 2026, Diageo broadened its travel-retail-exclusive lineup with Johnnie Walker Blue Label Azure and orchestrated over 100 airport activations for Don Julio and Casamigos, strategically aligned with FIFA World Cup tourism in North and South America.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Counterfeit and illicit trade are affecting brand integrity | -0.8% | MEA core (South Africa, Nigeria, Kenya), spill-over to Latin America and South Asia | Short term (≤ 2 years) |

| Stringent excise taxation and import duties | -0.7% | Global: highest impact in the Europe, North America, Ireland, Canada, and India | Medium term (2–4 years) |

| Climate change impact on ultra-premium vineyard yields | -0.4% | Europe (Bordeaux, Champagne), North America (Napa Valley, Sonoma), and emerging wine regions | Long term (≥ 4 years) |

| Rising sober-curious movement in developed markets | -0.9% | North America, the Europe (particularly Northern Europe), and Australia | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Counterfeit and Illicit Trade Affecting Brand Integrity

Counterfeit and illicit trade are undermining the global luxury wines and spirits market, eroding brand integrity, diminishing consumer trust, and exposing premium beverage companies to both revenue losses and reputational harm. Premium labels, with their high resale value, are prime targets for counterfeiters. These nefarious actors employ tactics like bottle refilling, falsified packaging, smuggling, and leveraging illegal distribution networks. The Organization for Economic Co-operation and Development notes that organized crime is increasingly drawn to the illicit alcohol trade, lured by its high profit margins and the low risk of detection. Alarmingly, counterfeit alcohol is making its way into legitimate retail and hospitality sectors. Further underscoring the gravity of the situation, the OECD reported in 2025 that counterfeit and pirated goods constituted nearly 2.3% of global trade, posing significant threats to premium consumer industries, notably luxury spirits. In a bid to counter these challenges, industry bodies like TRACIT advocated for ethanol-control frameworks and bolstered customs enforcement in 2024. By 2025, luxury spirits brands were not just on the defensive; they actively integrated anti-counterfeit technologies. Innovations like QR-enabled authentication, tamper-proof closures, and invisible packaging security systems were deployed to safeguard their premium whisky, cognac, and champagne portfolios. Looking ahead to 2026, the industry was set to embrace even more sophisticated measures. Advanced authentication technologies, including AI-driven track-and-trace systems and through-bottle spectroscopy, were being rolled out to bolster authenticity verification and enhance supply-chain transparency in the high-stakes luxury spirits arena.

Stringent Excise Taxation and Import Duties

Global luxury wines and spirits markets face challenges from stringent excise taxes and high import duties, which inflate retail prices, reduce cross-border trade competitiveness, and limit affordability for premium alcoholic beverages in both emerging and developed economies. Products like luxury wines, Scotch whisky, cognac, tequila, and imported champagnes are particularly impacted, as excise structures and customs tariffs significantly raise their final consumer prices. The World Trade Organization notes that alcoholic beverages encounter substantial tariff and non-tariff barriers, especially in the Asia-Pacific and emerging markets, where import duties on spirits often exceed 100%, restricting global luxury brands' market access. In India, the Confederation of Indian Alcoholic Beverage Companies (CIABC) reported in 2024 that cumulative duties and state-level taxes can triple the retail prices of imported liquor, hindering premium spirits' penetration. Similarly, the Distilled Spirits Council of the United States stated in 2025 that retaliatory tariffs and excise-related trade barriers continued to constrain American whiskey exports, limiting premium brand growth. To counter these pressures, the industry is adapting. In 2024, premium spirits companies localized bottling and packaging to reduce import-related costs. By 2025, luxury wine and spirits producers will have introduced travel-retail-exclusive offerings and smaller premium pack sizes to maintain consumer accessibility. By 2026, multinational beverage companies accelerated partnerships and domestic production agreements in high-tariff countries to offset excise burdens and remain competitive in the luxury alcohol segment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Spirits Lead as Luxury Wines Accelerate

Spirits held 55.7% of the luxury wines and spirits market size in 2025, while the luxury wines segment is forecast to grow at a 6.8% CAGR through 2031. Spirits dominate the market due to strong global demand for premium whisky, tequila, cognac, and vodka, supported by cocktail culture, travel retail expansion, and higher margins in ultra-premium categories. The Distilled Spirits Council of the United States reported that premium-and-above spirits continued outperforming standard categories in 2025, particularly tequila and American whiskey exports. In 2024, Diageo reopened the Port Ellen distillery in Scotland to strengthen luxury Scotch production, while in 2025 it formed the Diageo Luxury Group to accelerate premium portfolio expansion.

Luxury wines are the fastest-growing segment due to rising demand for collectible vintages, luxury wine tourism, premium dining experiences, and affluent consumers seeking provenance-driven brands. The International Organization of Vine and Wine highlighted continued resilience in premium wine consumption despite broader volume moderation globally. In 2024, Treasury Wine Estates expanded investments in premium winemaking and luxury-focused operations, including its high-end production facilities and Penfolds portfolio. During 2025, the company accelerated acquisitions and divestments to prioritize luxury labels, while in 2026, demand for Penfolds in China and Asia surged significantly, with Treasury Wine reporting double-digit regional depletion growth supported by premium red wine demand and expanded Asia-focused regional operations.

By End User: Female Buyers Reshape Premium Consumption

The Men segment accounted for 59.36% of the luxury wines and spirits market in 2025, while the women segment is projected to grow at a 7.28% CAGR over 2026–2031. Men continue to dominate luxury alcohol consumption due to higher spending on premium whisky, cognac, and aged spirits, particularly in corporate hospitality, luxury bars, and collector-driven categories. The Distilled Spirits Council of the United States noted in 2025 that premium American whiskey and tequila sales remained heavily driven by male consumers and luxury on-premise demand. In line with this, in 2024, Brown-Forman expanded its ultra-premium Jack Daniel’s portfolio with new aged whiskey launches, while during 2025–2026 the company strengthened premium visitor experiences and distillery tourism investments in Tennessee to reinforce brand loyalty among affluent male consumers and collectors globally.

The women segment is the fastest-growing category due to increasing female purchasing power, evolving social drinking patterns, and growing preference for premium wines, low-alcohol luxury beverages, and experiential consumption. The International Organization of Vine and Wine highlighted in 2025 that premium wine consumption among younger and female consumers continued rising across urban markets globally. In 2024, Moët Hennessy expanded women-focused experiential champagne campaigns and premium rosé offerings, while 2025–2026 witnessed partnerships with luxury hospitality and lifestyle brands targeting female consumers through curated tasting events, luxury travel experiences, and premium sparkling wine innovations across Asia-Pacific and North America.

By Distribution Channel: Off-Trade Dominant as On-Trade Narrows the Gap

On-Trade registers the fastest growth at a 7.34% CAGR over 2026–2031, while the off-Trade channels, encompassing specialty/liquor stores and other retail formats, retained 62.36% of the market in 2025. Off-trade dominates due to wider accessibility, premium retail assortments, e-commerce expansion, and growing at-home luxury consumption trends. The Wine & Spirits Wholesalers of America highlighted in 2025 that premium alcohol sales through retail and liquor store channels remained resilient despite inflationary pressures. Moreover, in 2024, Total Wine & More expanded premium spirits and luxury wine selections across new U.S. store locations, while 2025–2026 witnessed increased partnerships with luxury beverage brands and omnichannel retail investments to strengthen premium consumer engagement and direct-to-consumer purchasing convenience.

The on-trade segment is the fastest-growing channel due to rising luxury hospitality spending, experiential dining trends, and premium cocktail culture across upscale bars, hotels, and fine-dining venues. In 2025, Cointreau partnered with The World’s 50 Best Bars as the official orange liqueur partner across North America, Asia, and global awards programs, directly supporting bartender collaborations, immersive cocktail events, and luxury mixology experiences. In 2026, the partnership expanded into Europe’s 50 Best Bars in Amsterdam alongside new guest-shift activations and product launches, strengthening premium spirits visibility within elite hospitality venues globally[3]Source: Cointreau, "Cointreau partners with the world's 50 best bars", cointreau.com.

Geography Analysis

Europe led the luxury wines and spirits market with a 35.40% share in 2025 due to its deep-rooted wine and spirits heritage, established luxury tourism industry, and concentration of premium producers across France, Italy, and Scotland. The Comité Européen des Entreprises Vins highlighted in 2025 that European wine exports maintained strong value growth despite volume moderation, driven by premiumization trends. In 2024, LVMH expanded its Moët Hennessy luxury portfolio through premium champagne and cognac launches, while 2025–2026 witnessed continued investments in vineyard modernization, whisky tourism infrastructure, and luxury hospitality partnerships across Europe.

Asia-Pacific projects the steepest growth trajectory at an 8.10% CAGR over 2026–2031, supported by rising affluent populations, urbanization, and growing demand for imported premium alcohol in China, India, Japan, and Southeast Asia. The International Wine and Spirits Research reported in 2025 that India and Southeast Asia were among the fastest-growing premium spirits markets globally. In 2024, Pernod Ricard expanded premium whisky operations and brand activations across India and China, while there were increased luxury wine imports, Asia-focused product launches, and premium retail expansions targeting younger affluent consumers.

North America demonstrates stable growth due to mature premium alcohol consumption patterns, strong luxury hospitality demand, and resilient spending by high-net-worth consumers despite economic moderation. The Distilled Spirits Council of the United States reported in 2025 that high-end tequila, American whiskey, and ready-to-drink premium cocktails sustained value growth in the U.S. market. In 2024, Constellation Brands expanded its premium wine and spirits portfolio through innovation-led investments, while 2025–2026 witnessed continued luxury product launches, experiential tasting programs, and premium distillery tourism expansions across the United States and Canada.

Competitive Landscape

The luxury wines and spirits market exhibits a partially consolidated structure at the portfolio level, with LVMH Moët Hennessy, Pernod Ricard, and Diageo commanding the highest-value global segments. These companies strengthened ultra-premium portfolios through luxury-focused investments, hospitality collaborations, and limited-edition product launches targeting affluent consumers and high-growth travel retail channels. LVMH accelerated experiential luxury strategies through exclusive champagne tourism and premium retail partnerships, while Pernod Ricard expanded premium whisky and cognac visibility across Asia-Pacific and global duty-free markets.

Competition in the market increasingly centers on premiumization, heritage branding, and experiential consumer engagement. In 2025, Diageo established the Diageo Luxury Group to unify luxury spirits operations and accelerate growth across premium Scotch, tequila, and rare spirits categories. The company also expanded luxury hospitality and sports partnerships linked to international events through 2026. Meanwhile, Rémy Cointreau strengthened its luxury mixology strategy through partnerships with The World’s 50 Best Bars, increasing premium cognac and liqueur visibility within elite hospitality venues and global cocktail programs.

Market participants are also pursuing acquisitions, regional expansions, and direct-to-consumer initiatives to strengthen competitive positioning. In June 2025, Treasury Wine Estates accelerated its luxury-led portfolio strategy by prioritizing Penfolds and other premium wine assets across Asia and North America. Simultaneously, Brown-Forman expanded premium whiskey tourism and experiential retail investments in the United States, while several luxury producers increased exclusive membership programs, cellar experiences, and digital personalization capabilities to strengthen customer loyalty and improve margins in the ultra-premium beverage segment.

Luxury Wines And Spirits Industry Leaders

-

LVMH Moët Hennessy Louis Vuitton

-

Pernod Ricard SA

-

Diageo plc

-

Bacardi Limited

-

Brown-Forman Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Gordon & MacPhail launched its Connoisseurs Choice Heritage Collection, comprising 100 sets at GBP 18,000 per set of five single malts, including Dallas Dhu 1971, Port Ellen 1980, and Rosebank 1991. The release reinforced the industry's structural shift toward curated, scarcity-anchored rare whisky collections commanding significant premiums over conventional age-statement releases.

- November 2025: Changi Airport Group's World of Wines & Spirits 2025, in partnership with LOTTE Duty Free, featured 63 exceptional bottles from 29 luxury labels across five immersive experiential zones. Highlight sales included The Macallan Red Collection 40 Years Old at SGD 25,000 (approximately USD 18,500), setting a new Asia travel retail benchmark for ultra-premium spirits presentation.

- June 2025: Diageo India's United Spirits subsidiary acquired NAO Spirits, producer of Greater Than and Hapusa premium craft gins, for USD 15.2 million, marking a strategic entry into India's fast-growing artisanal gin segment and expanding Diageo's India-origin luxury spirits portfolio at the premium craft tier.

Luxury Wines And Spirits Market Report Scope

Luxury wines and spirits are high-end alcoholic beverages defined by exceptional craftsmanship, distinct heritage, rarity, and prestigious quality that confer status. The global luxury wines and spirits market is segmented by product type, end user, distribution channel, and geography. By product type, the market is segmented into wines and spirits. The wines segment is further sub-segmented into still wines and sparkling wines. The spirits segment is further sub-segmented into whisky, cognac, rum, tequila and mezcal, vodka, liqueurs, and other luxury spirits. By end user, the market is segmented into men and women. By distribution channel, the market is segmented into on-trade and off-trade. The off-trade segment is further sub-segmented into specialty/liquor stores and other off-trade channels. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The Market Forecasts are Provided in Terms of Value (USD).

| Wines | Still Wines |

| Sparkling Wines | |

| Spirits | Whisky |

| Cognac | |

| Rum | |

| Tequila and Mezcal | |

| Vodka | |

| Liqueurs | |

| Other Luxury Spirits |

| Men |

| Women |

| On-Trade | |

| Off-Trade | Specialty/Liquor Stores |

| Other Off-Trade Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Peru | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| Product Type | Wines | Still Wines |

| Sparkling Wines | ||

| Spirits | Whisky | |

| Cognac | ||

| Rum | ||

| Tequila and Mezcal | ||

| Vodka | ||

| Liqueurs | ||

| Other Luxury Spirits | ||

| End User | Men | |

| Women | ||

| Distribution Channel | On-Trade | |

| Off-Trade | Specialty/Liquor Stores | |

| Other Off-Trade Channels | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Peru | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the expected value by 2031?

The luxury wines and spirits market is forecast to reach USD 429.8 billion by 2031 from USD 311.9 billion in 2026, which implies a 6.6% CAGR over 2026-2031.

Which product group currently leads revenue?

Spirits led with 55.7% of revenue in 2025, supported by Scotch whisky, Cognac, and premium agave categories, while luxury wines are set to grow faster at 6.8% through 2031.

Why is Asia-Pacific expected to grow fastest?

Asia-Pacific is projected to expand at 8.1% CAGR because India remains an early premiumization market, and 2026 company results indicate improving momentum in China.

How important are tariffs and excise duties to profitability?

They are a meaningful constraint because the U.S. imposed a 10% duty on European wine and spirits imports from February 2026, and tax administration in markets such as Ireland and Canada continues to raise cost pressure.

Page last updated on: