Market Overview

| Study Period | 2021 - 2031 |

|---|---|

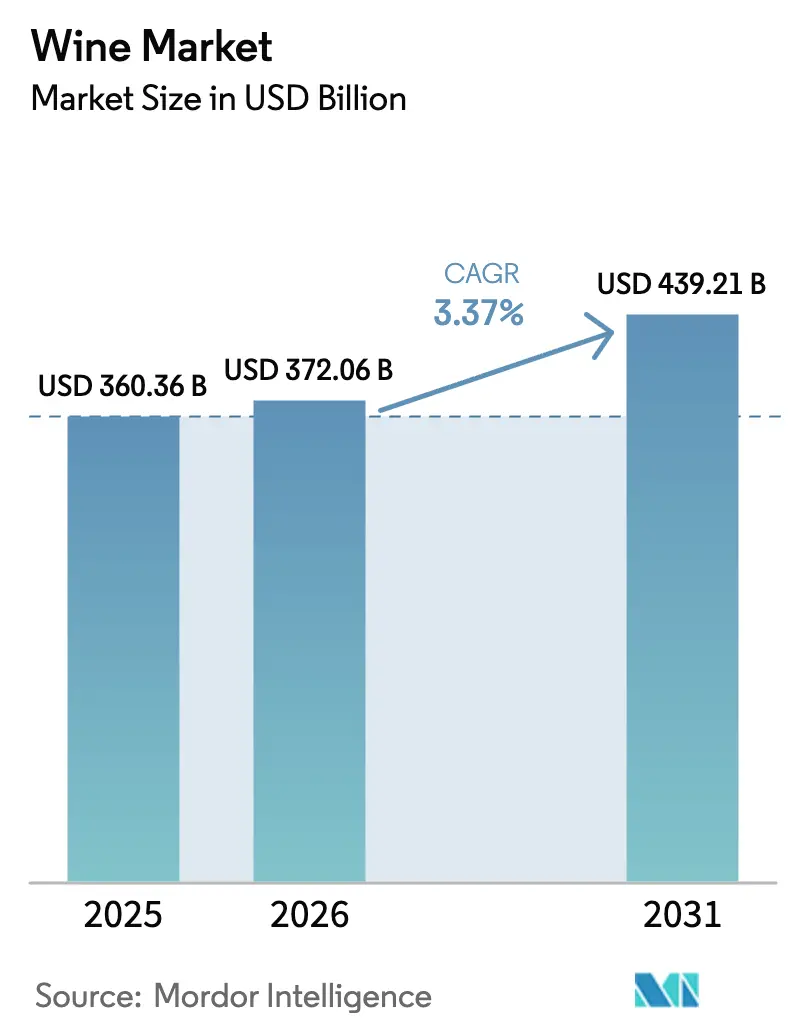

| Market Size (2026) | USD 372.06 Billion |

| Market Size (2031) | USD 439.21 Billion |

| Growth Rate (2026 - 2031) | 3.37% CAGR |

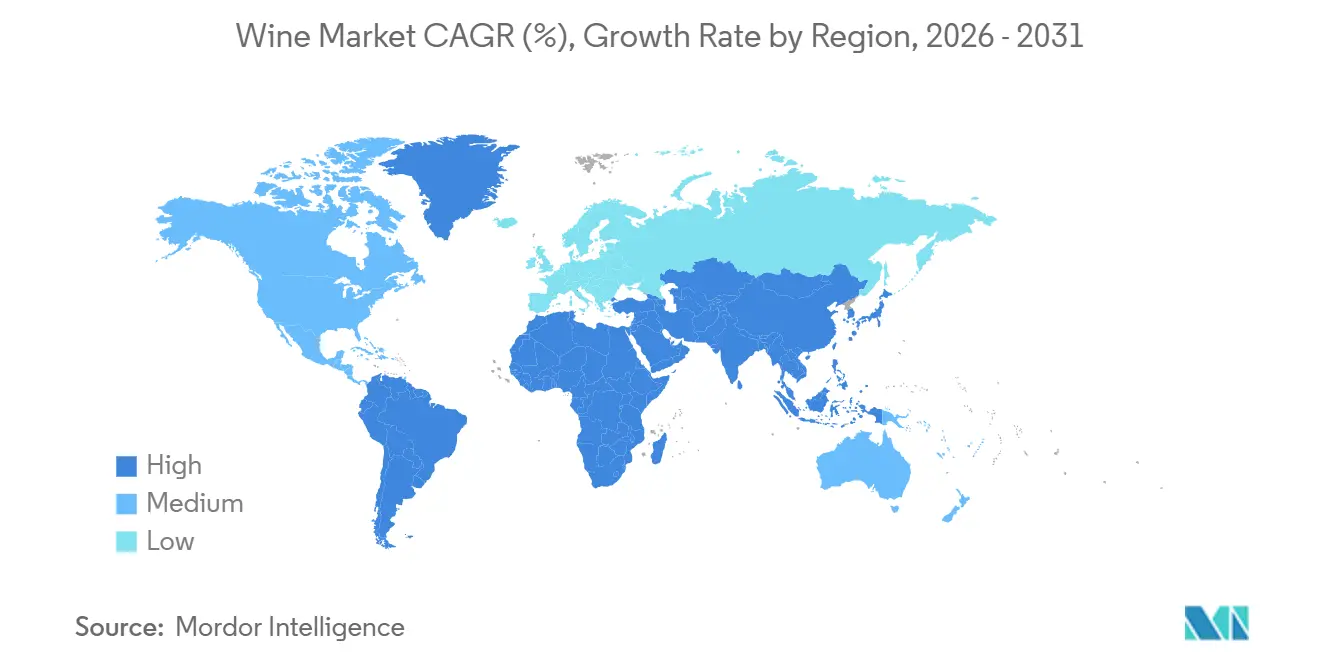

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Wine Market Analysis by Mordor Intelligence

The wine market stands at USD 360.36 billion in 2025, and is expected to grow from USD 372.06 billion in 2026 to reach USD 439.21 billion by 2031, representing a CAGR of 3.37%. This growth reflects an increase in value that surpasses unit volume growth, driven by consumers opting for higher-margin labels. Factors such as premium positioning, expanding tourism, and the adoption of direct-to-consumer (DTC) channels help mitigate challenges like climate-induced yield reductions and glass supply constraints. Europe maintains its leadership due to established production hubs and protected appellations, which ensure consistent quality and heritage appeal. Meanwhile, the Asia-Pacific region experiences the fastest growth as urban middle-class consumers increasingly embrace wine culture, influenced by rising disposable incomes and evolving lifestyle preferences. While larger players benefit from shelf prominence and economies of scale, the market remains highly fragmented, supported by numerous family estates and cooperatives that cater to niche demands and regional tastes.

Key Report Takeaways

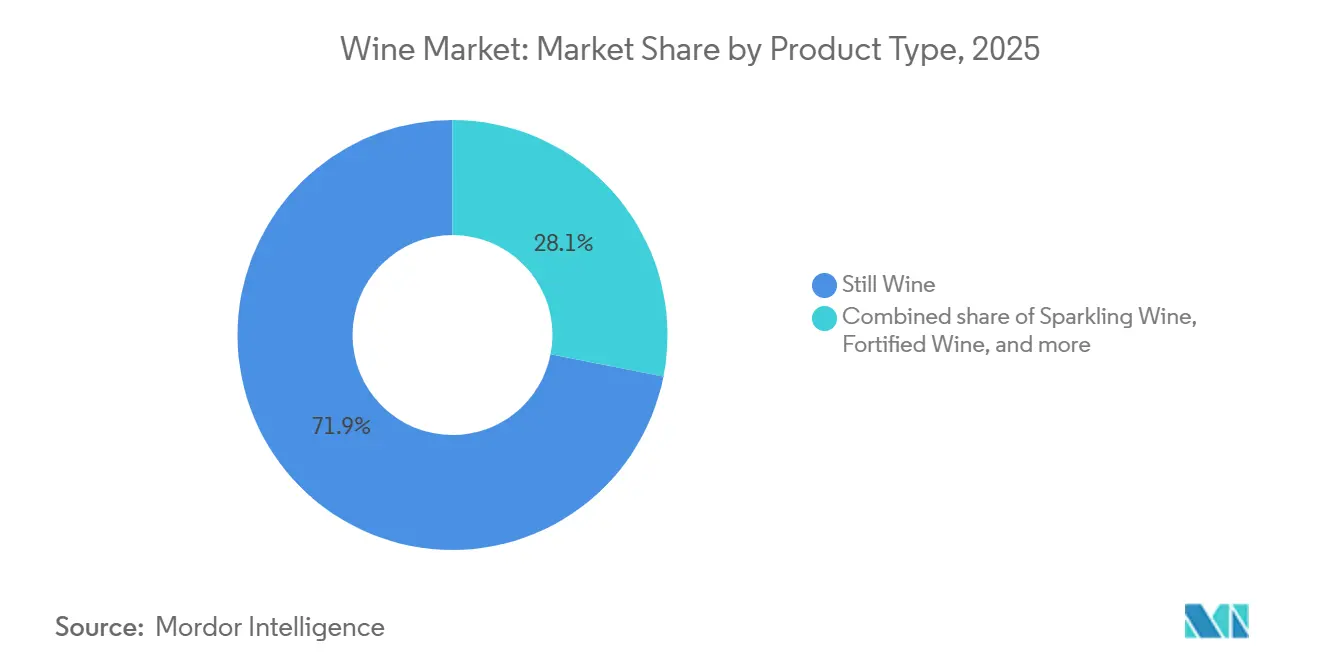

- By product type, still wine held 71.90% of the 2025 product-type share, and sparkling wine is projected to grow at a 4.0% CAGR through 2031.

- By color, red wine led with 48.23% of the 2025 color share, whereas rosé is forecast to advance at a 4.12% CAGR to 2031.

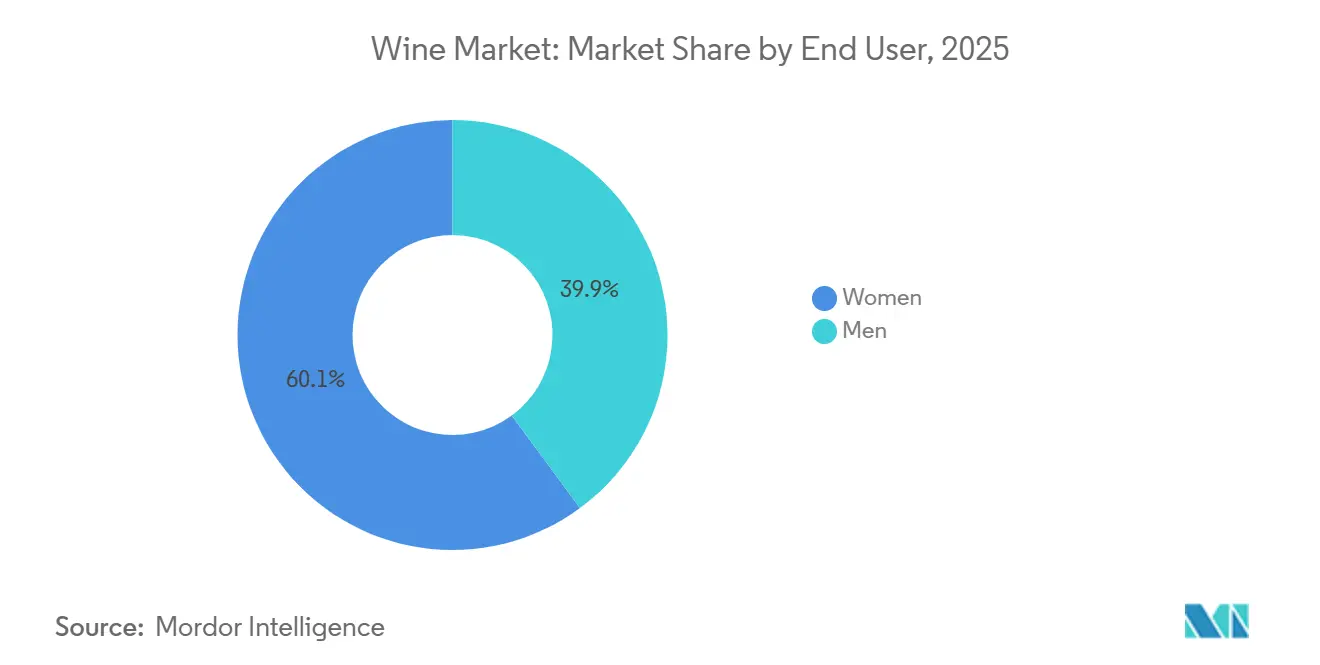

- By end user, women accounted for 60.11% of 2025 consumption, and men are set to rise at a 4.49% CAGR through 2031.

- By distribution channels, off-trade channels captured 59.65% distribution share in 2025, while on-trade is rebounding at a 3.69% CAGR to 2031.

- By geography, Europe commanded 45.34% of the 2025 regional share, and Asia-Pacific is poised for a 5.46% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Wine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing tourism and hospitality footprint | +0.5% | Europe, North America, South America | Medium term (2-4 years) |

| Rising preference for low-/no-alcohol wines | +0.4% | North America, Europe, early adoption in Asia-Pacific urban centers | Short term (≤ 2 years) |

| Premium and super-premium demand surge | +0.6% | Global | Long term (≥ 4 years) |

| Climate-resilient varietal research | +0.3% | Europe, North America, Southern Hemisphere | Long term (≥ 4 years) |

| Blockchain-enabled provenance | +0.2% | Global e-commerce hubs | Medium term (2-4 years) |

| Vineyard robotics and AI analytics | +0.3% | North America, Europe, Australia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing tourism and hospitality footprint

Wine tourism has transitioned from a niche offering to a significant revenue source, accounting for approximately 25% of total winery income and mitigating the impact of wholesale margin compression. The United Nations World Tourism Organization (UNWTO) Global Conference in 2025 highlighted wine tourism's importance in regional development, as destinations use wine experiences to attract millennials and Gen Z consumers interested in authentic cultural experiences[1]Source: "UN Tourism Global Conference on Wine Tourism highlights value of Culture", untourism.int . This trend is particularly evident in Europe's established wine regions, such as Bordeaux, Tuscany, and Rioja, as well as in emerging destinations like Chile's Colchagua Valley and South Africa's Stellenbosch, where government tourism boards actively promote wine trails as cultural heritage assets. The integration of hospitality extends beyond tasting rooms to include on-premise dining, where restaurants and hotels feature curated wine lists that encourage the trial of premium labels, fostering brand discovery and repeat purchases. This approach also shields producers from the effects of retailer consolidation by leveraging direct sales channels, which bypass intermediary margins and provide valuable consumer data for targeted marketing efforts.

Rising consumer preference for low-/no-alcohol wines

The demand for low- and no-alcohol wines is growing as health-conscious consumers, particularly Generation Z and millennials, seek moderation without complete abstinence. European producers have responded by investing in dealcoholization technologies, such as reverse osmosis and vacuum distillation, which preserve varietal character while reducing alcohol by volume to 0.5% or below. However, regulatory clarity remains inconsistent. In the United States, the TTB permits "non-alcoholic wine" labeling for products under 0.5% ABV, while the European Union enforces stricter thresholds under its wine common market organization. This category expansion also addresses emerging markets where cultural or religious norms limit traditional wine consumption, creating opportunities for incremental volume growth in the Middle East and parts of Asia-Pacific. Producers like Treasury Wine Estates have introduced dedicated NoLo sub-brands, signaling that this segment has evolved from experimental to a strategic growth area, as highlighted in the Treasury Wine Estates Investor Presentation 2025[2]Source: "2025 Annual Results Investor and Analyst Presentation", www.tweglobal.com..

Surge in premium and super-premium wine demand

Premiumization continues to reshape the wine market. This trend is driven by affluent consumers in North America and Asia-Pacific, who view wine as both a luxury consumable and an investable asset, as evidenced by auction indices tracking Bordeaux first growths and Burgundy grand crus. LVMH's Moët Hennessy division reported that its prestige champagne portfolio maintained pricing power despite macroeconomic challenges, with Dom Pérignon and Krug achieving mid-single-digit volume growth in 2024, as noted in the LVMH Annual Report 2024[3]Source: "Financial Documents fiscal Year Ended December 31, 2024", lvmh-com . In contrast, mainstream and value wine segments face structural decline. Constellation Brands, for instance, divested lower-margin brands to focus on its premium portfolio, including The Prisoner and Kim Crawford, as detailed in its 2024 10-K filing. This bifurcation creates strategic imperatives: large-scale players must either shift toward premium offerings or exit the market, while boutique estates leverage scarcity and terroir narratives to command ultra-premium pricing.

Climate-resilient varietal Research and Development expands viable terroirs

Climate volatility, including erratic frost events, heatwaves, and shifting precipitation patterns, has driven investment in resilient grape genetics and adaptive viticultural practices. PIWI varieties (fungus-resistant hybrids) have gained traction in Europe, where organic certification requirements and reduced fungicide usage align with consumer sustainability expectations. Germany and Switzerland, for example, have seen PIWI plantings exceed 1,000 hectares as producers aim to lower input costs while maintaining quality, according to European Commission Agricultural Research. These innovations are expanding the geographic footprint of premium wine production, challenging traditional appellations and creating new origin stories that appeal to exploratory consumers. The strategic implication is a gradual decoupling of terroir from latitude, as advancements in technology and genetics mitigate climatic disadvantages. However, regulatory frameworks governing varietal labeling and appellation rules will play a critical role in determining the pace at which these innovations achieve commercial scale.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent and divergent alcohol regulation | -0.4% | Global, acute in North America (state-by-state variance), Asia-Pacific (import tariffs, licensing) | Long term (≥ 4 years) |

| High production costs amplified by climate volatility | -0.5% | Europe, North America, Australia (established regions facing yield variability) | Medium term (2-4 years) |

| Sophisticated counterfeits in e-commerce channels | -0.2% | Global e-commerce, concentrated in Asia-Pacific and emerging online markets | Short term (≤ 2 years) |

| Glass and logistics bottlenecks inflate packaging costs | -0.3% | Global, acute in Europe and North America (glass supply concentration) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent and divergent alcohol regulations

Regulatory fragmentation imposes significant compliance costs and restricts market access, particularly for exporters dealing with diverse labeling, taxation, and distribution rules. In the United States, the three-tier system, which mandates the separation of producers, distributors, and retailers, limits direct-to-consumer shipping. The Alcohol and Tobacco Tax and Trade Bureau (TTB) has modernized its Certificate of Label Approval (COLA) processes, reducing approval timelines. In the Asia-Pacific region, tariff structures and import licensing regimes vary significantly. For example, China's reinstatement of its zero-tariff policy on Australian wine in 2024, following a three-year suspension, contrasts sharply with India's duties exceeding 150%, which hinder legal imports and encourage grey-market activity. In the European Union, the geographical indication framework protects regional appellations but limits varietal flexibility, complicating efforts by new-world producers to transparently communicate grape composition.

High production costs amplified by climate volatility

Climate-induced yield variability has significantly increased production costs through various factors, including the need for enhanced irrigation systems, frost-protection infrastructure, higher insurance premiums, and adaptive canopy management. According to the International Organisation of Vine and Wine (OIV), global wine production in 2024 dropped to 225.8, the lowest in six decades, due to spring frosts in Europe and drought conditions in South America. This forced producers to either procure additional fruit at elevated spot prices or reduce output. Energy-intensive measures, such as wind machines for frost mitigation and desalination for irrigation in water-scarce areas, have added recurring operational expenses, compressing profit margins, particularly for mid-sized producers without economies of scale. Seasonal labor shortages have further driven overtime premiums and investments in mechanization, which require extended payback periods. These cost pressures disproportionately impact regions with marginal climates and limited access to capital, accelerating industry consolidation as smaller estates either exit the market or sell to larger, better-capitalized entities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Sparkling Effervescence Outpaces Still Tradition

In 2025, still wine accounted for 71.90% of the product-type share, reflecting its established role in both everyday and fine-dining settings. However, sparkling wine is projected to grow at a CAGR of 4.0% through 2031, surpassing the category average. The increased accessibility of Prosecco, facilitated by the cost-efficient Charmat method, has expanded sparkling wine consumption beyond celebratory occasions. Italian sparkling wine exports reached record volumes in 2024 despite macroeconomic challenges, according to Italian Wine Central. In contrast, Champagne relies on its scarcity and appellation prestige to maintain ultra-premium pricing.

Brands such as LVMH's Moët and Chandon and Veuve Clicquot prioritized margins over market share in 2024, as inventory destocking concluded, as noted in the LVMH Annual Report 2024. Other wine types, such as vermouth, aromatized wines, and pétillant-naturel, remain niche but appeal to craft-focused consumers seeking novelty and artisanal origins. Still wine continues to dominate in on-trade fine dining, where sommeliers emphasize terroir and vintage variation in curated wine lists. In off-trade channels, still wine remains a staple for everyday consumption, with value-conscious buyers focusing on cost per serving rather than packaging innovations. Fortified wine faces challenges as younger consumers show less interest in sweet, high-alcohol profiles. However, premium tawny ports and single-quinta vintages retain appeal among collectors.

By Color: Rosé Gains While Red Holds Tradition

In 2025, red wine accounted for 48.23% of the color-based market share, supported by established varietals such as Cabernet Sauvignon, Merlot, and Pinot Noir, which dominate on-trade wine lists and collector cellars. However, rosé wine is projected to grow at a CAGR of 4.12% through 2031, driven by evolving year-round consumption patterns and increasing premiumization. Provence-style rosé, known for its pale hue and dry profile, has moved beyond its traditional seasonal appeal. Producers like Château d'Esclans and Whispering Angel have gained significant recognition in North America and the Asia-Pacific regions. White wine, which holds the remaining market share, benefits from its versatility in food pairings and popularity during warm-weather occasions, with Chardonnay and Sauvignon Blanc leading varietal sales.

The growth of rosé wine is further supported by its geographic expansion beyond its Mediterranean origins. Regions such as Australia, South Africa, and California have increased rosé production by utilizing existing red-grape vineyards through saignée or direct-press methods. This approach allows producers to capture additional margins without requiring new vineyard plantings. The segmentation by color aligns with consumption occasions: red wine is preferred for formal dining and cellaring, white wine for casual meals and aperitifs, and rosé for social gatherings and outdoor events.

By End User: Women Lead, Men Accelerate

Women represented 60.11% of the end-user share in 2025, driven by consistent engagement in wellness-focused and lower-alcohol categories. However, men are projected to grow at a CAGR of 4.49% through 2031, as the craft and premium wine segments attract male consumers interested in artisanal origins and collectible labels. Marketing strategies targeting women focus on lifestyle integration, with brands like Sula Vineyards in India and Kim Crawford in New Zealand utilizing social media and influencer partnerships to foster community engagement and encourage product trials. In contrast, male consumers show a stronger preference for full-bodied reds, fortified wines, and limited-production offerings that convey expertise and investment value.

The end-user landscape is shifting as traditional gender associations diminish. Male participation in wine clubs and tasting events has increased, driven by craft spirits enthusiasts transitioning into wine and younger demographics rejecting gendered consumption norms. Meanwhile, female sommeliers and winemakers are gaining visibility, challenging industry stereotypes and enhancing wine's cultural appeal. Producers are adapting by adopting gender-neutral branding and packaging that highlight terroir, sustainability, and craftsmanship rather than lifestyle-oriented messaging. The strategic importance of this segmentation lies in optimizing channels and messaging: brands targeting women should focus on digital engagement, subscription-based models, and wellness narratives, while those targeting men should emphasize scarcity, critic ratings, and vertical tasting experiences.

By Distribution Channel: Off-Trade Dominates, On-Trade Recovers

Off-trade channels accounted for 59.65% of the distribution share in 2025, including specialty liquor stores, supermarkets, and e-commerce platforms. However, on-trade channels are projected to grow at a CAGR of 3.69% through 2031, driven by the recovery of hospitality venues and the increasing appeal of experiential dining, which boosts per-bottle spending. Specialty liquor stores remain a key component of the off-trade segment, offering curated selections and knowledgeable staff that provide a middle ground between mass-market grocery stores and on-premise options. On-trade channels, including restaurants, bars, and hotels, achieve higher per-unit pricing, with high markups over wholesale prices being common in fine dining establishments.

The distribution segmentation highlights structural changes in consumer behavior and regulatory frameworks. Off-trade dominance is supported by factors such as convenience, price transparency, and the growth of direct-to-consumer (DTC) models, which bypass traditional three-tier systems where legally allowed. Specialty liquor stores differentiate themselves through educational tastings, staff training, and curated product collections, which justify premium pricing and foster customer loyalty. On-trade recovery has been uneven, with casual dining and bars recovering more quickly than fine dining establishments, which continue to face challenges such as labor shortages and higher operating costs.

Geography Analysis

Europe generated 44.45% of global wine revenues in 2024, supported by established cultural traditions and concentrated wine-producing regions. Consumer behavior shows a shift from daily consumption to weekend and special occasion drinking, resulting in decreased low-price volume but increased premium segment share. In France, wine remains the primary alcoholic beverage, with strong adoption among 18-25-year-olds. Italy's market growth is driven by Denominazione di Origine Controllata e Garantita (DOCG) promotional activities and increased exports to the United States. European producers face strict environmental regulations, leading to increased adoption of organic certifications and biodynamic practices, which increase production costs while providing marketing benefits.

The Asia-Pacific region is projected to grow at a CAGR of 5.46% through 2030, driven by various factors across key markets. In China, market expansion is fueled by the increasing production of domestic premium wines, supported by advancements in winemaking techniques and the growing popularity of locally produced high-quality wines. Additionally, the development of duty-free retail channels has further boosted accessibility and demand for premium wine products. In India, growth is underpinned by the rise of wine tourism initiatives in Maharashtra, which combine agricultural experiences, such as vineyard tours and wine tastings. South Korean consumers exhibit a strong inclination toward sweeter wines, reflecting cultural taste preferences, while Japanese buyers demonstrate a growing demand for sparkling Moscato, driven by its versatility and appeal in social settings. Thailand's wine market is also expanding, supported by increasing urbanization and a growing middle class with higher disposable incomes. Furthermore, digital platforms enable direct shipments from small European producers to Asian consumers, bypassing traditional import barriers and reducing costs.

South American exporters, particularly those from Chile and Argentina, leverage free-trade agreements to sustain their market presence amid growing competition from Spain and Portugal. These agreements provide exporters with reduced tariffs and improved access to international markets, enabling them to remain competitive in an increasingly crowded landscape. Additionally, these countries focus on enhancing the quality and branding of their wines to appeal to global consumers. The Middle East and Africa regions demonstrate long-term growth potential, despite regulatory challenges, as affluent urban areas continue to import premium wines for high-end restaurants. Wealthy consumers in these regions are increasingly seeking high-quality products, creating opportunities for exporters to cater to niche markets. However, navigating complex regulatory frameworks and import restrictions remains a critical challenge. Achieving success in these varied markets necessitates adherence to regulatory requirements and the implementation of tailored communication strategies that address the unique preferences and cultural nuances of each market.

Regulatory Landscape

Regulation in the global wine market is shaped by product-definition rules, labeling and health disclosures, and trade measures that can change landed cost and route-to-market access. In the European Union, Regulation (EU) 2026/471 (February 2026) updated wine-sector market rules, including harmonized labeling terminology for reduced-alcohol wine products and other simplifications intended to reduce operational burden. The EU continues to enforce geographical indications (GIs) and traceability requirements, which affect varietal naming and label design across member states.

In the United States, alcohol compliance remains split between federal oversight and state-by-state distribution constraints. The Alcohol and Tobacco Tax and Trade Bureau (TTB) published a Notice of Proposed Rulemaking in January 2025 on mandatory Alcohol Facts statements, including alcohol and calorie/nutrient information, for beverage alcohol labels under the Federal Alcohol Administration Act. This adds packaging, data, and approval-workflow needs for producers selling across multiple states and channels. Trade policy is also a variable for exporters: the Office of the United States Trade Representative (USTR) highlighted reciprocal trade frameworks in its 2026 Trade Policy Agenda, while the National Trade Estimate Report 2026 continues to catalog non-tariff barriers relevant to wine, reinforcing the need for multi-market compliance and flexible labeling for global brands.

Competitive Landscape

The global wine market is characterized by a fragmented competitive structure, with a low concentration score. This reflects the presence of numerous producers, ranging from small family estates to large multinational conglomerates. The fragmentation is driven by wine's terroir-based differentiation, where regional appellations and microclimates create natural barriers to commoditization. Companies like Constellation Brands, Treasury Wine Estates, and E. & J. Gallo leverage extensive portfolios and strong retailer relationships to secure premium shelf space and negotiate volume discounts. However, brand loyalty remains dispersed as consumers frequently switch between varietals, regions, and price tiers.

White-space opportunities are evident in the premiumization of emerging markets, including India, Southeast Asia, and sub-Saharan Africa. Local producers in these regions can capture higher margins by positioning domestic wines as accessible luxury products. Additionally, the low-/no-alcohol wine segment presents growth potential, as incumbents have been slow to invest in this category. Technology adoption is becoming a key differentiator in the wine market. For example, Treasury Wine Estates has implemented precision viticulture platforms and data analytics to optimize vineyard management. LVMH's Moët Hennessy division has concentrated investments on ultra-premium champagne and prestige still wines, while divesting or deprioritizing value brands to protect margins and brand equity.

Emerging disruptors, such as direct-to-consumer specialists Winc and Naked Wines, are leveraging subscription models and algorithmic recommendations to bypass traditional retail channels. This approach allows them to capture consumer data and retain margins that were historically claimed by wholesalers and retailers. Additionally, smaller producers, particularly organic and biodynamic estates, are gaining traction by appealing to sustainability-conscious consumers who are willing to pay premiums for certified practices and transparent supply chains. Patent activity in vineyard automation and AI-driven quality control is accelerating. Companies like Monarch Tractor and Trimble are filing patents for autonomous equipment and sensor integration, signaling that intellectual property in agricultural technology will become a competitive advantage for capital-intensive producers.

Wine Industry Leaders

-

Bacardi Limited

-

E. & J. Gallo Winery

-

Constellation Brands Inc.

-

Pernod Ricard

-

Bronco Wine Co.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulatory modernization and compliance-driven product innovation are creating whitespace in lower- and reduced-alcohol wine formats, supported by clearer terminology and sector measures in the European Union under Regulation (EU) 2026/471 (February 2026). This complements producers' use of dealcoholization technologies, such as reverse osmosis and vacuum distillation, already referenced in category strategies, and can support portfolios that transfer across off-trade retail and direct-to-consumer (DTC) programs where permitted.

Supply-chain and route-to-market investments are also becoming a practical lever to protect margins amid glass, logistics, and climate-related cost pressure. In Europe, named projects point to consolidation across bottling, ageing, and distribution capabilities: KEO PLC announced plans for a EUR 25 million bottling and distribution center in Limassol (May 2026), and Mack & Schuhle Italia announced a EUR 16 million investment to expand its Laterza wine plant (July 2026). In Asia-Pacific, market access and labeling strategy remain tangible opportunity areas for exporters and domestic champions: Wine Australia reported final negotiations on a new Australia-EU Wine Agreement (March 2026) aimed at simplified certification and GI-related protections, while in India, Sula Vineyards signed a definitive agreement to acquire the 19-acre Chandon estate in Nashik (March 2026), adding production infrastructure that supports premium sparkling and experiential wine-tourism-led positioning.

Recent Industry Developments

- June 2026: Bronco Wine Co. announced the acquisition of Resurrection Brands, a sales and marketing organization representing family-owned wineries including McManis Family Vineyards, Provenance Brands, and LangeTwins Family Winery & Vineyards. The deal expands Bronco's national representation and route-to-market capabilities, strengthening its ability to scale premium and boutique labels through wholesale channels.

- April 2026: Pernod Ricard completed the disposal of its Mumm sparkling wine activities in the United States, including Mumm Sparkling California, Mumm Napa, and DVX, to Trinchero Family Wine and Spirits. The transaction alters competitive positioning in US sparkling wine by transferring established brands and production assets to a specialist wine operator while supporting Pernod Ricard's portfolio streamlining.

- June 2025: Viva Wine Group signed a binding agreement to acquire 88.59% of Delta Wines in the Netherlands for EUR 57 million. The acquisition strengthens Viva Wine Group's distribution footprint in Europe and adds scale in an off-trade-oriented market structure where retail and logistics capability can influence brand visibility and pricing.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers the value of wine sold for consumption through retail and on-premise channels, counted across major producing and consuming countries and then consolidated to a global total.

Scope exclusions: We exclude non-alcoholic grape beverages, flavored wine coolers, and winemaking equipment or packaging materials.

Segmentation Overview

-

By Product Type

- Fortified Wine

- Still Wine

- Sparkling Wine

- Others Wine Types

-

By Color

- Red Wine

- White Wine

- Rose Wine

-

By End User

- Men

- Women

-

By Distribution Channel

- On-Trade

-

Off-Trade

- Specialty/Liquor Stores

- Other off-Trade Channels

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work was used to set the fact base before modeling, mainly by aligning what counts as wine in trade and production reporting and by understanding how value moves across the chain. Public sources such as the International Organisation of Vine and Wine (OIV), UN Comtrade, national customs statistics, and agriculture or food agencies were referenced for production, exports, imports, and the consumption direction. We also used central bank or finance ministry releases for exchange-rate context and inflation signals that can influence pricing comparisons across years.

To make the model practical, we added supporting inputs from company annual reports, investor presentations, and reputable press coverage to track portfolio mix shifts and channel trends. Select paid subscriptions were used in a limited way for company financials and intelligence, and for shipment-level trade checks where public tables were too aggregated to interpret. The desk research sources listed above are illustrative, and we consulted additional public and paid sources for cross-checks, clarification, and validation.

Primary Interviews and Surveys

Primary interviews and surveys were carried out with a mix of producers, distributors, importers, retailers, and on-trade buyers so that pricing logic and channel splits could be validated beyond what is visible in public datasets. We also spoke with industry experts across the Americas, EMEA, and APAC to confirm how premiumization, packaging formats, and trade flows are changing demand, and to pressure-test the assumptions used in the forecast.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 16% | APAC: 39% |

| Mid tier: 48% | Functional/Unit leaders: 33% | EMEA: 37% |

| Smaller Players: 22% | Managers: 51% | Americas: 24% |

Market-Sizing & Forecasting

Sizing starts from a top-down build where production and trade data are reconstructed into an apparent consumption pool by country, and then converted into value using pricing and mix assumptions that we check in interviews. To keep the totals grounded, we corroborated results with selective bottom-up approximations such as sampled brand and private-label price ladders, channel checks on on-trade versus off-trade splits, and producer revenue sanity checks where disclosures were available.

The model uses a small set of repeatable inputs, including wine production volumes, import and export values, per capita consumption direction, on-trade reopening strength, and average price progression by category (still versus sparkling) and color mix. When data gaps occur, especially in smaller markets and informal channels, assumptions are filled using proxy markets with similar income levels and drinking patterns, then adjusted after expert feedback.

For forecasting, we applied scenario analysis so the base case reflects expected changes in volume and price mix, followed by a check against macro indicators such as disposable income, tourism activity for on-trade demand, and inflation-driven price shifts. Final growth paths are revised only after the forecast outputs align with what primary respondents see in their order patterns and portfolio planning.

Data Validation & Update Cycle

Outputs are validated through multiple checks, including comparing implied consumption against trade and production signals, testing year-to-year price and mix movements for sudden jumps, and reviewing channel shares for logical consistency by region. When a variance looks unusual, we re-check the source series, revisit the conversion steps, and re-contact select experts to confirm whether a real market event explains the change.

A second analyst review is completed before sign-off so assumptions, calculations, and definitions stay consistent across regions and time periods. Reports are refreshed annually, and interim updates are made when material events occur, such as policy changes, sharp currency moves, or major supply shocks. Before delivery, an analyst completes a final review pass so clients receive the latest updated view.

Mordor Intelligence's Wine Market Estimate Compared With Other Published Estimates

Published wine market values often differ because the scope can shift between ex-manufacturer value and retail spending, and because some studies treat adjacent alcohol categories or related beverages as part of the total. Differences also come from how pricing is projected, how on-trade versus off-trade is split, and how quickly assumptions are updated when trade flows and consumer demand shift.

Some external estimates appear to reflect broader retail value pools and faster premium-price escalation, which can raise the headline number even if volumes stay stable. In Mordor Intelligence, the total is kept to wine sold for consumption, with clear exclusions for non-wine beverages. Pricing is updated using trade-value signals and interview-validated mix shifts before totals are finalized.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 360.36 B (2025) | |

| Global Consultancy A | USD 549.65 B (2025) | Uses a broader revenue lens that can align closer to retail spending, and applies a faster premiumization curve by channel, which lifts the 2025 value versus an ex-manufacturer style build. |

| Industry Publisher B | USD 622.85 B (2026) | Reported for 2026 and reflects a higher price trajectory into the forecast base year, with channel and type assumptions that imply a larger value pool when rolled up globally. |

The spread in the table is mainly explained by how value is defined and how aggressively price and mix are allowed to move year over year. By tying the total to observable production and trade signals and then checking the pricing logic through interviews, the estimate stays traceable to a defined demand pool and repeatable calculation steps.

Key Questions Answered in the Report

What is the current size of the global wine market?

The wine market stands at USD 372.06 billion in 2026.

How fast is the wine market expected to grow?

It is projected to expand at a 3.37% CAGR, reaching USD 439.21 billion by 2031.

Which region is growing fastest in the wine market?

Asia-Pacific leads with a 5.46% CAGR through 2031, driven by rising middle class incomes and expanding wine culture.

What challenges do wine producers face from regulations?

New European Union and United States labeling rules require detailed ingredient and nutrition information, raising compliance costs and operational complexity.

Page last updated on: